Valuing Quarries & Mines

© 2013 Business Valuation Resources, LLC

© 2013 Business Valuation Resources, LLC

[email protected]

1

VALUING QUARRIES

& MINES

JUNE 2013

© 2013 Business Valuation Resources, LLC

[email protected]

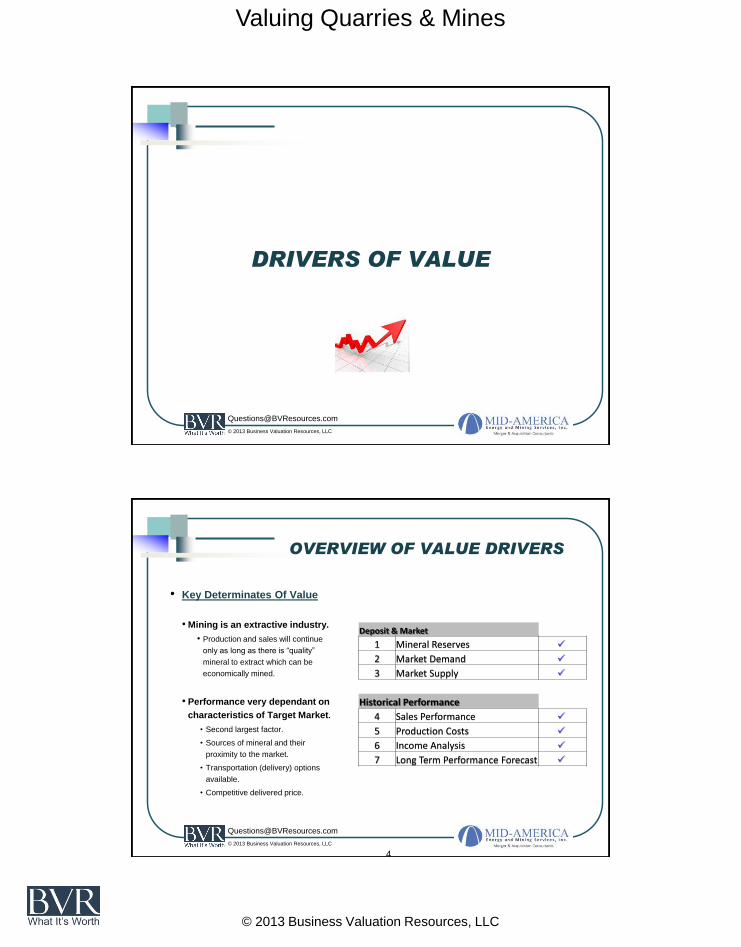

• Today’s Presenters:

• Mike Nowobilski – President Mid-America Energy & Mining Services, Inc.

• Active in Mining Industry since 1976

• Mergers & Acquisitions and Valuations since 1990.

• BS Geology & MBA

• Dwight Davis - Principal Dwight Davis & Associates, PSC

• Active In Mining Industry Since 1977

• Mergers & Acquisitions, Market Analysis and Valuations since 1988

• BS Engineering

• Presentation’s Objectives:

Describe those factors which determine a Quarry’s or Mine’s profitability

(“Valuation Drivers”).

Discuss applicable valuation methodology employed by the mining industry.

2

OBJECTIVES

Valuing Quarries & Mines

© 2013 Business Valuation Resources, LLC

© 2013 Business Valuation Resources, LLC

[email protected]

DRIVERS OF VALUE

© 2013 Business Valuation Resources, LLC

[email protected]

4

OVERVIEW OF VALUE DRIVERS

• Key Determinates Of Value

• Mining is an extractive industry.

• Production and sales will continue

only as long as there is “quality”

mineral to extract which can be

economically mined.

• Performance very dependant on

characteristics of Target Market.

• Second largest factor.

• Sources of mineral and their

proximity to the market.

• Transportation (delivery) options

available.

• Competitive delivered price.

Deposit & Market

1 Mineral Reserves

2 Market Demand

3 Market Supply

Historical Performance

4 Sales Performance

5 Production Costs

6 Income Analysis

7 Long Term Performance Forecast

Valuing Quarries & Mines

© 2013 Business Valuation Resources, LLC

© 2013 Business Valuation Resources, LLC

[email protected]

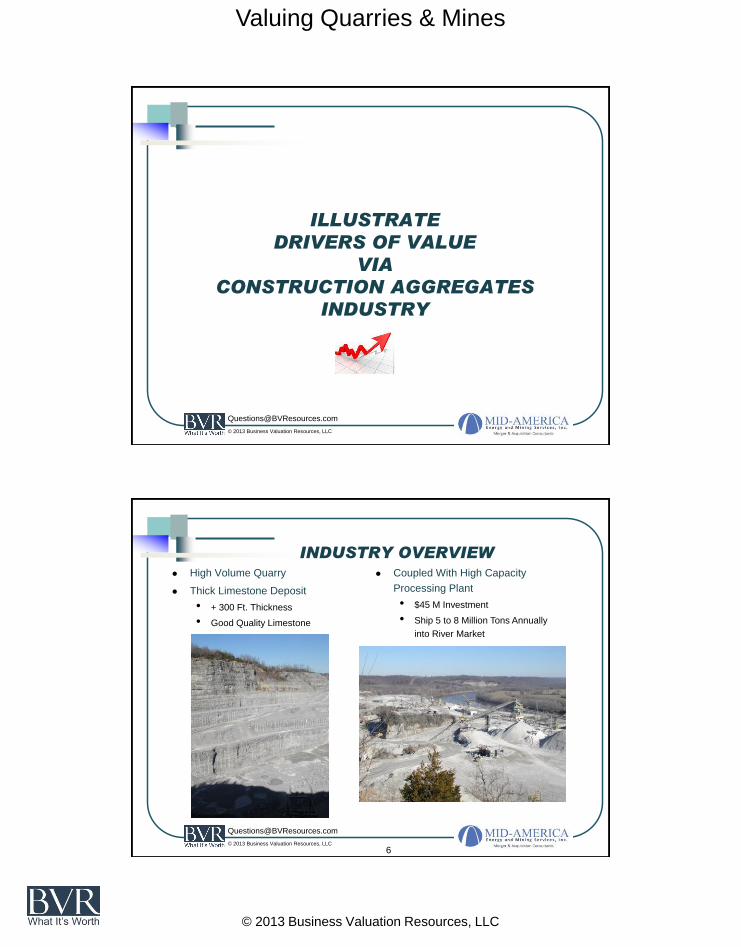

ILLUSTRATE

DRIVERS OF VALUE

VIA

CONSTRUCTION AGGREGATES

INDUSTRY

© 2013 Business Valuation Resources, LLC

[email protected]

