USAGE OF MOBILE BANKING AND ITS EFFECTS ON CONSUMER BEHAVIOR IN THAILAND BY MR. CHANA SILPARCHA AN INDEPENDENT STUDY SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF SCIENCE PROGRAM IN MARKETING (INTERNATIONAL PROGRAM) FACULTY OF COMMERCE AND ACCOUNTANCY THAMMASAT UNIVERSITY ACADEMIC YEAR 2017 COPYRIGHT OF THAMMASAT UNIVERSITY Ref. code: 25605902040087AGC

Transcript

USAGE OF MOBILE BANKING AND ITS EFFECTS ON

CONSUMER BEHAVIOR IN THAILAND

BY

MR. CHANA SILPARCHA

AN INDEPENDENT STUDY SUBMITTED IN PARTIAL

FULFILLMENT OF

THE REQUIREMENTS FOR THE DEGREE OF

MASTER OF SCIENCE PROGRAM IN MARKETING

(INTERNATIONAL PROGRAM)

FACULTY OF COMMERCE AND ACCOUNTANCY

THAMMASAT UNIVERSITY

ACADEMIC YEAR 2017

COPYRIGHT OF THAMMASAT UNIVERSITY

Ref. code: 25605902040087AGC

USAGE OF MOBILE BANKING AND ITS EFFECTS ON

CONSUMER BEHAVIOR IN THAILAND

BY

MR. CHANA SILPARCHA

AN INDEPENDENT STUDY SUBMITTED IN PARTIAL

FULFILLMENT OF

THE REQUIREMENTS FOR THE DEGREE OF

MASTER OF SCIENCE PROGRAM IN MARKETING

(INTERNATIONAL PROGRAM)

FACULTY OF COMMERCE AND ACCOUNTANCY

THAMMASAT UNIVERSITY

ACADEMIC YEAR 2017

COPYRIGHT OF THAMMASAT UNIVERSITY

Ref. code: 25605902040087AGC

(1)

Independent Study Title USAGE OF MOBILE BANKING AND ITS

EFFECTS ON CONSUMER BEHAVIOR IN

THAILAND

Author Mr. Chana Silparcha

Degree Master of Science Program in Marketing

(International Program)

Major Field/Faculty/University Faculty of Commerce and Accountancy

Thammasat University

Independent Study Advisor Associate Professor Kenneth E. Miller, Ph.D.

Academic Year 2017

ABSTRACT

“What is the first thing you do when you wake up in the morning?” it

is highly likely that the answer is you looked at your smartphone. In 2016, Deloitte

conducted a global mobile consumer survey and discovered that 61 percent of people

check their phones within 5 minutes after waking up. Dubbed “the most innovative

invention in the 21st century”, smartphones impacted our lives in many ways and

revolutionized multiple industries. One of the industries disrupted is the banking

industry as mobile banking empowered us to conduct banking activities anywhere at

any time through the comfort of our smartphones. Similar to other ASEAN countries,

Thailand experienced exponential growth in usage of mobile banking as a result of e-

commerce expansion and improved e-payment infrastructure.

Ref. code: 25605902040087AGC

(2)

Although studies on the underlying factors that influence mobile banking

adoption has been extensively conducted, research to examine after-adoption behavior

has been neglected. Thus, this research captures the current situation of mobile

banking in Thailand and categorizes mobile banking users into different segments.

Banks and government sectors alike will benefit from this comprehensive research as

they can apply insights to generate suitable products for banking customers and

Payment” (89 percent.) Figure 4.3 exhibits 1) the number of respondents who know a

particular mobile banking service 2) the number of respondents currently using a

particular mobile banking service 3) the number of respondents using a particular

mobile banking service most often. A three percent drop from knowing money

transfer to using money transfer and a 22 percent drop from using money transfer to

using most often can be observed. Similarly, an eight percent drop from knowing

account balance check to using account balance check, and a 79 percent drop from

using account balance check to using most often can be observed. Finally, a 26

percent drop from knowing bill payment to using bill payment and an astounding 92%

drop from using bill payment to using most often can be observed. Although

respondents know and use all 3 services, money transfer is by far the most used

mobile banking service.

Figure 4.3: Top 3 Mobile Banking Service Conversion Rate

Ref. code: 25605902040087AGC

20

4.2.3 Segmentation

Based on Pearson correlation among 7 mobile banking attributes, 2 compelling

correlations stood out. First, a positive correlation between “Security” and the

“Reliability”, r = 0.559, n = 192, p = 0.000. Second, another positive correlation

between “Recommendation from peers” and “Online Review”, r = 0.687, n = 192,

p = 0.000 can be observed. Further factor analysis was conducted as other attributes

were also correlated. Please refer to results in Appendix E for more details.

