20

Current Opportunities - Venture Capital in Chile January 2015

Current Opportunities - Venture Capital in Chile

January 2015

Content

1. What Do We Understand by Venture Capital? 03

2. Venture Capital History in Chile 05

3. General Overview of the VC&PE industries in Chile 07

4. Current Opportunities 11

5. Execution Alternatives 13

1. What do we understand by Venture Capital?

4

-Incubators

-Universities

1. What do we understand by Venture Capital?

1.1 Brief Description of Venture Capital

Venture Capital (VC) Funds, usually invest in young

companies with businesses at early stages of development

The VC industry starts around the 60´s in the US but is not

until the 80s that gets an estimated size of USD 750 million

The industry targets accelerated growth of young companies

with exits in around 2 to 7 years

VC funds not only provide capital but also a high level

network actively participating in every business it invests

Business Development Process

Brief Description Investment Focus

Private Equity / Bank Debt Hedge Funds

Bank Debt Venture Capital

High

high Low

Deal S

ize

Risk

Research Start-up Development Scalability

Venture Capital

- Project / Asset Finance

- Acquisition Finance / Private

Equity / IPO

The VC funds are usually

structured for a 10 year tenure

They usually are either in the

Start-up or the Development

stages of the process Seed Capital

Angels

2. Venture Capital History in Chile

6

2. Venture Capital History in Chile

1997 Incentive Program Investment Funds

(F1 Line)

2005 Incentive Program Investment Funds Risk Capital (F2 Line)

2006 Incentive Program Investment Funds Risk Capital (F3 Line)

2008 Direct investment in Investment Funds Program (K1 Line)

2010 Re-design of the incentive programs

Start-Up Chile in launched

2011 Fénix Program

2012 Early Stages Incentive Program (FT Line)

2.1 Timeline Overview

The VC Industry in Chile has aggressively expanded during the last 4 years primarily because of the various incentives the Chilean

government has granted to the industry since 1997 through the National Development Corporation (CORFO for its acronym in Spanish)

It’s not until 2010 that the industry jumps into something real with the re-design of the Inventive Programs and the creation of Start-up Chile,

today known as a world class incubator/accelerator program for entrepreneurs around the world

Even though the industry has shown activity, most of its investments have occurred in the later development stages of a company which

has closely related to a more Private Equity approach rather than a “true” Venture Capital one