6

INDUSTRY OVERVIEW High Volume Quarry

Thick Limestone Deposit

• + 300 Ft. Thickness

• Good Quality Limestone

Coupled With High Capacity

Processing Plant

• $45 M Investment

• Ship 5 to 8 Million Tons Annually

into River Market

Valuing Quarries & Mines

© 2013 Business Valuation Resources, LLC

© 2013 Business Valuation Resources, LLC

[email protected]

7

INDUSTRY OVERVIEW

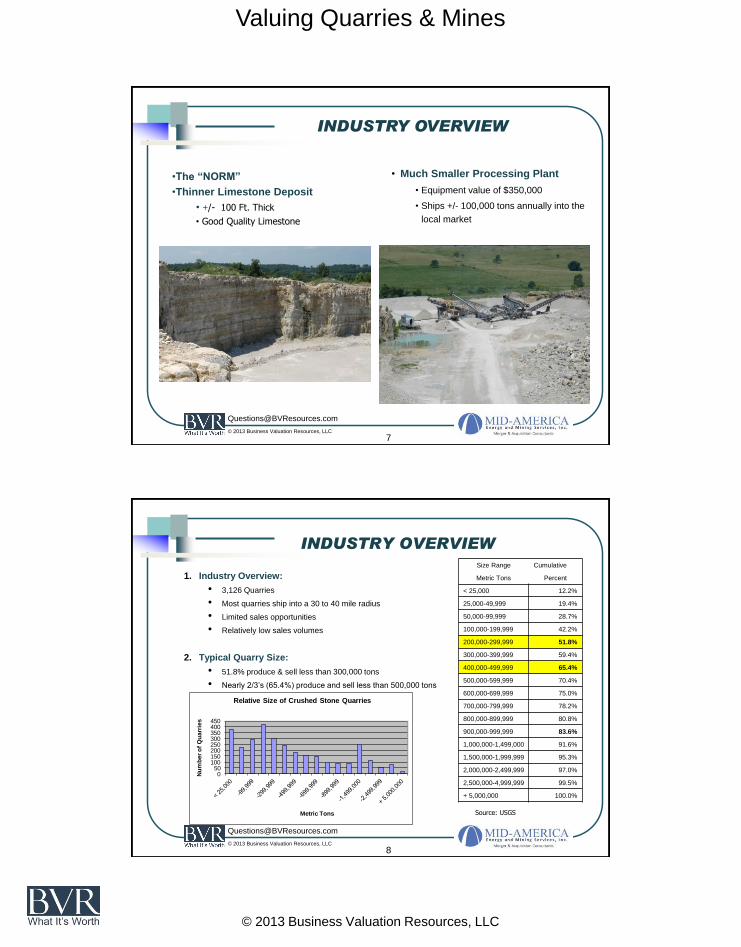

• Much Smaller Processing Plant

• Equipment value of $350,000

• Ships +/- 100,000 tons annually into the

local market

•The “NORM”

•Thinner Limestone Deposit

• +/- 100 Ft. Thick

• Good Quality Limestone

© 2013 Business Valuation Resources, LLC

[email protected]

8

INDUSTRY OVERVIEW

1. Industry Overview:

• 3,126 Quarries

• Most quarries ship into a 30 to 40 mile radius

• Limited sales opportunities

• Relatively low sales volumes

2. Typical Quarry Size:

• 51.8% produce & sell less than 300,000 tons

• Nearly 2/3’s (65.4%) produce and sell less than 500,000 tons

Size Range Cumulative

Metric Tons Percent

< 25,000 12.2%

25,000-49,999 19.4%

50,000-99,999 28.7%

100,000-199,999 42.2%

200,000-299,999 51.8%

300,000-399,999 59.4%

400,000-499,999 65.4%

500,000-599,999 70.4%

600,000-699,999 75.0%

700,000-799,999 78.2%

800,000-899,999 80.8%

900,000-999,999 83.6%

1,000,000-1,499,000 91.6%

1,500,000-1,999,999 95.3%

2,000,000-2,499,999 97.0%

2,500,000-4,999,999 99.5%

+ 5,000,000 100.0%

050

100150200250300350400450

Nu

mb

er

of

Qu

arr

ies

Metric Tons

Relative Size of Crushed Stone Quarries

Source: USGS

Valuing Quarries & Mines

© 2013 Business Valuation Resources, LLC

© 2013 Business Valuation Resources, LLC

[email protected]

#1. MINERAL RESERVES

Deposit & Market

1 Mineral Reserves

2 Market Demand

3 Market Supply

© 2013 Business Valuation Resources, LLC

[email protected]

10

#1. MINERAL RESERVES

• Definition: Economically mineable part of a Measured and/ or Indicated Mineral Resource;

Focus on Mineable with Current Technology and Merchantable at a Reasonable Profit.

• Control: Owned, Leased, Sublease; Zoned or Capable of Being Zoned; Permitted or Capable of

Being Permitted. Option can not be considered as control.

• Classification: Consist of: 1) Proven Reserves has been confirmed by adequate exploration

and testing to confirm geologic and grade continuity and 2) Probable Reserves can be estimated

with a reasonable level of confidence. Does not consist of Resource generally believed to occur

with reasonable prospects for eventual extraction

• Quantity (Mine Life): Size, thickness, shape, depth, mineral content well established and

determined to meet both mineable and merchantable criteria

• Quality: Reserves broken out by appropriate sales criteria; i.e. A Rock, B Rock, C Rock based

on state approval parameters and testing of each and every ledge.

• Cost Structure: Variability across property, overburden increase or decrease, changes of

mining conditions or costs.

