21

Coming Attraction: The Investment Appeal of Entertainment Production Facilities OCTOBER 2020 VIEWPOINT

Coming Attraction: The Investment Appeal of Entertainment Production Facilities

OCTOBER 2020

VIEWPOINT

OCTOBER 2020 CBRE Research © 2020 CBRE, Inc. | 2

U.S. VIEWPOINT

Contents

Executive Summary ...........................................................................................................3

Introduction ......................................................................................................................4

Production Space In An Evolving Content Landscape ........................................................5

Entertainment Employment Growth ..................................................................................7

Covid-19 Impacts ............................................................................................................11

Explosive Growth Of Video Streaming ............................................................................12

Incentives & The Global Production Ecosystem ................................................................13

Adaptive Re-Use Accelerates ..........................................................................................14

Case Study: Siren Studios, Hollywood .............................................................................15

Georgia ...........................................................................................................................16

New York ........................................................................................................................17

British Columbia ........................................................................................................ 18

Ontario ..................................................................................................................... 19

Louisiana .................................................................................................................. 20

OCTOBER 2020 CBRE Research © 2020 CBRE, Inc. | 3

U.S. VIEWPOINT

EXECUTIVE SUMMARY

• Asthemedia&entertainmentindustryentersaneraofaccelerateddemand,productionfacilitiesareanincreasinglyattractivecommercialrealestateinvestment.

• Mostofthe11millionsq.ft.ofsoundstagespaceinNorthAmericaisconcentratedinfilminghubslikeLosAngelesandGeorgia.LosAngelesaloneaccountsforhalfofthisinventory.

• Institutionalinvestorshavebeenincreasinglyattractedtothesoundstagesectoroverthepastdecade,creatingaburgeoningnewassetclasswithincommercialrealestate.

• Theentertainmentindustryisamajorspaceoccupierandemploysmorethan3millionpeopleintheU.S.COVID-19restrictionsthathavelimitedentertainmentproductioncausedatemporarydecreaseinindustryemploymentbutdemandforproductionspacehasbeengrowingrapidly,largelyduetoapandemic-related74%year-over-yearincreaseinstreamingvideodemand.

• Filmproductionlocationsareincreasinglyfar-flung,astaxincentiveprogramshavehelpedstateslikeGeorgiaandLouisianabecomemajorproductioncenters.However,traditionalentertainmenthubslikeLosAngelesandNewYorkremainprimesourcesofindustrytalent.

Eric WillettResearch Director, PSW Thought Leadership

Dan HunkerResearch Analyst, PSW Thought Leadership

Lewis HornePresident,PSW

OCTOBER 2020 CBRE Research © 2020 CBRE, Inc. | 4

U.S. VIEWPOINT

INTRODUCTION

TheentertainmentindustryhaslongbeensynonymouswithLosAngeles—thehomeofHollywood,moviestarsandmajorstudios.Itis,afterall,wherethemovieindustrybeganandithasremainedtheepicenterofglobalentertainmentoutputforwelloveracentury.Butasmovieproductionbecomesmoreexpensive,contentproductionbecomesubiquitousandindoorproductionspacegrowsscarcer,themagicofTinseltownisexpandingtootherU.S.markets.

ThisCBREViewpointdetailsthebreadthofproductionspace(commonlyknownassoundstages)acrossNorthAmericaandcomplementsCBRE’srecentreportontheLosAngelesproductionscene.Soundstageshaveoftenbeenoverlookedasattractivecommercialrealestateassetsduetotherelativelysmallsizeofthesector’sfootprint,butthedynamismofcontentcreationandtheexpandingreachofinstitutionalcapitalischangingthis.Indeed,soundstageshavebecomeaburgeoningassetclassamonginstitutionalinvestorsoverthepastdecade.

OCTOBER 2020 CBRE Research © 2020 CBRE, Inc. | 5

U.S. VIEWPOINT

Source: “Casting Call: Los Angeles’s Starring Role in the Evolving Production Landscape,” CBRE Research, Q3 2020 1. “Sound stages” or “production space” is defined as a structure dedicated to filming movies, television, music videos, streaming content, and more. Standing sets, back lots, on-site locations, ranches, office complexes, production mills, post-production space, and sound mixing labs were excluded.

