FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR’S REPORT DON AVANTE ASSOCIATES II, L.P. A California Limited Partnership Village Avante Apartments FHA Project No. 121-35883-PM December 31, 2013 and 2012

Transcript

FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR’S REPORT

DON AVANTE ASSOCIATES II, L.P.

A California Limited Partnership

Village Avante Apartments FHA Project No. 121-35883-PM

December 31, 2013 and 2012

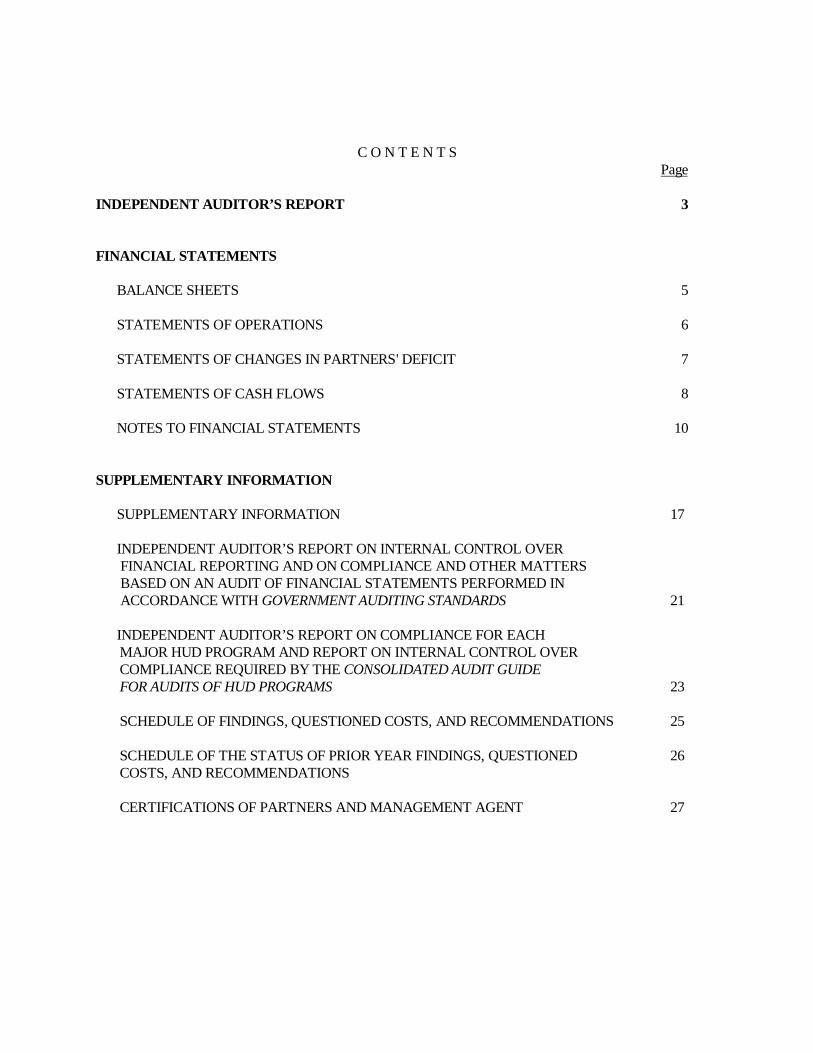

C O N T E N T S Page INDEPENDENT AUDITOR’S REPORT 3 FINANCIAL STATEMENTS BALANCE SHEETS 5 STATEMENTS OF OPERATIONS 6 STATEMENTS OF CHANGES IN PARTNERS' DEFICIT 7 STATEMENTS OF CASH FLOWS 8 NOTES TO FINANCIAL STATEMENTS 10 SUPPLEMENTARY INFORMATION SUPPLEMENTARY INFORMATION 17 INDEPENDENT AUDITOR’S REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS 21 INDEPENDENT AUDITOR’S REPORT ON COMPLIANCE FOR EACH MAJOR HUD PROGRAM AND REPORT ON INTERNAL CONTROL OVER COMPLIANCE REQUIRED BY THE CONSOLIDATED AUDIT GUIDE FOR AUDITS OF HUD PROGRAMS 23

SCHEDULE OF FINDINGS, QUESTIONED COSTS, AND RECOMMENDATIONS 25 SCHEDULE OF THE STATUS OF PRIOR YEAR FINDINGS, QUESTIONED 26 COSTS, AND RECOMMENDATIONS CERTIFICATIONS OF PARTNERS AND MANAGEMENT AGENT 27

INDEPENDENT AUDITOR’S REPORT To the Partners Don Avante Associates II, L.P. A California Limited Partnership Report on the Financial Statements We have audited the accompanying financial statements of Don Avante Associates II, L.P., a California Limited Partnership, FHA Project No. 121-35883-PM which comprise the balance sheets as of December 31, 2013 and 2012, and the related statements of operations, changes in partners' deficit, and cash flows for the years then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Don Avante Associates II, L.P., a California Limited Partnership, as of December 31, 2013 and 2012, and the results of its operations, changes in partners' deficit, and cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America.

