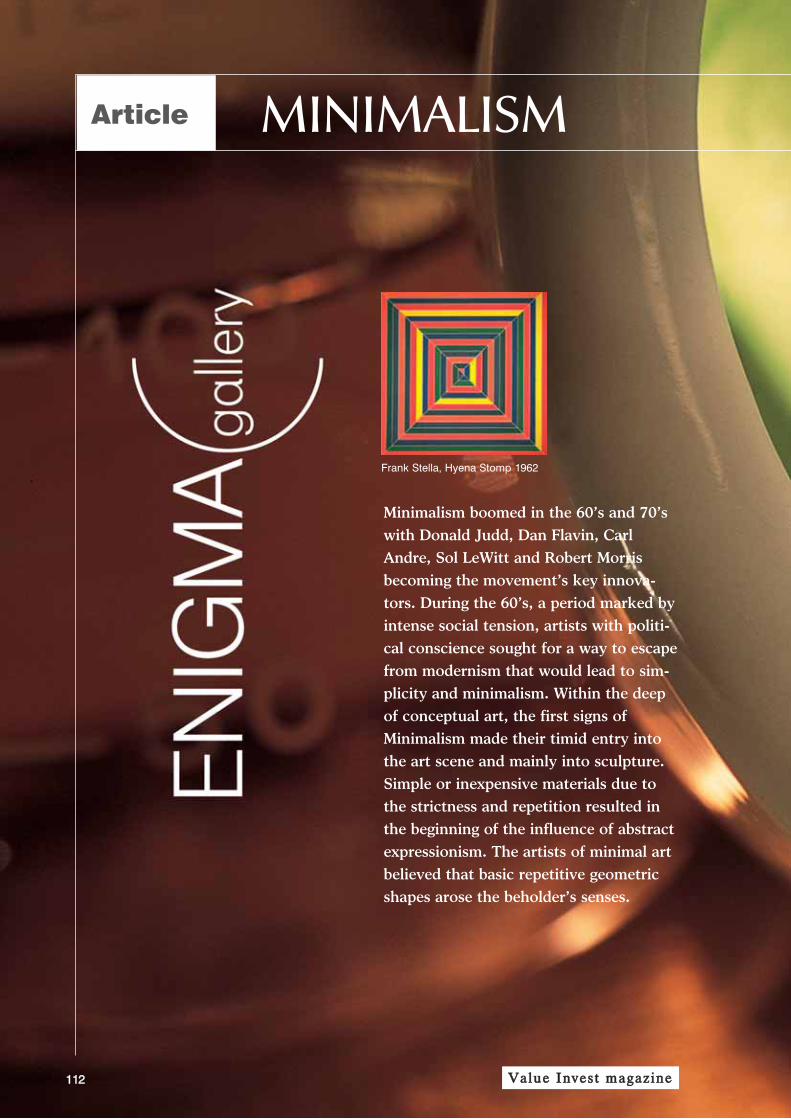

VALUE INVEST by Valuation & Research Specialists www.valueinvest.gr Issue 1, 2 nd Semester 2007 • Greek Economy & Equities • Market Risk • Real Options & Pricing of Shares • Creating an Effective IR Paradigm • Saving versus Investing • Greek M&A in Turkey • Past Oil Crises • Valuing Banking Stocks • Case Studies • The Art of Minimalism

When we started forming the Value Invest Magazine atVRS (Valuation & Research Specialists) a few monthsago, we had in mind a “new generation” magazine thatincorporates new voices and ideas destined for theinternational market of professionals in the securitiesand investment banking industry.This magazine is written and applied by practitioners.We wish to offer the readers, insights from some of ourfavorite commentators in the finance area, from boththe professional and the academic community.

As we are professionals in financial analysis andvaluation of listed and non-listed companies, withextensive insight in several businesses, our magazine’smission is also to serve our business philosophy andvision. As a result, we have put a lot of effort onpresenting a number of relevant issues and real casestudies that we believe will provide useful information,way of thinking and methodologies to the readers.In the current issue, as well as future ones, we will tryto present “fresh” financial tools and business ideasthat combine innovation and technology featuringsmall and medium sized organizations.

Here at Value Invest Magazine, we have made aconcerted effort to deliver more valuableinformation to readers like you.

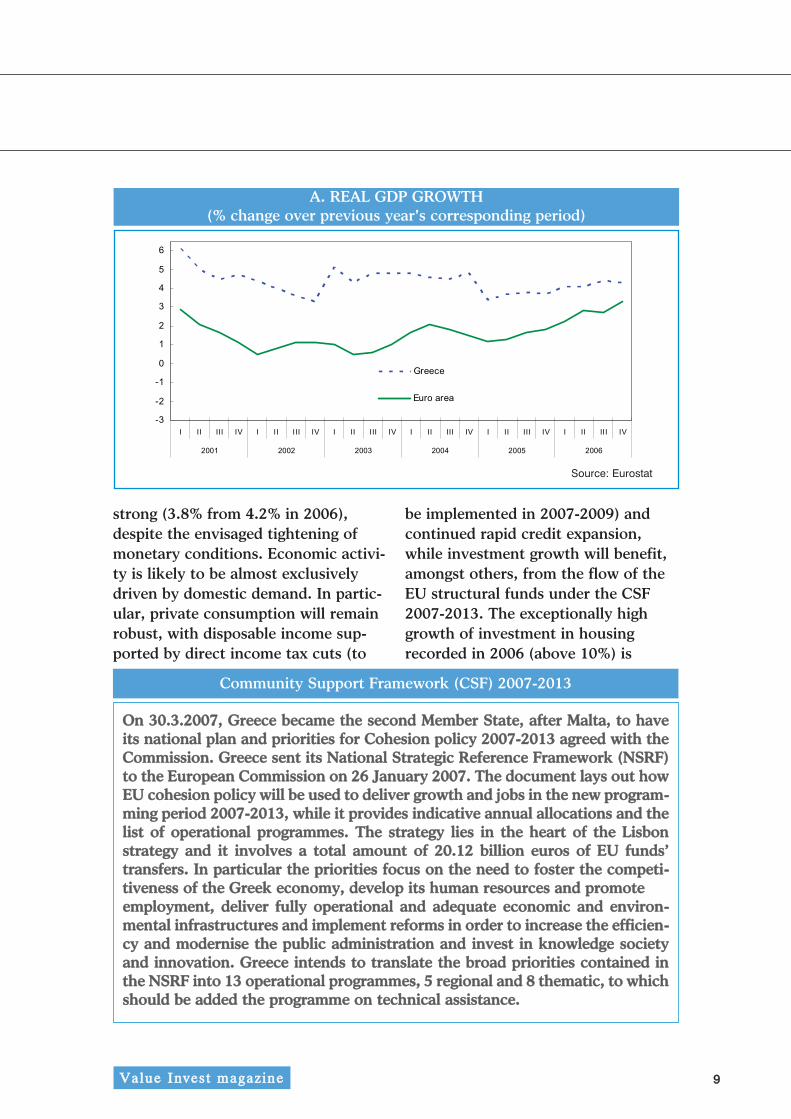

The Greek economy continued toexpand at a buoyant rate, recording areal GDP growth of 4.3% y-o-y in Q42006 and of 4.2% in 2006 as a whole,despite the high and volatile energyprices and the tightening of the fiscaland the monetary policy. This annualrate of growth was significantly higherthan the respective rate of 2.6% of theeuro area and 3.2% of the EU-27,placing Greece amongst the fastestgrowing advanced economies inEurope. The main factors that havesupported the strong and continuousgrowth over the last decade (4.1%period average), i.e. the high rates ofprivate consumption and investmentgrowth, are still in effect. Indeed, pri-vate consumption grew by 3.4% in2006, underpinned by rising real dis-posable income -which grew roughlyby 4.0% in 2006 compared to 2.0% in2005-, increasing household wealth,due to the rising market value of realestate property, and continued rapidcredit expansion. In the same vein,gross fixed capital formation increasedby 6.3% in 2006, driven mainly bystrong corporate investment and pri-vate investment in the housing sector.

The improved profitability of the busi-ness sector, supported by robustdomestic and foreign demand, coupledwith the favourable lending conditionsand the considerable investmentincentives within the framework ofthe Investment Law (in effect sinceMarch 2005) have resulted in accelera-tion of corporate investment by 6 to8% in 2006. On the other hand, theannual contribution of net exports toGDP growth continued to be negative.Consistent with sustained growth, inQ4 2006 unemployment fell sharply to8.8% (from 9.7% in Q4 2005), whileemployment further increased.Looking forward, growth is projectedto decelerate in 2007, but remain

DYNAMIC SECURITIESVALUATION & RESEARCH SPECIALISTS

VVaalluuee IInnvveesstt mmaaggaazziinnee

Greek Economy & EquitiesQuarterly Review, April 2007

99

strong (3.8% from 4.2% in 2006),despite the envisaged tightening ofmonetary conditions. Economic activi-ty is likely to be almost exclusivelydriven by domestic demand. In partic-ular, private consumption will remainrobust, with disposable income sup-ported by direct income tax cuts (to

be implemented in 2007-2009) andcontinued rapid credit expansion,while investment growth will benefit,amongst others, from the flow of theEU structural funds under the CSF2007-2013. The exceptionally highgrowth of investment in housingrecorded in 2006 (above 10%) is

Α. REAL GDP GROWTH(% change over previous year's corresponding period)

Source: Eurostat

1100

expected to ease somewhat in 2007, asthe stock of available houses hasincreased along with the households’mortgage repayment burden, due tothe interest rates rise. Exports’ volumeof goods and services is likely toincrease as well, due to the sustainedgrowth of the international economyand trade. The annual unemploymentrate is projected to drop towards8.3%, the lowest of the last decade.The Greek authorities revised upwardsthe level of GDP by 25.7% in 2006.The Greek Statistical Office hasexplained that this major revision is,amongst others, the result ofimproved measurement of the fast-growing services sector. The revisedGDP figures are currently being exam-ined thoroughly by Eurostat, so thefinal approval should not be expectedearlier than autumn 2007.Turning to price developments, thefall in oil prices has had a sizeableeffect on headline inflation sinceSeptember 2006, while indirect tax

increases and secondary effects fromhigh energy prices and high unitlabour cost growth have resulted inrelative high core inflation (i.e. head-line inflation excluding fresh food andenergy prices). Headline inflation fellto 3.2% in 2006 (from 3.5% in 2005) -and is expected to continue its down-ward trend in 2007, but remain elevat-ed (2.9%) - while core inflationreached 2.7%. Given the favourableeconomic environment, monetary pol-icy continues to be on the accom-modative side, with the key ECB inter-est rates moderate, money and creditgrowth vigorous, and liquidity in theeuro area as a whole ample. However,as upside risks on the demand sideremain, the ECB raised once again itspolicy rate on 14 March 2007 by 25basis points to 3.75%.The implementation of the 2006 budg-et may be considered as satisfactorywith current revenues growing at ratesof 10.4% in 2006 from 5.6% in 2005,considerably above the rate of nomi-

Dynamic Securities - Valuation & Research Specialists

VVaalluuee IInnvveesstt mmaaggaazziinnee

Β. INFLATION RATE(% change over previous year's corresponding period)

1111VVaalluuee IInnvveesstt mmaaggaazziinnee

C. Greece: International Trade

Source: Greek Statistical Office.

nal GDP growth (7.8%), aided by therecovery of VAT revenues and, to alesser extent, the increased settlementrates of overdue tax liabilities. Thereis still room, however, for the govern-ment to cash in larger part of the sub-stantial amount of overdue tax liabili-ties, which have ballooned during thepast few years. The negative effect onthe fiscal revenues from the reductionof corporate tax rate from 32% in2005 to 29% in 2006 was partly offsetby some indirect tax increases ontobacco, mobile phones and gasolinein July 2006, the introduction of VATon real estate transactions and somelump sum revenues, such as the 315million euros from the taxation ofcommercial banks’ reserves. Primaryexpenditure decelerated significantlyto 3.7% in 2006, from the substantial-ly elevated levels in 2004-2005, whilethe deficit of the public investmentbudget has been retained to 2.3% of