PRODUCTION SPACE IN AN EVOLVING CONTENT LANDSCAPE

1.2MSFBritish Columbia

5.5MSFLos Angeles

0.7MSFLouisiana

1.8MSFAtlanta

1.5MSFNew York

0.8MSFOntario

Figure 1. Major North American Markets By Production Space Footprint

Aproductionspace,1alsoknownasasoundstage,generallyisafacilityforfilmingmoviesandtelevisionprograms.SoundstagespaceacrossNorthAmericatotalsmorethan11millionsq.ft.,mostofitinfilminghubslikeLosAngelesandGeorgia.LosAngelesaloneaccountsforhalfofthistotalwith441soundstagesoperatedby64filmandtelevisionstudios.

Theseproductionspaceshavelongbeenoverlookedasinvestmentassetsduetotheirownershipstructure,limitedinventoryandintensiveoperatingmodel.However,institutionalinvestorshavebeenincreasinglyattractedtothesoundstagesectoroverthepastdecade,catalyzingtheirrapidevolutionasanassetclass.

Theadventofstreamingvideohascreatedseeminglyinsatiabledemandforcontentthatpresentsuniqueopportunitiesforrealestateinvestors.Thetopfivestreamingcompaniesinvestedastaggering$25billioninnewproductionsin2019alone,resultinginintensecompetitionforanyavailablefilmingspacease-commerceandlogisticscompaniesoperatorsjostleforthesameindustrialfacilitiesbyfilmandtelevision

OCTOBER 2020 CBRE Research © 2020 CBRE, Inc. | 6

U.S. VIEWPOINT

studios.Occupancyratesforproductionspaceinmostmajormarketshavebeenwellabove90%forseveralyears.

Simultaneously,thelargeamountofcapitalenteringthesoundstagemarkethasalsohelpedtoshiftthecompetitivelandscape.Overthepastdecade,well-heeledinstitutionalinvestorsandoperatorshavemovedsoughttobuildportfoliosandstandardizeoperationsofproductionspace.HudsonPacificPropertiesandHackmanCapitalhavebeenespeciallyactiveinlargeacquisitions.Forexample,HudsonPacificsolda49%stakeinthreeHollywoodstudiosandfiveon-lotoradjacentClassAofficepropertiestoBlackstoneatavaluationof$1.69billion.AndHackmanCapitalrecentlyacquiredNewYork’siconicSilvercupStudios.

Muchasinotheremergentcommercialrealestateassetclassesoverthepastseveraldecades,theinfluxofcapitaltoproductionstudioshasdrivenstandardizationacrossthesector.Asaresult,productionsectorcaprateshavebeguntoconvergewiththoseofothermoreliquidassetclasses.

OCTOBER 2020 CBRE Research © 2020 CBRE, Inc. | 7

U.S. VIEWPOINT

Figure 2: Entertainment Industry Employment Density By State

ENTERTAINMENT EMPLOYMENT GROWTH

TheU.S.istheworldleaderinmediacreation.In2018,morethan3.4millionpeoplewereemployedintheU.S.entertainmentindustry,2representingapproximately2.3%ofthenation’stotalworkforce.Overthepastdecade,theevolutionoftheentertainmentindustry—especiallytheriseofstreamingvideoondemand(SVOD)andconsumerdemandformorecontent—hasledtobroad-basedemploymentgrowth.From2010to2018,U.S.entertainmentsectoremploymentgrewby20%ornearly670,000jobs.

1 “Production space” is defined as a structure dedicated to filming movies, television, music videos, streaming content and more. Standing sets, back lots, on-site locations, ranches, office complexes, production mills, post-production space and sound mixing labs were excluded. 2 The “entertainment industry” includes the following NAICS Association industry codes: 512 — Motion Picture and Sound Recording, 515 — Broadcasting (excluding internet) and 711 — Performing Arts and Spectator Sports. Source: LAEDC, California Employment Development Department (CA EDD), Q3 2020. Source: U.S. Department of Commerce – Bureau of Economic Analysis (BEA), CBRE Research, Q3 2020.

