Page 1

ValueGuideMarch 2020

Intelligent Investing

Stock IdeaStock Updates

ViewpointsSector Updates

Regular Features

Report CardEarnings Guide

Products & Services

PMSMF PicksAdvisory

Trader’s Edge

Technical ViewCurrencies

F&O Insights

For Private Circulation only www.sharekhan.com

Contagion CrisisContagion Crisis

Page 2

Whether you’re a trader, an investor or a complete newbie who has recently opened an account with Sharekhan, there’s a module designed especially for you.

Register today

Take your pickChoose from a variety of courses from customised categories

It’s completely onlineAttend the sessions from anywhere you want, all you need is an internet connection

Learn it liveGet a feel of the markets and how they work by attending the sessions during market hours

3 Reasons to be a Classroom regular

Come one, come allThere’s something for everyone at

Sharekhan Classroom

I am a Beginner I am an Online Trader I am an Investor

Explore the module of your choice

I am a Trader

Registered O�ce: Sharekhan Limited, 10th Floor, Beta Building, Lodha iThink Techno Campus, O�. JVLR, Opp. Kanjurmarg Railway Station, Kanjurmarg (East), Mumbai – 400042, Maharashtra. Tel: 022 - 61150000. Sharekhan Ltd.: SEBI Regn. Nos.: BSE / NSE / MSEI (CASH / F&O / CD) / MCX - Commodity: INZ000171337; DP: NSDL/CD-SL-IN-DP-365-2018; PMS: INP000005786; Mutual Fund: ARN 20669; Research Analyst: INH000006183; Compliance O¤cer: Mr. Joby John Meledan; Tel: 022-61150000; email id: [email protected] ; For any queries or grievances kindly email [email protected] or contact: [email protected] : Client should read the Risk Disclosure Document issued by SEBI & relevant exchanges and the T&C on www.sharekhan.com; Investment in securities market are subject to market risks, read all the related documents carefully before investing.

Page 3

CONTENTS

3March 2020 Sharekhan ValueGuide3June 2017 Sharekhan ValueGuide

disclaimer

Disclaimer: This document has been prepared by Sharekhan Ltd. (SHAREKHAN) and is intended for use only by the person or entity to which it is addressed to. This Document may contain confidential and/or privileged material and is not for any type of circulation and any review, retransmission, or any other use is strictly prohibited. This Document is subject to changes without prior notice. This document does not constitute an offer to sell or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. Though disseminated to all customers who are due to receive the same, not all customers may receive this report at the same time. SHAREKHAN will not treat recipients as customers by virtue of their receiving this report.

The information contained herein is obtained from publicly available data or other sources believed to be reliable and SHAREKHAN has not independently verified the accuracy and completeness of the said data and hence it should not be relied upon as such. While we would endeavour to update the information herein on reasonable basis, SHAREKHAN, its subsidiaries and associated compa-nies, their directors and employees (“SHAREKHAN and affiliates”) are under no obligation to update or keep the information current. Also, there may be regulatory, compliance, or other reasons that may prevent SHAREKHAN and affiliates from doing so. This document is prepared for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Recipients of this report should also be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The user assumes the entire risk of any use made of this information. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. We do not undertake to advise you as to any change of our views. Affiliates of Sharekhan may have issued other reports that are inconsistent with and reach different conclusions from the information presented in this report.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject SHAREKHAN and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.

The analyst certifies that the analyst has not dealt or traded directly or indirectly in securities of the company and that all of the views expressed in this document accurately reflect his or her personal views about the subject company or companies and its or their securities and do not necessarily reflect those of SHAREKHAN. The analyst further certifies that neither he or its associates or his relatives has any direct or indirect financial interest nor have actual or beneficial ownership of 1% or more in the securities of the company at the end of the month immediately preceding the date of publication of the research report nor have any material conflict of interest nor has served as officer, director or employee or engaged in market making activity of the company. Further, the analyst has also not been a part of the team which has managed or co-managed the public offerings of the company and no part of the analyst’s compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this document. Sharekhan Limited or its associates or analysts have not received any compensation for investment banking, merchant banking, brokerage services or any compensation or other benefits from the subject company or from third party in the past twelve months in connection with the research report.

Either SHAREKHAN or its affiliates or its directors or employees / representatives / clients or their relatives may have position(s), make market, act as principal or engage in transactions of purchase or sell of securities, from time to time or may be materially interested in any of the securities or related securities referred to in this report and they may have used the information set forth herein before publication. SHAREKHAN may from time to time solicit from, or perform investment banking, or other services for, any company mentioned herein. Without limiting any of the foregoing, in no event shall SHAREKHAN, any of its affiliates or any third party involved in, or related to, computing or compiling the information have any liability for any damages of any kind.

Compliance Officer: Mr. Joby John Meledan; Tel: 022-61150000; email id: [email protected] ;

For any queries or grievances kindly email [email protected] or contact: [email protected]

Registered Office: Sharekhan Limited, 10th Floor, Beta Building, Lodha iThink Techno Campus, Off. JVLR, Opp. Kanjurmarg Railway Station, Kanjurmarg (East), Mumbai – 400042, Maharashtra. Tel: 022 - 61150000. Sharekhan Ltd.: SEBI Regn. Nos.: BSE / NSE / MSEI (CASH / F&O / CD) / MCX - Commodity: INZ000171337; DP: NSDL/CDSL-IN-DP-365-2018; PMS: INP000005786; Mutual Fund: ARN 20669; Research Analyst: INH000006183; For any complaints email at [email protected] . Disclaimer: Client should read the Risk Disclosure Document issued by SEBI & relevant exchanges and the T&C on www.sharekhan.com; Investment in securities market are subject to market risks, read all the related documents carefully before investing.

Stock markets in India and

the world over are in a tizzy

as the Coronavirus outbreak

tightens its grip day by day.

Unfortunately, the outbreak

has come at a time when major

global economies have already

From the Editor’s Desk

PMS DESK

ProPrime - Prime Picks 44

ProPrime - Diversified Equity 45

MUTUAL FUND DESK 47

ValueGuideMarch 2020

Intelligent Investing

Stock IdeaStock Updates

ViewpointsSector Updates

Regular Features

Report CardEarnings Guide

Products & Services

PMSMF PicksAdvisory

Trader’s Edge

Technical ViewCurrencies

F&O Insights

For Private Circulation only www.sharekhan.com

Contagion CrisisContagion Crisis

06

EQUITY

FUNDAMENTALS

TECHNICALS DERIVATIVES

Nifty 40 View 41

ADVISORY DESK DERIVATIVES

MID Trades 46 Derivatives Ideas 46

CURRENCY

FUNDAMENTALS

USD-INR 42 GBP-INR 42

EUR-INR 42 JPY-INR 42

TECHNICALS

USD-INR 43 GBP-INR 43

EUR-INR 43 JPY-INR 43

Stock Idea 07 REGULAR FEATURES

Stock Update 09 Report Card 04

Sector Update 36 Earnings Guide 51

been slowing down due to US-China trade tariff war and

other geopolitical issues hurting business sentiments....

Page 4

EQUITY FUNDAMENTALSREPORT CARD

4March 2020 Sharekhan ValueGuide

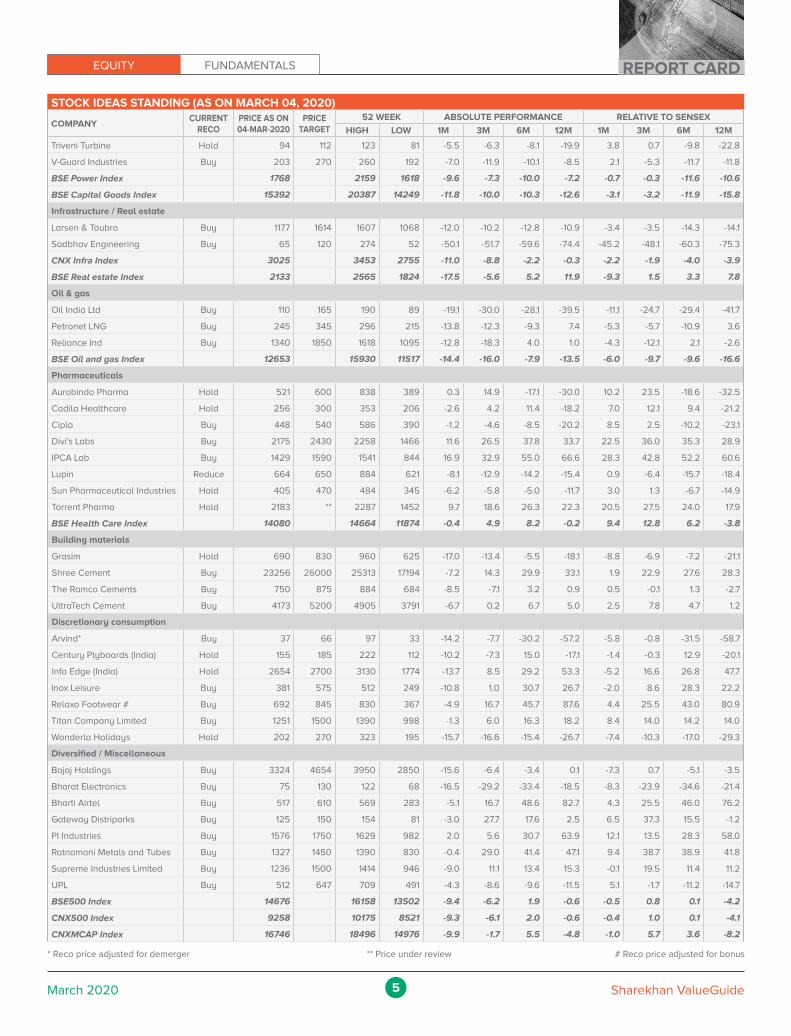

STOCK IDEAS STANDING (AS ON MARCH 04, 2020)

COMPANYCURRENT

RECOPRICE AS ON04-MAR-2020

PRICETARGET

52 WEEK ABSOLUTE PERFORMANCE RELATIVE TO SENSEX

HIGH LOW 1M 3M 6M 12M 1M 3M 6M 12M

Automobiles

Apollo Tyres Buy 140 200 236 125 -16.3 -20.5 -21.1 -35.8 -8.1 -14.6 -22.6 -38.1

Ashok Leyland Hold 72 90 98 57 -12.0 -6.9 11.4 -18.2 -3.4 0.1 9.4 -21.1

Bajaj Auto Buy 2712 3670 3315 2400 -9.3 -10.9 0.6 -0.3 -0.4 -4.2 -1.2 -3.8

Hero MotoCorp Hold 2046 2750 3023 1916 -13.1 -11.3 -21.2 -23.3 -4.5 -4.6 -22.6 -26.0