• Sufficiency of Reserves: Usually 20 – 25 year minimum mine life

Valuing Quarries & Mines

© 2013 Business Valuation Resources, LLC

© 2013 Business Valuation Resources, LLC

[email protected]

11

#1. MINERAL RESERVES

Reserves Defined by Prior Drilling

• Area East of E, C, G has been previously mined (Active Pit)

• Areas West shows more overburden and thinner limestone thickness

© 2013 Business Valuation Resources, LLC

[email protected]

12

#1. MINERAL RESERVES

Reserve Classification

• Areas in Yellow are Owned Proven Reserves; separated by Prairie Ditch (non-mineable

and access issues)

• Area in Purple is Probable Reserves; no drilling info and late in mine plan

• Resource (general geologic knowledge but not measured)

Valuing Quarries & Mines

© 2013 Business Valuation Resources, LLC

© 2013 Business Valuation Resources, LLC

[email protected]

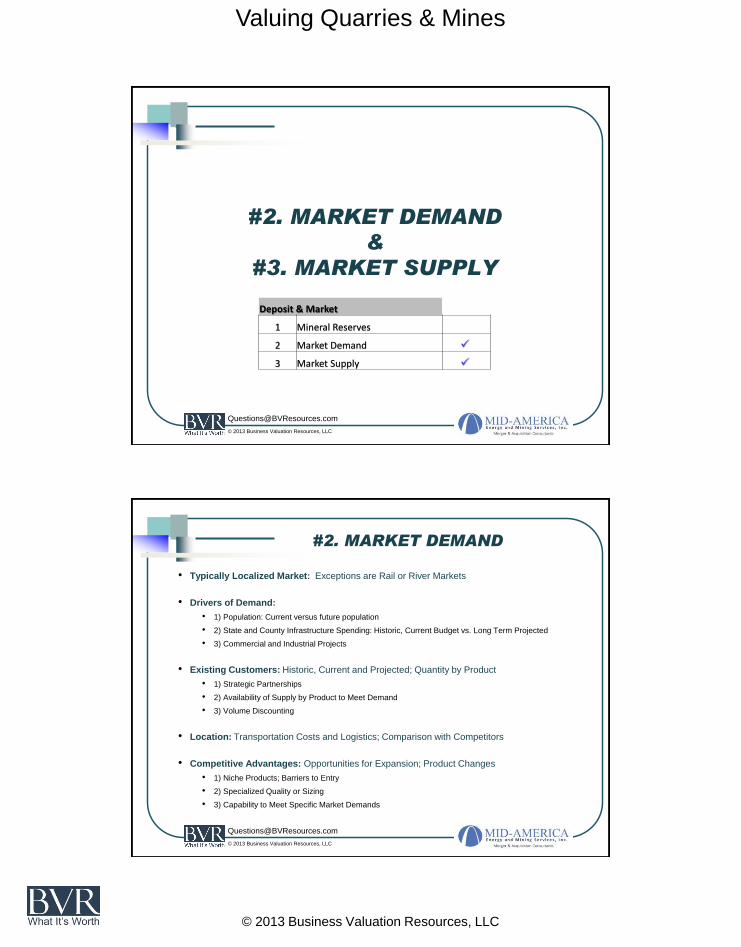

#2. MARKET DEMAND

&

#3. MARKET SUPPLY

Deposit & Market

1 Mineral Reserves

2 Market Demand

3 Market Supply

© 2013 Business Valuation Resources, LLC

[email protected]

#2. MARKET DEMAND

• Typically Localized Market: Exceptions are Rail or River Markets

• Drivers of Demand:

• 1) Population: Current versus future population

• 2) State and County Infrastructure Spending: Historic, Current Budget vs. Long Term Projected

• 3) Commercial and Industrial Projects

• Existing Customers: Historic, Current and Projected; Quantity by Product

• 1) Strategic Partnerships

• 2) Availability of Supply by Product to Meet Demand

• 3) Volume Discounting

• Location: Transportation Costs and Logistics; Comparison with Competitors

• Competitive Advantages: Opportunities for Expansion; Product Changes

• 1) Niche Products; Barriers to Entry

• 2) Specialized Quality or Sizing

• 3) Capability to Meet Specific Market Demands

Valuing Quarries & Mines

© 2013 Business Valuation Resources, LLC

© 2013 Business Valuation Resources, LLC

[email protected]

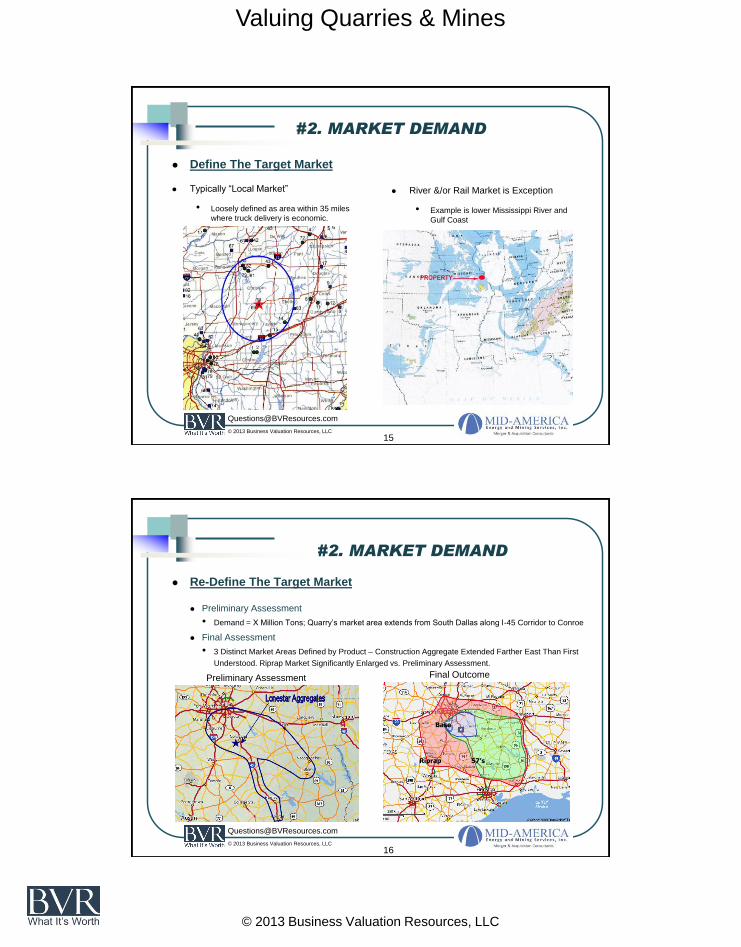

#2. MARKET DEMAND

Define The Target Market

Typically “Local Market”

• Loosely defined as area within 35 miles

where truck delivery is economic.

River &/or Rail Market is Exception

• Example is lower Mississippi River and

Gulf Coast

15

© 2013 Business Valuation Resources, LLC

[email protected]

16

#2. MARKET DEMAND

Re-Define The Target Market

Preliminary Assessment

• Demand = X Million Tons; Quarry’s market area extends from South Dallas along I-45 Corridor to Conroe

Final Assessment

• 3 Distinct Market Areas Defined by Product – Construction Aggregate Extended Farther East Than First

Understood. Riprap Market Significantly Enlarged vs. Preliminary Assessment.

