68

© CPFL Energia 2009. Todos os direitos reservados. Overview and Outlook Wilson Ferreira Jr CEO of CPFL Energia

| Date post: | 14-Apr-2017 |

| Category: |

Investor Relations |

| Upload: | cpfl-ri |

| View: | 248 times |

| Download: | 0 times |

© CPFL Energia 2009. Todos os direitos reservados.

Overview and Outlook Wilson Ferreira Jr CEO of CPFL Energia

Benefits of the IPO

Injection of funds

Access to capital

markets

Efficiency

Innovation and process improvement

Improved governance

“Novo Mercado”

+

Implementation

of controls (SOX)

Creation of Value

Company Growth

Comparability

Benchmarking process

How has the IPO contributed to CPFL Energia?

2

IPO - Sep/2004 Sep/2014 Var. CAGR (% p.a.)

Companies (CNPJs) 11 125 + 114 +27.5%

Power sold in concession area (GWh/year)1,2

36,679 59,640 + 62.6% +5.0%

Installed capacity 812 MW 3,127 MW3 + 285.1% +14.4%

Number of free clients

42 289 +247 +21.3%

Market cap (R$ billion)4 8.3 18.1 + 118.1% +8.1%

EBITDA (R$ million)2,5 2,648 3,956 + 49.4% +4.1%

CPFL Energia – Overview

1) In the concession area; 2) Sales and EBITDA refer to the 12 months ended September; 3) Including Desa assets; 4) IPO quote: R$ 17.22/common share and Dec 2, 2014: R$ 18.79/common share; 5) Amounts in constant currency of Sep/14.

3

Privatization

1998 2002 2004 2000 1997 2001 2003

IPO

2004 2006 2005 2007

IPO

2008 2010 2009 2011 2012 2013 2014

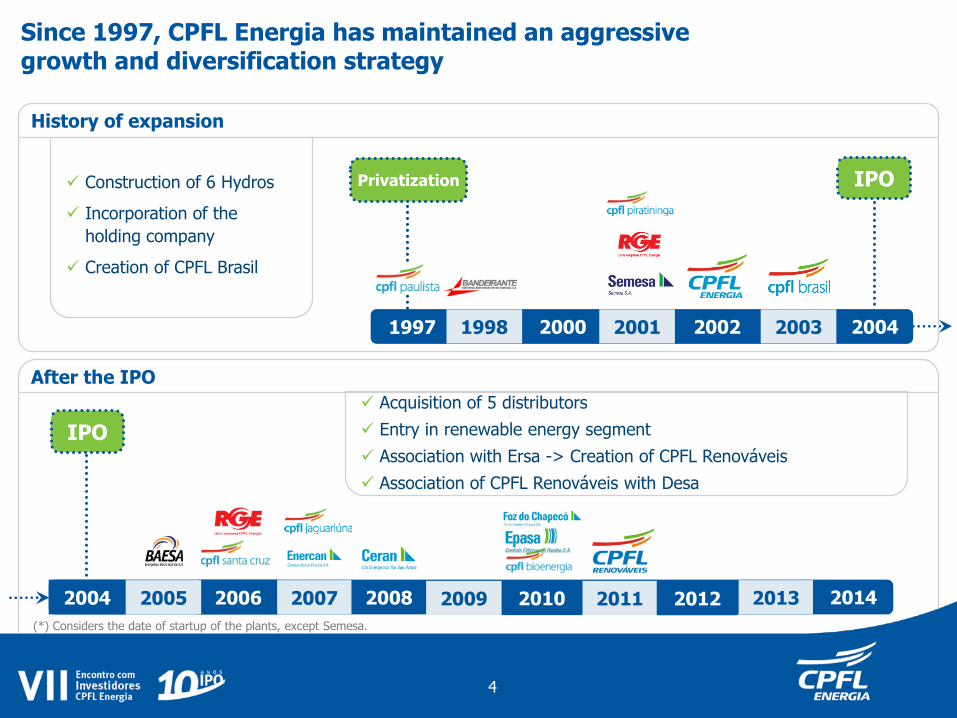

Since 1997, CPFL Energia has maintained an aggressive growth and diversification strategy

History of expansion

After the IPO

Construction of 6 Hydros

Incorporation of the

holding company

Creation of CPFL Brasil

Acquisition of 5 distributors

Entry in renewable energy segment

Association with Ersa -> Creation of CPFL Renováveis

Association of CPFL Renováveis with Desa

4

(*) Considers the date of startup of the plants, except Semesa.

CPFL Energia in the last 10 years

Sustainability Differentiated Corporate

Governance

Financial Discipline and Value Creation Synergic Growth and

Operating Efficiency

Generation and Commercialization

Segments

Distribution

Services and Telecom

CPFL Energia in the last 10 years

Sustainability Differentiated Corporate

Governance

Financial Discipline and Value Creation Synergic Growth and

Operating Efficiency

Generation and Commercialization

Segments

Distribution

Services and Telecom

Generation & Commercialization

2005 2003 2007 2008 2010 2004

IPO

Commercial Expertise

Clear growth strategy in the Generation and Commercialization segment

IPO proceeds: drive the expansion

of the Generation Segment

Expansion of free market

Building customer loyalty

Acquisition of customers outside the distributors’ area

8

2005 2003 2007 2008 2010 2004

IPO

Commercial Expertise

Clear growth strategy in the Generation and Commercialization segment

IPO proceeds: drive the expansion

of the Generation Segment

Expansion of free market

Building customer loyalty

Acquisition of customers outside the distributors' area

9

Increased project risk

Auctions of structuring projects: Project return < CPFL return

2005 2003 2007 2008 2010 2004

IPO

Commercial Expertise

Clear growth strategy in the Generation and Commercialization segment

IPO proceeds: drive the expansion

of the Generation Segment

New focus: renewable energy

Investment in alternative sources: biomass and wind

Acquisition of existing assets

Creation of CPFL Renováveis

Energy auctions and free market

Long-term PPAs protected/indexed to inflation (term of 20-30 years)

Between 2010 and 2011

Expansion of free market

Building customer loyalty

Acquisition of customers outside the distributors' area

10

Increased project risk

Auctions of structuring projects: Project return < CPFL return

Increased project risk

2005 2003 2007 2008 2010 2013

IPO

2011 2004

IPO

Commercial Expertise

Clear growth strategy in the Generation and Commercialization segment

IPO proceeds: drive the expansion

of the Generation Segment

Renewable Energy:

new growth driver

New focus: renewable energy

Investment in alternative sources: biomass and wind

Acquisition of existing assets

Creation of CPFL Renováveis

Energy auctions and free market

Long-term PPAs protected/indexed to inflation (term of 20-30 years)

Expansion of free market

Building customer loyalty

Acquisition of customers outside the distributors' area

Guarantee of energy from renewable sources

Focus on special consumers

New sources: Solar etc.

Synergy with CPFL Brasil

Auctions of structuring projects: Project return < CPFL return

Between 2010 and 2011

11

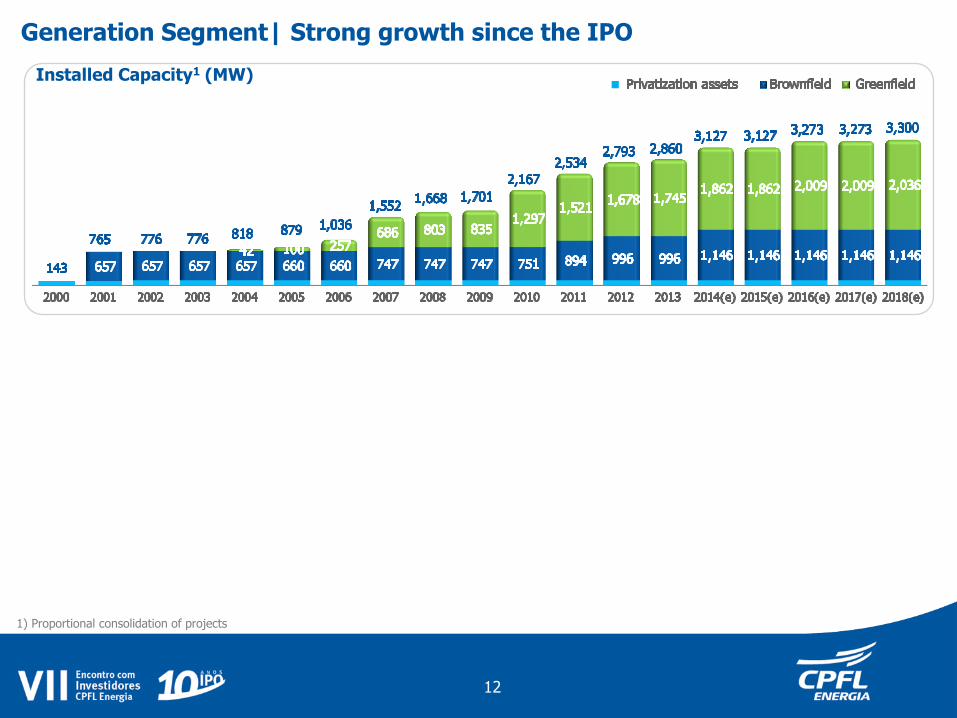

Generation Segment| Strong growth since the IPO

1) Proportional consolidation of projects

12

Installed Capacity1 (MW)

Conventional Sources | 18 plants in operation 8 Hydros and 2 TPPs

Installed Capacity1 (MW)