GDP, due to increased flows of EUfunds and reduced public investmentexpenditure. Overall, the general gov-ernment deficit fell substantially to2.6% of GDP in 2006 from 5.5% ofGDP in 2005 and 7.9% of GDP in2004, as recently confirmed byEurostat. In structural terms, theadjustment has been expenditure-driv-en, but also several measures intro-duced in order to tackle tax fraud andevasion, like the improvement of taxadministration, combined with thebroadening of tax bases have raisedthe level of revenues. According to theEuropean Commission’s estimates,Greek fiscal deficit will remain in 2007below the Maastricht Treaty’s 3% ofGDP limit, increasing thus the likeli-hood of Greece soon exiting from theExcessive Deficit Procedure. The long-term consolidation and sustainabilityof public finances, however, will notbe possible without wide-range

1122

reforms of the pension and health caresystems.On the external front, despite the rela-tive strong growth of exports of goods(13.8%) and of tourist receipts (4.8%),the current account deficit furtherworsened to 12.1% of GDP in 2006, asimports of goods accelerated to23.2%, mainly due to increased oiland shipping payments [Note 1] androbust private consumption. RecentBoG data indicate that in January-February 2007, the current accountdeficit widened by 41,136 million overthe same period of 2006 and reached45,913 million, reflecting mainly ahike in the trade deficit. In the sameperiod, direct investment showed anet outflow of 41,901 million (com-pared with a net inflow of 4364 mil-lion in the same period of 2006).Overall, developments in the balanceof payments indicate that the highgrowth of domestic demand and thecontinuous worsening of competitive-ness with respect to unit labour costsare the cause of the rapid deteriora-tion of the current account balance. Infact, real effective exchange rate hasappreciated by 20-30% on a unitlabour cost basis and by 10% on a CPIbasis since EMU accession [Note 2].In the same vein, conjectural indica-tors point to continuing robust growthin domestic demand. According to thelatest figures, the turnover in retailtrade recorded a rise by 14.7% at cur-rent prices in December 2006 as com-pared to December 2005, while thevolume of retail trade (i.e. turnover in

retail trade at constant prices)increased by 10.5% in the respectiveperiod. The increase derived mainlyfrom furniture, electrical equipment,household equipment, clothes andfootwear sales.Several of the large global retailerswho have recently entered the marketare already expanding rapidly acrossthe country, attempting to gain mar-ket share through highly competitiveoffers, boosting durable goods sales.Growth in manufacturing productionrose by 1.4% in 2006, despite the con-tinuing substantial decline in the pro-duction of textiles and clothing as aresult of international competitionthat affects both Greece’s domesticmarket and its main trading partners.Amongst the main industrial group-ings, of particular importance was theproduction increase in capital goodsand consumer durables. Business con-fidence as measured by the PMI indexmoved above the neutral 50 mark inJanuary 2007 to 51.8, after havingfallen to 49.9 in December. The vol-ume of residential construction activi-ty (as measured by building permits)

Dynamic Securities - Valuation & Research Specialists

VVaalluuee IInnvveesstt mmaaggaazziinnee

1133

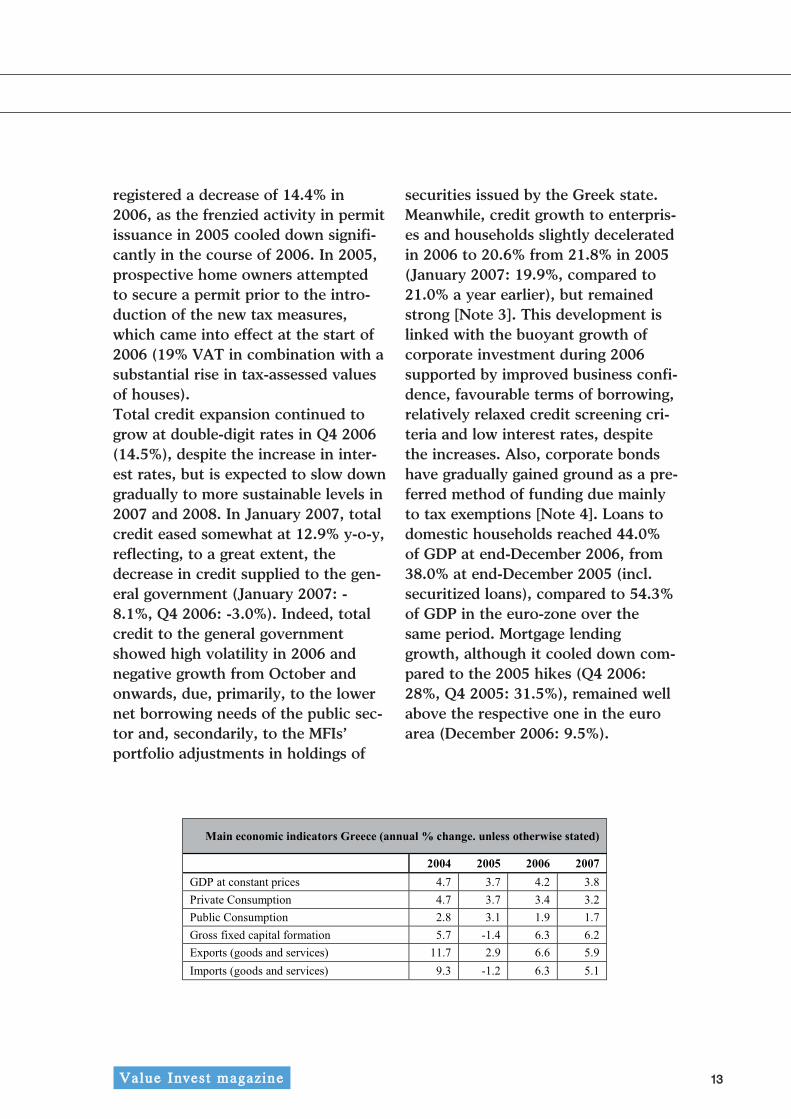

registered a decrease of 14.4% in2006, as the frenzied activity in permitissuance in 2005 cooled down signifi-cantly in the course of 2006. In 2005,prospective home owners attemptedto secure a permit prior to the intro-duction of the new tax measures,which came into effect at the start of2006 (19% VAT in combination with asubstantial rise in tax-assessed valuesof houses).Total credit expansion continued togrow at double-digit rates in Q4 2006(14.5%), despite the increase in inter-est rates, but is expected to slow downgradually to more sustainable levels in2007 and 2008. In January 2007, totalcredit eased somewhat at 12.9% y-o-y,reflecting, to a great extent, thedecrease in credit supplied to the gen-eral government (January 2007: -8.1%, Q4 2006: -3.0%). Indeed, totalcredit to the general governmentshowed high volatility in 2006 andnegative growth from October andonwards, due, primarily, to the lowernet borrowing needs of the public sec-tor and, secondarily, to the MFIs’portfolio adjustments in holdings of

securities issued by the Greek state.Meanwhile, credit growth to enterpris-es and households slightly deceleratedin 2006 to 20.6% from 21.8% in 2005(January 2007: 19.9%, compared to21.0% a year earlier), but remainedstrong [Note 3]. This development islinked with the buoyant growth ofcorporate investment during 2006supported by improved business confi-dence, favourable terms of borrowing,relatively relaxed credit screening cri-teria and low interest rates, despitethe increases. Also, corporate bondshave gradually gained ground as a pre-ferred method of funding due mainlyto tax exemptions [Note 4]. Loans todomestic households reached 44.0%of GDP at end-December 2006, from38.0% at end-December 2005 (incl.securitized loans), compared to 54.3%of GDP in the euro-zone over thesame period. Mortgage lendinggrowth, although it cooled down com-pared to the 2005 hikes (Q4 2006:28%, Q4 2005: 31.5%), remained wellabove the respective one in the euroarea (December 2006: 9.5%).

VVaalluuee IInnvveesstt mmaaggaazziinnee

1144

Dynamic Securities - Valuation & Research Specialists

VVaalluuee IInnvveesstt mmaaggaazziinnee

Sources: IMF, European Commission, Bank of Greece, OECD, Ministry of Finance

1155

BBuullggaarriiaa::Bulgaria’s economy expanded by 6.2%in 2006 (compared to 5.5% in 2005)and is projected to achieve the samelevel of growth in 2007. Despite therestrictive measures undertaken torestraint credit expansion and the risein consumer prices, private consump-tion expanded, as well as investment,which had only marginally slowed inH2 2006. The economy currentlyenjoys large capital inflows, which areprojected to increase further in thefollowing years, benefiting from EUaccession and transfers and theannounced cut of the corporate taxrate from its current level of 15% to10% in 2007. Developments in theexport market improved, but growthof imports’ outpaced that of exports,resulting in further deterioration ofthe current account deficit to 15.9%of GDP in 2006 from 11.3% of GDP in

2005. Although these deficits havebeen largely financed by inflows offoreign direct investment in recentyears, they are associated with strongdomestic demand growth and repre-sent an important challenge for theauthorities. Inflation, as measured bythe CPI, increased to 7.3% in 2006(from 5.0% in 2005), mainly due to ahike of excise duties, as a result of taxharmonization with the EU, and highinternational energy prices. CPI infla-tion is forecasted to decrease at 5.3%in 2007. Unemployment fell in 2006for the first time in recent years toone-digit figure (9.0%) and is expectedto continue its downward trend.Turning to fiscal policy, the govern-ment, mimicking developments in itsneighbour and accession partnerRomania, approved a future reductionof the budget surplus, which exceededthe target budget surplus of 3% in

VVaalluuee IInnvveesstt mmaaggaazziinnee

Note on South-eastern Europe (Bulgaria, Romania, Albania,FYROM, Serbia and Montenegro) and Mediterranean countries(Turkey, Egypt)

2006, to 0.8% of GDP in 2007 and0.6% in 2008, on the basis of neededEU accession-related infrastructureinvestments. Government also plansto enter the Exchange RateMechanism- 2 (ERM-II) around spring2007 with the aim to adopt euro by2012.

RRoommaanniiaa::Economic activity in 2006 bouncedback strongly to 7.7%, after the slow-down to 4.1% in 2005, driven by abroad-based recovery in industrialactivity, construction and agriculture.Particularly in Romania, total outputis generated to a relatively largedegree in agriculture (14.3%) andindustry (36.8%, including construc-tion), compared with 1.9% and 26.2%respectively in the EU-25. Since thestart of the transition process towardsa market economy, however, a pro-found structural reorientation hastaken place from agriculture andindustry towards services. Domesticdemand, fostered by rapid privateconsumption and investment growth,has been the main engine of growth inthe post-flooding reconstruction peri-od. Net exports remained a drag onthe economy with imports growingalmost twice as fast as exports.Despite the growth in export volumes,after the slump in 2005 due to theremoval of trade and textile quotas onChinese imports, the current accountdeficit widened considerably in 2006to 10.3% of GDP. CPI Inflation fell to6.6% in 2006 (from 9.0% in 2005), as

a result of lower oil and food pricesand the appreciation of the Leu (7% vsthe euro and 16% vs the dollar).Unemployment increased only moder-ately to 7.4% in 2006 (from 7.2% in2005) and is foreseen to remain broad-ly stable. The fiscal authorities ran ageneral government budget deficit of1.7% of GDP in 2006, targeting adeficit of 2.8% in 2007 as a result ofthe EU-accession related expenditureneeds. The Romanian government hasset as target date for entry in the euroarea the year 2014, in order to securethat all necessary preparations willhave been completed till then.