Preliminary Assessment

Final Outcome

Riprap 57’s

Base

Valuing Quarries & Mines

© 2013 Business Valuation Resources, LLC

© 2013 Business Valuation Resources, LLC

[email protected]

17

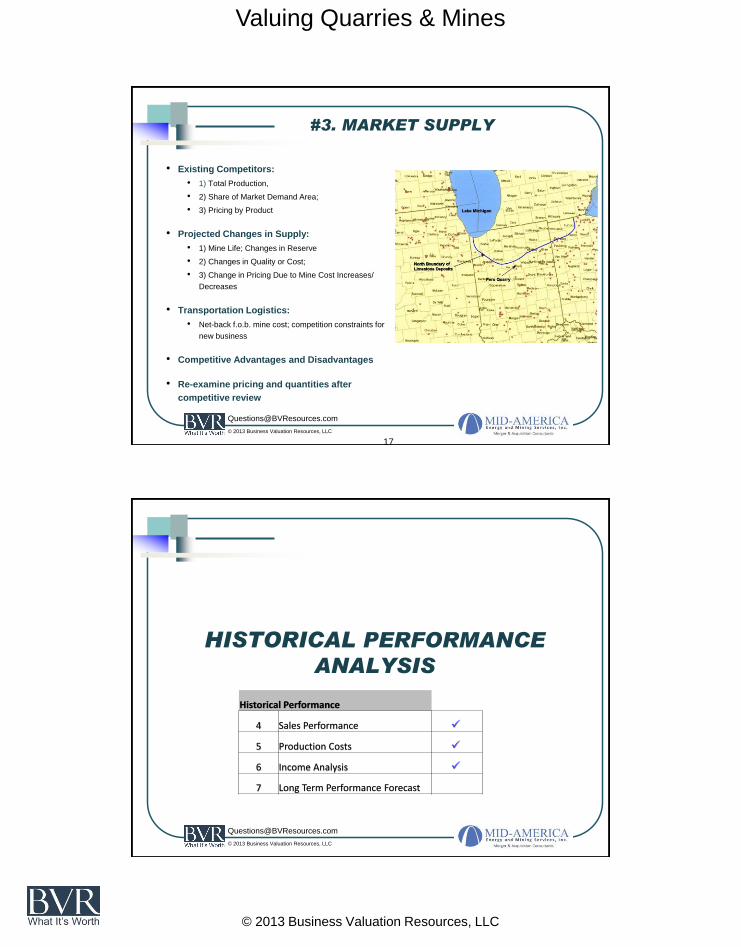

#3. MARKET SUPPLY

• Existing Competitors:

• 1) Total Production,

• 2) Share of Market Demand Area;

• 3) Pricing by Product

• Projected Changes in Supply:

• 1) Mine Life; Changes in Reserve

• 2) Changes in Quality or Cost;

• 3) Change in Pricing Due to Mine Cost Increases/

Decreases

• Transportation Logistics:

• Net-back f.o.b. mine cost; competition constraints for

new business

• Competitive Advantages and Disadvantages

• Re-examine pricing and quantities after

competitive review

© 2013 Business Valuation Resources, LLC

[email protected]

HISTORICAL PERFORMANCE

ANALYSIS

Historical Performance

4 Sales Performance

5 Production Costs

6 Income Analysis

7 Long Term Performance Forecast

Valuing Quarries & Mines

© 2013 Business Valuation Resources, LLC

© 2013 Business Valuation Resources, LLC

[email protected]

• General Rule of Thumb

• Four years of information:

• Balance Sheets, Income Statements & Cash Flow Statements

• Internal Statements

• Plus Audited Financials / Reviewed Financials / Compiled Financials

• Tax Returns

• Sales Information

• Equipment Lists

Objective: Defendable Historical Financials = Defendable Profits/ Cash Flows

• Key Point #1: Recast Sales Revenues & Expenses

• Key Point #2: Eliminate Financing Expenses.

• Assume business and/or assets are sold “Free & Clear of All Liens & Encumbrances”.

19

HISTORICAL PERFORMANCE

OVERVIEW

© 2013 Business Valuation Resources, LLC

[email protected]

20

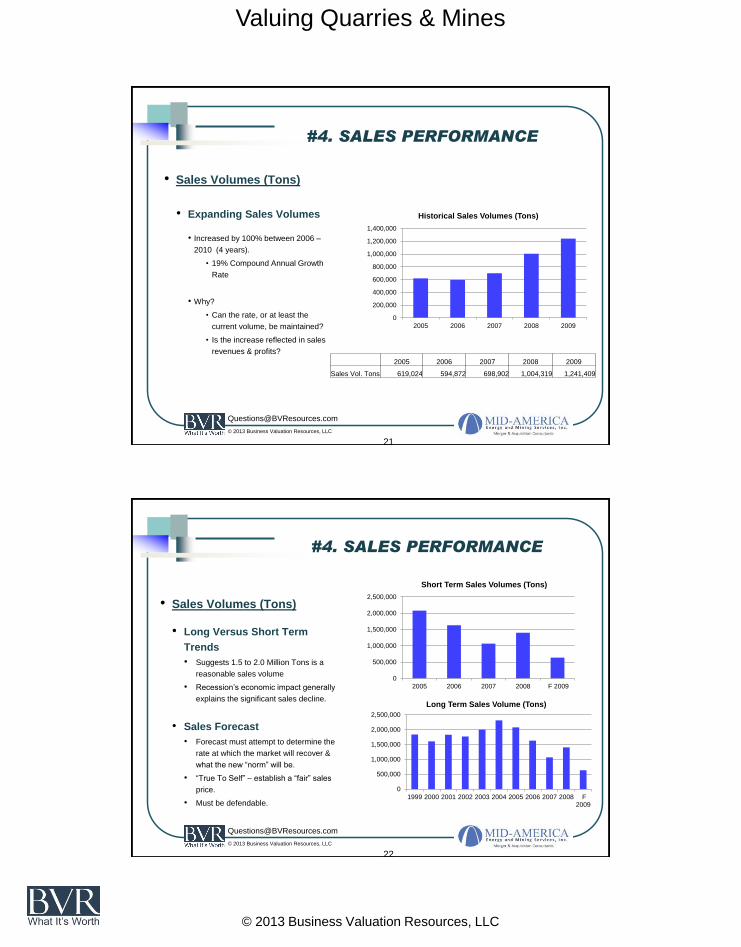

#4. SALES PERFORMANCE

• General Rule of Thumb

• Four years of information:

• Annual Sales Volumes (Tons, Units)

• Annual Sales Revenues

• Average Annual Unit Sales Prices (any price increases?)

