Prepared by: C. Douglas Cloud

Professor Emeritus of Accounting

Pepperdine University

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Variable Costing for Management Analysis

Chapter 20

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Learning Objectives

1. Describe and illustrate reporting income from

operations under absorption and variable

costing.

2. Describe and illustrate the effects of absorption

and variable costing on analyzing income

from operations.

3. Describe management’s use of absorption and

variable costing.

4. Use variable costing for analyzing market

segments, including product, territories, and

salespersons segments.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Learning Objectives

5. Use variable costing for analyzing and

explaining changes in contribution margin as

a result of quantity and price factors.

6. Describe and illustrate the use of variable

costing for service firms.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Describe and

illustrate reporting

income from

operations under

absorption and

variable costing.

Learning Objective 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

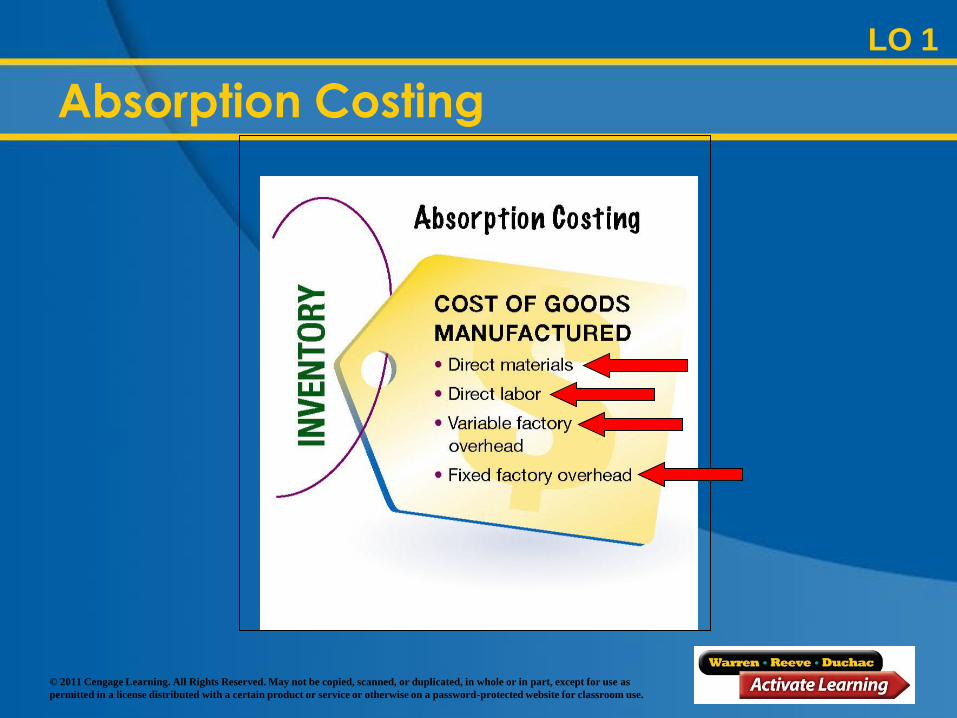

Absorption costing is required under

generally accepted accounting principles

for financial statements distributed to

external users.

Absorption Costing

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Absorption Costing

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Variable Costing

LO 1

For internal use in decision making,

managers often use variable costing,

sometimes called direct costing.

The cost of goods manufactured includes

only variable manufacturing costs.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Variable Costing

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

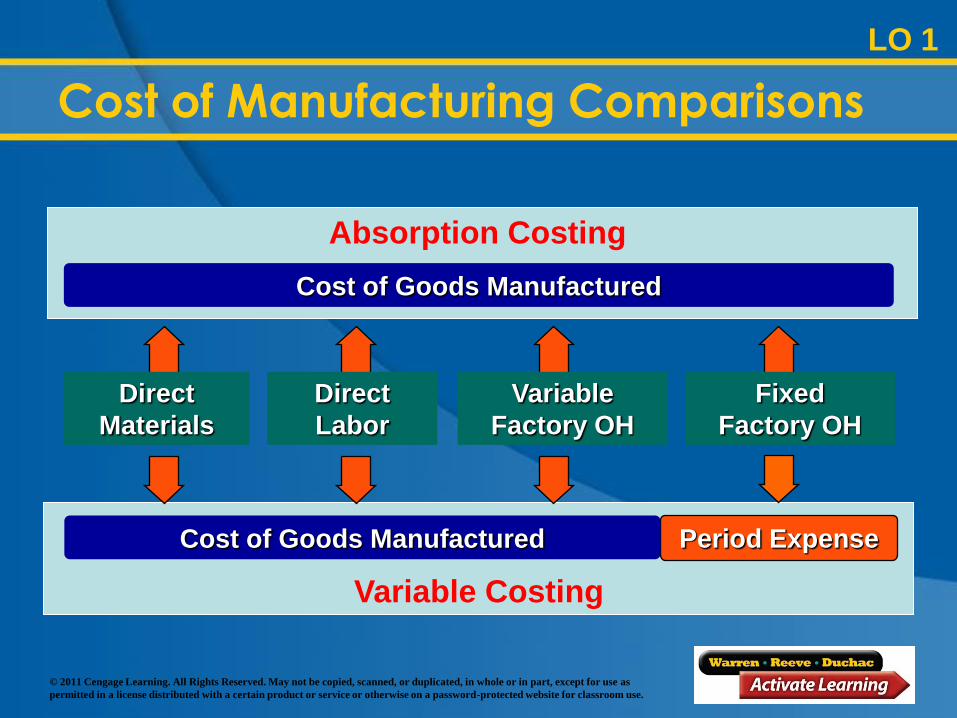

Period Expense

Variable Costing

Absorption Costing

Cost of Goods Manufactured

Cost of Goods Manufactured

Direct

Materials

Direct

Labor

Variable

Factory OH

Fixed

Factory OH

Cost of Manufacturing Comparisons

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Variable Costing

LO 1

Manufacturing margin is sales less variable

cost of goods sold.

Variable cost of goods sold consists of

direct materials, direct labor, and variable

factory overhead for the units sold.

Contribution margin is manufacturing

margin less variable selling and

administrative expenses.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

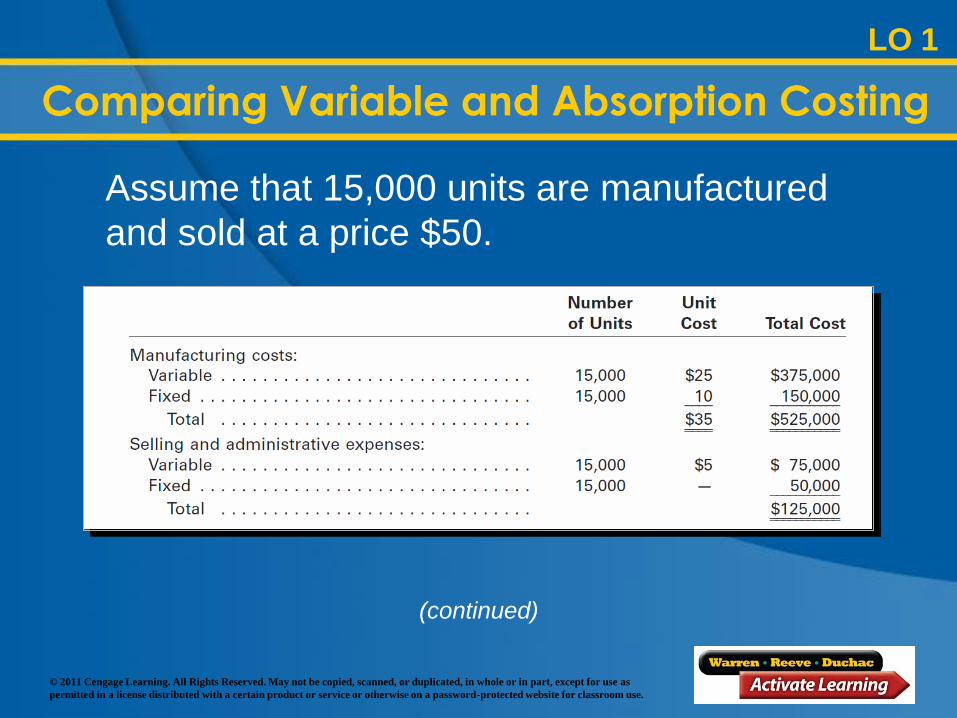

Assume that 15,000 units are manufactured

and sold at a price $50.