INDEPENDENT AUDITOR’S REPORT (Continued) Other Matters Other Information Our audits were conducted for the purpose of forming an opinion on the financial statements taken as a whole. The accompanying supplementary information shown on pages 17 to 27 is presented for purposes of additional analysis, and is not a required part of the financial statements. The accompany supplementary information shown on pages 17 to 27 is the responsibility of management and was derived from and relates directly to the underlying accounting and other audit records used to prepare the financial statements. Such information has been subjected to the auditing procedures applied in the audit of the financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the accompanying supplementary information shown on pages 17 to 27 is fairly stated, in all material respects, in relation to the financial statements taken as a whole. Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued a report dated March 13, 2014 on our consideration of Don Avante Associates II, L.P.’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, grant agreements, and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering Don Avante Associates II, L.P.’s internal control over financial reporting and compliance.

Moraga, California March 13, 2014 Lead Auditor: Annette M. Spiteri, CPA Federal Tax Identification Number: 68-01990999

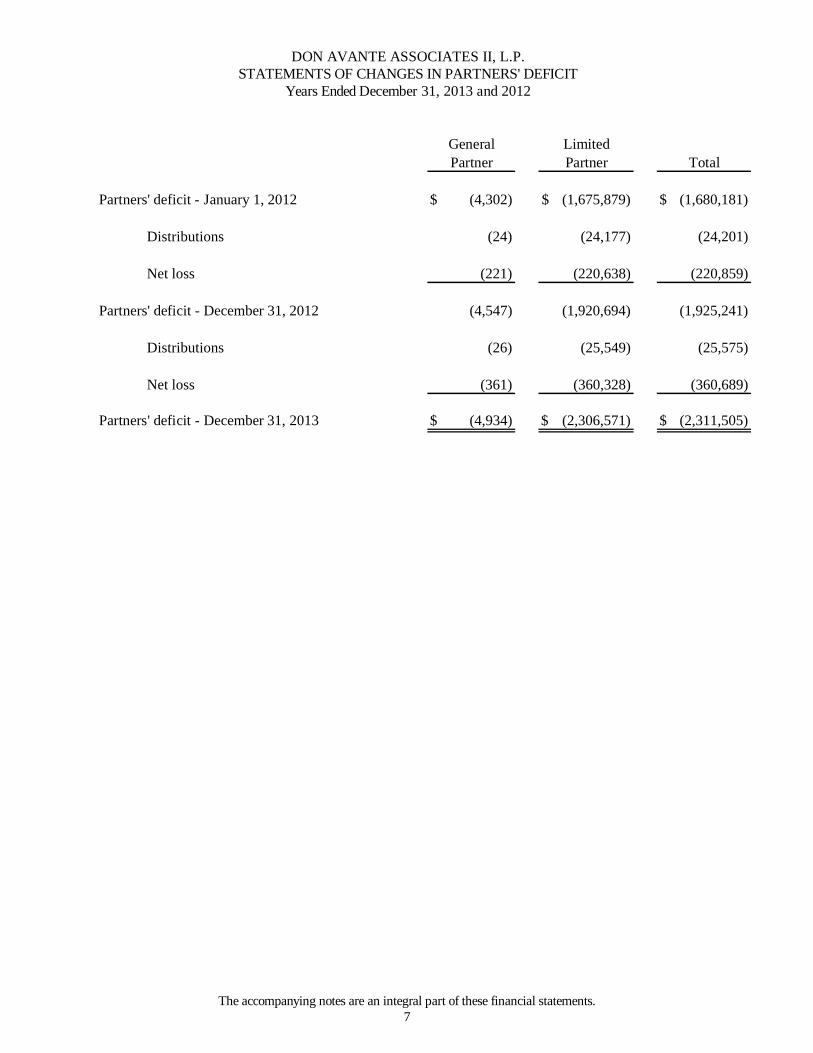

The accompanying notes are an integral part of these financial statements. 5

DON AVANTE ASSOCIATES II, L.P. BALANCE SHEETS

December 31, 2013 and 2012

ASSETS

Property and equipment1410 Land $ 1,230,000 $ 1,230,0001420 Buildings and improvements 10,900,962 10,887,6331460 Furnishings and equipment 960,218 885,7101400T Total property and equipment 13,091,180 13,003,343 1495 Less accumulated depreciation (5,264,446) (4,892,136) 1400N Net property and equipment 7,826,734 8,111,207