M&M Buy 475 665 704 441 -18.8 -7.7 -11.0 -27.5 -10.8 -0.7 -12.7 -30.1

Maruti Suzuki Hold 6384 7500 7759 5446 -8.2 -6.4 4.2 -7.4 0.8 0.6 2.3 -10.7

TVS Motor Hold 410 485 525 338 -12.2 -6.3 9.1 -15.0 -3.6 0.7 7.1 -18.0

BSE Auto Index 15644 20412 14662 -14.3 -10.5 -1.8 -18.5 -5.9 -3.7 -3.6 -21.4

Banks & Finance

Axis Bank Buy 682 882 828 615 -10.8 -8.4 -2.0 -8.6 -2.0 -1.5 -3.8 -11.9

Bajaj Finance Buy 4286 5000 4923 2745 -9.2 7.2 25.6 53.3 -0.3 15.2 23.3 47.8

Bajaj Finserv Buy 8800 11000 10297 6581 -10.5 -2.8 20.0 30.3 -1.7 4.5 17.8 25.6

Bank of Baroda Hold 73 105 144 69 -21.7 -26.1 -24.0 -36.0 -14.0 -20.5 -25.4 -38.3

Bank of India Hold 48 70 108 40 -30.0 -33.5 -28.6 -49.3 -23.1 -28.5 -29.9 -51.2

Federal Bank Buy 83 110 110 70 -13.5 -4.9 -3.7 -7.0 -5.0 2.3 -5.5 -10.3

HDFC Buy 2206 2800 2500 1884 -13.4 -6.9 3.3 12.9 -4.9 0.1 1.5 8.9

HDFC Bank Buy 1149 1510 1306 1059 -8.5 -8.9 1.1 8.8 0.5 -2.1 -0.8 4.9

ICICI Bank Buy 508 630 552 370 -10.2 -7.3 24.3 31.1 -1.4 -0.4 22.0 26.4

LIC Housing Finance Hold 321 460 587 282 -30.9 -29.1 -24.2 -37.3 -24.1 -23.7 -25.6 -39.6

Max Financial Buy 591 ** 612 370 8.4 0.7 28.3 27.6 19.0 8.3 26.0 23.0

Punjab National Bank Hold 44 65 100 39 -27.8 -29.7 -30.9 -48.6 -20.7 -24.4 -32.2 -50.5

SBI Buy 285 415 374 244 -16.0 -15.5 -1.3 -2.7 -7.7 -9.1 -3.0 -6.2

Union Bank of India Reduce 36 ** 100 34 -25.1 -33.2 -33.4 -53.7 -17.7 -28.2 -34.6 -55.4

BSE Bank Index 32939 37193 29858 -10.7 -10.5 4.4 3.6 -1.9 -3.8 2.5 -0.1

Consumer goods

Britannia Buy 3063 3670 3584 2300 -5.3 0.4 15.5 2.4 4.1 7.9 13.4 -1.3

Emami Hold 250 352 416 226 -20.7 -24.4 -17.9 -38.6 -12.9 -18.8 -19.4 -40.8

GSK Consumer Hold 9502 9950 9935 6856 3.4 8.7 21.3 36.5 13.5 16.8 19.1 31.6

Godrej Consumer Products Buy 632 865 772 556 -2.0 -3.6 7.2 -8.4 7.6 3.6 5.3 -11.7

Hindustan Unilever Buy 2176 2575 2308 1650 1.5 8.0 20.9 30.4 11.5 16.2 18.8 25.7

ITC Hold 188 242 310 175 -14.9 -25.3 -25.5 -35.2 -6.5 -19.7 -26.8 -37.5

Jyothy Laboratories Hold 123 175 200 119 -12.6 -23.5 -13.1 -32.6 -4.0 -17.8 -14.7 -35.0

Marico Buy 295 395 404 262 -7.6 -16.3 -24.8 -14.6 1.4 -10.0 -26.1 -17.7

Zydus Wellness Hold 1452 1575 1860 1212 -2.2 0.5 -14.3 14.3 7.4 8.1 -15.9 10.2

BSE FMCG Index 10920 12378 10388 -6.6 -6.5 -0.5 -4.9 2.5 0.5 -2.3 -8.3

IT / IT services

HCL Technologies# Buy 563 670 624 497 -5.6 1.4 3.4 9.5 3.7 9.0 1.6 5.6

Infosys Buy 759 820 847 615 -4.2 3.3 -11.0 3.6 5.2 11.1 -12.6 -0.2

Persistent Systems Buy 705 805 740 469 -1.0 2.5 24.2 6.2 8.7 10.2 21.9 2.4

Tata Consultancy Services Hold 2083 2300 2286 1887 -0.6 -0.1 -1.3 9.6 9.2 7.4 -3.1 5.7

Wipro Hold 229 285 302 213 -8.2 -6.9 -10.9 -19.1 0.8 0.1 -12.5 -22.0

BSE IT Index 15537 16587 14183 -3.8 1.6 -4.6 2.7 5.6 9.3 -6.3 -1.0

Capital goods / Power

CESC Buy 610 860 855 578 -15.5 -15.9 -22.3 -14.3 -7.2 -9.5 -23.7 -17.4

Finolex Cable Hold 324 410 508 300 -20.0 -10.6 -14.5 -25.6 -12.1 -3.9 -16.0 -28.3

Greaves Cotton Hold 130 155 157 112 -10.9 -3.6 -2.6 -4.3 -2.2 3.6 -4.4 -7.7

Kalpataru Power Transmission Buy 329 545 555 286 -27.1 -25.1 -26.7 -17.4 -20.0 -19.5 -28.0 -20.4

KEC International Buy 315 415 359 230 -6.0 20.3 33.3 18.8 3.2 29.4 30.9 14.5

Thermax Hold 900 1195 1181 833 -17.4 -11.5 -13.4 -11.9 -9.3 -4.9 -15.0 -15.1

Page 5

EQUITY FUNDAMENTALS REPORT CARD

5March 2020 Sharekhan ValueGuide

STOCK IDEAS STANDING (AS ON MARCH 04, 2020)

COMPANYCURRENT

RECOPRICE AS ON04-MAR-2020

PRICETARGET

52 WEEK ABSOLUTE PERFORMANCE RELATIVE TO SENSEX

HIGH LOW 1M 3M 6M 12M 1M 3M 6M 12M

Triveni Turbine Hold 94 112 123 81 -5.5 -6.3 -8.1 -19.9 3.8 0.7 -9.8 -22.8

V-Guard Industries Buy 203 270 260 192 -7.0 -11.9 -10.1 -8.5 2.1 -5.3 -11.7 -11.8

BSE Power Index 1768 2159 1618 -9.6 -7.3 -10.0 -7.2 -0.7 -0.3 -11.6 -10.6

BSE Capital Goods Index 15392 20387 14249 -11.8 -10.0 -10.3 -12.6 -3.1 -3.2 -11.9 -15.8

Infrastructure / Real estate

Larsen & Toubro Buy 1177 1614 1607 1068 -12.0 -10.2 -12.8 -10.9 -3.4 -3.5 -14.3 -14.1

Sadbhav Engineering Buy 65 120 274 52 -50.1 -51.7 -59.6 -74.4 -45.2 -48.1 -60.3 -75.3

CNX Infra Index 3025 3453 2755 -11.0 -8.8 -2.2 -0.3 -2.2 -1.9 -4.0 -3.9

BSE Real estate Index 2133 2565 1824 -17.5 -5.6 5.2 11.9 -9.3 1.5 3.3 7.8

Oil & gas

Oil India Ltd Buy 110 165 190 89 -19.1 -30.0 -28.1 -39.5 -11.1 -24.7 -29.4 -41.7

Petronet LNG Buy 245 345 296 215 -13.8 -12.3 -9.3 7.4 -5.3 -5.7 -10.9 3.6

Reliance Ind Buy 1340 1850 1618 1095 -12.8 -18.3 4.0 1.0 -4.3 -12.1 2.1 -2.6

BSE Oil and gas Index 12653 15930 11517 -14.4 -16.0 -7.9 -13.5 -6.0 -9.7 -9.6 -16.6

Pharmaceuticals

Aurobindo Pharma Hold 521 600 838 389 0.3 14.9 -17.1 -30.0 10.2 23.5 -18.6 -32.5

Cadila Healthcare Hold 256 300 353 206 -2.6 4.2 11.4 -18.2 7.0 12.1 9.4 -21.2

Cipla Buy 448 540 586 390 -1.2 -4.6 -8.5 -20.2 8.5 2.5 -10.2 -23.1

Divi's Labs Buy 2175 2430 2258 1466 11.6 26.5 37.8 33.7 22.5 36.0 35.3 28.9

IPCA Lab Buy 1429 1590 1541 844 16.9 32.9 55.0 66.6 28.3 42.8 52.2 60.6

Lupin Reduce 664 650 884 621 -8.1 -12.9 -14.2 -15.4 0.9 -6.4 -15.7 -18.4

Sun Pharmaceutical Industries Hold 405 470 484 345 -6.2 -5.8 -5.0 -11.7 3.0 1.3 -6.7 -14.9

Torrent Pharma Hold 2183 ** 2287 1452 9.7 18.6 26.3 22.3 20.5 27.5 24.0 17.9

BSE Health Care Index 14080 14664 11874 -0.4 4.9 8.2 -0.2 9.4 12.8 6.2 -3.8

Building materials

Grasim Hold 690 830 960 625 -17.0 -13.4 -5.5 -18.1 -8.8 -6.9 -7.2 -21.1

Shree Cement Buy 23256 26000 25313 17194 -7.2 14.3 29.9 33.1 1.9 22.9 27.6 28.3

The Ramco Cements Buy 750 875 884 684 -8.5 -7.1 3.2 0.9 0.5 -0.1 1.3 -2.7

UltraTech Cement Buy 4173 5200 4905 3791 -6.7 0.2 6.7 5.0 2.5 7.8 4.7 1.2

Discretionary consumption

Arvind* Buy 37 66 97 33 -14.2 -7.7 -30.2 -57.2 -5.8 -0.8 -31.5 -58.7

Century Plyboards (India) Hold 155 185 222 112 -10.2 -7.3 15.0 -17.1 -1.4 -0.3 12.9 -20.1