Comparing Variable and Absorption Costing

LO 1

(continued)

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Units Manufactured Equal Units Sold

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

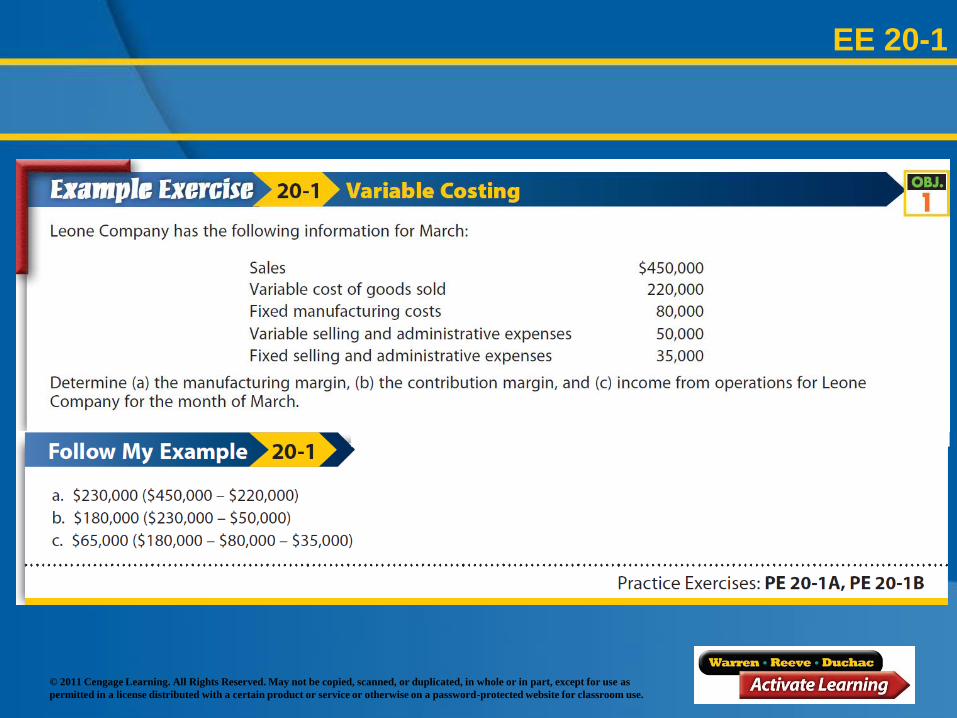

EE 20-1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

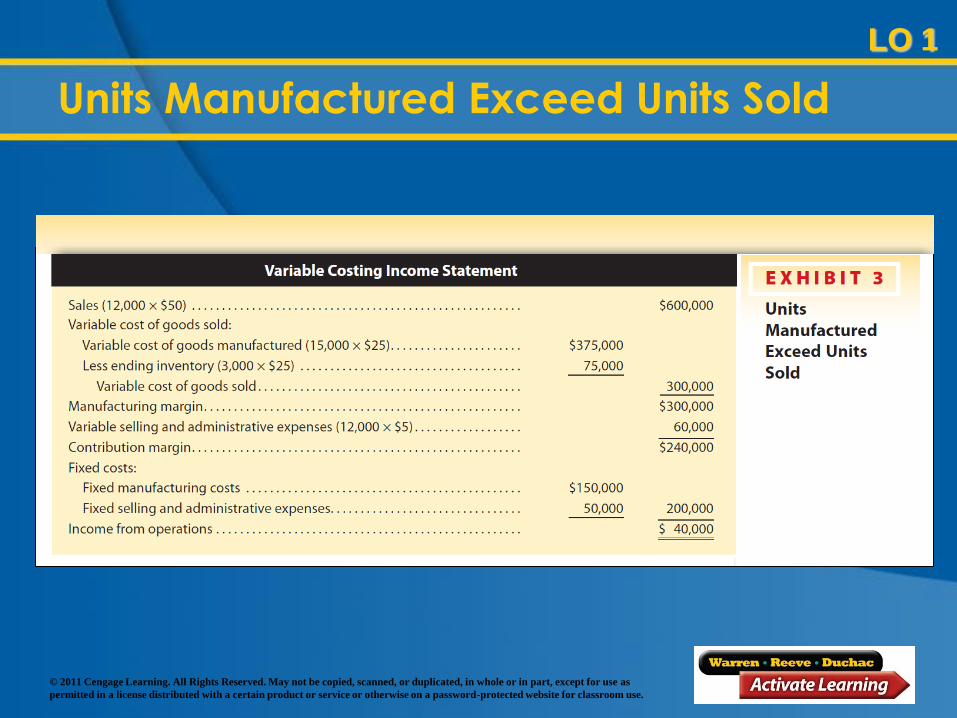

Units Manufactured Exceed Units Sold

Assume that in the preceding example only 12,000

units of the 15,000 units manufactured were sold.

Examine Exhibit 3 (next two slides) and you will

see that income from operations using variable

costing is $40,000, while absorption costing

provides an income from operations of $70,000.

(continued)

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

(continued)

Units Manufactured Exceed Units Sold

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Units Manufactured Exceed Units Sold

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

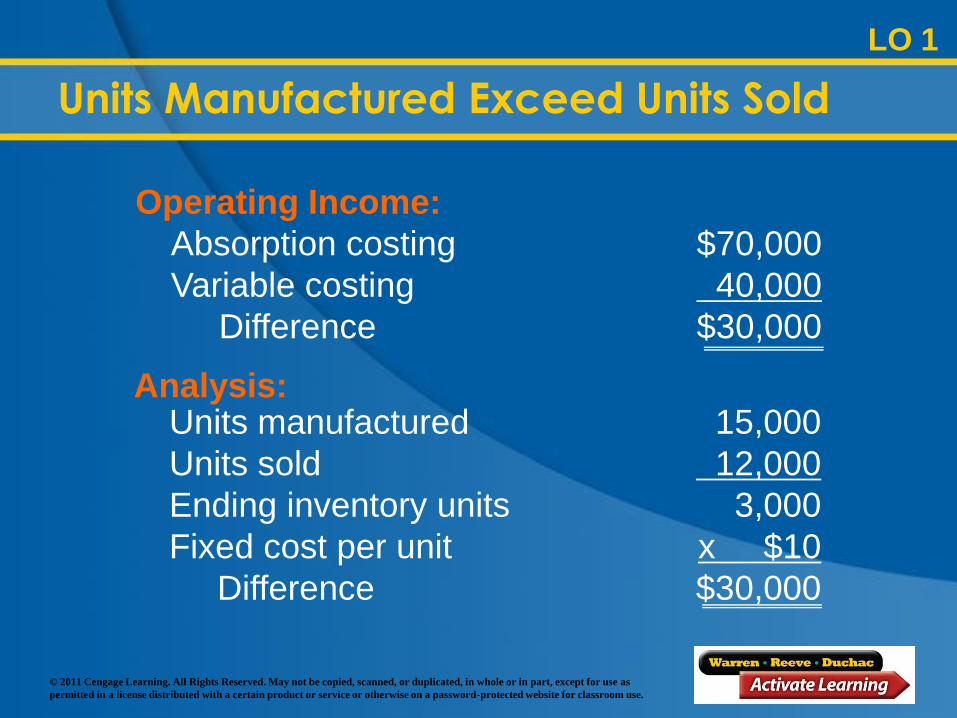

Why is absorption costing income higher when

units manufactured exceed units sold?

