79

A STUDY ON LOANS AND ADVANCES CHAPTER-I INTRODUCTION P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 1

| Date post: | 14-Apr-2017 |

| Category: |

Education |

| Upload: | vinay-kulkarni |

| View: | 177 times |

| Download: | 0 times |

A STUDY ON LOANS AND ADVANCES

CHAPTER-IINTRODUCTION

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 1

A STUDY ON LOANS AND ADVANCES

1.1 INTRODUCTION TO LOANS AND ADVANCES

Loans and advances are the most important aspect of any banking organization.

Loan is a type of debt. Like all debt instruments, a loan entails the Redistribution of

financial assets over time. The borrower initially receives an amount of money from the

lender, which they pay back, usually but not always in regular installment, to the lender.

This service is generally provided at a cost, referred to as interest on the debt .The Sum of

borrowed Money (Principal) that is generally repaid with interest. Loan– to –Value –Ratio

the relation between the amount of the mortgage loan and the appraised Value of the

property expressed as a percentage. Lock lenders guarantee that the mortgages are quoted

will be good for a specific Number of days from day of application. Money Margin, the

amount of a Lender adds to the index on an adjustable ratio mortgage to establish the

adjusted interest rate. ADVANCE is a term that describes a secured loan Made to a

member. Advances are offered at fixed or floating rates with specific Maturities or with

embedded options for early redemption. There are different types of loan offered by a bank.

Different loans fetch a different rate of interest and have different securities against them.

Consumer loans

Housing loans

Car loans

Education loans

Against mortgage

1.2 BACK GROUND OF THE STUDY:

The history of loans began… it’s likely that people have been practicing lending and

borrowing for as long there has been a concept of ownership. The history of loans and

advances can be documented at least several thousand Years back forms of lending were

evident in ancient Greek and Roman times of course… it is, however important to realize

that lending started much earlier than Many people would imagine and has its origin in

much older times.

1.3 OBJECTIVES OF THE STUDY:

To assess the different interest rate on the different loans schemes provided by the

bank.

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 2

A STUDY ON LOANS AND ADVANCES

To study different loans provided by the bank.

To study the growth of the loans and Advances

To study the Financial performance of the bank

To know the procedures followed by the society while issuing loans and advances.

To know the customer opinion with regard loans and advances of the society.

1.4 SCOPE OF THE STUDY:

To understand the concept of Loans and advances

This study is limited to only Beereshwar Co-operative Society, Haveri

Study covers last three years performance of the bank

1.5 RESEARCH METHODOLOGY:

Type of Research - Descriptive research is used in this study in order to identify the

lending practices of bank and determining customer’s level of satisfaction. The method used

was questionnaire and interview of the experienced loan officers, Collection of data:

1. Primary Data

a) Observation Method

b) Interview Method

2. Secondary Data

a) Annual reports of the bank

b) Books

c) Internet

1.6 LIMITATIONS OF THE STUDY:

This research was limited because of the fact that the major source of data is a form

the annual reports of the Bank, which was subject to accounting policies and practices

followed by the Bank. The major limitations are:

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 3

A STUDY ON LOANS AND ADVANCES

The study was limited to only one of the important activities of the organization

i.e. Loans and Advances

Due to strict confidently policy of the Bank the accounts departments provided

only screened information.

Accuracy of the data provided cannot be guaranteed which does not give a clear

idea about the actual functioning of the bank.

Study covers only last three years performance of the bank

Due to busy schedule of advance manager of the Banks. “Financial statements

obtain secondary data”.

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 4

A STUDY ON LOANS AND ADVANCES

CHAPTER-IICOMPANY PROFILE

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 5

A STUDY ON LOANS AND ADVANCES

2.1 INTRODUCTION TO CO-OPERATIVE BANKING

DEFINATION:

“A Co-operative bank, as its name indicates is an institution consisting of a number

of individuals who join together to pool their surplus savings for the purpose of eliminating

the profits of the bankers or money lenders with a view to distributing the same amongst the

depositors and borrowers.”

The Co-operative Banks Act, of 2007 (the Act) defines a co-operative bank as a co-

operative registered as a co-operative bank in terms of the Act whose members –

1. Are of similar occupation or profession or who are employed by a common

employer or who are employed within the same business district; or

2. Have common membership in an association or organisation, including a business,

religious, social, co-operative, labour or educational group; or

3. Reside within the same defined community or geographical area.

2.2 CHARACTERISTICS OF CO-OPERATIVE SOCIETY:

A co-operative society is a special type of business organization different from other

forms of organization,

1. Open membership: The membership of a Co-operative Society is open to all those who

have a common interest. A minimum of ten members are required to form a co-operative

society. The Co–operative society Act does not specify the maximum number of members

for any co-operative society. However, after the formation of the society, the member may

specify the maximum number of members.

