Indusind Media & Communications Limited CoDfidential - Not for Circulation PKFSridhar& Santhanam LLP Valuation of Broadband division of Indusind Media & Communications Limited 31^* July 2015 www.pkfindia.in Local Perspective, Global Focus

Transcript

Indusind Media & Communications Limited

CoDfidential - Not for Circulation

PKFSridhar& Santhanam LLP

Valuation of Broadband division of Indusind Media & Communications Limited

• Valuation of the Broadband division of IMCL as on 31®̂ July'15 was done by PKF Sridhar & Santhanam LLP

• Key objective was to get an independent valuation of IMCL's broadband division for the purpose of slump sale to a New Company based on the business plan which reflects the most optimistic assumptions for arriving at valuation conclusions

• The New Company would be entitled to commercially exploit perpetually the existing customer base and supply chain network without any further payment to IMCL for such rights in future

• Valuation analysis was done without a detailed due diligence based on full, frank and complete disclosure by IMCL of all matters that a qualified commercial investor would consider as affecting the valuation of Broadband division of IMCL

Key Valuation Drivers:

1. Existing CATV customer base of 9 mio including 2 Mlo 2. 10,000 Km of hybrid fibre optic cable network for cost subscribers in digital mode effective expansion of broadband connectivity

3. Brand visibility from over 300 channels through IN Digital 4. Best-in-ciass technology partners to build the required network broadband capability frameworks

5. Voice over Internet Protocol to be launched soon for IMCL subscribers and for commercial establishments

Conclusion:

6. Greater thrust on broadband under Digital India Programme of Government of India

Based on the analysis of valuation under various methods , we are of the opinion that Equity Value under the DCF method Is the most appropriate valuation of Broadband division of Indusind Media and Communications Ltd and accordingly valuation of its Broadband division is in the range of R s . 2,469 Million to R s . 2,678 Million.

Indusind Media and Communications Ltd (IMCL), a subsidiary of Hinduja Ventures Ltd., is one of India's largest integrated media companies in India

It has a pan - India presence with a reach of around 9 million subscribers including 2 million in digital mode in 32 locations and offers over 300 channels in the digital mode (IN Digital) and about 90 TV channels in the analogue mode (IN Cablenet).

The company offers the services under various heads

- In Cablenet - Analog Cable

n Digital - Digital Cable

n2Cable - Internet to Cable

n Phone - VOIP/ Internet Telephony

The Broadband business comprising of In2 cable and In Phone caters to around 30,000 customers

The company is considering a slump sale of its broadband division to a new company in line with its strategic plan

We understand that the purchaser of the business would be entitled to commercially exploit perpetually

- entire customer base of IMCL

-en t i re Franchisee and cable TV operator network of IMCL

-en t i re technical network infrastructure of IMCL

We are also informed that since IMCL would not seek any further future payment for such rights, the projected business plan also has been drawn up on most optimistic assumptions to reflect the best possible exploitation of these rights

In light of this scenario, IMCL requires an independent valuation of the Broad band division, reflecting the most optimistic assumptions to reflect the best possible exploitation of these rights, so that the full value of the division is captured in the valuation

IMCL has engaged PKF Sridhar & Santhanam LLP to provide such an independent valuation of its Broadband division for the purpose of slump sale to a New company

PKF Sridhar & Background of Broadband division of IMCL 1/2 santhanam LLP

• In2cable is the broadband / internet division of IMCL and is a "Category A" (all India) ISP licence holder

• Presently, it has a staff strength of 100 employees

• IMCL is a major broadband service provider in 12 cities and is enabling its network to offer several broadband services to its subscriber base

• It offers high speed Internet services to residential, corporate and SME customers.

• For corporate and SME customers IMCL offers dedicated leased line to enable them to manage their data transmission requirements

• In the Initial years, the growth of broadband subscriber base was not at par with the industry growth due to lack of focused attention to its broadband segment

• The company is currently implementing a broadband business plan in cooperation with external consultants and Intel as its technical partner to build a comprehensive services framework that can deliver leading edge voice, video, data and multimedia content services over any broadband or IP-centric network

• The broadband capability of cable systems presents opportunities for cable networks to facilitate the convergence of CATV, broadband data, telephony, and multimedia access

P K F Sridhar & Background of Broadband division of IMCL 2/2 santhanam LLP

The Strategic plan involves sale of the Broadband division to a new company (Newco) under a different ownership with a separate CEO managing the business in order to bring the required focus to grow this business

Newco will get full rights to utilize the existing customer base as well the supply chain network of IMCL and offer its services to these customer using the existing franchisees and cable TV operators network

Newco will also get rights to use the existing network to offer its services. However, it has to make the additional investments required for broad band enablement of the last mile

Sources of Information and Limitation to Scope of our Exercise 1/2

' Ciwiilaabn

PKF Sridhar & Santhanam LLP

Our mandate is to carry out a valuation analysis without a detailed due diligence based on full, frank and complete disclosure by IMCL of all matters that a qualified commercial investor would consider as affecting the valuation of Broadband division of IMCL

Information provided by Indusind Media & Communications Limited (IMCL)

• Financial Information - Historical unaudited Financial Statements for the last 3 years for Broadband

division of IMCL (FY13, FY14 and FY15) ~ Projected Business plan ( FY16 to FY20) that is to be adopted for the broad

band busines

• Consistent with the objectives of the valuation context the projected business plan is the most optimistic business plan in order to fully exploit the existing investment in the network and supply chain - t h e business plan has not been independently appraised by ourselves or any

external agency - W e r e we required to make such an appraisal, additional information could

come to our knowledge which may affect the valuation analysis and our current opinion on the valuation persented in this report

Sources of Information and Limitation to PKFSridhar&

Scope of our Exercise 2/2 santhanam LLP

• External Source

- Publicly available data on Peer companies

• Our conclusions are based on such information being complete and accurate in all material aspects and we have not carried out an audit of such information

• Our exercise should not be construed as:

- Due Diligence study on affairs of IMCL or its Broadband division

-Aud i t in accordance with Standards on Auditing

• Consequently we do not express an opinion on the financial statements used in the report

• Full, Frank and complete disclosure by IMCL of keymatters that a qualified commercial investor would consider affecting the valuation is given in next page

Key aspects disclosures by IMCL relied upon PKFSridhar&

by us 1/2 Santhanam LLP

Does the Technical network infrastructure have any limitations to offer broadband services that are consistent with the services provided by the competition and would enable the business to reach it envisaged market position ?

Has the required capital expenditure to technically put the Broadband division in a position to offer the services envisaged been provided in the Project business plan provided for the valuation ?

Post Slump sale .will the Newco need to make any payment for use of network , supply chain or any other item connected thereto Is IMCL likely to charge any fees ?

Does the Broadband division have full complement of staff for all the functions covered by the business cycle, Viz- Sales, Purchases, production, Inventory and Finance and their costs are factored in the business plan ?

Disclosure

No limitations considering current market offerings by competition

Yes. Our technical team has appraised this and confirmed the capital expenditure factored in the business plan

No. Post slump sale , no further payment for use of network , supply chain will be made by Newco. IMCL will not charge additional fee to Newco.

Yes, We have also factored in the cost of the proposed CEO of the business in the business plan

Key aspects disclosures by IMCL relied upon PKFSridhar&

by us 2/2 Santhanam LLP

Disclosure

Nil.

There are no dependencies

No

None

None

None. No such transactions

required in future

No contingent liabilities to be transferred to Broadband division. No other impediments

None

5 Is the broadband division fully Independent to execute all the activities required for its business cycles? List out dependencies if any

6 Is the cost structure of the company likely to change post the completion of the proposed transaction?

7 Any Legal disputes or other Litigation and its impact on the Broadband division proposed to be sold ?

8 Any regulatory restrictions that are currently affecting the performance of the Broad band division or would potentially affect the future performance ?

9 Intercompany and Group Transactions and any other related party transactions included in the business plan

10 Any Contingent Liabilities and other impediments in running the Broadband division during the entire business plan period

11 Any other disclosure that a qualified commercial investor would consider affecting the valuation

• Indusind Media & Communications Ltd. (IMCL), a subsidiary of Hinduja Ventures Ltd is one of India's largest integrated media companies

• It has a pan-India presence with a reach of around 9 million subscribers in 32 locations

• It is the pioneer in multi system operators

• It has plans for rapid digitalisation and expansion in the next two years with an expectation to reach over two million digital homes and over ten million analogue homes

• The company also engages in leasing out unused fibre to telcos, infrastructure providers, ISPs, and competitors

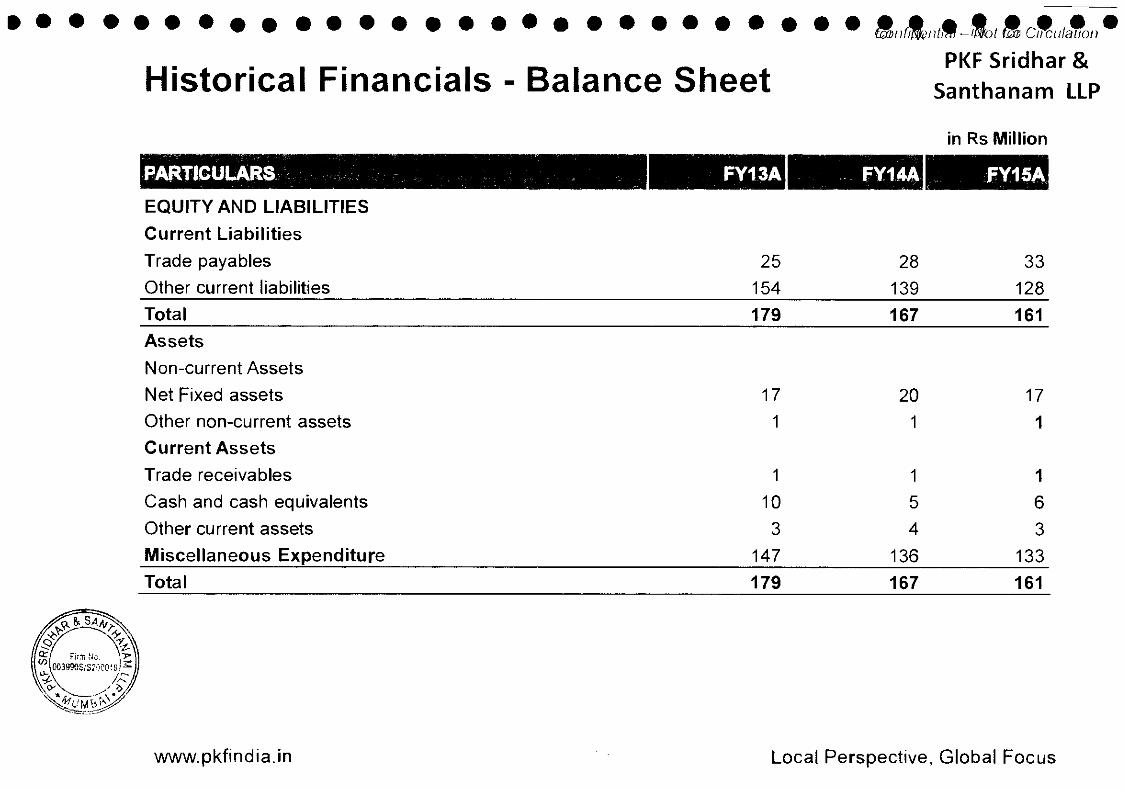

EQUITY AND LIABILITIES Current Liabilities Trade payables Other current liabilities

FY13A

25 154

Total 179 Assets Non-current Assets Net Fixed assets Other non-current assets Current Assets Trade receivables Cash and cash equivalents Other current assets Miscellaneous Expenditure Total

• IMCL began to focus on Broad band division in FY2013 by increasing its revenue through increase in subscriber base and trimming its employee cost and other expenses

• EBIDTA margin in FY 15 is reduced due to significant increase in License Fees in FY 15

• IMCL made investments in to its network in FY 2013 and FY 2014

• IMCL PAT and PBT margin has steadied in FY14 . However PBT margin decreased in FY 15 due to increase in depreciation in proportionate to additions in Fixed Assets mainly Internet equipments.

• The benefit of these investment is likely to be seen in future in terms of increased growth in customers and revenues therefrom

Total Internet Subscribers as on Dec 2014 was 267.39 Million (Source: TRAI )

Demand for Internet and related services in India Is growing at a fast pace. However, as per National Telecom Policy 2012 against a target for achieving 175 million broadband connections by 2017 only about 61 million have been achieved by 2014.

The broadband In India has already generated 9 million direct and indirect jobs. 1 % addition to the broadband penetration can add $2.7 billion to the GDP of the country in the year 2015

Cable players in India have started giving broadband services a lot of serious attention in fiscal 2015 due to low potentials for ARPUs from the conventional cable carriage and subscription business

Drivers of the Broadband Services:

Socio- economic:

Digital classrooms,Telemedicine,Electronic Banking, Entertainment, e -Governance

Commercial:

Video and web collaboration, Video on demand, Video surveillance. Smart - cities, cars, homes, grids,e-Commerce

Technological:

Cloud Computing,Smart devices,Optic Fibre Networks / 4G,M2M,Digitization of content, Social Networking

www.pkf ind ia . in

Internet Subscription base in India as of Dec 2014-267.39 Mio

Total Broadband subscriber base- 85.68 Mlo as on Dec 2014

. . A ^ ^, . P K F Sridhar & Industry Outlook santhanam LLP

" A 10 % increase in broadband penetration increases the per capita GDP by 1.38% in the

developing countries" World Bank

<d-7

!j -i^t r im No.

Broadband is seen as a backbone for the India's ambitious 'Digital India' initiative and Rs 7000- crore mega programme to build 100 smart cities besides many ongoing E-Governance Projects as well as robust eCommerce opportunity.

"India is set for a " digital revolution" as it implements a $18 billion program to expand high speed Internet access and offer government services online" Ravi Shankar Prasad , Minister of Communications and IT

Of the 4.7 Billion internet users in 2025, 700 million will be from India. {Source'. Microsoft Report Cyberspace 2025- Today's decisions, Tomorrow's Terrain - June 2014 )

According to the Telecom Regulatory Authority of India (TRAI), of India's 250 million households, only approximately 15 million, or six percent, have a wired broadband connection.

The Department of Telecom (DoT) is exploring the idea of using the services of cable operators and multiple system operators to provide broadband connectivity to customers . The idea is that cable TV provides last mile connectivity and this can be used to provide broadband connectivity by tweaking technology. {Source : The Hindu - March 2015 )

www.pkf ind ia . in Local Perspect ive, Global Focus

Growth Plans for Broadband Division PKF Sridhar & Santhanam LLP

IMCL has plans to increase the Broadband subscriber base from 30,000 to 2,50,000 in FY 2020 by exploring its current Digital customer base of 2 million subscribers .

Number of Subscribers

250000

200000

150000

100000

237500

50000 29700

30 0

78400 H

39400 I I 29700 ^ • H

;oJ| 6 0 J 1 6 0 J 3123

166250 •

121875 H H

, jj s y j 12JI FY2015 FY2016 FY2017 FY2018 FY2019 FY2020

We note that the business plan is to be made with most optimistic assumptions In the context of current valuation

Business plan involves - Increasing customer base from current 30,000 to 250,000

- Increasing ARPU/month from Rs.8,140 to Rs.9,420 by 2020

- Resulting in increased revenues from Rs. 83.57 Mio to Rs.2.080 Mio by 2020

~ Increase in EBITDA from 1 1 % to 35% by 2020

IMCL's assumptions are driven by following considerations - Current customer base of 2,000,000 and about 700,000 will be added by Dec 2015

- Other than this. IMCL has another 7 Million customers for analog

Only 10% of existing customer base are required to be converted Into broad band subscribers

Lack of focus post Nov 2012 in the broadband business and the cable TV ecosystem due to introduction and streamlining of the digitization mandate of the Government

With a separate CEO in an independent entity, the legacy constraints of the existing business would also not be there

- Further the plan has been developed using the most optimistic assumptions

Even considering the above, the plan is very aggressive and in view of this we have

www.pkfindia.in

placed a 10% additional risk while considering the discount rate

STRENGTHS Continuous growth plan with cable digitalization Pan India presence across 37 locations with 9 million subscribers Leveraging of existing customer base and infrastructure for broadband expansion 'One stop shop' to customers leading to lower subscription cost

OPPORTUNITIES Low broadband penetration in the country

and greater demand for internet connectivity from consumers Expand services to commercial establishment Greater thrust on Broadband under the Digital India Programme of the Government

www.pkfindia.in

PKF Sridhar & Santhanam LLP

CONCERNS Establishing in newer locations already having set top box installed households. Resistance from Local Cable operator in giving up ownership of customers Preparedness and adaptation to rapidly changing technology to deliver application that bring tangible value to peoples life Up gradation of network to cater to the ever increasing data traffic

THREATS • Established telecom companies expanding

its broadband subscriber base • Exposure to cyber-crime and host of other

security risk due to lack of appropriate security In the product, solutions and services

, . PKF Sridhar & Valuation Drivers santhanam l l p

Rich history of two decades in Cable TV network and Broadband service

One of the largest multi system operators providing services of Analogue and Digital cable, Internet, VlOP/ Internet Telephony

Analogue cable under the Brand name - IN Cablenet is considered as India's largest and the world's tenth largest cable TV service provider. Currently, 8.5 million cable connected TV homes across India receive their television programmes from In Cablenet

The key differentiator is the 10,000 km of hybrid fibre optic cable network of which 2,000 km is of underground fibre which will enable IMCL to have cost effective expansion of broadband business

Brand visibility from over 300 channels through IN Digital networks, Including radio / audio channels, which is currently the maximum number of channels provided on any distribution platform in India. This will help IMCL in the future growth plan

Broadband and Internet services provided through cable modems and Ethernet with plans for massive growth with cable digitalisation aided by new national broadband policy of the Government and TRAI

IMCL has engaged the best-in-class technology partners to build the required broadband capability frameworks.

Voice over Internet Protocol will be launched soon for IMCL subscribers and for commercial establishments

Our Standard Valuation Approach 't)mei)i^ -Not ^ C^ulmoii

PKF Sridhar & Santhanam LLP

• We generally will apply one or nnore valuation approaches, analysing principal characteristics of businesses relevant to value and particular considerations required in the valuation to arrive at valuation objective.

• Three broad valuation approaches are as explained below:

- I n c o m e A p p r o a c h : it considers the income that an asset will generate over its remaining useful life. Appropriate yield or discount rate is applied to the projected income stream to arrive at a capital value. Two commonly used methods under Income Approach are Capitalization Method and Discounted C a s h Flow Method

- D i r e c t M a r k e t C o m p a r i s o n A p p r o a c h : It is a comparative approach that compares the subject business to similar businesses, business ownership interests and securities which that have been exchanged in the market. The most common sources of data points are public stock markets, acquisition market and prior transactions in the subject business. Adjustments may be made to render similar business and subject business more comparable.

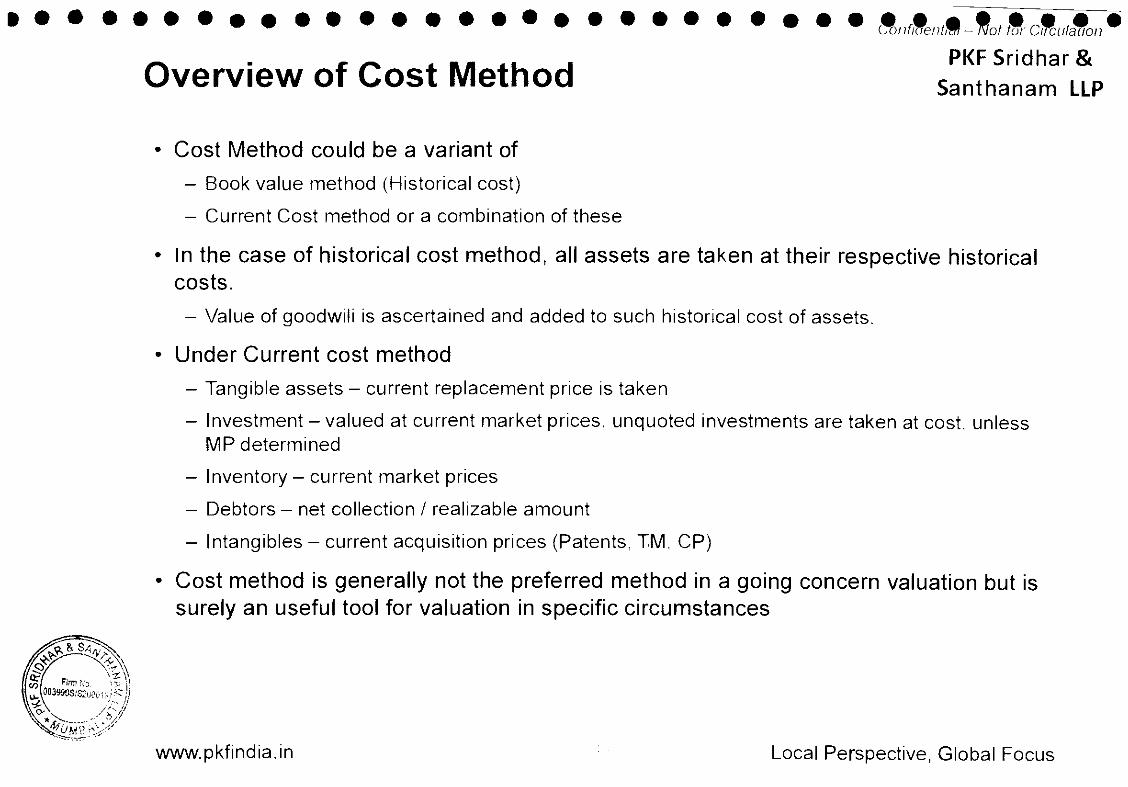

- C o s t A p p r o a c h : It considers the basic economic principle that a buyer will pay no more for an asset than the cost to obtain an asset of equal quality Appropriate adjustments are to be made considering undue time, inconvenience, risk and other factors involved towards the cost of modern equivalent.

• Average profits are capitalised at a proper rate of return, as applicable to the company and the industry.

• The Capitalisation approach can be structured in the following five steps, which are depicted in the graph opposite:

- Determine adjustments for extraordinary items, abnormal losses, taxation, appropriate weights to profits etc

- Decide on the blend of past and future years to be considered

- Determining the maintainable profits based on a blend of past and future financials, evaluating what is best reflective of the potential of the company;

- Determination of the capitalisation rate, which represents a rate of return that considers the relative risk of the Company;

- Determine the value of the business based on the maintainable profits as arrived at the appropriate capitalisation rate determined.

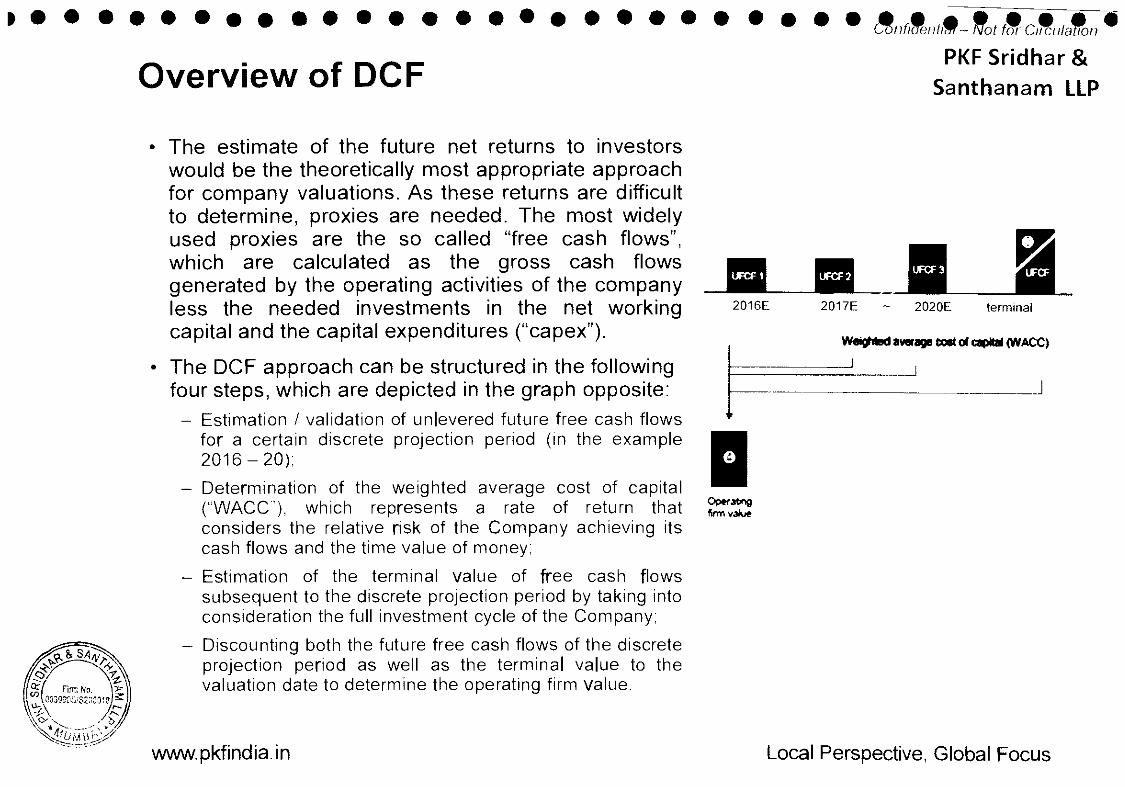

• The estimate of the future net returns to investors would be the theoretically most appropriate approach for company valuations. As these returns are difficult to determine, proxies are needed. The most widely used proxies are the so called "free cash flows", which are calculated as the gross cash flows generated by the operating activities of the company less the needed investments in the net working capital and the capital expenditures ("capex").

• The DCF approach can be structured in the following four steps, which are depicted in the graph opposite:

- Estimation / validation of unlevered future free cash flows for a certain discrete projection period (In the example 2 0 1 6 - 2 0 ) ;

- Determination of the weighted average cost of capital ('AA/ACCT which represents a rate of return that considers the relative risk of the Company achieving its cash flows and the time value of money;

- Estimation of the terminal value of free cash flows subsequent to the discrete projection period by taking into consideration the full investment cycle of the Company;

- Discounting both the future free cash flows of the discrete projection period as well as the terminal value to the valuation date to determine the operating firm value.

Overview of Market Multiple Method PKF Sridhar & Santhanam LLP

The market comparable approach determines the market value of a company by applying metrics from publicly traded companies ("peers group") in similar lines of business.

The conditions and prospects of companies in similar lines of business depend on common factors such as overall demand for their products and services. An analysis of the market multiples of companies engaged in similar businesses yields insights into investor perceptions and, therefore, the value of the subject business.

Key Financial Indicators viz: Revenue EBITDA

Book Value P/E

www.pkfindia.in

Analysis of publicly traded comparable companies.

Multiples based on current market capitalization of

Growth • Stable • Stable Nascent phase / returns business projects new Standard Peer group with high projects business companies capex Cash flow model available involvement projections Short to • No are Medium significant available term intangibles Unique outlook involved business model Long term outlook

Note: These are general criteria in selecting the right valuation model to use and on a case to case basis, judgement is applied by us in choosing the appropriate model for valuation

• Income Approach: Considered ~ IMCL is the pioneer and one of the largest multi system operators in the country with two decades of presence

in Cable TV network.

- Being into Cable TV and Broadband service, IMCL has plans for rapid digitalisation and expansion, considering the historical financials for valuation may not provide a fair value of business as industry outlook is on uptick

- However, DCF method is more appropriate which considers the future cash flow potential of the company as per current business plan

• Direct Market Comparison: Considered for Comparison - No Cable and Broadband service company ( except Hathway Cable) is listed on Indian stock exchange,

however telecom companies with revenue from internet/ broadband services are listed on NSE/ BSE,

- The identified peer companies have different business products mix and experience a different market dynamics .

- Broadband subscription is 10% of the total subscriber base of the peer companies. EV has been proportionately adjusted for arriving at EV/ Subscriber Multiple ( except Hathway Cable )

- Though these companies provide proxies for valuation indices, they are not directly comparable to IMCLs business.

- As there are wide variations in the business mix of each company, Market Multiple Method is considered only to draw comparison and support the valuation done using DCF method

- Thus with limitations on appropriate valuation indices available it is not possible to rely on Market Multiple Method to derive fair valuation of the business

• Cost Approach: Not Considered - Business is not asset driven and asset base is limited to internet equipment only

Cost approach will not showcase a fair benchmark for IMCL

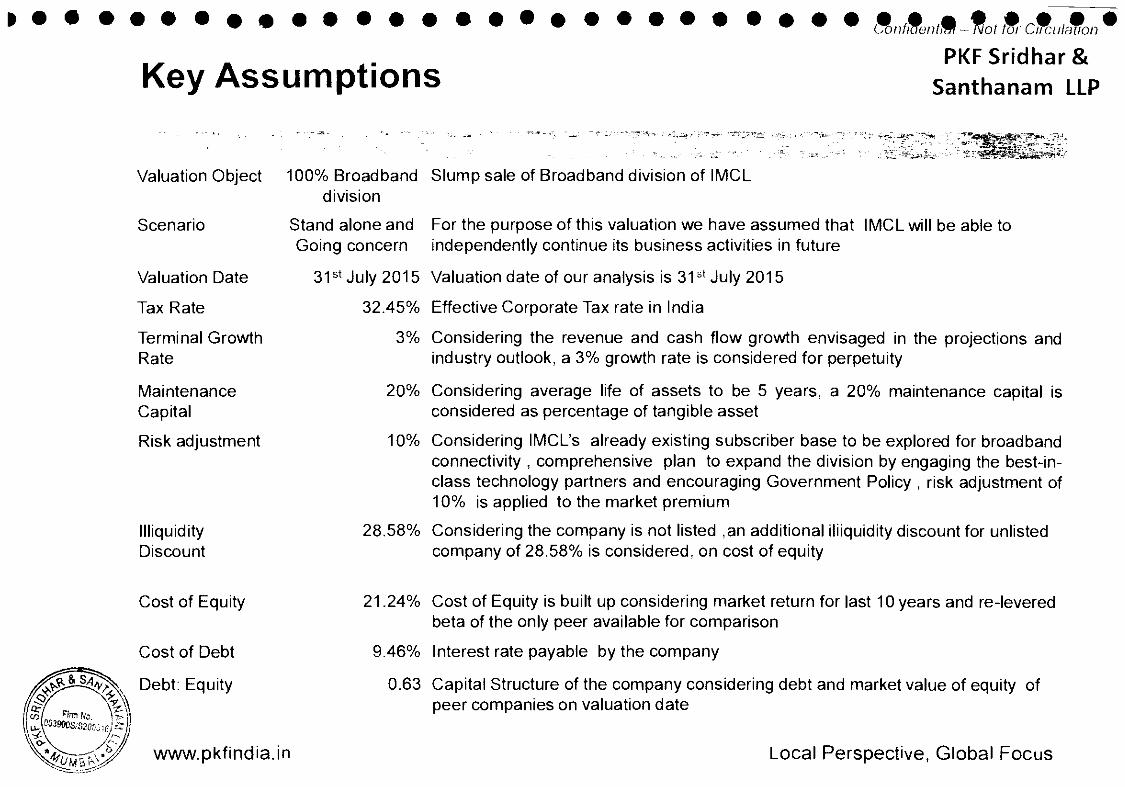

100% Broadband Slump sale of Broadband division of IMCL division

Stand alone and For the purpose of this valuation we have assumed that IMCL will be able to Going concern independently continue its business activities in future

31^^ July 2015 Valuation date of our analysis is 31^* July 2015

32.45% Effective Corporate Tax rate in India

3% Considering the revenue and cash flow growth envisaged in the projections and industry outlook, a 3% growth rate is considered for perpetuity

20% Considering average life of assets to be 5 years, a 20% maintenance capital is considered as percentage of tangible asset

10% Considering IMCL's already existing subscriber base to be explored for broadband connectivity , comprehensive plan to expand the division by engaging the best-in-class technology partners and encouraging Government Policy , risk adjustment of 10% is applied to the market premium

28.58% Considering the company is not listed ,an additional itiiquidity discount for unlisted company of 28.58% is considered, on cost of equity

Cost of Equity

Cost of Debt

Debt: Equity

www.pkfindia.in

21.24% Cost of Equity is built up considering market return for last 10 years and re-levered beta of the only peer available for comparison

9.46% Interest rate payable by the company

0.63 Capital Structure of the company considering debt and market value of equity of peer companies on valuation date

- Calculated considering returns on SNP CNX Index for last lOyears minus risk free rate of government bond - Calculated considering median beta of Peer Companies as on recent date to valuation

IMCL' Equity value based on the forecasted free cash flows for FY16 to FY20 and the terminal value of cash flows is estimated at R s . 2,569 Million

Sensitivity analysis examining the value impacts of incremental changes in the cost of capital (+/- 0.125%) and the growth rate (+/- 0.125%) is depicted above. Derived value range for 100% of IMCL Equity Value from R s . 2,469 Million to R s . 2,678 Million

Our conclusion is based on the prevailing market conditions and on the main assumption that the current business plan will not change in the future (same structure and strategy, no significant changes in the legal and the market environments, no departure of key staff etc.)

Based on the analysis of valuation under various methods and the rationale as enumerated in the Annexures, we are of the opinion that Equity Value under the DCF method is the most appropriate valuation of Broadband division of Indusind Media and Communications Ltd and accordtngly valuation of its Broadband division is in the range of R s . 2,469 Million to R s . 2,678 Million.

The results of this valuation should not be used for any purpose beyond Sept ,2015

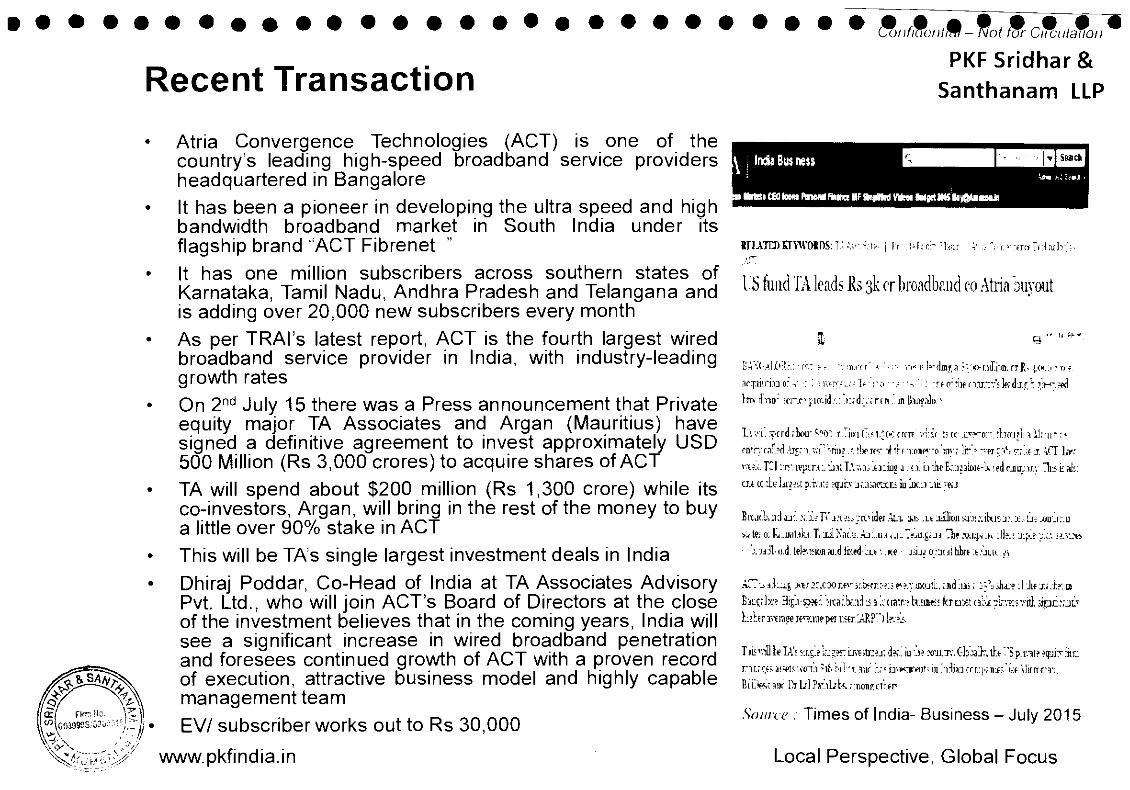

Recent Transaction Atria Convergence Technologies (ACT) is one of the country's leading high-speed broadband service providers headquartered in Bangalore It has been a pioneer in developing the ultra speed and high bandwidth broadband nnarket in South India under its flagship brand "ACT Fibrenet " It has one million subscribers across southern states of Karnataka, Tamil Nadu, Andhra Pradesh and Telangana and is adding over 20,000 new subscribers every month

• As per TRAI's latest report, ACT is the fourth largest wired broadband service provider in India, with industry-leading growth rates On 2"^ July 15 there was a Press announcement that Private equity major TA Associates and Argan (Mauritius) have signed a definitive agreement to invest approximately USD 500 Million (Rs 3,000 crores) to acquire shares of ACT

• TA will spend about $200 million (Rs 1,300 crore) while its co-investors, Argan, will bring in the rest of the money to buy a little over 90% stake in ACT This will be TA's single largest investment deals in India Dhiraj Poddar, Co-Head of India at TA Associates Advisory Pvt. Ltd., who will join ACT's Board of Directors at the close of the investment believes that in the coming years, India will see a significant increase in wired broadband penetration and foresees continued growth of ACT with a proven record of execution, attractive business model and highly capable management team EV/ subscriber works out to Rs 30,000

www.pkfindia.in

• r 9

PKF Sridhar & Santhanam LLP

India Bus ness

mR% CfO loeai towM fluna HF OnpHid W M irigctms kyOMsHJa

RTIATEDCTWORnSiT^Lvi t f . ] FT FFrrr "Iwi k ; ^ T X x m l r b x l ^

US tuiid ]"A leads Ks 3k cr broadband co Atria buvout

I'.'o-i. ̂ xrd.-bou- 5̂ 3:: .r.lioiGxi.̂ f-: f rrn vTir r7cc-xri<-p'.-,:bca/r T i l n i r , '

fDtr.T,ir.=d2jf;,--i,-,vi "'riuf x tWifritlh •r.nnp'̂o T X T Ir!̂ "••pi i'^^ TIAPT ACT Lr: *x-:.vTCl :xs:ivpcrxi. L J I ; D,".;:i_-x]:iLiE a :.fx u "Jie E,":i;3kij(-A led cjiuTTr. Tiisi; aJ;..

ci,( K i e piT. j ; ; jquhv •j.xixipar.i iu lix,:i A ye. i

Bujt.li.jJij;.i:T*'j.xji^ Tit'klei.̂ u i x - U .LOiy]iiX'j;..\iKix j:.x...tjT.j>u"j;-.u

Rationale for selection of DCF Method: 1. Peer Companies are mainly Telecom Companies (except Hath\A/ay),their business mix and growth potential are different. 2. Wireless voice and data significantly drives the valuation of telecom companies 3. IMCL's broadband division has a low base giving it an opportunity to have a high growth period in the next couple of

years with due management focus in the business 4. Valuation using Hathway EV/EBITDA multiple is significantly higher reflecting Hathway's maturing broadband business 5. Further the recent transaction in ACT, which is purely broadband business is at a significantly higher valuation

pnsidering all these and the objective of valuation being one derived from business plan reflecting the most optimistic umption we are of the opinion that DCF is the right choice.

EV/Subscriber value of major telecom companies is ranging from Rs 4,133 to Rs 13,353

ARPU level for broadband is significantly higher than voice base revenue of telecom companies

Hathway's EV/ subscriber value is comparatively lower as the subscriber base of 11.8 Mio includes the CATV (Analogue and digital) subscribers with 450 thousand broadband subscribers

ACT is at a much higher value (Rs.30,000 per subscriber) as EV/subscriber is based on broadband subscribers only.

In IMCL - Broad band divisions's case, EV per subscriber is based on 250,000 subscribers to be added by 2020 while ACT's valuation is based on its existing subscribers. Rs.30,000 at the end of 5 years if discounted is about Rs. 15.000/-

Considering the above in our view, IMCL- Broadband division's derived EV/subscriber value of Rs 10,276 is appropriately positioned in the above scale

This Document is primarily prepared for the client based on the information provided to us by the client.

The information contained herein is from publicly available data or other sources believed to be reliable. PKF Sridhar & Santhanam LLP and its associated firms, their partners and employees are under no obligation to update or keep the information current. We do not represent that information contained herein is accurate or complete and it should not be relied upon as such. This document is prepared for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. The decision as to whether to consummate any transaction with the target lies solely with the client and our findings or other work shall not in any way constitute a recommendation as to whether the client should or should not consummate any transaction or the price or other terms upon which any transaction should be consummated. The user assumes the entire risk of any use made of this information. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved).

By accepting this document the recipient agrees that neither the document nor any of the information therein shall be disclosed by the recipient or any of the recipient's employees or representatives to any one without our prior written consent. PKF Sridhar & Santhanam LLP is a member firm of the PKF International Limited network of legally independent firms. Neither the other member firms nor PKF International Limited is responsible or accept liability for the work or advice which PKF Sridhar & Santhanam LLP provides to its client and by using this report you acknowledge and accept that such other member firms and PKF International Limited do not owe you any duty in relation to the work or advice which we will from time to time provide to you or are required to provide to you.