Info Edge (India) Hold 2654 2700 3130 1774 -13.7 8.5 29.2 53.3 -5.2 16.6 26.8 47.7

Inox Leisure Buy 381 575 512 249 -10.8 1.0 30.7 26.7 -2.0 8.6 28.3 22.2

Relaxo Footwear # Buy 692 845 830 367 -4.9 16.7 45.7 87.6 4.4 25.5 43.0 80.9

Titan Company Limited Buy 1251 1500 1390 998 -1.3 6.0 16.3 18.2 8.4 14.0 14.2 14.0

Wonderla Holidays Hold 202 270 323 195 -15.7 -16.6 -15.4 -26.7 -7.4 -10.3 -17.0 -29.3

Diversified / Miscellaneous

Bajaj Holdings Buy 3324 4654 3950 2850 -15.6 -6.4 -3.4 0.1 -7.3 0.7 -5.1 -3.5

Bharat Electronics Buy 75 130 122 68 -16.5 -29.2 -33.4 -18.5 -8.3 -23.9 -34.6 -21.4

Bharti Airtel Buy 517 610 569 283 -5.1 16.7 48.6 82.7 4.3 25.5 46.0 76.2

Gateway Distriparks Buy 125 150 154 81 -3.0 27.7 17.6 2.5 6.5 37.3 15.5 -1.2

PI Industries Buy 1576 1750 1629 982 2.0 5.6 30.7 63.9 12.1 13.5 28.3 58.0

Ratnamani Metals and Tubes Buy 1327 1450 1390 830 -0.4 29.0 41.4 47.1 9.4 38.7 38.9 41.8

Supreme Industries Limited Buy 1236 1500 1414 946 -9.0 11.1 13.4 15.3 -0.1 19.5 11.4 11.2

UPL Buy 512 647 709 491 -4.3 -8.6 -9.6 -11.5 5.1 -1.7 -11.2 -14.7

BSE500 Index 14676 16158 13502 -9.4 -6.2 1.9 -0.6 -0.5 0.8 0.1 -4.2

CNX500 Index 9258 10175 8521 -9.3 -6.1 2.0 -0.6 -0.4 1.0 0.1 -4.1

CNXMCAP Index 16746 18496 14976 -9.9 -1.7 5.5 -4.8 -1.0 5.7 3.6 -8.2

* Reco price adjusted for demerger ** Price under review # Reco price adjusted for bonus

Page 6

6March 2020 Sharekhan ValueGuide

Contagion crisis

Stock markets in India and the world over are in a tizzy as the Coronavirus outbreak tightens its

grip day by day. Unfortunately, the outbreak has come at a time when major global economies

have already been slowing down due to US-China trade tariff war and other geopolitical issues

hurting business sentiments. To top it all, the friction between oil producing giants Saudi Arabia

and Russia threaten to bring in additional disruptions in the global economy.

After a seeming recovery seen post the Union Budget 2020, the benchmark indices had a

free-fall, with the Sensex alone losing nearly 1,500 points on the last day of February alone. The

selling pressure has spilled over to March as well.

Indian markets aren’t falling alone. The global environment has turned quite volatile given the

rising risk of a global economic slowdown. The cumulative impact of the Coronavirus and the

subsequent disruption has wiping off almost $8-10 trillion in investor wealth within a period of

few weeks.

In India, the situation is additionally worrisome. The contagion of financial duress threatens to

spread across the Indian financial system. Post the IL&FS meltdown and PMC Bank fiasco, the

banking regulator has stepped in to save one of the large private sector banks from going bust.

However, there is always an opportunity in adversity. In the past, it has been seen that such global

outbreaks have been controlled in a few months and the correction was a great opportunity to

invest.

Particularly in the case of Coronavirus, the general sense from experts is that the spread will

get controlled with the onset of summer as the virus is quite sensitive to heat (does not survive

beyond temperature of 26-28%). Moreover, the death rate is very low in case of Coronavirus at

0.4-0.5% for people below age of 60 years. This is marginally higher than deaths from common

flu in Europe every year.

From an economic perspective, the outbreak of Coronavirus has brought down crude oil prices

by 30% in the last couple of months, which is a huge positive for Indian economy in terms of

fiscal deficit and inflationary pressures. Moreover, central banks across the major regions have

cut interest rates and looking at infusing more cash to support their economy.

From an investor’s perspective, it is important to note that it is not practically possible to catch the

bottom or time the market. Past experience shows that buying after an over 12-15% correction

does give handsome returns over the next 6 to 12 months. Thus, the idea should be to focus on

quality stocks that have corrected by over 15% in a short timeframe and offer a good entry price

point to investors.

Fro

m t

he

Ed

ito

r’s

De

skFrom the Editor’s Desk

Page 7

EQUITY FUNDAMENTALS STOCK IDEA

7March 2020 Sharekhan ValueGuide

Date Company Report TypeRecommendation Reco Price

(Rs.)

Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 06, 2020 Aditya Birla Fashion and Retail Limited New Idea POSITIVE - 254 22-25% -

Summary

• Aditya Birla Fashion and Retail Limited (ABFRL) is one of India’s largest fashion and retail companies with a footprint of 8.1 million

square feet.

• Change in positioning of Pantaloon as fast fashion brand helped company clock strong recovery in the performance, with

revenues growing by 14% over FY2016-19 and OPM improving to 7.2% in FY2019 from 4.8% in FY2016.

• Despite the ongoing slowdown in discretionary spends, ABFRL has posted consistent performance with revenues growing by

~12% and OPM improving by 65 bps in 9MFY2020.

• The stock is trading at a discounted valuation of ~42.8x, lower than its close peers. We re-initiate a viewpoint on the stock and

expect a 20-25% upside from current levels in the next 12 months.

Read report - https://www.sharekhan.com/MediaGalary/Equity/ABRL-Feb06_2020.pdf

Feb 14, 2020 Mayur Uniquoters New Idea POSITIVE - 227 28-30% -

Summary

• We initiate viewpoint coverage on Mayur Uniquoters Ltd (MUL) with a positive view and expect 28-30% upside from current

levels.

• India’s largest manufacturer of synthetic leather, Mayur Uniquoters Limited (MUL) is poised to enter into the high-growth

trajectory.

• Addition of new clients in auto segment and foray into PU (polyurethane) segment to be the key growth drivers. We expect a

robust 13% topline CAGR over FY2020-FY2022.

• MUL has strong return ratios (> 20%) with cash at 20% of marketcap. MUL would generate strong free cash flows of Rs 200 cr

over next three years and is available at attractive P/E of 11.4x FY2021 and 9.5x its FY2022 earnings.

Read report - https://www.sharekhan.com/MediaGalary/Equity/Mayur_Uniquoters_NewIdea-Feb14_2020.pdf

Feb 18, 2020 Triveni Engineering Industries New Idea POSITIVE - 79 25-28% -

Summary

• The expected decline in domestic sugar production by ~20% in SY2019-SY2020 and lower production in key international

markets would keep domestic sugar prices in surge in FY2020-FY2021.

• Triveni Engineering Limited (TEL) is the largest integrated sugar manufacturing company in India. With a capacity of 61,000 TCD,

the company will be one of the key beneficiaries of lower sugar inventory and high sugar prices.

• Debt is expected to come down by Rs. 800 crore-850 crore over FY2019-FY2021 mainly on account of improving cash flows,

driven by lowering of sugar inventory and better profitability.

• We initiate viewpoint on TEL with a Positive view and potential upside of 25-28% from the current level.

Read report - https://www.sharekhan.com/MediaGalary/Equity/Triveni_Engg_NewIdea-Feb19_2020.pdf

� Upgrade � No change � Downgrade

� Note: The arrow indicates change in call and price target, if any, vis-à-vis the previous report

Page 8

EQUITY FUNDAMENTALSSTOCK IDEA

8March 2020 Sharekhan ValueGuide

Sharekhan Limited, its analyst or dependant(s) of the analyst might be holding or having a position in the companies mentioned in the article.

Date Company Report TypeRecommendation Reco Price

(Rs.)

Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 20, 2020 Asian Oilfield Services Limited New Idea POSITIVE - 137 28-30% -

Summary

• We initiate viewpoint coverage on Asian Oilfield Services Limited (AOSL) with a Positive view and expect 28-30% upside

potential.

• AOSL’s strong order book of ~Rs. 997 crore (domestic seismic survey at Rs. 580 crore, O&M at Rs. 210 crore and overseas

oil and gas facilities order at Rs. 207 crore) provides strong earnings growth visibility (expect 33% PAT CAGR over FY2020E-

FY2022E).

• The change of management control to new promoter (Oilmax Energy) in FY2017 has transformed AOSL with net cash of Rs52

crore as on December 2019 vs. net debt of Rs46 crore as on March 2017 and increase in net worth to Rs. 163 crore as on

December 2019 vs. only Rs. 10 crore as on March 2016.

• Open acreage licensing policy provides seismic opportunities worth Rs. 1,500 crore from the oil and gas space. Moreover,

privatisation of the coal sector would bring new opportunities worth Rs. 1,500 crore for seismic surveys.

Read report - https://www.sharekhan.com/MediaGalary/Equity/Asian_Oilfield_NewIdea-Feb20_2020.pdf

Page 9

Stock Update

9March 2020 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation Reco Price

(Rs.)

Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 01, 2020 ITC Stock Update HOLD 219 242

Summary

• Tax rate on cigarette increased by 6-12% depending on the size of the cigarettes; Weight average tax rate increase for ITC

stands at 9%.

• Cigarette sales volume growth continued to remain muted at 2% in Q3FY2020; price increase of ~10% would put further stress

on cigarettes sales volume in the near term.

• We have reduced our earnings estimates to factor in lower-than-earlier expected cigarette sales volume for FY2021 and

FY2022.

• We have downgraded our rating on the stock to Hold with a revised price target of Rs. 242.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/ITC-Feb01_2020.pdf

Feb 03, 2020 Relaxo Footwears Stock Update BUY 721 845

Summary

• Revenue grew by ~9% y-o-y, led by premiumisation, a favourable product mix and good growth across the brand portfolio.

• Benign input costs and a better product mix drove up gross margins by 504 bps, while comparable OPM rose by ~180 bps to

15%, owing to operating efficiencies; effect of Ind AS 116 on PBT stood at Rs. 2.2 crore.