OCTOBER 2020 CBRE Research © 2020 CBRE, Inc. | 8

U.S. VIEWPOINT

AsthehomeofHollywoodandmanyofthemostprominentmediabrands,Californiahasthelargestentertainmentemploymentbasetotalingmorethan628,000(upby97,000between2010and2018).NewYorkisthesecondlargestentertainmentmarket,employingnearly360,000people(upbymorethan48,000between2010and2018).Inrecentyears,otherstateshaveemergedasrichsourcesofentertainmenttalent.Texas,forexample,hadthesecondhighestamountofentertainmentjobsaddedsince2010(53,011)andhasquicklyrisentothethirdlargestmarketforentertainment-relatedprofessions.

Rank StateTotal

Employment

1 California 628,003

2 New York 358,120

3 Texas 216,548

4 Florida 192,666

5 Illinois 112,150

6 Georgia 109,858

7 Pennsylvania 105,005

8 Oregon 99,922

9 Massachusetts 86,460

10 North Carolina 86,358

Rank StateTotal

Employment

1 California 96,817

2 Texas 53,011

3 New York 48,854

4 Florida 47,101

5 Georgia 37,936

6 Oregon 23,628

7 North Carolina 22,200

8 Tennessee 20,772

9 Massachusetts 20,508

10 Pennsylvania 19,765

Figure 3: State Rankings By Total Entertainment Employment & Employment Growth

Source: U.S. Department of Commerce – Bureau of Economic Analysis (BEA), CBRE Research, Q3 2020.

Marketswitharelativelyhighsupplyofindoorfilmingspacehave,inturn,reportedincreasesinentertainmentindustryemployment.

OCTOBER 2020 CBRE Research © 2020 CBRE, Inc. | 9

U.S. VIEWPOINT

Despitetheexplosionoffilminginotherlocales,CaliforniaandNewYorkremaintheundisputedleadersinentertainmentemploymentandthepreferredhomeofbothon-andoff-screentalent.Accordingly,entertainmentproducerswanttobecloseby.

Theuseoftaxincentiveshasjump-startedgrowthoffilminginothermarketslikeGeorgia,whichhasbecomeahubforfeature-lengthfilmsthatrequireentertainmenttalenttotemporarilyrelocate.Asaresult,Georgia’smovieandsoundproductionemploymentbasehasgrownby161%or14,275jobsbetween2010and2018,comparedwithNewYork’s14%gainof9,034jobsoverthesameperiod.

Empl

oym

ent (

Thou

sand

s)

700

600

500

400

300

200

100

0

2010 2011 2012 2013 2014 2015 2016 2017 2018

California New York Georgia Louisana

+27%

+53%

+16%

+18%

Figure 4: Entertainment Employment Growth In Biggest U.S. Filming Hubs

Source: U.S. Department of Commerce – Bureau of Economic Analysis (BEA), CBRE Research, Q3 2020.

OCTOBER 2020 CBRE Research © 2020 CBRE, Inc. | 10

U.S. VIEWPOINT

Overallentertainmenttalent—actors,writers,directorsandproducers—hasgrownacrossallregions.Californiaaddedmorethan92,000performingjobsbetween2010and2018,anincreaseof30%.NewYorkandGeorgiaalsoaddedanimpressiveamountofentertainmenttalentaswell,increasingtheirperformingartslaborpoolsby44,724jobsand23,049respectively.

Figure 5: Entertainment Employment Growth By Major Filming Hubs & Industry Category, 2010–2018

Source: U.S. Department of Commerce – Bureau of Economic Analysis (BEA), CBRE Research, Q3 2020.

Louisiana

Motion Picture & Sound Recording

Broadcasting (except Internet)

Performing Arts, Spectator Sports, and Related Industries

Empl

oym

ent (

Thou

sand

s)100

80

60

40

20

0

(20)

California New York Georgia

92

45

23

914

OCTOBER 2020 CBRE Research © 2020 CBRE, Inc. | 11

U.S. VIEWPOINT

COVID-19 IMPACTS

Televisionandmovieproductionabruptlystoppedbeginninginmid-MarchduetoCOVID-19restrictions,causingasharpdeclineinentertainmentemployment.

Source: U.S. Bureau of Labor Statistics (BLS), CBRE Research, Q3 2020.