13

1) Proportional consolidation of projects

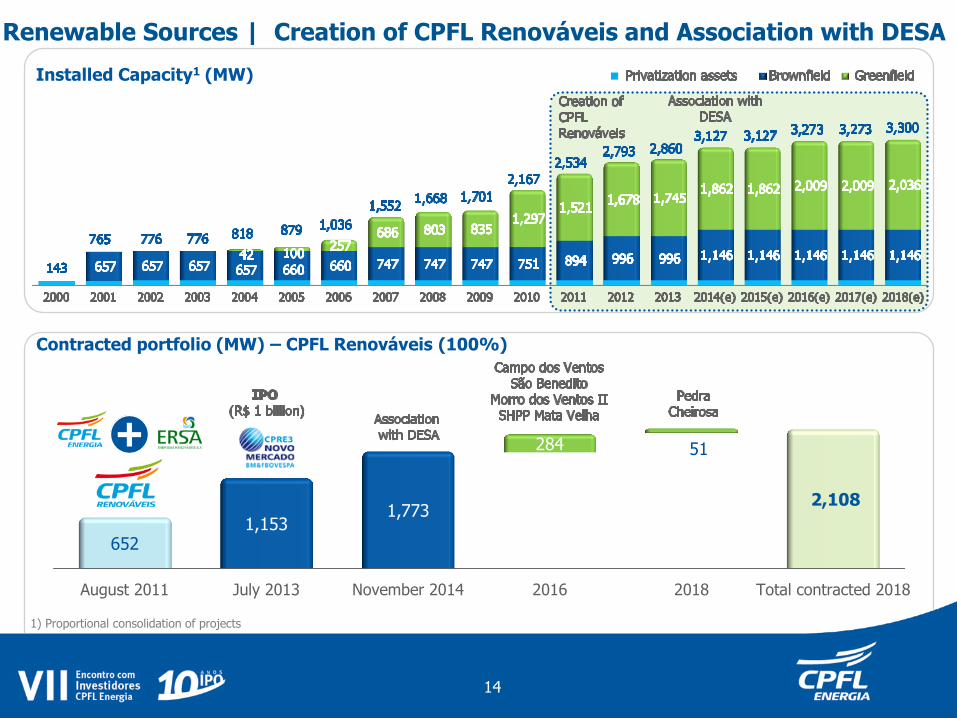

August 2011 July 2013 November 2014 2016 2018 Total contracted 2018

652

1,153 1,773

284 51

2,108

Contracted portfolio (MW) – CPFL Renováveis (100%)

+

Renewable Sources | Creation of CPFL Renováveis and Association with DESA

14

1) Proportional consolidation of projects

Installed Capacity1 (MW)

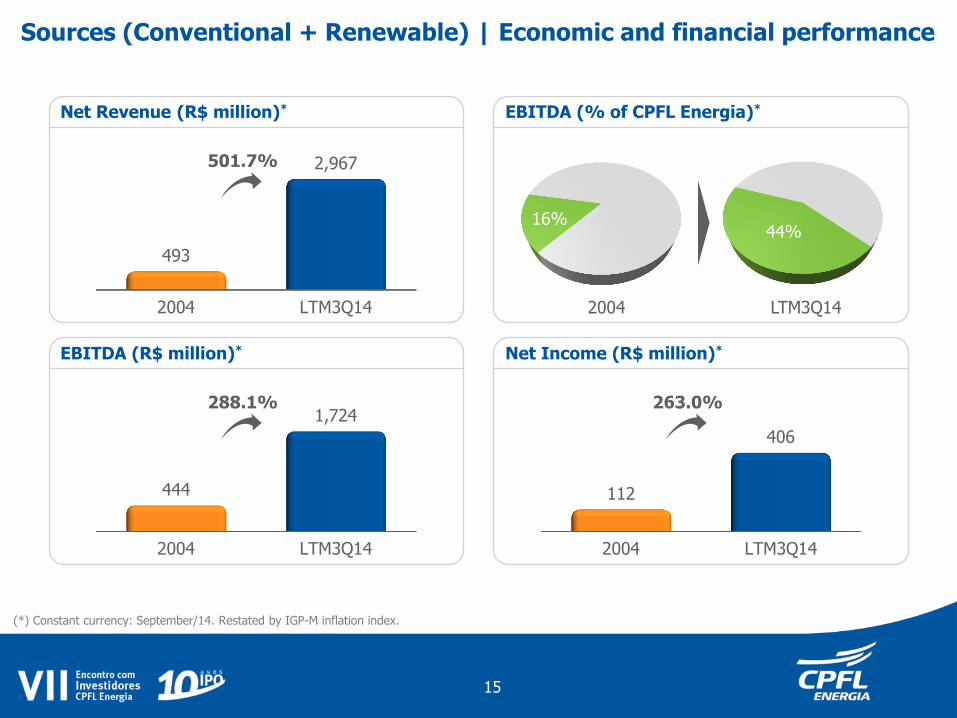

Net Revenue (R$ million)* EBITDA (% of CPFL Energia)*

EBITDA (R$ million)* Net Income (R$ million)*

Sources (Conventional + Renewable) | Economic and financial performance

2004 LTM3Q14

493

2,967 501.7%

2004 LTM3Q14

444

1,724 288.1%

2004 LTM3Q14

112

406

263.0%

2004 LTM3Q14

16% 44%

(*) Constant currency: September/14. Restated by IGP-M inflation index.

15

Despite the decline in the volume of energy sold, the Commercialization segment maintained its revenue and

margin levels

Margem Bruta

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

369

443

527

399 428

395

290 267

53

208

Gross income

Commercialization | Consistent results since the IPO

Evolution of revenue and energy sold Gross income

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

2,2

19 2

,781

2,6

46

2,6

26

2,5

87

2,2

87

2,0

30

2,2

72

2,1

15

2,1

99

1,9

01 2,3

51

2,1

02

1,8

70

1,8

83

1,8

22

1,5

93

1,7

12

1,5

54

1,3

44

Gross revenue [R$ Mn] Energy sold [Average MW]

Constant currency: September/14. Restated by IGP-M inflation index.