Table 4.4: Correlation between “Security & Reliability” and “Recommendation

from peers & Online Review”

Factor analysis using Varimax rotation methodology generated a KMO of

0.62, explaining 81 percent of the total variations with Eigenvalues > 0.6. Four

factors, namely, “Reliability”, “User Friendly”, “Review” and “Features” was derived

from the analysis. (See Appendix F) Subsequently, a two-step cluster analysis

including mobile banking usage frequency generated 3 clusters. (See Appendix G)

The first cluster is the smallest segment called “Old School Veterans”

representing 21 percent of total sample size. The segment tends to contain older

individuals with key characteristics including conservative, habitual and observant.

Ref. code: 25605902040087AGC

21

The second cluster is the largest segment called “Middle Aged Go-Getter”

representing 46 percent of the total sample size. This segment is made up of working

adults who are logical, practical and have systematic thinking. Finally, a segment

called “Youthful Minimalist”, which is the second largest cluster, representing 32

percent of the total sample size. Individuals in this segment tend to be younger,

tasteful, emotional and spontaneous. “Middle Aged Go-Getter” and “Youthful

Minimalist” are classified as heavy users and “Old School Veterans” is classified as

light users.

The “Middle Aged Go-Getter” segment seek high overall performance

(including security and features) of mobile banking. Members of this segment will not

tolerate technical malfunctions or inferior services. Interestingly, the “Youthful

Minimalist” segment which is also considered a heavy user, prioritizes ease of use and

convenience mobile banking. This segment views that user friendliness of mobile

banking applications fit into their fast-moving lifestyles. On the contrary, “Old School

Veterans” may not have a clear understanding of how mobile banking operates and

they heavily rely on close friends and online resources to facilitate mobile banking

adopt.

Figure 4.5:

Heavy and light

user cluster

analysis

Ref. code: 25605902040087AGC

22

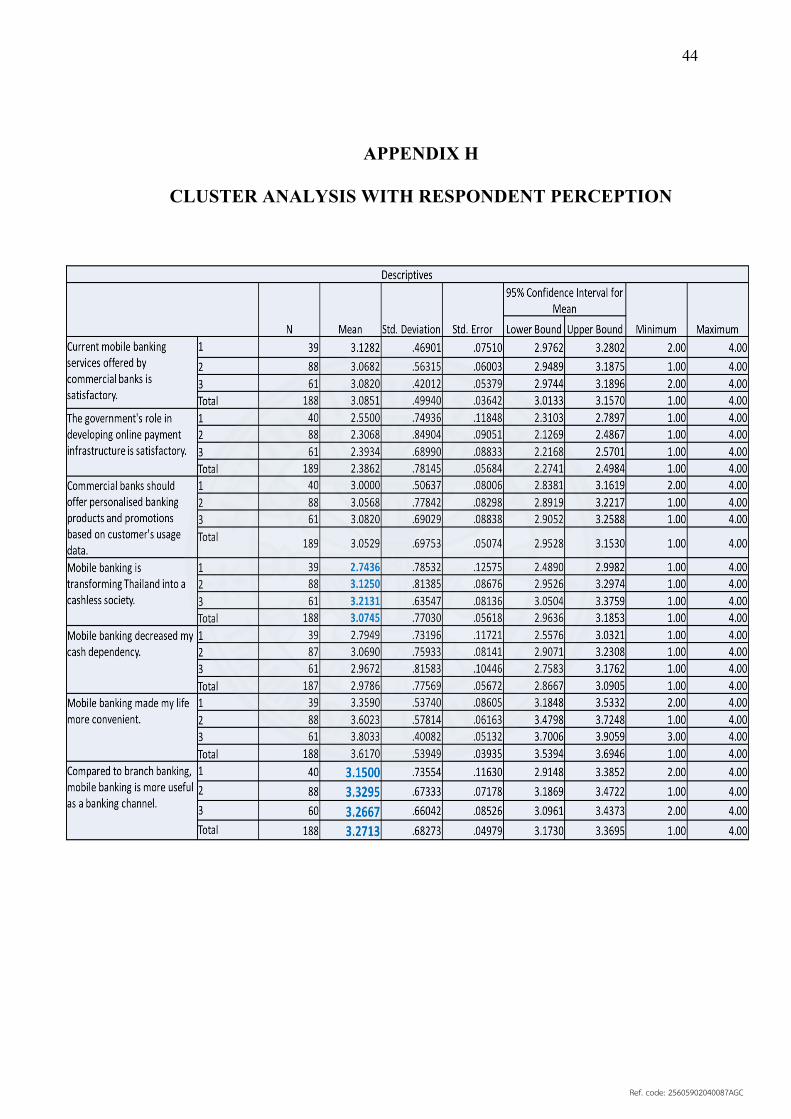

Although not statistically significant, further cluster analysis including user

perception of mobile banking show promising insights for each user segment. This

suggest that “Old School Veterans” do not believe that mobile banking will transform