Operating Income:

Absorption costing $70,000

Variable costing 40,000

Difference $30,000

Units Manufactured Exceed Units Sold

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Analysis: Units manufactured 15,000

Units sold 12,000

Ending inventory units 3,000

Fixed cost per unit x $10

Difference $30,000

Units Manufactured Exceed Units Sold

LO 1

Operating Income:

Absorption costing $70,000

Variable costing 40,000

Difference $30,000

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

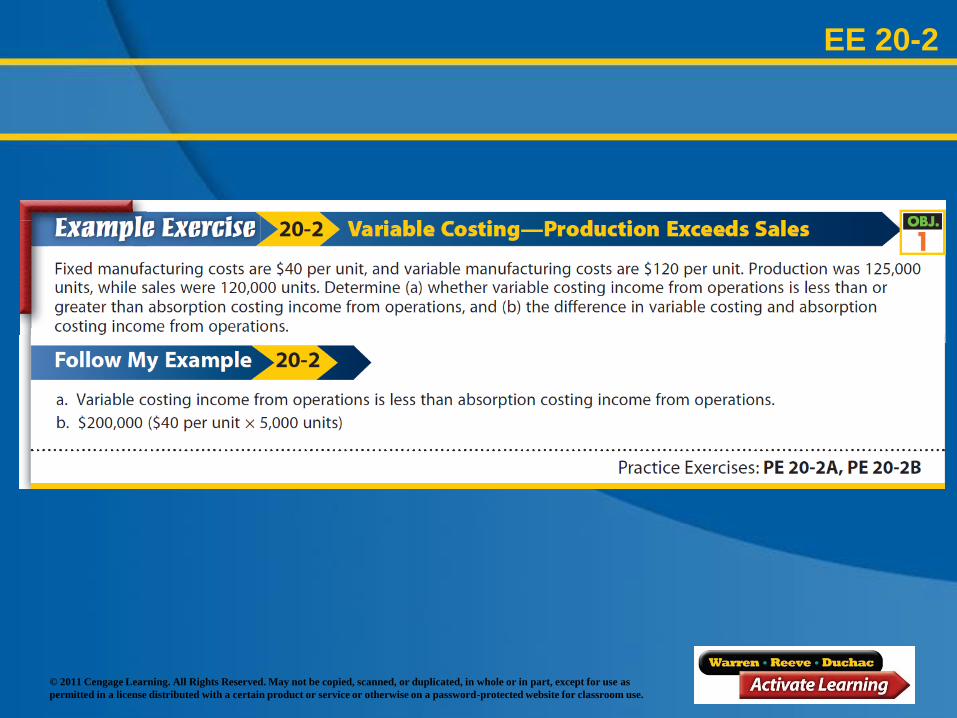

EE 20-2

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

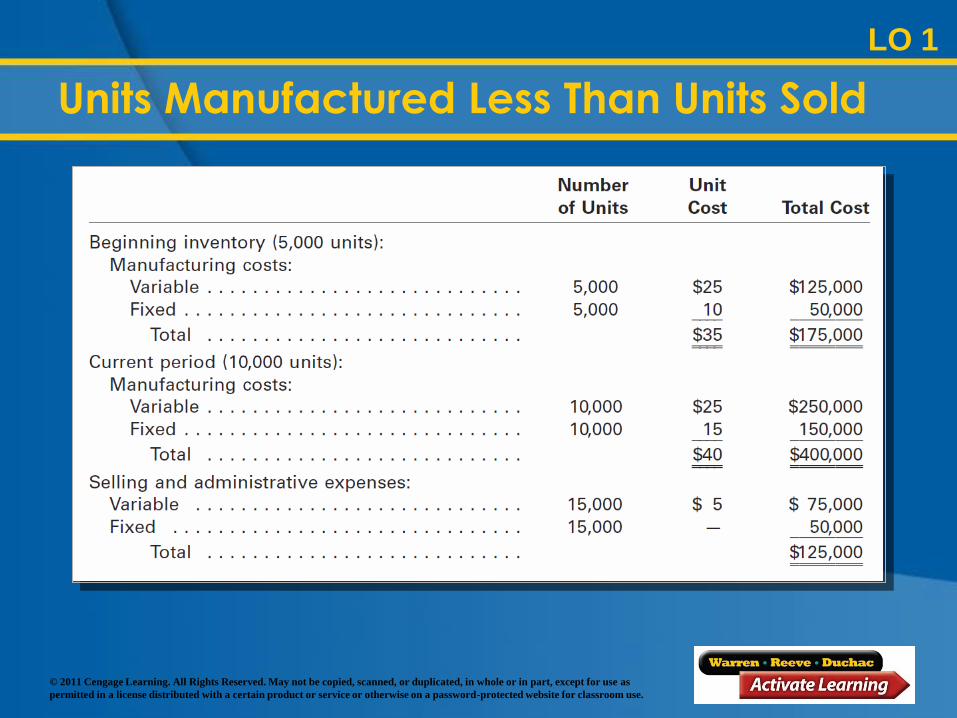

Assume that 5,000 units of inventory were on hand

at the beginning of a period, 10,000 units were

manufactured during the period, and 15,000 units

were sold at $50 per unit.