Net cash provided by operating activities $ 74,987 $ 196,069

2013 2012

10

DON AVANTE ASSOCIATES II, L.P. NOTES TO FINANCIAL STATEMENTS

December 31, 2013 and 2012

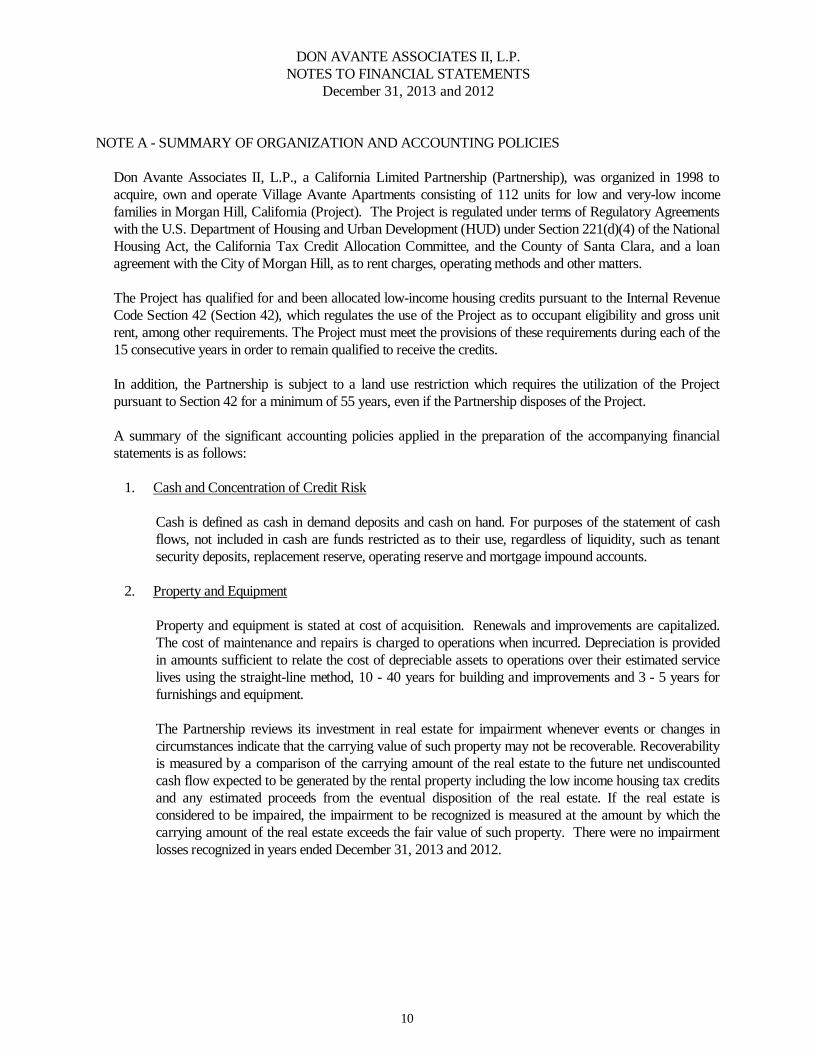

NOTE A - SUMMARY OF ORGANIZATION AND ACCOUNTING POLICIES

Don Avante Associates II, L.P., a California Limited Partnership (Partnership), was organized in 1998 to acquire, own and operate Village Avante Apartments consisting of 112 units for low and very-low income families in Morgan Hill, California (Project). The Project is regulated under terms of Regulatory Agreements with the U.S. Department of Housing and Urban Development (HUD) under Section 221(d)(4) of the National Housing Act, the California Tax Credit Allocation Committee, and the County of Santa Clara, and a loan agreement with the City of Morgan Hill, as to rent charges, operating methods and other matters. The Project has qualified for and been allocated low-income housing credits pursuant to the Internal Revenue Code Section 42 (Section 42), which regulates the use of the Project as to occupant eligibility and gross unit rent, among other requirements. The Project must meet the provisions of these requirements during each of the 15 consecutive years in order to remain qualified to receive the credits. In addition, the Partnership is subject to a land use restriction which requires the utilization of the Project pursuant to Section 42 for a minimum of 55 years, even if the Partnership disposes of the Project. A summary of the significant accounting policies applied in the preparation of the accompanying financial statements is as follows:

1. Cash and Concentration of Credit Risk

Cash is defined as cash in demand deposits and cash on hand. For purposes of the statement of cash flows, not included in cash are funds restricted as to their use, regardless of liquidity, such as tenant security deposits, replacement reserve, operating reserve and mortgage impound accounts.

2. Property and Equipment

Property and equipment is stated at cost of acquisition. Renewals and improvements are capitalized. The cost of maintenance and repairs is charged to operations when incurred. Depreciation is provided in amounts sufficient to relate the cost of depreciable assets to operations over their estimated service lives using the straight-line method, 10 - 40 years for building and improvements and 3 - 5 years for furnishings and equipment. The Partnership reviews its investment in real estate for impairment whenever events or changes in circumstances indicate that the carrying value of such property may not be recoverable. Recoverability is measured by a comparison of the carrying amount of the real estate to the future net undiscounted cash flow expected to be generated by the rental property including the low income housing tax credits and any estimated proceeds from the eventual disposition of the real estate. If the real estate is considered to be impaired, the impairment to be recognized is measured at the amount by which the carrying amount of the real estate exceeds the fair value of such property. There were no impairment losses recognized in years ended December 31, 2013 and 2012.

11

DON AVANTE ASSOCIATES II, L.P. NOTES TO FINANCIAL STATEMENTS

December 31, 2013 and 2012

NOTE A - SUMMARY OF ORGANIZATION AND ACCOUNTING POLICIES (Continued)

3. Tenant Receivables

The Partnership elects to record bad debt using the direct write-off method. Generally accepted accounting principles in the United States of America (GAAP) require that the allowance method be used to reflect bad debts. However, the effect of the use of the direct write-off method is not materially different from the result that would be obtained had the allowance method been followed.

4. Deferred Financing Costs, Other Deferred Costs and Amortization Financing costs are amortized over the term of the mortgage loan using the straight-line method. GAAP requires that the effective yield method be used to amortize financing costs; however, the effect of using the straight-line method is not materially different from the results that would have been obtained under the effective yield method.

5. Fair Value of Financial Instruments

The carrying amounts of financial instruments including cash and cash equivalents, accounts receivable, accounts payable and accrued expenses, and customer deposits approximate fair value due to the relatively short term maturity of these instruments. The carrying value of long-term debt approximates fair value based on prevailing borrowing rates currently available for loans with similar terms and maturities.

6. Tenant Rental Income

Rental income is recognized as rent becomes due. Rental payments received in advance are deferred until earned. All leases between the Partnership and tenants of the Project are operating leases. Lease terms are usually one year or less.

