64

Chapter 9: An Analysis of Conflict Vicki Curtis, Jeremy Wei, Jordan Hill, Cody Rice

| Date post: | 15-Dec-2015 |

| Category: |

Documents |

| Upload: | katie-esham |

| View: | 214 times |

| Download: | 0 times |

Chapter 9: An Analysis of Conflict

Vicki Curtis, Jeremy Wei, Jordan Hill, Cody Rice

Agenda

Introduction to Game Theory Non-Cooperative Game Theory Cooperative Game Theory Implications Holmstrom Reconciliation and Conclusion of

Chapter 9 Article: Project Earnings Manipulation:

An Ethics Case Based on Agency Theory

Introduction to Game Theory

Underlies many current issues in financial accounting theory

Models the interaction of two or more players

Occurs in the presence of uncertainty and information asymmetry

Game theory is more complex than decision theory and the theory of investment

Another View

The number of players lies “in between” the number in single person decision theory and in markets.

In game theory the number of players is greater than one, but is sufficiently small

Types of Games

Many different types of games Classified as cooperative or non-

cooperative Cooperative game: parties can enter

into a binding agreement. Non-cooperative game: an

oligolopolistic industry is an example of a non-cooperative game

Non-Cooperative Game Theory

Single-Period Game

Constituencies of financial statement users

Both parties are aware of the other parties reactions in making their decisions

Game theory provides a framework for studying the conflict and predicting what decisions the other party will make

Classified as a non-cooperative game

Utility Payoffs in a Non-Cooperative Game

Answer

RD Since both parties know the other

parties strategy this is the only strategy pair that each party will be satisfied with his or her decision.

This is called the Nash Equilibrium

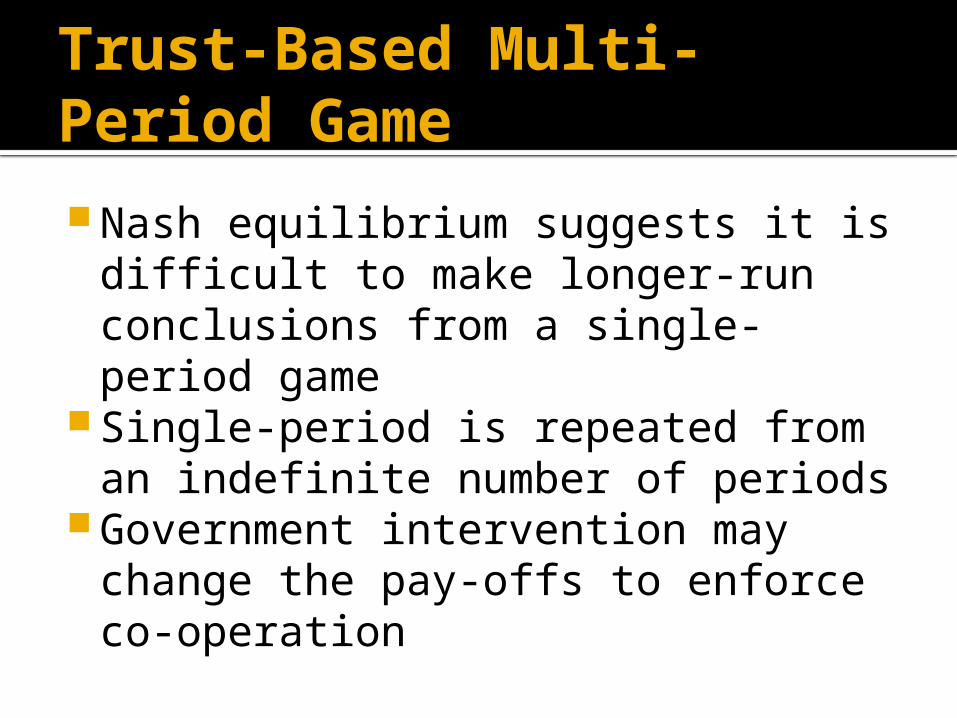

Trust-Based Multi-Period Game

Nash equilibrium suggests it is difficult to make longer-run conclusions from a single-period game

