DOI: 10.4018/IJWLTT.2020070103 International Journal of Web-Based Learning and Teaching Technologies Volume 15 • Issue 3 • July-September 2020 31 Using Deming’s Cycle for Improvement in a Course: A Case Study Anil K. Aggarwal, University of Baltimore, USA ABSTRACT Theboundariesbetweenaccountingandtechnologyisbecomingfuzzierasaccountingcompaniesare becomingconsultingcompanies.Digitaleconomiesarechangingbusinessmodelsandcompaniesthat donotadeptcanbecomeobsoleteveryfast.Evenprofessionalorganizationsarerecommendingusing technologytomodernize,automateandexpediteaccountingdiscipline.Therefore,itisnecessaryto trainpersonneltobecomecompetentinbothtechnologyandaccounting.Universitiesarefulfillingthis requirementbyofferingcoursessuchasAccountingInformationSystems,dataanalytics,bigdata,etc. ThisarticleusesDeming’sPlanDoCheckAct(PDCA)cycleforlongitudinalassessmentandimprovement oftheAIScourse.Insteadofre-inventingthewheel,instructorscanlearnfromourexperience.This articlewouldbeusefulforinstructorstryingdifferentandemergingapproaches.Inaddition,thisarticle wouldbeusefulforinstructorstryingtoengagestudentsandtotrainthemforfuturechallenges. KeyWoRDS Accounting Information Systems, Case Study, Longitudinal Assessment, PDCA Cycle INTRoDUCTIoN Astechnologydiffusesacrossorganizations,functionalboundariesarebecomingblurred.Accounting firm, Deloitte Touche Tohmatsu Limited (DTTL), advertises themselves as offering technology services,“Todaybusinessandtechnologyareinextricablylinked…keepingpacewiththeemerging technologylandscapecanbedifficultforeventhemosttech-savvyleaders.”Businessesarerecognizing theevolvingnatureoffastpacedtechnologiesthatischangingclientrequirements.Clientsareasking foracompleteseamlesssolutiontotheirproblems.Itisnotonlytax,auditorbalancesheets,butit is“off-the-shelf”totalpackagetheyaredemanding.Bigaccountingcompaniesaretransformingas AccountingInformationSystemsServices(AISS)companiesbyprovidingnotonlytaxandaudit consultation,butalsoITrelatedadvicetotheirclients.AccordingtoaPathwayCommissionReport onAccountingEducation,(2012): …businesses are processes, not buckets of accounting information. If the accounting community continues to concentrate on the financial accounting system and not understanding the technology Thisarticle,originallypublishedunderIGIGlobal’scopyrightonJuly1,2020willproceedwithpublicationasanOpenAccessarticlestart- ingonJanuary28,2021inthegoldOpenAccessjournal,InternationalJournalofWeb-BasedLearningandTeachingTechnologies(con- vertedtogoldOpenAccessJanuary1,2021),andwillbedistributedunderthetermsoftheCreativeCommonsAttributionLicense(http:// creativecommons.org/licenses/by/4.0/)whichpermitsunrestricteduse,distribution,andproductioninanymedium,providedtheauthorof theoriginalworkandoriginalpublicationsourceareproperlycredited.

Transcript

DOI: 10.4018/IJWLTT.2020070103

International Journal of Web-Based Learning and Teaching TechnologiesVolume 15 • Issue 3 • July-September 2020

…businesses are processes, not buckets of accounting information. If the accounting community continues to concentrate on the financial accounting system and not understanding the technology

International Journal of Web-Based Learning and Teaching TechnologiesVolume 15 • Issue 3 • July-September 2020

32

and dynamic business processes that run companies of the 21st century, the accounting profession has the potential to become obsolete. While this may be a bit strong, the point was made loud and clear: Our students and faculty need to adapt to the speed of change of technology and business practices.