7. Advertising Costs

Advertising costs are charged to operations when incurred. 8. Risks and Uncertainties

The Partnership is subject to various risks and uncertainties in the ordinary course of business that could have adverse impacts on its operating results and financial condition. Future operations could be affected by changes in the economy or other conditions in the geographical area where the Project is located or by changes in federal, state and/or local low-income housing subsidies or the demand for such housing.

9. Management's Estimates

Management uses estimates and assumptions in preparing financial statements. Those estimates and assumptions affect the reported amounts of assets and liabilities and the reported revenues and expenses. Actual results could differ from those estimates.

12

DON AVANTE ASSOCIATES II, L.P. NOTES TO FINANCIAL STATEMENTS

December 31, 2013 and 2012 NOTE A - SUMMARY OF ORGANIZATION AND ACCOUNTING POLICIES (Continued)

10. Income Taxes

Net earnings (loss) are reportable, on the accrual basis, by the partners on their individual tax returns, and, accordingly, no provision for income taxes has been made in the financial statements. The Partnership believes that it does not have any uncertain tax positions that are material to the financial statements. The federal and state tax returns for the years ending December 31, 2012, 2011, 2010 and 2009 are subject to examination by regulatory agencies, generally for three years and four years after they were filed for the federal and state returns, respectively.

11. Subsequent Events Subsequent events were evaluated through March 13, 2014, which is the date the financial statements were available to be issued.

NOTE B - DEFERRED COSTS

Deferred costs at December 31 consist of the following:

Mortgage payable to Midland Loan Services in the amount of $6,216,165 is due in monthly installments of $38,250, based upon a 30 year amortization of the loan including interest at 5.77%. The loan is insured by HUD, secured by a deed of trust on the Project, and is due in full in the year 2040. Principal payments due for each of the next five years ending December 31 are estimated as follows:

DON AVANTE ASSOCIATES II, L.P. NOTES TO FINANCIAL STATEMENTS

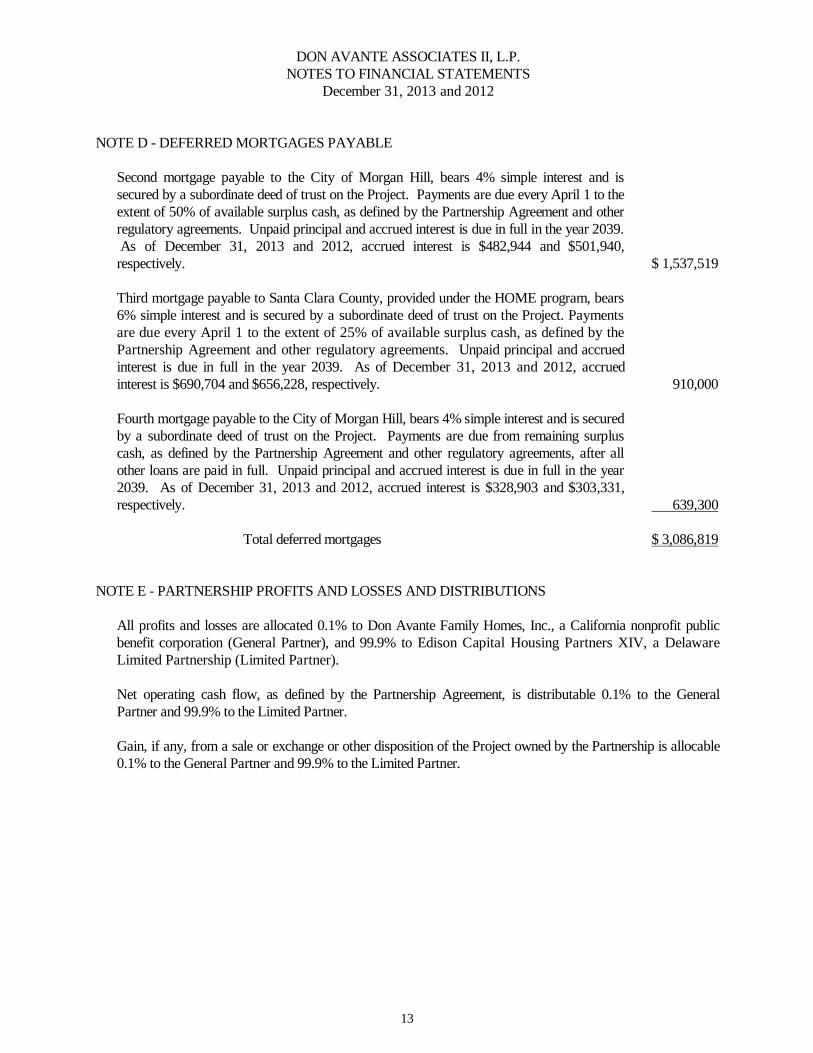

December 31, 2013 and 2012 NOTE D - DEFERRED MORTGAGES PAYABLE

Second mortgage payable to the City of Morgan Hill, bears 4% simple interest and is secured by a subordinate deed of trust on the Project. Payments are due every April 1 to the extent of 50% of available surplus cash, as defined by the Partnership Agreement and other regulatory agreements. Unpaid principal and accrued interest is due in full in the year 2039. As of December 31, 2013 and 2012, accrued interest is $482,944 and $501,940, respectively. $ 1,537,519

