14

Value based Management (BCG approach) Presented by:- Avinash Ahuja (11101) Jagdish Devjani (11111)

| Date post: | 21-Apr-2015 |

| Category: |

Documents |

| Upload: | avinash-ahuja |

| View: | 265 times |

| Download: | 8 times |

Value based Management(BCG approach)

Presented by:- Avinash Ahuja (11101)

Jagdish Devjani (11111)

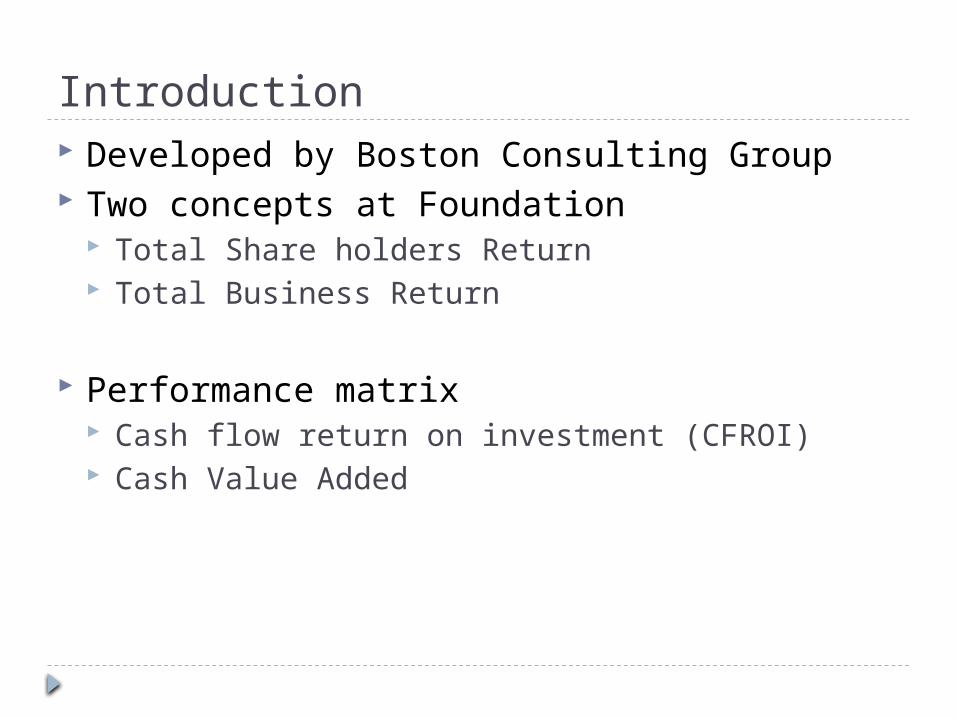

Introduction Developed by Boston Consulting Group Two concepts at Foundation

Total Share holders Return Total Business Return