AAllbbaanniiaa::Albania's macroeconomic perform-ance has remained strong. Inflation islow, the external position hasimproved, and economic growth wasrobust, although real GDP decreasedto 5.0% in 2006 from 5.5% in 2005.Economic expansion has continued tobe driven by private consumption andinvestment, based on rapid householdcredit expansion and strong remit-tance inflows. Although activity inconstruction slowed down—in partowing to a sharp reduction in thenumber of construction permits anddelays in the execution of publicinvestment—a faster-than-anticipatedrecovery in electricity production andan improvement of exports served asmitigating factors. Inflation over thepast year has generally been close tothe Bank of Albania’s lower boundaryof the 2-4% target range, while the

Dynamic Securities - Valuation & Research Specialists

VVaalluuee IInnvveesstt mmaaggaazziinnee

1177

current account deficit decreased to5.9% from 6.5% in 2005, as traditionalexports such as footwear recoveredand new export opportunitiesemerged. These favourable develop-ments owe much to sound macroeco-nomic policies and continued strongcommitment to program implementa-tion, but maintaining these gainsalongside further reduction in povertyrequires additional growth-enhancingstructural reforms. The authorities arecommitted to fiscal discipline, and areimplementing a fiscal program thataims to reduce public debt while pro-viding adequate funding for priorityprojects in infrastructure, health, andeducation. The recent measures takenby the Bank of Albania to strengthenthe regulatory and prudential frame-works will further reduce the risksposed by rapid credit growth. In theenergy sector, the InternationalFinance Corporation has been selectedas an advisor for the privatization ofthe distribution arm of the nationalelectricity company (KESH).Concerted efforts are needed toensure stable energy supply and fur-ther improve the financial perform-ance of KESH.

FFYYRROOMM::Economic growth slightly acceleratedin 2006 to 4.0% from 3.8% in 2005and is expected reach 4.5% in 2007.Economic expansion is driven by pri-vate consumption and investmentsupported by improved confidence,increasing real disposable income and

rapid credit expansion, benefitingfrom the country’s candidate statusfor EU membership. Export activitystill remains weak, but workers remit-tances form a significant part of theprivate transfers’ inflow. These havehelped to reduce the current accountdeficit from 7.7% of GDP in 2004 to1.3% of GDP in 2005. In 2006, thecurrent account balance turned posi-tive (0.5%). Inflation picked up to3.2% in 2006 from 0.5% in 2005,reflecting higher transport prices, dueto elevated energy prices, and largeincreases in excise taxes on tobaccoand beverages, as a result of EU har-monization policies. The currency pegand the very tight fiscal policies, part-ly contained the inflationary pres-sures, but their effect was limited.Unemployment remained excessivelyhigh at 36.1% by mid-2006. The pub-lic finances continued to remain closeto balance, but future efforts shouldfocus on improving tax administrationand containing upward wage pres-sures.

SSeerrbbiiaa::Economic activity decreased at 5.4%in 2006 (from 6.2% in 2005), but stillremains on positive track supportedby continued credit expansion and ris-ing wages. Inflation despite its sharpdrop at 12.7% in 2006 from 17.3% in2005 still remains high, while the cur-rent account deficit dramaticallywidened to 12.3% of GDP in 2006from 9.5% of GDP in 2005, despiteenhanced export activity, strong

VVaalluuee IInnvveesstt mmaaggaazziinnee

1188

Dynamic Securities - Valuation & Research Specialists

VVaalluuee IInnvveesstt mmaaggaazziinnee

remittances and privatization-orientedFDI inflows. The high inflation andcurrent account deficits need to bebrought under control without damag-ing the real economy through anappropriate mix of policies. TheNational Bank of Serbia (NBS) under-took a policy shift in 2006, opting forgreater exchange rate flexibilitythrough a new focus on inflation tar-geting. The NBS reduced the key poli-cy rate to 11.5% in February 2007(from 18% in September 2006), butthere seems to be no room for anexpansionary monetary policy, giventhe current high inflation rate. TheIMF noted recently that governmentneeds to proceed with tax and pensionsystem reform, as well as the privati-zation of state owned monopolies.Political uncertainties, especially con-cerning the future of Kosovo and howto resume association talks with theEU (suspended in May 2006) remainin the spotlight. Since the generalelections on 21 January 2007, therehas been no official governmentformed, but only an interim one.

MMoonntteenneeggrroo::Real GDP grew by 5.5% in 2006,recording the strongest performancesince the start of transition. Consumerprices increased to 3.5% from 2.6% in2005, but still compared to the hyper-inflation of the past years (2000:97.1%), inflationary pressures appearto be well contained. The fiscal andcurrent account deficits continued

their declining trend. Severe unem-ployment remains a key political andeconomic problem for this entireregion. Montenegro is in a similar situ-ation to other transition countriesthat attempt fundamental reforms.The reform process initially generateshardship and pressures on the budget.A stable currency and a balancedbudget are only first steps towards theestablishment of a market economy.Currently, the government is alsolaunching further comprehensivereforms, including the judicial system,education, public sector, and privati-sation of the remaining state ownedenterprises. There have already beensome important privatizations (alu-minium complex KAP and financialsector), as well as significant inflowsof foreign investments that are expect-ed to enhance private sector ledgrowth. This especially relates to serv-ice sectors (tourism, trade and trans-port) which have great potential. On18 January 2007, Montenegro joinedthe World Bank and IMF. Montenegrois also pursuing membership in theWorld Trade Organization and is nego-tiating a Stabilization and Associationagreement with the European Unionin anticipation of eventual member-ship.

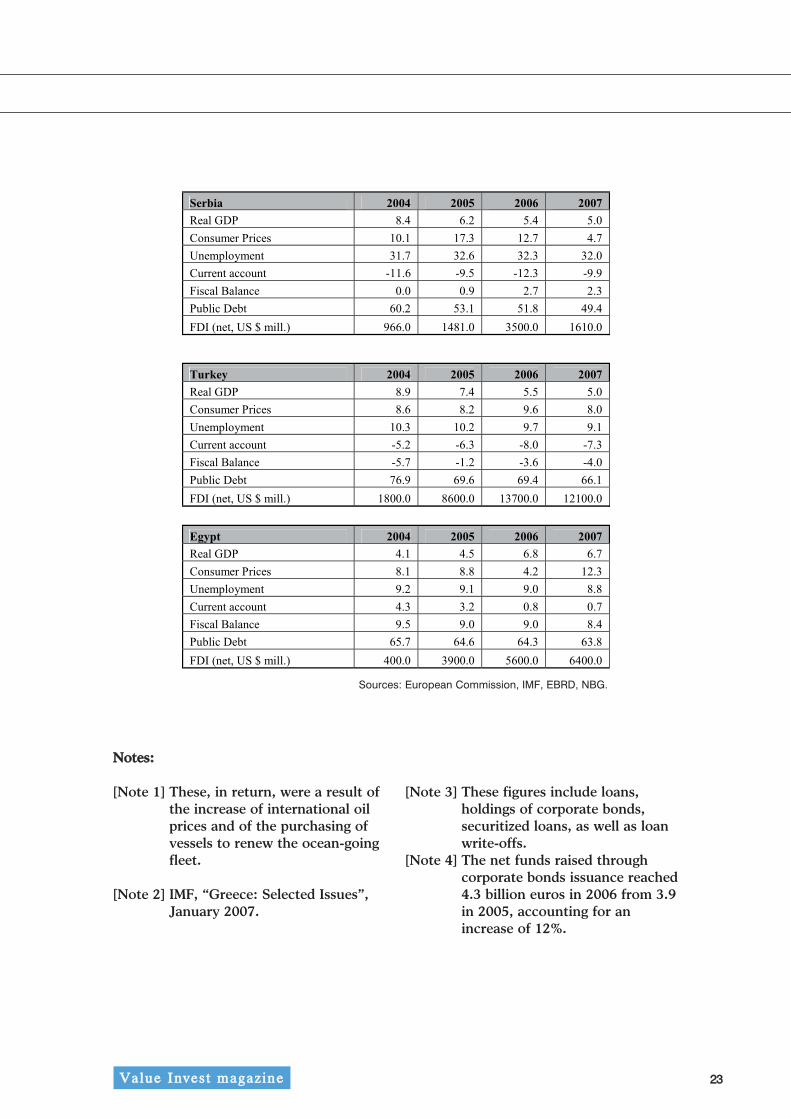

TTuurrkkeeyy::In Turkey, concerns about the widen-ing current account deficit led tosharp downward pressure on the liraduring the May-June 2006 emerging

1199VVaalluuee IInnvveesstt mmaaggaazziinnee

market correction, triggering anabrupt tightening of monetary policy.Growth has subsequently deceleratedsignificantly from 7.4% in 2005 to5.5%. Domestic demand continued toslow down in response to rapid inter-est rate increases (by 425 bps) and isexpected to contract further, loweringGDP growth forecast to 5.0% in 2007.The most worrying development hasbeen the dramatic increase in inflationto 9.6% in 2006 (year’s target: 5%)from 8.2% in 2005, reflecting in largepart the high oil prices and the depre-ciation of the Turkish lira vis-à-vis theeuro and the dollar, estimated to be asmuch as 30%, but inflation is expectedto fall to 8.0% in 2007. The exchangerate pass-through to inflation is highand a source of future concern, as itmakes the Turkish economy vulnera-ble to external shocks. Unemploymentrecorded a small fall to below 10.0%,while the public finances worsened.The general government deficitexceeded 4.0% of GDP, affected byexcessive public sector wage increasesand contraction of GDP growth, andis projected to be even higher in 2007due to expected increased publicspending prior to the presidential andparliamentary elections. Currentaccount deficit has deteriorated in2006 to 8.0% of GDP, the highest levelin recent years, reflecting strongdomestic demand and import growth.Nevertheless, it is expected to befinanced relatively easy through pri-vate debt and FDI, although the levelof risk aversion of portfolio investors

towards the emerging markets hasincreased globally. Turkey continuesto be oriented towards future EUmembership, but no comprehensibleefforts have been initiated yet.

EEggyypptt::GDP growth has gathered additionalmomentum in 2006 (6.8% from 4.5%in 2005) and is projected to remain atthe same level in 2007. Surprisingly,inflation has considerably cooleddown to 4.2% in 2006 from 8.8% in2005, perhaps as a result of the timelyand appropriate tightening of mone-tary policy by the Central Bank ofEgypt, but is forecasted to pick upagain to double-digit rates (12.3% in2007). The current account balancehas remained in surplus (0.9% in2006). Overall, the Egyptian reformslaunched in 2004 appear to havefocused well on the most critical con-straints—reducing red tape and taxrates, and improving access to foreignexchange—thereby getting a stronggrowth response out of a limited set ofreforms. However, inefficient bureau-cracy remains an important obstacleto higher growth and reforms in thisarea should continue to have highpayoffs. Ongoing reforms are alsoaddressing constraints that are likelyto become binding soon (or havebecome so already), such as inefficientfinancial intermediation and high pub-lic debt. Improvements in educationmay rapidly become a critical factorfor sustaining higher growth.

With so many MBA programmes on offer, your choice of school is crucial. An MBA from the University of Strathclyde's Graduate School of Business, a constituentpart of the Strathclyde Business School faculty, is the best investment you can make in your career as a professional manager. Strathclyde’s international reputation,combined with its high academic and selection standards, is your guarantee that your MBA will retain its value in the years to come.The Strathclyde MBA has been available outside the UK since 1988. Over 2000 course participants have now graduated, and over 1500 are currently studying theprogramme in their own country. This success is due to the unique delivery structure developed with the local partner incorporating elements of full-time, part-timeand open learning modes of study.The programme has been available in Greece since 1996, and is run in partnership with International Management Studies (IMS).