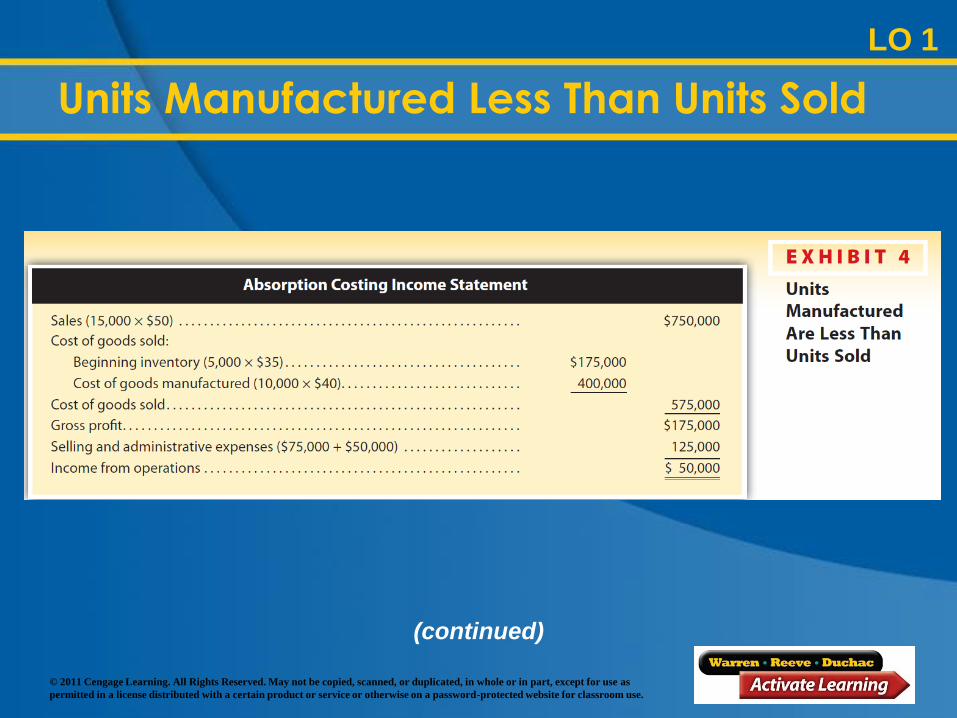

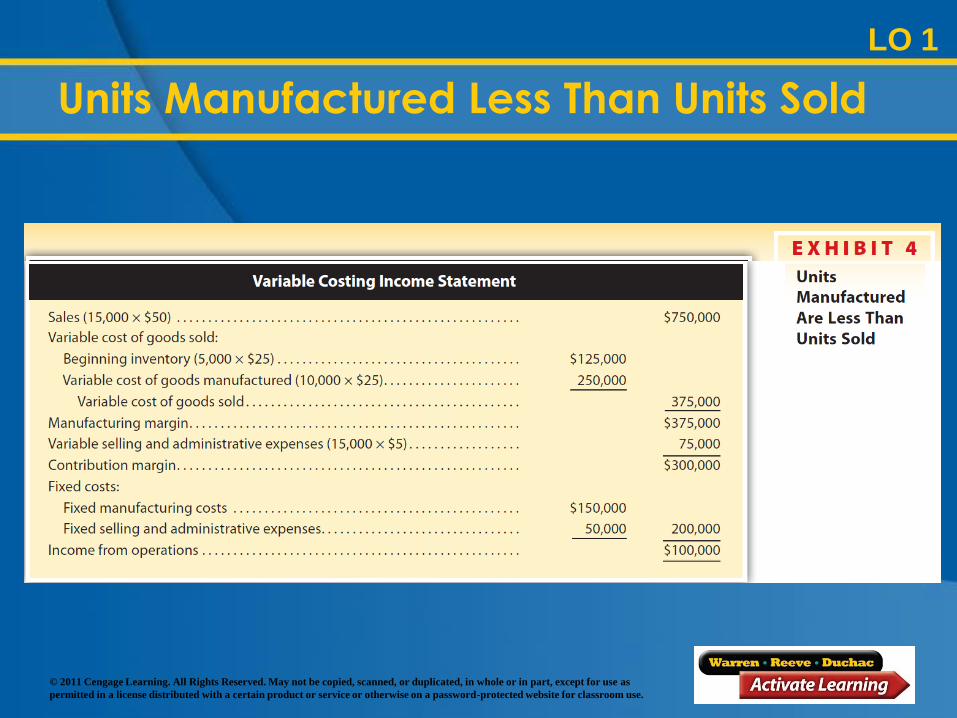

Units Manufactured Less Than Units Sold

LO 1

(continued)

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Units Manufactured Less Than Units Sold

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

(continued)

Units Manufactured Less Than Units Sold

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Units Manufactured Less Than Units Sold

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EE 20-3

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

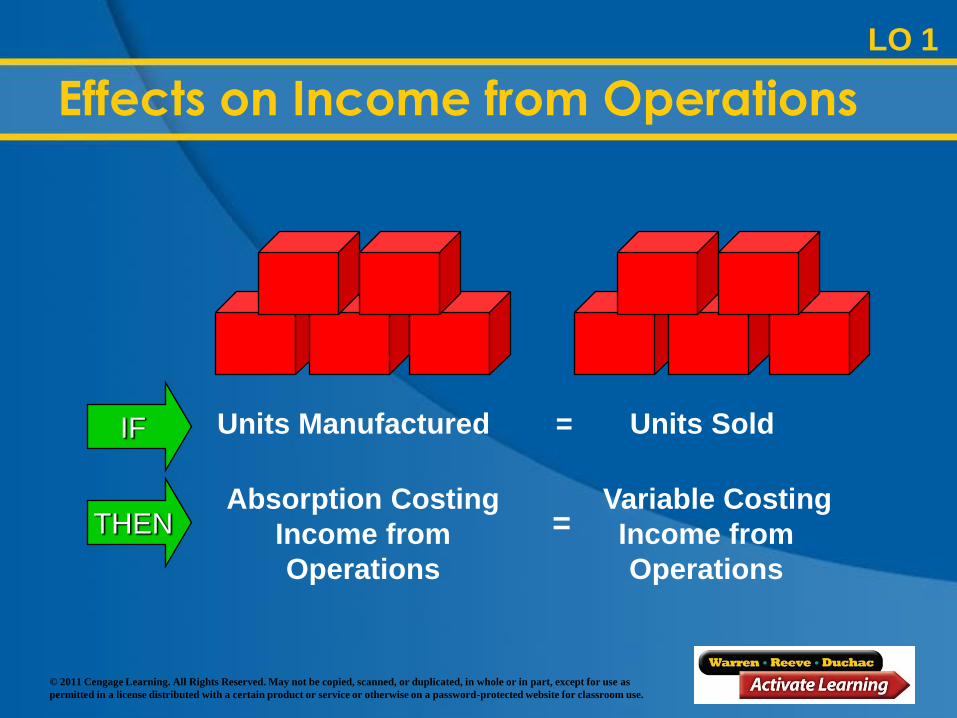

IF Units Manufactured = Units Sold

THEN Absorption Costing

Income from

Operations

Variable Costing

Income from

Operations

=

Effects on Income from Operations

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

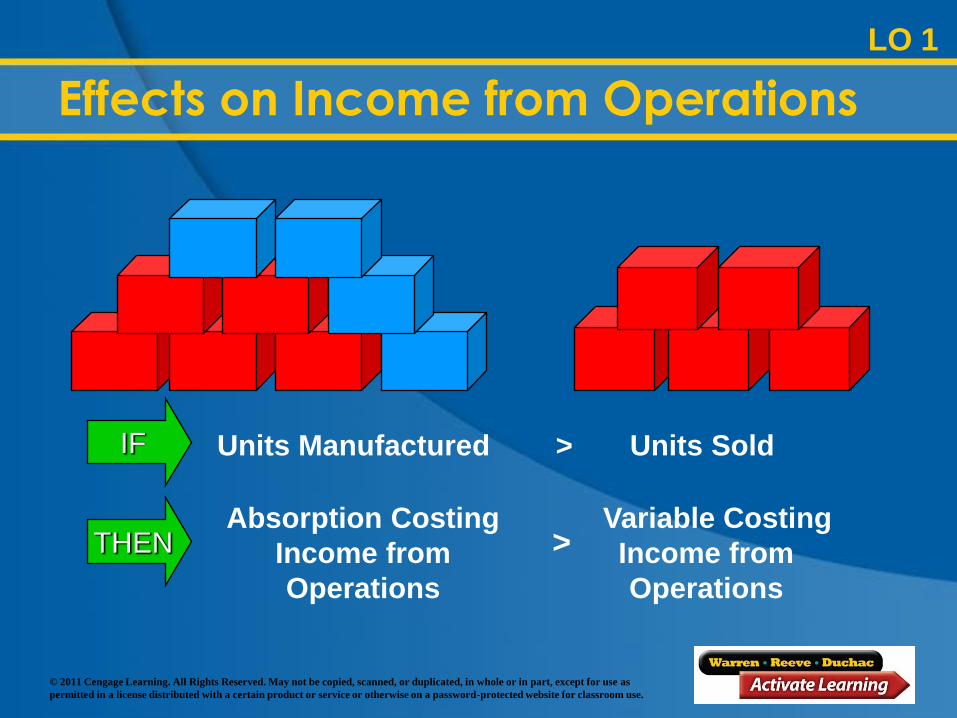

IF Units Manufactured > Units Sold

THEN Absorption Costing

Income from

Operations

Variable Costing

Income from

Operations

>

Effects on Income from Operations

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

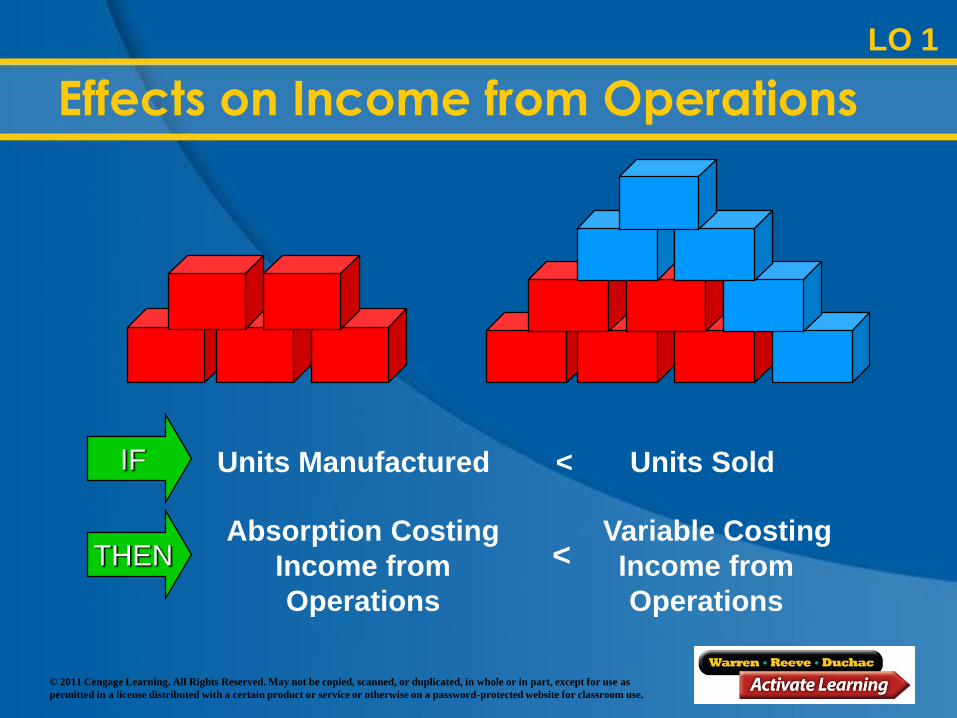

THEN Absorption Costing

Income from

Operations

Variable Costing

Income from

Operations

<

IF Units Manufactured < Units Sold

Effects on Income from Operations

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Describe and

illustrate the effects

of absorption and

variable costing on

analyzing income

from operations.