2. Voluntary Association: Members join the co-operative society voluntarily that is by

choice. A member can join the society as and when he likes, continue for as long as he likes

and leave the society at will.

3. State control: To protect the interest of members, co-operative societies are placed under

state control. While getting registered, a society has to submit details about the members

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 6

A STUDY ON LOANS AND ADVANCES

and the business it is to undertake. It has to maintain books of accounts, which are to be

audited by government auditors.

4. Sources of Finance: In a co-operative society capital is contributed by all the members.

However, it can easily raise loans and secure grants from government after its registration.

5. Democratic Management: Co-operative societies are managed on democratic lines. The

society is managed by a group known as “Board of Directors”. The members of the board of

directors are the elected representatives of the society. Each member has a single vote,

irrespective of the number of shares held. For example, In a village credit society the small

farmer having one share has equal voting right as that of a landlord having 20 shares.

6. Service motive: Co-operatives are not formed to maximize profit like other forms of

business organization. The main purpose of a Co-operative Society is to provide service to

its members. For example, In a Consumer Co-operative Store, goods are sold to its

members at a reasonable price by retaining a small margin of profit. It also provides better

quality goods to its members and the general public.

7. Separate Legal Entity: A Co-operative Society is registered under the Co-operative

Societies Act. After registration a society becomes a separate legal entity, with limited

liability of its members. Death, insolvency or lunacy of a member does not affect the

existence of a society. It can enter into agreements with others and can purchase or sell

properties in its own name.

8. Distribution of Surplus: Every co-operative society in addition to providing services to

its Members also generates some profit while conducting business. Profits are not earned at

the cost of its members. Profit generated is distributed to its members not on the basis of the

shares held by the members (like the company form of business), but on the basis of

members participation in the business of the society. For example, In a consumer co-

operative store only a small part of the profit is distributed to members as dividend on their

shares; a major part of the profit is paid as purchase bonus to members on the basis of goods

purchased by each member from the society.

9. Self-help through mutual co-operation: Co-operative Societies thrive on the principle

of mutual help. They are the organizations of financially weaker sections of society. Co-

operative Societies convert the weakness of members into strength by adopting the principle

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 7

A STUDY ON LOANS AND ADVANCES

of self-help through mutual co-operation. It is only by working jointly on the principle of

“Each for all and all for each”, the members can fight exploitation and secure a place in

society.

2.3 PRINCIPLES OF CO-OPERATIVE SECTOR:

1. LEGAL STATUS:

A co-operative Society is a body corporate registered under the applicable state Act

with perpetual succession having a common seal. It can acquire hold and dispose of

properties, enter into contracts and it can sue and it can be sued.

2. VOLUNTARY ASSOCIATION:

Co-operative Society is essentially an organization or an association of persons who

have come together for the common purpose of economic development or for mutual help.

3. SELF HELP AND MUTUAL HELP:

The Co-operative Societies office bearers/executive committee is elected as per

democratic election procedure. The Co-operative Society function under the principle of

self help and mutual help which means each will help for themselves and all will help

others.

4. DEMOCRATIC CONTROLS:

The Control of Co-operative enterprise is not in the hand of capitalists can corner the

share capital and control the interest in any undertaking which would be a private

undertaking.

5. EQUALITY:

In co-operative Sector, the principle of “One man one Vote” Is provided in the

statute so as to ensure that the capital does not dominate the administration of co-operative

Society.

6. OPEN MEMBERSHIP:

Any person can apply for the membership of the Society without any discrimination.

The membership is open for all.

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 8

A STUDY ON LOANS AND ADVANCES

7. SOCIAL APPROACH / NO PROFIT MOTIVE:

As the Society is working on democratic principle and the office bearers of the

Society will be functioning like trustees for the better management of the society and there

is no separate benefit to the executive committee members. Service is the main motto and

the profit is not the main concern in co-operative societies.

8. PROFITS AND RETURNS TO THE MEMBERS:

Co-operative Society is an association of members and certain percentage profits

earned by the society, as decided in the meeting of the General body will be distributed in

the form of dividend to the members.

9. LIMITED INTEREST ON SHARES:

Irrespective of the shareholding, each member has only one vote in the decision-

making in the General body meeting or at the time of election of the committee for

management. The shares are not traded in the stock exchange. The State Co-op. Act also

prescribes the maximum amount, which member can hold as a share capital in any society.

