27

Variable Annuities Variable Annuities Abusive Sales Practices Abusive Sales Practices and Liability and Liability By Joel D. Feldman Anapol, Schwartz, Weiss, Cohan, Feldman & Smalley

| Date post: | 15-Dec-2015 |

| Category: |

Documents |

| Upload: | juan-cogdill |

| View: | 220 times |

| Download: | 0 times |

Variable AnnuitiesVariable Annuities

Abusive Sales Practices Abusive Sales Practices and Liabilityand Liability

By Joel D. Feldman

Anapol, Schwartz, Weiss, Cohan, Feldman & Smalley

IntroductionIntroduction

Individual InvestorsNASD and NYSE Arbitration

ProgramsTort Law ConceptsPersonal Injury Settlement Proceeds

Variable AnnuitiesVariable Annuities

What are they?– Annuities – Insurance Contracts– Tax Deferred Growth– Annuitization

Sub-accountsSub-accounts

Variable Annuities subject to stock market risk based upon the nature of sub-account investments

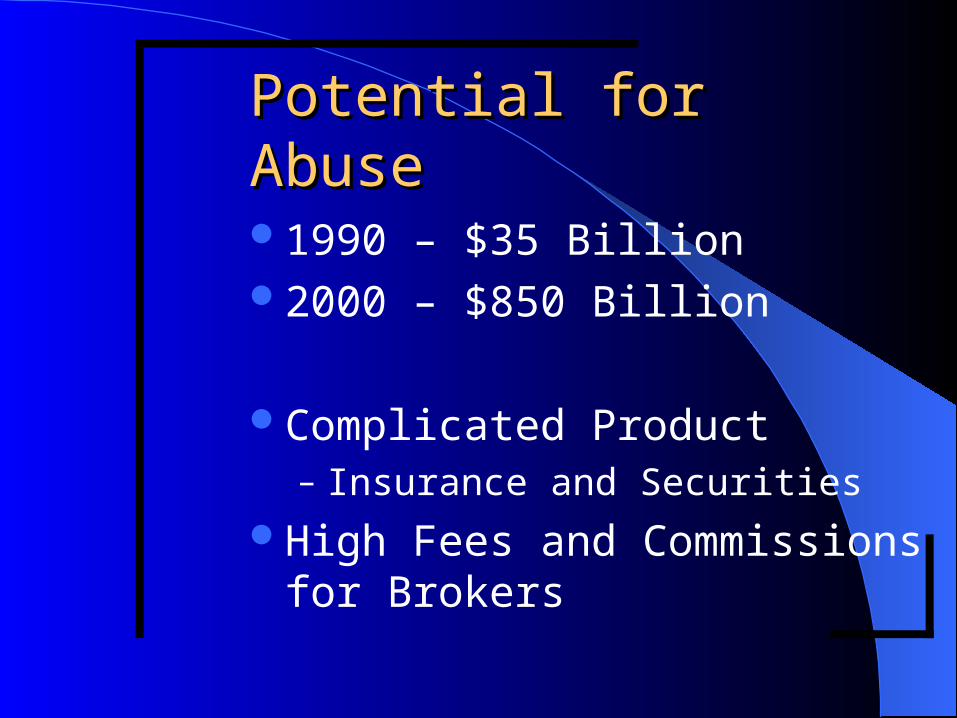

Potential for AbusePotential for Abuse

1990 – $35 Billion2000 – $850 Billion

Complicated Product– Insurance and Securities

High Fees and Commissions for Brokers

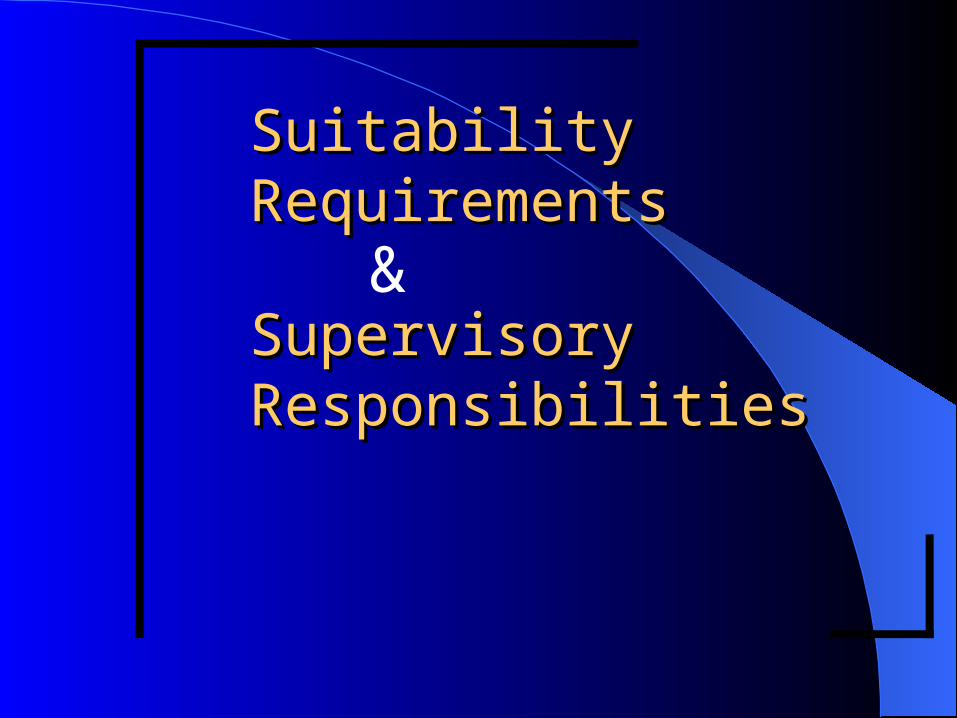

Suitability Suitability RequirementsRequirements

Supervisory Supervisory ResponsibilitiesResponsibilities

&