IIMMSS –– GGrreeeeccee CCeennttrreeInternational Management Studies was set up in Greece by a team of British management education specialists to provide high quality management development pro-grammes to experienced and talented professionals. IMS runs a wide range of business seminars for both companies and individuals and offers a number of Britishpostgraduate management degrees, including the MSc in Finance and the MSc in Marketing with the University of Strathclyde.Located at 85 Dinokratous in Kolonaki, IMS houses seminar rooms, a computer network and a management education library. Locally appointed tutors combineexcellent academic qualifications with solid professional experience.International Management Studies is responsible for promoting the MBA in Greece, handling enquiries, providing information and receiving applications. In order tomaintain high standards of consistency throughout the world, all admissions decisions are made by the University of Strathclyde. IMS provides local administrativeservices as well as holding counselling sessions, seminars and examinations. USGSB provides core teaching materials and sends Strathclyde University faculty membersto Greece to run intensive seminars. IMS also has a number of local management education specialists who provide ongoing counselling support. All assessment is theresponsibility of Strathclyde and successful participants will be awarded a University of Strathclyde Master of Business Administration.

22 MMeetthhooddss ooff ssttuuddyyThe Strathclyde University MBA in Greece incorporates a flexible style of delivery – full-time, part-time and open learning elements in a 180 credit format. Many par-ticipants continue to work while taking the course over two years. This makes the programme a viable and valuable alternative for the busy professional and his com-pany since it combines the benefits of learning with immediate practical application to his working environment.

HHooww ddooeess tthhee pprrooggrraammmmee wwoorrkk??Each year is divided into two six-month semesters. For the first four months participants will study core learning materials and attend local counselling sessions.Strathclyde staff then come to Athens to run intensive seminars. Examinations are held in the sixth month.These intensive seminars ensure that all MBA students have the same learning experience and reach the same standards. They also enable Strathclyde staff to modifytheir teaching so that it is relevant to the contexts in which the course participants are working. The intensive seminars are mainly based around the core learningelements, but also cover business simulations and management skills i.e. the development of managerial competence. This flexibility allows busy executives to gain afirst class international MBA in their own country, without interrupting their careers.

AAccccrreeddiittaattiioonnAccreditation is a good guide to how a business school is regarded by its peers. This year has seen the business school gain full international accreditation, with allthree accrediting bodies around the world - EQUIS (Europe), AMBA (International MBA quality assurance) and AACSB (North America) – approving the school asoffering excellent management education.As one of only 23 business schools in the world with this standing, and the only business school in Scotland to be accredited so highly, Strathclyde continues to leadthe way in high quality business education. We also hold excellent ratings for both our research and the quality of our teaching.

AAMMBBAA ((TThhee AAssssoocciiaattiioonn ooff MMBBAAss))All Strathclyde MBA programmes are accredited by AMBA and all students are eligible to join after enrolment on an MBA course. www.mba.org.uk

EEQQUUIISS ((EEuurrooppeeaann FFoouunnddaattiioonn ffoorr MMaannaaggeemmeenntt DDeevveellooppmmeenntt))Strathclyde is one of only 16 UK business schools to receive EQUIS accreditation. www.efmd.be

AAAACCSSBB ((TThhee AAssssoocciiaattiioonn ttoo AAddvvaannccee CCoolllleeggiiaattee SScchhoooollss ooff BBuussiinneessss))Strathclyde received accreditiaton from this prestigious body in December 2003. www.aacsb.edu

While offered in partnership with IMS, responsibility for academic quality control resides with Strathclyde, and is the same as for the United Kingdom programmes.Successful MBA students (via international centres) will be awarded the same Strathclyde University MBA as all UK students and will be invited to attend the gradua-tion ceremony held annually at Strathclyde University, Glasgow.

CCoouurrssee DDuurraattiioonnThe Strathclyde MBA (part-time via international centres) has been specially designed for busy executives who need to combine career and family commitments withthe demands of MBA studies. This flexibility enables students to graduate within two years. However, studies may be spread over a longer period to a maximum ofsix years. Subject to availability, those students wishing to accelerate their studies may be able to join the full-time MBA programme at Strathclyde University inGlasgow at the elective stage during June and July each year. This enables them to complete their electives within a shorter period as well as experience working withparticipants from all over the world.

IInnttaakkee ddaatteessThere are two intakes for the Strathclyde MBA in Greece each year – in April and October. Finalised course dates and timetables are available from IMS.

AApppplliiccaattiioonnssEntry requirements are a good first degree, proficiency in English and several years' work experience (a minimum of 3 years is mandatory). Candidates who do nothold the normal requirements but are clearly of MBA potential may be offered entry to the MBA via the Diploma route. Visit the Graduate School of Business (www.worldclassmba.com) website for detailed information about the programme such as the syllabus and reputation of theStrathclyde MBA. Contact International Management Studies to request a brochure or to arrange an appointment at which you can discuss whether the MBA is suitable for you andwhether it meets your career needs.

[Note 3] These figures include loans,holdings of corporate bonds,securitized loans, as well as loanwrite-offs.

[Note 4] The net funds raised throughcorporate bonds issuance reached4.3 billion euros in 2006 from 3.9in 2005, accounting for anincrease of 12%.

2244

Dynamic Securities - Valuation & Research Specialists

VVaalluuee IInnvveesstt mmaaggaazziinnee

The Greek Equity Market in the First Quarter 2007

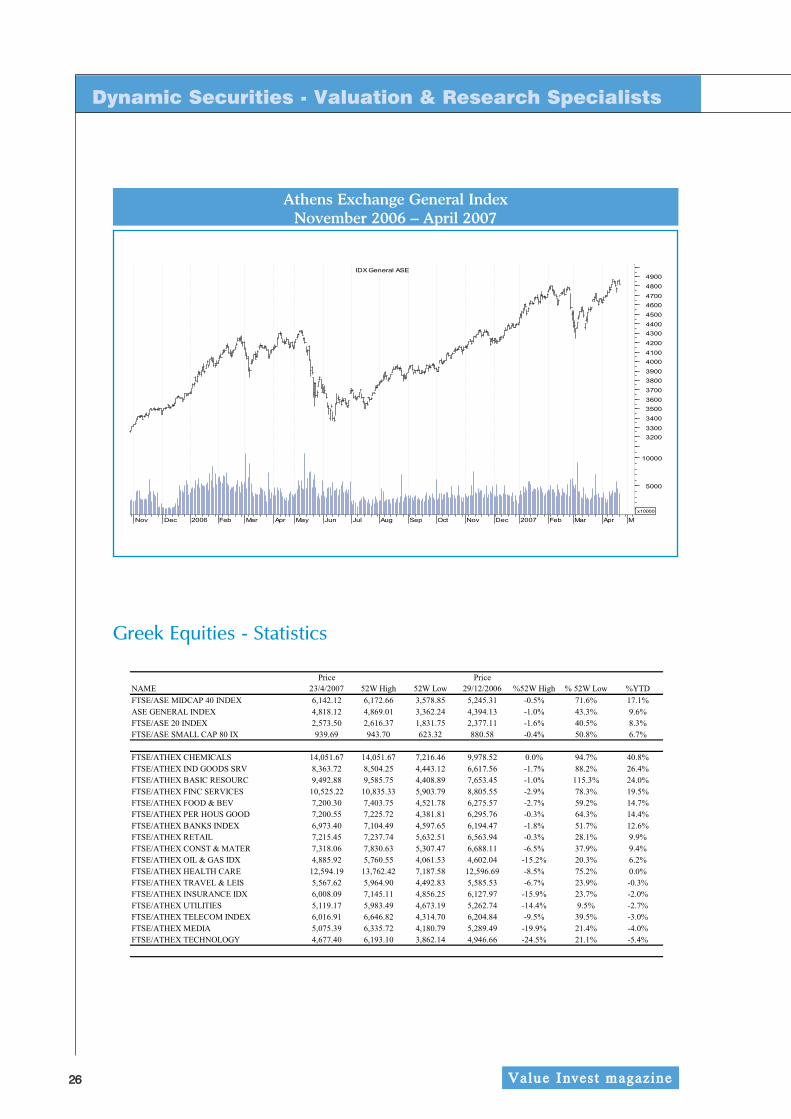

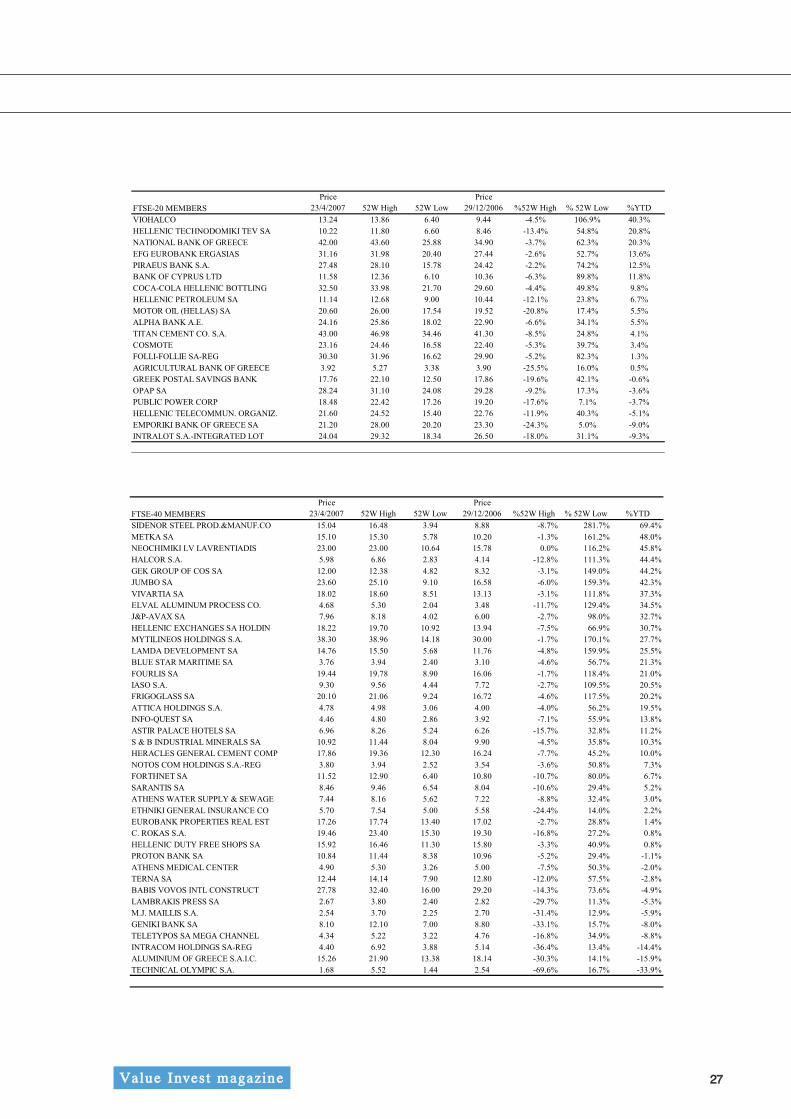

In tandem with the other devel-oped stock markets across theglobe, the positive sentimentremained in Athens Exchange inthe first months of 2007 despitethe short-period sell-off observedat the end of February as investorsworried about the status of the USeconomy and the drop in Shanghaistock exchange.The high growth rates of the globaleconomy, the remaining excess liq-uidity and the corporate profitabili-ty supported the rebound in pricesand in April the global stock mar-ket indices re-gained their highs.Following this trend, the Athensstock exchange composite indexclimbed to 7-year highs in Aprilsupported by strong corporateprofitability that approached 30%y-o-y. M&A deals maintained theinterest while foreign investorsincreased their participation intotal market capitalization.Overall, the composite index ended9.6% up y-t-d (for the periodJanuary the 1st till April the 23rd).The Mid-cap 40 index continued itsimpressive performance (17.1%),while FTSE-20 and FTSE-80indices, although remained in posi-

tive grounds, lagged the compositeindex. Chemicals reported animpressive 40.8% followed byIndustrial goods (26.4%) and Basicresources (24%), while six sectoralindices reported losses for the year.Looking at the performance ofindividual companies that consti-tute the three FTSE indices,Viohalco group of companies con-tinued its strong performancereporting a 40.3% y-t-d return sup-ported by the corporate develop-ments of its subsidiaries, whilebanking shares are back in fashionfollowing the developments in theirprofitability especially to the partthat is attributed to Balkans.Five FTSE-20 members reportednegative performance as they werehit by unsuccessful corporatedevelopments. Healthy mid-capcompanies reported substantialdouble digit performance figures ascorporate deals continued, andonly 11 out of 40 companies thatconstitute the FTSE-40 reportednegative performance.