Peak to Trough (Jan to May)

Jobs Recovered

Peak to Current (Jan to Aug)

-600 -500 -400 -300 -200 -100 0

42

-259

-241

-247

-229

-24

-19

Motion Picture & Sound Recording

Broadcasting (except Internet)

Performing Arts, Spectator Sports, and Related Industries

Figure 6: Covid-19 Impact On U.S. Entertainment Industry Employment

Thesejoblosseslikelyaretemporarygivenpentupdemand,andmanystalledproductionshavesinceresumed.Inmid-July,NewYorkallowedproductioncrewsnolargerthan50peopletoresumework.PinewoodAtlanta,thelargeststudioinGeorgia,planstoreopenthisfallwithstringentsafetyguidelinesforitsproductioncrews.

OCTOBER 2020 CBRE Research © 2020 CBRE, Inc. | 12

U.S. VIEWPOINT

EXPLOSIVE GROWTH OF VIDEO STREAMING

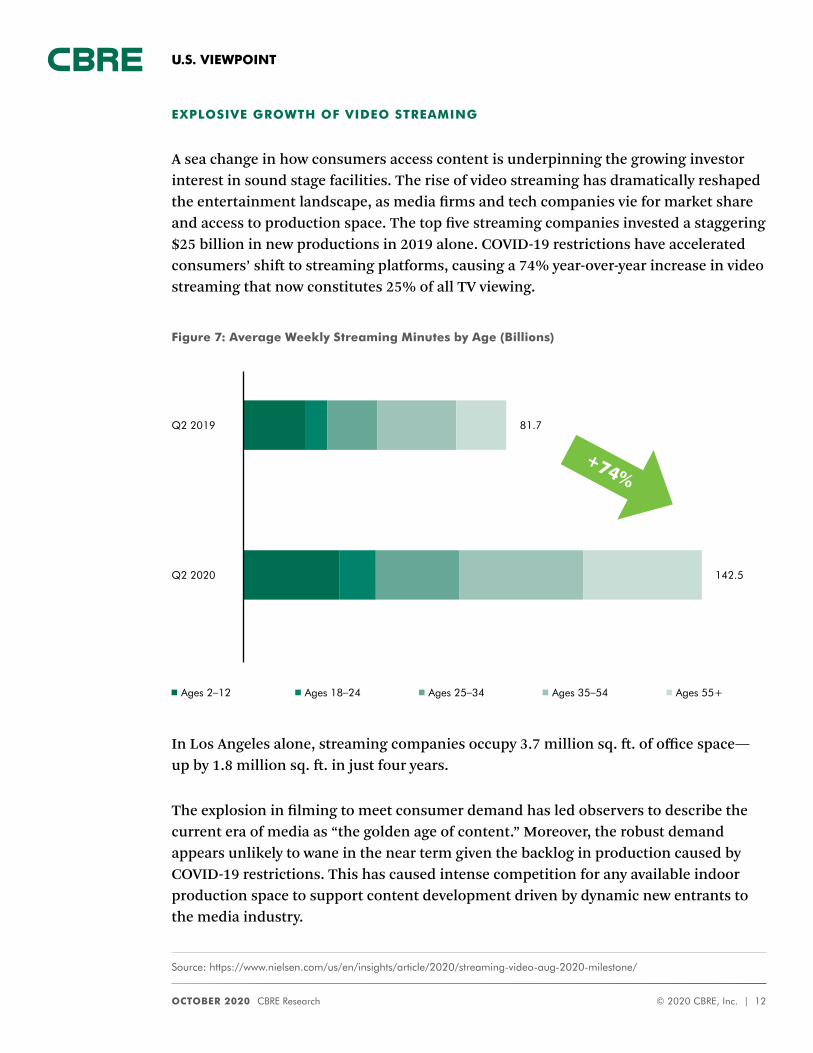

Aseachangeinhowconsumersaccesscontentisunderpinningthegrowinginvestorinterestinsoundstagefacilities.Theriseofvideostreaminghasdramaticallyreshapedtheentertainmentlandscape,asmediafirmsandtechcompaniesvieformarketshareandaccesstoproductionspace.Thetopfivestreamingcompaniesinvestedastaggering$25billioninnewproductionsin2019alone.COVID-19restrictionshaveacceleratedconsumers’shifttostreamingplatforms,causinga74%year-over-yearincreaseinvideostreamingthatnowconstitutes25%ofallTVviewing.