Under M.C.S. Act, 1960 as per Section 28 other than Government or other societies shall

not hold more than 1/5 of the total capital or interest in shares or exceeding Rs. 20,000/-

which the State Government power to change by way of notification.

10. PERSONAL PARTICIPATION:

The shareholders have to personally attend the meeting or for voting. They are not

allowed to appoint proxies for attending the general body or for voting in the resolution to

be passed.

2.4 ORGANIZATION OF CO-OPERATIVE BANKS

Co-operative banks may be organized in two ways

A. On the bases of the principals of Raiffesen and

B. On the bases of principals of schedule delittze.

It is important to remember that Raiffesen and Schulze Delittze were the pioneers of

banks movement in Germany.

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 9

A STUDY ON LOANS AND ADVANCES

A. RAIFFESISEN BANK

In the organization of banks in the rural areas the principals of Raiffesen are

adopted. Therefore they are called Raiffesen bank. They are organized on the following

principals.

Ten or more person can form such a bank.

Shares are not issued but capital is obtained by barrowings from the members on

their join responsibility.

The liability of the members is unlimited.

Members belong to the same village.

There is no entrance fee.

Loans are granted on personal security only for productive purpose.

B. SCHULZE DELITTZE BANK

The banking organized in urban areas are based on the principals of Hulze delittze

and hence. They are called schulze delittze bank.

The following are the principals…..

Membership is very large.

Office bearers are paid salaries.

Dividends are paid to the members on their paid-up share capital.

General banking business is conduct by the bank.

Entrance fee is charged.

Membership is open only to those who earn an income.

The aim of such a bank is more materialistic than human Italian.

The liability of the members is limited.

2.5 IMPORTANCE OF CO-OPERATIVE BANKINGCo-operative bank forms an integral part of banking system in India. This bank

operates mainly for the benefit of rural area, particularly the agricultural sector. Co-

operative bank mobilize deposits and supply agricultural and rural credit with the wider

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 10

A STUDY ON LOANS AND ADVANCES

outreach. They are the main source for the institutional credit to farmers. They are chiefly

responsible for breaking the monopoly of moneylenders in providing credit to agriculturists.

Co-operative bank has also been an important instrument for various development schemes,

particularly subsidy-based programmes for the poor. Co-operative banks operate for non-

agricultural sector also but their role is small.

Though much smaller as compared to scheduled commercial banks, co-operative

banks constitute an important segment of the Indian banking system. They have extensive

branch network and reach out to people in remote areas. They have traditionally played an

important role in creating banking habits among the lower and middle income groups and in

strengthening the rural credit delivery system.

2.6 CLASSIFICATION OF CREDIT CO OPERATIVE SOCIETY:

CLASSIFICATION OF CO-PERATIVE BANKS:

The Co-operative banking structure in India comprises of:

1. Urban Co-operative Banks

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 11

A STUDY ON LOANS AND ADVANCES

2. Rural Co-operatives

Some co-operative banks are scheduled banks, while others are nonscheduled banks.

For instance, State Co-operative banks and some Urban Co-operative banks are scheduled

banks but other co-operative banks are non-scheduled banks.

Scheduled banks are those banks which have been included in the second schedule of

the Reserve bank of India act of 1934.

The banks included in this schedule list should fulfill two conditions :

1. The paid capital and collected funds of bank should not be less than Rs. 5 lakh.

2. Any activity of the bank will not adversely affect the interests of depositors.

Every Scheduled bank enjoys the following facilities.:

1. Such bank becomes eligible for debts/loans on bank rate from the RBI

2. Such bank automatically acquire the membership of clearing house.

1. Urban Co-operative Banks:

Urban Co-operative Banks is also referred as Primary Co-operative banks by the

Reserve Bank of India. Among the non-agricultural credit societies urban co-operative

banks occupy an important place. This bank is started in India with the object of catering to

the banking and credit requirements of the urban middle classes.

The RBI defines Urban Co-operative banks as “small sized co-operatively organized

banking units which operate in metropolitan, urban and semi-urban centers to cater mainly

to the needs of small borrowers, viz. owners of small scale industrial units, retail traders,

professional and salaries classes.”

Urban Co-operative banks mobilize savings from the middle and lower income

groups and purvey credit to small borrowers, including weaker sections of the society.

These banks organize on a limited liability basis, generally extend their area of operation

over a town. The main functions of these banks are to promote thrift by attracting deposits

from members and non-members and to advance loans to the members. It is registered

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 12

A STUDY ON LOANS AND ADVANCES

under Co-operatives Societies Act of the respective state Governments. Prior to 1966,

Urban Co-operative banks were exclusively under the purview of State Government. From

March 1, 1966 certain provisions of Banking Regulation Act have been made applicable to

these banks. Consequently, the RBI became the regulatory an supervisory authority of

Urban Co-operative Banks for their related operations. Managerial aspects of such banks

continue to remain with State Governments under the respective Co-operative Societies Act.