NNootteess:: Year to date performanceconcerns the period 30 December2005 – 23 April 2007.

2266

Dynamic Securities - Valuation & Research Specialists

VVaalluuee IInnvveesstt mmaaggaazziinnee

Athens Exchange General IndexNovember 2006 – April 2007

Greek Equities - Statistics

2277VVaalluuee IInnvveesstt mmaaggaazziinnee

2288

Dynamic Securities - Valuation & Research Specialists

VVaalluuee IInnvveesstt mmaaggaazziinnee

2299

DISCLOSURE STATEMENT

This document has been prepared and issuedby DYNAMIC SECURITIES SA which is regu-lated by the Hellenic Capital MarketCommission and is subject to the rules of con-duct applicable to investment firms (EPEYs) asestablished under Greek regulations. DYNAM-IC SECURITIES SA is not engaged in anyagreement with the subject companies for thepreparation of this document.

Dynamic Securities SA has prepared the aboveresearch material and its contents are for infor-mation purposes only and should not be con-strued as an offer to sell or a solicitation tobuy any securities. The information containedin this report including any expression of opin-ion has been taken from sources believed to bereliable but it cannot be guaranteed and nowarranty is given that such information isaccurate or complete and it should not berelied upon as such and are subject to changewithout further notice. Dynamic Securities SAand/or its associated group companies or a per-son or persons connected with the companymay from time to time act on their ownaccount in transactions covered in its researchreports. Dynamic Securities SA may do andmay seek to do business with companies cov-ered in its research reports. As a result,investors should be aware that the firm mighthave a conflict of interest that could affect theimpartiality of this report. Investors shouldconsider this report as only a single factor inmaking their investment decision. Securitiesmentioned in this report are subject to invest-ment risks including the loss of initial capitalinvested. Dynamic Securities SA does notaccept any liability whatsoever for any director consequential loss arising from any use ofthis document or its contents. This report isaddressed to professional investors only andno part of this report may be reproduced orpassed on in any manner without prior permis-sion.

• At the date of the issuance of this report(mentioned in the first page of the report)DYNAMIC SECURITIES SA does not holdmore than 5% of a class of common equitysecurities on any company mentioned in thisreport.

• At the date of the issuance of this report(mentioned in the first page of the report)none of the subject companies mentioned inthis report owns more than 5% of DYNAMICSECURITIES SA or any of its affiliated com-panies. DYNAMIC SECURITIES SA does notact as a market maker for the securities ofthe company.

• DYNAMIC SECURITIES SA has not providedunderwriting services to the company cov-ered in the report.

• DYNAMIC SECURITIES SA has not receivedcompensation from the company for finan-cial advisory services during the past 12months.

• DYNAMIC SECURITIES SA has not receivedcompensation from the company for thepreparation of the research report.

Internal procedures: a) The research depart-ment is situated in an area where only employ-ees of the department have access in order toensure secured confidentiality. The data andrecords of the department are out of reach ofthe other departments. Chinese Walls are setbetween the research department and otherdepartments so that DYNAMIC SECURITIESSA can abide by the provisions regarding confi-dential information and market abuse.

Analyst CertificationThe analyst responsible for the content of thisresearch report (in whole or in part), certifiesthat a) all the views about the companies andsecurities contained in this report accuratelyreflect the personal views of the respectiveauthor and b) no part of our compensationwas or will be directly or indirectly related tothe specific recommendations or view of thisreport. The author of this report may haveheld or hold in the future shares of the compa-ny covered in its research reports. The analystor at least one of the analysts mentioned inthis report are Certified as “Analyst of Equitiesand the Market” by the Hellenic CapitalMarket Commission.

Analyst Stock Ratings All of the above denote investment ratings (notrecommendations) which refer to our overallview of the company based not only on valua-tion but on qualitative factors as well.

VVaalluuee IInnvveesstt mmaaggaazziinnee

3300

IInnttrroodduuccttiioonn

Market risk, as defined by the BaselCommittee, is the risk of losses in on-and off-balance-sheet positions arisingfrom movements in market prices.The issue has become of specialimportance as the increased exposureof financial institutions to a widerange of financial products ignited anera of increased market risk. Value-at-Risk (VaR) has become themain theoretical tool for quantifyingmarket risk for the trading book offinancial institutions, and the tradi-tional methodologies applied for theestimation of VaR (variance-covari-ance, Historical Simulation, MonteCarlo) utilise the standard deviation asa measure of the variability of tradingor theoretical values of many prod-ucts.

Over the years, many attempts haveemerged as alternatives in forecastingfinancial volatility, the main input inVAR models. RiskMetricsTM approachto forecast volatility with the IGARCHmodel often proved ineffective againstthe classic method of equally weightedvolatility [Alexander και Leigh (1997)].Additionally, conventional methods toestimate VaR such as variance-covari-ance and historical simulation do notaccount for market dynamics, het-

eroscedastic behaviour and the distri-bution of risk factors [Kuester et al.(2003)]. For the application of histori-cal simulation (HS) some alternativemethodologies were proposed by[Barone–Adesi et al. (1999)] toaccount for the heteroscedasticity ofmarket risk factors. Despite their relative advantages anddisadvantages, none of the conven-tional approaches to estimate VaR isfocused completely on the extremevalues of the market risk factors dis-tributions. Danielsson and de Vries(1997) showed that the estimation ofVaR with EVT produces better resultsto that of HS coupled with IGARCH,mainly because it combines some ofthe advantages of both parametric(IGARCH) and non-parametric (HS)models. [Gencay and Selcuk (2004)]demonstrated that Extreme ValueTheory (EVT) is more efficient com-pared to Variance Covariance (VC)and HS on the estimation of the dailyVaR values from the stock market ofnine emerging markets for higher con-fidence intervals. [McNeil and Frey(2000)] when trying to account staticforecasts produced by parametric[Kellezi and Gilli (2000)] and semi-parametric [Dacorogna et al. (1995)]variations of EVT, suggested the useof conditional EVT that accounts forheteroscedastic effects of the residuals

Quantifying market risk:an evaluation of alternativetechniques

3311

and creates the respective quintiles toestimate VaR. Within the aforemen-tioned framework, the present studypresents an evaluation of threemethodologies to estimate VaR thataccount for heteroscedasticity (condi-tional EVT) and conventional models(VC and HS) on a combined portfolioof two financial products, stocks asrepresented by the S&P500 index andopen exchange rate position in USdollars (the $/4 exchange rate). Thedata cover the period from January 2,1997 to March 14, 2004 and the com-bined portfolio was formed using ran-dom positions which change on adaily basis.

MMeetthhooddoollooggyy

Internal VaR models attempt to esti-mate the losses of a portfolio that mayarise during a predefined interval(usually next working day) and notexceed a specified frequency ofappearances (e.g. confidence level of99%, 95%, etc.). Every VaR toolassumes the modelling of logarithmicreturns as:

where, Xt and Xt-1 the value of aproduct at time t and its first lagrespectively. The simplest method for a VaR esti-mate is the HS one, mainly due to theleast computational resources that arerequired, and according to which thenext day VaR for a confidence level q,is found from the empirical quintile Qq

of a sorted sample of n sorted andi.i.d. observations up to this day:

The second method tested, the VCone, is based on equation (3)

where the correlation matrix C detailsthe correlations between the portfolioproducts and VCUVaRt+1 includes therespective VaR estimate for each prod-uct. Each product’s VaR with an openposition wi,t (in 4) is found from a sen-sitivity coefficient Li,t and the futurevariability of returns σi,t+1 for a quin-tile Qq based on the confidence level qof the normal distribution:

Third, we applied the Conditional EVTby which we measured the distribu-tion of exceedances (Y) above athreshold reference (u) based on equa-tion (5), where its parameters are esti-mated using maximum likelihood:

Using equation (5), the conditionalEVT approach is approached by usingthe standardized residuals that resultfrom a AR(1)-GARCH(1,1) model:

RReessuullttss

In the literature there are two mainapproaches that evaluate the VaR esti-

VVaalluuee IInnvveesstt mmaaggaazziinnee

3322

mates of any method: statistical, suchas root mean square error (RMSE),mean error (ME), mean absolute error(MAE), etc., and economic, such asthe number of exceedances of predic-tions from real values, the success of atrading rule and etc. However, the for-mer are often biased and noisy estima-tors [Christodoulakis and Satchell(2004)]. Thus, in the present study thefinancial measures included in theBasel Committee Amendment wereselected. This approach shows themost efficient model as the one withthe least number of over-shootingsusing back-testing [Kalyvas et al.(2006)].

The results reported that EVT is themost conservative method reportingby far the highest daily VaR estimateduring the entire 7 years period. Thebiggest percentage difference betweenthe VaR estimates of the three modelsfor the same day was found betweenEVT and VC, in favour of the first,while the respective differencebetween the estimates of EVT to theother models was much smaller onaverage. The other two models (VC,and HS) exhibit, on average, similarestimates. Accordingly, the resultingcapital requirements according to theEVT are higher compared to the othermodels.

In addition, EVT appears to producethe least number of over-shootings on‘back-testing’ (9) when these are esti-mated using a moving window of thelast 250 observations against 22 forthe VC and 20 for the HS. The maxi-mum number produced by EVT wasfound equal to 4 where as the other

models produce a maximum of 7(Figure 1).

CCoonncclluussiioonn

This study was focused in the study ofportfolios created by open positions inforeign exchange and stock productsthat are traded in spot market com-pareing three different methodologiesto estimate VaR, namely VC, HS, andconditional EVT, for randomly select-ed portfolios. EVT was found to pro-duce the most conservative estimatesof VaR against the other methods, aresult that may impose some disad-vantages for its daily calculation byfinancial institutions.The findings of this study are in accor-dance with those found in the litera-ture according to which the semi-parametric EVT is the optimal estima-tor of VaR against other methodolo-gies. Adding to the conclusions ofother studies, the empirical findingsshowed that novel methodologies inthe estimation of VaR appear to beeffective for every risk factor theyhave been applied to, but for themoment they do not seem to be theoptimal solution, in terms of capitalrequirements, for financial institu-tions, when their portfolios is com-prised from the examined products.However, since EVT includes the ele-ment of extreme events, the benefitsto other portfolios with highly riskproducts (e.g. options, swaps etc.)should be thoroughly examined.Furthermore, the fact that EVT is alsoto model crisis situations should alsobe accounted for, which may signifi-cantly reduce operational risk.

Lampros Kalyvas - Athanasios Sfetsos - Ioannis Asimakopoulos

VVaalluuee IInnvveesstt mmaaggaazziinnee

3333VVaalluuee IInnvveesstt mmaaggaazziinnee

10987654321

10987654321

10987654321

Figure 1:Overshootings of VaR estimates against observed losses

Conditional EVT

Historical Simulation

Variance Covariance

3344

RReeffeerreenncceess

Alexander, C. O. and Leigh, C. T., Onthe Covariance Matrices used inValue-at-Risk Models, Journal ofDerivatives, 4:3, pp. 50-62, 1997.

Barone-Adesi, G., Giannopoulos, K.and Vosper, L., VaR withoutCorrelations for Portfolios ofDerivative Securities, Journal ofFutures Markets, 19, pp. 583-602,1999.

Christodoulakis, G. and Satchell, S.,Forecast Evaluation in the Presence ofUnobserved Volatility, EconometricReviews, Vol. 23, No. 3, pp. 175-198,2004.