• Top 10 Customers’ Sales Detail By Year

• Objective

• Determine Sales Trends

• Growing, stagnant, or declining sales volumes

• Ability to increase sales prices.

• Basis (Justification) For Sales Forecast

Valuing Quarries & Mines

© 2013 Business Valuation Resources, LLC

© 2013 Business Valuation Resources, LLC

[email protected]

21

#4. SALES PERFORMANCE

• Sales Volumes (Tons)

• Expanding Sales Volumes

• Increased by 100% between 2006 –

2010 (4 years).

• 19% Compound Annual Growth

Rate

• Why?

• Can the rate, or at least the

current volume, be maintained?

• Is the increase reflected in sales

revenues & profits?

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

2005 2006 2007 2008 2009

Historical Sales Volumes (Tons)

2005 2006 2007 2008 2009

Sales Vol. Tons 619,024 594,872 698,902 1,004,319 1,241,409

© 2013 Business Valuation Resources, LLC

[email protected]

22

#4. SALES PERFORMANCE

• Sales Volumes (Tons)

• Long Versus Short Term

Trends

• Suggests 1.5 to 2.0 Million Tons is a

reasonable sales volume

• Recession’s economic impact generally

explains the significant sales decline.

• Sales Forecast

• Forecast must attempt to determine the

rate at which the market will recover &

what the new “norm” will be.

• “True To Self” – establish a “fair” sales

price.

• Must be defendable.

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

2005 2006 2007 2008 F 2009

Short Term Sales Volumes (Tons)

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 F2009

Long Term Sales Volume (Tons)

Valuing Quarries & Mines

© 2013 Business Valuation Resources, LLC

© 2013 Business Valuation Resources, LLC

[email protected]

23

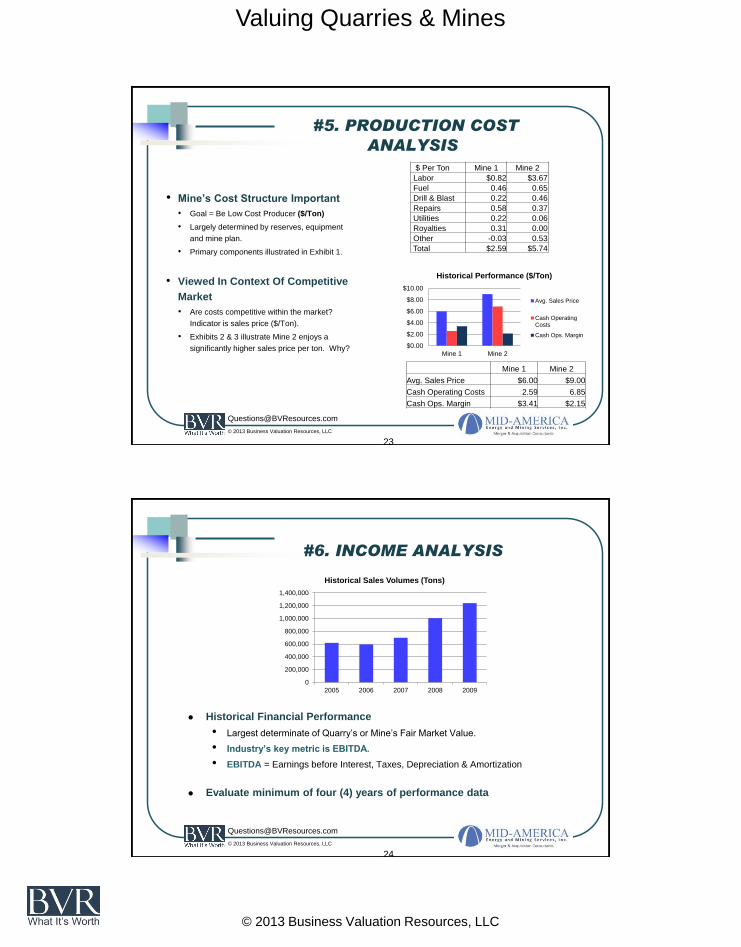

#5. PRODUCTION COST

ANALYSIS

• Mine’s Cost Structure Important

• Goal = Be Low Cost Producer ($/Ton)

• Largely determined by reserves, equipment

and mine plan.

• Primary components illustrated in Exhibit 1.

• Viewed In Context Of Competitive

Market

• Are costs competitive within the market?

Indicator is sales price ($/Ton).

• Exhibits 2 & 3 illustrate Mine 2 enjoys a

significantly higher sales price per ton. Why?

$ Per Ton Mine 1 Mine 2

Labor $0.82 $3.67

Fuel 0.46 0.65

Drill & Blast 0.22 0.46

Repairs 0.58 0.37

Utilities 0.22 0.06

Royalties 0.31 0.00

Other -0.03 0.53

Total $2.59 $5.74

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

Mine 1 Mine 2

Historical Performance ($/Ton)

Avg. Sales Price

Cash OperatingCosts

Cash Ops. Margin

Mine 1 Mine 2

Avg. Sales Price $6.00 $9.00

Cash Operating Costs 2.59 6.85

Cash Ops. Margin $3.41 $2.15

© 2013 Business Valuation Resources, LLC

[email protected]

24

#6. INCOME ANALYSIS

Historical Financial Performance

• Largest determinate of Quarry’s or Mine’s Fair Market Value.

• Industry’s key metric is EBITDA.

• EBITDA = Earnings before Interest, Taxes, Depreciation & Amortization

Evaluate minimum of four (4) years of performance data

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

2005 2006 2007 2008 2009

Historical Sales Volumes (Tons)

Valuing Quarries & Mines

© 2013 Business Valuation Resources, LLC

© 2013 Business Valuation Resources, LLC

[email protected]