These banks with multi-presence are regulated by the Central Governments and registered

under Multi-State Co-operative Societies Act. The RBI extends refinance to Urban Co-

operative Banks at bank ate against their advances to tiny and cottage industrial units. These

banks grants sizeable loans and advances under priority sector for lending to small business

enterprises, retail trade, road and water transport operators and professional and self-

employed persons. Urban Co-operative banks are mostly located in towns and cities and

cater to the credit requirement of the urban clientele.

The objectives and functions of the Urban Co-operative banks:

Primarily, to raise funds for lending money to its members.

To attract deposits from members as well as non-members.

To encourage thrift, self-help and mutual aid among members.

To draw, make, accept, discount, buy, sell, collect and deal in bills of exchange,

drafts, certificates and other securities.

To provide safe-deposit vaults.

Area of Operation :

The area of operation of these banks are usually restricted by its byelaws to a

municipal area or a town. In some occasions it exceeds this limit. The study group on Credit

Co-operatives in Non-Agricultural Sectors has recommended that normally, it would be

advisable for an urban cooperative bank to restrict its area of operation to the municipality

or the taluka town where it operates.

2. Rural Co-operatives:

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 13

A STUDY ON LOANS AND ADVANCES

Rural Cooperative Banking plays an important role in meeting the growing credit

needs of rural population of India. It provides institutional credit to the agricultural and rural

sector. The inadequacy of rural credit engaged the attention of RBI and Government

throughout the 1950s and 1960s. One important feature of providing agriculture credit in

India has been the existence of a widespread network of rural financial institutions. The

rural credit structure consists of many types of financial institutions as large scale branch

expansion was undertaken to create a strong institution based in rural area. It has served as

an important instrument of credit delivery in rural and agricultural areas. The separate

structure of rural Co-operative sector for long-term and short-term loans has enabled these

institutions to develop a specialized institution for rural credit delivery. The volume of

credit flowing through these institution has increased. The Rural Co-operative structure has

traditionally been bifurcated into two parallel wings, i.e.

I. Short-term Rural Co-operatives,

II. Long-term Rural Co-operatives.

There is a larger network of co-operative banks in the rural sector, consisting of 29

State Co-operative Banks and 367 District Central Cooperative Banks, with 13,025

branches. In addition, there are 92,000 Primary Agricultural Co-operative Credit Societies

19 State Land Development Banks and 745 Primary Land Development Banks, along with

1,847 branches, which are not strictly banks as they are not covered under the Banking

Regulation Act, 1949. The RBI Governor's proposals should therefore, encompass the entire

Co-operative banking system.

I. SHORT-TERM RURAL CO-OPERATIVES :

The short-term rural co-operatives provide crop and other working capital loans to

farmers and rural artisans primarily for short-term purpose.

These institutions have federal three-tier structure.

At the Apex of the system is a State Co-operative bank in each state.

At the middle (or district) level, there are Central Co-operative Banks also known as

District Co-operative banks.

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 14

A STUDY ON LOANS AND ADVANCES

At the lowest (or village) level, are the Primary Agricultural Credit Societies.

i. State Co-operative Banks:

State Co-operative Banks are the apex of the three-tier Co-operative structure

dispensing mainly short/medium term credit. It is the principal society in a State which is

registered or deemed to be registered under the Government Societies Act, 1912, or any

other law for the time being in force in India relating to co-operative societies and the

primary object of which is the financing of the other societies in the State which are

registered or deemed to be registered. The State Co-operative Banks receive current and

fixed deposits from its constituent banks as well as savings, current and fixed deposits from

the general public and from local boards, other local authorities, etc. Further, they receive

loans from the RBI and NABARD. NABARD is the supervisory authority for State Co-

operative Banks. The state government contributes the certain portion of their working

capital. The principal function of State Co-operative Banks is to assist the Central Co-

operative Banks and to balance excesses and deficiencies in the resources of Central Co-

operative Banks. It also act as the “balancing centre” for Central Co-operative Banks in the

sense that surplus fund of some of these banks are made available to other needy banks. It

also serves the link between RBI and the Central Co-operative Banks and Primary

Agriculture Credit Societies. But the connection between the State Co-operative Banks and

Primary Co-operative Societies is not direct. The Central Co-operative Banks are acting as

intermediaries between the State Co-operative Banks and Primary societies.

ii. Central Co-operative Banks:

Central Co-operative Banks form the middle tier of Cooperative credit institutions.