Dacorogna, M., Muller, U., Pictet, O.and de Vries, C. The distribution ofextremal foreign exchange ratesreturns in extremely large data sets,Preprint, Olsen and Associates, June1995.

Danielsson, J., and de Vries, C. G.,Value at Risk and Extreme Returns,London School of Economics,Financial Markets Group Discussion

Paper no. 273, 1997.

Kalyvas, L. and Akkizidis I. withZourka, I. and Bouchereau, V.,Integrating Market, Credit andOperational Risk: A guide for bankersand risk professionals, RiskBooks,London, 2006

Kellezi, E. and Gilli, M., Extreme valuetheory for tail-related risk measures,Preprint, Department of Econometricsand FAME, University of Geneva,2000.

Kuester, K., Mittnik, S. and Paolella,M., Value-at-Risk Prediction: A com-parison of alternative strategies, CFSworkshop, Frankfurt, 2003.

McNeil, A. J. and Frey, R., Estimationof tail-related risk measures for het-eroskedastic financial time series: anExtreme Value Approach, Journal ofEmpirical Finance, 7, pp. 271-300,2000.

Lampros Kalyvas - Athanasios Sfetsos - Ioannis Asimakopoulos

VVaalluuee IInnvveesstt mmaaggaazziinnee

AAuutthhoorrss

LLaammpprrooss KKaallyyvvaass Bank of GreeceDepartment for the Supervision ofCredit and Financial InstitutionsRisk Analysis and SupervisoryTechniques Division

In some cases, option theory isbelieved to be superior to the naïvediscounted cash flow approach to val-uation because it captures the value ofreal options arising from managerialand strategic flexibility. Bearing this inmind, we investigate the extend towhich company valuation of listedcompanies is associated with the exis-tence of real options. In particular, thestudy evaluates the real options ofcompanies listed on the Athens StockExchange during the time period ofJanuary 1990 to December 1999. Initially, we examine the events thatreveal the existence of real optionsheld by the companies and eventuallytheir exercise. For this purpose, plansand decisions about company-widecapital expenditure and about specificprojects are included into the sample.In addition, plans or decisions, whichinclude funds for the purpose ofacquisitions and tender offers andplans or decisions by corporate sub-sidiaries, are included. The originalsample of events was compiled byexamining the company capitalincrease leaflets and company annualreports, information revealed to the

press and discussion with the compa-ny management. First, it is shown thatthe presence of growth options isassociated with excessive returns dur-ing the event period. The results rejectthe hypothesis that real options arenot recognised in the market placeand indicate that market participantsare normally informed one day beforethe announcement. The value of com-panies that have growth optionsincreases till the third day after realoption announcement. Furthermorewe examine whether the real optionsare value relevant in the context ofresidual income valuation model fol-lowing mainly the Ohlson (1995)residual income model and methodol-ogy developed in Green, Stark andThomas (1996). Our study indicatesthat the growth options are a signifi-cant explanatory variable in the con-text of the residual income valuationmodel. Our results provide some sup-port of the predictive ability of theresidual income model and are gener-ally in line with findings from UK andUSA researchers. Besides there issome support over the hypothesis thatgrowth options are value relevant,

Konstantinos Vergos

VVaalluuee IInnvveesstt mmaaggaazziinnee

Real Options and the pricingof shares: empiricalevidence from the AthensStock Exhange

3377

since they contribute in the predictiveability of residual income models.Also, our findings from cross-sectionalmodels match to our findings from theexamination of the effect of optionannouncements to companies' value.Our findings are also similar to find-ings over the effect of R&D announce-ments in other markets. Overall ourstudy should provide a link betweenthe real option theory and market val-uation. Moreover, these findings arepromising, because they reveal thatmarket valuation practices and thereal option theory converge in thecase of the growth options.

11.. IInnttrroodduuccttiioonn

In our study we will examine eventsthat reveal the existence and exercis-ing of real options of companies listedon the Athens Stock Exchange. Forthis purpose, plans and decisionsabout company-wide capital expendi-tures and about specific projects areincluded into the sample. In addition,plans or decisions, which includefunds for the purpose of acquisitionsand tender offers and plans or deci-sions by corporate subsidiaries, areincluded. We will examine events forthe 1989-1999 period. We examineddaily closing share prices and only onetype of share of every company, themost marketable one. To be includedin the sample, the share of a companythat is examined in our study had tobe listed on the Athens StockExchange at the time the manage-ment’s intentions were revealed and atthe time the announcement wasmade. The share prices are adjustedfor capital increases and dividends.

We use data from the electronicEFFECT database. The original sampleof events was compiled by the exami-nation of the companies’ capitalincrease leaflets and companies’ annu-al reports, information revealed to thepress and discussion with the compa-ny’ s management. The articles werecollected from daily and weekly news-papers. We also use the electronicdatabase of Reuters Business Briefingto crosscheck the time of informationreleases.

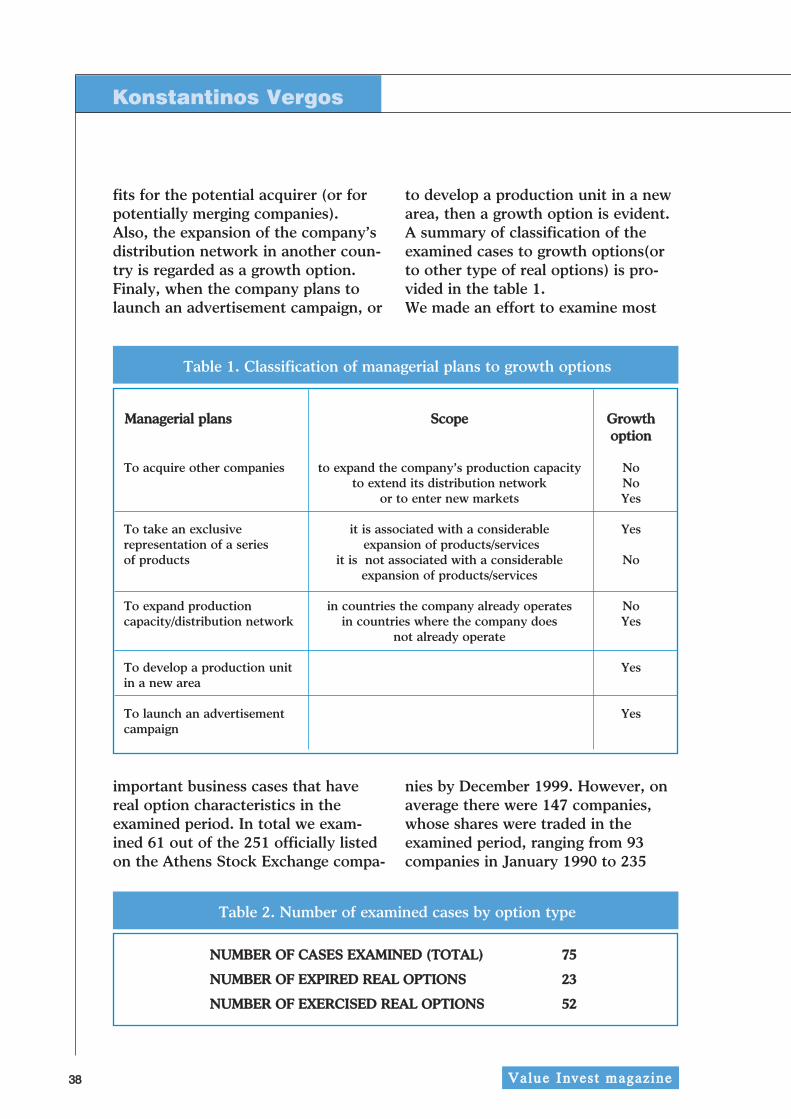

We examine five types of businessdecisions that have growth optioncharacteristics and their economiceffect can be quantified. These are theoptions

• to acquire other companies,• to take an exclusive representation

of a series of products, • to expand production capacity/

distribution network, • to develop a production unit in a

new area, • to launch an advertisement

campaign.

The management considers acquiringother companies so as to expand thecompany’s production capacity, toextend its distribution network, or toenter new markets. If acquisition leadsto the entry in new markets, then thecompany holds a corporate growthoption.Similarly, the option to acquire othercompanies or the option to merge isexamined in cases the acquisition (ormerger) may induce identifiable bene-

VVaalluuee IInnvveesstt mmaaggaazziinnee

3388

fits for the potential acquirer (or forpotentially merging companies).Also, the expansion of the company’sdistribution network in another coun-try is regarded as a growth option.Finaly, when the company plans tolaunch an advertisement campaign, or

to develop a production unit in a newarea, then a growth option is evident. A summary of classification of theexamined cases to growth options(orto other type of real options) is pro-vided in the table 1.We made an effort to examine most

Konstantinos Vergos

VVaalluuee IInnvveesstt mmaaggaazziinnee

Table 1. Classification of managerial plans to growth options

To acquire other companies to expand the company’s production capacity Noto extend its distribution network No

or to enter new markets Yes

To take an exclusive it is associated with a considerable Yesrepresentation of a series expansion of products/servicesof products it is not associated with a considerable No

expansion of products/services

To expand production in countries the company already operates Nocapacity/distribution network in countries where the company does Yes

important business cases that havereal option characteristics in theexamined period. In total we exam-ined 61 out of the 251 officially listedon the Athens Stock Exchange compa-

nies by December 1999. However, onaverage there were 147 companies,whose shares were traded in theexamined period, ranging from 93companies in January 1990 to 235

3399

companies in December 1999.The number of examined cases byoption type is illustrated in thetable 2.There are two main research questionsto investigate. First, we investigatewhether real options are recognised bythe marketplace. Second, we examinecontribution of real options to compa-ny's value in the context of residualincome valuation.

33.. RReeaall OOppttiioonn RReeccooggnniittiioonn

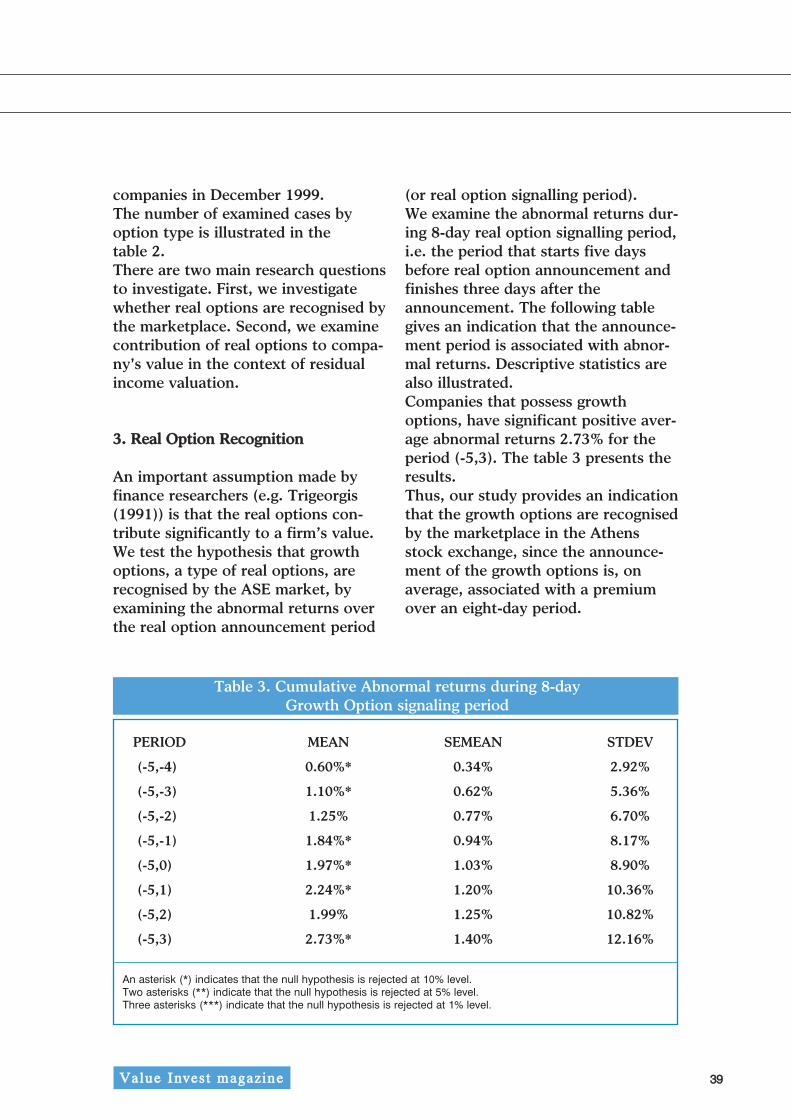

An important assumption made byfinance researchers (e.g. Trigeorgis(1991)) is that the real options con-tribute significantly to a firm’s value.We test the hypothesis that growthoptions, a type of real options, arerecognised by the ASE market, byexamining the abnormal returns overthe real option announcement period

(or real option signalling period). We examine the abnormal returns dur-ing 8-day real option signalling period,i.e. the period that starts five daysbefore real option announcement andfinishes three days after theannouncement. The following tablegives an indication that the announce-ment period is associated with abnor-mal returns. Descriptive statistics arealso illustrated.Companies that possess growthoptions, have significant positive aver-age abnormal returns 2.73% for theperiod (-5,3). The table 3 presents theresults.Thus, our study provides an indicationthat the growth options are recognisedby the marketplace in the Athensstock exchange, since the announce-ment of the growth options is, onaverage, associated with a premiumover an eight-day period.