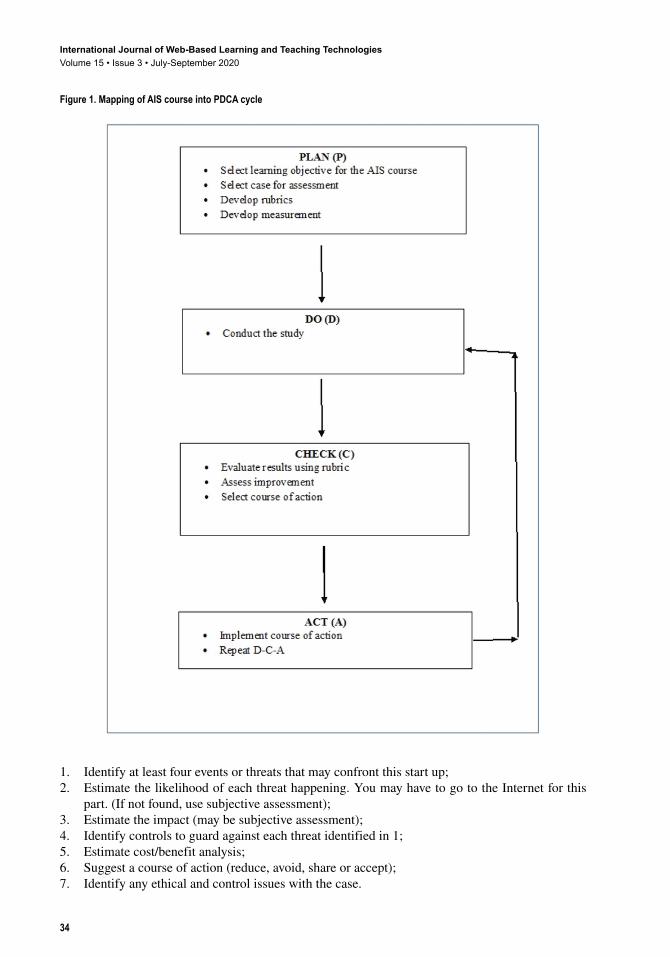

Advances in technologydemandcompleteandseamless training thatgoesacross functionalareas.Ascompaniesprovidewholesolutions,itbecomesmoreimportantnotonlytocomplywithregulationsliketheSOX,HIPPA,etc.,buttoaccomplishthemefficientlyandintheshortesttimepossible.Technologyistheretoassistinthisendeavor.UniversitiesarefulfillingthisknowledgegapbyofferingcoursessuchasAccountingInformationSystemAIS),DataAnalytics inAccountingetc.).Universitiesmusttrainstudentstobetterunderstandthedata,processesandtechnologythatcangeneratedesiredreportsandinsightstosatisfyorvalidatecompliance.AISisamovingtargetsincetechnologyischangingrapidly.ItisimportantnotonlydevelopanAIScoursebutalsotoimproveitcontinually.Thispaperaddressesonesuchcourse,namelyAIS,andstudiesitscontinuousimprovementusingPDCAcycleproposedbyDeming.ThisstudyshouldbebeneficialtofacultyplanningtoengagestudentsandcontinuallyimprovetheAIScourses.Insteadofreinventingthewheel,thisstudyprovidesanexcellentstartingpointforcontinuousimprovementandtheassessmentprocess.