These are the independent units in as much as the State Co-operative Banks have control to

control or supervise their affairs. They are of two kinds i.e. ‘pure’ and ‘mixed’. Those banks

are the membership of which is confined to co-operative organizations only are included in

‘pure’ type, while those banks the membership of which is open to co-operative

organizations as well as to the individuals are included in ‘mixed’ type. The pure type of

Central Banks can be seen in Kerala, Bombay, Orissa, etc., while the mixed type can be

seen in Andhra Pradesh, Assam, Tamil Nadu, etc. The pure type of banks is based on strict

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 15

A STUDY ON LOANS AND ADVANCES

cooperative principles. However, the mixed type has an advantage over the pure type in so

far as they can draw their funds from the non-agricultural sector too.

The Central Co-operative Banks draw their funds from share capital, deposits, loans

from the State C-operative Banks and where State Banks do not exist from the RBI,

NABARD and commercial banks. NABARD is the supervisory authority for Central Co-

operative Banks. Deposits constitute the major component of sources of funds, followed by

borrowings. The main function of Central Co-operative Banks is to finance the primary

credit societies. In addition they carry on Commercial banking activities like acceptance of

deposits, granting of loans and advances on the security of first class guilt-edged securities,

fixed deposit receipts, gold, bullion, goods and documents of title to goods, collection of

bills, cheques, etc., safe custody of valuables and agency services. They are expected to

attract deposits from the general public. They also act as ‘balancing centres’, making

available access funds of one primary to another which is in need of them.

The central co-operative banks are located at the district headquarters or some

prominent town of the district. These banks have a few private individuals also who provide

both finance and management. The central cooperative banks have three sources of funds,

Their own share capital and reserves

Deposits from the public and

Loans from the state co-operative banks

iii. Primary Agriculture Credit Societies :

Primary Agricultural Credit Societies is the foundation of the co-operative credit

system on which the superstructure of the shortterm co-operative credit system rests. It

deals directly with individual farmers, provide short and medium term credit, supply

agricultural inputs, distribute consume articles and also arrange for the marketing of

products of its members through a co-operative marketing societies. These societies form

the basic unit of co-operative credit system in India. These voluntary societies based on

principle of one man one vote has posed challenge to exploitative practices of the village

moneylenders. The farmers and other small-time borrowers come in direct contact with

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 16

A STUDY ON LOANS AND ADVANCES

these societies. The success of the co-operative credit movement depend largely on the

strength of these village level societies.

The major objective of Primary agricultural Credit Societies is to serve the need of

weaker sections of these society. For this purpose, the people with limited means,

particularly with schedules castes and scheduled tribes, are encouraged to become members

of these societies. So, they must function effectively as well-managed and multi-purpose

institutions mobilizing the savings of the rural people and providing the package of services

including credit, supply of agricultural inputs and implements, consumer goods, marketing

services and technical guidance with focus on weaker sections. Government has promoted

multi-purpose societies in tribal areas for the benefit of people living there.

II. Long-term Rural Co-operatives :

The long-term rural co-operative provide typically medium and long-term loans for

making investments in agriculture, rural industries and in the recent period, housing.

Generally, these co-operatives have two tiers, i.e. State Co-operative Agriculture and

Development Banks (SCARBDs) at the state level and Primary Co-operative Agriculture

and Rural Development Banks (PCARDBs) at the taluka or tehsil level. However, some

States have a unitary structure with the state level banks operating through their own

branches.

i. State Co-operative Agriculture and Development Banks (SCARBDs):

State Co-operative Agriculture and Development Banks constitute the upper-tier of

long term co-operative credit structure. Though long term credit co-operatives have been

allowed to access public deposits under certain conditions, such deposits constitute a

relatively small proportion of their total liabilities. They are mostly dependent on

borrowings for on-lending.

The main objective of the Co-operative State Agriculture and Rural Development

bank is to finance primary agriculture and rural development banks. The bank undertakes

the following functions to achieve the above objectives:-

(a) Floatation of Debentures;

(b) Receiving Deposits;

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 17

A STUDY ON LOANS AND ADVANCES

(c) Grant of loans to primary co-operative agriculture and rural development banks for

purposes approved by the National Bank for Agricultural and Rural Development

and Registrar of Co-operative Societies;

(d) To function as the agent of any co-operative bank subject to such conditions as the

Registrar may specify;

(e) To develop, assist and co-ordinate the work of affiliated primary co-operative

agriculture and rural development banks.