Third mortgage payable to Santa Clara County, provided under the HOME program, bears 6% simple interest and is secured by a subordinate deed of trust on the Project. Payments are due every April 1 to the extent of 25% of available surplus cash, as defined by the Partnership Agreement and other regulatory agreements. Unpaid principal and accrued interest is due in full in the year 2039. As of December 31, 2013 and 2012, accrued interest is $690,704 and $656,228, respectively. 910,000 Fourth mortgage payable to the City of Morgan Hill, bears 4% simple interest and is secured by a subordinate deed of trust on the Project. Payments are due from remaining surplus cash, as defined by the Partnership Agreement and other regulatory agreements, after all other loans are paid in full. Unpaid principal and accrued interest is due in full in the year 2039. As of December 31, 2013 and 2012, accrued interest is $328,903 and $303,331, respectively. 639,300 Total deferred mortgages $ 3,086,819

NOTE E - PARTNERSHIP PROFITS AND LOSSES AND DISTRIBUTIONS All profits and losses are allocated 0.1% to Don Avante Family Homes, Inc., a California nonprofit public

benefit corporation (General Partner), and 99.9% to Edison Capital Housing Partners XIV, a Delaware Limited Partnership (Limited Partner).

Net operating cash flow, as defined by the Partnership Agreement, is distributable 0.1% to the General

Partner and 99.9% to the Limited Partner.

Gain, if any, from a sale or exchange or other disposition of the Project owned by the Partnership is allocable 0.1% to the General Partner and 99.9% to the Limited Partner.

14

DON AVANTE ASSOCIATES II, L.P. NOTES TO FINANCIAL STATEMENTS

December 31, 2013 and 2012 NOTE F - RELATED PARTY TRANSACTIONS Property Management Fee

The Project is managed by EAH, Inc., a California nonprofit public benefit corporation (EAH), which is affiliated with the General Partner by key employees who are members on the Board of Directors of the General Partner. HUD has approved a management fee of 4.71% of collections, capped at $66 per unit per month, effective January 1, 2012 through December 31, 2014. For the years ended December 31, the following fees were paid to EAH:

As of December 31, 2013, receivable from other project consists of an amount due from an affiliated project for reimbursement of operating expenses totaling $3,111. As of December 31, 2013 and 2012, accounts payable includes amounts due to EAH for reimbursement of operating expenses totaling $13,936 and $17,764, respectively.

LP Asset Management Fee

The Limited Partner is entitled to an annual asset management fee of $6,000, which increases annually by 3.5%. This fee shall be paid only from available surplus cash, as defined by the Partnership Agreement and other regulatory agreements, as follows: $3,000 plus annual increase (I) before loan payments and $3,000 plus annual increase (II) after loan payments. As of December 31, 2013 and 2012, cumulative fees earned and unpaid amount to $9,382 and $9,065, respectively.

Partnership Management Fee

The General Partner is entitled to an annual partnership management fee of $25,000, which increases annually by 3.5%. This fee shall be paid only from available surplus cash, as defined by the Partnership Agreement and other regulatory agreements, as follows: $22,000 plus annual increase (I) before loan payments and $3,000 plus annual increase (II) after loan payments. As of December 31, 2013 and 2012, cumulative fees earned and unpaid amount to $40,469 and $39,100, respectively. Incentive Management Fee

The Partnership shall pay the General Partner annually, in arrears, an incentive management fee equal to 50% of surplus cash, as defined by the Partnership Agreement and other regulatory agreements, remaining after other priority payments not to exceed $50,000 annually. This fee shall not accrue. For the years ending December 31, 2013 and 2012, fees were paid in the amount of $25,575 and $24,201, respectively.

15

DON AVANTE ASSOCIATES II, L.P. NOTES TO FINANCIAL STATEMENTS

December 31, 2013 and 2012 NOTE F - RELATED PARTY TRANSACTIONS (Continued)

General Partner Guaranty Advances

The Indemnification Agreement provides for obligations of the General Partner, to advance funds for reductions of projected tax benefits. As of December 31, 2013, no funds have been advanced in connection with this guarantee.

NOTE G - HOUSING ASSISTANCE PAYMENT CONTRACT AGREEMENTS

The Partnership has entered into Housing Assistance Payments (HAP) Contract with HUD on behalf of qualified tenants. The contract covers 10 of the 112 units and is renewed annually on January 1. HUD has established various guidelines for the renewal of these contracts. For the years ended December 31, 2013 and 2012, receipts under the HAP Contracts totaled $138,900 and $140,455, respectively.

NOTE H - OPTION AGREEMENT

The General Partner has entered into an option agreement to purchase the Project. The option period commences January 1, 2015 and expires December 31, 2015. The purchase price of the Project shall be the greater of the then fair market value of the Project or the assumption of the outstanding debt secured by deeds of trust on the Project plus any other obligations of the Partnership.

NOTE I – CONTINGENCY

The Project’s low-income housing credits are contingent on its ability to maintain compliance with applicable sections of Section 42. Failure to maintain compliance with occupant eligibility, and/or unit gross rent, or to correct noncompliance within a specified time period, could result in recapture of previously taken tax credits plus interest.