• Sustained volume growth, premiumisation, cost efficiencies and wider presence in untapped markets and a higher duty on

imported footwear will drive operating performance in the coming quarters.

• We broadly maintain our estimates for FY2020, FY2021 and FY2022 and maintain a Buy rating on the stock with a revised PT

of Rs. 845.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Relaxo-Feb03_2020.pdf

Feb 03, 2020 V-Guard Industries Stock Update BUY 218 270

Summary

• We retain Buy on V-Guard Industries Limited (V-Guard) with a revised PT of Rs. 270 lowering our valuation multiple due to near

term headwinds and rolling forward it to FY22E earnings.

• V-Guard reported lower than estimated net profit at Rs. 42.9 crore (up 27% y-o-y) on account of muted topline growth (up 5.4%

y-o-y) and lower than expected OPM (due to lower absorption of fixed costs led by muted revenue growth).

• The focus areas of the company will be increasing its non-South presence, expansion into adjacencies and improving efficiencies

which should revive its revenue growth to double digit over the medium term.

• Uncertainties with respect to Coronavirus in Kerala and China (being key supplier for electrical components) can affect near

term earnings.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/V-Guard-Feb03_2020.pdf

� Upgrade � No change � Downgrade

� Note: The arrow indicates change in call and price target, if any, vis-à-vis the previous report

Page 10

Stock Update

10March 2020 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation Reco Price

(Rs.)

Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 03, 2020 Triveni Turbine Stock Update HOLD 99 112

Summary

• We retain our Hold rating on Triveni Turbine Limited (TTL) with a revised PT of Rs. 112 due to near-term uncertainties in terms of

execution, order inflow and rolling forward our valuation multiple to FY2022E earnings.

• In Q3FY2020, revenue was lower than estimates on sluggish performance in domestic markets, although the company reported

better performance in exports. Net earnings were boosted by better operational performance.

• We expect the company to report a revenue and earnings CAGR of 11% and 16%, during FY2019-FY2022E, respectively.

• Order booking grew by 11% y-o-y for Q3FY2020, although order backlog stands lower by ~8% y-o-y.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Tiveni_Turbine-Feb03_2020.pdf

Feb 03, 2020 HDFC Life Insurance Company Viewpoint POSITIVE 566 12-15%

Summary

• HDFC Life is expected to only be impacted marginally by the new norms introduced in the Union Budget.

• The company has relatively lower dependence on investment linked products (~28% of APE), and hence we don’t expect it to

be impacted significantly.

• We have introduced FY22E EV estimates and have adjusted the valuation multiples for the stock under the changed scenario.

• We maintain our Positive view and expect a 12-15% upside from current levels.

Read report - https://www.sharekhan.com/MediaGalary/Equity/HDFC_Life-Feb03_2020.pdf

Feb 03, 2020 Power Grid Corporation of India Viewpoint POSITIVE 188 20-22%

Summary

• We maintain our Positive view on Power Grid Corporation of India Ltd. and expect 20-22% upside as strong order pipeline

provides visibility for sustained earnings growth over the next couple of years. Valuation attractive at 1.3x its FY22E P/BV.

• Strong PAT growth of 15% y-o-y to Rs. 2,654 crore, slightly above our estimates. Asset capitalisation increased to Rs. 5,230 crore

versus Rs. 4,221 crore in Q2FY2020.

• Management reiterated asset capitalisation guidance of Rs. 20,000 crore – Rs. 25,000 crore for FY2020E and target for

FY2021E is at Rs. 15,000 crore. Capex guidance of Rs. 10,500 crore for FY2021E vs. Rs15,000 crore in FY2020E.

• Removal of DDT and decline in capex could result into higher dividend payout.

Read report - https://www.sharekhan.com/MediaGalary/Equity/Power_Grid-Feb03_2020.pdf

Feb 03, 2020 ICICI Prudential Life Insurance Company Ltd Viewpoint POSITIVE 446 12-15%

Summary

• ICICI Prudential Life (IPRU), which has ~70% exposure to investment-linked products such as ULIP, is expected to be impacted

by the new norms.

• IPRU is available at 2.4x its FY2022E EV, which we believe is reasonable given the quality of the franchise and business metrics.

• We believe while the structural story for the insurance sector is intact, near-term stock performance may remain volatile until

clarity emerges.

• We maintain our Positive view on the stock with a revised upside potential of 12-15%.

Read report - https://www.sharekhan.com/MediaGalary/Equity/ICICI_Prud_Life-Feb03_2020.pdf

Page 11

Stock Update

11March 2020 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation Reco Price

(Rs.)

Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 03, 2020 Indian Hotels Company Viewpoint POSITIVE 141 22-25%

Summary

• Consolidated revenue grew by 3.7% y-o-y to Rs. 1,372.7 crore, while standalone revenue rose by 6.5% (driven by 5.6% growth

in the RevPAR).

• Consolidated OPM on a comparable basis improved by 339 bps to 29.6%, led by better performance of the India business and

operating efficiencies.

• Domestic demand-supply gap widened, with room demand growing by 4.7%, while supply increased by just 2.7%; domestic

RevPAR improved to 5.5%.

• Management expects RevPAR to cross 7% in FY2021, which augurs well for hotel industry; we stay Positive on the stock and

expect a 22-25% upside from current levels.

Read report - https://www.sharekhan.com/MediaGalary/Equity/IHCL-Feb03_2020.pdf

Feb 03, 2020 Vinati Organics Ltd Viewpoint NEUTRAL 1,953 6-8%

Summary

• We downgrade Vinati Organics (Vinati) to Neutral and revise the potential upside to 6-8% as demand environment looks

challenging for its key products ATBS and IBB in the near term.

• However, we like the company’s business model from a long-term perspective as it operates in niche segments and has an

exceptional product basket that have a significant market share globally.

• Owing to soft performance and weak demand environment, we cut our earnings estimates for FY2020E/FY2021E/FY2022E by

11%/14%/19%; hence expect revenue and earnings CAGRs of 12.2% and 15.4%, respectively, over FY2019-FY2022E.

• The company delivered soft performance during Q3FY2020 with Revenue, EBITDA and PAT registering a decline of 21%, 22%

and 6% respectively.

Read report - https://www.sharekhan.com/MediaGalary/Equity/Vinati-Feb03_2020.pdf

Feb 04, 2020 Titan Company Stock Update BUY 1,276 1,500

Summary

• Consolidated revenue grew by 11.2% y-o-y driven by a 10.6% growth in the standalone jewellery business and strong growth of

34% and 69% clocked by subsidiaries TEAL and Caratlane, respectively.

• Despite higher gold prices, the company maintained its margins of jewellery business at 13%; overall reported OPM improved

by 74 bps to 12% (comparable OPM stood flat 11.2%).

• The management has guided for an 11-13% growth in the jewellery business in Q4FY2020.

• We have fine-tuned our earnings estimates for FY2021 and FY2022 and maintain our Buy recommendation with a revised PT

of Rs. 1,500.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Titan-Feb04_2020.pdf

Page 12

Stock Update

12March 2020 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation Reco Price

(Rs.)

Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 04, 2020 TVS Motor Stock Update HOLD 455 485

Summary

• We upgrade our recommendation on TVS Motors Ltd (TVSM) to “Hold” from “Reduce” earlier. Our PT stands at Rs 485.

• Q3FY20 results were ahead of our as well as street expectations as the company managed to improve margins despite double

digit fall in topline.

• 2W industry is expected to recover from H2FY21; margin improvement is expected to sustain due to increased localization and

cost control measures.

• We expect TVSM earnings to grow in double digits from FY21 as against flattish earnings expected over FY2018-2020 period.

• We have broadly retained estimates for FY21 and introduced FY22 earnings. Stock currently trades at 20.7x FY22 earnings

which is close to its long term historical average.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/TVS_Motor-Feb04_2020.pdf

Feb 04, 2020 Century Plyboards (India) Stock Update HOLD 169 185

Summary

• We downgrade Century Plyboards (Century) to Hold with a revised PT of Rs. 185, lowering the valuation multiple, led by a lower-

than-expected earnings growth trajectory in the next two years and rolling forward it to FY2022E earnings.

• In Q3FY2020, Century reported muted revenue growth while adjusted OPM surprised positively. Adjusting for a Rs. 45.6 crore

impairment loss, the net profit rose by 68.5% y-o-y.

• The management expects muted revenue growth of 5-6% for FY2020, while OPM are expected to tread higher. GST-related

benefits are expected to accrue at much slower pace.

• MDF/Particle board greenfield capacity expansion to be undertaken post lifting of stay by the UP state government on issued

licenses. The hearing of the case on 13th February, 2020.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/CenturyPly-Feb04_2020.pdf

Feb 04, 2020 Tata Global Beverages Viewpoint POSITIVE 380 22-24%

Summary

• Tata Global Beverages (TGBL) registered mixed numbers in Q3FY2020. Revenues rose by ~3%, driven by a 7% growth in the

India business.

• Benign input prices (Tea and Coffee) led to an almost 200 bps improvement in operating margins to 12.2%.

• The company received NCLT approval for merger of Tata Chemicals’ consumer business with TGBL, which would result in

portfolio expansion and margin accretion over the next two years.

• We have broadly maintained our earnings estimates for FY2021 and FY2022; and retain our Positive view on the stock with a

22-24% upside.

Read report - https://www.sharekhan.com/MediaGalary/Equity/TGBL-Feb04_2020.pdf

Page 13

Stock Update

13March 2020 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation Reco Price

(Rs.)

Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 04, 2020 SRF Limited Viewpoint POSITIVE 3,745 13-15%

Summary

• We maintain our Positive stance of SRF with potential upside of 13-15%.

• Considering 9MFY2020 performance, we have fine tuned our numbers for FY2020E, FY2021E and FY2022E to factor in strong

growth momentum in the chemicals business, improved profitability in the packaging film business and weak performance in

the technical textiles business.

• Considering strong buoyancy in the chemical business, the company has further announced capex of Rs. 304 crore to produce

intermediates for agro chemcials and to debottleneck the HFC capacity.

• Strong Q3 performance led by the chemical segment, wherein revenue grew by 39% and EBIT margin improved by 455 BPS

y-o-y to 17.6%. Overall revenue grew by 2.3% y-o-y, EBITDA margin improved by 384 BPS y-o-y to 21.1%, while tax credit of Rs.