SuitabilitySuitability

NASD Conduct Rule 2310– Recommending Purchase, Sale, or

Exchange– Reasonable Grounds for Believing

Recommendation is Suitable for the Customer

Facts Disclosed by the Customer– Other Security Holdings– Financial Situation

Investment Investment ObjectivesObjectives

Risk Risk ToleranceTolerance

&

Supervision Supervision

NASD Conduct Rule 3010(a)(1)Members must establish systems to

supervise activities of agents designed to achieve compliance with applicable securities laws and regulations.

Mr. and Mrs. JonesMr. and Mrs. Jones

Mrs. is retired – age 62Mr. is retired – age 66Both have a high school educationBoth need a current incomeNeither need life insuranceBoth are Risk Averse

Mr. and Mrs. JonesMr. and Mrs. Jones

Prior Investment Experience– U.S. Savings Bonds– Bank CD’s– Mr. Jones – Participated in Company

Retirement Plan

Investment ObjectivesInvestment Objectivesand Risk Toleranceand Risk ToleranceI do not want to worry about losing

my moneyI do not need to make a lot of

money, I just want to be secure and have a guaranteed income

I do not trust the stock market

Mr. and Mrs. JonesMr. and Mrs. Jones

Mrs. Jones Personal Injury Settlement

Net $750,000

What should be done with the money?

Financial Advisor

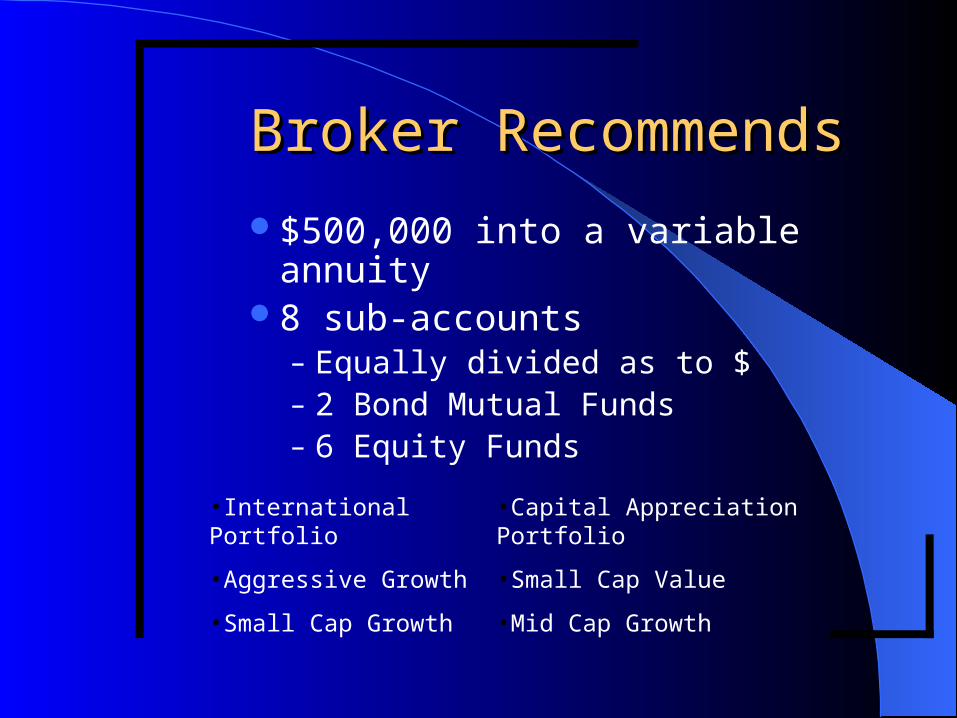

Broker RecommendsBroker Recommends

$500,000 into a variable annuity8 sub-accounts

– Equally divided as to $– 2 Bond Mutual Funds– 6 Equity Funds

•International Portfolio

•Aggressive Growth

•Small Cap Growth

•Capital Appreciation Portfolio

•Small Cap Value

•Mid Cap Growth

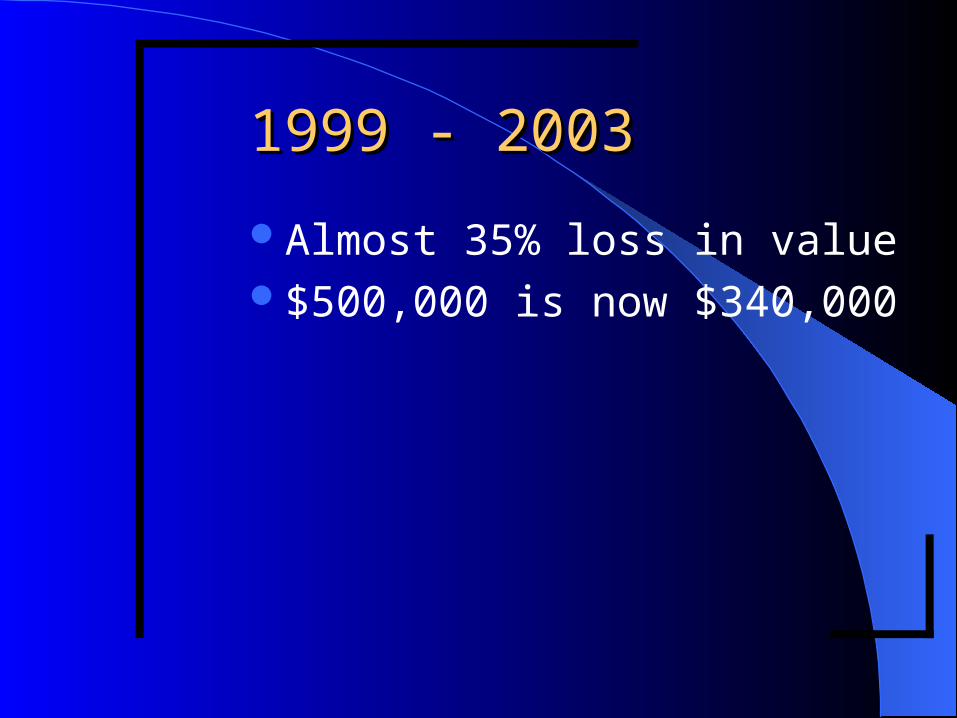

1999 - 20031999 - 2003

Almost 35% loss in value$500,000 is now $340,000

ConfusionConfusionMisunderstanding Misunderstanding Deception?Deception?It is guaranteed you cannot lose your