SUPPLEMENTARY INFORMATION

17

DON AVANTE ASSOCIATES II, L.P. SUPPLEMENTARY INFORMATION

December 31, 2013 and 2012 SCHEDULES OF OPERATING EXPENSES

2013 2012Administrative expenses

6210 Advertising $ 936 $ 4056310 Office salaries 17,207 23,1576311 Office supplies 2,948 4,9676311 Computer charges 731 1,5466311 Computer licensing and internet charges 8,175 5,982 6311 Office equipment rental 419 - 6320 Property management fees 83,084 81,3246330 Manager's salary 67,549 52,2526331 Manager's rent free unit 17,796 17,7966340 Legal expense 2,523 3,271 6350 Audit expense 9,800 9,5716351 Bookkeeping fees/accounting services 19,596 19,5966311 Telephone and answering service 7,099 6,8456370 Bad debts 3,756 1736390 Compliance monitoring fees 20,892 20,8926390 Social service coordinator 15,770 18,852 6390 Computer learning center expenses 7,067 6,948 6390 Seminars and training 2,417 3,1756390 Miscellaneous administrative 11,893 8,4976263T Total administrative expenses $ 299,658 $ 285,249

Utilities6450 Electricity $ 11,268 $ 9,2546451 Water 90,726 76,1736452 Gas 47,377 56,5466453 Sewer 85,440 50,9456400T Total utilities $ 234,811 $ 192,918

Operating and maintenance6510 Janitorial and cleaning payroll $ 31,289 $ 29,3236515 Janitorial and cleaning supplies 1,131 1,4546520 Janitorial and cleaning contract 4,160 1,5356520 Exterminating contracts 15,186 10,2096525 Trash removal 67,633 65,8176530 Security contract 29,681 20,8796515 Grounds supplies - 1506520 Grounds contracts 39,390 53,6606510 Repairs payroll 108,871 93,7516521 Maintenance rent free unit 16,224 16,2246515 Repairs materials 20,896 25,1866520 Repairs contract 111,800 55,8546520 Decorating contracts 26,435 5,4006515 Decorating supplies 22,211 22,1846590 Cable TV 508 425 6590 Miscellaneous operating and maintenance 7,650 13,7686500T Total operating and maintenance $ 503,065 $ 415,819

18

DON AVANTE ASSOCIATES II, L.P. SUPPLEMENTARY INFORMATION

December 31, 2013 and 2012

SCHEDULES OF OPERATING EXPENSES (Continued)

2013 2012Taxes and insurance

6710 Real estate taxes $ 8,706 $ 8,4196711 Payroll taxes 18,764 18,9966720 Property and liability insurance 40,602 33,7046722 Workmen's compensation 13,761 8,8616723 Health insurance and other employee benefits 46,402 46,8556790 Miscellaneous taxes and licenses 861 1,0436790 Directors and officers insurance 199 1616700T Total taxes and insurance $ 129,295 $ 118,039

Financial expenses6820 Interest expense on mortgage $ 361,272 $ 366,7386830 Interest expense on deferred mortgages 141,673 141,6736850 Mortgage insurance premium 33,253 31,5296890 Bond administrative fees 8,591 8,591 6800T Total financial expenses $ 544,789 $ 548,531

SCHEDULES OF OTHER PAYMENTS Mortgage principal payments $ 97,263 $ 91,824 Mortgage interest payments 361,740 367,179 Replacement reserve deposits 43,824 43,453

Total other payments $ 502,827 $ 502,456

STATEMENT OF ACTIVITIES, PART II

Total principal payments required under the mortgage, even if payments under aWorkout Agreement are more or less than those required under the mortgage $ 97,263

Replacement reserve deposits required, even if payments may be temporarilysuspended or waived $ 33,648

Replacement reserve and residual receipt releases which are included as expense items on the Statement of Activities $ 43,176

19

DON AVANTE ASSOCIATES II, L.P. SUPPLEMENTARY INFORMATION

December 31, 2013 and 2012

REPLACEMENT RESERVE In accordance with the Partnership Agreement, City of Morgan Hill and TRI Capital Corporation loan agreements, a

replacement reserve account is established and funded on a monthly basis. The TRI Loan Agreement and HUD Regulatory Agreement require an annual funding of $33,648. The City of Morgan Hill loan agreement and Partnership Agreement require deposits of $28,000 increasing at 3.5% per year, $43,793 for 2013. Accordingly, restricted cash is held to be used for replacement property as follows:

In accordance with the Partnership Agreement, an operating reserve account has been established and funded in the initial amount of $112,000. Annual deposits are not required. Funds are to be used for operating deficits. Accordingly, restricted cash is held as follows:

DON AVANTE ASSOCIATES II, L.P. SUPPLEMENTARY INFORMATION

December 31, 2013 and 2012

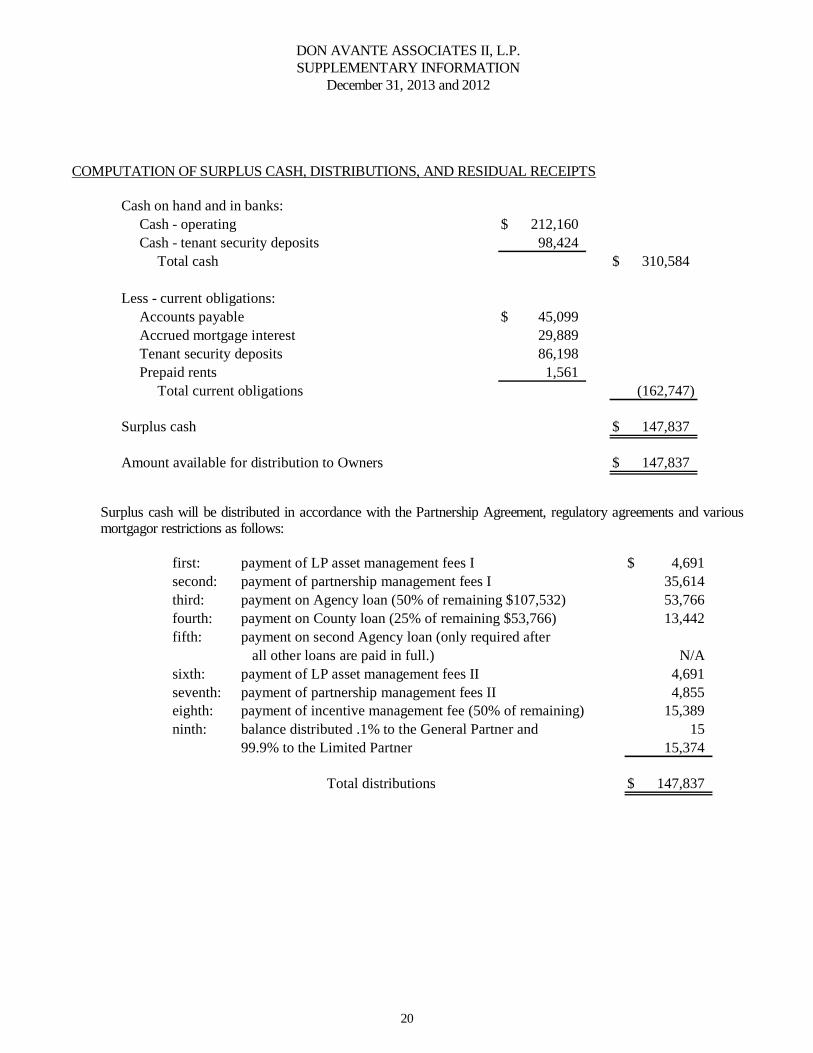

COMPUTATION OF SURPLUS CASH, DISTRIBUTIONS, AND RESIDUAL RECEIPTS

Cash on hand and in banks:Cash - operating $ 212,160 Cash - tenant security deposits 98,424

Total cash $ 310,584

Less - current obligations:Accounts payable $ 45,099 Accrued mortgage interest 29,889 Tenant security deposits 86,198 Prepaid rents 1,561

Total current obligations (162,747)

Surplus cash $ 147,837

Amount available for distribution to Owners $ 147,837

Surplus cash will be distributed in accordance with the Partnership Agreement, regulatory agreements and various

mortgagor restrictions as follows:

first: payment of LP asset management fees I $ 4,691 second: payment of partnership management fees I 35,614 third: payment on Agency loan (50% of remaining $107,532) 53,766 fourth: payment on County loan (25% of remaining $53,766) 13,442 fifth: payment on second Agency loan (only required after

all other loans are paid in full.) N/Asixth: payment of LP asset management fees II 4,691 seventh: payment of partnership management fees II 4,855 eighth: payment of incentive management fee (50% of remaining) 15,389 ninth: balance distributed .1% to the General Partner and 15

99.9% to the Limited Partner 15,374

Total distributions $ 147,837

21

BOWERS, NARASKY & DALEY, LLP Certified Public Accountants 1024 Country Club Drive, Moraga, California 94556 (925) 376-2195

INDEPENDENT AUDITOR’S REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN

ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS To the Partners Don Avante Associates II, L.P. A California Limited Partnership We have audited, in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States, the financial statements of Don Avante Associates II, L.P., a California Limited Partnership, which comprise the balance sheet as of December 31, 2013, and the related statements of operations, changes in partners' deficit, and cash flows for the year then ended, and the related notes to the financial statements and have issued our report thereon dated March 13, 2014. Internal Control Over Financial Reporting In planning and performing our audit of the financial statements, we considered Don Avante Associates II, L.P.’s internal control over financial reporting (internal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinion on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of Don Avante Associates II, L.P.’s internal control. Accordingly, we do not express an opinion on the effectiveness of Don Avante Associates II, L.P.’s internal control. A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct misstatements on a timely basis. A material weakness is a deficiency, or combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of Don Avante Associates II, L.P.’s financial statements will not be prevented, or detected and corrected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance. Our consideration of internal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant deficiencies. Given these limitations, during our audit we did not identify any deficiencies in internal control that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified. Compliance and Other Matters As part of obtaining reasonable assurance about whether Don Avante Associates II, L.P.’s financial statements are free of material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts and grant agreements, noncompliance with which could have a material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit and, accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance that are required to be reported under Government Auditing Standards.

22

INDEPENDENT AUDITOR’S REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON

COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS (Continued)

Purpose of this Report The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the results of that testing, and not to provide an opinion on the effectiveness of Don Avante Associates II, L.P.’s internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering Don Avante Associates II, L.P.’s internal control and on compliance. Accordingly, this communication is not suitable for any other purpose.