25

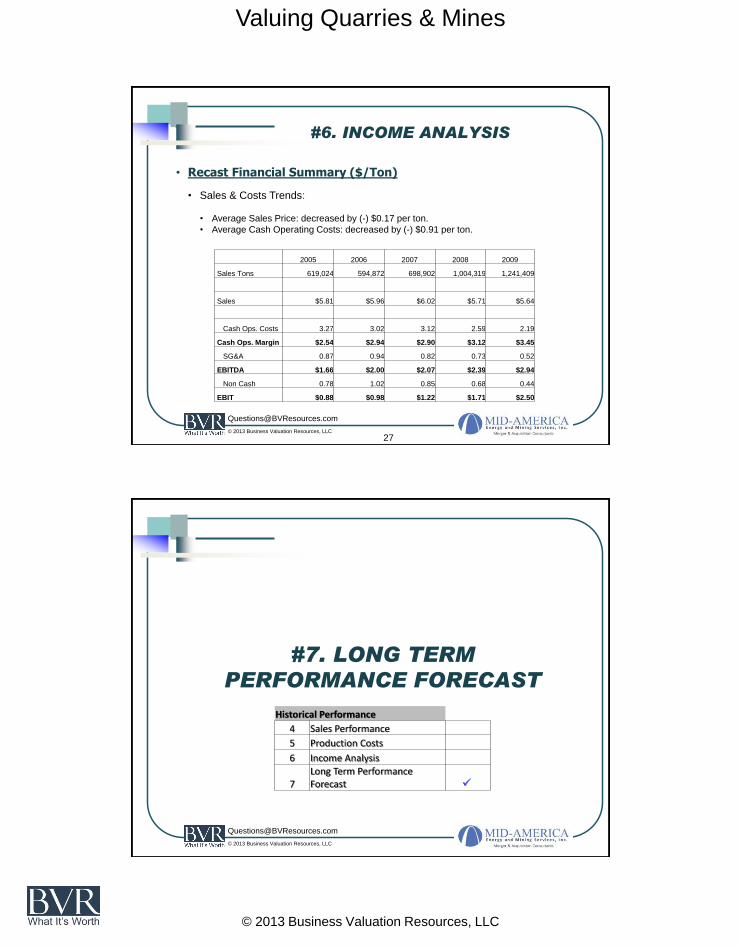

#6. INCOME ANALYSIS

Recast Financial Performance

• Key Observations:

• Sales Revenues increase $3.4 million (+95%)

• Profits (EBITDA) increase $2.6 million (+254%).

• Question ability to maintain growth trajectory.

• Key Observations ($/Ton):

• Sales Revenues decline - $0.17 per ton.

• Cash Operating Costs decline - $1.08 per ton.

• Profits Increase:

• Cash Operating Margin + $0.91 per ton.

• EBITDA + $1.28 per ton.

• Question ability to maintain cost improvements.

$0

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

$7,000,000

$8,000,000

2005 2006 2007 2008 2009

Historical Financial Performance

Revenues

Cash Ops. Margin

EBITDA

EBIT

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

2005 2006 2007 2008 2009

Historical Financial Performance ($/Ton)

Revenues

Cash Ops. Margin

EBITDA

EBIT

© 2013 Business Valuation Resources, LLC

[email protected]

#6. INCOME ANALYSIS

26

2005 2006 2007 2008 2009

Sales Tons 619,024 594,872 698,902 1,004,319 1,241,409

Sales $3,596,670 $3,547,811 $4,207,470 $5,734,813 $7,001,827

Cash Ops. Costs 2,025,896 1,798,128 2,182,725 2,606,111 2,713,197

Cash Ops. Margin $1,570,774 $1,749,683 $2,024,745 $3,128,702 $4,288,630

SG&A 541,497 557,089 576,267 728,157 642,468

EBITDA $1,029,277 $1,192,594 $1,448,478 $2,400,545 $3,646,162

% Sales 28.6% 33.6% 34.4% 41.9% 52.1%

Non Cash 485,227 607,780 592,329 679,279 540,974

EBIT $544,050 $584,814 $856,149 $1,721,266 $3,105,188

% Sales 15.1% 16.5% 20.3% 30.0% 44.3%

• Recast Financial Summary

• EBITDA Trend: EBITDA increased $2.7 million, or 173 percent (173%) during five

year period.

• Recast Performance: Recast sales revenues, operations costs and SG&A expenses.

Valuing Quarries & Mines

© 2013 Business Valuation Resources, LLC

© 2013 Business Valuation Resources, LLC

[email protected]

#6. INCOME ANALYSIS

27

2005 2006 2007 2008 2009

Sales Tons 619,024 594,872 698,902 1,004,319 1,241,409

Sales $5.81 $5.96 $6.02 $5.71 $5.64

Cash Ops. Costs 3.27 3.02 3.12 2.59 2.19

Cash Ops. Margin $2.54 $2.94 $2.90 $3.12 $3.45

SG&A 0.87 0.94 0.82 0.73 0.52

EBITDA $1.66 $2.00 $2.07 $2.39 $2.94

Non Cash 0.78 1.02 0.85 0.68 0.44

EBIT $0.88 $0.98 $1.22 $1.71 $2.50

• Recast Financial Summary ($/Ton)

• Sales & Costs Trends:

• Average Sales Price: decreased by (-) $0.17 per ton.

• Average Cash Operating Costs: decreased by (-) $0.91 per ton.

© 2013 Business Valuation Resources, LLC

[email protected]

#7. LONG TERM

PERFORMANCE FORECAST

Historical Performance

4 Sales Performance

5 Production Costs

6 Income Analysis

7 Long Term Performance Forecast

Valuing Quarries & Mines

© 2013 Business Valuation Resources, LLC

© 2013 Business Valuation Resources, LLC

[email protected]

29

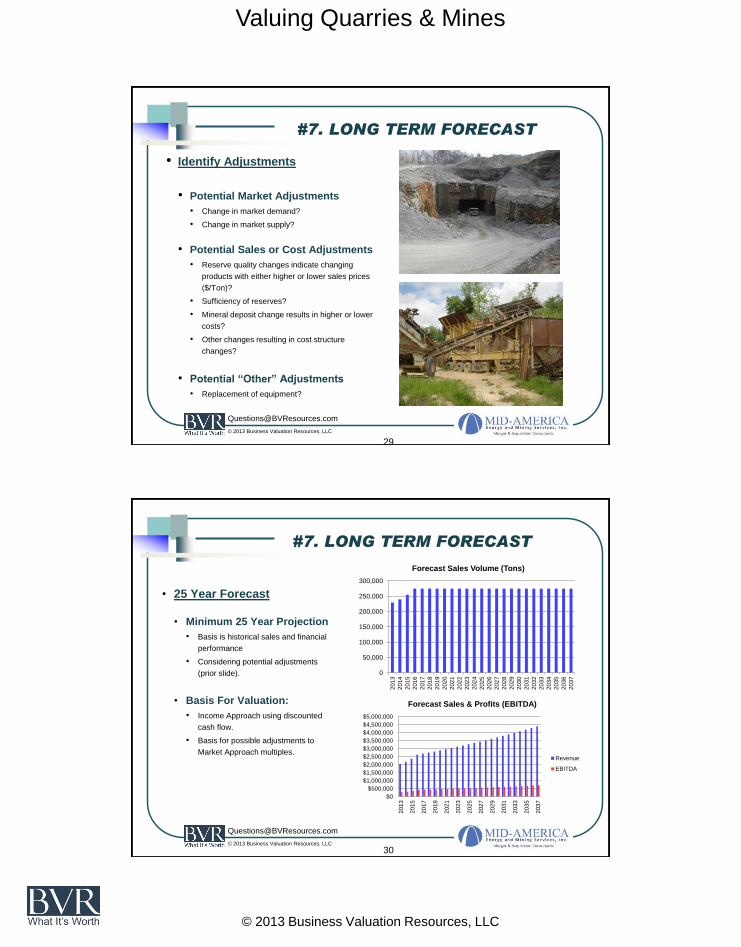

#7. LONG TERM FORECAST

• Identify Adjustments

• Potential Market Adjustments

• Change in market demand?