Thailand into a cashless society. On the contrary, heavy users such as “Youthful

Minimalist” believe that mobile banking made their lives more convenient. (See

appendix H)

Table 4.5: Results from cluster analysis with respondent’s perception

Table 4.6: Anova results from cluster analysis with respondent’s perception

Ref. code: 25605902040087AGC

23

CHAPTER 5

CONCLUSIONS AND RECOMMENDATIONS

5.1 Conclusion and Managerial Implication

According to qualitative research as well as frequency, factor and cluster

analysis, the majority of Thais have a positive perception towards mobile banking.

Furthermore, 2 out of 3 user segments identified by the research are heavy users that

highly value reliability and user friendliness. Interestingly, the remaining cluster of

light users who value word of mouth and online review has the potential to turn into a

heavy user if they were better educated about the product. As Thailand’s smartphone

penetration increases, more Thais will likely adopt mobile banking and the following

implications for commercial banks can be implemented.

5.1.1 Managerial Implication for Commercial Banks

Firstly, there are only 2 dominant brands in the market and the remaining

5 banks must compete more aggressively in terms of brand awareness and usage

frequency. Although the research identified 3 top-of-mind mobile banking brands, it

was clear that, K Plus and SCB Easy were the only two that dominated the market.

This finding is not surprising as Kasikorn Bank and Siam Commercial Bank invested

heavily in their digital banking infrastructure. However, this is a wake-up call for the

remaining 5 banks. One possible solution is to reduce traditional banking channels

costs and increase invest in innovative banking solutions such as QR code payment

infrastructure to catch up with technological advancement. Another solution is to

secure user’s Prompt Pay registration as a means of obtaining a user’s “Primary

Ref. code: 25605902040087AGC

24

Account.” Users will prefer to use the primary account to transfer money rather than

secondary accounts because Prompt Pay is more convenient. This strategy will attract

more traffic to the mobile banking application and create a ripple effect to generate

more awareness among prospect users.

Secondly, offering a wide range of services is not a sustainable competitive

advantage. Research findings suggests money transfer is the most commonly used

service, followed by account balance check and bill payment. However, the majority

of users do not use the remaining 13 services currently offered by various commercial

banks. As a result, it would be impractical to invest and roll out insignificant service

extensions such as insurance purchase and branch location. Rather, commercial banks

should integrate and reinvent their mobile banking application into user’s daily lives.

This will transform mobile banking from a payment channel into a multi-purpose

lifestyle platform capable of ride hailing, food delivery and online shopping. Higher

usage frequency also translates to a bigger potential in monetizing user data.

Ultimately, commercial banks will have to compete against non-bank players such as

e-wallet companies that are aiming to disrupt the banking industry.

5.2 Research Limitations

Although this research was carefully planned and executed, 2 main limitations

emerged. Firstly, the diversity of respondents’ profiles was limited. This is because

the majority of respondents are corporate employees living in Bangkok with similar

education background. Collecting more response from other population groups such

as the working class as well as senior management could have generated other

insightful findings.

Ref. code: 25605902040087AGC

25

Secondly, with limited time and resources, the research failed to gasp a better

understanding of non-bank players which represents a considerable portion of

Thailand’s Fintech industry. Moreover, a deeper study of the government sector will

produce a holistic understanding of the industry as they are a responsible for shaping

digital banking policies and infrastructure.

5.3 Suggestions for Future Studies

The intention of this research was to identify overall user behavior and to

identify consumer segments; however, the findings are relatively generalized.

Therefore, future studies should specifically target one out of three user segments

defined by this study or other potential segments including teenagers, entrepreneurs

and pensioners. It is also important to investigate how to increase usage frequency

among current heavy users or how to transform light users into heavy users.

Furthermore, commercial banks will find financial profiles and user profitability of

each segments highly useful. Aside from Thai mobile banking users, other potential

user segments to conduct further study on are Chinese tourists who heavily rely on e-

payment at home and abroad. Further studies have the potential to increase usage

frequency and satisfaction of heavy users, increase mobile banking adoption for light

users and ultimately transform Thailand into a cashless society.