123 crore doubled RPAT to Rs. 343 crore.

Read report - https://www.sharekhan.com/MediaGalary/Equity/SRF-Feb04_2020.pdf

Feb 04, 2020 Affle India Limited Viewpoint POSITIVE 1,798 10-12%

Summary

• We stay Positive on Affle India (Affle) and expect a 10-12% upside in the next 10-12 months.

• Revenue beat in a tough macro environment; margins contract due to higher inventory and data costs and employee expenses.

• Revenue growth momentum in Q4FY2020 on y-o-y basis is expected accelerate on the back of advertisers’ spending spill-over

and lower base effect.

• Management remains confident that the company would deliver at least 25% CAGR of revenue growth till 2025, led by its CPCU

model and expanding scope of products for both consumer and advertisers.

Read report - https://www.sharekhan.com/MediaGalary/Equity/Affle-Feb04_2020.pdf

Feb 05, 2020 Bharti Airtel Stock Update BUY 534 610

Summary

• We maintain our Buy rating on Bharti Airtel with a revised price target (PT) of Rs. 610.

• Steady EBITDA performance, scope for growth in 4G subscribers and improving free cash flows make us optimistic on the stock.

• Revenue beat estimates, led by tariff hikes in Q3; EBITDA margin remained in line with our estimates.

• Given higher consumption of data and recent developments in Indian wireless industry, we believe that the company would

hike tariffs again in 12-18 months.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Bharti_Airtel-Feb05_2020.pdf

Feb 05, 2020 Cipla Stock Update BUY 447 540

Summary

• We maintain our Buy recommendation on the stock with an unchanged PT of Rs. 540.

• Cipla reported muted results for Q3FY2020. PAT missed estimates.

• India business is on strong footing with the management looking to merge all the three segments in the India business under

one, leading to generation of significant synergies.

• Strong new launch line up is expected to drive the US business.

• We expect Cipla’s topline and PAT to clock a CAGR of 13% and 23%, respectively, over the next two years.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Cipla-Feb05_2020.pdf

Page 14

Stock Update

14March 2020 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation Reco Price

(Rs.)

Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 05, 2020 Cadila Healthcare Stock Update HOLD 272 300

Summary

• We retain our Hold Recommendation on Cadila Healthcare Limited (Cadila) with a revised PT of Rs 300.

• Cadila reported weak results for Q3FY2020.

• We expect regulatory issues at the Moraiya plant to overweigh on the stock until completely resolved. The management has

stopped production at Moraiya Plant and is in midst of a site transfer to Liva.

• We expect the Sales and PAT to grow at a CAGR of 9.5% and 10% respectively over the next two years.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Cadila-Feb05_2020.pdf

Feb 05, 2020 Thermax Stock Update HOLD 1,074 1,195

Summary

• We retain our Hold rating on Thermax with an unchanged PT of Rs. 1,195 on account of a cautious outlook in order tendering.

• In Q3FY20, Thermax achieved steady execution and operating margins improved. A lower effective tax rate pulls up net profit.

• Weak order inflow barring one large FGD order for Q3FY2020 and modest execution during the same period depleted the exit

order backlog to 0.8x TTM consolidated revenues.

• Management expects better ordering both in its energy and environment segments as the enquiries pipeline remains positive

in domestic as well as international markets.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Thermax-Feb05_2020.pdf

Feb 05, 2020 Apollo Tyres Stock Update BUY 168 200

Summary

• We upgrade our recommendation on Apollo Tyres Ltd (ATL) to “Buy” from “Hold. Our PT stands at Rs 200.

• Domestic market is expected to recover from FY21 driven by improved economy and increased infrastructure investment by

Government.

• Margins are expected to improve driven by soft commodity prices and ramp up at Hungary plant.

• We expect ATL to report strong 28% earnings CAGR over the next two years as against earnings drop expected in FY20.

• We introduce FY22 estimates and rollover our target multiple of 12x on FY22 earnings.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Apollo_Tyres-Feb05_2020.pdf

Feb 05, 2020 Max Financial Services Stock Update BUY 484 590

Summary

• Max Financial Services (MFS) posted modest numbers for Q3FY2020, with steady business growth but moderating margin. The

life insurance business, MLIC saw GWP increasing by 10.1% y-o-y.

• Valuation for MFS appears attractive and is at a significant discount compared to some of the listed bank-owned insurance

players.

• We find that there are significant long-term positives in the strong operational numbers for the company.

• We maintain our Buy rating with an unchanged PT of Rs. 590.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Max-Feb05_2020.pdf

Page 15

Stock Update

15March 2020 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation Reco Price

(Rs.)

Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 05, 2020 Jyothy Laboratories Stock Update HOLD 145 175

Summary

• Jyothy Laboratories (JLL) registered yet another quarter of subdued numbers in Q3FY2020 with revenues declining by ~6%

(while volumes fell by 5.6%) and OPM declining by 30 bps y-o-y.

• Revenues fell by around 4% mainly because of a one-off moderation in institutional sales.

• The management expects revenue growth to get back to 4-5% in Q4FY2020 with OPM remaining stable on y-o-y basis.

• We have reduced our earnings estimates for FY2020 and FY2021 to factor in lower than expected performance; we maintain

Hold with a revised PT of Rs. 175.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Jyothi_Lab-Feb05_2020.pdf

Feb 05, 2020 Zydus Wellness Stock Update HOLD 1,435 1,575

Summary

• After consolidation of Heinz portfolio, revenue growth was muted at 4-5% on like-to-like basis, affected by sustained demand

slowdown and seasonality in the portfolio.

• Profitability was affected due to change in revenue mix (lesser contribution from high-margin products) and higher input prices

(including milk and palm oil prices).

• Sales and distribution integration with Heinz has been over and the benefits of integration will start flowing from FY2021.

• We have reduced our earnings estimates for FY2020 and FY2021 to factor in lower-than-earlier expected margins and maintain

our Hold rating with a revised PT of Rs. 1,575.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Zydus-Feb05_2020.pdf

Feb 05, 2020 Exide Industries Viewpoint POSITIVE 186 20-22%

Summary

• Exide Industries Ltd (Exide) Q3 results were in line on the operating front. Higher other income led to Profit beat.

• We expect Exide to report healthy 7% topline growth over the next two years driven by recovery in Auto OEM and improved

traction in industrial segment.

• New focus areas such as e-rickshaws and solar power would aid in topline growth.

• We retain positive view and expect 20-22% upside. Valuations at 12.5x FY22 earnings are attractive and lower than long term

historical average of 17x.

Read report - https://www.sharekhan.com/MediaGalary/Equity/Exide-Feb05_2020.pdf

Feb 05, 2020 Gujarat Gas Limited Viewpoint POSITIVE 296 13-15%

Summary

• Q3FY20 operating profit/PAT at Rs. 371 crore/Rs197 crore, rose by 15%/31% y-o-y and were above our estimates due to a better-

than-expected EBITDA margin, higher other income and lower interest cost.

• Q3FY20 exit gas sales volume run-rate at 10 mmscmd; Management guided for 8% annual volume growth outlook for next

couple of years.

• Development of six new geographical areas and environmental push to curb pollution would lead to next leg of volume growth.

• We stay Positive on Gujarat Gas and expect a 13-15% upside given strong volume led earning growth visibility.

Read report - https://www.sharekhan.com/MediaGalary/Equity/Gujarat_Gas-Feb05_2020.pdf

Page 16

Stock Update

16March 2020 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation Reco Price

(Rs.)

Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 05, 2020 Mahindra Logistics Limited Viewpoint NEUTRAL 400 3-5%

Summary

• We retain a Neutral view on Mahindra Logistics Limited (MLL) on account of a material cut in net earnings for FY2020-FY2021

and a challenging business outlook for the medium term.

• Q3 net earnings continued to be affected by a slowdown in the auto sector, dragging down revenue, while increased overheads

eroded adjusted OPM, dragging net profit by 19% y-o-y.

• MLL added 1.2msf of warehousing capacity during 9MFY2020 taking the total warehouse space to 16.5 msf.

• Focus areas to be higher non-auto revenue, speeding up freight forwarding business, enhancing value added services, being

asset-light, increasing leased warehousing space and investment in technology.

Read report - https://www.sharekhan.com/MediaGalary/Equity/Mahindra_Logistic-Feb05_2020.pdf

Feb 06, 2020 Hero MotoCorp Stock Update HOLD 2,412 2,750

Summary

• Q3FY2020 results were better than our as well as street estimates as operating margins surprised positively. Cost control

measures, soft commodity prices and better mix helpled in margin expansion.

• Hero expects industry demand to remain weak in the next 2-3 quarters due to steep cost increases (12-15%) on account of

transition to BS6 emission norms.

• Hero expects sustained recovery to take time and expects recovery from H2FY21 driven by improved economic growth and

higher rabi sowing.

• We retain Hold rating on the stock with a revised PT of Rs. 2,750. PE of 13.4x FY22 earnings is close to historical average of

15-16x.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/HeroMoto_Corp-Feb06_2020.pdf

Feb 06, 2020 Divi’s Laboratories Stock Update BUY 2,023 2,200

Summary

• We maintain our Buy rating on Divis Laboratories (Divis) with a revised PT of Rs. 2,200.

• Divis Q3FY2020 numbers were soft, but management maintained revenue growth guidance of 10% for FY2020, pointing to a

sturdy topline growth in Q4FY2020.

• Long-term growth to remain healthy, led by backward integration, aggressive capacity expansion, outsourcing potentials and

opportunities in China.

• We expect the company to report a sales and profit CAGR of 20% and 22%, respectively in the next two years.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/DiviLab-Feb06_2020.pdf

Feb 06, 2020 Federal Bank Stock Update BUY 93 110

Summary

• We maintain Buy rating on Federal Bank with a revised target price of Rs 110..

• The stock trades at inexpensive valuations and offers scope of re-rating as the earnings cycle recovers.

• The bank posted strong results for Q3 FY20 with a sharp decline in net stressed loans to ~2.3% of loans (down by 14 BPS q-o-q)

in Q3 FY20, helped by the resolution of a large restructured account in the airline sector.

• We believe incremental loans to better-rated borrowers, no addition to the stressed pool, and high provision coverage are

positives, but asset-quality performance and margins will continue to be key monitorables.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/FederalBank-Feb06_2020.pdf

Page 17

Stock Update

17March 2020 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation Reco Price

(Rs.)

Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 06, 2020 Ratnamani Metals & Tubes Stock Update BUY 1,276 1,450

Summary

• We maintain our Buy rating on Ratnamani Metals & Tubes Limited (RMTL) with a revised PT of Rs. 1,450.

• We remain Positive on RMTL due to its strong balance sheet and its ability to generate superior return ratios despite capacity

expansion programmes.

• The management provides an encouraging outlook which will help in healthy order intake in coming quarters. Margin guidance

to remain in the range of 16-17%.

• RMTL reported a mixed quarter with beat on revenue, while margin was below expectation owing to a higher share of low

margin line pipes.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Ratnamani-Feb06_2020.pdf

Feb 06, 2020 Greaves Cotton Stock Update HOLD 140 155

Summary

• Greaves results were ahead of estimates as margins surprised positively. Margins improved on yoy basis despite fall in the

topline.

• Going ahead, we expect volume pressure to sustain as diesel 3W engines are expected to fall in FY21 due to steep cost

increases post BS6 emission norm.

• Drop in diesel 3W volumes would offset the strong growth in electric scooters and aftermarkets and we expect GCL volumes

to be flattish for FY2021.

• We retain Hold rating on the stock with revised PT of Rs 155 as we rollover to FY22 estimates. At CMP, stock is trading at P/E of

16.6x FY22 earnings which is close to long term historical average.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Greaves_Cotton-Feb06_2020.pdf

Feb 06, 2020 Hindustan Petroleum Corporation Limited Viewpoint POSITIVE 243 12-15%

Summary

• Q3FY20 PAT, at Rs. 747 crore (up 2.4x y-o-y, down 28.8% q-o-q) lagged our estimates due to a miss in refining margins and

lower refining throughput. Core GRM was weak at $1.5/bbl (down 43% q-o-q).

• Recent decline in crude oil prices are expected to lower fuel under-recoveries and thus reduce working capital burden for

OMCs.

• HPCL’s FY21E EV/EBITDA of 6.1x is at a steep discount of 34% versus that of BPCL. Tactical opportunity arising out of the

government’s divestment plan could deliver healthy returns in the next 8-12 months given a potential re-rating.

• Hence, we maintain our Positive view on HPCL and expect a 12-15% upside from current levels.

Read report - https://www.sharekhan.com/MediaGalary/Equity/HPCL-Feb06_2020.pdf

Page 18

Stock Update

18March 2020 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation Reco Price

(Rs.)

Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 06, 2020 Indraprastha Gas Limited Viewpoint POSITIVE 522 10-12%

Summary

• We maintain our Positive view on Indraprastha Gas Limited (IGL) and expect 10-12% upside as lower domestic gas prices and

regulatory push are expected to drive margin expansion and volume growth.

• Q3FY2020 PAT at Rs. 284 crore (up 43.4% y-o-y) was ahead of our estimate due to beat in gas sales volume at 6.7 mmscmd (up

13.4% y-o-y), EBITDA margin at Rs. 6.4/scm (up 8.1% y-o-y) and higher-than-expected other income.

• CNG and PNG volume was up by 11.6% and 18.4% y-o-y respectively in Q3FY2020.

• IGL’s premium valuation of 26.8x its FY2022E EPS as compared to its peers to sustain supported by superior volume growth

visibility.

Read report - https://www.sharekhan.com/MediaGalary/Equity/IGL-Feb06_2020.pdf

Feb 06, 2020 PNC Infratech Limited Viewpoint POSITIVE 195 18-20%

Summary

• We retain our Positive view on PNC Infratech (PNC) with 18-20% upside potential on account of strong net earnings growth

visibility of a 35% CAGR over FY2019-FY2021E, led by a 38% CAGR in execution.

• In Q3FY2020, PNC maintained strong execution with 67.5% y-o-y standalone net revenue growth, stable OPM and net earnings

growth of 63% y-o-y.

• PNC maintained 60% y-o-y revenue growth guidance for FY2020 and expects 18-20% revenue growth for FY2021. Order inflow

guidance stays at Rs. 6,000 crore-7,000 crore despite Rs. 1,000 crore plus order inflows for fiscal year till date.

• We expect PNC to be one of the beneficiaries from the government’s Rs. 103 lakh crore infrastructure investment planned till

2025.

Read report - https://www.sharekhan.com/MediaGalary/Equity/PNC_Infra-Feb06_2020.pdf

Feb 06, 2020 Sudarshan Chemicals Industries Viewpoint POSITIVE 480 10-12%

Summary

• We reiterate our Positive view on Sudarshan Chemical Industries Limited (SCIL) with a potential upside of 12-15%.

• The company is likely to deliver healthy revenue and earnings CAGR of 14.1% and 28.8%, respectively, over FY2019-FY2022E.

• Growth momentum to continue as capex plans are on track and likely to contribute significantly in FY2021E.

• The company delivered healthy performance in Q3FY2020, ahead of expectation. Revenue/adjusted EBITDA and adjusted PAT

increased by 8%/67% and 86% y-o-y, respectively.

Read report - https://www.sharekhan.com/MediaGalary/Equity/Sudarshan-Feb06_2020.pdf

Feb 07, 2020 UPL Stock Update BUY 543 647

Summary

• We have upgraded our rating on UPL Limited (UPL) to BUY with a revised price target of Rs 647/share as the risk-reward matrix

turns favourable.

• We have fine tuned our numbers for FY2020E and FY2021E and introduced FY2022E estimates and believe that the company

will be able to deliver revenue and earnings CAGR of 10.0% and 29.5% over FY2020-22E.

• The management maintains its guidance of revenue growth of 8-10% & EBITDA growth of 16-20% for FY2020E and expects to

pare down debt by US$ 500 million by the end of Q4FY2020E.

• As the new season kicks off, the management expects the inventory levels to normalise by the end of Q4FY2020E resulting in

improved operating cash flow position leading to debt reduction.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/UPL-Feb07_2020.pdf

Page 19

Stock Update

19March 2020 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation Reco Price

(Rs.)

Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 07, 2020 GlaxoSmithKline Consumer Healthcare Stock Update HOLD 9,238 9,950

Summary

• Revenue grew by 4% y-o-y, driven by a 6% growth in the Health food drinks category; domestic sales volumes grew by 3%..

• Higher milk prices led to 126 bps decline in gross margins; lower employee cost and efficiencies drove up OPM by 212 bps.

• The Chandigarh Bench of the NCLT at its hearing held on February 03, 2020 has reserved its order on the scheme of GSK

Consumer’s merger with Hindustan Unilever (HUL) and the Company is now awaiting the formal order.

• We have broadly maintained earnings estimates for FY2020/21; retain Hold with a revised PT of Rs. 9,950.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/GSK_Consumer-Feb07_2020.pdf

Feb 07, 2020 Aurobindo Pharma Stock Update HOLD 547 600

Summary

• We maintain our Hold recommendation on Aurobindo Pharma Limited (Aurobindo) with a revised PT of Rs. 600.

• Q3FY2020 results were broadly in line with estimates..

• Aurobindo is witnessing elevated scrutiny from the USFDA. More than half of the filling done are from impacted plants and

approvals are likely to be delayed. Regulatory hurdles would overweigh on the stock performance, until successfully resolved.

• We expect the company to report sales and profit CAGRs of 19% and 10%, respectively, in the next two years.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Aurobindo-Feb07_2020.pdf

Feb 07, 2020 Punjab National Bank Stock Update HOLD 59 65

Summary

• Punjab National Bank (PNB) posted weak Q3FY2020 performance, with muted business growth and weak asset quality.

• PNB currently trades at <0.5x its FY2022E book value, which reflects concerns on its asset-quality outlook and sluggish loan

growth prospects.

• We have introduced FY2022E estimates in this report.

• We maintain our rating to Hold with a revised PT of Rs. 65.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/PNB-Feb07_2020.pdf

Feb 07, 2020 KEC International Stock Update BUY 347 415

Summary

• We maintain a Buy rating on KEC International Limited (KEC) with a revised price target of Rs. 415 revising our valuation multiple

given a healthy order backlog along with order inflow visibility in international T&D non T&D business and KEC’s ability to ramp-

up execution.

• KEC clocked healthy revenue growth driven by strong execution in T&D (SAE) with stable OPM. Stable operational performance

along with lower tax outgo resulted in strong net earnings growth.

• The management reiterated its guidance for 15% revenue growth with stable OPM for FY20 as it is expected to deliver strong

growth on increased scalability in non-T&D business and stable execution in the T&D business.

• Order book remains healthy providing 1.8x TTM revenues and order inflows for FY20 expected to remain at similar levels as

of FY2019.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/KEC-Feb07_2020.pdf

Page 20

Stock Update

20March 2020 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation Reco Price

(Rs.)

Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 07, 2020 PTC India Stock Update BOOK OUT - 56 - -

Summary

• We drop our coverage on PTC India and recommend Book out as the continued weak performance of financial services arm is

a cause of concern for stock and it also lack positive triggers in the near to medium term.

• Plans to divest stakes in non-core subsidiaries (PTC India Financial Services and PTC Energy) is progressing at slow place and

would take time to materialise given the stress in the NBFC sector (high NPAs and provisions).

• Q3FY20 operating profit (excluding surcharge income) declined 15.6% y-o-y to Rs48 crore due to 11% y-o-y decline in gross

margin (excluding surcharge income) at 3.7 paisa per unit; growth in power trading volume was weak at 1.8% y-o-y.

• Short-term contracted volume fell by 24% y-o-y to 5,228 million units while medium and long-term contracts were up by 31%

y-o-y to 7,924 million units (accounting for 60% of total volumes in Q3FY2020).

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/PTC_India-Feb07_2020.pdf

Feb 07, 2020 NTPC Limited Viewpoint POSITIVE 116 18-20%

Summary

• We maintain our Positive view on NTPC and expect an 18-20% upside given strong earnings growth outlook, attractive valuation

of 0.9x FY21E P/BV and healthy dividend yield of 5-6%.

• The strong commercialization schedule (6GW in FY20E and 5.3GW in FY21E at group level) would drive growth in regulated

equity. This coupled with lower fixed cost under-recoveries to drive earnings 13% PAT CAGR over FY2019-FY2022E.

• NTPC’s Q3FY2020 PAT was by up 25.6% y-o-y (down 8.2% q-o-q) to Rs. 2995, crore, which was marginally ahead of our

estimates. The growth in PAT was driven by lower fixed cost under-recoveries.