The bank issues long term and medium term loans towards agricultural and allied

activities like construction of godowns, cattle shed, farm house, purchase of lands etc., and

for minor irrigation purposes like construction of new wells, deepening of existing wells

etc., In addition, long term loans are also sanctioned for animal husbandry, fisheries,

plantation, farm mechanization, non-farm sector and other non-minor irrigation schemes.

ii. Primary Co-operative Agriculture and Rural Development Banks (PCARDBs):

Primary Co-operative Agriculture and Rural Development Banks are the lowest

layer of long term credit co-operatives. It is primarily dependent on the borrowings for their

lending business.

They provide credit for developmental purposes like minor irrigation, cultivation of

plantation crops and for diversified purposes like poultry, dairying and sericulture on

schematic basis. They get requisite financial assistance from the Co-operative State

Agriculture and Rural Development Bank.

In order to widen their scope of lending to compete with other financial agencies,

the primary co-operative agriculture and rural development banks have been permitted to

finance artisans, craftmen and small scale entrepreneurs. They have also been permitted to

issue loans to small road transport operators in rural areas for purchase of goods carriers and

passenger vehicles.

As a result, during 2007-08, the Primary Co-operative Agriculture and Rural

Development Banks have again started lending for the Non-Farm Sector including Jewel

Loans.

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 18

A STUDY ON LOANS AND ADVANCES

2.7 LIMITATIONS OF CO–OPERATIVE SOCIETY:The co-operative form of business organization also suffers from various limitations.

1. Limited Capital: The amount of capital that a co-operative society can raise from its

member is very limited because the membership is generally confined to a particular section

of the society. Again due to low rate of return the members do not invest more capital.

Government’s assistance is often inadequate for most of the co-operative societies.

2. Problems in Management: Generally it is seen that co-operative societies do not

function efficiently due to lack of managerial talent. The members or their elected

representatives are not experienced enough to manage the society. Again, because of limited

capital they are not able to get the benefits of professional management.

3. Lack of Motivation: Every co-operative society is formed to render service to its

members rather than to earn profit. This does not provide enough motivation to the

members to put in their best effort and manage the society efficiently.

4. Lack of Co-operation: The co-operative societies are formed with the idea of mutual co-

operation. But it is often seen that there is a lot of friction between the members because of

personality differences, ego clash, etc. The selfish attitude of members may sometimes

bring an end to the society.

5. Dependence on Government: The inadequacy of capital and various other limitations

make co-operative societies dependant on the government for support and patronage in

terms of grants, loans subsidies, etc. Due to this, the Government some time directly

interferes in the management of the society and also Audit their annual accounts.

2.8 Co-operative Movement In the world

The earliest co-operatives were set-up among the weavers, in other words workers in

cottage industries, who were the first and the hardest hit by the development of the

mercantile economy and the industrial revolution.

So the weavers, in order to gain access to the market in the tools of their trade or to

the market in foodstuffs set up the first co-operative in Scotland (Fenwick, 1761; Govan,

1777; Darvel, 1840), in France (Lyons, 1835), in England (Rockdale, 1844) and in Germany

(Chemnitz, 1845).

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 19

A STUDY ON LOANS AND ADVANCES

Though co-operation and mutual enterprise has been an essence of human-society

ever since it evolved, the real co-operative movement can be credited to the Rockdale

Pioneers who established a co-operative consumer store in North England. This store can be

called as the first in the co-operative consumer movement.

The "Rockdale Pioneers", made their first aim to establish co-operatives where the

members would not only be their own merchants but also their own producers and their own

employers.

Around this time the co-operative movement was more at an utilitarian level. The

concept though old, was just being implemented and was growing slowly. Many great

thinkers far sighted men and visionaries were applying their minds to find practical

solutions to the new problems and to work out better systems of social organization.

In France Charles Fourier (1722-1837) , a commercial clerk published in 1822 his

main work, a Treatise on Domestic Agricultural Association. This could be one of the first

works on co-operation. In France Saint-Simon (1760-1865) worked on various theories of

"associations". But it was Proudhon (1796-1865) who advocated mutual aid and "free

credit" for free access to the money market and Buchez (1796-1865) who championed the

idea of inalienable collective capital and workers production co-operative societies.

Schulze-Delitzsch (1808-1883) was the apostle of urban credit co-operatives and co-

operatives in handicrafts, while F.W.Raiffeisen (1818-1888) did the same for rural credit

Though all these visionaries had articulated the philosophy of co-operation it was

not until the World-War II that an Authoritative Commission was appointed by the

International Co-operative Alliance.