16

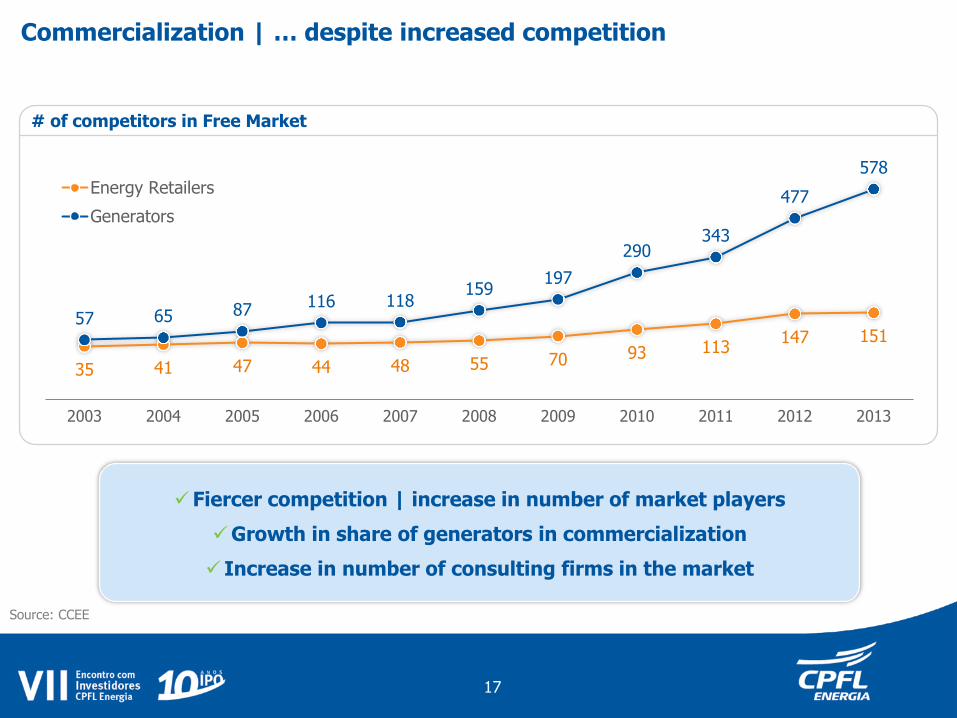

Commercialization | … despite increased competition

35 41 47 44 48 55 70 93 113 147 151

57 65 87 116 118

159 197

290 343

477

578

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Energy Retailers

Generators

# of competitors in Free Market

Source: CCEE

Fiercer competition | increase in number of market players

Growth in share of generators in commercialization

Increase in number of consulting firms in the market

17

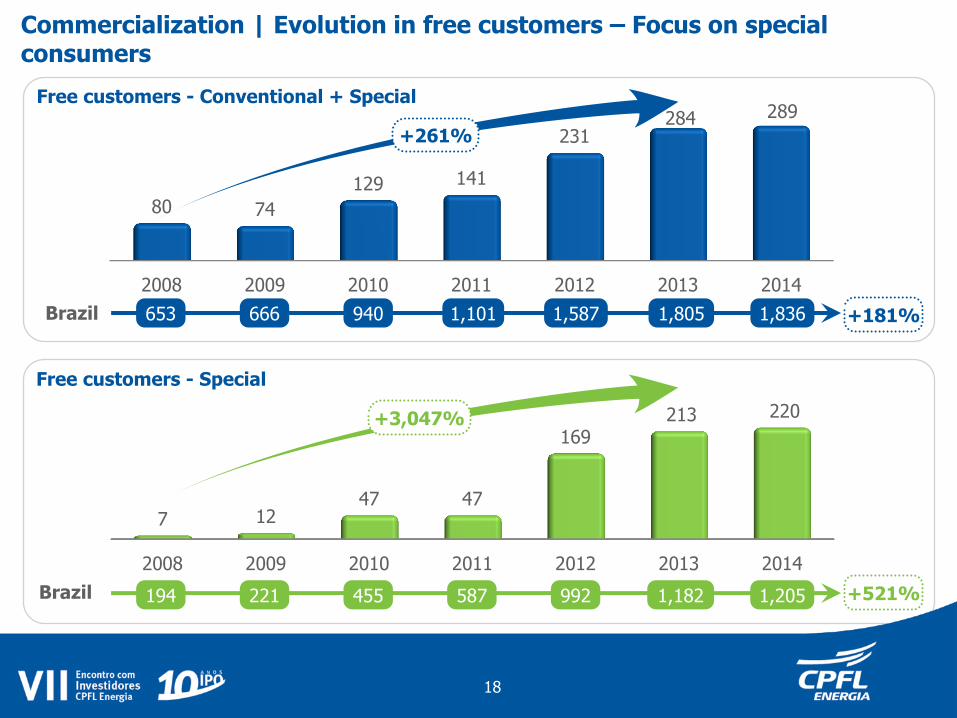

Commercialization | Evolution in free customers – Focus on special consumers

2008 2009 2010 2011 2012 2013 2014

7 12 47 47

169 213 220

+181%

+521%

1,836 1,805 1,587 1,101 940 666 653

1,205 1,182 992 587 455 221 194

+261%

+3,047%

Brazil

Brazil

Free customers - Conventional + Special

Free customers - Special

2008 2009 2010 2011 2012 2013 2014

80 74

129 141

231 284 289

18

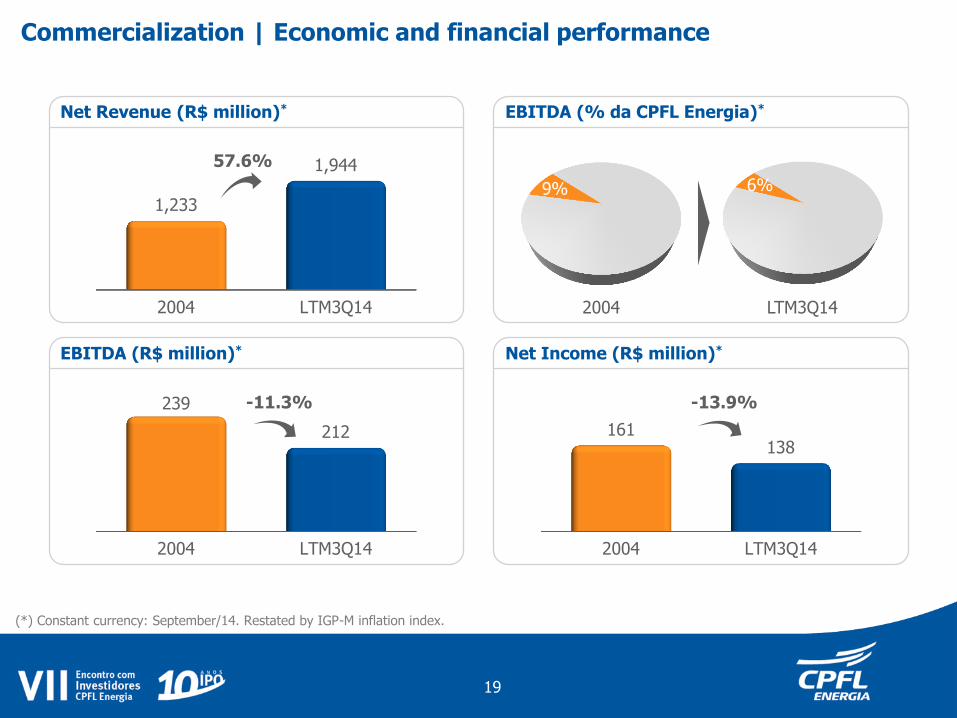

Net Revenue (R$ million)* EBITDA (% da CPFL Energia)*

EBITDA (R$ million)* Net Income (R$ million)*

Commercialization | Economic and financial performance

2004 LTM3Q14

1,233

1,944 57.6%

2004 LTM3Q14

239

212

-11.3%

2004 LTM3Q14

161 138

-13.9%

2004 LTM3Q14

9% 6%

(*) Constant currency: September/14. Restated by IGP-M inflation index.

19

CPFL Energia in the last 10 years

Sustainability

Differentiated Corporate Governance

Financial Discipline and Value Creation Synergic Growth and

Operating Efficiency

Generation and Commercialization

Segments

Distribution

Services and Telecom

Distribution segment continues to be CPFL Energia’s flagship operation

1) Acquisition of 67.3%; 2) Acquisition of the remaining 32.7%.

Integration CPFL Piratininga

1

Acquisition CPFL Santa Cruz

Acquisition RGE

2

IPO Acquisition

CPFL Jaguariúna

2008 2006 2004 2002 2001 1997

Growth of client base and electricity assets

Significant market expansion

Operating efficiency

Synergy and economies of scale

Investments in expansion and modernization of grid (smart grid)

Growth of CPFL’s Distribution business

21

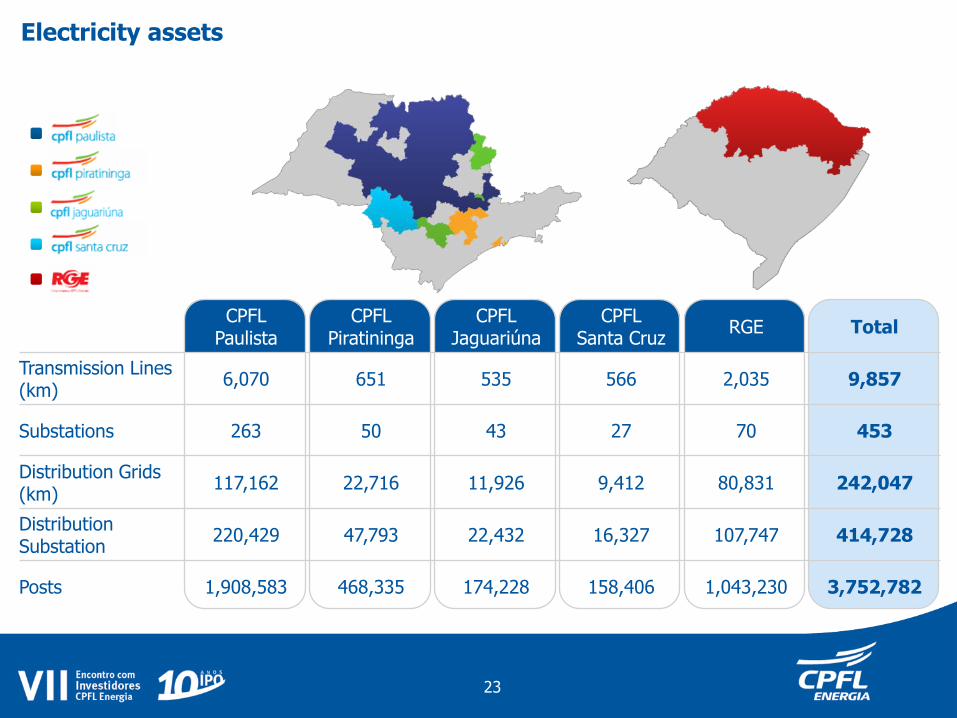

Distribution Municipalities served 561

Concession areas (‘000 km2) 177

Inhabitants (millions) 18.0

Market Share (%) 13%

Customers (‘000) 7,551

Employees 6,061

Market (GWh)* 59,640

Base Sep/14. (*) 12 months ended Sep/14

Electricity assets

CPFL Paulista

CPFL Piratininga

CPFL Jaguariúna

CPFL Santa Cruz

RGE Total

Transmission Lines (km)

6,070 651 535 566 2,035 9,857

Substations 263 50 43 27 70 453

Distribution Grids (km)

117,162 22,716 11,926 9,412 80,831 242,047

Distribution Substation

220,429 47,793 22,432 16,327 107,747 414,728

Posts 1,908,583 468,335 174,228 158,406 1,043,230 3,752,782

23

157.4

171.8 178.2

1989 202.6 205.4

214.5 210.5

235.5 239.8 242.0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Sep/14

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 12M

3Q14

Cativo

TUSD

# of customers (millions)

Grid extension ('000 Km)

Sales in the Concession Area (GWh)1

5.5 5.6 5.7

6.3 6.4 6.6 6.7 7.0

7.2 7.4 7.6

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Sep/14

CAGR 5.1%

177 185 196

223 234 243 247

270 327

380 415

9,299 10,358 10,459

12,356 12,423 12,502 12,659 13,650 13,650

14,535 15,744

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Sep/14

Transformers

Substations

Substations (MVA) and Transformers (‘000)

Growth has been significant in recent years…

CAGR 4.4%

CAGR 3.2%

CAGR 5.4%

CAGR 8.9%

24

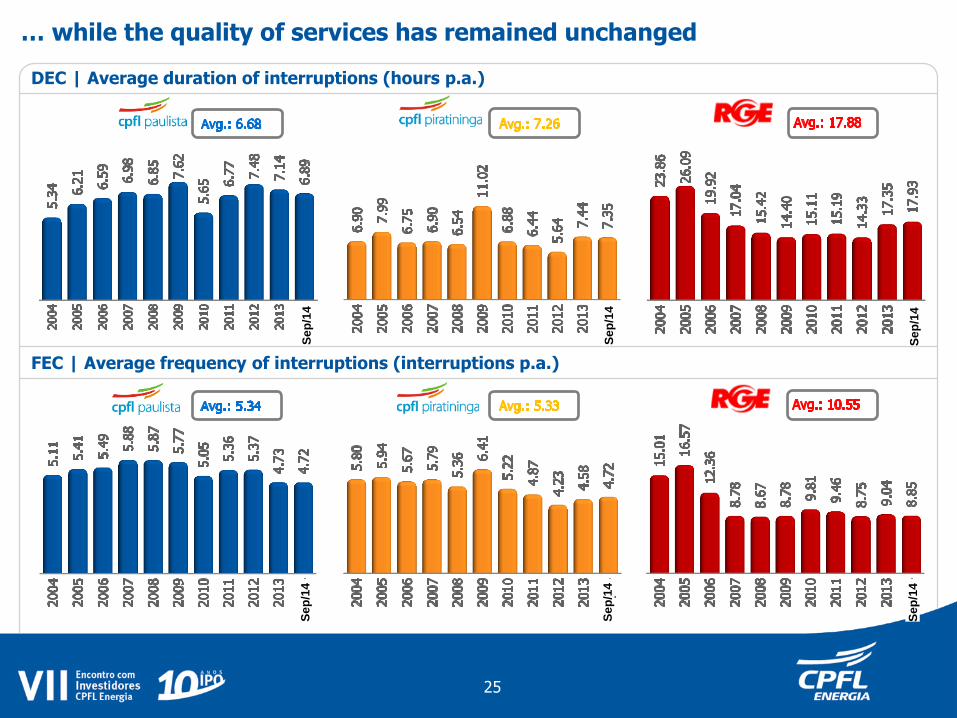

… while the quality of services has remained unchanged

DEC | Average duration of interruptions (hours p.a.)

FEC | Average frequency of interruptions (interruptions p.a.)