3. General Overview of the VC&PE Industries in Chile

8

0

5

10

15

20

25

0

10

20

30

40

50

60

70

80

Investment # of Startups

3. General Overview of the VC&PE Industries in Chile

3.1 General Description

The VC&PE industry in Chile accounts for over 40 funds and

a total amount of realized investments of around $460 million

The average ticket invested is nearly US$ 2.6 million where

almost 80% of the tickets supersede the US$ 1 million

threshold

During the last 4 years, the average ticket has decreased

nearly 70%, closing US$1,1 millions in 2013

On the flipside, during those same 4 years the amount of

impacted companies has rapidly increased

As of December 2013, over 165 companies have been

impacted, being that same year the year record with over 22

investments

Average Ticket per Investment per Year

Ticket Distribution by Investment

0

1

2

3

4

5

Source: CORFO Source: CORFO

22%

38%

27%

12%

< 1.000.000 MM < 3.000.000 MM

< 5.000.000 MM < 7.000.000 MM

Invested Amounts & Impacted Companies

Source: CORFO

US$ MM US$ MM # Startups

𝑥

9

0

20

40

60

80

100

120

140

3. General Overview of the VC&PE Industries in Chile

3.1 General Description (cont.’)

Aproved Lines by Corfo per Year

Fund Size Distribution

0

2

4

6

8

10

12

The tendency towards lesser average tickets is positively

correlated to Chilean government incentives, a better

understanding of how the industry works, and a development

of the ecosystem

The majority of the funds in Chile have a size of around US$

15 to US$ 20 millions

Over the last couple of years, CORFO has approved lines for

VC investment of over $650 million

Sample of companies Chilean funds have invested during

the last couple of years: Source: CORFO

Source: CORFO

US$ MM

Source: CORFO

$ 5M $ 10M $ 15M $ 20M $ 25M $ 30M $ 35M

10

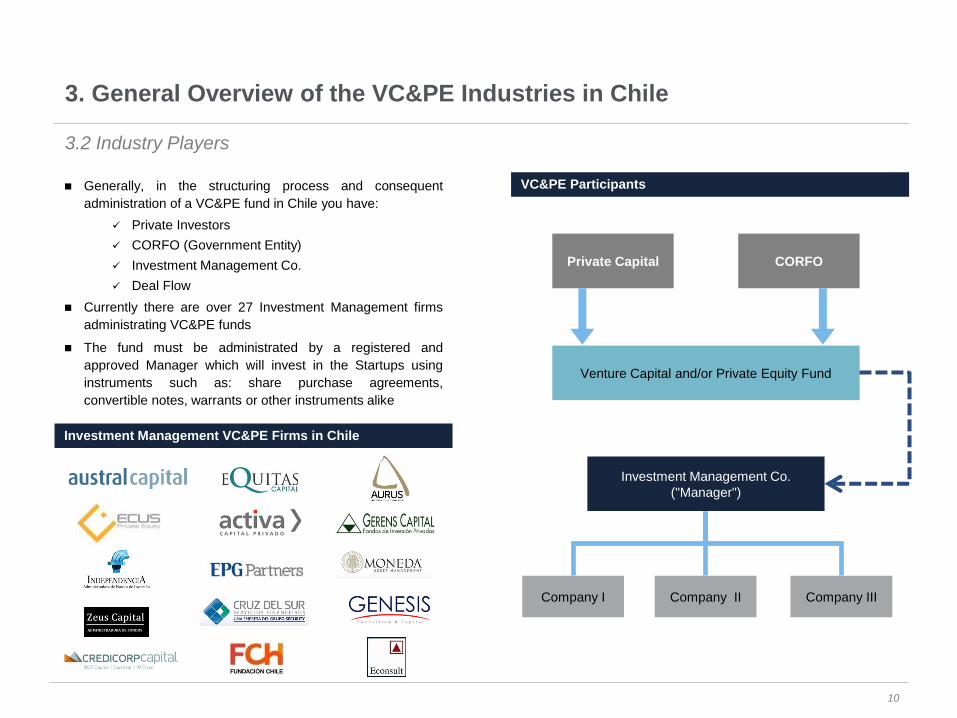

3. General Overview of the VC&PE Industries in Chile

3.2 Industry Players

Generally, in the structuring process and consequent

administration of a VC&PE fund in Chile you have:

Private Investors

CORFO (Government Entity)

Investment Management Co.

Deal Flow

Currently there are over 27 Investment Management firms

administrating VC&PE funds

The fund must be administrated by a registered and

approved Manager which will invest in the Startups using

instruments such as: share purchase agreements,

convertible notes, warrants or other instruments alike

Private Capital CORFO

Venture Capital and/or Private Equity Fund

Investment Management Co.

("Manager")

Company I Company II Company III

VC&PE Participants

Investment Management VC&PE Firms in Chile

4. Current Opportunities in Chile for Venture Capitalists

12

4. Current Opportunities in Chile for Venture Capitalists

4.1 Local Investment & Deal Flow

Up to date, the majority of the funds deployed by the industry

are destined to mid sized companies leaving a great number

of early stage startups without financing

Due to the number of incubators in Chile, there is a great

amount of Startups requiring small tickets at early stages

A great number of Startups looking for financing are

targeting foreign investors because of the limited tickets

given locally within the US$50.000 y US$1.000.000 range

Although there are some accelerator programs starting

operations in Chile, Startups’ ecosystem needs more

Understanding of how early stage financing works is a must

Examples of Incubators in Chile Current GAP

Financing Cycle

850 startups

financed

US$ 30MM+

contributed by

CORFO

40% growth on

application

volume

~35% have

raised US$ 96

MM aprox.

following

graduation

80% of the

capital raised

is comming

from abroad

Average

investment US$

50.000 to US$

4MM

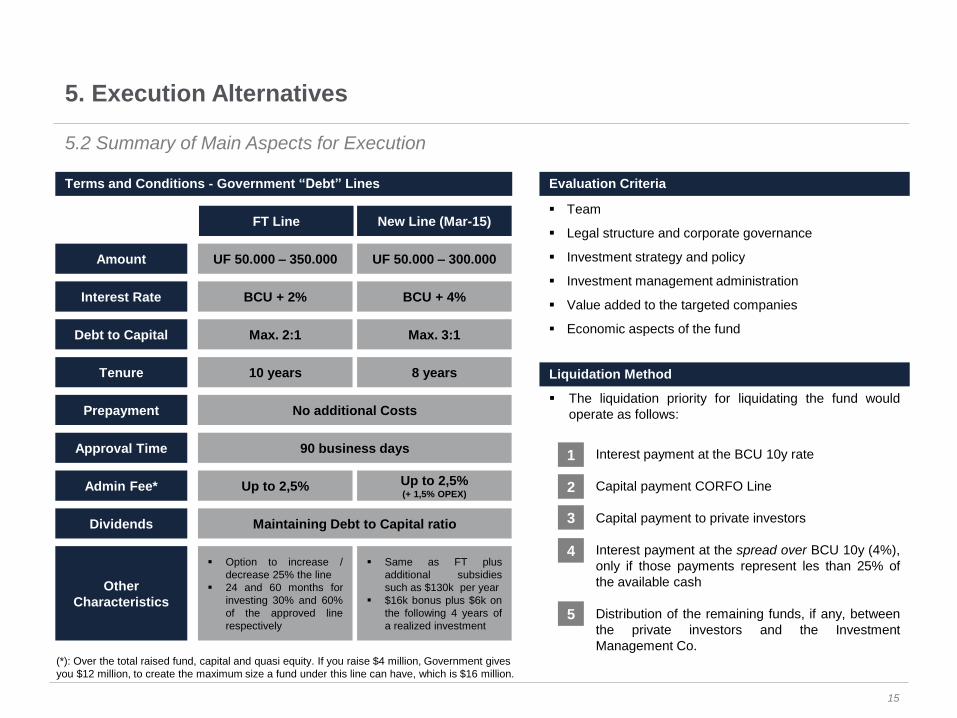

5. Execution Alternatives

14

5. Execution Alternatives

5.1 Opportunity Description

Considering current incentives given and financed by the government, in order to foster the Venture Capital industry for early stage

financing, there’s a clear opportunity for new players to enter the industry

The government is pushing hard for granting lines to foreign investors who can prove track record and can contribute with nurturing the

network abroad

The government debt given as a quasi equity contribution, the leverage ratio and the interest rates offered are a great opportunity for

diminishing associated risks to this type of funds

Chile is considered to be a good place for setting up a Hub to target LatAm markets

Currently, the government is giving two possible alternatives for Investment Funds wanting to enter early stage ventures: The FT line and a

new line to be approved and launched during the first quarter of 2015 supporting the foundation and/or arrival of new accelerators

Early Stage - FT Line Early Stage – New Line*

Fund Size Max. US$ 40 millions Max. US$ 16 millions

Ticket US$ 300.000 – 5.000.000 US$ 20.000 – 500.000

Premoney Valuation US$ 3.000.000 – 25.000.000 US$ 250.000 – 2.000.000

Time Since Conception 1 – 3 years Up to 18 months

Breakeven Milestone 1 – 3 years 2 – 4 years

Targeted Ownership (%) 10% - 25% 7% - 25%

Expected Exit 2 – 7 years 3 – 7 years

Targeted Return on Investment x10 – x30

(*): Conditions described for this new line can change expected to be launched on March 2015

15

5. Execution Alternatives

5.2 Summary of Main Aspects for Execution

Amount

Debt to Capital

FT Line New Line (Mar-15)

Up to 2,5% Up to 2,5% (+ 1,5% OPEX)

UF 50.000 – 350.000 UF 50.000 – 300.000

Max. 2:1 Max. 3:1

Admin Fee*

Interest Rate BCU + 2% BCU + 4%

Tenure 10 years 8 years

Prepayment No additional Costs

Approval Time 90 business days

Dividends Maintaining Debt to Capital ratio

Other

Characteristics

Option to increase /

decrease 25% the line

24 and 60 months for

investing 30% and 60%

of the approved line

respectively

Same as FT plus

additional subsidies

such as $130k per year

$16k bonus plus $6k on

the following 4 years of

a realized investment

(*): Over the total raised fund, capital and quasi equity. If you raise $4 million, Government gives

you $12 million, to create the maximum size a fund under this line can have, which is $16 million.

Terms and Conditions - Government “Debt” Lines

The liquidation priority for liquidating the fund would

operate as follows:

Interest payment at the BCU 10y rate

Capital payment CORFO Line

Capital payment to private investors

Interest payment at the spread over BCU 10y (4%),

only if those payments represent les than 25% of

the available cash

Distribution of the remaining funds, if any, between

the private investors and the Investment

Management Co.