This Commission formulated or rather formalized the principles of co-

operation. They are : Voluntary and open membership

Democratic Management

Limited interest on capital

Patronage dividend in proportion of members' transactions

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 20

A STUDY ON LOANS AND ADVANCES

Education and Training and

Co - operation among co-operatives

There have been also other principles like the principles of political neutrality,

correct weight and measures, purity of goods and thrift which were also taken into

consideration.

These principles have been reformulated recently by the Manchester Congress in

1995. These principles are acknowledged by all over the world. The Cooperative principles

have been incorporated in Karnataka Souharda Sahakari Act, 1997 as a separate chapter.

2.9 Movement in INDIA

The origins of the co-operative banking movement in India can be traced to the close

of nineteenth century when, inspired by the success of the experiments related to the

cooperative movement in Britain and the co-operative credit movement in Germany, such

societies were set up in India.

Now, Co-operative movement is quite well established in India. The first legislation

on co-operation was passed in 1904. In 1914 the Maclagen committee envisaged a three tier

structure for co-operative banking viz. Primary Agricultural Credit Societies (PACs) at the

grass root level, Central Co-operative Banks at the district level and State Co-operative

Banks at state level or Apex Level.

In the beginning of 20th century availability of credit in India more particularly in

rural areas, was almost absent. Agricultural and related activities were starved of organised,

institutional credit. The rural folk had to depend entirely on the money lenders, who lent

often at usurious rates of interest.

The co-operative banks arrived in India in the beginning of 20th Century as an

official effort to create a new type of institution based on the principles of co-operative

organisation and management, suitable for problems peculiar to Indian conditions. These

banks were conceived as substitutes for money lenders, to provide timely and adequate

short-term and long-term institutional credit at reasonable rates of interest.

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 21

A STUDY ON LOANS AND ADVANCES

The Anyonya Co-operative Bank in India is considered to have been the first co-

operative bank in Asia which was formed nearly 100 years back in Baroda. It was

established in 1889 with the name Anyonya Sahayakari Mandali Co-operative Bank Limited, with a primary objective of providing an alternative to

exploitation by money lenders for Baroda's residents.

In the formative stage Co-operative Banks were Urban Co-operative Societies run

on community basis and their lending activities were restricted to meeting the credit

requirements of their members. The concept of Urban Co-operative Bank was first spelt out

by Mehta Bhansali Committee in 1939 which defined on Urban Co-operative Bank .

Provisions of Section 5 (CCV) of Banking Regulation Act, 1949 (as applicable to Co-

operative Societies) defined an Urban Co-operative Bank as a Primary Co-operative Bank

other than a Primary Co-operative Society were made applicable in 1966.

With gradual growth and also given philip with the economic boom, urban banking

sector received tremendous boost and started diversifying its credit portfolio. Besides giving

traditional lending activity meeting the credit requirements of their customers they started

catering to various sorts of customers viz. self-employed, small businessmen / industries,

house finance, consumer finance, personal finance etc

2.10 Movement in Karnataka

Karnataka has a special place in the Indian co-operative sector, as it is one of the

first states to have started the movement. We are proud to say that, the first agricultural

credit cooperative society in Karnataka started in a village called Kanaginahaala, Gadag

district, in 1905. In the same year, a consumer cooperative society also started in Bangalore.

Prior to unification of states present Karnataka was divided into various provinces

such as Hyderabad, Mumbai, Mysore, Madras etc. All provinces had their own Law relating

to co-operative Societies. They are

Madras Co-operative Societies Act, 1932

Madras Land Mortgage Act, 1934

Kodagu Co-operative Societies Act, 1936

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 22

A STUDY ON LOANS AND ADVANCES

Mysore Co-operative Societies Act, 1948

Hyderabad Co-operative Societies Act, 1952

Hyderabad Land Mortgage Act, 1949

After unification of states in 1956, The Mysore Co-operative Societies Act, 1959

was enacted which applies to whole Mysore State. It came into force from June 1, 1950.

Mysore State was renamed as Karnataka in 1973 and the Act was also renamed as

Karnataka State Co-operative Societies Act, 1959.

As on March 2004, Karnataka has 32,804 co-operative societies under which

27,261 are active Among these, 15,468 societies are profitable and 12,756 are under loss.

Around 9367 Milk co-operative societies, 301 urban cooperative banks and around 2000

credit cooperative societies are some of the sectors in Co-operative field which are

profitable in the state. Karnataka has 9,367 milk cooperatives, which are producing over 23

lakh liters of milk every day.

The state has over 4,000 Primary Agricultural societies and over 10.12lakh farmers

are benefited from these co-operatives. In Karnataka 100% villages are covered by co-

operative Societies.