Performance matrix Cash flow return on investment (CFROI) Cash Value Added

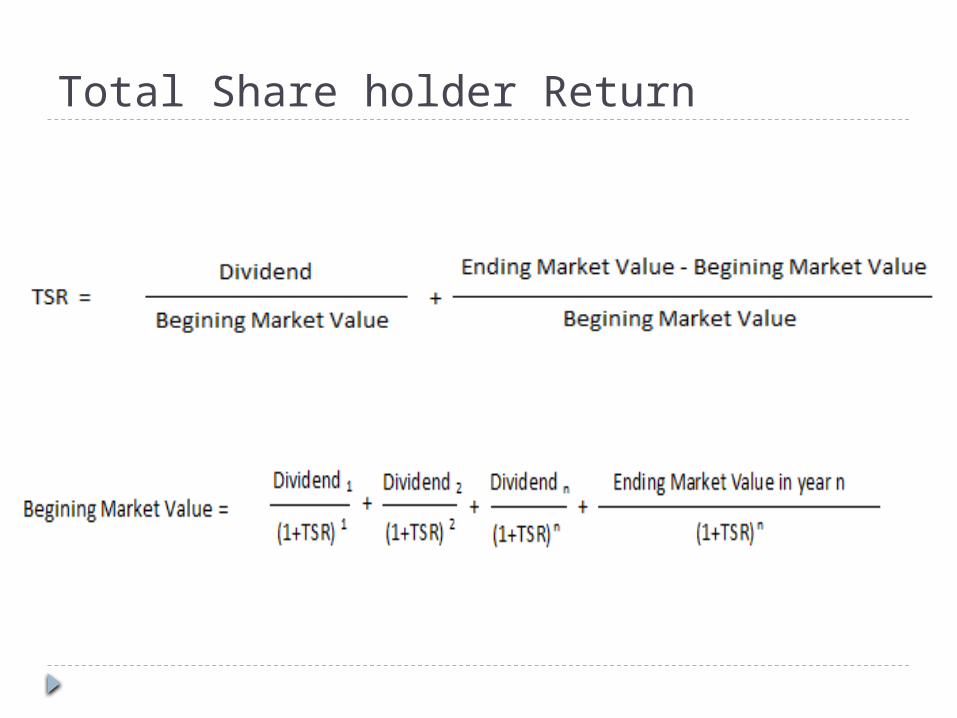

Total Share holder Return

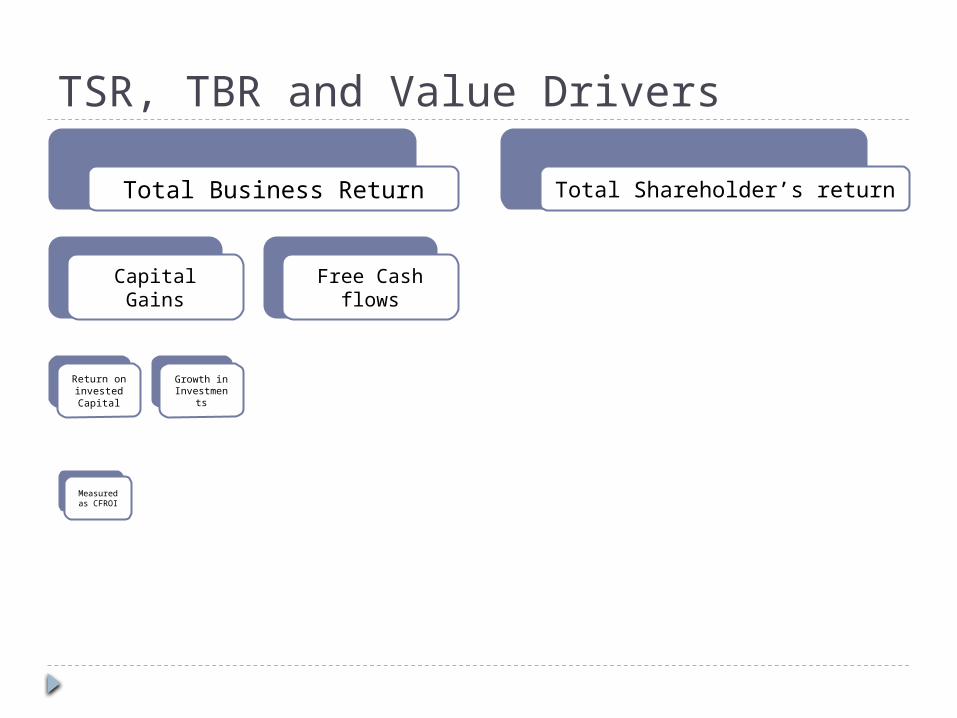

TSR, TBR and Value Drivers

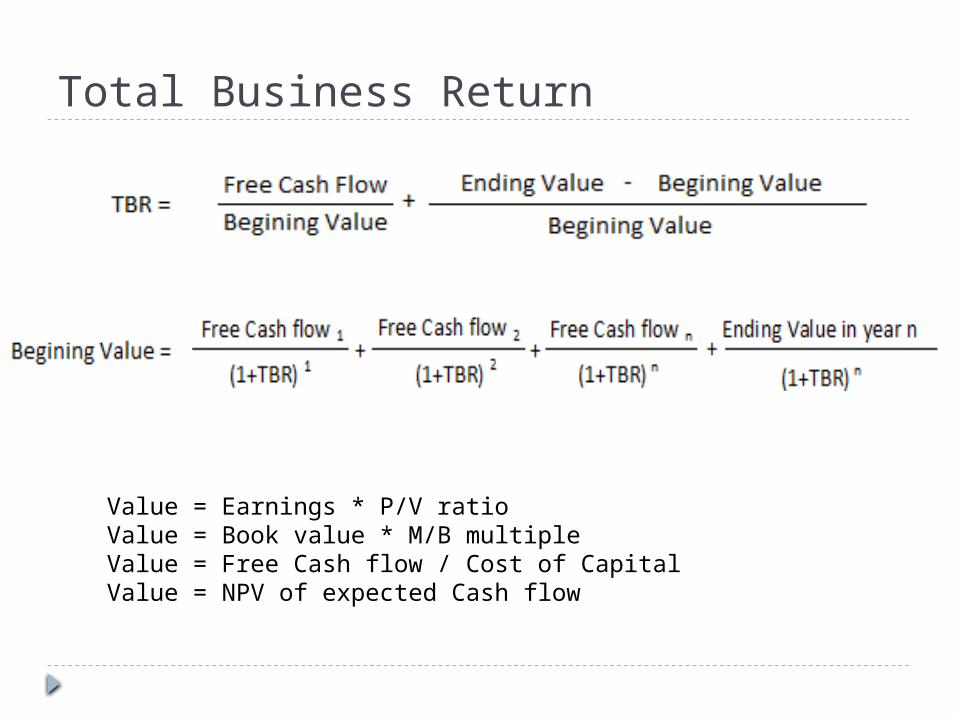

Total Business Return

Capital Gains

Return on invested Capital

Measured as CFROI

Growth in Investmen

ts

Free Cash flows

Total Shareholder’s return

Total Business Return

Value = Earnings * P/V ratioValue = Book value * M/B multipleValue = Free Cash flow / Cost of CapitalValue = NPV of expected Cash flow