Ref. code: 25605902040087AGC

26

REFERENCES

Alker, T. (2016). CROWDFUNDING SUCCESS FACTORS IN THAILAND. Colleg e of Management, Master of Management. Bangkok, Thailand: Mahdiol University. Retrieved October 14, 2017, from Globalbizresearch: http://globalbizresearch.org/Bangkok_Thailand_Conference_2017_feb1/docs/doc/2.%20Finance,%20Account%20&%20Banking/T744.pdf

Allison, A. L. (2016, November 1). The Hierarchy of Effects Model in Advertising. Retrieved March 7, 2018, from Propaganda For Change: http://persuasion-and-influence.blogspot.com/2016/11/the-hierarchy-of-effects-model_1.html

Bangkok Post. (2016, June 28). Smartphone subscriptions near 50m. Retrieved from Bangkok Post Technology: https://www.bangkokpost.com/tech/local-news/1021773/smartphone-subscriptions-near-50m

Bank of Thailand. (2017, August 31). Use of mobile banking and internet banking. Retrieved from Bank of Thailand Official Web Site: http://www2.bot.or.th/statistics/ReportPage.aspx?reportID=688&language=eng

Bank of Thailand. (2017, August 31). Use of mobile banking and internet banking. Retrieved from Bank of Thailand Official Website: http://www2.bot.or.th/statistics/ReportPage.aspx?reportID=688&language=eng

Bayus, B. L., & Kuppuswamy, V. (2015, October 28). A REVIEW OF CROWDFUNDING RESEARCH AND FINDINGS. (D. Mitra, Ed.) Retrieved September 14, 2017, from SSRN: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2685739

Boonperm, J., Wayuparb, S., Mutraden, A., & Tangpoolcharoen, J. (2016, March). Thailand Internet User Profile 2015. Retrieved November 24, 2017, from Electronic Transactions Development Agency: http://unctad.org/meetings/en/Contribution/dtl_eweek2016_ETDA_IUP_en.pdf

Carlos T., T. O. (2017). Literature review of mobile The current issue and full text archive of this journal is available on Emerald Insight. International Journal of Bank Marketing, 1048.

Charles, B. S. (2017, June 6). Security Intelligence. (IBM, Producer, & IBM) Retrieved from Securityintelligence.com: https://securityintelligence.com/is-mobile-banking-safe/

Chung, K. C. (2009, December ). Understanding factors affecting trust in and satisfaction with mobile banking in Korea: A modified DeLone and McLean’s model perspective. Interacting With Computers, 385-392.

Ref. code: 25605902040087AGC

27

Crowdsourcing.org. (2012, May). CROWDFUNDING INDUSTRY REPORT : Market Trends, Composition and Crowdfunding Platforms. Retrieved November 14, 2017, from Crowdfunding: http://www.crowdfunding.nl/wp-content/uploads/2012/05/92834651-Massolution-abridged-Crowd-Funding-Industry-Report1.pdf

Cumming, D., Schwienbacher, A., & Leboeuf, G. (2014, January). Crowdfunding Models: Keep-it-All vs. All-or-Nothing. Retrieved December 3, 2017, from Researchgate: https://www.researchgate.net/publication/272306935_Crowdfunding_Models_Keep-it-All_vs_All-or-Nothing

David T., M. S. (2013). Analytics: The real-world use of big data in financial services. Saïd Business School at the University of Oxford . New York: IBM Global Business Services .

DBS Group Research. (2015). Regional Industry Focus ASEAN Banks. Singapore: DBS Vickers Securities.

Deloiotte. (2015). Digital banking for small and medium-sized enterprises Improving access to finance for the underserved. Deloiotte Southeast Asia .

Deloitte. (2010). Mobile banking A catalyst for improving bank performance. Deloitte Development.

Deshwal, Dr. Parul. (2015, December). A Study of Mobile Banking in India. International Journal of Adcanced Research in IT and Engineering, 6-7.

Deshwal, Dr. Parul. (2015, December). A Study of Mobile Banking in India. International Journal of Advanced Research in IT and Engineering, 2-4.

Education, M. o. (2017, August). Aveage Education Years for Thai Population 2012-2017. Retrieved March 26, 2018, from Ministry of Education: http://backoffice.onec.go.th/uploads/Book/1554-file.pdf

Gerber, E., Hui, J., & Kuo, P.-Y. (2012, Febuary). Crowdfunding: Why People are Motivated to Post and Fund Projects on Crowdfunding Platforms. Retrieved September 17, 2017, from ResearchGate: https://www.researchgate.net/publication/261359489_Crowdfunding_Why_People_are_Motivated_to_Post_and_Fund_Projects_on_Crowdfunding_Platforms

Hoehle, H. H. (2012). Advancing task-technology fit theory: a formative measurement approach to determining task-channel fit for electronic banking channels. Information Systems Foundations: Theory Building in Information Systems, 133-169.

index mundi. (2018, January 20). Thailand Demographics Profile 2018. Retrieved March 26, 2018, from index mundi: https://www.indexmundi.com/thailand/demographics_profile.html

Ref. code: 25605902040087AGC

28

Index Mundi. (2018, January 20). Thailand Demographics Profile 2018. Retrieved April 1, 2018, from Index Muni : https://www.indexmundi.com/thailand/demographics_profile.html

Investopedia. (2018, March 7). Hierarchy-Of-Effects Theory. Retrieved from Investorpedia: https://www.investopedia.com/terms/h/hierarchy-of-effects-theory.asp#ixzz5936AAmxa

Investopedia. (n.d.). Herd Instinct. Retrieved December 5, 2017, from Investopedia: https://www.investopedia.com/terms/h/herdinstinct.asp

Kasikorn Research. (2017). PromptPay to Help Create Cashless Society and Long-Term Economic Benefits Despite Cutting Banks’ Fee Income . Bangkok: Kasikorn Research.