VVaalluuee IInnvveesstt mmaaggaazziinnee

Table 3. Cumulative Abnormal returns during 8-dayGrowth Option signaling period

PERIOD MEAN SEMEAN STDEV

(-5,-4) 0.60%* 0.34% 2.92%

(-5,-3) 1.10%* 0.62% 5.36%

(-5,-2) 1.25% 0.77% 6.70%

(-5,-1) 1.84%* 0.94% 8.17%

(-5,0) 1.97%* 1.03% 8.90%

(-5,1) 2.24%* 1.20% 10.36%

(-5,2) 1.99% 1.25% 10.82%

(-5,3) 2.73%* 1.40% 12.16%

An asterisk (*) indicates that the null hypothesis is rejected at 10% level.Two asterisks (**) indicate that the null hypothesis is rejected at 5% level. Three asterisks (***) indicate that the null hypothesis is rejected at 1% level.

According to the "clean surplus equa-tion", as presented by Ohlson (1995),the market value of a company can bemodelled as a linear function ofEarnings, Closing Book Value and netDividends,

and

given thatdt are net dividends at time txt are earnings in period tbt is book value at time txt

a are abnormal earmingsr is the risk-free interestA less restricted form of the "cleansurplus equation", allows for othercontrol variables.

wherePt is the market value of the firm'sstock at time tYt is the book value of equity at time tXt is reported accounting earnings attime tr is the risk-free interest(Xt-rYt-1) is abnormal earningsZt is a vector of other informationvariables at time tWe investigate the value relevance ofreal options by incorporating factors

in these models. Equation (3), can betransformed to the following equationthat is deflated by Book Value, so asto allow for control for size factors.

To examine whether the real optionscontribute during their lifetime to thecompany’s value in the share market,in the context of "clean surplus" litera-ture we compute regression coeffi-cients and t-statistics of the followingregression.

whereMVi,t is market value for firm I sixmonths after the end of year tBVi,t is book value for firm I at the endof financial year tRIi,t is residual income for firm I inyear tGRO is the number of months of pres-ence of growth option before itbecame exercisedGRO is the number of months of pres-ence of growth option before itexpired unexercisedOur results, expressed on Table 4 pro-vide some evidence that leads to thesupport of clean surplus hypothesis.Both the coefficients of 1/BV andRI/BV are positive (0.38 and 1.153respectively) and significant at 1%level of significance. The presence ofthe growth options for a monthincreases the company's MarketValue by 0.265 times the BookValue(Coefficient of GRO variable).Growth options that expired unexer-cised had an insignificant effect on

Konstantinos Vergos

VVaalluuee IInnvveesstt mmaaggaazziinnee

4411VVaalluuee IInnvveesstt mmaaggaazziinnee

Table 4. Regression statistics over the period 1990-1998, Examined model:

Sample requirements: Companies having MV/BV>9 or BV<0 are excluded

PERIOD 1990-1998

Intercept 1.597***

t-stat 22.258

1/BVi,t 0.38***

t-stat 5.229

RIi,t/BVi,t 1.153***

t-stat 5.472

GRO 0.265***

t-stat 4.286

GROXT 0.106

t-stat 0.780

R-sq-adj 5.06%

Sample 1150

An asterisk (*) indicates that the null hypothesis is rejected at 10% level.

Two asterisks (**) indicate that the null hypothesis is rejected at 5% level.

Three asterisks (***) indicate that the null hypothesis is rejected at 1% level.

company value. The Regression fit is low(R square adjusted is 5.05%). Equally, the effect of the real options oncompanies' value is weak and insignifi-cant when we examine data on an annu-al base (Table 5). The growth optionshave positive effect on corporate marketvalue in most of the years (five out of

seven). Nevertheless, regression coeffi-cients are unstable over time. The smallsample size at an annual base, may givean explanation to real option coefficientinstability as well as to their generallylow statistical significance in annualregressions. Our findings can be partlycompared to other studies in the area of

4422

residual income valuation. Regressingdeflated Residual Income, Book Valueand real Options against the differenceof Book Value from Market Valueleads to lower predictive ability com-pared to the predictive ability of themodels examined in Sougiannis(1994)and Green, Stark and Thomas (1996). The R-sq in our study is 5.7% whilein Green, Stark and Thomas (1996) itis 91.4% - 91.7% and in Sougiannis itis 32%. The coefficient of residualincome (RI) is higher than the unity(1.153) and significant at 1% level.However, the coefficient of RI is high-

er in previous studies (in Sougiannisstudy it is 2.75 and in Green, Starkand Thomas study it is 4.65 and 4.77).Maybe the inclusion of growth optionvariable captures an important part ofresidual income value. Nevertheless,intercept, closing Book Value andresidual income are found statisticallysignificant and positive as in Green,Stark and Thomas (1996) study. Theregression coefficient of Book Value isfound higher in our study (1.59 versus0.86 and 0.91 found in the Green,Stark and Thomas (1996) study).

Konstantinos Vergos

VVaalluuee IInnvveesstt mmaaggaazziinnee

Table 5. Annual Regression statistics over the period 1990-1998,Examined model:

Sample requirements: Companies having MV/BV>9 or BV<0 are excluded

PERIOD 1990 1991 1992 1993 1994 1995 1996 1997 1998

An important assumption made in thisstudy is that market efficiency exists.If market efficiency is not evident,investors do not form their expecta-tions in terms of risk and return or atleast they do not form these expecta-tions with uniform criteria. If this isevident, our model simply breaksdown.Not including additional control vari-ables in cross-sectional regressions isalso a limitation. However, R&Dexpenditures, which is the single mostimportant factor included in otherstudies, were particularly small andmade by less than 5% of the examinedcompanies, whilst part of these expen-ditures is associated with real options.Similarly, we did not find sufficientdata to examine the effect of advertis-ing expenditure on companies' marketvalue, examined in Shah and Stark(2001).Also, although pooled data pro-vide some support over real optionvalue relevance, annual data aresomewhat unstable, probably due tosmall sample deficiencies.Nevertheless, our research designincludes all sectors, so it leads to thegeneralization of our conclusions. Ourdata include financial companies sincepast studies do not provide any evi-dence that earnings, book value andreal options are not determinants ofthe value of financial institutions. We do not account for the role ofinformation costs. According toBellalah (2003) there are sunk costsincurred during the phase of gatheringinformation about the project and theopportunity to invest. Bellalah (2003)proposes some models that providesome insights into the importance of

these costs and may explain why com-panies that let their growth optionsexpire do not have market premium.Also, the models developed by Lintand Pennings (2003) may provide arationale to part of our findings. Lintand Pennings (2003) use an optionapproach to the New ProductDevelopment process to develop aframework that incorporates marketand technology uncertainties in allgo/no-go decisions. According to Lintand Pennings (2003) the projects dur-ing the R&D phase or after the R&Dstage that combine negative Net pres-ent Value and low uncertainty will beabandoned. In our view these casesmay fit to the growth options that themanagement let them expired. Also,issues useful to be examined in thefuture should be the benefits of firstmovers. Tsekrekos (2003) develops anequilibrium framework for real optionexercise where the focus is on theeffect of first-mover's advantages.First-mover advantages are found tohave an asymmetric effect on rivalfirms' values. The more volatile indus-tries should experience more separat-ed firm entries over time the moresubstantial the first-mover privileges.Paxson and Pinto (2003) model theleader and follower value functionsfor a duopoly environment. Assumingthe leader's market share evolvesaccording to an immigration anddeath process, the follower's valuefunction is less sensitive than theleader's value function to marketshare until the expected revenueexceeds the follower's trigger invest-ment level. Besides, the follower's trig-ger increases with market share and

Konstantinos Vergos

VVaalluuee IInnvveesstt mmaaggaazziinnee

4455

revenue volatility. Overall, our study leads to some indi-cations. First, it is shown that thepresence of growth options is associat-ed with abnormal returns during theevent period. The results reject thehypothesis that real options are notrecognised in the market place andindicate that market participants arenormally informed before theannouncement. The value of compa-nies that have real options increasestill the third day after real optionannouncement. Second, there is somesupport over the hypothesis that thegrowth options are value relevant dur-ing their life, since they can explain asignificant part of the appreciation ofMarket Value over Book Value.Thirdthere is some support of the predictiveability of the residual income model.Also, our findings over the predictiveability of residual income model aregenerally in line with findings fromUK and USA researchers. Therefore,our study provides some support overthe validity of residual income marketin the Greek share market.Furthermore, our study shows thatmarket seems to compensate thegrowth options that were finally exer-cised. Besides, the longer the durationof the growth options, the higher theappreciation of companies' marketvalue. The latter finding is in line withobserved practices of market valueappreciation of companies having highduration growth options, like Internetcompanies. Therefore our findingsmay partly give validity the continu-ous appreciation of Internet compa-nies. Finally, our findings from cross-sectional models match to our find-ings from the part of our study that

examines the effect of optionannouncements to companies' value.In particular, our event study findsthat exercised growth options com-pensate to company market value.These findings are also similar to find-ings over the effect of R&D announce-ments in other markets. Overall ourstudy should provide a link betweenthe real option theory and market val-uation. Moreover, these findings arepromising, because they reveal thatmarket valuation practices and thereal option theory converge in thecase of the growth options.

BBiibblliiooggrraapphhyy

1. Bellalah M., On irreversibility, sunkcosts and investment under incom-plete information, in Real R&Doption, 2003, Paxson (ed.),Buttererworth-Heinemann, Oxford,UK

2. Green J., Stark A., Thomas H., UKEvidence on the market valuationof research and development expen-ditures, Journal of Business Financeand Accounting, March 1996,pp.191-216.

3. Lint O., Pennings E., An optionsapproach to new product develop-ment: experience from PhilipsElectronics, in Real R&D option,2003, Paxson (ed.), Buttererworth-Heinemann, Oxford, UK

4. Ohlson J., Earnings, book valuesand dividends in security valuation,Contemporary AccountingResearch, spring 1995, pp.661-687.

VVaalluuee IInnvveesstt mmaaggaazziinnee

4466

5. Paxson D., Pinto H., Leader/follow-er real value functions if the marketshare follows a birth/death process,in Real R&D option, 2003, Paxson(ed.), Buttererworth-Heinemann,Oxford, UK

6. Trigeorgis L., A Log TransformedBinomial Numerical AnalysisMethod for Valuing Complex Multi-Option Investments, Journal ofFinancial and Quantitative Analysis,September 1991, pp. 309-326.