25

Se

p/1

4

Se

p/1

4

Se

p/1

4

Se

p/1

4

Se

p/1

4

Se

p/1

4

CPFL is an industry benchmark for productivity

1) PMSO published in the financial statements, at 2013 prices. Excludes non-recurring effects of 2005, 2011, 2012 and 2013. 2) CSN, indicator which weights km of grid (12%), customers (28%) and market (60%), used by OFGEM and proxy of the new ANEEL methodology

36.5

43.8

49.2

58.6

Disco 1 Disco 2 Disco 4 Disco 3

Peers (data as of 2013)

PMSO1 by CSV2 – productivity gain of 5% p.a. since the acquisition of RGE in 2006

49.3

44.3 41.5 40.9

45.2

38.3 37.0 37.1 36.8

35.2

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

CPFL Energia (8 distributors)

40.8

32.9

5% p.a.

Implementation of the operating model of CPFL Energia

Acquisition and integration of RGE, Santa Cruz and Jaguariúna

Increasingly more automated and efficient operation

Economies of scale

Synergies

Productivity increase

26

Acquisition of RGE

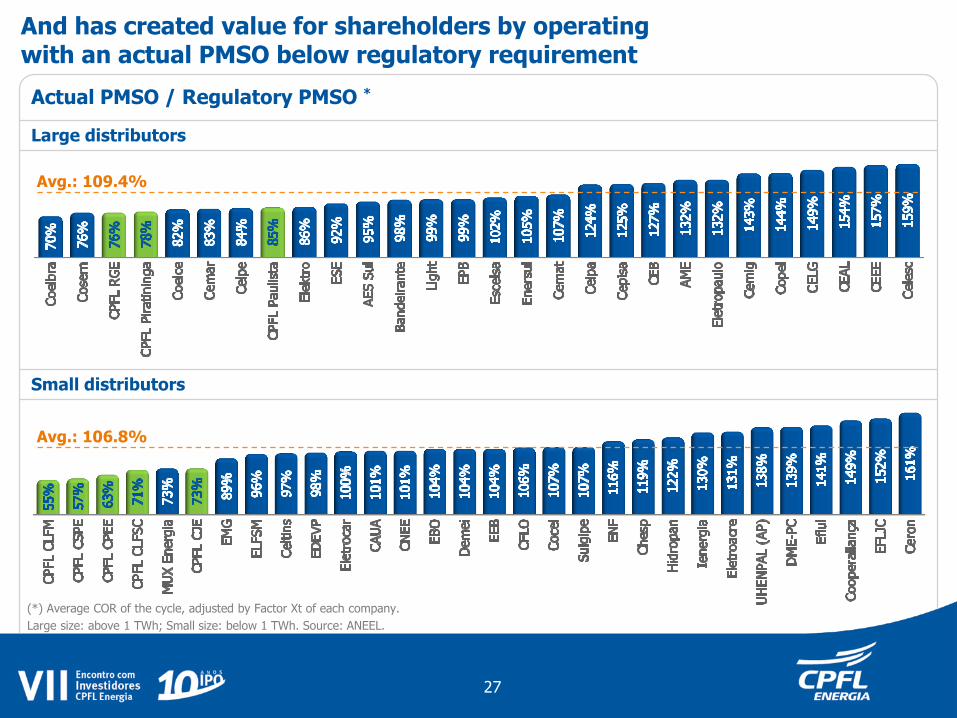

And has created value for shareholders by operating with an actual PMSO below regulatory requirement

Small distributors

Large distributors

Actual PMSO / Regulatory PMSO *

(*) Average COR of the cycle, adjusted by Factor Xt of each company.

Large size: above 1 TWh; Small size: below 1 TWh. Source: ANEEL.

Avg.: 109.4%

Avg.: 106.8%

27

Peers

Indicator AES

Eletropaulo Elektro AES Sul CEMIG COELBA Avg.

DEC 7.1 7.4 17.4 8.0 8.5 14.1 12.5 22.5 18.31

FEC 4.7 4.6 9.0 4.4 5.0 7.4 6.3 8.9 10.51

Overall Losses (%) 7.9 5.8 9.6 9.9 9.5 11.0 11.2 14.0 14.01

Revenue Quality 0.88 1.10 0.75 1.5 2.7 0.9 7.2 8.3 8.51

Delinquency (%) over 90 days overdue

0.20 0.56 0.91 0.53 0.59 1.69 5.58 4.91 3.911

CPFL is also a benchmark in quality and commercial indicators

Source: Abradee Award 2014 and ANEEL. 1) Brazil Average (63 companies). 2) Impact on EBITDA as from 2015

Op

era

tio

na

l C

om

me

rcia

l

28

Modernization enabled the reduction by 53% of incidents in the modernized grids.

Modernizing the distribution grid

2013 2012 2011

Number of incidents (Paulista and Piratininga)

Modernization of Urban Grid

Company Primary

Protected Secondary Insulated

Piratininga 26% 56%

Paulista 20% 33%

And invests in modernizing the distribution grid

Spacer Cable

Multiplex

From 2010 through Jun/14:

Investments of over R$ 180 million

Modernization of 5,291 Km of grid

Improvement in grid quality, optimizing maintenance costs

12,963

16,857 Avg.2011/2012 = 14,910

-53%

7,056

29

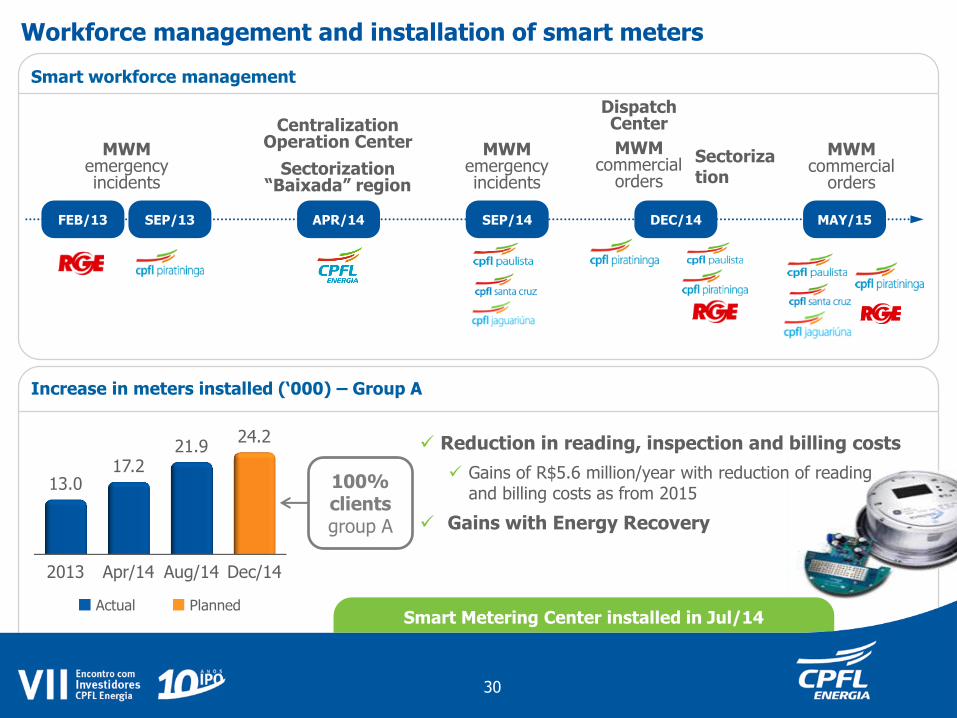

Workforce management and installation of smart meters

Smart workforce management

MWM emergency incidents

Centralization Operation Center

Sectorization “Baixada” region

Dispatch Center

MWM commercial

orders

MWM commercial

orders

MWM emergency incidents

FEB/13 SEP/13 APR/14 SEP/14 DEC/14 MAY/15

Increase in meters installed (‘000) – Group A

2013 Apr/14 Aug/14 Dec/14

13.0 17.2

21.9 24.2

Reduction in reading, inspection and billing costs

Gains of R$5.6 million/year with reduction of reading and billing costs as from 2015

Gains with Energy Recovery

Smart Metering Center installed in Jul/14 Actual Planned

Sectorization

30

100% clients group A

Net Revenue (R$ million)* EBITDA (% CPFL Energia)*

EBITDA (R$ million)* Net Income (R$ million)*

Distribution | Economic and financial performance

2004 LTM3Q14

9,945

11,252 13.1%

2004 LTM3Q14

2,040 2,019

-1.0%

2004 LTM3Q14

509

855 68.0%

2004 LTM3Q14

75%

50%

(*) Constant currency - September/14. Restated by IGP-M inflation index. 2014 amounts adjusted for regulatory assets and liabilities and non-recurring effects.

31

CPFL Energia in the last 10 years

Sustainability

Differentiated Corporate Governance

Financial Discipline and Value Creation Synergic Growth and

Operating Efficiency

Generation and Commercialization

Segments

Distribution

Services and Telecom

Services & Telecom

Incorporation: 2008

Provision of customer relationship services to utility companies:

call center

face-to-face service

back office

credit recovery

ombudsman

help desk and sales

Foundation: 2006

Offers a wide range of value-added services:

engineering projects for transmission and distribution grids

equipment maintenance and recovery

self-generation grids

collection of utilities’ bills through an established authorized network

Service Segment

34

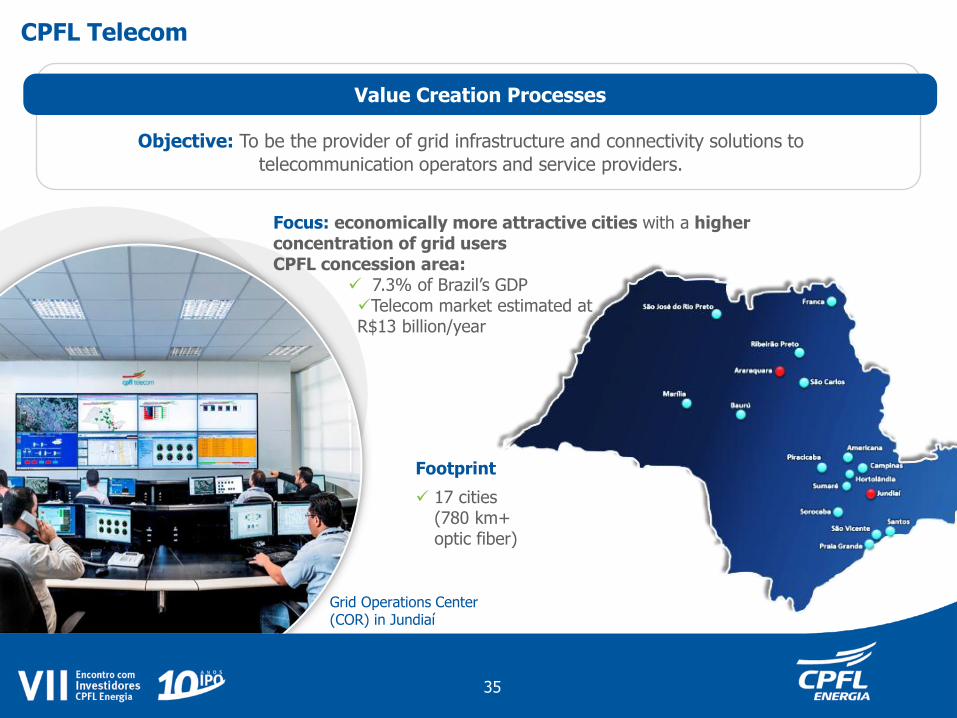

Focus: economically more attractive cities with a higher concentration of grid users CPFL concession area:

7.3% of Brazil’s GDP Telecom market estimated at R$13 billion/year

Value Creation Processes

Objective: To be the provider of grid infrastructure and connectivity solutions to

telecommunication operators and service providers.