Kuppuswamy, V., & Bayus , B. L. (2013, March 16). CROWDFUNDING CREATIVE IDEAS: THE DYNAMICS OF PROJECT BACKERS IN KICKSTARTE. Retrieved October 14, 2017, from https://funginstitute.berkeley.edu/wp-content/uploads/2013/11/Crowdfunding_Creative_Ideas.pdf

Laukkanen, T. (2007). Internet vs mobile banking: comparing customer value perceptions. Business Process Management Journal, 788-797.

Lor, M. J. (2017, September 9). Asiola Performance as a leading Crowdfunding in Thailand. (P. Kangwankit, Interviewer)

Massolution. (2015, March 31). 2015 Massolution Report Released: Crowdfunding Market Grows 167% in 2014, Crowdfunding Platforms Raise $16.2 Billion. Retrieved November 14, 2017, from NCFA : National Crowdfunding Association of Canada: http://ncfacanada.org/2015-massolution-report-released-crowdfunding-market-grows-167-in-2014-crowdfunding-platforms-raise-16-2-billion/

McKinsey&Company. (2015). Digital Banking in ASEAN: Increasing Consumer Sophistication and Openness. Asia Consumer Insights Center. McKinsey&Company.

McKinsey&Company. (2015). Digital Banking in Asia: What do consumers really want? . McKinsey&Company.

Meyskens, M., & Bird, L. (2015, January). Crowdfunding and Value Creation. Retrieved December 5, 2017, from Researchgate: https://www.researchgate.net/publication/277637559_Crowdfunding_and_Value_Creation

Mollick, E. (2013, June 26). The Untold story behind Kickstarter stats. Retrieved September 26, 2017, from Appsblogger: http://www.appsblogger.com/behind-kickstarter-crowdfunding-stats/

Ref. code: 25605902040087AGC

29

Moritz, A., & Block, J. H. (2014, August 11). Crowdfunding: A Literature Review and Research Directions. Retrieved November 9, 2017, from SSRN: https://papers.ssrn.com/sol3/Papers.cfm?abstract_id=2554444

Munongo, S. K. (2013, November 1). Extending the Technology Acceptance Model to Mobile Banking Adoption in Rural Zimbabwe. Journal of Business Administration and Education, 51-79.

Nielsen. (2014, Febuary 12). Nielsen Pressroom. Retrieved from Nielsen Official Website: http://www.nielsen.com/my/en/press-room/2014/preferred-payment-methods.html

P. Dupas, S. G. (2012, Febuary). CHALLENGES IN BANKING THE RURAL POOR: EVIDENCE FROM KENYA'S WESTERN PROVINCE. National Bureau of Economic Research Working Paper Series.

Philipp Haas, I. B. (2014). An empirical taxonomy of crowdfunding. Conference: International Conference on Information Systems (ICIS) 2014, (p. 18). Auckland, New Zealand. Retrieved November 17, 2017, from Paper presented at the International Conference on Information Systems: https://www.alexandria.unisg.ch/234893/1/Haas%20et%20al%20-%20An%20Empirical%20Taxonomy%20of%20Crowdfunding%20Intermediaries.pdf

Prive, T. (2012, November 27). What Is Crowdfunding And How Does It Benefit The Economy. Retrieved November 9, 2017, from Forbes: https://www.forbes.com/sites/tanyaprive/2012/11/27/what-is-crowdfunding-and-how-does-it-benefit-the-economy/#2f57fbc1be63

Pual Belleflamme, T. L. (2012, April 25). Crowdfunding: Tapping the Right Crowd. Retrieved November 9, 2017, from Innovation & Regulation Chair: http://innovation-regulation2.telecom-paristech.fr/wp-content/uploads/2012/10/Belleflamme-CROWD-2012-06-20_SMJ.pdf

Qiu, C. (2013, October 27). Issues in Crowdfunding: Theoretical and Empirical Investigation on Kickstarter. Retrieved November 15, 2017, from SSRN: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2345872

Rammile, N. &. (2012). Understanding resistance to cell phone banking adoption through the application of the technology acceptance model (TAM). African Journal of Business Management, 86-97.