• PAF for coal-based power plants improved to 88% in Q3FY2020 versus 85% in Q3FY2019 and 84% in Q2FY2020.

Read report - https://www.sharekhan.com/MediaGalary/Equity/NTPC-Feb07_2020.pdf

Feb 07, 2020 Bata India Viewpoint POSITIVE 1,833 18-20%

Summary

• Bata India’s (Bata) Q3FY2020 revenue grew by 6.5% y-o-y, driven by 4.5% growth in the retail channel and over 20% growth in

the wholesale channel (SSSG stood at ~2%), driven by premiumisation and innovation.

• Operating performance was steady with GPM and comparable OPM expansion of 208 BPS and 30 BPS, respectively; one-time

deferred tax adjustment impacted profitability.

• Store additions, focus on women’s footwear segment and improving contribution from premium end-products will drive

operating performance in the near to medium.

• We have broadly maintained our estimates for FY2021 and FY2022; We retain our Positive view with 18-20% upside from

current levels.

Read report - https://www.sharekhan.com/MediaGalary/Equity/Bata-Feb07_2020.pdf

Page 21

Stock Update

21March 2020 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation Reco Price

(Rs.)

Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 07, 2020 Varun Beverages Viewpoint POSITIVE 843 13-15%

Summary

• Varun Beverages Limited (VBL) ended CY2019 on strong footing with revenues growing by 42%, while PAT rose by 61%; largely

driven by strong volume growth of 45% (organic volume growth of 13%).

• Despite integration of some of the acquired territories in south and west, the OPM improved by 30 bps to 20% in CY2019 and

expected to gradually improve in the coming years.

• We expect organic volume growth of 13-15% to sustain along with strong double-digit growth in the international business.

• We maintain our Positive view on the stock with 13-15% upside from current levels.

Read report - https://www.sharekhan.com/MediaGalary/Equity/VBL-Feb07_2020.pdf

Feb 07, 2020 Trent Limited Viewpoint POSITIVE 663 16-18%

Summary

• Trent delivered strong performance in Q3FY2020 with revenue growth of ~33% driven by consistent SSSG of ~10%.

• Gross margins declined by 240 BPS due to higher discounts and change in revenue mix; reported OPM improved significantly

to 20% due to Ind AS 116.

• We expect the SSSG momentum to sustain in low double digits aided by improving store fundamentals, higher contribution

from private brands and higher investment on brands.

• We have increased our earnings estimates for FY2020, FY2021 and FY2022; we maintain our positive view on the stock with

16-18% upside from current levels.

Read report - https://www.sharekhan.com/MediaGalary/Equity/Trent-Feb07_2020.pdf

Feb 10, 2020 Sun Pharmaceutical Industries Stock Update HOLD 420 470

Summary

• We retain hold recommendation on Sun Pharmaceuticals limited (Sun Pharma) with a revised PT of Rs 470.

• Q3FY2020 results are in line with estimates operationally; however lower other Incomes, high depreciation & tax led to a PAT

miss.

• Going ahead lack of new product launches in the specialty segment, continued higher specialty promotional spends and price

erosion in US base business are likely to weigh on the performance.

• We expect headwinds and overhang to stay and hence despite reasonable valuations we don’t have a constructive view on

Sun Pharma.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Sun_Pharma-Feb10_2020.pdf

Feb 10, 2020 Britannia Industries Stock Update BUY 3,155 3,670

Summary

• Britannia Industries’ (Britannia’s) net revenue grew by ~4% driven by a 2% volume growth and a 2% rise in realisations.

• Despite 3-4% inflation in raw material costs, the company saw gross margins dip by just 44 bps. OPM improved by 94 bps, led

by operating efficiencies and cost-saving initiatives.

• New products/ categories continue to perform well and contributed close to a 2% revenue growth.

• The stock is currently trading at 45.6x and 38.7x its FY2021E and FY2022E earnings; we maintain Buy with a revised PT of Rs.

3,670.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Britannia-Feb10_2020.pdf

Page 22

Stock Update

22March 2020 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation Reco Price

(Rs.)

Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 10, 2020 Grasim Industries Stock Update HOLD 759 830

Summary

• We retain Hold on Grasim Industries Limited (Grasim) with revised PT of Rs. 830 lowering our standalone estimates led by weak

outlook in its key verticals over near to medium term.

• In Q3FY2020, Grasim’s standalone adjusted net profit was affected by weak realizations in both its VSF and chemical divisions

affected by capacity overhang and muted demand environment.

• Grasim’s capacity expansion plan stay on track to benefit over a longer term as the demand environment revives in its standalone

businesses.

• The near-term outlook for viscose and chemical remains challenging due to capacity overhang, soft demand and continuing

U.S.-China trade war.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Grasim-Feb10_2020.pdf

Feb 10, 2020 Emami Stock Update HOLD 293 352

Summary

• Consolidated revenue stood flat at Rs. 813 crore, winter products portfolio affected by delayed season; non-winter product

sales volumes grew by 10%.

• Gross margins improved by 124 bps due to benign raw material costs; OPM stood flat at 32.5% due to higher advertising spends.

• Promoter’s pledged share will reduce to 20% of promoter’s holding from current ~72% post the cement business sale.

• Normal summer to help growth recover in Q4; maintain Hold with unchanged PT of Rs. 352.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Emami-Feb10_2020.pdf

Feb 10, 2020 Union Bank of India Stock Update REDUCE 51 45

Summary

• Q3FY20 numbers were modest as slippages remained elevated, proving to be a dampener on the asset quality side.

• NII grew by 25.7% y-o-y mainly as the bank was expected to emerge from low base last year.

• Despite the large capital infusion by the governmentlast quarter, we believe that the asset quality is still volatile and the

impending merger will be an additional overhang on the stock’s performance.

• We maintain our Reduce rating on the stock with a revised price target (PT) of Rs. 45.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/UBI-Feb10_2020.pdf

Feb 10, 2020 GAIL (India) Limited Viewpoint POSITIVE 122 25-27%

Summary

• GAIL’s Q3FY2020 adjusted operating profit at Rs2,072 crore (down 22.5% y-o-y; up 18.5% q-o-q) was above our estimates due

to higher profitability in natural gas transmission and gas trading business; Adjusted PAT at Rs1,251 crore was marginally above

our estimates.

• Outlook for the core business has improved given expectation of pick-up in gas transmission and trading volume.

• GAIL is trading at trading at an attractive valuation of 4.9x FY2022E EV/EBITDA, which is near its trough valuation and 45%

discount to historical one-year forward EV/EBITDA of 9x).

• Hence, we maintain our Positive view on GAIL and expect 25-27% upside.

Read report - https://www.sharekhan.com/MediaGalary/Equity/GAIL-Feb10_2020.pdf

Page 23

Stock Update

23March 2020 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation Reco Price

(Rs.)

Price Target/ Upside (%)

Latest Chg Latest Chg

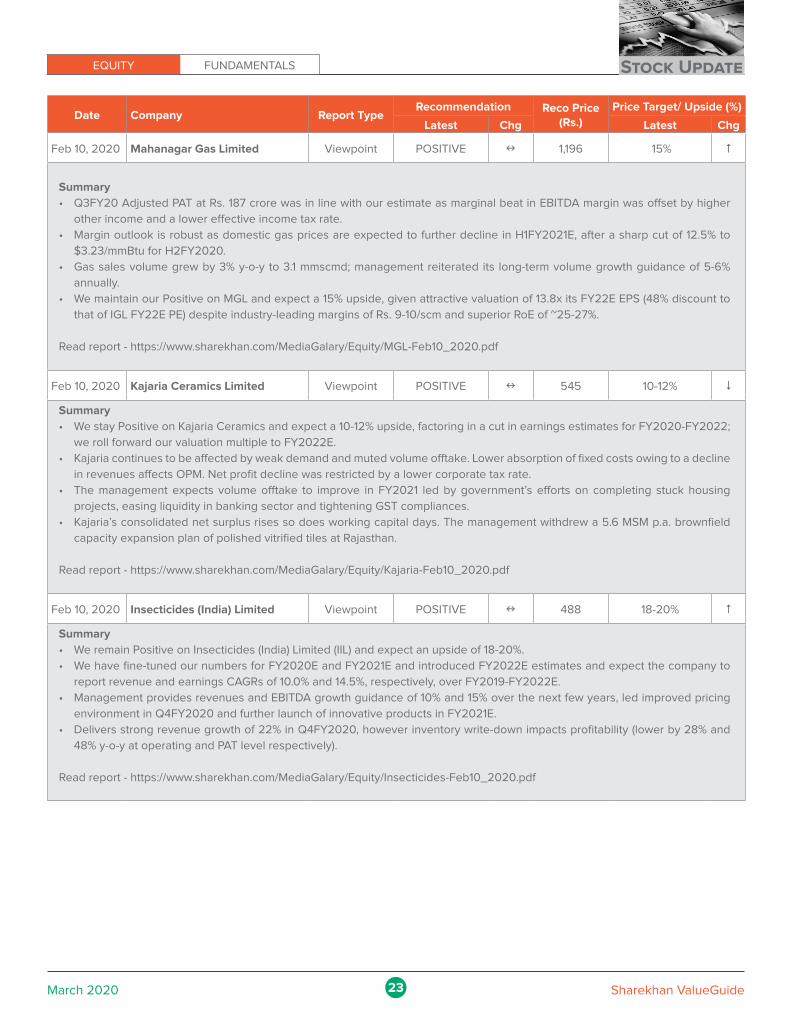

Feb 10, 2020 Mahanagar Gas Limited Viewpoint POSITIVE 1,196 15%

Summary

• Q3FY20 Adjusted PAT at Rs. 187 crore was in line with our estimate as marginal beat in EBITDA margin was offset by higher

other income and a lower effective income tax rate.

• Margin outlook is robust as domestic gas prices are expected to further decline in H1FY2021E, after a sharp cut of 12.5% to

$3.23/mmBtu for H2FY2020.

• Gas sales volume grew by 3% y-o-y to 3.1 mmscmd; management reiterated its long-term volume growth guidance of 5-6%

annually.

• We maintain our Positive on MGL and expect a 15% upside, given attractive valuation of 13.8x its FY22E EPS (48% discount to

that of IGL FY22E PE) despite industry-leading margins of Rs. 9-10/scm and superior RoE of ~25-27%.