AIS is becoming a critical part of all businesses. Özdoğan (2017) noted that technology-basedaccounting start-ups with both accounting professionals and entrepreneurs having an expertiseon information technologieswill come togetherandwill increase in the future,andcloud-basedaccounting initiativeswill shape the futureof theprofession.Adler et al. (2016)noted that it isimportant to train student in real-world understandings of accounting. Describing the currentresearch in accounting, Sangster (2015) noted “accounting faculty publish top-quality researchonaccountingregulation, financialmarkets,business finance,auditing, internationalaccounting,managementaccounting,taxation,accountinginsociety,andmore,butnotonwhattheydointheir‘dayjob’–teachingaccounting.”Borthicketal.(2017)alsoshowedimportanceofdataanalysisindecisionmaking.SeveralothersliketheDTTreport(2015),PWCreport(2015)havealsostressedtheimportanceoftechnologyandaccounting.FollowingSangster,AdlerandBorthickthispaperfocusesonanevolvingaccountingcourse-accountinginformationsystems.AISisoneareathatisfusingdifferentdisciplineslikeaccounting,informationsystems,law,databaseanddataanalyticstonameafewanduniversitiesarepreparingstudentsfortheseemergingchallenges.ThoughPDCAwasprimarilyusedinmanufacturing,severalauthorsrecentlyhaveusedittoimprovetheircourse,programsandskills.Sharifetal.(2000)usedPDCAcycletostudyAccountinginformationsystemprogramandrevisedtheirprogramsbasedonseveraliterations.Theireffortswere,however,weredirectedondevelopinganAISprogramratherthanimprovinganAIScourse.Knightetal.(2012)employedDeming’sPDCACycleofcontinuousimprovementasasystematicproceduretoassessPublicRelationsWriting.Afterseveralcyclestheyconcludedpublicrelationswritingisafundamentalskillforstudents’successandpedagogythatteachesstudentstowritenewsreleases.Taniguchietal.(2018)studiedaProjectManagementInformationSystems(PMIS)courseusingPDCAcycle.Authorsconcluded,“thecontinuousimprovementonthereportingqualityofPMISwasfoundtobeeffectiveinachievingqualityofPMISoutputinformationtohelpmanagersindecisionmaking,planning,organizingandcontrollingtheproject.Itwasalsoeffectiveinpositivelyinfluencingprojectmanagementsuccess in termsof thefollowingthreeprojectmanagementdimensions:Doing theprojectattheacceptabletime;Observingthebudget(cost)andMeetingthequalityspecificationsoftheproject.”ThoughabovestudiesusedPDCAapproachbutwerenotdirectlyrelatedtoanAIScourse.Inthisstudy,resultsfromdirectmeasurementsareusedtoevaluateandimprovethecourse.Specifically,threesemesterresultsarecomparedforstudentperformance.Whiletheresultsshow

International Journal of Web-Based Learning and Teaching TechnologiesVolume 15 • Issue 3 • July-September 2020

Accounting Information System (AIS)AISisdefinedasacoursethat:

combines the study and practice of accounting with the design, implementation, and monitoring of information systems. Such systems use modern information technology resources together with traditional accounting controls and methods to provide users the financial information necessary to manage their organizations. (Henson, 2009)

As evidenced by the course objective, AIS includes information systems with accountingapplications.Thiscourseisanatypicalaccountingcoursesinceoutcomesmaybeapproximate(ormany)ratherthanabsolute.Thenextsectiondescribesthemethodologyandthehypothesis.

“A” was given if the student was able to comprehend, analyze and apply the concepts correctly on one hand and an “F” was given if the student did not do any of the part correctly.Since the first two parts (plan and do of the PDCA cycle) are defined to some extent, we will concentrate on the last two parts: check and act.

The Case StudyThestudyinvolvesanundergraduateclassinanAIScoursethatisrequiredofallaccountingmajorsatamid-Atlanticuniversity.Studywasconductedinhybridandweb-basedclasses.Hybridclassesusedwebextensivelyforbothtextualandsoftwareknowledge.Atypicalclasshas12to50studentsdependingonthesemesteranddeliverymode.Thecoursehasmanyinformation-relatedcomponentsandsoftwarecompetenciesareneededtosuccessfullycompletethiscourse.Therewere63studentsinsemester1,53studentsinsemester2and28studentsinsemester3.Thetypicalstudentintheseclassesiseitherafreshmanorsophomoreanddoesnothaveaformalbackgroundininformationsystems.Studentpopulationhasnotchangedovertimeintermsoffunctionalorsurfaceleveldiversityremovingage,gender,raceorfunctionalexpertiseimpactonthetreatmentanditsoutcome.

An assignment on controls was used for this study. This assignment was selected due tocompetencyrequirementsbothinaccountingandintechnology.Abriefdescriptionofassignmentisincludedhere.