Learning Objective 2

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

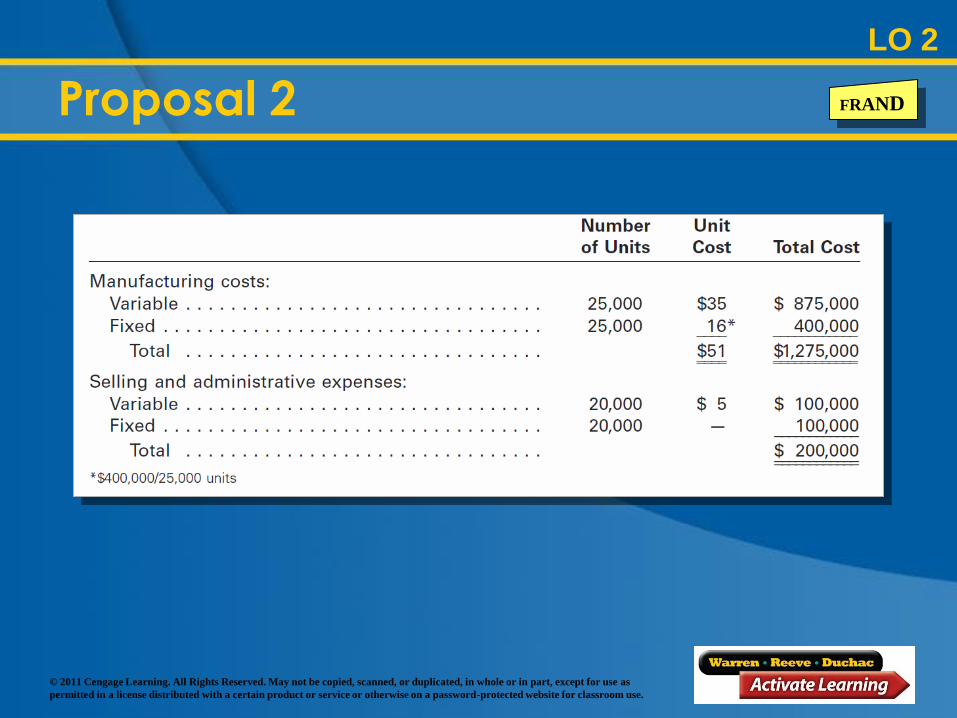

Frand Manufacturing Company has no beginning

inventory, and sales are estimated to be 20,000

units at $75 per unit, regardless of production

levels.

The management of Frand Manufacturing

Company is evaluating whether to manufacture

20,000 units (Proposal 1) or 25,000 units

(Proposal 2).

Frand Manufacturing Company

LO 2

FRAND

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Proposal 1

LO 2

FRAND

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Proposal 2

LO 2

FRAND

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 2

Income Analysis Under Absorption

and Variable Costing FRAND

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 2

Income Analysis Under Absorption

and Variable Costing FRAND

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EE 20-4

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Learning Objective 3

Describe

management’s use of

absorption and

variable costing.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 3

Using Absorption and Variable Costing

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Controlling Costs

For a specific level of management,

controllable costs are costs that can be

influenced by management at that level.

Noncontrollable costs are costs that

another level of management controls.

LO 3

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 3

Pricing Products

Many factors enter into determining the

selling price of a product.

The cost of making the product is significant

in all pricing decisions.

In the short run, fixed costs cannot be

avoided.

In the long run, a company must set its

selling price high enough to cover all costs

and expenses and generate income.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 3

Planning Production

In the short run, planning production is

limited to existing capacity.

In the long run, planning production can

consider expanding capacity.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 3

Analyzing Contribution Margins

Managers often plan and control operations

by evaluating the differences between

planned and actual contribution margins.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 3

Analyzing Market Segments

A market segment is a portion of a business

that can be analyzed using sales, costs,

and expenses to determine its profitability.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Learning Objective 4

Use variable costing for

analyzing market

segments, including

product, territories, and

salespersons segments.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 4

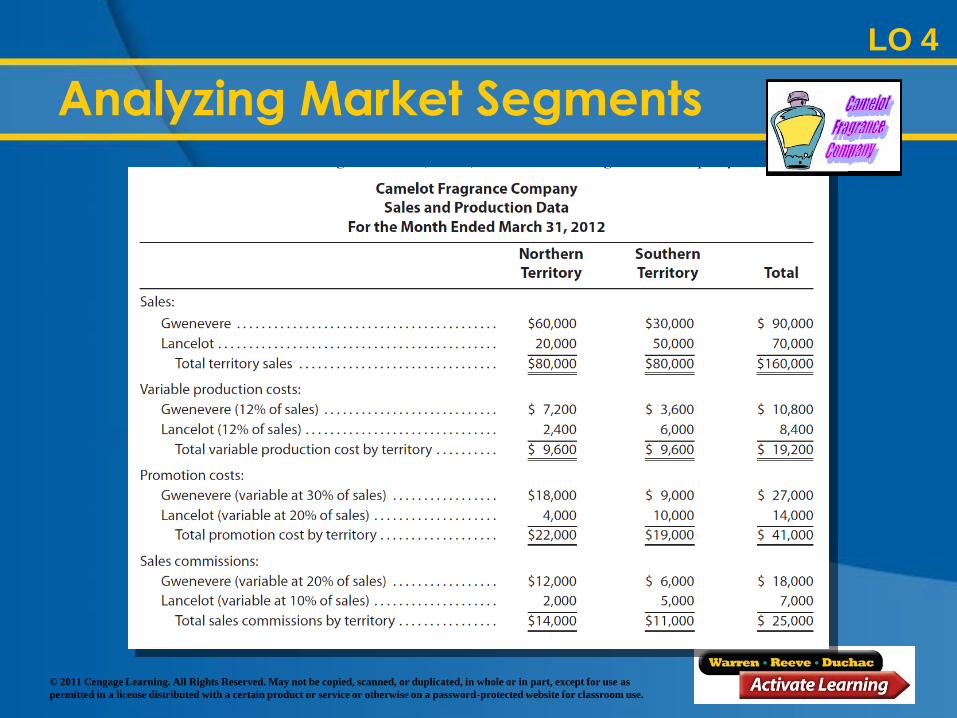

Analyzing Market Segments

Camelot Fragrance Company manufactures and

sells Gwenevere perfume for women and the

Lancelot cologne line for men. The company’s

data for the month ended March 31, 2012, is

shown in the next slide.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 4

Analyzing Market Segments

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 4

Sales Territory Profitability Analysis

Sales territory profitability analysis may lead

management to do the following:

Reduce costs in lower-profit sales territories

Increase sales efforts in higher-profit

territories

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

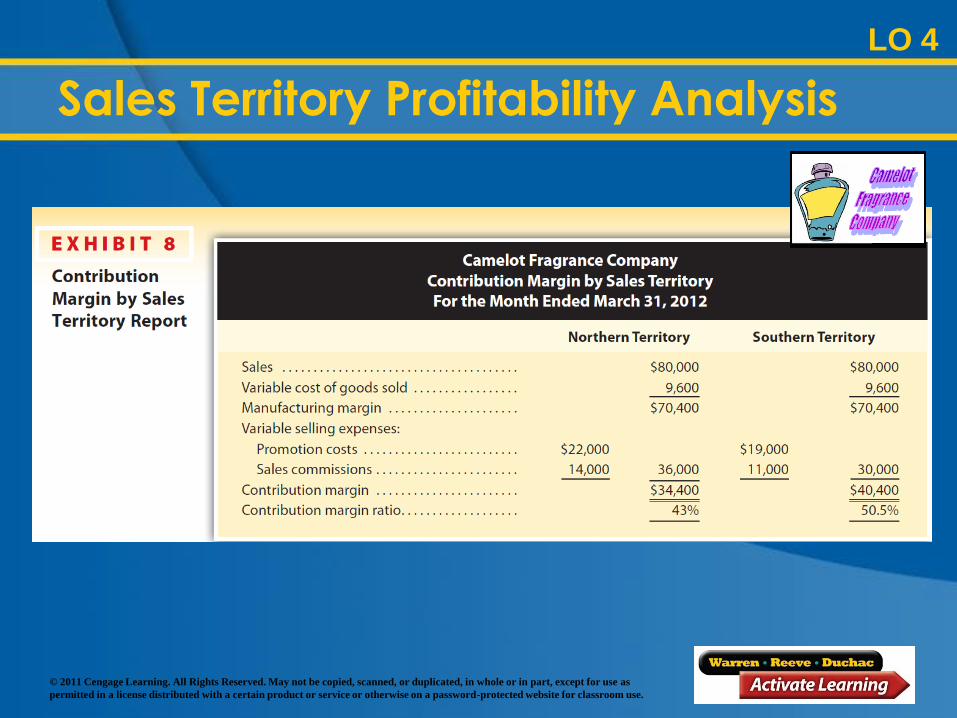

LO 4

Sales Territory Profitability Analysis

To illustrate the analysis of profit differences by

sales territory, Exhibit 8 shows the variable

costing income statement by sales territories for

Camelot Fragrance Company.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 4

Sales Territory Profitability Analysis

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

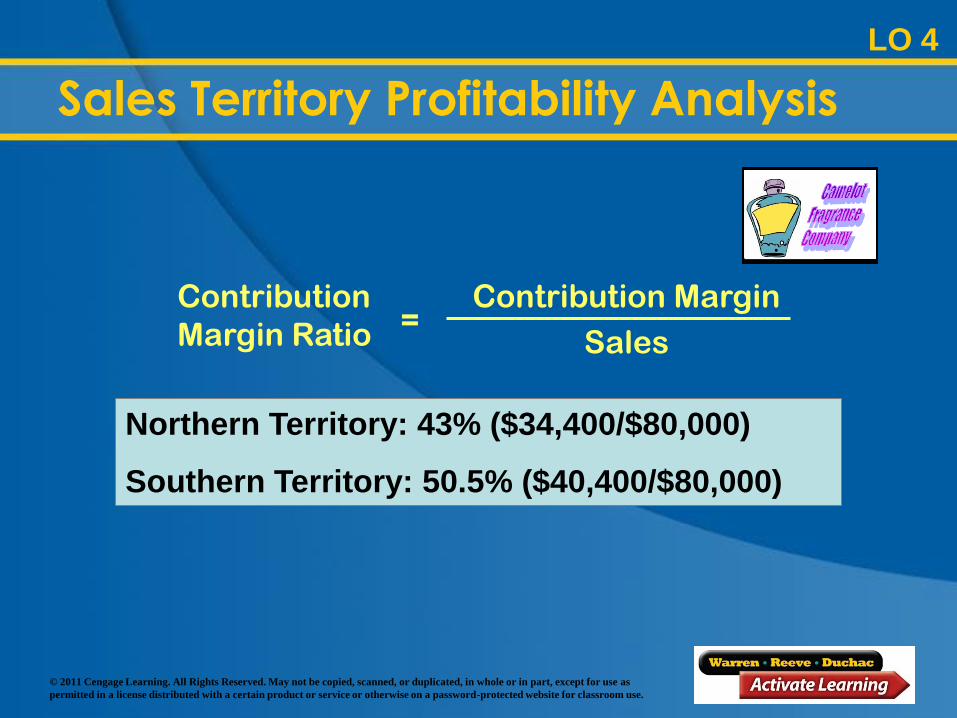

Contribution

Margin Ratio = Contribution Margin

Sales

Northern Territory: 43% ($34,400/$80,000)

Southern Territory: 50.5% ($40,400/$80,000)

LO 4

Sales Territory Profitability Analysis

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 4

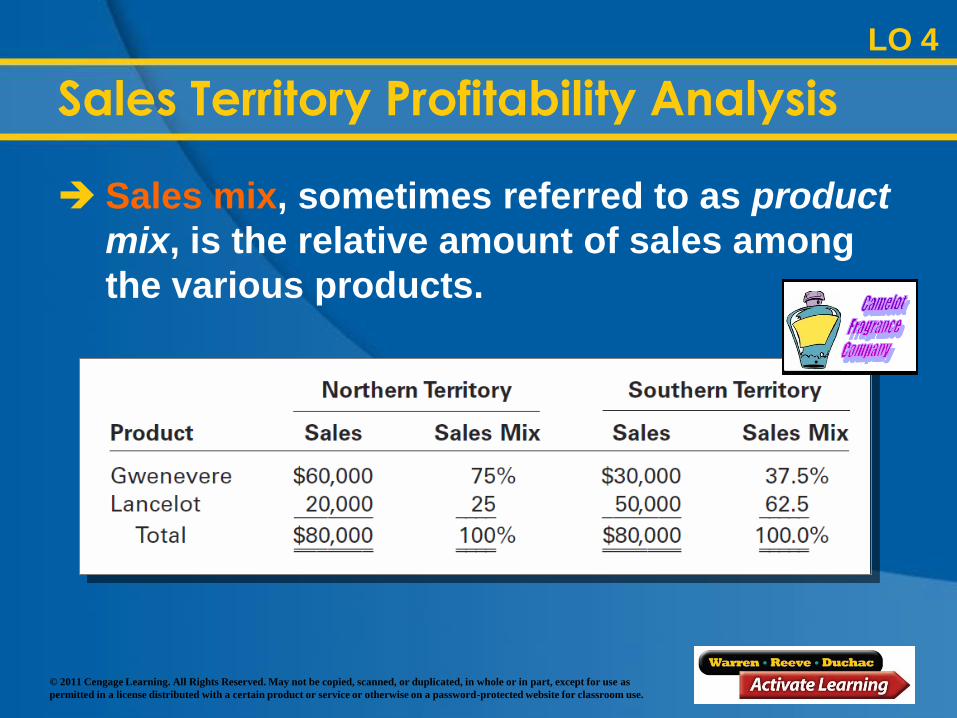

Sales Territory Profitability Analysis

Sales mix, sometimes referred to as product

mix, is the relative amount of sales among

the various products.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Product Profitability Analysis

A company should focus its sales efforts on

products that will provide the maximum

total contribution margin.

LO 4

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Product Profitability Analysis

LO 4

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

A salesperson profitability report is useful

in evaluating sales performance.

Such a report normally includes total sales,

variable cost of goods sold, variable selling

expenses, contribution margin, and

contribution margin ratio for each

salesperson.