Uses of TBR

Strategic Planning

Resource Allocation

Incentive Compensation

Resource Allocation Perspective

Question

High Priority for

Reinvestment

Do not Fund Question

TBR of business plan v/s target TBR

Negative 0 Positive

Positive

Negative

0Current CFROIv/sCost of Capital

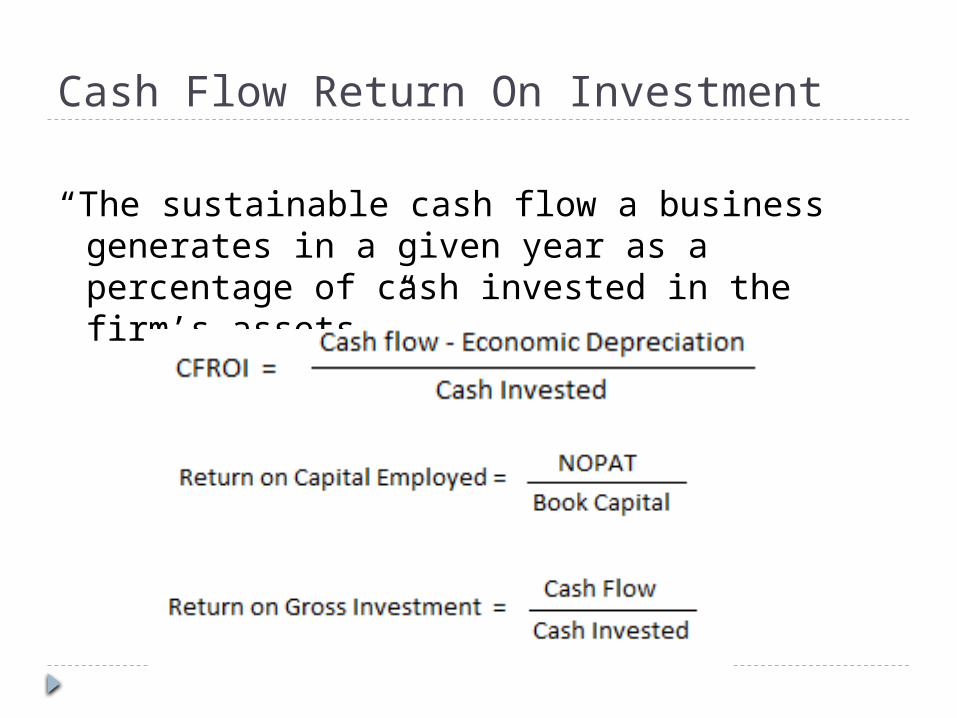

Cash Flow Return On Investment

“The sustainable cash flow a business generates in a given year as a percentage of cash invested in the firm’s assets.”