Single-period is repeated from an indefinite number of periods

Government intervention may change the pay-offs to enforce co-operation

Trust-Based Multi-Period Game

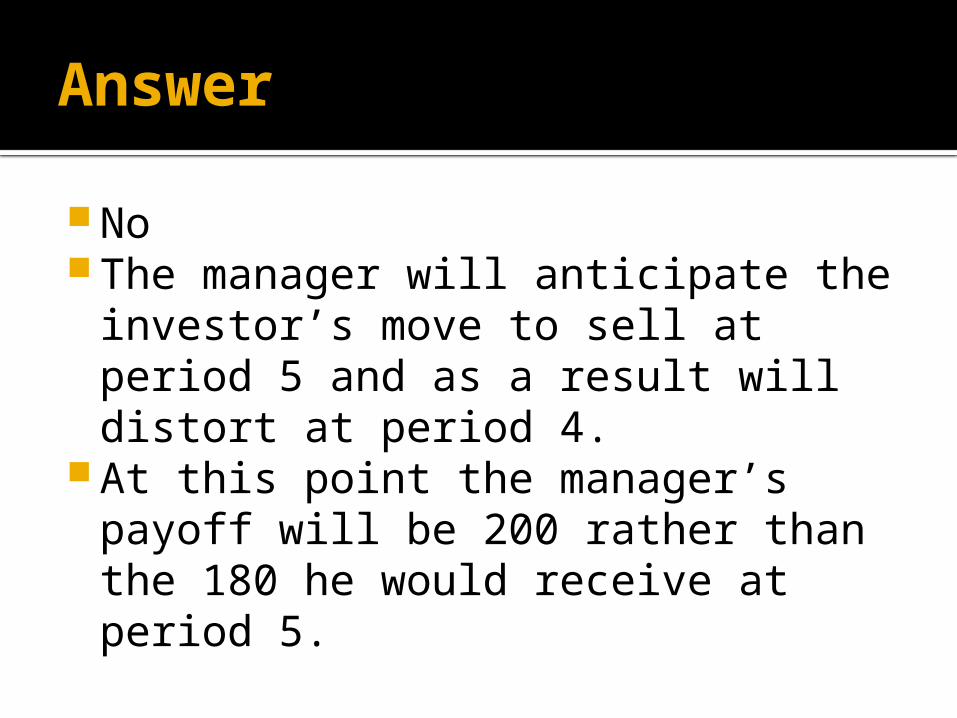

Answer

No The manager will anticipate the

investor’s move to sell at period 5 and as a result will distort at period 4.

At this point the manager’s payoff will be 200 rather than the 180 he would receive at period 5.

Trust-Based Multi-Period Game

Answer

Further to the strategy just explained, the game would continue to unravel as both parties anticipate that the other will end the game on their next turn.

This goes all the way back to period 1 where the investor will end the game and players receive the Nash equilibrium pay-offs of the single-period game