CPFL Telecom

Footprint

17 cities (780 km+ optic fiber)

Grid Operations Center (COR) in Jundiaí

35

Net Revenue (R$ million)* EBITDA (% CPFL Energia)*

EBITDA (R$ million)* Net Income (R$ million)*

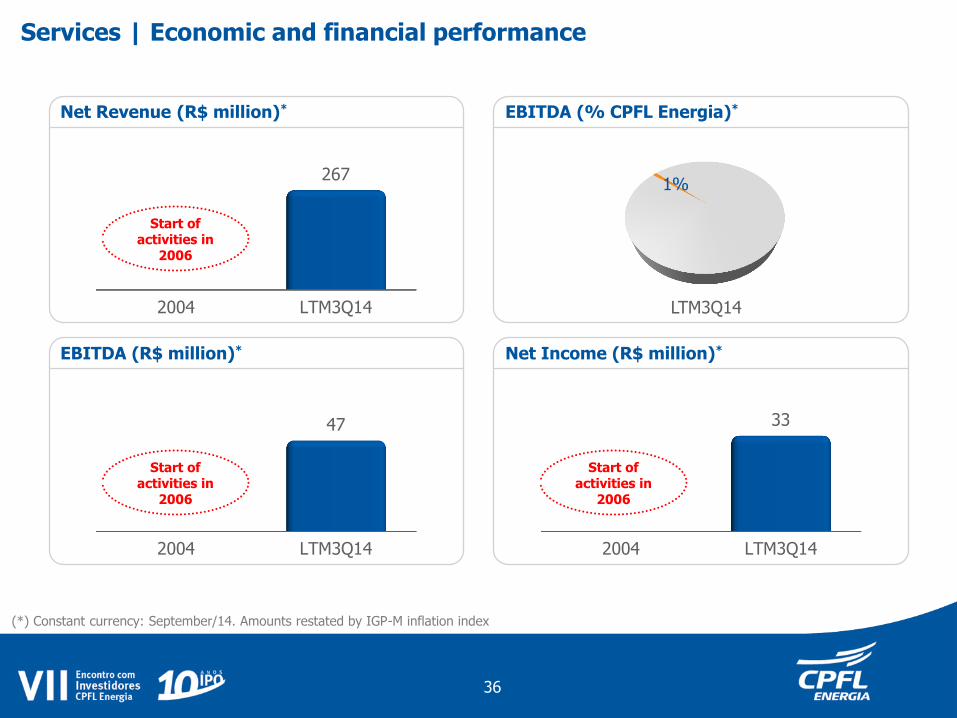

Services | Economic and financial performance

2004 LTM3Q14

267

2004 LTM3Q14

47

2004 LTM3Q14

33

LTM3Q14

9% 1%

(*) Constant currency: September/14. Amounts restated by IGP-M inflation index

Start of activities in

2006

Start of activities in

2006

Start of activities in

2006

36

CPFL Energia in the last 10 years

Sustainability

Differentiated Corporate Governance

Financial Discipline and Value Creation Synergic Growth and

Operating Efficiency

Generation and Commercialization

Segments

Distribution

Services and Telecom

Net Revenue (R$ million)* EBITDA (% consolidated)*

EBITDA (R$ million)* Net Income (R$ million)*

CPFL Energia | Economic and financial performance

2004 LTM3Q14

10,611

14,697 38.5%

2004 LTM3Q14

2,648

3,956

2004 LTM3Q14

440

1,235 181.0%

2004 LTM3Q14

75%

50%

(*) Constant currency - September/14. Restated by IGP-M inflation index. 2014 amounts adjusted for regulatory assets and liabilities and non-recurring effects.

49.4%

9% 6%

16% 44%

C

G

D

C/S

G

D

38

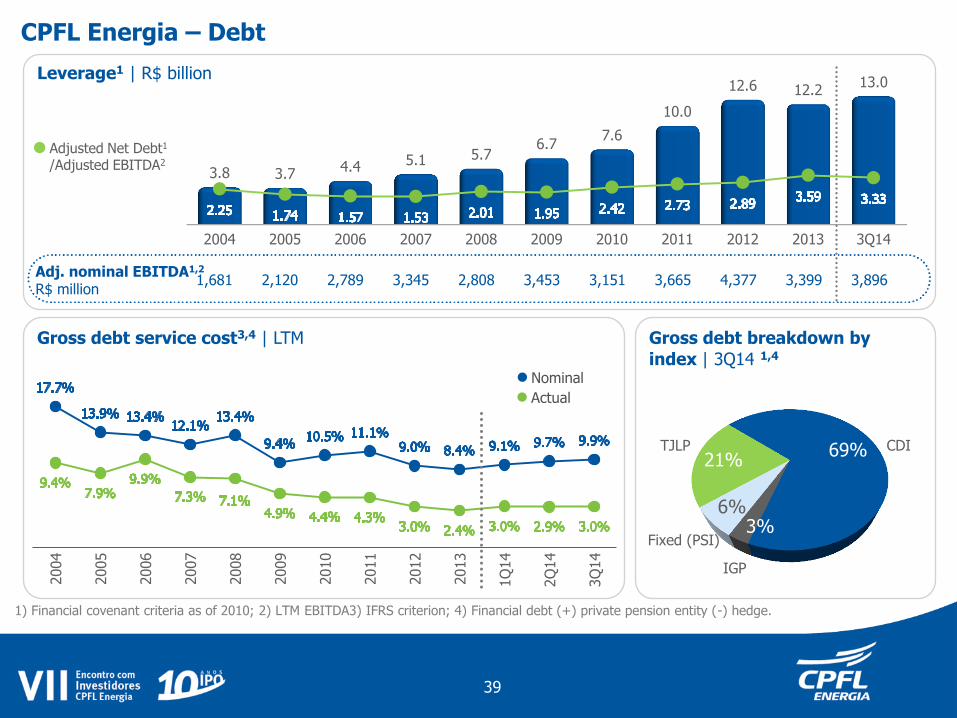

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 3Q14

3.8 3.7 4.4 5.1 5.7 6.7

7.6

10.0

12.6 12.2 13.0

Leverage1 | R$ billion

Adjusted Net Debt1

/Adjusted EBITDA2

1,681 2,120 2,789 3,345 2,808 3,453 3,151 3,665 4,377 3,399 3,896 Adj. nominal EBITDA1,2

R$ million

69%

3% 6%

21% CDI

Fixed (PSI)

IGP

TJLP

Gross debt breakdown by

index | 3Q14 1,4

Gross debt service cost3,4 | LTM

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

1Q

14

2Q

14

3Q

14

Nominal

Actual

1) Financial covenant criteria as of 2010; 2) LTM EBITDA3) IFRS criterion; 4) Financial debt (+) private pension entity (-) hedge.

CPFL Energia – Debt

39

Dividend Yield 1 (last 12 months) Declared dividends2 (R$ million) Average quote at close (R$/common share)3

2H04 1H05 2H05 1H06 2H06 1H07 2H07 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14

140

401 498

612 722

842 719

602 606 572 655

774

486

748 758 640

456 363

568

422

8.9 9.43 11.67

15.02 14.13 15,87 17.99 18.05 16.69 15.77 16.51 18.44 20.18 22.05 21.95

26.30 22.95

21.11 19.80 18.35

3.7%

6.5%

9.1% 8.7% 9.6%

10.9% 9.7%

7.6% 7.3% 7.6% 7.9% 8.6%

6.9% 6.0%

7.1% 6.1%

4.6% 3.9%

4.8% 5.4%

CPFL Energia – Dividends

Since the IPO in Sep/14, CPFL has been paying dividends close to the entire net income, reaching R$11.6 billion in nominal terms, or R$15.5 billion in real terms4

(1) Dividend yield in the last two six-month periods; (2) Refers to dividends declared. Payment in the subsequent six-month period; (3) Considers the quote adjusted by stock split/reverse split on June 29, 2011 (not adjusted for earnings); (4) Adjusted by IGP-M (Jun/14).