Source: https://www.nielsen.com/us/en/insights/article/2020/streaming-video-aug-2020-milestone/

Figure 7: Average Weekly Streaming Minutes by Age (Billions)

Q2 2019 81.7

Q2 2020 142.5

Ages 2–12 Ages 18–24 Ages 25–34 Ages 35–54 Ages 55+

InLosAngelesalone,streamingcompaniesoccupy3.7millionsq.ft.ofofficespace—upby1.8millionsq.ft.injustfouryears.

Theexplosioninfilmingtomeetconsumerdemandhasledobserverstodescribethecurrenteraofmediaas“thegoldenageofcontent.”Moreover,therobustdemandappearsunlikelytowaneintheneartermgiventhebackloginproductioncausedbyCOVID-19restrictions.Thishascausedintensecompetitionforanyavailableindoorproductionspacetosupportcontentdevelopmentdrivenbydynamicnewentrantstothemediaindustry.

+74%

OCTOBER 2020 CBRE Research © 2020 CBRE, Inc. | 13

U.S. VIEWPOINT

INCENTIVES & THE GLOBAL PRODUCTION ECOSYSTEM

Majorfilmproductionsincreasinglyaretakingplaceinfar-flunglocations,buttraditionalmarketslikeLosAngelesandNewYorkCityremainthecentralhubsformediaandentertainment.EmergingfilmlocaleslikeGeorgiaandLouisianahaveheavilyleveragedtaxincentiveprogramstocatalyzetheirnascentmediaandentertainmentsectors.

Source: CBRE Research, Q3 2020.

Figure 8: Summary Of Tax Incentives By Major Filming Market

Thelion’sshareoffilmbudgetsisforpost-productionand“above-the-line”costs(on-andoff-cameracreativetalent)thatproductionstudiosfrequentlyfinddifficultorimpossibletorenegotiate.“Below-the-line”costsofhourlylaborandfilmingareeasiertoreduce.Andthemosteffectivewaytodothisisbymovingtheproductionoutofhigh-costmarketstothosewithlowerlaborrates,cheaperrentsandfavorabletaxpolicies.Despitetheeconomicadvantagestolow-costmarkets,talentismoreapttofilmout-of-stateforafeaturefilmasopposedtoatelevisionshoot,asmoviefilmingtypicallylastsbetween1–2months.

California Georgia New YorkBritish Columbia

Ontario Louisiana

Theatrical Features

62 36 57 16 4 6

Streaming Features

11 3 13 3 2 2

Total Features 73 39 70 19 6 8

Sound Stage SF

5.5 MSF 1.8 MSF 1.5 MSF 1.2 MSF 0.8 MSF 0.7 MSF

Tax Credit Amount (For Features)

20% (non-indie); 25% indie

20% 30% 28% 21.5% 25%

Credit Type

Non-transferable (non-indie); Transferable (indie)

Transferable Refundable Refundable Refundable Refundable

Sunset Date 2025 None 2022 None None None

Annual Cap (US$)

$330 Million

None$420 Million

None None$150 Million

Tax

Cre

dit C

hara

cter

istic

sFe

atu

re F

ilms

OCTOBER 2020 CBRE Research © 2020 CBRE, Inc. | 14

U.S. VIEWPOINT

Inyearsahead,theNorthAmericanfilmindustryshouldbecomemoreinterconnectedascontentproduction,post-productionandmanagementbecomemoreglobalized.Amidthisevolution,thekeyentertainmenthubsareaddingmoreprofessionalservicesinsupportoftheglobalentertainmentecosystem.Forexample,LosAngeles’sexplosiveemploymentgrowthofpromoters,agentsandmanagers(up140%since2010)hasoutpacedits35%increaseinperformersoverthesametime,reflectingthecity’scentralroleinprovidingtotalfilmproductioninfrastructure.