• Change in market supply?

• Potential Sales or Cost Adjustments

• Reserve quality changes indicate changing

products with either higher or lower sales prices

($/Ton)?

• Sufficiency of reserves?

• Mineral deposit change results in higher or lower

costs?

• Other changes resulting in cost structure

changes?

• Potential “Other” Adjustments

• Replacement of equipment?

© 2013 Business Valuation Resources, LLC

[email protected]

30

#7. LONG TERM FORECAST

• 25 Year Forecast

• Minimum 25 Year Projection

• Basis is historical sales and financial

performance

• Considering potential adjustments

(prior slide).

• Basis For Valuation:

• Income Approach using discounted

cash flow.

• Basis for possible adjustments to

Market Approach multiples.

0

50,000

100,000

150,000

200,000

250,000

300,000

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

202

2

202

3

202

4

202

5

202

6

202

7

202

8

202

9

203

0

203

1

203

2

203

3

203

4

203

5

203

6

203

7Forecast Sales Volume (Tons)

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

$4,500,000

$5,000,000

201

3

201

5

201

7

201

9

202

1

202

3

202

5

202

7

202

9

203

1

203

3

203

5

203

7

Forecast Sales & Profits (EBITDA)

Revenue

EBITDA

Valuing Quarries & Mines

© 2013 Business Valuation Resources, LLC

© 2013 Business Valuation Resources, LLC

[email protected]

VALUING

THE QUARRY OR MINE

© 2013 Business Valuation Resources, LLC

[email protected]

• Textbook Definition of Business Value is:

American Society of Appraisers’ definition of fair market value is “the amount at which property

would change hands between a willing seller and a willing buyer when neither is acting under

compulsion and when both have reasonable knowledge of the relevant facts.”

• Three Primary Valuation Methods:

1. Income Approach

Valued As An On Going Concern

2. Market Approach

Valued As An On Going Concern

3. Asset Based Approach

Valued As Sum Of Asset Values

32

OVERVIEW

Valuing Quarries & Mines

© 2013 Business Valuation Resources, LLC

© 2013 Business Valuation Resources, LLC

[email protected]

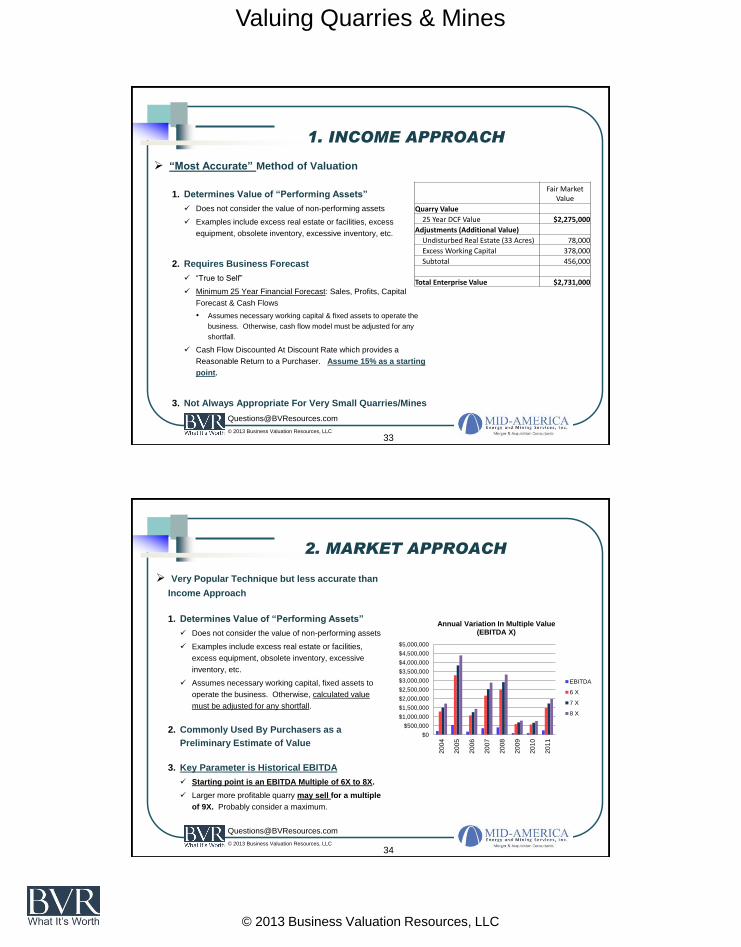

33

1. INCOME APPROACH

“Most Accurate” Method of Valuation

1. Determines Value of “Performing Assets”

Does not consider the value of non-performing assets

Examples include excess real estate or facilities, excess

equipment, obsolete inventory, excessive inventory, etc.

2. Requires Business Forecast

“True to Self”

Minimum 25 Year Financial Forecast: Sales, Profits, Capital

Forecast & Cash Flows

• Assumes necessary working capital & fixed assets to operate the

business. Otherwise, cash flow model must be adjusted for any

shortfall.

Cash Flow Discounted At Discount Rate which provides a

Reasonable Return to a Purchaser. Assume 15% as a starting

point.

3. Not Always Appropriate For Very Small Quarries/Mines

Fair Market

Value

Quarry Value

25 Year DCF Value $2,275,000

Adjustments (Additional Value)

Undisturbed Real Estate (33 Acres) 78,000

Excess Working Capital 378,000

Subtotal 456,000

Total Enterprise Value $2,731,000

© 2013 Business Valuation Resources, LLC

[email protected]

34

2. MARKET APPROACH

Very Popular Technique but less accurate than

Income Approach

1. Determines Value of “Performing Assets”

Does not consider the value of non-performing assets

Examples include excess real estate or facilities,

excess equipment, obsolete inventory, excessive

inventory, etc.