40

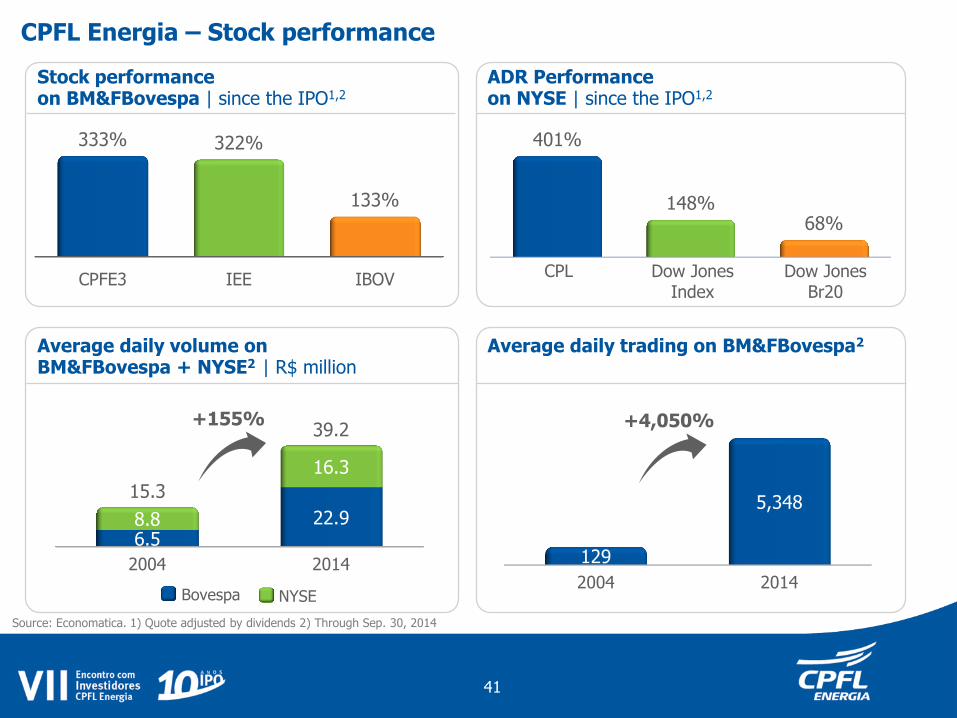

CPFL Energia – Stock performance

Source: Economatica. 1) Quote adjusted by dividends 2) Through Sep. 30, 2014

CPFE3 IEE IBOV

333% 322%

133%

401%

148% 68%

CPL Dow Jones Br20

Dow Jones Index

Bovespa NYSE

Average daily volume on BM&FBovespa + NYSE2 | R$ million

Average daily trading on BM&FBovespa2

ADR Performance on NYSE | since the IPO1,2

Stock performance on BM&FBovespa | since the IPO1,2

2004 2014

6.5 22.9 8.8

16.3

+155%

15.3

39.2

2004 2014

129

5,348

+4,050%

41

CPFL Energia in the last 10 years

Sustainability

Differentiated Corporate Governance

Financial Discipline and Value Creation Synergic Growth and

Operating Efficiency

Generation and Commercialization

Segments

Distribution

Services and Telecom

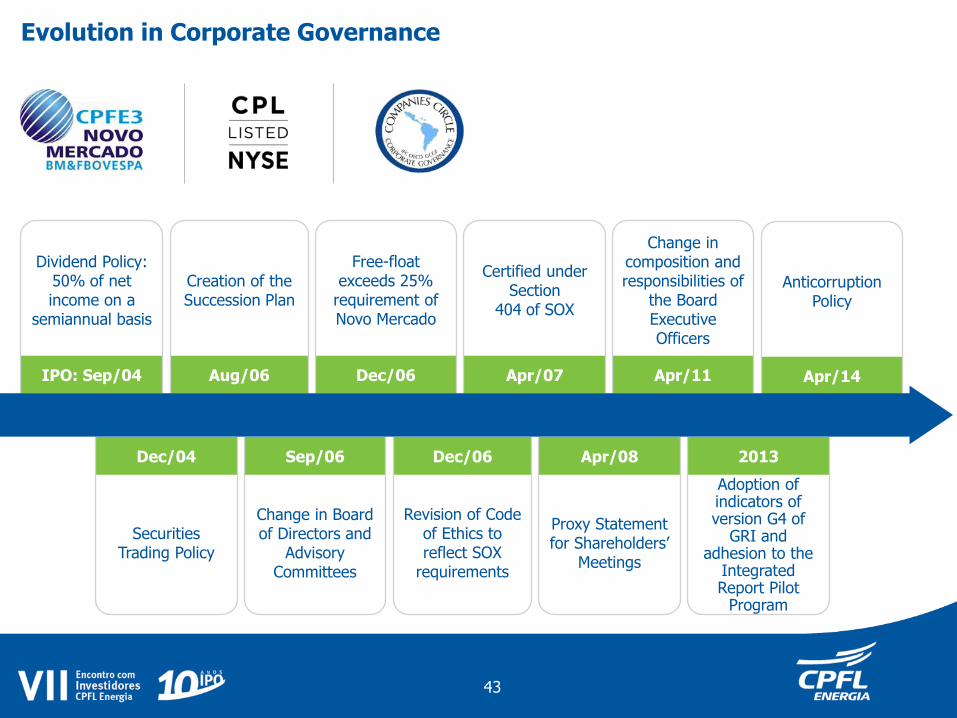

Evolution in Corporate Governance

Securities Trading Policy

Dividend Policy: 50% of net income on a

semiannual basis

Creation of the Succession Plan

Free-float exceeds 25%

requirement of Novo Mercado

Certified under Section

404 of SOX

Change in composition and responsibilities of

the Board Executive Officers

Change in Board of Directors and

Advisory Committees

Revision of Code of Ethics to reflect SOX

requirements

Proxy Statement for Shareholders’

Meetings

Adoption of indicators of version G4 of

GRI and adhesion to the

Integrated Report Pilot

Program

IPO: Sep/04 Aug/06 Dec/06 Apr/07 Apr/11

Dec/04 Sep/06 Dec/06 Apr/08 2013

Anticorruption Policy

Apr/14

43

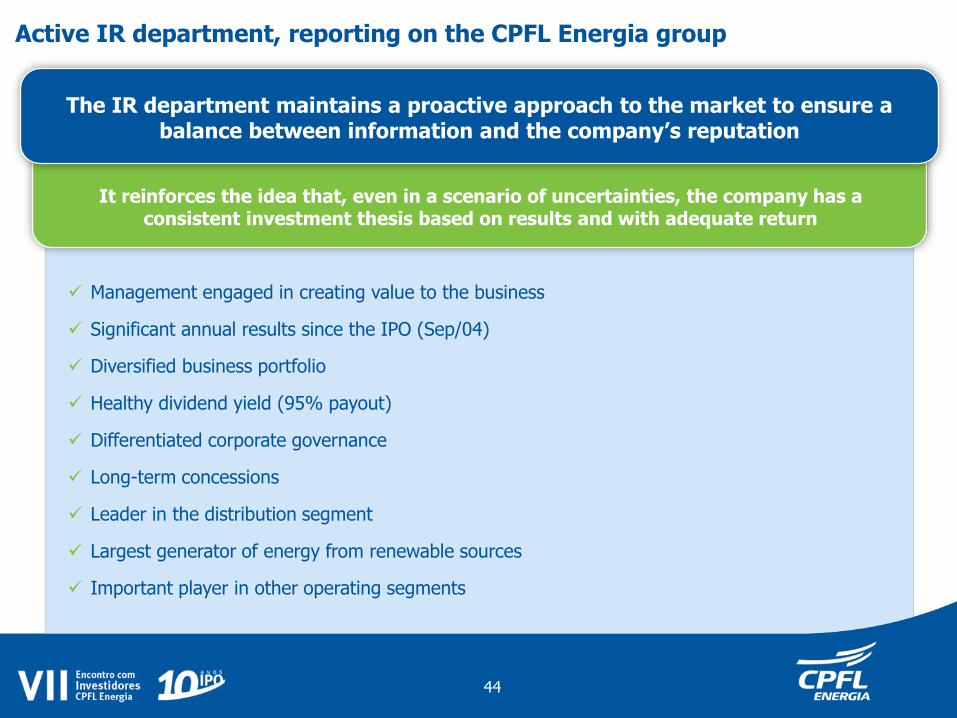

Active IR department, reporting on the CPFL Energia group

Management engaged in creating value to the business

Significant annual results since the IPO (Sep/04)

Diversified business portfolio

Healthy dividend yield (95% payout)

Differentiated corporate governance

Long-term concessions

Leader in the distribution segment

Largest generator of energy from renewable sources

Important player in other operating segments

It reinforces the idea that, even in a scenario of uncertainties, the company has a consistent investment thesis based on results and with adequate return

The IR department maintains a proactive approach to the market to ensure a balance between information and the company’s reputation

44

CPFL Energia present in major indexes

1,454+ meetings

142 conferences 78 domestic and 64 international

7 Investor Meetings

74 Public Meetings with Analysts

45

CPFL Energia in the last 10 years

Sustainability

Differentiated Corporate Governance

Financial Discipline and Value Creation Synergic Growth and

Operating Efficiency

Generation and Commercialization

Segments

Distribution

Services and Telecom

Evolution of Sustainability at CPFL Energia

Increasingly more comprehensive concept of responsibility

Welfare

Until 1999

Donations

External actions in support of community

Social Responsibility 2000 to 2003

Process management (certification)

Pursuit of quality processes

Introducing the Concept 2004 to2006

Quality relations

Management of relationship with

stakeholders (long-term

relationship)

Pursuing a Leading Role

As of 2006

Sharing

Mobilization and benchmark

Transition to a new economy

As of 2009

Innovation and cultural change

Guidelines for new

businesses

Corporate sustainability

Sta

ge

Fo

cu

s o

f a

cti

on

A

pp

roa

ch

Inclusion in businesses As of 2013

Strategic approach to sustainability

Sustainability as

Value driver

From welfare to sustainable businesses

47

Sustainability Concept at CPFL Energia

Energy is essential for

the wellness of people

and the development

of society.

We believe that

generating and using

energy in a

sustainable manner

is vital for the future of

mankind.

Vision

To provide

sustainable energy

solutions with

excellence and

competitiveness,

operating in close

integration with the

community.

Mission

• Value Creation

• Commitment

• Safety/Quality of Life

• Austerity

• Sustainability

• Trust and Respect

• Overcoming

challenges

• Entrepreneurship

Principles

CPFL Energia is Brazil’s

largest private group in

the electricity sector,

offering sustainable

energy solutions

through innovative

strategies and talented

professionals.

Positioning

The consolidation of its growth strategy through the implementation of targets and indicators for business units resulted in the inclusion of Sustainability as a driver of value in its strategic

plan.

Sustainability Platform

48

Do assistencialismo aos negócios sustentáveis Principais Prêmios e Reconhecimentos

CPFL Energia

Model Company – Guia Exame de Sustentabilidade We have been present in 11 of the 15 editions 2002|2003|2004|2006|2007|2008|2009|2010|2012|2013|2014

CPFL Energia

Época Empresa Verde Award: 2012 (among 20 best practices) Época Mudanças Climáticas Award: 2012 (winner in the Services category)

ISE – 2015 portfolio

CPFL Energia included in the index for the 10th consecutive year. Company is one of the 13 groups

included in ISE since its creation in Dec/05.