SCB Economic Intelligence Center. (2016, October 13). EIC Analysis / Interesting Topics. Retrieved from SCB Economic Intelligence Center: https://www.scbeic.com/en/detail/product/2913

STARTUP FUNDING BOOK. (2017, November 17). TYPES OF CROWDFUNDING RELEVANT FOR STARTUPS. Retrieved from STARTUP FUNDING BOOK: https://startupfundingbook.com/category/crowdfunding/

Ref. code: 25605902040087AGC

30

Statista. (2017). Crowdfunding : Thailand. Retrieved November 15, 2017, from Statista: https://www.statista.com/outlook/335/126/crowdfunding/thailand#

Statista. (2017). Thailand Fintech Overview. Retrieved from www.statista.com: https://www.statista.com/outlook/295/126/fintech/thailand#

Taylor, B. (2015, May 22). 6 things almost every viral Kickstarter has in common. Retrieved October 14, 2017, from PCWorld: https://www.pcworld.com/article/2924327/web-social/6-things-almost-every-viral-kickstarter-has-in-common.html

Team, T. (2017, December 27). Here’s What Happened in Thailand’s Startup Ecosystem in 2017. Retrieved March 29, 2018, from Techsauce: https://techsauce.co/en/country-en/thailand-en/heres-happened-thailands-startup-ecosystem-2017/

Technavio Research. (2017, August 14). Global Crowdfunding Market - Segmentation and Forecast by Technavio. Retrieved September 30, 2017, from BusinessWire: http://www.businesswire.com/news/home/20170814005545/en/Global-Crowdfunding-Market---Segmentation-Forecast-Technavio

The Asian Banker. (2017, July 4). The Asian Banker Official Website. Retrieved from Research Note: http://www.theasianbanker.com/updates-and-articles/mobile-banking-seen-to-overtake-internet-banking

The Nation. (2016, December 23). Digitisation of banking system to continue in 2017. Retrieved from www.nationmultimedia.com: http://www.nationmultimedia.com/news/business/EconomyAndTourism/30302676

The Nation. (2017, August 31). The Nation, Thailand Portal. Retrieved from The Nation Official Website: http://www.nationmultimedia.com/detail/Economy/30325327

Thuy, N. N. (2017, August). The Impact of Project and Founder Quality on funding success. CROWDFUNDING IN VIETNAM: The Impact of Project and Founder Quality on funding success., 59. Retrieved January 20, 2018, from http://essay.utwente.nl/73270/1/Nguyen_MA_BMS.pdf

Ward, C., & Ramachandran, V. (2010). Crowdfunding the next hit: Microfunding online experience. Retrieved November 15, 2017, from In Workshop on Computational Social Science and the Wisdom of Crowds at NIPS2010: http://people.cs.umass.edu/~wallach/workshops/nips2010css/papers/ward.pdf

XinLuo, H. J. (2010, May). Examining Multi- Dimensional Trust and Multi-Faceted Risk in Initial Acceptance of Emerging Technologies: An Empirical Study of Mobile Banking Services. Decision Support Systems, 222-234.

Yeh, A. (2015, October 6). New Research Study: 7 Stats from 100,000 Crowdfunding Campaigns. Retrieved November 17, 2017, from Indiegogo:

Hi! I want to thank you for taking the time to meet with me today. My name is

Win and I would like to talk to you about your perception and past experience

regarding mobile banking in Thailand. The interview should take less than an hour. I

hope you don’t mind me voice recording the session because I don’t want to miss any

of your comments. All of your responses will be kept confidential and I will ensure

that any information I include in my report does not identify you as the respondent.

Remember, you don’t have to talk about anything you don’t want to and you may end

the interview at any time. Feel free to ask any questions before we begin the session.

1.2 Questions

1) Describe the top 3 words that comes to your mind when you think about mobile banking (e.g. convenient, money transfer, Prompt Pay)

2) Identify all mobile banking services that you are aware of (e.g. money transfer, bank balance check, bill payment.)

3) Describe your mobile banking usage frequency and time of usage (e.g. weekly, mid-day.)

4) Describe mobile banking purpose of use (e.g. online shopping, work-related, personal affairs)

5) Describe mobile banking services that you have used and the average amount per transaction (e.g. money transfer, bill payment, approximately 2,000 THB per transaction)

6) Describe any positive perceptions or experiences that you have towards mobile banking, if any (e.g. convenient, cashless society, diverse service offerings.) Please provide justification for your response.

Ref. code: 25605902040087AGC

34

7) Describe any negative perceptions or experiences that you have towards mobile banking, if any (e.g. security concerns, application malfunction, hard to use.) Describe how did you overcame those negative experiences.