Assumes necessary working capital, fixed assets to

operate the business. Otherwise, calculated value

must be adjusted for any shortfall.

2. Commonly Used By Purchasers as a

Preliminary Estimate of Value

3. Key Parameter is Historical EBITDA

Starting point is an EBITDA Multiple of 6X to 8X.

Larger more profitable quarry may sell for a multiple

of 9X. Probably consider a maximum.

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

$4,500,000

$5,000,000

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Annual Variation In Multiple Value (EBITDA X)

EBITDA

6 X

7 X

8 X

Valuing Quarries & Mines

© 2013 Business Valuation Resources, LLC

© 2013 Business Valuation Resources, LLC

[email protected]

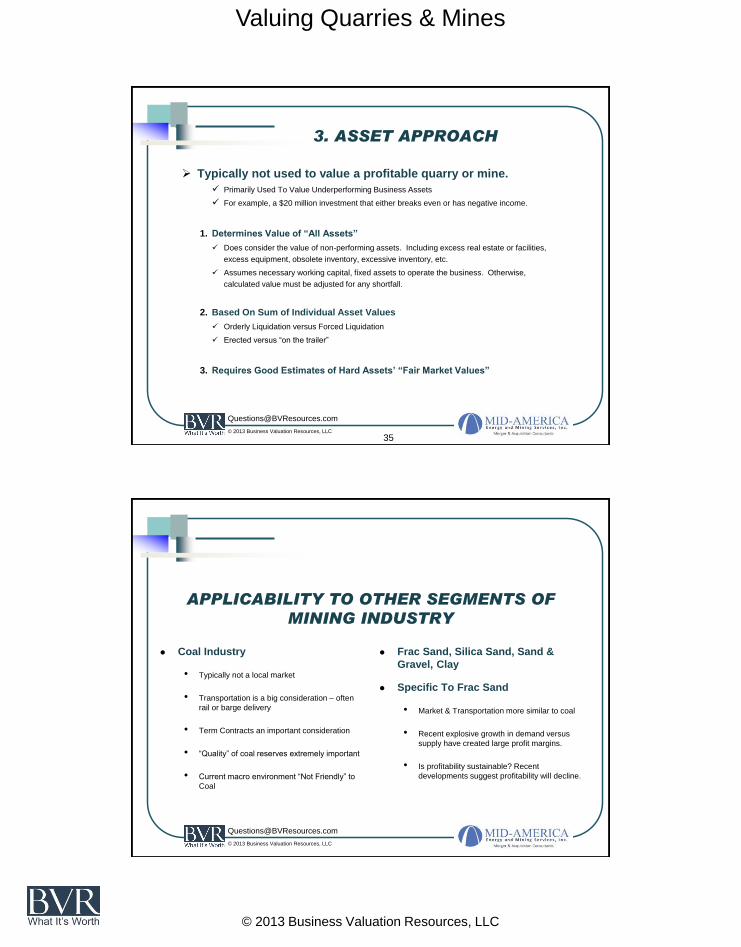

Typically not used to value a profitable quarry or mine.

Primarily Used To Value Underperforming Business Assets

For example, a $20 million investment that either breaks even or has negative income.

1. Determines Value of “All Assets”

Does consider the value of non-performing assets. Including excess real estate or facilities,

excess equipment, obsolete inventory, excessive inventory, etc.

Assumes necessary working capital, fixed assets to operate the business. Otherwise,

calculated value must be adjusted for any shortfall.

2. Based On Sum of Individual Asset Values

Orderly Liquidation versus Forced Liquidation

Erected versus “on the trailer”

3. Requires Good Estimates of Hard Assets’ “Fair Market Values”

35

3. ASSET APPROACH

© 2013 Business Valuation Resources, LLC

[email protected]

APPLICABILITY TO OTHER SEGMENTS OF

MINING INDUSTRY

Coal Industry

• Typically not a local market

• Transportation is a big consideration – often

rail or barge delivery

• Term Contracts an important consideration

• “Quality” of coal reserves extremely important

• Current macro environment “Not Friendly” to

Coal

Frac Sand, Silica Sand, Sand &

Gravel, Clay

Specific To Frac Sand

• Market & Transportation more similar to coal

• Recent explosive growth in demand versus

supply have created large profit margins.

• Is profitability sustainable? Recent

developments suggest profitability will decline.

Valuing Quarries & Mines

© 2013 Business Valuation Resources, LLC

© 2013 Business Valuation Resources, LLC

[email protected]

37

MIKE NOWOBILSKI

Mike Nowobilski

Professional Profile

INTRODUCTION

Mr. Nowobilski founded Mid-America Energy & Mining Services, Inc. following a 25-year

career of executive management, mergers & acquisitions (M&A), and operations experience

in the mining, energy and natural resource industries. He specializes in directing valuations

and M&A assignments on behalf of the owners of small and middle market companies. Mr.

Nowobilski serves both “buyer” and “seller” clients.

BACKGROUND

Mr. Nowobilski’s M&A experience includes participation in successful transactions valued at

more than $1 billion since 1990. His experience includes both company and mineral

property assessments and valuations, buyer-seller negotiations, definitive purchase

agreement negotiations, due diligence, negotiations with major lending institutions, and the

procurement of private equity capital.

Mr. Nowobilski received his Bachelor of Science degree from the University of Illinois in

Champaign, Illinois and his Master of Business Administration degree from Southern Illinois

University.

© 2013 Business Valuation Resources, LLC

[email protected]

38

DWIGHT DAVIS

Dwight Davis

Professional Profile

INTRODUCTION

Mr. Davis has over 20 years of professional and managerial experience in acquisitions

and divestitures (M&A), market analysis, asset management and operations engineering

within the natural resource industry. His resume includes management positions with

Zeigler Coal Holding Company, Shell Mining Company and A. T. Massey Coal Company.

BACKGROUND

Mr. Davis’s natural resource industry experience spans 35 years and includes the

acquisition and divestiture of numerous natural resource operations, coal mines and

mineral reserves. His experience includes all phases of the acquisition and divestiture

process - from identification, evaluation, due diligence and final closing of various

operating mining operations and numerous mineral properties.

Mr. Davis received his B.S. degree in Engineering from the University of Louisville. In

addition to his role as an associate with Mid-America Energy & Mining Services, Inc., he

owns and operates Dwight Davis & Associates, PSC. His engineering and consulting

firm provides a broad range of services specific to the natural resource industry.