The assignment involved a startup food delivery business created by three students, “Threecollegefriends,Johnny,Mesi,andFordareplanningtostartajointventureFood_r_us.Eachofthemiswillingtoput$50,000forthisnewventure.Therearemanyrisksinsuchastartupandtheyrealizeifthebusinessfailstheycouldloseitall.Probabilityofthishappeningis20%.”Theywereprovideddetailsofoperationsandhiringissues,suchas,“TheywillrunthebusinessfromJohnny’sbasementto minimize facility costs.Food_r_us, however, needs to fill twomajor positions, awebmasterandanaccountant.Ms.Lee,afriendofMs.MesiisapossiblewebmastercandidateandMr.Petty,youngerbrotherofJohnnyisapossibleaccountantcandidate.Ms.LeeisworkingasawebmasterforeBayhasacomputersciencedegreeandMr.Pettyisworkingasasalesmanatalocalcardealerandhashighschooldiploma.IfMs.Leeishired,shewouldhavetoresignfromeBay.Thefollowingdeliverableswererequired:

International Journal of Web-Based Learning and Teaching TechnologiesVolume 15 • Issue 3 • July-September 2020

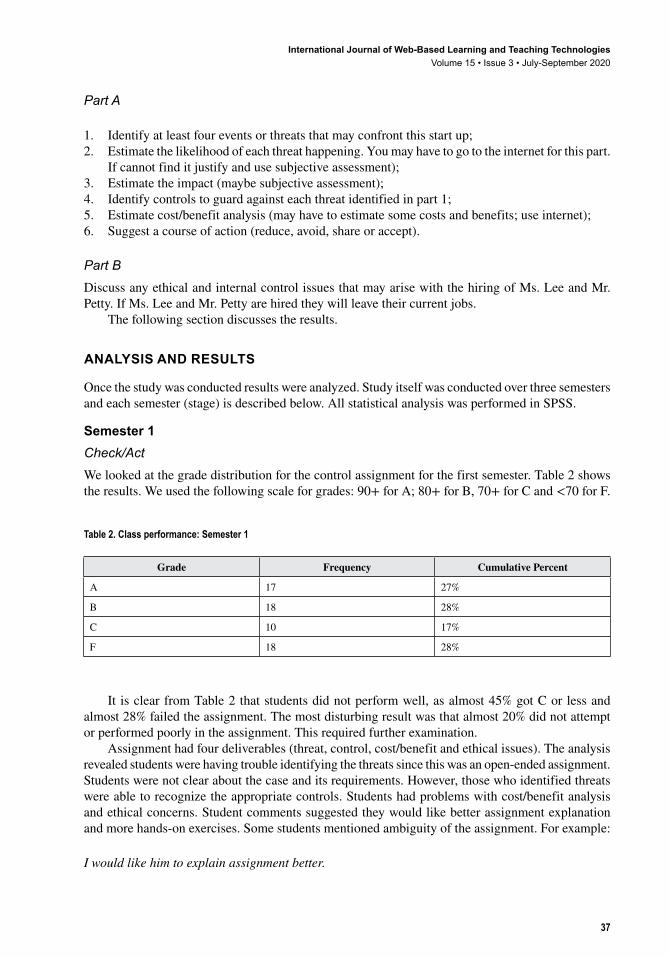

It isclearfromTable2thatstudentsdidnotperformwell,asalmost45%gotCorlessandalmost28%failedtheassignment.Themostdisturbingresultwasthatalmost20%didnotattemptorperformedpoorlyintheassignment.Thisrequiredfurtherexamination.

Check/ActSemester2analysisrevealedthatmoststudentswereabletoidentifythreatsandappropriatecontrols,butwerestillhavingproblemsidentifyingethicalissuesandestimatingcost/benefitsofeachcontrol.To reduce the impactof the repeateduseof a case,original casewasmodifiedwith adifferentscenariobutsimilarrequirements.Thistime,however,weadoptedaroleplayingapproach.Jordietal.(2016)havesuggestedusingdigitalgamestoimprovestudentperformance.Inaddition,Riley

Table 3a. Group statistics

Semesters N Mean Std. Deviation

Assgn32 53 19.7830 6.06575

1 63 15.8095 9.50527

Table 3b. Independent samples test

t-Test for Equality of Means

t df Sig. (2-Tailed)

Assgn3Equalvariancesassumed 2.626 114 .010

Equalvariancesnotassumed 2.724 106.733 .008

International Journal of Web-Based Learning and Teaching TechnologiesVolume 15 • Issue 3 • July-September 2020

Post AnalysisWewantedtolookattheoverallresultsofthisstudy.Table5summarizesthethreesemestersofPDCAcycleresults.Table5summarizestheresultsandFigure2providesgraphicalrepresentationofthestudyovertime.

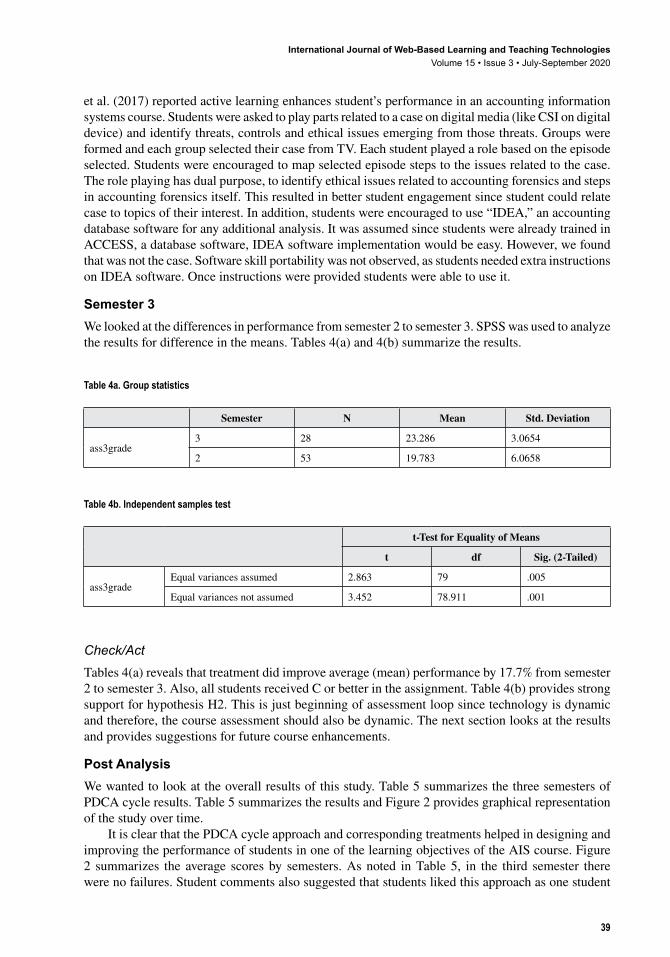

ItisclearthatthePDCAcycleapproachandcorrespondingtreatmentshelpedindesigningandimprovingtheperformanceofstudentsinoneofthelearningobjectivesoftheAIScourse.Figure2 summarizes the average scoresby semesters.Asnoted inTable5, in the third semester therewerenofailures.Studentcommentsalsosuggestedthatstudentslikedthisapproachasonestudent

Table 4a. Group statistics

Semester N Mean Std. Deviation

ass3grade3 28 23.286 3.0654

2 53 19.783 6.0658

Table 4b. Independent samples test

t-Test for Equality of Means

t df Sig. (2-Tailed)

ass3gradeEqualvariancesassumed 2.863 79 .005

Equalvariancesnotassumed 3.452 78.911 .001

International Journal of Web-Based Learning and Teaching TechnologiesVolume 15 • Issue 3 • July-September 2020

Act/FutureThoughwedidachieveourgoa,theAIScourseisamovingtarget.Technologyisrapidlyevolvingandcoursemustevolvewiththetechnology.Researchershaveemphasizedtheimportanceofdata,which in the21stcenturyalso includesunstructureddata.Tornow(2015)discussed theneedsoftoday’sstudentsandconcluded,“studentsshouldbeexposedtoamultitudeofdifferentaccountingsoftwaresothattheylearntomovebeyond“pointandclick”toastageofanalysisthatwillallowthemtoadapttowhateversystemstheyseelaterintheircareers.Dillaetal.(2015)wentastepfurtherandsuggestedteachingdatavisualizationtodetectfraud.Businessintelligenceisbecomingimportantsinceaccountingdealswith rawdata.There is abundanceofdata, students should learnhow toanalyzeandextract“intelligence”,beittodetectfraudortoimproveprocesses.Ina2014AICPAsurvey,researchersfoundelectronicdataanalysis(bigdata)wasnumberoneissueforForensicandvaluationprofessionals.BusinessintelligenceandDataminingareemergingrapidlyandrecentlymanyresearchers(Sivarajahetal.,2017;Richinetal.,2016;Dillaetal.,2015;Vasarhelyietal.,

Skill PortabilityDonotassumeoncestudentslearnasoftwaretheycanport it toanothersoftware.Forexample,studentswholearnedACCESSwerenotabletolearnIDEAontheirownorwithlittleguidance.

International Journal of Web-Based Learning and Teaching TechnologiesVolume 15 • Issue 3 • July-September 2020

43

ReFeReNCeS

Adler,R.,&Stringer,C.(2016).Practitionermentoringofundergraduateaccountingstudents:Helpingpreparestudentstobecomeaccountingprofessionals.Accounting and Finance.

Byrnes,P.,Criste,T.,Stewart,T.,&,Vasarhelyi,M.(2014).Reimagining Auditing in a Wired World.AICPA.Retrievedfromwww.aicpa.org/interestareas/frc/assuranceadvisoryservices/downloadabledocuments/whitepaper_blue_sky_scenario-pinkbook.pdf

Borthick,A.F.,Schneider,G.P.,&Viscelli,T.R.(2016).AnalyzingDataforDecisionMaking:IntegratingSpreadsheetModelingandDatabaseQuerying.Issues in Accounting Education Teaching Notes,32(1),25–41.

Arnold,V.(2018).Thechangingtechnologicalenvironmentandthefutureofbehaviouralresearchinaccounting.Accounting and Finance,58(2),315–339.doi:10.1111/acfi.12218

Bloom,B.S. (1956).Taxonomy of Educational objectives, handbook I: The Cognitive Domain.NewYork:DavidMckayCoInc.

Brooks,G.(2013).AssessmentandAcademicWriting:ALookattheUseofRubricsintheSecondLanguageWritingClassroom.Kwansei Gakuin University humanities review,(17),227-240.

Cascini,K.,&Rich,A.(2007).DevelopingcriticalthinkingskillsintheintermediateAccountingClass:Usingsimulationswithrubrics.Journal of Business Case Studies,3(2).

deKlerk,S.,Eggen,T.J.,&Veldkamp,B.P.(2016).Amethodologyforapplyingstudents’interactivetaskperformancescoresfromamultimedia-basedperformanceassessmentinaBayesianNetwork.Computers in Human Behavior,60,264–279.doi:10.1016/j.chb.2016.02.071

Deming,W.E.(1986).Out of the Crisis.Cambridge,MA:MITCenterforAdvancedEngineeringStudy.

Dilla,W.N.,&Raschke,R.L.(2015).Datavisualizationforfrauddetection:Practiceimplicationsandacallforfutureresearch.International Journal of Accounting Information Systems,16,1–22.

GelinasandDull.(2015).Accounting Information Systems.CengageLearning,Pub.

Henson,W.(2009).Accounting Information Systems.Retrievedfromhttp://earticles.info/e/a/title/ACCOUNTING-INFORMATION-SYSTEMS/

Juran,J.M.(1989).Juran on leadership for quality.NewYork:FreePress.

Knight,J.E.,&Allen,S.(2012).ApplyingthePDCAcycletothecomplextaskofteachingandassessingpublicrelationswriting.International Journal of Higher Education,1(2),67.doi:10.5430/ijhe.v1n2p67

Mancini,D.,Dameri,R.P.,&Bonollo,E.(2016).Lookingforsynergiesbetweenaccountingandinformationtechnologies.InStrengthening information and control systems(pp.1–12).Cham:Springer.doi:10.1007/978-3-319-26488-2_1

Richins,G.,Stapleton,A.,Stratopoulos,T.C.,&Wong,C.(2016).DataAnalyticsandBigData:Opportunityor Threat for the Accounting Profession? Retrieved from https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2813817

Riley,J.,&Ward,K.(2017,May).Ward,KerryWard(2017)ActiveLearning,CooperativeActiveLearning,andPassiveLearningMethodsinanAccountingInformationSystemsCourse.Issues in Accounting Education,32(2),1–16.doi:10.2308/iace-51366

Romney&Steinbart.(2015).Accounting Information Systems.Prentice-Hallpub.

Schaefer,T.,&Stevens,J.S.(2016).UsingRubricstoAssessAccountingLearningGoalAchievement.Issues in Accounting Education,31(1),17–28.doi:10.2308/iace-51261

Sharifi,M.,McCombs,G.B.,&Okopny,D.R.(2000).WhyContinuousImprovementForAnAccountingInformationSystemsProgram?The Review of Accounting Information Systems,4(1),21–29.

Shepherd,C.M.,&Mullane,A.M.(2011).Rubrics:Thekeytofairnessinperformancebasedassessments.Journal of College Teaching and Learning,5(9).doi:10.19030/tlc.v5i9.1231

Sivarajah,U.,Kamal,M.M.,Irani,Z.,&Weerakkody,V.(2017).CriticalanalysisofBigDatachallengesandanalyticalmethods.Journal of Business Research,70,263–286.doi:10.1016/j.jbusres.2016.08.001

Smith, J., & Binti Puasa, S. (2016, February). Critical factors of accounting information systems (AIS)effectiveness:aqualitativestudyoftheMalaysianfederalgovernment.InProceedings of the British Accounting & Finance Association Annual Conference 2016.AcademicPress.

Stegeman, M., Barendsen, E., & Smetsers, S. (2016). Designing a rubric for feedback on code quality inprogrammingcourses.InProceedings of the 16th Koli Calling International Conference on Computing Education Research(pp.160-164).ACM.doi:10.1145/2999541.2999555

Taniguchi,A.,&Onosato,M.(2018).EffectofContinuousImprovementontheReportingQualityofProjectManagementInformationSystemforProjectManagementSuccess,I.J.Information Technology and Computer Science,1,1–15.

The Pathways Commission Charting a National Strategy for the Next Generation of Accountants. (2012).Retrievedfromhttp://blog.aicpa.org/2012/08/in-the-news-pathways-commission-releases-report-on-future-of-accounting-education.html#sthash.BoIRSmTo.dpbs

Wilkin,C.L.(2014).EnhancingtheAIScurriculum:Integrationofaresearch-led,problem-basedlearningtask.Journal of Accounting Education,32(2),185–199.doi:10.1016/j.jaccedu.2014.04.001

Xu,H.(2015).WhatarethemostimportantfactorsforaccountinginformationqualityandtheirimpactonAISdataqualityoutcomes?Journal of Data and Information Quality,5(4),14.doi:10.1145/2700833

International Journal of Web-Based Learning and Teaching TechnologiesVolume 15 • Issue 3 • July-September 2020

45

Anil Aggarwal is a Professor in the Merrick School of Business at the University of Baltimore. Dr. Aggarwal was a Fulbright scholar and held Lockheed Martin Research and BGE Chair at the University of Baltimore. He has published in many journals, including Computers and Operations Research, Decision Sciences, Information and Management, Production and Operation Management, e-Service, Decision Sciences - Journal of Innovative Education, Journal of Information Technology Education: Innovations in Practice, Total Quality Management & Business Excellence, eService, International Journal of Web-Based Learning and Teaching Technologies and Journal of EUC and many national and international professional proceedings. He has published four edited books -- web-based education (2), cloud computing (1) and Big Data (1). His current research interests include web-based education, business ethics, Big Data, virtual team collaboration, and Cloud computing.