23

A Primer on Corporate Venture Capital Investing Background Ho w compa nies use it Different models, pros and cons Strategic vs. Financial Goals Key Lessons Case examples

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 1/23

A Primer on Corporate

Venture Capital Investing

� Background

� How companies use it� Different models, pros and cons

� Strategic vs. Financial Goals

� Key Lessons

� Case examples

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 2/23

Background� Venture capital investing has grown rapidly over the last 20 years

� Corporate-backed venture capital investments have grown even morerapidly

� 1997 - 30 corporate venture capital funds; 2000 - 300+ such funds, andcounting«

� Intel is the poster child of this revolution with $7B under management;major bottom line impact

� Past efforts of corporations have often been failures (Xerox, Exxon) -many reasons, but often because they are built on a product based

paradigm

� That¶s not how successful ventures work: customer (need) focused,competence-based

� Few (5-7%) of entrepreneurs follow their initial business plan

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 3/23

More Background

� Comment made that there is too much money chasing deals(drive-by-fundings)

� Market doesn¶t like companies to invest in other public

companies, even if successful (Adobe/Yahoo)

� ³This is an inopportune time to be a rookie at this´

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 4/23

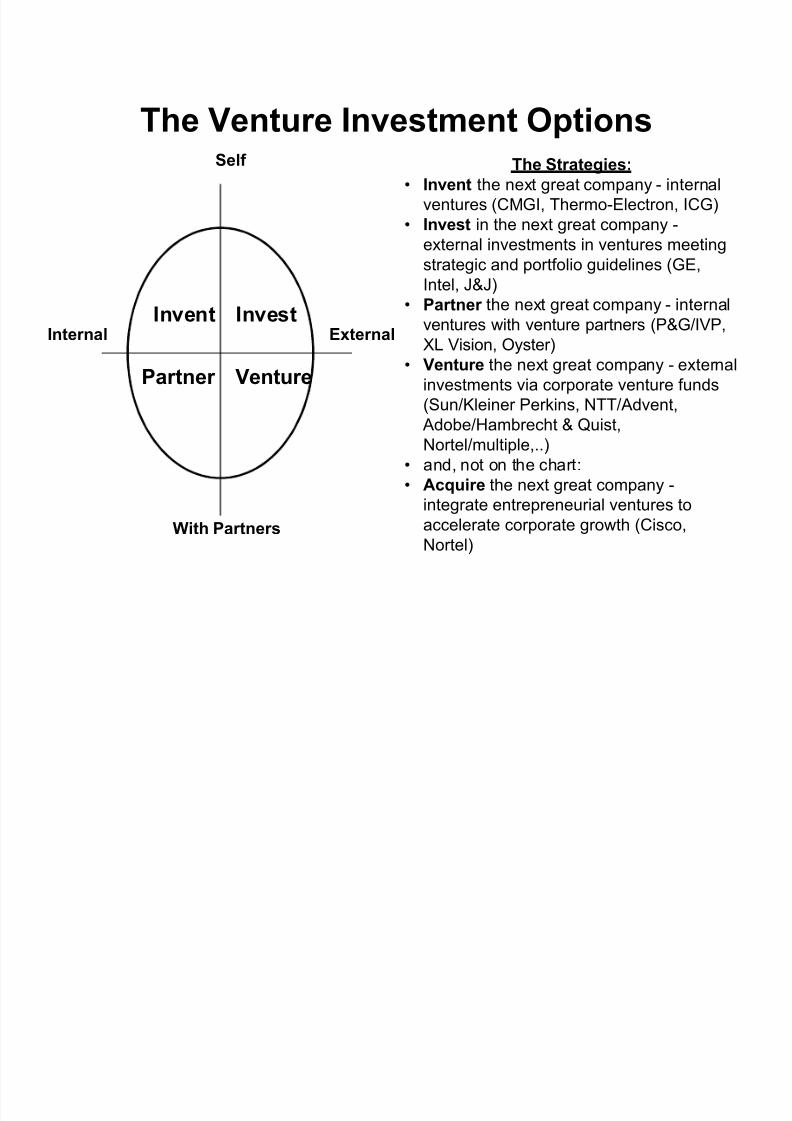

The Venture Investment OptionsSelf

With Partners

Internal External

Partner

Invent Invest

Venture

The Strategies:

� Invent the next great company - internalventures (CMGI, Thermo-Electron, ICG)

� Invest in the next great company -external investments in ventures meetingstrategic and portfolio guidelines (GE,Intel, J&J)

� Partner the next great company - internalventures with venture partners (P&G/IVP,XL Vision, Oyster)

� Venture the next great company - externalinvestments via corporate venture funds(Sun/Kleiner Perkins, NTT/Advent,

Adobe/Hambrecht & Quist,Nortel/multiple,..)

� and, not on the chart:� Acquire the next great company -

integrate entrepreneurial ventures toaccelerate corporate growth (Cisco,

Nortel)

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 5/23

Venture InvestmentM

odels� 1st decision: invest directly or through a VC firm

± Direct saves a lot of money (VC¶s take 20-30% of gains)

± Bad news is: once employees learn the trade, they leave to

become VC¶s!

� VC¶s run pooled funds (multiple investors) or directed funds(single investor)

± Large differences in levels of proactivity on part of investors

± Fee and participation structure very negotiable

± ³Good´ clients can negotiate co-investment rights and access todeal flow

� Larger Investors can go direct by setting up standalonesubsidiaries that allow their deal-makers to be compensated likeVC¶s

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 6/23

Strategic Vs. Financial Goals� No consensus on strategic value of VC investing (but

remember, 90% of investments are <3 years old!)

� There is consensus on the financial value of VC investing

� Comment by fund managers: financial results are your onlydefense!

� Companies vary widely in their use of strategic screens for their investments

� Best practice seems to be to treat the investments as financial

plays, but to use the strategic and technical strengths of theinvestor to improve the deal and the results

� The darker side: VC investments provide a rich source of gainsand losses that can be realized selectively and dropped to thebottom line to manage earnings.

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 7/23

Cases:

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 8/23

Cisco: ± Have no R&D, build new businesses by acquiring

and integrating

± Target is startups that don¶t want the hassles of going public

± Have 2% turnover after acquisitions

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 9/23

Thermo-Electron: ± Model is to spin out internal ventures

± A chief scientist has ~3 years to found a business

and take it out (gets 1/2-1% equity) ± Will raise outside capital or go straight to IPO, or

may buy shell companies to house venture

± Money back guarantee to investors

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 10/23

Nortel: ± Limited partner in 5-6 venture funds

± Negotiate side by side agreements, and get to

look at ~80% of deal flow ± Has led to direct acquisitions (Bay networks)

± Also do internal ventures but find these too timeand resource intensive

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 11/23

Advent International (Boston-

based VC firm) ± Have $4B under management, 16 offices, 100

professionals

± Manage pooled and directed funds - work closelywith corps to develop strategic value, co-located

± Minimum investments: pooled fund: $10M,dedicated fund: $30M

± Don¶t allow investors to veto choices ± Deal flow stricture: look at 7,500/yr, log in 3,500-4,000, determine 1,000-1,500 to be qualified, do300-500 detailed studies, make 30-50 investments

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 12/23

AT&T Labs: ± See R&D as a profit center

± Invest technology, IP, not cash - want to put

technology in a company that will commercialize itand sell it back to divisions

± Will take in VC money and syndicate a deal

± Don¶t discuss their investments with their divisions

± Divisions still contract with the labs for their sustaining technologies

± Work their networks of VC¶s for deal flow

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 13/23

DOW Chemical ± Started fund in 1995 as a ³self-financing program

for access to early stage technologies of

relevance to Dow ± Saw poor results at peer companies - R&D based,strategically oriented, un-diversified