8) To what extend did the adoption and advancement of mobile banking change your behavior as a consumer (e.g. less cash dependent, subconsciously spend more money, increased trust in e-commerce)

9) If you could give any recommendations to commercial banks or government agencies regarding mobile banking, what are the top 3 recommendations you would give?

1.3 Interview closing

Feel free to add any additional comments before we end the interview. I’ll be

analyzing the information you and others gave me and I’ll be happy to send you a

copy of my research, if you are interested. Thank you for your time.

Ref. code: 25605902040087AGC

35

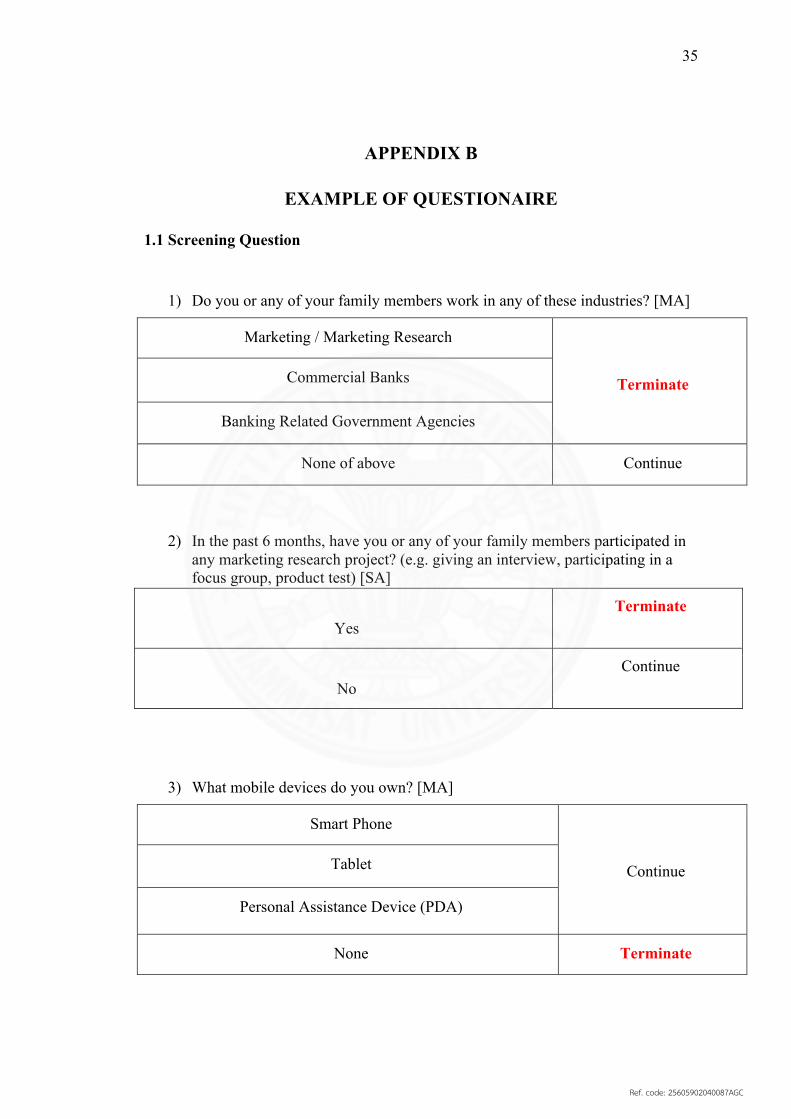

APPENDIX B

EXAMPLE OF QUESTIONAIRE

1.1 Screening Question

1) Do you or any of your family members work in any of these industries? [MA]

Marketing / Marketing Research

Terminate Commercial Banks

Banking Related Government Agencies

None of above Continue

2) In the past 6 months, have you or any of your family members participated in any marketing research project? (e.g. giving an interview, participating in a focus group, product test) [SA]

Yes

Terminate

No

Continue

3) What mobile devices do you own? [MA]

Smart Phone

Continue Tablet

Personal Assistance Device (PDA)