Co-operative Game Theory

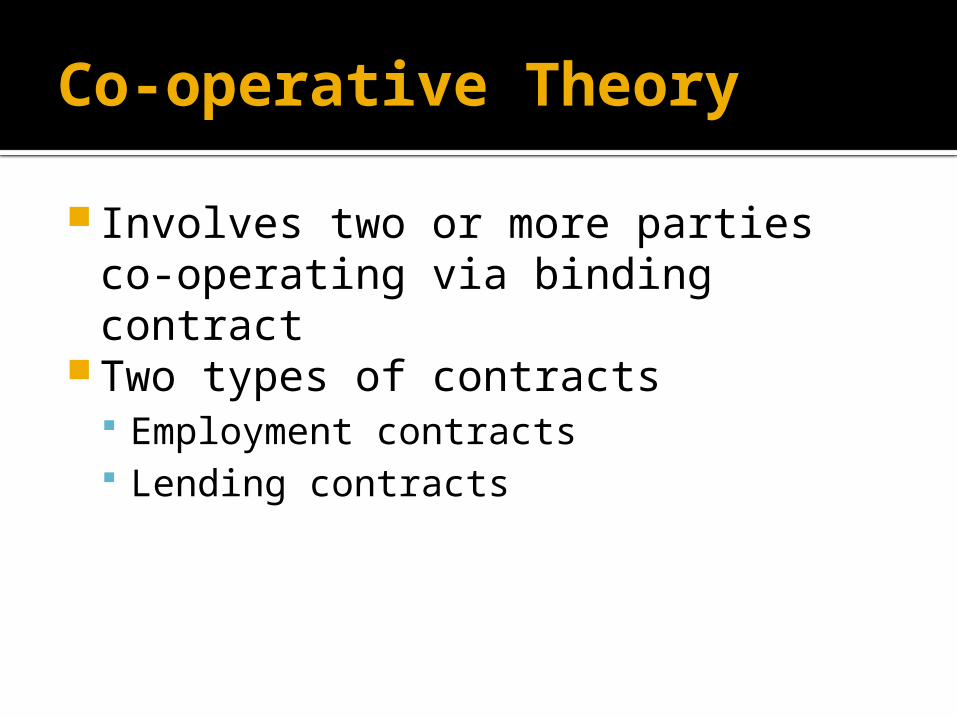

Co-operative Theory

Involves two or more parties co-operating via binding contract

Two types of contracts Employment contracts Lending contracts

Agency Theory

A branch of game theory that studies the design of contracts to motivate a rational agent to act on behalf of a principal when the agent’s interest would otherwise conflict with those of a principal Main concept is principal vs. agent

Agency Theory Illustration

Game Inc.

Game Theory Outline

Owner Maximize their payoff (expected cash flow)▪ First Best: option with highest pay off▪ Second Best: option with second highest pay off

Manager Maximize their utility (expected benefit)

Agency Cost Difference between first best and second

best Must minimize this cost

Game Inc.

Game Inc. is a company that has a single owner and single manager Owner = principal Manager = agent▪ Manager gets paid $25 per year

In this company, there are two possible payouts: Good times (G) = $100 Bad times (B) = $55

Payout and Utility

Payout Represents the receipt of cash generated by

the company Measured by expected cashflows▪ E(cf) = p(x1) + p(x2)....p(xz)

Utility Represents the net benefit for the manager’s

effort Measured by square root of monetary

compensation net of disutility▪ E(u) = √(x) - D

Manager

The manager has two choices Work hard Slack off

If the manager works hard: Probability of G = 0.6 Probability of B = 0.4

If the manager slacks off: Probability of G = 0.4 Probability of B = 0.6

Payoff Table

Work Hard (W) Slack Off (S)

Pay-off Probability Pay-off Probability

Good Times (G) $100 0.6 $100 0.4

Bad Times (B) $55 0.4 $55 0.6

What the Owner Wants?

Managerial effort can increase the odds of a high payout (i.e. $100) Therefore a rational owner would want

the manager to work hard Can be illustrated by their expected

payoff:

E(G) = 0.6(100-25) + 0.4 (55-25) = 57E(B) = 0.4(100-25) + 0.4 (100-25) = 48

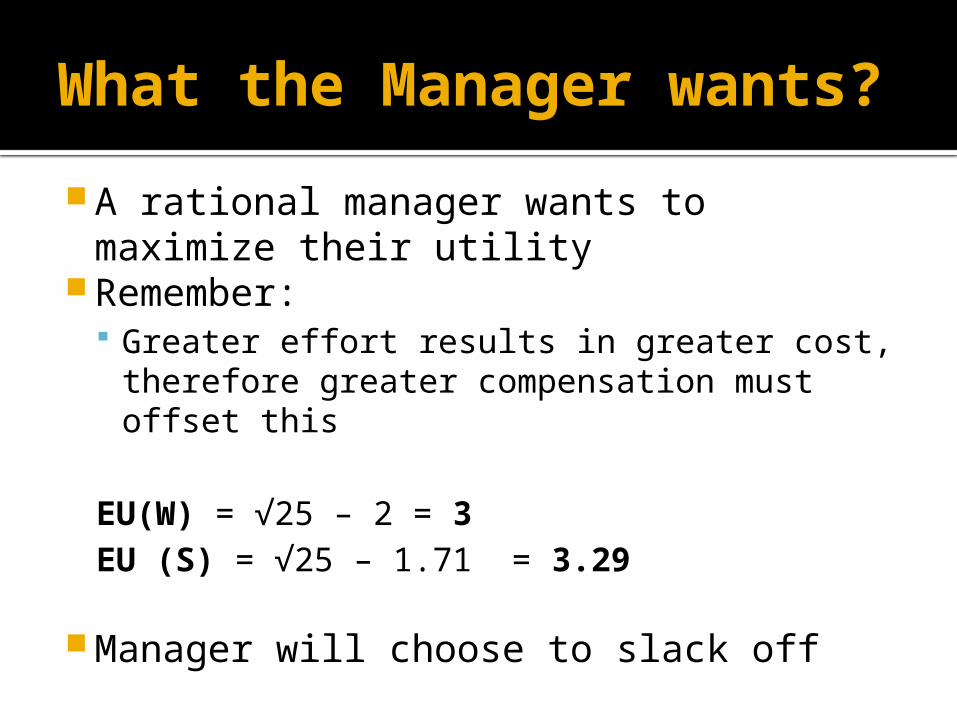

What the Manager wants? A rational manager wants to maximize

their utility Remember:

Greater effort results in greater cost, therefore greater compensation must offset this

EU(W) = √25 – 2 = 3EU (S) = √25 – 1.71 = 3.29

Manager will choose to slack off

What does this imply?

A Moral Hazard Exists!

Moral Hazard Manager will choose to slack off despite

the owner wanting them to work hard

Owner must find a way to overcome this moral hazard

What can the owner do?

1. Put up with manager slacking off2. Direct monitoring of managerial

performance3. Indirect monitoring of managerial

performance4. Rent company to manager5. Share pay off with manager

Remember: Must find the option that results in the highest pay off

Put up with slacking off

Owner allows manager to slack off Evidently not ideal as this will not

result in the highest expected pay off

Agency Cost = 57 – 48 = 9

Direct Monitoring

Owner observes the actions of the manager to ensure they are working hard Thus guarantee manager works hard (W)

Ideally, the best option as this guarantees the highest pay off (G)

Realistically, impossible as owners do not have the time or resources to do this Results in an information asymmetry between

manager and owner (moral hazard)

Indirect Monitoring

Owner were to determine the manager’s effort based on the ending payoff

If pay off = B, owner would know manager slacked off

Realistically impossible since there are external factors that could effect payoff E.g. Recession, natural disaster, etc...

Owner rents the firm

Owner gives up the risks and rewards of Game Inc. in exchange for a guaranteed pay off of $51

Manager will now be willing to work hard (W) since they take on risks and rewards

Not ideal since the pay off is below ideal

Agency Cost = 57 – 51 = 6

Sharing profits with manager Based on a performance measure, the

owner could determine the pay of a manager Net income is common measure

By sharing the risks, the manager becomes risk averse (rather than risk neutral) Results in manager wanting to work hard

This is clearly most ideal option!

Note about Net Income

Net Income does not represent pay off, it is an indicator of potential payoff While it is the best indicator, it is not

perfect Imperfection due to:

Estimations Accruals

As a result, there is a risk of noisy (imperfect) net income

Updated Probabilities

Due to imperfect net income, the probabilities are now updated: If payoff is $100 – net income will be ▪ 80% chance of $115 (correct)▪ 20% chance of $40 (incorrect)

If payoff is $55 – net income will be▪ 20% chance of $115 (incorrect)▪ 80% chance of $40 (correct)