ADAPTIVE RE-USE ACCELERATES

Thesurgeincontentproductionandproliferationofstreamingplatformshasdrivenintensedemandforregionalproductionspace.Withsoundstagevacancyratesconsistentlyinthelowsingle-digitsandsteadilyclimbingrentalratesinthemostin-demandlocations,productioncompanieshaveincreasinglysoughtalternativefilminglocations.

Atitsmostbasic,thephysicalrequirementsforeffectivesoundstagespace(e.g.,highceilingsandlargeunobstructedfloorplates)closelyresemblethoseoftheaverageindustrialbuilding.Certainbuildingcharacteristicsareuniquetosoundstages,particularlysoundproofingandsuspendedweightloads.Forlessdemandingproductions,traditionalindustrialspaceoftenwillsuffice.Asaresult,manyindustrialpropertiesareofinteresttoproductioncompaniesandinvestors.

InpredominantlyinfillmarketslikeLosAngelesandNewYork,conversionsofindustrialpropertiestoproductionfacilitiesareincreasinglycommon.

Amid this evolution, the key entertainment hubs are adding more professional services in support of the global entertainment ecosystem.

OCTOBER 2020 CBRE Research © 2020 CBRE, Inc. | 15

U.S. VIEWPOINT

7Stages

5,419 SF Average Stage Size

37,930 SF Total Production Space

CASE STUDY: SIREN STUDIOS, HOLLYWOOD

SirenStudios,locatedintheheartofHollywood,exemplifiestheadaptivereuseofnon-studiospace.Itssevenstagesincludebothformerindustrialspaceandnewpurpose-builtconstruction.Withover$50millioninvestedinupgradingthespaces,thestudioispopularforsmallershootsthatarebestsuitedfortheitssmallfloorplates,includingfashionphotographyandadvertisements.

OCTOBER 2020 CBRE Research © 2020 CBRE, Inc. | 16

U.S. VIEWPOINT

GEORGIA

•GeorgiaisthesecondlargestfilmingmarketintheU.S.bytotalsoundstagesquarefeet.

•Entertainmentemploymentgrewbynearly38,000jobsfrom2010to2018—anincreaseof53%—asproductioncompaniesincreasinglyusedthestateasasiteforfeaturefilms.

•Mid-tolarge-sizedstagespaceisfarmorecommoninGeorgiathanin

California,dueinlargeparttotherelativeyouthofthefilmingmarket.

•High-ceilingstagesaboundinGeorgia,meaningthemarketcaneasilyaccommodatelarge-scaleandintricatesets.

•UnlikeCalifornia,Georgia’staxincentiveprogramisunhamperedbyannualcapsorexpirationdates,makingtheprocessofsecuringtaxcreditslesschallenging.

STUDIO SPOTLIGHT: PINEWOOD ATLANTA

Locatedjust30minutesfromdowntownAtlanta,PinewoodAtlantaStudioshasquicklybecomeoneofGeorgia’smostsought-afterfilminglocations.Sittingonmorethan700acres,thestudioencompasses18soundstagestotalingover360,000sq.ft.offilmableindoorspace—thelargestsoundstagefootprintinthestate.Sinceopeningin2014,thestudiohashostedsomeofthebiggestboxofficedrawsinthepastdecade,includingMarvel’s“Ant-ManandtheWasp”and“Avengers:Endgame.”

SOUND STAGE BREAK DOWN BY SIZE SEGMENT

65stages with

<5K SF

0 10 20 30 40 50 60 70

<5,000

5,000–9,999

10,000–14,999

15,000–19,999

20,000–29,999

30,000–39,999

>40,000

65

62

21

29

6

1

SOUND STAGE BREAKDOWN BY HEIGHT SEGMENT

<10 Ft.

10–19 Ft.

20–29 Ft.

30–39 Ft.

40–49 Ft.

>50 Ft.

Unknown

0 10 20 30 40 50 60 70 80 90

83stages with

ceiling height 10–19 FT

83

4

46

42

4

5

QUICK FACTS:

OCTOBER 2020 CBRE Research © 2020 CBRE, Inc. | 17

U.S. VIEWPOINT

NEW YORK

•Despitebeingthethirdlargestfilmmarketbysoundstagesquarefeet,NewYork’sfilmindustryistheoldestinthenation,beginningin1896.