Moraga, California March 13, 2014

23

BOWERS, NARASKY & DALEY, LLP Certified Public Accountants

1024 Country Club Drive, Moraga, California 94556 (925) 376-2195

INDEPENDENT AUDITOR’S REPORT ON COMPLIANCE FOR EACH MAJOR HUD PROGRAM AND ON INTERNAL CONTROL OVER COMPLIANCE REQUIRED BY THE CONSOLIDATED AUDIT GUIDE FOR

AUDITS OF HUD PROGRAMS

To the Partners Don Avante Associates II, L.P. A California Limited Partnership Report on Compliance for Each Major HUD Program We have audited Don Avante Associates II, L.P.’s compliance with the compliance requirements described in the Consolidated Audit Guide for Audits of HUD Programs (the Guide), that could have a direct and material effect on each of Don Avante Associates II, L.P.’s major U.S. Department of Housing and Urban Development (HUD) programs for the year ended December 31, 2013. Don Avante Associates II, L.P.’s major HUD program is mortgage insurance under section 221(d)(4). Management’s Responsibility Management is responsible for compliance with the requirements of laws, regulations, contracts and grants applicable to its HUD programs. Auditor’s Responsibility Our responsibility is to express an opinion on compliance for each of Don Avante Associates II, L.P.’s major HUD programs based on our audit of the compliance requirements referred to above. We conducted our audit of compliance in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; and the Guide. Those standards and the Guide require that we plan and perform the audit to obtain reasonable assurance about whether noncompliance with the compliance requirements referred to above that could have a direct and material effect on a major HUD program occurred. An audit includes examining, on a test basis, evidence about the Don Avante Associates II, L.P.’s compliance with those requirements and performing such other procedures as we considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinion on compliance for each major HUD program. However, our audit does not provide a legal determination of Don Avante Associates II, L.P.’s compliance. Opinion on Each Major HUD Program In our opinion, Don Avante Associates II, L.P. complied, in all material respects, with the compliance requirements referred to above that could have a direct and material effect on each of its major HUD programs for the year ended December 31, 2013.

24

INDEPENDENT AUDITOR’S REPORT ON COMPLIANCE FOR EACH MAJOR HUD PROGRAM AND ON INTERNAL CONTROL OVER COMPLIANCE REQUIRED BY THE CONSOLIDATED AUDIT GUIDE FOR

AUDITS OF HUD PROGRAMS (Continued) Report on Internal Control Over Compliance Management of Don Avante Associates II, L.P. is responsible for establishing and maintaining effective internal control over compliance with the specific compliance requirements referred to above. In planning and performing our audit of compliance, we considered Don Avante Associates II, L.P.’s internal control over compliance with the requirements that could have a direct and material effect on each major HUD program to determine the auditing procedures that are appropriate in the circumstances for the purpose of expressing our opinion on compliance for each major HUD program and to test and report on internal control over compliance in accordance with the Guide, but not for the purpose of expressing an opinion on the effectiveness of internal control over compliance. Accordingly, we do not express an opinion on the effectiveness of Don Avante Associates II, L.P.’s internal control over compliance. A deficiency in internal control over compliance exists when the design or operation of a control over compliance does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, noncompliance with a compliance requirement of a HUD program on a timely basis. A material weakness in internal control over compliance is a deficiency, or combination of deficiencies, in internal control over compliance, such that there is a reasonable possibility that material noncompliance with a compliance requirement of a HUD program will not be prevented, or detected and corrected, on a timely basis. A significant deficiency in internal control over compliance is a deficiency, or combination of deficiencies, in internal control over compliance with compliance requirement of a HUD program that is less severe than a material weakness in internal control over compliance, yet important enough to merit attention by those charged with governance. Our consideration of internal control over compliance was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control over compliance that might be material weaknesses or significant deficiencies. We did not identify any deficiencies in internal control over compliance that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified. The purpose of this report on internal control over compliance is solely to describe the scope of our testing of internal control over compliance and the results of our testing based on the requirements of the Guide. Accordingly, this report is not suitable for any other purpose.

Moraga, California March 13, 2014

25

DON AVANTE ASSOCIATES II, L.P. SCHEDULE OF FINDINGS, QUESTIONED COSTS,

AND RECOMMENDATIONS December 31, 2013

Our audit disclosed no findings that are required to be reported herein under the HUD Consolidated Audit Guide.

26

DON AVANTE ASSOCIATES II, L.P. SCHEDULE OF THE STATUS OF PRIOR AUDIT FINDINGS,

QUESTIONED COSTS, AND RECOMMENDATIONS December 31, 2013

1. Findings from audit report dated March 5, 2013, for the period ended December 31, 2012, issued by Bowers, Narasky & Daley, LLP.

There were findings from the prior audit to report.

2. Findings from audit, attestation, or other studies performed by HUD, another Federal Agency, or a contract administrator during the year ended December 31, 2013.

There were no reports issued by HUD OIG or other Federal agencies or contract administrators during the year ended December 31, 2013.

3. Deficiencies listed in letters or reports issued by HUD management as a result of reviews of the entity’s activities that relate to the audit objectives during the year ended December 31, 2013.

There were no letters or reports issued by HUD management during the year ended December 31, 2013.

27

DON AVANTE ASSOCIATES II, L.P. CERTIFICATIONS OF PARTNERS AND MANAGEMENT AGENT

December 31, 2013

CERTIFICATION OF PARTNERS

We, as partners of Don Avante Associates II, L.P., hereby certify that we have examined the accompanying financial statements and supplemental data of Don Avante Associates II, L.P. and to the best of our knowledge and belief, these financial statements and data are complete and accurate. Name Title Date Name Title Date DON AVANTE ASSOCIATES II, L.P. Employer ID No. 94-3310728

CERTIFICATION OF MANAGEMENT AGENT

We hereby certify that we have examined the accompanying financial statements and supplemental data of Don Avante Associates II, L.P. and, to the best of our knowledge and belief, the same is complete and accurate.

Name Title Date EAH, INC. Employer ID No. 94-1699153