7. Tsekrekos E., The effect of first-

mover’s advantages on the strategicexercise of real options, in RealR&D option, 2003, Paxson (ed.),Buttererworth-Heinemann, Oxford,UK

8. Shah Z., Stark A., On the value rel-evance of major media advertisingexpenditures in the UK, 2001,Unpublished working paper

9. Sougiannis T., The accountingbased valuation of corporate R&D,The Accounting Review, Jan 1994,pp.44-68.

Konstantinos Vergos

VVaalluuee IInnvveesstt mmaaggaazziinnee

1 The variables are deflated by Closing Book Value

2 (MV-BV)/BV=α0+α1(1/BV)+α2(Ε/BV)+α3 (RI/BV)+λ1 Z1 + λ2 Z2+λ3 Z3 + λ4 Z4 + λ5 Z5 + λ6 Z6 + εi,t, given that z1 isthe market share possessed by firm I in year t,z2 is the degree of concentration for the industry to which firm ibelongs in year t,z3 is the ratio of short- and long-term debt to shareholders' equity plus reserves for firm i in yeart,z4 is the ratio of short- and long-term debt to shareholders' equity plus reserves for the industry to which firm Ibelongs in year t,z5 is (z3-z4)2,, z6 is the average variance of the stock returns for firm I for the four quarters endingin the quarter of the financial year-end.

AAuutthhoorr

Konstantinos Vergos, PhD President of Hellenic Association ofCertified Stock Market Analyst Head of Research, PentedekasSecurities S.A., Greece

Presented in 1st International Seminarin Quantitative Methods in Industryand Commerce, 26-27 May 2003, TEIof Athens, Athens, Greece

Investor relations (IR) is becomingslowly but progressively a disciplineand/or an art between a rock and ahard place. In other words a functionthat makes the difference for the list-ed companies’ communication processto the markets. Especially nowadayswith so many issues on corporateaccountability and effectiveness, theIR function is the one that arisesbeyond and above the corporate gov-ernance guidelines, which are univer-sal and standardised to many nationalequity markets and countries, espe-cially to the economic building blockssuch as European Union, NAFTA, etc.It is the one that makes the invest-ment case of a listed company and itslisted stock to be recognised and beon the radar system of the fund man-agers. The objective of this article is to pin-point/identify the involuntary and vol-untary disclosure strategies used bylisted companies and to evaluate theireffectiveness. As a consequence, I tryto extract an effective IR path/methodin order to attain the predeterminedgoals such as increase firm visibility,improve its liquidity and share pricethrough upgraded disclosure.

However to measure the effectivenessof the IR activities is a difficult task aswell as a dilemma and there is nostandard answer to it. I believe, as anIR practitioner that, ultimately the IRis measured up with some identifiablefactors. These factors mostly belongto the voluntary disclosure pool thatthe IRO and the senior managementcan use. The friendly, interactive andwell-informed company’s web site, theincreasing number of private meetingswith investors especially institutionalinvestors, the implementation of aroadshow policy, even the adequateand timely feedback to analysts arevariables which the IRO can intensifyor minimize well beyond theCorporate Governance principles andregulations. Other factors are moreobvious and simpler such as the num-ber of institutional investors year byyear, the retaining of existinginvestors, the number of people (endusers, institutional and individualinvestors) that know the companywell (through constant communica-tion and disclosure) and the increaseof the share price of the underlyingstock.Furthermore, as the local and globalmoney managers and analysts indi-cate, the Investor Relations Officer(IRO) has to plan strategy and tactics

on a global scale with clarity,resourcefulness and flexibility. For asmall, periphery but somehow dynam-ic market such as Greece, the IROmust add professionalism, seriousnessand reputation. Then, if properlyorchestrate his/her IR options, activi-ties and communication effectivenesseven the most disbelieving, pessimisticand suspicious targeted local andespecially global fund manager willinvest in the underlying Greek stock.Nevertheless, in order to attract USand European pension funds andother institutional investors into amarket such as Greece, which in reali-ty is still an emerging market, betterdisclosure, transparency and high gov-ernance standards and practices arealso key elements. Indeed, globalexperience indicates that investorsultimately pay more if they are com-

fortable with good returns coupledwith disclosure.

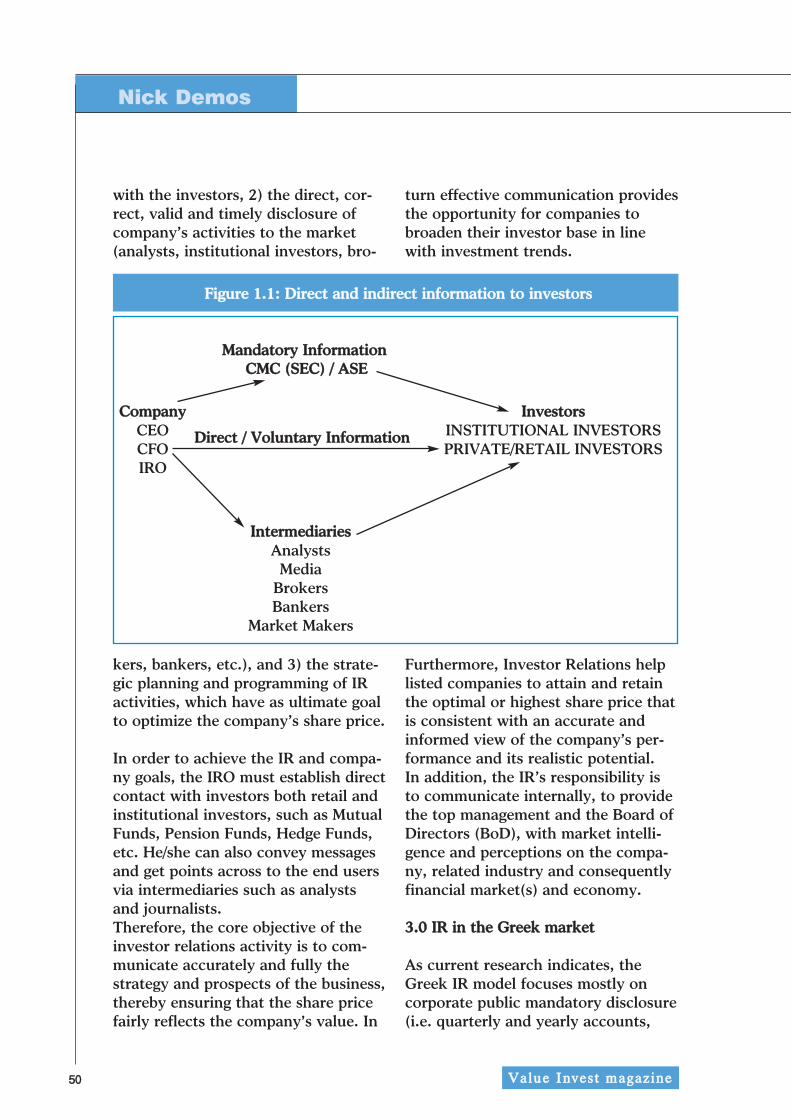

IR is a multidisciplinary function thatcombines principles, methods andtools from sciences and arts such asfinance, accounting, marketing, eco-nomics, game theory, public relationsand psychology.Most people accept that the IR func-tion does help the information flowbetween the listed companies andtheir audience (figure 1.1). It comesout of the basic need of communicat-ing the company’s information to themarket but as a silo of informationcan be used by the different interestedparties to their benefits. Exactly thenthe regulators appear in order to con-trol and direct the communicationchannel to a/the mutually benefit ofthe market.Managers run the listed firms (intrust), who plan and implement thestrategic and marketing plans andtherefore control all vital companyinformation. On the other side, allshareholders and stakeholders (i.e.suppliers, bankers, customers, etc)have little or no information on thecompany’s activities and performance.Thus this information asymmetry,between the two groups, creates theneed for an information processorsuch as the IR function. And the IRadventure begins, since as processor,is always between a hard place and arock.The basic aim of the InvestorRelations (IR) department, accordingto my experience is: 1) the creationand cultivation of relations of trust

VVaalluuee IInnvveesstt mmaaggaazziinnee

5500

with the investors, 2) the direct, cor-rect, valid and timely disclosure ofcompany’s activities to the market(analysts, institutional investors, bro-

kers, bankers, etc.), and 3) the strate-gic planning and programming of IRactivities, which have as ultimate goalto optimize the company’s share price.

In order to achieve the IR and compa-ny goals, the IRO must establish directcontact with investors both retail andinstitutional investors, such as MutualFunds, Pension Funds, Hedge Funds,etc. He/she can also convey messagesand get points across to the end usersvia intermediaries such as analystsand journalists.Therefore, the core objective of theinvestor relations activity is to com-municate accurately and fully thestrategy and prospects of the business,thereby ensuring that the share pricefairly reflects the company's value. In

turn effective communication providesthe opportunity for companies tobroaden their investor base in linewith investment trends.

Furthermore, Investor Relations helplisted companies to attain and retainthe optimal or highest share price thatis consistent with an accurate andinformed view of the company’s per-formance and its realistic potential.In addition, the IR’s responsibility isto communicate internally, to providethe top management and the Board ofDirectors (BoD), with market intelli-gence and perceptions on the compa-ny, related industry and consequentlyfinancial market(s) and economy.

33..00 IIRR iinn tthhee GGrreeeekk mmaarrkkeett

As current research indicates, theGreek IR model focuses mostly oncorporate public mandatory disclosure(i.e. quarterly and yearly accounts,

press releases, etc) according to by-laws and regulation and on any“impulsive action” internally by thepeople from the registry (metocholo-gio) department. In addition, in theGreek model we observe that themedia people not only substitute theinternal people who process the infor-mation but also affect at a large scalethe message given to the marketdirectly or via the sell side analysts’dailys.

Moreover, it looks as if most Greekcompanies, especially the small ones,ignore the requirements of the partic-ular IR position and rush to fill themwith non-qualified individuals. Insteadof hiring individuals with a strong per-sonality who combine market, sector,company and even some legal knowl-edge, and have some experience inportfolio management, public rela-tions and marketing, they attempt tofill the IRO positions with individuals

VVaalluuee IInnvveesstt mmaaggaazziinnee

IR CONSTRAINTS (REQUIREMENTS)

IR OPERATIONAL SET UP

IIRR TTOOOOLLSS // MMEEAANNSS

REGULATED DISCLOSURE VOLUNTARY DISCLOSURE via INTERMEDIARIES DISCLOSURE

whose most important asset may betheir relationship with the owners orthe top executives of the company, oranalysts or brokers simply trying toflee the shrinking brokerage business.These people, as a whole, fail toimpress foreign institutional investors.Adopting voluntary and mostly invol-untary disclosure policies and engag-ing in pre-marketing and proactiveroadshows abroad should be part ofthe listed firms’ “tool kit.” Failing todo so in an increasingly competitivelandscape for international institution-al funds may result in stock underper-formance, which could possibly hurtthe firm’s image among shareholdersand on aggregate undermine theAthens bourse’s future.Experience and opinions indicate thata number of factors may deter activeforeign funds from investing inAthens. The small sizes of the localstock market, its lack of depth in liq-uidity, etc are some of them.However, the biggest problem facinglocal firms is their inability to “sellthemselves” to the group of activeinternational investors. This is the jobof the Investor Relations Officer (IRO)but most Greek firms do not haveone. Although it is necessary forGreek firms to go out, market them-selves and attract the foreign funds bypursuing active and proactive IRstrategies, few seem to have takennotice and tried to comply.

The basic attributes for the effective-ness of the IR activity is the appropri-ate diagnosis of the specific firm’sneeds as well as the creative strategic