Dow Jones Sustainability Index Emerging Markets (DJSI Emerging Markets)

For the 3rd time, we have been included in the index that evaluates the performance of leaders in sustainability in emerging markets. The current portfolio includes 86 companies, 17 of which are Brazilian.

Benchmark in Business Sustainability

Carbon Disclosure Project

Since 2006, CPFL Energia reports to the market, through CDP Investor and CDP Supply Chain, its

activities regarding greenhouse gas emissions, where it is considered a benchmark not only in the

electricity sector but also in Brazil.

“Respondent of the Brazilian edition of the Climate Change program 2014”

49

The future of CPFL Energia

Conventional generation

Renewable generation

Commercialization

Distribution

Services & Telecom

The future of CPFL Energia

Conventional generation Renewable generation

Commercialization

Distribution

Services & Telecom

Rationale of creation of value of the Distribution business

Purchase of Energy Costs transferred to the tariff

Any time mismatches accounted for as CVA and transferred in the following year adjustment

Parcela A (76% da receita)

Parcel A (76% of revenue)

Charges and Transport

Focus on creating value from the business

Regulation through incentive enables the creation of value through efficient management and investments in RAB

Regulatory and institutional management are drivers of value creation

Parcel B (24% of revenue)

Operating efficiency

Investment in RAB

Discussions of the methodology for the 4CRTP do not change the value creation rationale

Other Revenues

52

Recognize the level of real losses for companies with low level of technical and non-technical losses, establishing an “attainable” base for Regulatory Losses of other distributors

Recognize as expense the amounts not accepted in the asset base of distributors

Recognize a non-compensated Asset Management Fee (avoiding exchange of asset). Existing alternatives result in a range that is specific for each company, between 10%-20% of regulatory WACC

Recognize revenues from Surplus Reactive Power and Excess over Contracted Demand are part of the initial balance of the concession agreement

Partial sharing of productivity in detriment to full capture

Maintenance of asset valuation by VNR for key equipment. Smaller components and additional costs calculated with support from constructive modules.

Revision of the need for contractual amendment to provide new ancillary activities

Maintenance of methodology Revision: from 1.11% to 1.91%

Maintenance of methodology. Restatement of the index of social and economic complexity

Improvement of 3CRTP benchmarking model

Defense of the maintenance of the concept of spread over real PMSO for the most efficient companies

CPFL’s demand is for ANEEL to conduct an analysis of the global consistency of results

RAB

COR

Other revenues

X Factor

Losses

CPFL Energia Proposal Aneel Proposal

53

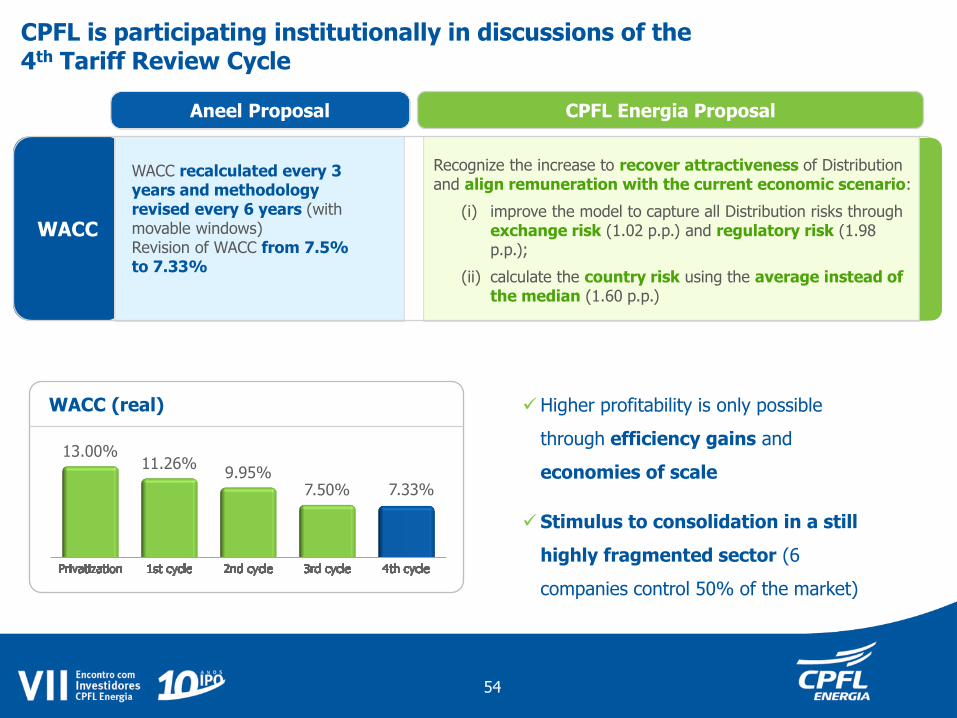

CPFL is participating institutionally in discussions of the 4th Tariff Review Cycle (4CRTP)

WACC

CPFL is participating institutionally in discussions of the 4th Tariff Review Cycle

WACC recalculated every 3 years and methodology revised every 6 years (with movable windows) Revision of WACC from 7.5% to 7.33%

13.00% 11.26%

9.95% 7.50% 7.33%

Higher profitability is only possible

through efficiency gains and

economies of scale

Stimulus to consolidation in a still

highly fragmented sector (6

companies control 50% of the market)

Recognize the increase to recover attractiveness of Distribution and align remuneration with the current economic scenario:

(i) improve the model to capture all Distribution risks through exchange risk (1.02 p.p.) and regulatory risk (1.98 p.p.);

(ii) calculate the country risk using the average instead of the median (1.60 p.p.)

WACC (real)

CPFL Energia Proposal Aneel Proposal

54

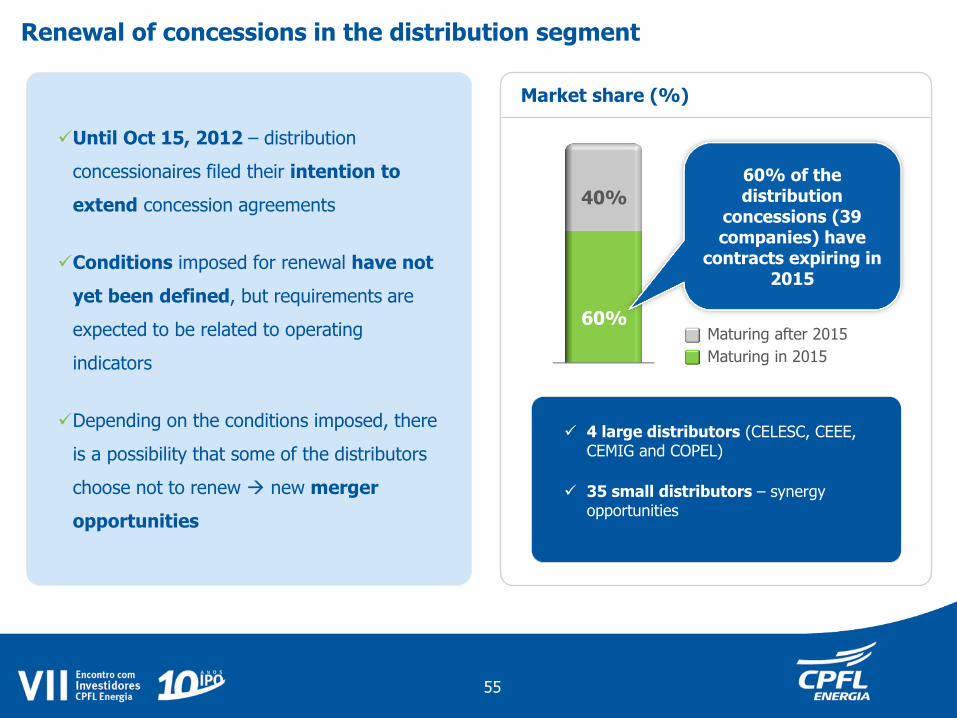

Maturing in 2015

Maturing after 2015

4 large distributors (CELESC, CEEE, CEMIG and COPEL)

35 small distributors – synergy opportunities

Until Oct 15, 2012 – distribution

concessionaires filed their intention to

extend concession agreements

Conditions imposed for renewal have not

yet been defined, but requirements are

expected to be related to operating

indicators

Depending on the conditions imposed, there

is a possibility that some of the distributors

choose not to renew new merger

opportunities

60%

40%

60% of the distribution

concessions (39 companies) have

contracts expiring in 2015

Renewal of concessions in the distribution segment

Market share (%)

55

The future of CPFL Energia

Conventional sources Renewable sources

Commercialization

Distribution

Services & Telecom

PhysicalGuarantee

Actualgeneration

100

92

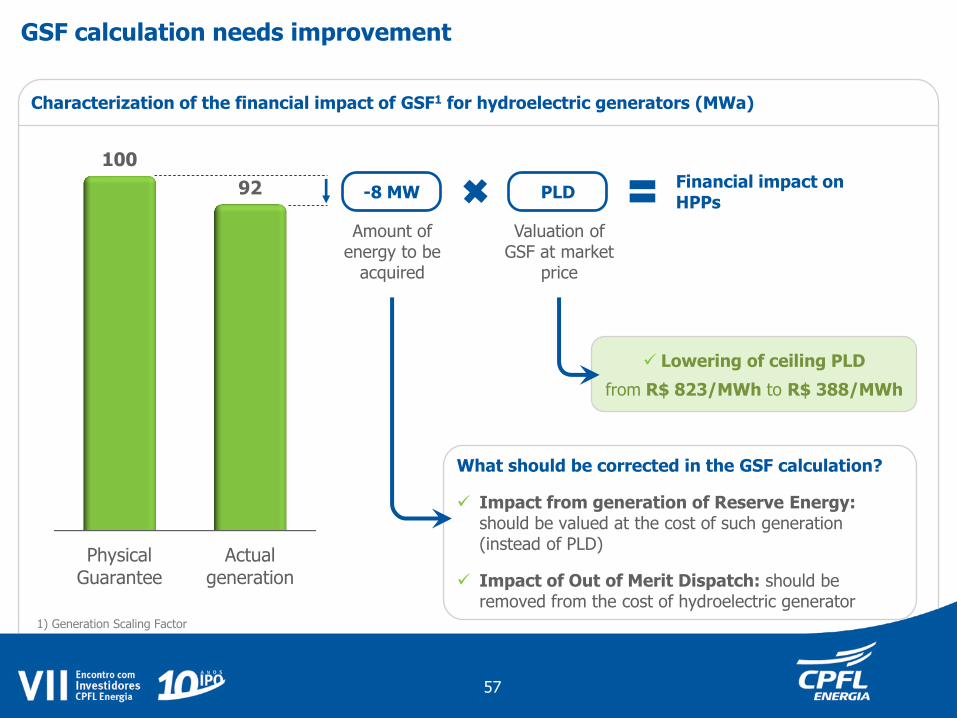

GSF calculation needs improvement

Characterization of the financial impact of GSF1 for hydroelectric generators (MWa)

-8 MW

Amount of energy to be

acquired

Valuation of GSF at market

price

PLD Financial impact on HPPs

Lowering of ceiling PLD

from R$ 823/MWh to R$ 388/MWh

What should be corrected in the GSF calculation?