•NewYork’entertainmentsectoremploymentgrewby49,000jobsfrom2010to2018—anincreaseof16%.

•Duetothedensityofthemarket,smalltomid-sizedstagesaremorecommonthanlargerones.

•Low-ceilingsproductionfacilitiesarecommon,makingthembest-suitedsmallerscaleproductionsliketelevisionseries.

•LikeCalifornia,NewYork’sfilmtaxincentiveprogramhasanannualcap.Totalstatewideincentivescurrentlymaxoutat$420million(comparedwithCalifornia’s$330million).

STUDIO SPOTLIGHT: BROADWAY STAGES

Startingin1983asasinglesoundstageconvertedfromanoldmovietheaterinAstoria,Queens,BroadwayStageshasbecomethelargestfilmstudioinNewYorkCity.WithlocationsspreadacrossQueens,StatenIslandandBrooklyn,thestudiooperatesnearly40stagestotalingmorethan400,000sq.ft.ofindoorsoundstagespace.Recentnotableproductionsincludetelevision’s“SaturdayNightLive,”“Marvel’sDaredevil,”“Mr.Robot”and“TheMarvelousMrs.Maisel.”

SOUND STAGE BREAK DOWN BY SIZE SEGMENT

65stages with

<5K SF

0 10 20 30 40 50 60 70

<5,000

5,000–9,999

10,000–14,999

15,000–19,999

20,000–29,999

30,000–39,999

>40,000

65

62

21

29

6

1

SOUND STAGE BREAKDOWN BY HEIGHT SEGMENT

<10 Ft.

10–19 Ft.

20–29 Ft.

30–39 Ft.

40–49 Ft.

>50 Ft.

Unknown

0 10 20 30 40 50 60 70 80 90

83stages with

ceiling height 10–19 FT

83

4

46

42

4

5

QUICK FACTS:

OCTOBER 2020 CBRE Research © 2020 CBRE, Inc. | 18

U.S. VIEWPOINT

BRITISH COLUMBIA QUICK FACTS:

•ThefourthlargestfilmingmarketinNorthAmerica,BritishColumbiawasoneofthefirstplacestoadopttaxincentivesformovieandtelevisionproductions.

•Mid-tolarge-sizedstagesaremostcommon.

•High-ceilingstagesareplentifulandcanaccommodatelarge-scaleproductions.

STUDIO SPOTLIGHT: MAMMOTH STUDIOS

LocatedinBurnaby,MammothStudioslivesuptoitsnameasthelargestfilmstudioinBritishColumbiawithmorethan250,000sq.ft.ofindoorfilmingspace.MammothStudiosisalsohometothelargestsoundstageinNorthAmericaat123,883sq.ft.and40feettall.Severalbigbudgetfilmshavebeenmadehere,including“SonictheHedgehog,”“ThePredator,”“TheRevenant”and“Deadpool2.”

SOUND STAGE BREAK DOWN BY SIZE SEGMENT

23stages with 15K–19K SF

0 5 10 15 20 25

<5,000

5,000–9,999

10,000–14,999

15,000–19,999

20,000–29,999

30,000–39,999

>40,000

16

1623

13

32

SOUND STAGE BREAKDOWN BY HEIGHT SEGMENT

<10 Ft.

10–19 Ft.

20–29 Ft.

30–39 Ft.

40–49 Ft.

>50 Ft.

Unknown

0 5 10 15 20 25 30 35

32stages with

ceiling height 40–49FT

1

13

15

32

3

OCTOBER 2020 CBRE Research © 2020 CBRE, Inc. | 19

U.S. VIEWPOINT

ONTARIO QUICK FACTS:

•Ontariohasanumberofvaryingstagesizes,thoughsmalltomid-sizedstagesaremostcommon.

•Standardheightstagesarethenorm.

STUDIO SPOTLIGHT: PINEWOOD STUDIOS TORONTO

Onlyafewminutes’drivefromtheStudioDistrict,PinewoodStudios’Torontolocationistheprimarypurpose-builtfacilityinthecity.Thestudiohas12soundstages,includinganearly46,000-sq.-ft.megastage,foratotalofmorethan208,000sq.ft.ofindoorfilmingspace.PinewoodTorontohashostedanumberofgenremovieandtelevisionproductionsovertheyears,including“IT:ChapterTwo,”“SHAZAM!,”“StarTrek:Discovery”and“TheExpanse.”