± ³Subordination of financial to strategic criteria isusually fatal´

± Work through selected funds that see Dow as avalue-added investor (source of deal flow)

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 14/23

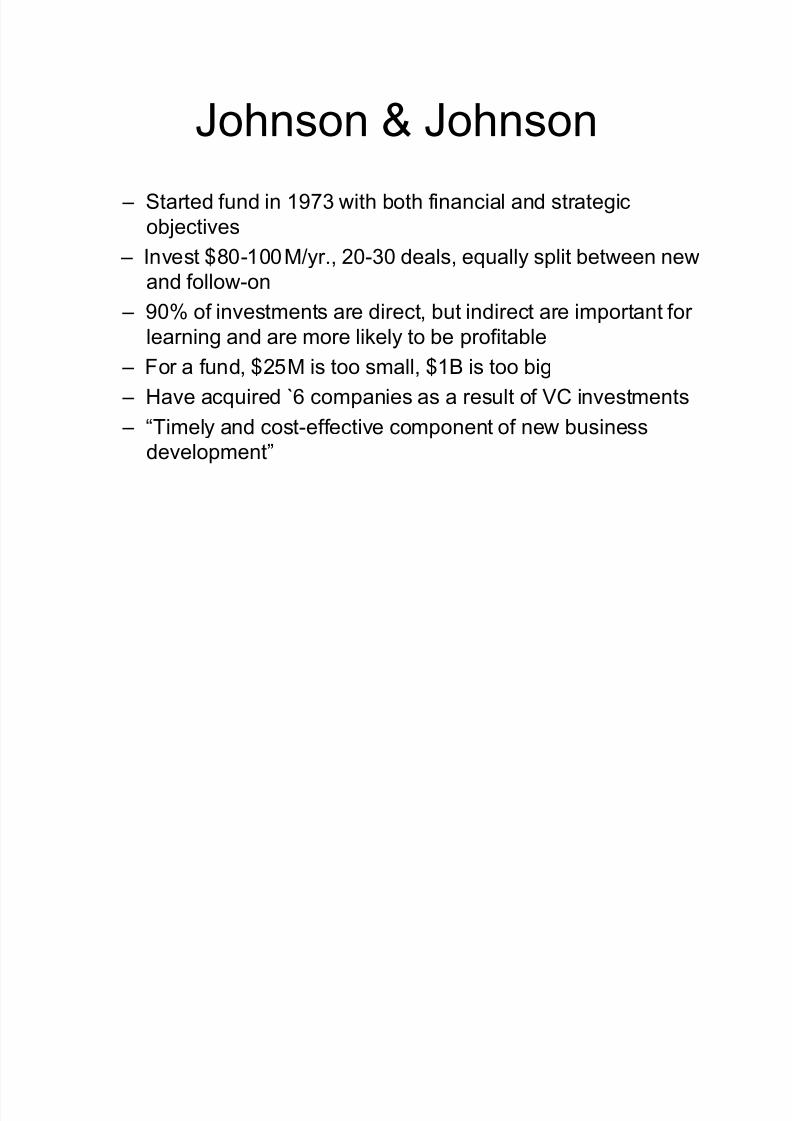

Johnson & Johnson ± Started fund in 1973 with both financial and strategic

objectives

± Invest $80-100M/yr., 20-30 deals, equally split between new

and follow-on ± 90% of investments are direct, but indirect are important for

learning and are more likely to be profitable

± For a fund, $25M is too small, $1B is too big

± Have acquired `6 companies as a result of VC investments

± ³Timely and cost-effective component of new businessdevelopment´

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 15/23

Sonera ± Found it necessary to separate internal and external

ventures (external need fast decisions and a long-term viewof profits)

± Make 8-12 investments per year at $1-5M per + follow-on¶s ± Target - 50% of investments should have some sort of

business or technology relationship to divisions

± Narrow technology focus, but see 1,000 deals/year

± Make both direct and fund investments

± Lessons learned: this is a top management issue, it needs toreport there, need the right people, your reputation andnetwork are critical to deal flow

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 16/23

Philips Electronics ± Started venture fund 1998, because: mature businesses,

excessive reliance on internal R&D

± Define targets within scope of existing business, but not yet

realized ± Part of corporate strategy office, 9 people, BOD approves all

deals.