None Terminate

Ref. code: 25605902040087AGC

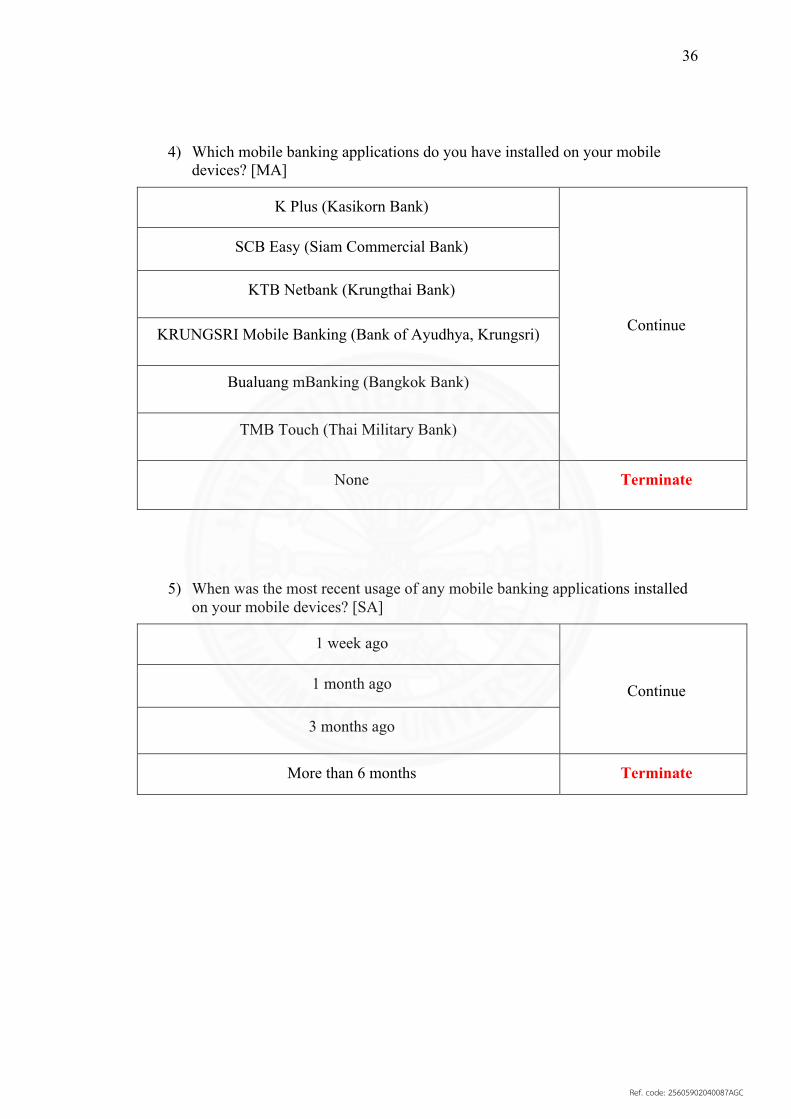

36

4) Which mobile banking applications do you have installed on your mobile devices? [MA]

K Plus (Kasikorn Bank)

Continue

SCB Easy (Siam Commercial Bank)

KTB Netbank (Krungthai Bank)

KRUNGSRI Mobile Banking (Bank of Ayudhya, Krungsri)

Bualuang mBanking (Bangkok Bank)

TMB Touch (Thai Military Bank)

None Terminate

5) When was the most recent usage of any mobile banking applications installed on your mobile devices? [SA]

1 week ago

Continue 1 month ago

3 months ago

More than 6 months Terminate

Ref. code: 25605902040087AGC

37

6) What is your age? [SA]

Less than 15 years old Terminate

15 – 24 years old

Continue

25 – 34 years old

35 – 44 years old

45 – 54 years old

Over 54 years old Terminate

1.2 Survey Question

Objectives Methodology Sample Research Questions

3.1 To identify awareness and usage among current mobile banking users

3.1.1 To identify mobile banking usage rate

3.1.2 To identify service awareness

Online Survey Questionnaire

Which mobile banking applications do you know?

Which mobile banking applications have you used?

What are the top 3 mobile banking applications that comes to your mind?

How often do you use mobile banking applications?

What are the services available on mobile banking that you know of?

Ref. code: 25605902040087AGC

38

3.2 Explore current behavior of current mobile banking user

3.2.1 To determine behavior usage purpose

3.2.2 To determine the importance of available services that drive usage

3.2.3 To determine usage occasion

3.2.4 To determine average transaction amount

Online Survey Questionnaire

What is the 3 most common services you use in mobile banking?

Do you use mobile banking for personal accounts or work related matters?

What mobile banking services would you like banks to develop in the future?

What services would you like banks to eliminate in the future?

How satisfied are you with your current interactions with mobile banking?

Which attributes are important to you when adopting a mobile banking application?

What time or the day do you use mobile banking the most?

On average how much do you spend on transaction?

3.3 To identify mobile banking user segment

3.3.1 To explore demographic profiles, lifestyle and behavior of each user segment

3.3.2 To identify mobile banking needs of each segment

Online Survey Questionnaire

What is your gender?

What is your average monthly income?

What is your average monthly household income?

What kind of a lifestyle do you have?

In what ways can banks improvement mobile banking?

3.4 To identify any changes in consumer behavior influenced by mobile banking

Online Survey Questionnaire

Did mobile banking have a positive or negative impact on your life?

What behavioral changes did you have after mobile banking adoption?