Impact from generation of Reserve Energy: should be valued at the cost of such generation (instead of PLD)

Impact of Out of Merit Dispatch: should be removed from the cost of hydroelectric generator

57

1) Generation Scaling Factor

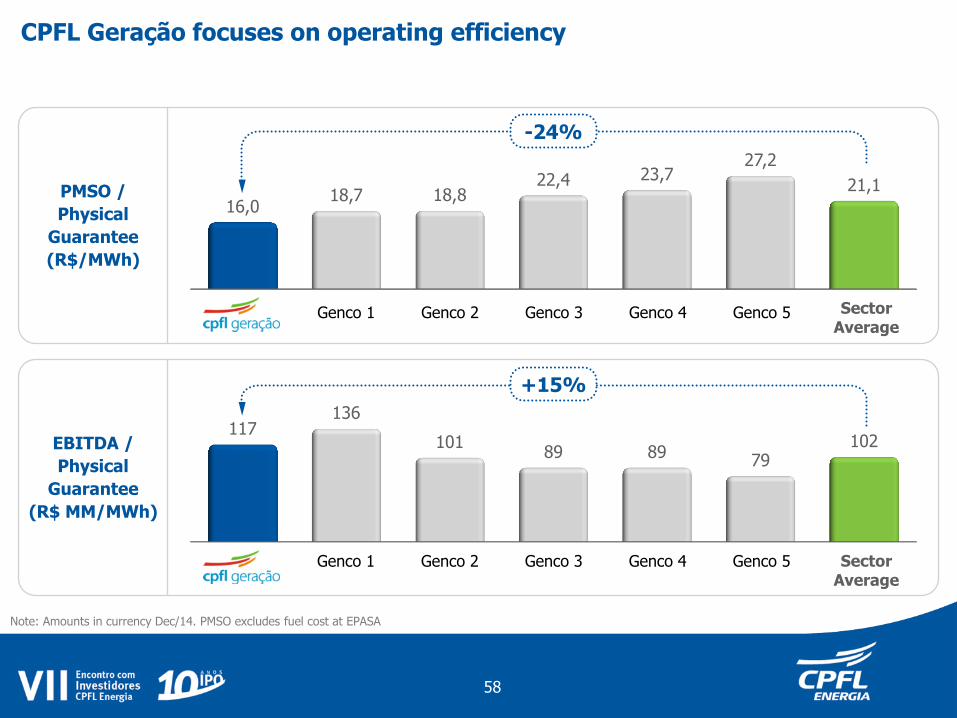

16,0 18,7 18,8

22,4 23,7 27,2

21,1

CPFL Geração focuses on operating efficiency

Note: Amounts in currency Dec/14. PMSO excludes fuel cost at EPASA

PMSO /

Physical

Guarantee

(R$/MWh)

EBITDA /

Physical

Guarantee

(R$ MM/MWh)

Sector Average

Sector Average

117 136

101 89 89 79

102

-24%

+15%

58

Genco 1 Genco 2 Genco 3 Genco 4 Genco 5

Genco 1 Genco 2 Genco 3 Genco 4 Genco 5

The future of CPFL Energia

Conventional sources Renewable sources

Commercialization

Distribution

Services & Telecom

Largest player in renewable energy sector1

399

940

670

190

532 464

71 19 157

1,002

462

353 159 197 38

370

116 13

1.1

3

335

940

670 652 532

464

353 349

229 195

58 34

2,108

Under construction

SHPP

Biomass

Solar

Wind

1,772

Market share > 8%

Consolidation

opportunities

CPFL Renováveis | Consolidation opportunities

60

(1) Installed capacity in operation (MW).

Potential growth in renewable energy market

86

117

11

12

11

20 17

47

Renováveis

Outros

Gás Natural

Hidro

2023 estimated 2013 actual

Increase in Brazil’s installed capacity by

source | GW

4.6% p.a.

196

125

CAGR

0.9%

10.5%

6.5%

3.1% 2

Renewable energies in Brazil should grow 10.5% p.a., from 17 GW in 2013 to 47 GW in

2023

1% Wind Potential: 350GW

Installed capacity: 3.8GW

29% SHPP Potential: 17.5GW Installed capacity: 5.0GW

54% Biomass Potential: 17.2GW Installed capacity: 9.3GW

Potential to be explored in Brazil2

Actual

61

(1) Potential: PDE 2022; installed capacity: BIG - ANEEL August/2014; (2) Includes estimated import from Itaipu HPP not consumed by Paraguay

Renewables

Other

Natural Gas

Hydro²

Sustainability & Safety

Operating efficiency

Growth

Strategic guidelines for CPFL Renováveis

High operating performance and efficacy in management, supported by controls, processes, systems, organizational structure and institutional presence.

To be the benchmark in sustainability, contributing to the development of the communities where we operate, while striving for safety, the environment and reduction of greenhouse gas emissions.

Maintain business growth with value creation (returns above cost of capital).

Excellence in implementation of generation, M&A and innovation projects.

62

The future of CPFL Energia

Conventional sources Renewable sources

Commercialization

Distribution

Services & Telecom

64

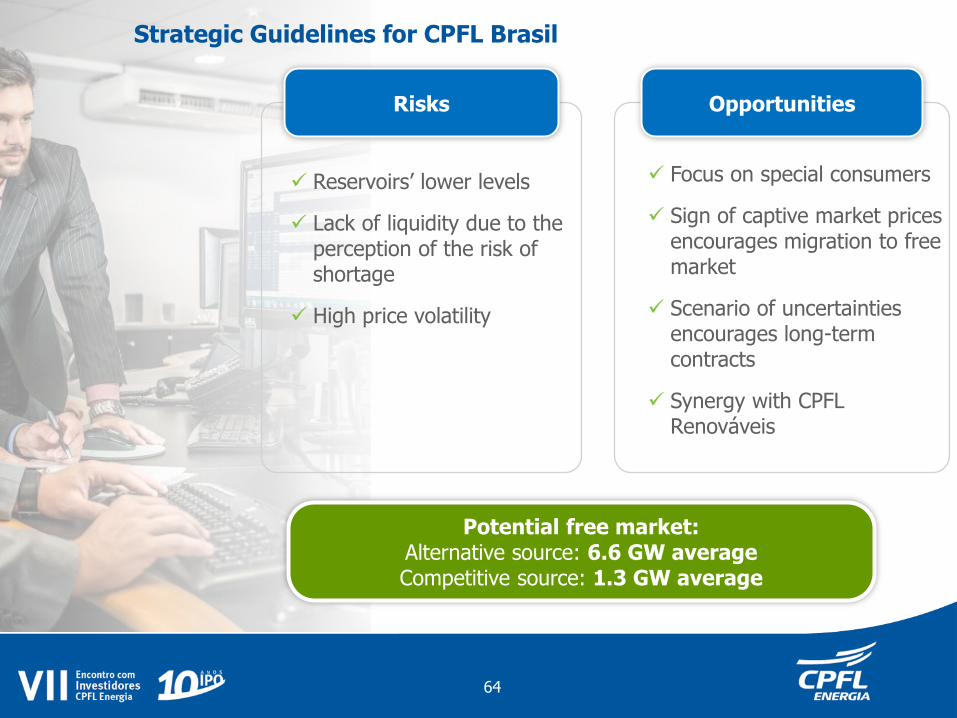

Reservoirs’ lower levels

Lack of liquidity due to the perception of the risk of shortage

High price volatility

Potential free market: Alternative source: 6.6 GW average Competitive source: 1.3 GW average

Focus on special consumers

Sign of captive market prices encourages migration to free market

Scenario of uncertainties encourages long-term contracts

Synergy with CPFL Renováveis

Strategic Guidelines for CPFL Brasil

Risks Opportunities

The future of CPFL Energia

Conventional sources Renewable sources

Commercialization

Distribution

Services & Telecom

Market enjoying accelerated growth, especially in broadband, requires investment

Growth of sales and revenue generation in the 17 cities where the project has been implemented

Geographic expansion on demand, according to client requirements and profitability of projects

CPFL Telecom

Opportunities for CPFL Serviços and CPFL Telecom

CPFL Serviços

Development of qualified manpower and suppliers, improving the quality of services

Use of technology to improve productivity and quality

Financial capacity to invest in new technologies

66

GENERATION

• To act on both institutional and regulatory fronts to mitigate business risks

• To be efficient in managing energy contracts

• Maintain the leadership in operating efficiency across the sector

Strategic guidelines of the current businesses of CPFL Energia

COMMERCIALIZATION

• To maximize value in the free market by operating within the risk thresholds

• To operate with the focus on special clients

• To explore synergies through strategic operations: ESCO and Retail Commercialization

DISTRIBUTION

• To be the leader in operating efficiency by investing in technology, automation and innovation

• To act on both institutional and regulatory fronts to ensure sustainability of the sector

SERVICES

• To operate with the focus on Technical Services, with technology and productivity

• To mitigate service risk by hiring qualified manpower and suppliers

RENEWABLES

• Growth while creating value through acquisitions and greenfield projects

• To be the leader in operating efficiency in the Renewables segment

TELECOM

• Sales growth in the 17 cities where the project has been implemented

• Geographic expansion on demand according to client requirements and profitability of projects

67