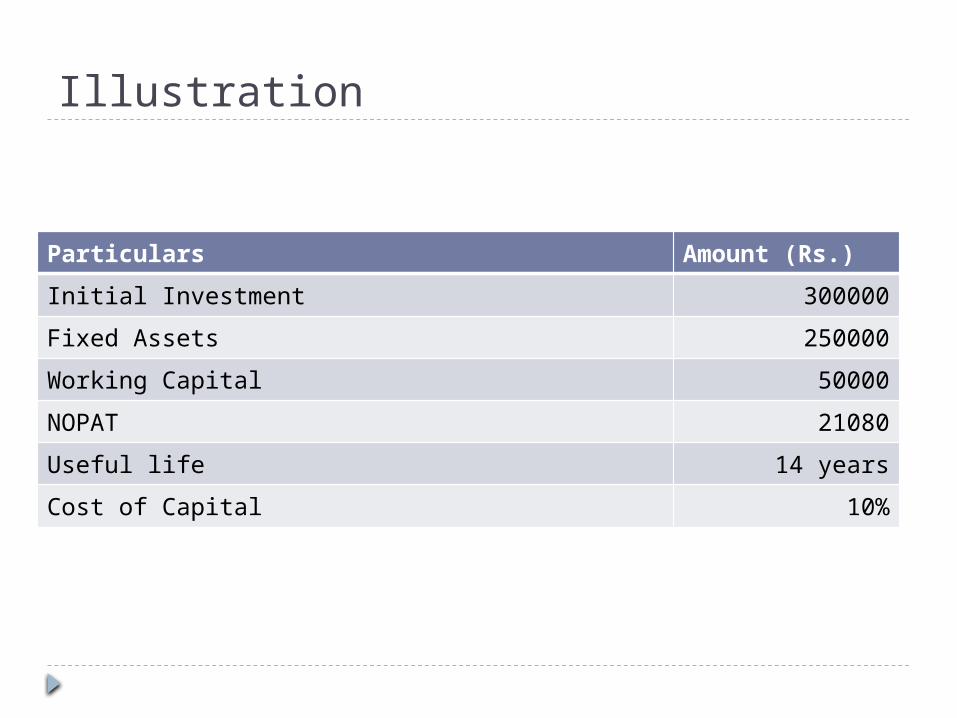

Illustration

Particulars Amount (Rs.)