Read report - https://www.sharekhan.com/MediaGalary/Equity/MGL-Feb10_2020.pdf

Feb 10, 2020 Kajaria Ceramics Limited Viewpoint POSITIVE 545 10-12%

Summary

• We stay Positive on Kajaria Ceramics and expect a 10-12% upside, factoring in a cut in earnings estimates for FY2020-FY2022;

we roll forward our valuation multiple to FY2022E.

• Kajaria continues to be affected by weak demand and muted volume offtake. Lower absorption of fixed costs owing to a decline

in revenues affects OPM. Net profit decline was restricted by a lower corporate tax rate.

• The management expects volume offtake to improve in FY2021 led by government’s efforts on completing stuck housing

projects, easing liquidity in banking sector and tightening GST compliances.

• Kajaria’s consolidated net surplus rises so does working capital days. The management withdrew a 5.6 MSM p.a. brownfield

capacity expansion plan of polished vitrified tiles at Rajasthan.

Read report - https://www.sharekhan.com/MediaGalary/Equity/Kajaria-Feb10_2020.pdf

Feb 10, 2020 Insecticides (India) Limited Viewpoint POSITIVE 488 18-20%

Summary

• We remain Positive on Insecticides (India) Limited (IIL) and expect an upside of 18-20%.

• We have fine-tuned our numbers for FY2020E and FY2021E and introduced FY2022E estimates and expect the company to

report revenue and earnings CAGRs of 10.0% and 14.5%, respectively, over FY2019-FY2022E.

• Management provides revenues and EBITDA growth guidance of 10% and 15% over the next few years, led improved pricing

environment in Q4FY2020 and further launch of innovative products in FY2021E.

• Delivers strong revenue growth of 22% in Q4FY2020, however inventory write-down impacts profitability (lower by 28% and

48% y-o-y at operating and PAT level respectively).

Read report - https://www.sharekhan.com/MediaGalary/Equity/Insecticides-Feb10_2020.pdf

Page 24

Stock Update

24March 2020 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation Reco Price

(Rs.)

Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 10, 2020 Mastek Limited Viewpoint POSITIVE 417 23-25%

Summary

• We maintain our Positive stance on Mastek Limited and expect a 23-25% upside from current levels.

• Mastek announced the acquisition of Evosys’ Middle East business for $65 million and the merger of Evosys India, US, UK and

RoW businesses for a consideration of 15% of Mastek shares to Evosys’ promoters.

• This deal would allow Mastek to access fast-growing segments, and verticals; also allow Mastek to cross-sale its services as

Evosys has strong 1000+ customers base (100+ customers with revenue of $1 billion+).

• Despite dilution of share, the deal is EPS accretive and will increase our EPS estimates by 14/17% for FY2021/FY2022E

respectively.

Read report - https://www.sharekhan.com/MediaGalary/Equity/Mastek-Feb10_2020.pdf

Feb 11, 2020 Petronet LNG Stock Update BUY 264 345

Summary

• Petronet LNG’s (PLNG’s) Q3FY2020 adjusted operating profit of Rs. 988 crore (up 16.4% y-o-y; down 5.6% q-o-q) was below our

estimate due to a miss in Dahej volume at 222 tBtu (up 12.7% y-o-y). Adjusted PAT at Rs. 730 crore (up 29.1% y-o-y; down 10.8%

q-o-q), exceeded our estimates of Rs. 649 crore.

• Work on the Kochi-Mangalore pipeline is on track and the pipeline is likely to get commissioned by March 2020. Ramp-up

of Kochi terminal’s utilisation rate and further capacity expansion at Dahej to 19.5 mmt would drive volume growth over next

couple of years.

• PLNG’s valuation of 11x FY2022E EPS seems attractive, given a strong volume-led earnings growth visibility (we expect an

EBITDA/PAT CAGR of 13%/8% over FY2020E-FY2022E) and robust RoE of 29-30%.

• We maintain a Buy rating on PLNG with unchanged price target of Rs. 345.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Petronet_LNG-Feb11_2020.pdf

Feb 11, 2020 Mahindra & Mahindra Stock Update BUY 524 665

Summary

• In Q3FY2020, M&M’s margins improved y-o-y despite 6% fall in topline owing to cost-control initiatives, better mix and softening

commodity prices.

• New launches in the utility vehicle segment and conversion of the entire portfolio to petrol would drive auto volumes. Also,

tractor volumes would return to growth trajectory in FY21 due to higher rabi sowing and water reservoir.

• M&M’s volumes would improve substantially and we expect mid-single digit growth in the next two years as against a 9% drop

expected in FY2020.

• We retain our Buy rating on the stock with revised SOTP-based price target PT of Rs. 665 as we rollover to FY22 earnings. P/E

of ~10x FY22 earnings is attractive and below long term average of 15x.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/MnM-Feb11_2020.pdf

Page 25

Stock Update

25March 2020 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation Reco Price

(Rs.)

Price Target/ Upside (%)

Latest Chg Latest Chg

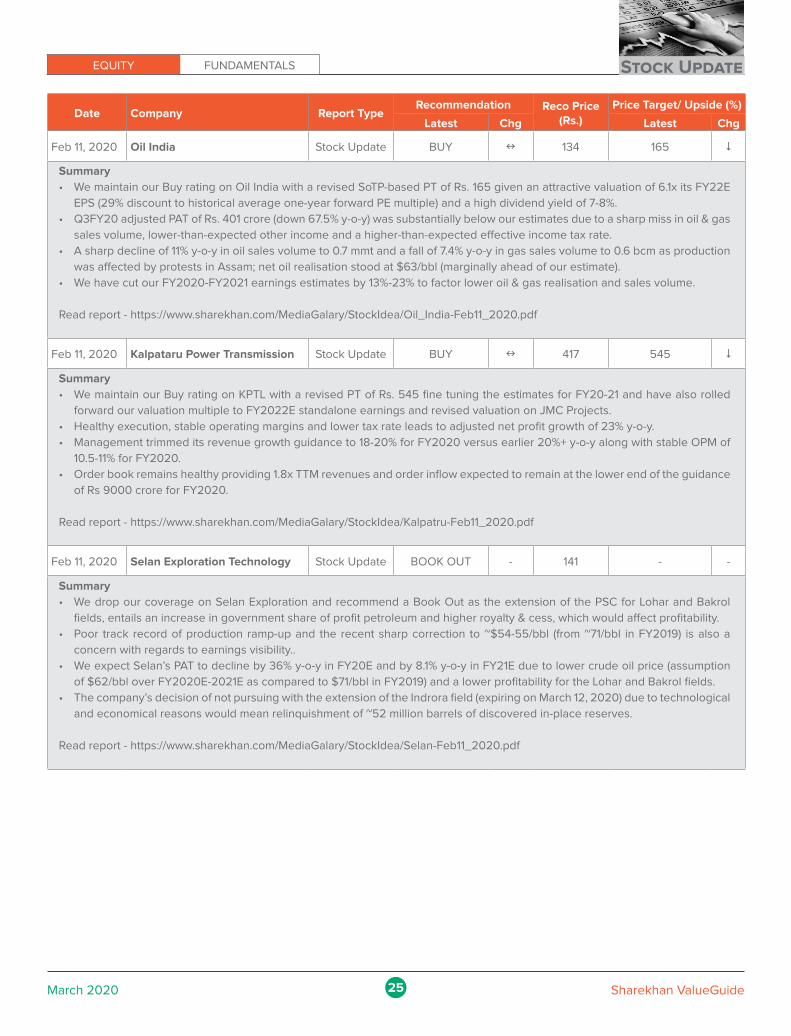

Feb 11, 2020 Oil India Stock Update BUY 134 165

Summary

• We maintain our Buy rating on Oil India with a revised SoTP-based PT of Rs. 165 given an attractive valuation of 6.1x its FY22E

EPS (29% discount to historical average one-year forward PE multiple) and a high dividend yield of 7-8%.

• Q3FY20 adjusted PAT of Rs. 401 crore (down 67.5% y-o-y) was substantially below our estimates due to a sharp miss in oil & gas

sales volume, lower-than-expected other income and a higher-than-expected effective income tax rate.

• A sharp decline of 11% y-o-y in oil sales volume to 0.7 mmt and a fall of 7.4% y-o-y in gas sales volume to 0.6 bcm as production

was affected by protests in Assam; net oil realisation stood at $63/bbl (marginally ahead of our estimate).

• We have cut our FY2020-FY2021 earnings estimates by 13%-23% to factor lower oil & gas realisation and sales volume.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Oil_India-Feb11_2020.pdf

Feb 11, 2020 Kalpataru Power Transmission Stock Update BUY 417 545

Summary

• We maintain our Buy rating on KPTL with a revised PT of Rs. 545 fine tuning the estimates for FY20-21 and have also rolled

forward our valuation multiple to FY2022E standalone earnings and revised valuation on JMC Projects.

• Healthy execution, stable operating margins and lower tax rate leads to adjusted net profit growth of 23% y-o-y.

• Management trimmed its revenue growth guidance to 18-20% for FY2020 versus earlier 20%+ y-o-y along with stable OPM of

10.5-11% for FY2020.

• Order book remains healthy providing 1.8x TTM revenues and order inflow expected to remain at the lower end of the guidance

of Rs 9000 crore for FY2020.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Kalpatru-Feb11_2020.pdf

Feb 11, 2020 Selan Exploration Technology Stock Update BOOK OUT - 141 - -

Summary

• We drop our coverage on Selan Exploration and recommend a Book Out as the extension of the PSC for Lohar and Bakrol

fields, entails an increase in government share of profit petroleum and higher royalty & cess, which would affect profitability.

• Poor track record of production ramp-up and the recent sharp correction to ~$54-55/bbl (from ~71/bbl in FY2019) is also a

concern with regards to earnings visibility..

• We expect Selan’s PAT to decline by 36% y-o-y in FY20E and by 8.1% y-o-y in FY21E due to lower crude oil price (assumption

of $62/bbl over FY2020E-2021E as compared to $71/bbl in FY2019) and a lower profitability for the Lohar and Bakrol fields.

• The company’s decision of not pursuing with the extension of the Indrora field (expiring on March 12, 2020) due to technological

and economical reasons would mean relinquishment of ~52 million barrels of discovered in-place reserves.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Selan-Feb11_2020.pdf

Page 26

Stock Update

26March 2020 Sharekhan ValueGuide