Salesperson Profitability Analysis

LO 4

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Salesperson Profitability Analysis

LO 4

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

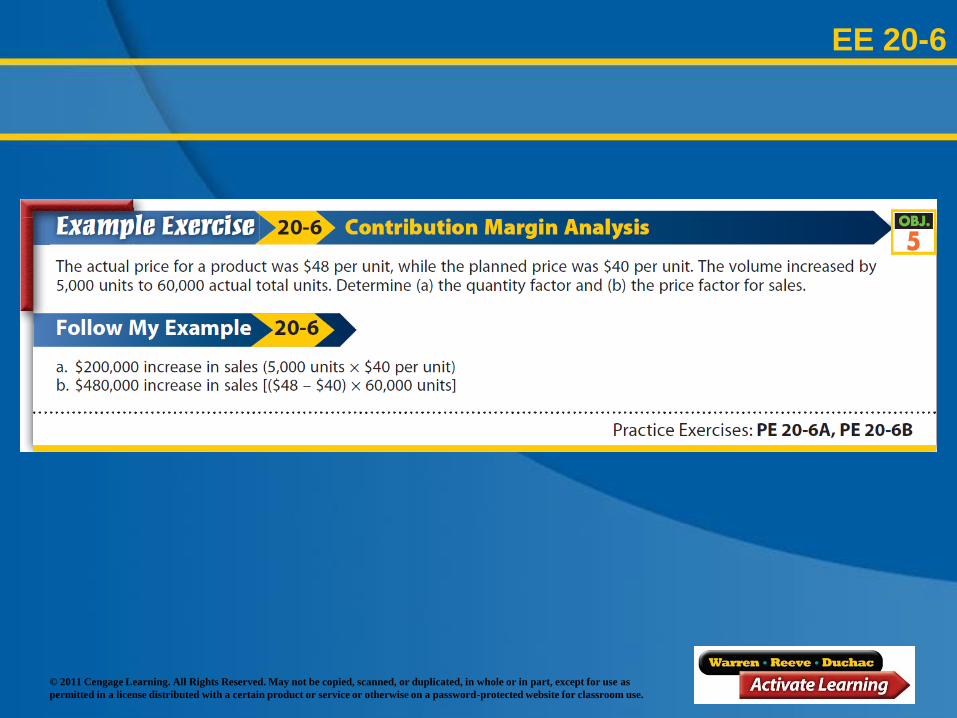

EE 20-5

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Learning Objective 5

Use variable costing for

analyzing and

explaining changes in

contribution margin as a

result of quantity and

price factors.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 5

Contribution Margin Analysis

Contribution margin analysis focuses on

explaining the differences between

planned and actual contribution margins.

A difference between the planned and

actual contribution margin may be caused

by an increase or a decrease in:

Sales

Variable costs

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 5

Contribution Margin Analysis

An increase or a decrease in sales or

variable costs may in turn be due to an

increase or a decrease in the:

Number of units sold

Unit sales price or unit cost

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Sales

Quantity

Factor

Actual

Units

Sold

Planned

Units of

Sales

Planned

Sales

Price = – ×

Variable Cost

Quantity

Factor

Planned

Units of

Sales

Actual

Units

Sold

Planned

Unit

Cost = – ×

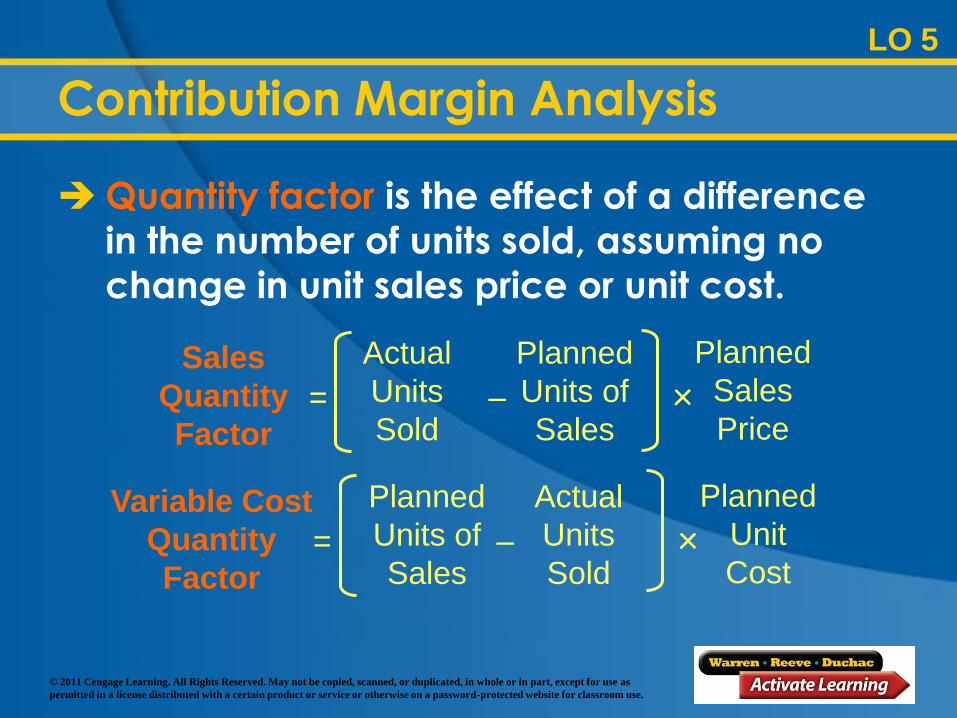

LO 5

Contribution Margin Analysis

Quantity factor is the effect of a difference

in the number of units sold, assuming no

change in unit sales price or unit cost.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Unit

Price

Factor

Actual

Selling

Price per

Unit

Planned

Selling

Price per

Unit

Actual

Units

Sold = – ×

Unit

Cost

Factor

Planned

Cost per

Unit

Actual

Cost per

Unit

Actual

Units

Sold = – ×

LO 5

Contribution Margin Analysis

Unit price factor or unit cost factor is the

effect of a difference in unit sales price or

unit cost on the number of units sold.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