SOUND STAGE BREAK DOWN BY SIZE SEGMENT

15stages with 10K–14K SF

0 2 4 6 8 10 12 14 16

<5,000

5,000–9,999

10,000–14,999

15,000–19,999

20,000–29,999

30,000–39,999

>40,000

10

615

10

8

22

SOUND STAGE BREAKDOWN BY HEIGHT SEGMENT

<10 Ft.

10–19 Ft.

20–29 Ft.

30–39 Ft.

40–49 Ft.

>50 Ft.

Unknown

0 2 4 6 8 10 12 14 16 18

16stages with

ceiling height 20–29 FT

7

16

15

7

4

3

1

OCTOBER 2020 CBRE Research © 2020 CBRE, Inc. | 20

U.S. VIEWPOINT

LOUISIANA QUICK FACTS:

•Whilesmallcomparedtootherfilmingmarkets,Louisianahasbecomeatop-tierfilminglocationamongmajorstudios.

•Louisiana’sentertainmentsectoremploymentgrewbynearly8,000jobsfrom2010to2018—anincreaseof27%.

•Themarkethasarangeofstagesizesthatcanaccommodateawidearrayofproductionneeds.

•Mid-tohigh-ceilingspaceiscommon.

•Thestateoffersafilmtaxincentiveprogramcappedat$150millionperyear.

SOUND STAGE BREAK DOWN BY SIZE SEGMENT

11stages with 20K–29K SF

0 2 4 6 8 10 12

<5,000

5,000–9,999

10,000–14,999

15,000–19,999

20,000–29,999

30,000–39,999

>40,000

38

75

116

SOUND STAGE BREAKDOWN BY HEIGHT SEGMENT

<10 Ft.

10–19 Ft.

20–29 Ft.

30–39 Ft.

40–49 Ft.

>50 Ft.

Unknown

0 5 10 15 20 25 30 35

53stages with

ceiling height 40–49FT

4

4

21

7

5

STUDIO SPOTLIGHT: CELTIC STUDIOS

CelticStudios(alsoknownastheCelticMediaCentre)isthelargestfilmproductionstudioinLouisiana.Establishedin2008,itincludessevensoundstagestotalingnearly150,000sq.ft.ofindoorfilmingspace.Thestudiobillsitselfasaone-stopshopforfilming,offeringalmost100,000sq.ft.ofofficespaceforproductionneeds.RecentproductionsfilmedatCelticStudiosinclude“FantasticFour,”“Oblivion”and“Greyhound.”

© Copyright 2020 All rights reserved. Information contained herein, including projections, has been obtained from sources believed to be reliable, but has not been verified for accuracy or completeness. CBRE, Inc. makes no guarantee, warranty or representation about it. Any reliance on such information is solely at your own risk. This information is exclusively for use by CBRE clients and professionals and may not be reproduced without the prior written permission of CBRE’s Global Chief Economist.

To learn more about CBRE Research, or to access additional research reports, please visit Research and Reports.

U.S. VIEWPOINT

Richard Barkham, PhD, MRICSGlobal Chief Economist & Head of Americas Research CBRE+ 617 912 [email protected]

Spencer G. LevyChairman & Senior Economic Advisor CBRE | Americas Research+ 617 912 [email protected]

Julie WhelanHead of Occupier ResearchCBRE | Americas Research+1 617 912 [email protected]

Eric WillettResearch Director, PSW Thought Leadership +1 213 613 [email protected]

Dan HunkerResearch Analyst, PSW Thought Leadership +1 909 418 [email protected]

Whitley CollinsGlobal President, Advisory & Transaction Services | Occupier+1 310 363 [email protected]

Lew HornePresident, PSW +1 213 613 [email protected]

FOR MORE INFORMATION ABOUT CBRE RESEARCH, PLEASE CONTACT:

FOR MORE INFORMATION ABOUT THIS REPORT, PLEASE CONTACT:

FOR MORE INFORMATION ABOUT OCCUPIER SERVICES AND THE PRODUCTION LANDSCAPE, PLEASE CONTACT: