23

74 74 V. IFRS 4 Insurance Project

7474

V. IFRS 4 Insurance Project

7575

Agenda

» Background

» Two of the key objectives

» Measurement of Insurance Contracts

» Estimating the Margin (s)

» Acquisition Costs

» Discount Rate

» Timeline

See also:

http://www.iasb.org/Current+Projects/IASB+Projects/Insurance+Contracts/Insurance+Contracts.htm

7676

Background

» About time

» Debated for the past 10 years

» Need to fix IFRS 4 Phase 1

» Phase 1 was seen as a transitional phase

7777

Two key objectives

» Measurement of insurance liabilities

» Easy to understand

7878

Overview

» Phase I v/s Phase II

• Phase I

• No single method

• National GAAP is allowed under IFRS phase I

• Very difficult to understand the accounts of insurers

• Very difficult to compare across companies

• Very difficult to compare across jurisdictions

• Not prospective i.e. not based on future cash flows of the contract

• Insurance accounting seen as a black box

7979

Overview

» Phase I v/s Phase II

• Phase II

• A single methodology

• Easier to understand and compare

• Prospective i.e. consider future cash flows

• Use of discount rate

• On an expected basis i.e probability weighted

8080

Overview

» Phase II

» Measurement of insurance contracts i.e. measurement of one insurance contract

» For each contract, measurement of cash outflows on a discounted basis that will form the liabilities on the balance sheet

» For each contract the cash inflows (premiums) will be invested in financial instruments and will be the major part of the assets on the balance sheet

» The assets will support the liabilities

8181

Measurement of insurance liabilities

» Methodology

Single model for all insurance contracts

Prospective

Three building blocks

Contracts with the same risk should be accounted for at the same amount irrespective of how they are sold

The contracts should be re-measured at every reporting date to include the most up to date information, avoiding the „locking-in‟ of assumptions.

If the measurement of the liability on day one exceed the amount of premium paid (e.g. onerous contract), the loss should be taken immediately through income

N.B. Insurance liabilities and insurance contracts one and same thing

8282

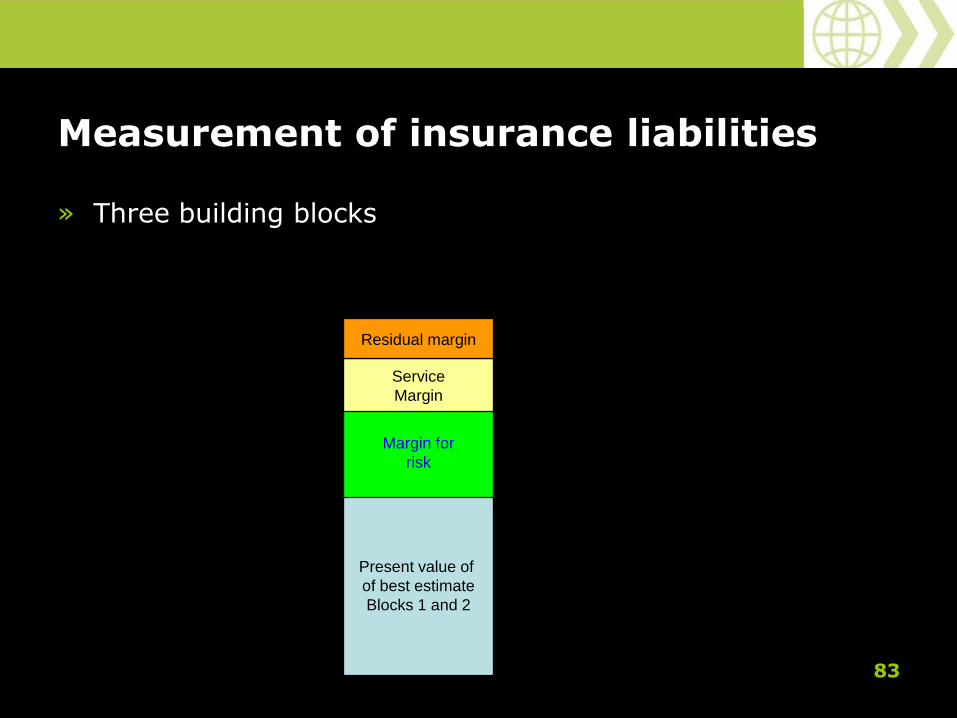

Measurement of insurance liabilities

» Three building blocks

• Block 1: Future cash flows on a probability basis (Best Estimate) also referred as undiscounted probability weighted estimate of future cash flows

• Block 2: Discount the cash flows with a discount rate to account for the effect of time value of money

• Block 3:

- Risk Margin

- Service Margin

- Residual Margin

8383

Measurement of insurance liabilities

» Three building blocks

Present value of

of best estimate

Blocks 1 and 2

Margin for

risk

Service

Margin

Residual margin

8484

Measurement of insurance liabilities

» Best estimate of cash flows

• Non-life e.g. car insurance

• Non life

- Typically 1 year

- Straightforward

- Relatively easy to apply compared to life

8585

Measurement of insurance liabilities

» Best Estimate of cash flows

• Life

• Can be 30 years contract

• Difficult to identify cash flows

• Difficult to identify which cash flows the policyholders are entitled to

• Difficult to identify where and when does the contract terminate i.e. contract boundaries

• Difficult to identify conditions link to renewable contract e.g when and how

8686

Measurement of insurance liabilities

» Best estimate and margin for risk

• Margin represents the underlying estimation uncertainty

• Example:

- Contract A - Payout can be 100 or nil with equal probabilities

- Contract B – Payout can be 51 or 49 with equal probabilities

- What is the probability weighted present value of all the future cash flows in the above two scenarios?

- Which one should in principle amount to a higher liability?

- Which carries more risk?

8787

Measurement of insurance liabilities

» Margin for risk

• The risk margin aims to represent the level of uncertainty in the insurance contract

• Contract A has more risk or uncertainty attached to it and therefore has a higher risk margin. Contract A will have a higher liability

8888

Measurement of insurance liabilities

» Building blocks

• Discount rate: which one to use?

• Risk free discount rates

• Risk free but adjusted with illiquidity premium

8989

Measurement of insurance liabilities

» Discount rate

• Discount rate should reflect the time value of money and risk is reflected in the risk margin. Therefore, in principle, the discount rate is generally called a risk-free rate

• Risk free rates are thought of as government bonds rates

• Financial instruments featuring risk-free rates are generally highly liquid

• However, insurance liabilities are not as liquid as government bonds

• Insurance liabilities are difficult to sell or trade

• That is why some people think that the discount rate should include some element of liquidity risk

9090

Measurement of insurance liabilities

» Discount rate

• This element of liquidity risk would increase the discount rate higher

• Example: Return on highly liquid risk free rate assets could be 5% and premium on illiquidity could add a further 0.8%. This is premium that investors would ask for holding something that is not liquid

• When markets are dislocated, the illiquidity premium could be much higher

• When discounting large amounts over a long period the difference when using risk free discount rate or an illiquidity adjusted discount rate could be very significant

• Choice of discount rate could have significant implications on the value of the insurance liabilities

9191

Measurement of insurance liabilities

» Calibration

• The IASB requires that the initial liability be calculated by calibrating the three building blocks against the premium receivable after the deduction of incremental acquisition costs

• If there is no adjustment for acquisition costs, contracts sold through a more expensive channel (high street broker) will have a higher liability than a similar contract sold through a less expensive route (internet)

• This is because of the presence of a portion in the premium that the policyholder pays to fund the cost of signing the policy

• Incremental costs (selling, underwriting and initiating costs)

• Should not include other direct costs

9292

Measurement of insurance liabilities

» Calibration

• The IASB also requires the recognition of “new business revenue”

• The “new business revenue” is capped to the incremental acquisition costs incurred

• There should never be an accounting profit from selling insurance

• All acquisition costs whether incremental or not must always be expensed through income as incurred although a portion of those acquisition costs would normally be offset by the “new business revenue” on day one

• The above principle is consistent with IAS 39 transaction costs

9393

Measurement of insurance liabilities

» Other key issues to be resolved by the IASB• Selection of appropriate discount rate

• Participating contracts

• Measurement by individual contract or portfolio

9494

Issues for regulators

» Are you up to date on these issues?

» Have you discussed with the auditors in your jurisdictions their state of readiness?

» What is the preparation stage of the insurance industry?

» What is the capacity and ability of supervisors and the industry to supervise and implement the new insurance standard?

» Do you have plan?

9595

Timeline

» Exposure draft to be ready in Q2 of 2010

» Standard to be applicable in 2013

9696

Next steps

» Where can we help on practical issues

• Update on developments on international accounting issues

• Provide help in applying IFRS and regulatory adjustments

• Help you to analyse annual reports

» Provide platform for information exchange and distant learning

» Organise further learning events in your jurisdiction or centrally in Vienna

» Where do we go from here?