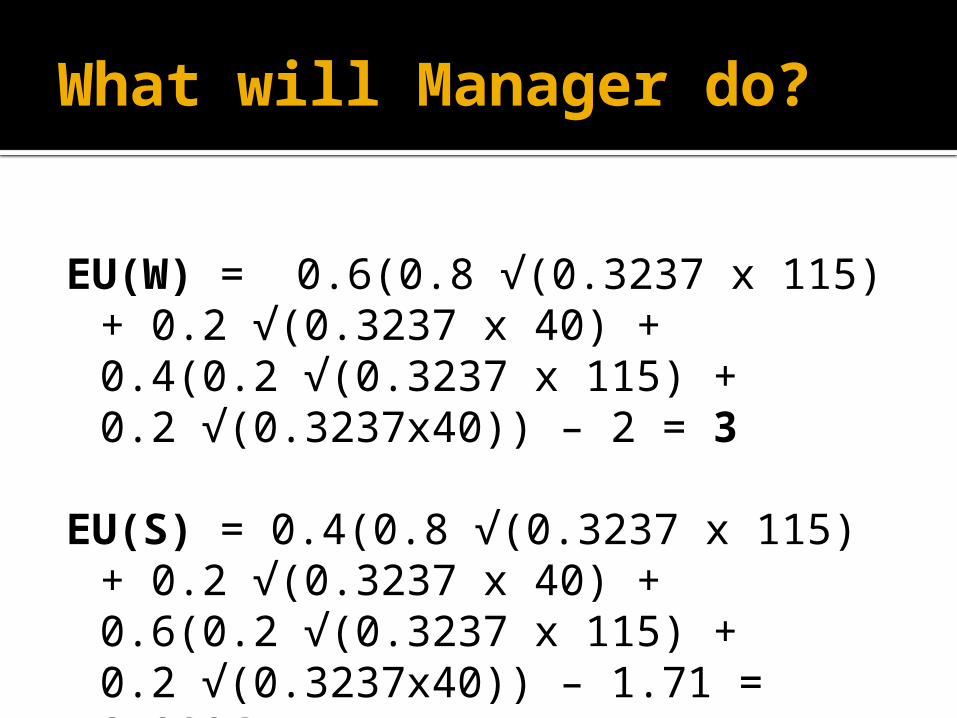

What will Manager do?

EU(W) = 0.6(0.8 √(0.3237 x 115) + 0.2 √(0.3237 x 40) + 0.4(0.2 √(0.3237 x 115) + 0.2 √(0.3237x40)) – 2 = 3

EU(S) = 0.4(0.8 √(0.3237 x 115) + 0.2 √(0.3237 x 40) + 0.6(0.2 √(0.3237 x 115) + 0.2 √(0.3237x40)) – 1.71 = 2.9896

What will the Owner get?

E(W) = 0.6(0.8(100-0.3237 x 115)) + 0.2(100 – (0.3237 x 40)) + 0.4(0.2(55-(0.3237x115) + 0.8(0.3237x40)) = 55.456

Agency Cost = 57 – 55.456 = 1.544

Implications

Appears as though we have minimized the agency costs due to the moral hazard

If accountants can improve net income to better reflect pay off, imperfections can be reduced

Results in reduced compensation risk Paying a manager for a high net income

when the actual payoff will be low

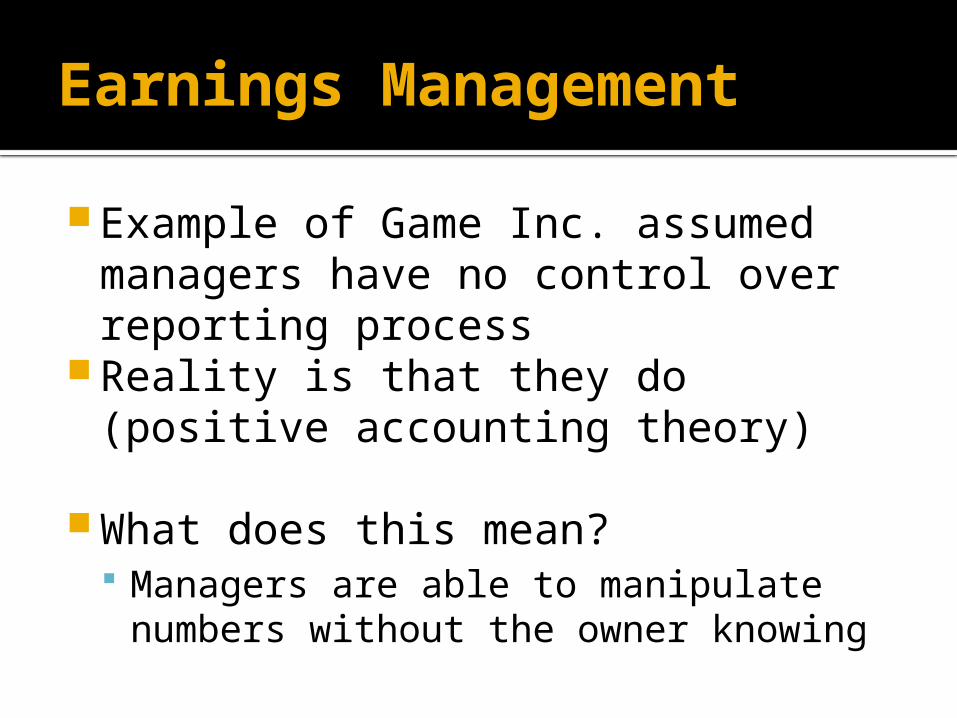

Earnings Management

Example of Game Inc. assumed managers have no control over reporting process

Reality is that they do (positive accounting theory)

What does this mean? Managers are able to manipulate

numbers without the owner knowing

Controlling Earnings Management

Through regulations like GAAP, this can prevent absolute earnings management

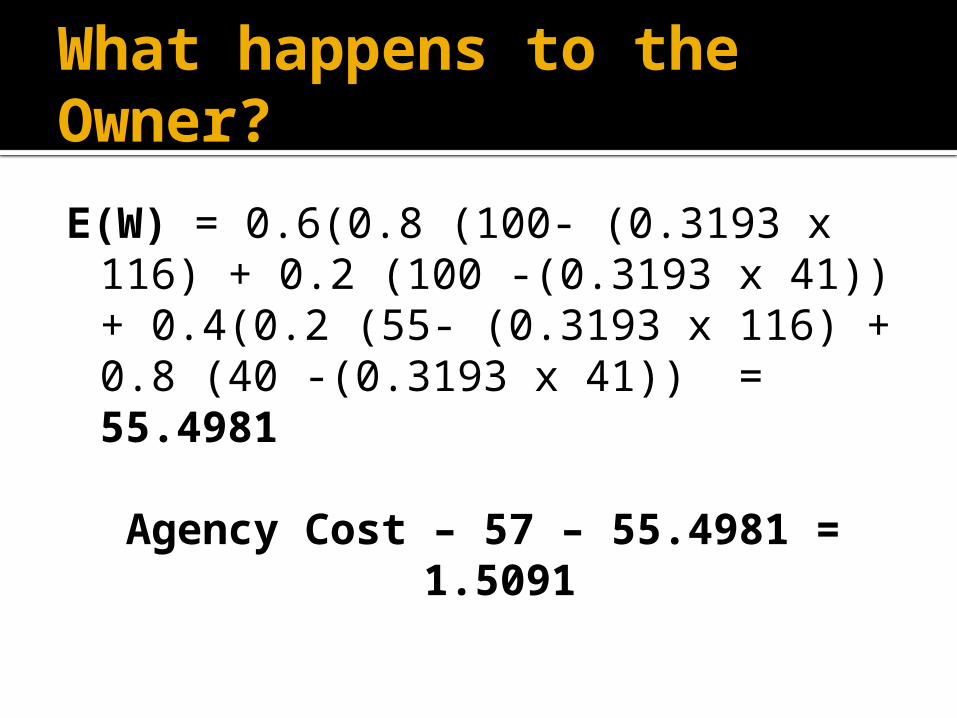

Let’s now assume Net income is a range▪ 115 = 111 – 116 ▪ 40 = 36 – 41

What will the Manager do?

EU(W) = 0.6(0.8 √(0.3193x116) + 0.2 √(0.3193 x 41)) + 0.4(0.2 √(0.3193x116) + 0.8 √(0.3193 x 41) – 2 = 3

EU(S) = 0.4(0.8 √(0.3193x116) + 0.2 √(0.3193 x 41)) + 0.6(0.2 √(0.3193x116) + 0.8 √(0.3193 x 41) – 1.71 = 2.99

As you can see, the owner will work hard

What happens to the Owner?

E(W) = 0.6(0.8 (100- (0.3193 x 116) + 0.2 (100 -(0.3193 x 41)) + 0.4(0.2 (55- (0.3193 x 116) + 0.8 (40 -(0.3193 x 41)) = 55.4981

Agency Cost – 57 – 55.4981 = 1.5091

Summary of Game Inc.

Evidently there will always be a moral hazard between managers and owners

Given the restrictions of owners ability to influence the managerial actions, there is an information asymmetry

Through accounting regulations (i.e. GAAP), accountants can influence managerial actions

Thus, reducing agency cost!

To summarize

Agency cost illustrates the role of accountants in financial reporting

Role 1: Create accounting policies that can

increase the accuracy of net income as a predictor

Role 2: Create regulations that reduce a

managers ability to manipulate net income

Bondholder-Manager Lending Contract

Bondholder-Manager Lending Contract

Principal cannot observe actions of manager

Moral hazard problem Information Asymmetry

Conflict of interest

Bondholder-Manager Lending Contract

Divergence of Interests

Raising interest rates acts as a deterrent for managers

Reduce the cost of borrowing capital Limit dividends Limit additional borrowing

Implications of Agency Theory for Accounting

Recall: Agency theory

Compensate the managers as a part of the

Holmström Agency Model Rigidity of Contracts

Holmström

Contributed to the agency model

Use of simultaneous performance measures Net income Share price performance

Performance Measure Characteristics

Performance Measure Characteristics

Sensitivity Manager effort Understand manager motivation Reserve Recognition Accounting

Precision A reciprocal of the variance of the noise How good is it predicting payoff?

Performance Measure Characteristics

Ensure both measures are: Jointly observable Relates to net income Reveals more information