Initial Investment 300000

Fixed Assets 250000

Working Capital 50000

NOPAT 21080

Useful life 14 years

Cost of Capital 10%

Annual Measurement of project

Year 1 Year 2 Year 3

NOPAT 21080 21080 21080

Depreciation 17857 17857 17857

Cash Flow 38937 38937 38937

Economic depreciation 8937 8937 8937

Sustainable Cash Flow 30000 30000 30000

Book Capital 300000 210715 103573

CFROI (%) 10.00 10.00 10.00

ROCE (%) 7.03 10.00 20.35

ROGI (%) 12.98 12.98 12.98

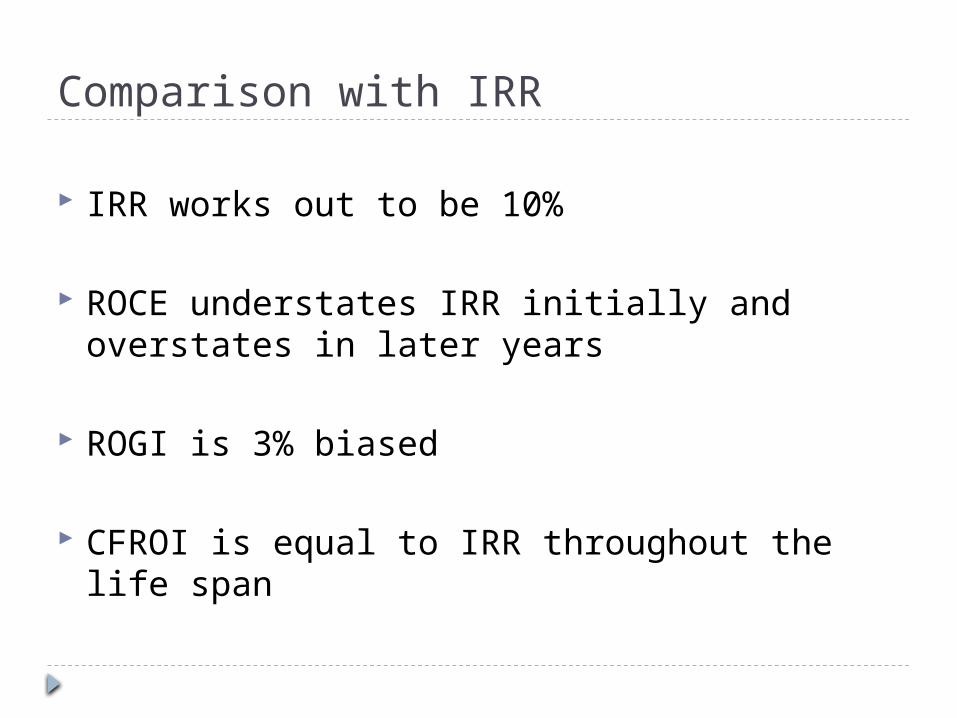

Comparison with IRR

IRR works out to be 10%

ROCE understates IRR initially and overstates in later years

ROGI is 3% biased

CFROI is equal to IRR throughout the life span

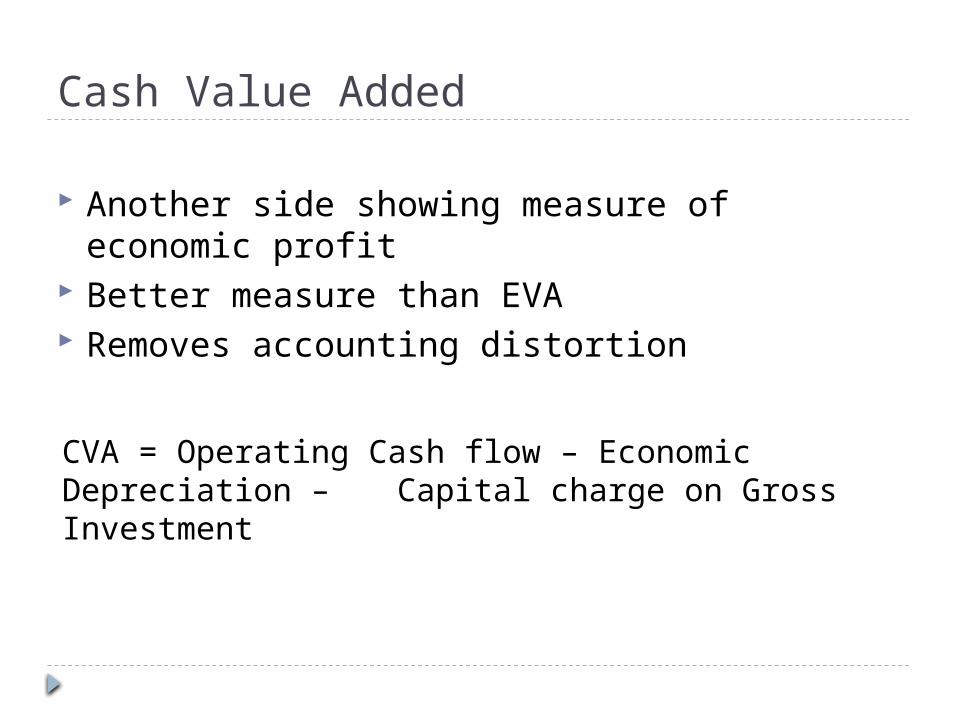

Cash Value Added

Another side showing measure of economic profit

Better measure than EVA Removes accounting distortion

CVA = Operating Cash flow – Economic Depreciation – Capital charge on Gross Investment

Comparing EVA and CVAEVA

Year 1 Year 6 Year 12

NOPAT 21080 21080 21080

Book Capital 300000 210715 103573

Capital Charge (10%) 30000 21072 10357

EVA (8920) 8 10732

CVA

NOPAT 21080 21080 21080

Depreciation 17857 17857 17857

Cash flow 38937 38937 38937

Economic Depreciation 8937 8937 8937

Cash Invested 300000 300000 300000

Cost of Capital 10% 10% 10%

Capital Charge 30000 30000 30000

CVA 0 0 0