Liquidation Method

1

2

3

4

5

Evaluation Criteria

Team

Legal structure and corporate governance

Investment strategy and policy

Investment management administration

Value added to the targeted companies

Economic aspects of the fund

6. Understanding the Accelerator Model

17

6. Understanding the Accelerator Model

6.1 Main Characteristics of an Accelerator Program

Accelerator programs officially start with Y Combinator in 2005

Consists on an intensive 3 months program, targeting rapid

growth and development of a starting business

It includes educational components, speakers and support of a

vast network of mentors with experience on different industries

It promotes networking among entrepreneurs creating virtuous

cycles within the different participating Startups

In exchange of capital, mentorships, network and other perks,

Startups give 4% to 9% participation through instruments such

as SAFEs, Convertible Notes or Equity

General Overview

Alumni

Advantages

Accelerators

Less investment risk , among other things, due to:

Smaller investment ticket

Know, improve and accelerate a Startup during the term

of the program

Management can be tested in-house by their day to day

decision making

Available mentor feedback constantly challenging the

viability of the Startup

Network

Good accelerator programs increase success probabilities of a

Startup between 10% and 15% after the 5th year in the US

More than 700

since 2005

Valued portfolio of

over US$ 30 bn

US$ 120,000 – 7%

average

investment -

participation

More than 400

startups sincce

2007

~89% still active or

has been acquired

US$ 18k – 6%

$100k extra

More than 800

startups since

2010

Present in more

than 40 countries

US$ 100,000 – 7%

$500k extra

18

6. Understanding the Accelerator Model (Cont.’)

6.1 Main Characteristics of an Accelerator Program (Cont.’)

Accelerator's Ecosystem Results

Company

Estimated Returm*

Seed Capital Last VC

Zynga 860x 4x

Groupon 410x 5x

Twitter 316x 4x

MySQL 103x 3x

DropBox 16x 6x

AirBnB 53x 3x

According to US statistics, 80% of the startups graduating from

an accelerator program should achieve financing rounds on

the following 3 to 6 months from Demo Day

In the US, VCs and Angels financed around 1.500 startups and

50.000 respectively. While a VC finances 1/400 investments

reviewed, an Angel finances 1/40

There is a consistency towards obtaining higher returns on

early stage investments with the accelerator program model

(*) Source: Nxtp.Labs

Startups

Angels

Venture

Capital

Network

Mentors

Universities

Pitch / Demo

Day

The admissions rate of an accelerator is as

challenging as the top schools in the US with an

incredible 1 to 10% acceptance rate

Investors who could follow Startups during the

accelerator program or after the Demo Day

Investors who could follow Startups during the

accelerator program or after the Demo Day

Developed through the program and include

other entrepreneurs, startups, mentors,

investors, etc.

People with business knowledge, entrepreneurial

experience or a particular ability that will

accompany Startups helping them develop and

expand their businesses

Important resource for deal flow coming from full

time students or associated incubators

Closing event of a graduated generation which

shows how ready Startups are for receiving real

time investment

19

An idea of what you would need for setting up an accelerator

(apart from one of the most important things: Network):

6. Understanding the Accelerator Model (Cont.’)

6.2 A Chilean example of an Accelerator program to launch

How does it works Requirements

Process

1 month 2 months 3 months 3 – 6 following months

To admitted Startups:

- Office Space

- Mentorship

- LatAm Network

- Academic Program

- US$ 25.000 for 7%

Team Resources

Manager

Hacker

Associate / Analyst

Associate / Analyst Intern

Office Space

Mentorship

Academic Program

US$ 25.000 investment per

Startup

- 10 to 15 startups per cycle (10% of the applicants)

- 2 to 3 cycles per year

- Constant Business Testing and Market Fit improvement

Mentorships

Courses

Talks - Pitch / Demo Day

- Financing rounds

- Optional additional financing of

US$100.000 – 150.000

1. Admission: The admission process can take between 2 to 3

months from application to final admission. The small ticket

investment in exchange of participation follows final admission

2. Courses, Talks, and mentorships: Part of the essence of the

program that strengthen the educational component of it.

Facilitates networking among entrepreneurs with other potential

investors and mentors in order to improve and develop their

businesses

3. Demo Day: Closing event symbolizing the graduation of the

program were every Startup presents their business to potential

investors

4. Additional Financing: Exiting the program, entrepreneurs will

need to secure additional financing from VCs, and or Angels

VCs, Angels or others

Courses

20

Special thanks to those who participated in the conception of this brief presentation, specially to: Carla Munizaga, Ismael Ugarte, Nicolás Sanchez, and Cristián Anfossi

![[vc 1037 - listing.archiviolocation.com · [vc 1037] ARCHIVIOLOCATION.COM [vc 1037] ARCHIVIOLOCATION.COM [vc 1037] ARCHIVIOLOCATION.COM [vc 1037] ARCHIVIOLOCATION.COM. archivio location](https://static.documents.pub/doc/80x56/5fcd99d1df347e1ae154645c/vc-1037-vc-1037-archiviolocationcom-vc-1037-archiviolocationcom-vc-1037.jpg)