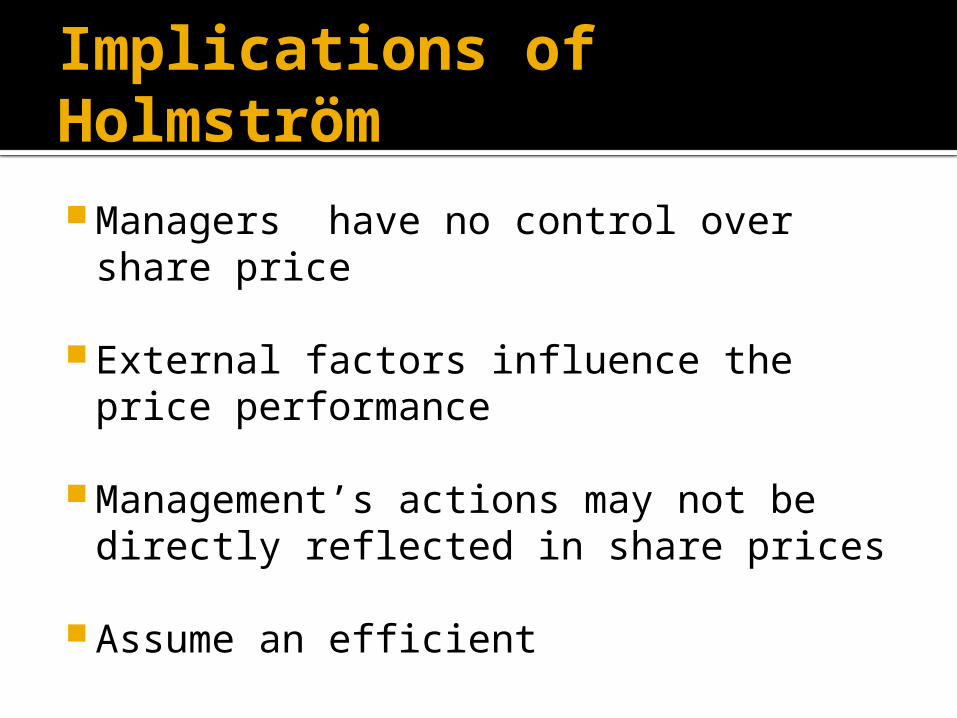

Implications of Holmström Managers have no control over share

price

External factors influence the price performance

Management’s actions may not be directly reflected in share prices

Assume an efficient

Rigidity of Contracts

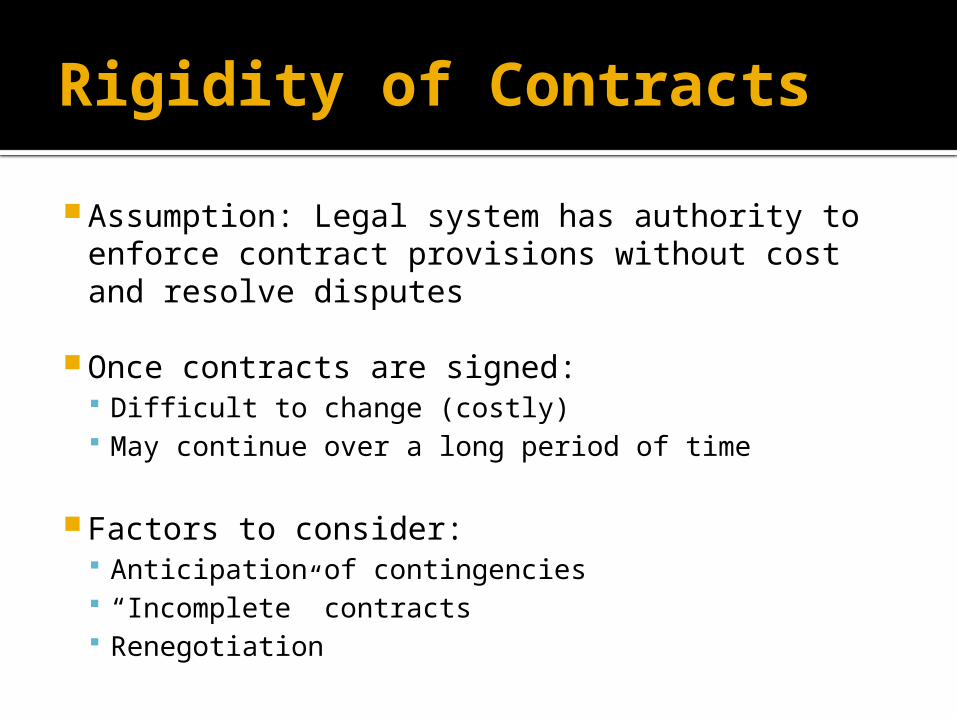

Assumption: Legal system has authority to enforce contract provisions without cost and resolve disputes

Once contracts are signed: Difficult to change (costly) May continue over a long period of time

Factors to consider: Anticipation of contingencies “Incomplete” contracts Renegotiation

Reconciliation and Conclusion

Manager’s remuneration depends on net income and lending contracts

Contract covenants affect the manager’s actions

Managers still have the ability to manipulate accounting policies irrespective of the effect on decision usefulness to investors

Reconciliation and Conclusion

Investor reaction and cost of capital is affected by accounting policy choice regardless of impact on cash flow

Means of communicating inside information to the public.

Reconciliation and Conclusion

Conflict theories

Net income’s role in motivation and monitoring manager performance

Net income competes with other performance measures

Earnings management allows shirking – lower payoffs

Project Earnings Manipulation: An Ethics Case based on Agency Theory

Sue Davies Decision

$2 million of R&D costs to allocate Could cause project she manages

incur a loss Will lose her bonus

Could allocate to other projects Upper management pressure to meet

growth targets

Question 1

How much cost should be charged to unfinished products if K(3) is to

a) break even?

What is the impact on Sue’s bonus?

Question 1

b) earn a normal level of profit?

Which scenario does she have more incentive to choose, why?

Accounting for Contracts

Contract Costs Identifiable with or allocable to

specific contracts Direct materials Direct labour Overhead

Already incurred Expected costs to complete

Question 3

Does Accounting for Contracts provide useful guidelines in this situation?

Is the decision material?

Does it matter if it is material?

Question 4

Impact on stakeholders

Who are the stakeholders? What are their rights and

expectations? What is Sue’s obligation to each?

Question 2

Decision Time!

Imagine you are Sue Davies, how would you allocate the remaining $2 million of R&D?

Why?