initial investmentA minimum level of income

payments is guaranteed

Principal is GuaranteedPrincipal is Guaranteed

Correct – But only if and when Mrs. Jones dies

Guaranteed Minimum Guaranteed Minimum Income BenefitIncome BenefitYes – But

– Policy must be in force for 10 years– Annuitization is Necessary

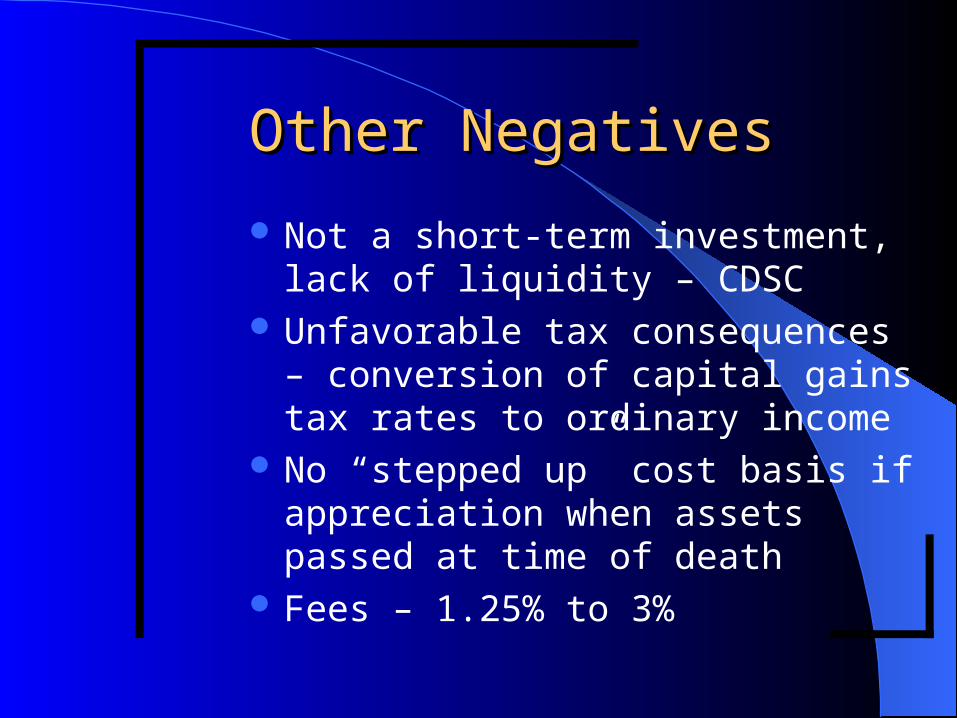

Other NegativesOther Negatives

Not a short-term investment, lack of liquidity – CDSC

Unfavorable tax consequences – conversion of capital gains tax rates to ordinary income

No “stepped up” cost basis if appreciation when assets passed at time of death

Fees – 1.25% to 3%

Mr. and Mrs. JonesMr. and Mrs. Jones

Never should have been sold any variable annuity– Tax deferral not important– No need for life insurance– Had a real need for guaranteed principal

Negligence, Breach of Contract, Breach of Fiduciary Duty, Uniform Trade Practices Consumer Protection Law (UTPCPL), Fraud

Deceived or ConfusedDeceived or Confused

Or Both?

DamagesDamages

Rescission– Return of $500,000 investment

(less actual value)

Interest from Date of Sale of Variable Annuity

Attorney’s Fees and CostsUTPCPL – Treble Damages

NASD Conduct RulesNASD Conduct Rules

Actual and Proposed

Heightened Suitability Requirements“Plain English” Risk Disclosures

– See Exhibit ??

Heightened Supervisory Requirements

Warning SignsWarning SignsOlder ClientsQualified AccountsNeed for LiquidityNo Need for Life InsuranceUnsophisticated ClientsNeed for Income and Preservation of

Capital“1035” Exchanges

Variable AnnuitiesVariable Annuities

Abusive Sales Practices Abusive Sales Practices and Liabilityand Liability

By Joel D. Feldman

Anapol, Schwartz, Weiss, Cohan, Feldman & Smalley