± Invested $40M last year, $100-150 this year

± Direct investments only, 2cond round or later, $1-10M, 5-

20% equity

± Priorities are financial, but normal to have a businessrelationship between a target and a division

± Sometimes conflict with divisions if they want things likeexclusivity; if so, VC group will not invest

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 17/23

GE Equity ± 8 years old, have $4B invested, 350 individual

investments

± Have 5 basic practices, 110 professionals ± 1/3 of deals come through divisions

± Investments in 75 funds to maintain relationships

± Have an alumni network - employees that have

left to work for VC¶s ± Develop deal flow by researching technology,

personal relationships

± ³Winners´ don¶t come over the transom very often

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 18/23

Intel Capital� Have 150 ³deal doers´, attached to business units

� Most deals have matching business agreements

� Mostly invest side by side with VC¶s� 1999 was first year to go outside US - went to 30%

� Use observer seats on boards for transparency

� Once an investment is OK¶d to sell, it is turned over

to corporate treasury

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 19/23

OneM

otorola Ventures� Different from Motorola Inc. portfolio - designed to be

³out there´

� Proposed in 1997, split out of corporate strategy -weren¶t getting good early stage deal flow

� Have $200M invested in 40 companies

� Develop shopping lists with divisions

� Also put on ³fashion shows´ for divisions - intelligencegathering point

� Struggled in early days to get BOD approval for alldeals - now a streamlined board

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 20/23

Miscellaneous Facts

� Investment cycle: ± decision -1 week, completion - 1 month (East River Partners)

± 3-10 weeks, 6-8 weeks normal (GE Equity)

� Money is more nervous now, longer due diligence,³no shop´ clauses and breakup penalties

� Funds may establish ³friends and family´ side funds(no carrying fees) to motivate associates to refer

deals

� Most investors don¶t take board seats, some takeobserver seats

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 21/23

Specific Issues for

Corporations� VC¶s like corporate investments:

± acquisition potential is an additional end-game

± ventures with corporate investors are more often successful than

those without� But, corporate money is still often seen as dumb money, pay a

premium to invest (need to push back on this)

� What corporations need to be successful:

± dedicated (independent) VC arm

± committed money ± single point of contact (and keeping of key personnel)

± follow-on money

� Insist on transparency

� Avoid deals that are captives of Fortune 500 companies

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 22/23

Key Learnings� Deal flow is key

� Ventures are structured around liquidityevents (IPO¶s or acquisitions)

� Financial considerations must prevail

� Venture activity is strongly concentratedin a few industries (IT, e-commerce, lifesciences)

8/7/2019 Venture Capital Primer

http://slidepdf.com/reader/full/venture-capital-primer 23/23

Recommendations� Venture funding is an important part of new business

development

� the choice of how to do it depends on the corporate vision, and

how the company structures to get the value out of theinvestments

� To learn the ropes, it is almost mandatory to start by investing inexisting VC funds

� These relationships should be leveraged to gain co-investment

rights as we bring more to the table.� Since most VC activity is concentrated in areas removed from

our core businesses, we can add value by developing deal flowin non-traditional areas

![VENTURE CAPITAL FOR SUSTAINABILITY 2007 REPORT [2007] Venture Capital... · growing sector as Venture Capital for Sustainability ... Venture Capitalists’ stake in ... Venture Capital](https://static.documents.pub/doc/80x56/5a7926b77f8b9a00168dc540/venture-capital-for-sustainability-2007-2007-venture-capitalgrowing-sector.jpg)