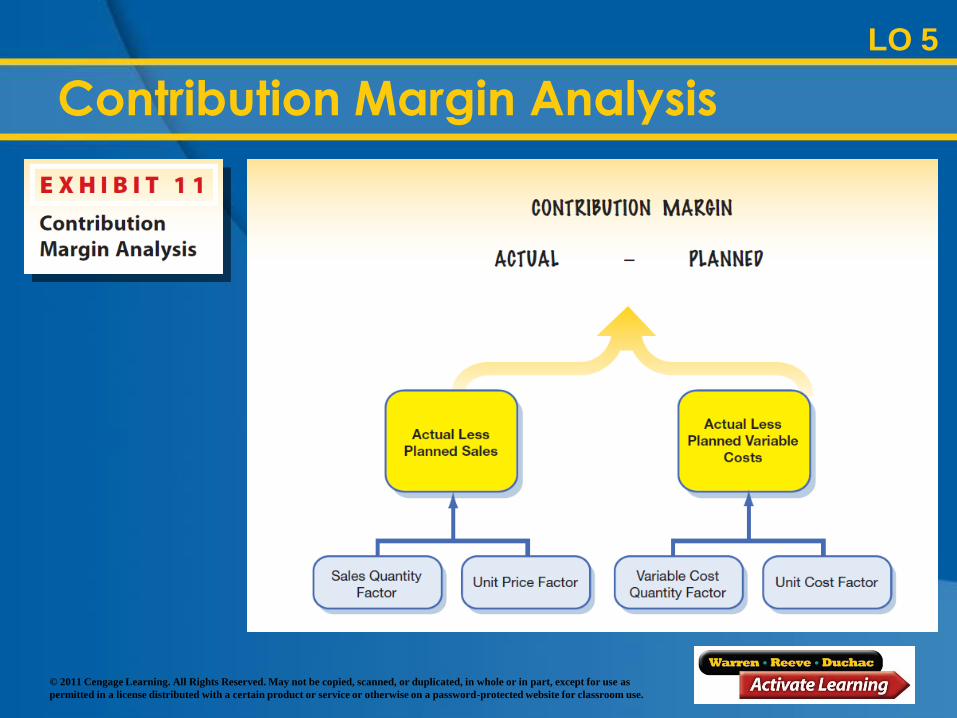

LO 5

Contribution Margin Analysis

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

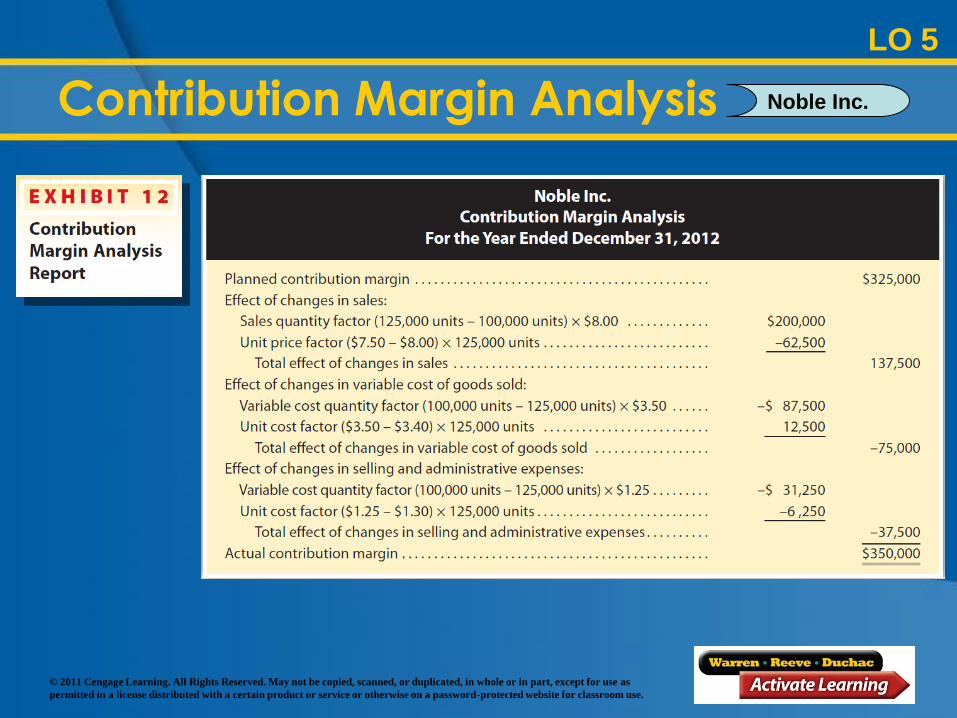

LO 5

Contribution Margin Analysis

Year Ended December 31, 2012

Noble Inc.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 5

Contribution Margin Analysis Noble Inc.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EE 20-6

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Learning Objective 6

Describe and

illustrate the use of

variable costing for

service firms.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Variable Costing for Service Firms

Unlike a manufacturing company, a service

company does not make or sell a product.

As a result, service companies do not have

inventory and, thus, do not allocate fixed

costs to inventory using absorption costing

concepts.

LO 6

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

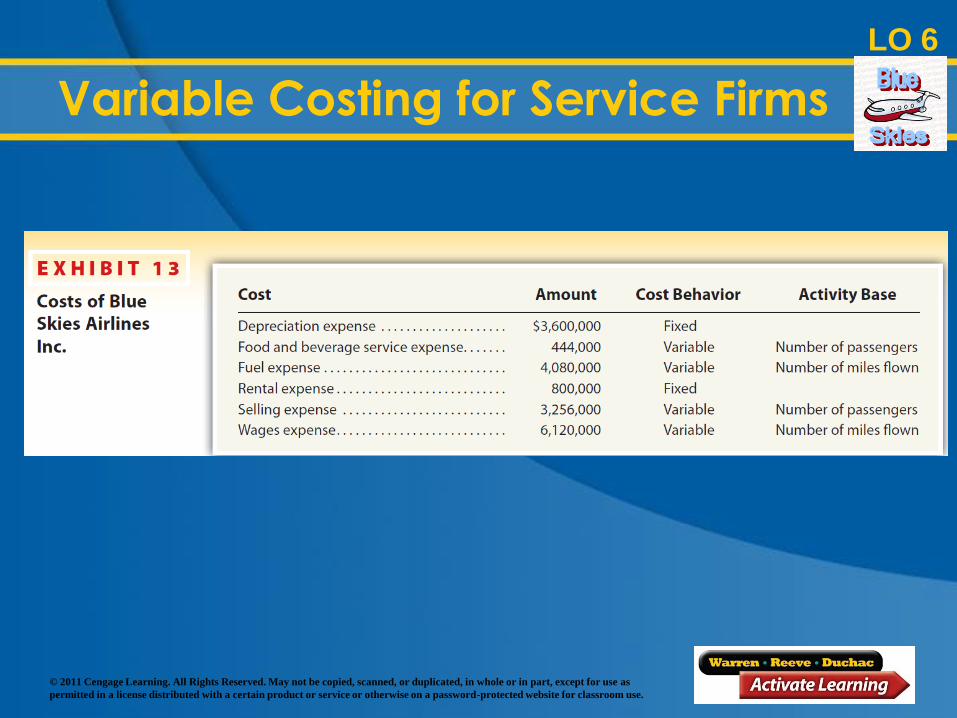

Service firms can report and analyze contribution

margin as the difference between revenues and

variable costs. To analyze a service firm, we will

use Blues Skies Airlines. The fixed and variable

costs associated with operating Blue Skies are

shown in Exhibit 13 (next slide).

Variable Costing for Service Firms

LO 6

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Variable Costing for Service Firms

LO 6

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

The variable costing income statement for Blue

Skies Airlines is shown in Exhibit 14 (next slide).

Blue Skies Airlines uses the activity base number

of passengers for food and beverage service and

selling expenses. The company uses number of

miles flown for fuel and wages expenses.

Variable Costing for Service Firms

LO 6

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Variable Costing for Service Firms

LO 6

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

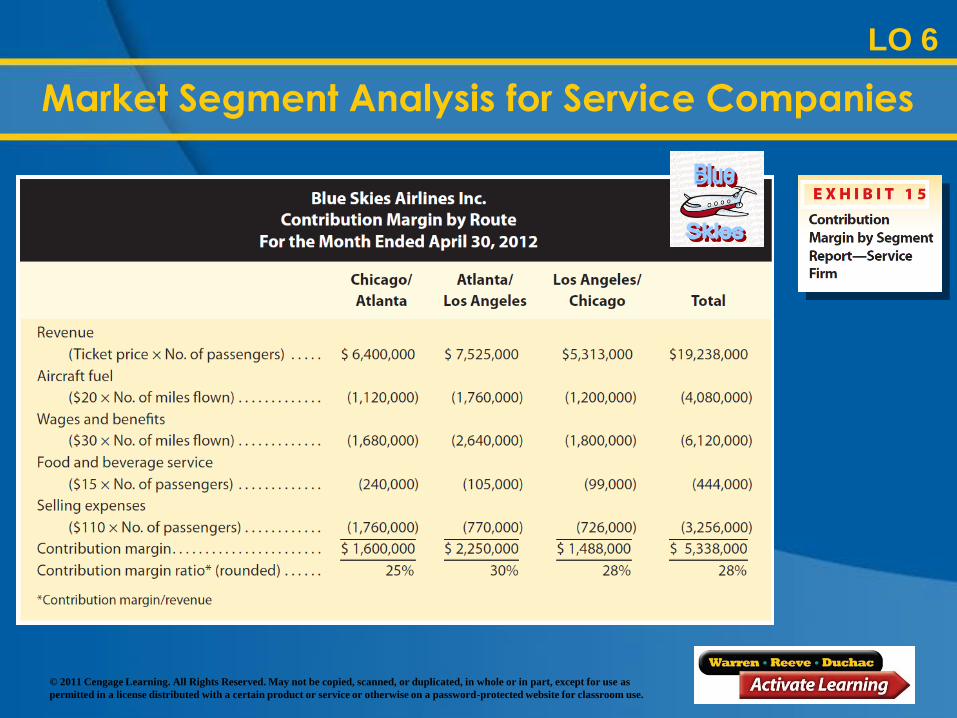

LO 6

Market Segment Analysis for Service Companies

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Blue Skies Airlines

LO 6

Market Segment Analysis for Service Companies

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Market Segment Analysis for Service Companies

LO 6

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Contribution Margin Analysis

LO 6

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Contribution Margin Analysis

LO 6

Prepared by: C. Douglas Cloud

Professor Emeritus of Accounting

Pepperdine University

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Variable Costing for Management Analysis

The End