And the success is evident. Almost 50 percent of the total sugar production in India

is contributed by sugar co-operatives and over 60 percent of the total fertilizer distribution

in the country is handled by the co-operatives. The consumer co-operatives are slowly

becoming the backbone of the public distribution system and the marketing co-operatives

are handling agricultural produce with an outstanding growth rate.

The National Co-operative Development Corporation (NCDC), a statutory body was

set up in 1963 by the Union ministry of Civil Supplies and Co-operation, to promote the co-

operative movement in India.

Further there is the Indian Farmers Fertilizer Co-operative LTD (IFFCO), which has

been successful in setting up an effective marketing network in most of the states for selling

modern farming technology instead of fertilizers alone. The operations of IFFCO are

handled through its more than 30,000 member co-operatives.

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 23

A STUDY ON LOANS AND ADVANCES

3.11 Co-operative movement in Haveri:

Haveri district is situated the North-Western parts of Karnataka state districts are

Uttar Kannada, Gadag, Bellary, Dharwad, Davanagri and Shimoga Districts. It is a plain

geographical area.

Haveri District consists of seven talukas namely Haveri, Ranebennur, Hirekerur,

Byadagi, Shiggavi, Savanur and Hangal in Haveri District. Co-operative movement started

intill with Registration of Handiganur Gram Seva Sahakari Sangh. Now 966 co-operative

societies are registered in the district. Out of these 892 co-operational societies are working

especially 388 milk co-operative societies are functioning well under profit.

These are 6,45,825 co-operative members enrolled in the district out of this 34,880

are Scheduled Caste; 54,673 are Scheduled Tribes and 52,991 are women Co-operatives.

Working capital of all these co-operative societies is Rs.787.68 taken major role in

economic activities in the district and 3850 employees are employed by these societies.

Milk co-operative societies have major oriole in economic activities and provided

employment to the rural folks last year, these societies produced Rs.3187.96 cores worth of

milk.

12 urban Co-operative banks are working in the district, out of this 10 urban bank

are working under good condition out of 1 Facts in the district. One TAPCMS i.e.

Hirekerur. TAPCMS is good working will all marketing activities. 88 non-agricultural co-

operative societies are working in good condition with working capital of Rs.64.84 crores.

7 PACRD banks are working in district. These banks have advanced Rs4043.53 Lakhs

against the target of Rs.1742.73 Lakhs in 2012-13 and 223 primary co-operative agricultural

societies are advanced Rs.321.84 Lakhs in 2012-13.

Co-operative Department also implemented Yashaswini Farmers Health Scheme i.e.

major social plan of Government of Karnataka. In this plan 62,095 members have enrolled

in the 2012-13. 11,182 members have benefitted in the scheme with worth of Rs.346.26

Lakhs.

2.12 INTRODUCTION OF SBCS LTD:

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 24

A STUDY ON LOANS AND ADVANCES

Shri Beereshwar Souhard credit Sahakari Ltd, a well known name in co-operative

sector of Karnataka, with the strong intention of socio economic development of the

masses. Shri Beereshwara Souhard Credit Sahakari Ltd was established at Examba in the

year 1991, only with Rs.3 Lakhs rupees of initial share capital this institute has operated it

balance sheet at remote and rural area, now it has increased its strength to Rs.408 crores

working capital with 51388+ shareholders, operating its balance through 85 branches all

over Karnataka.

Through the co-operative movement every year They are writing success stories

since 1991. It was possible due to the strong commitment shown by their management, staff

and the faith entrusted by the honorable member of various organizations in US. They have

seen successful in keeping their flag flying high all these years and They are sure, even in

the days to come well continue to excel performance in economic, education and social

field.

This year They witnessed a historic event as the Beereshwar Souhard Credit

Sahakari Ltd Examba tied up with reliance many for its Gold investment and Gold

accumulation plan. It was the first time in India where reliance has tied up with any private

organization for this venture. They have received over wheeling response for this scheme

from all sectors.

There was yet another feature in the co-operative of Jolle Udyog Samuha, as They

launched Shri Beereshwar Marketing Pvt Ltd at Tajvivanta, Bangalore. It is a multilevel

marketing company that is coming with various products of with very high rewards. Hi-tech

online software is developed for the company and a sophisticated office is set up at

Jayanagar, Bangalore. Response for this referral marketing is tremendous and They are sure

in the near future. Everyone associated with this company will be successful in their lives

because of financial stability. Recently SBML has launched its North India operations from

Patna and will be expanding towards North-east very soon.

Jolle Udyog Samuha is always committed for the well being of its staff and student.

The Institution have already insured the Rikshaw drivers, Group D employees of village

panchayats and Town Municipalities. This premium is fully paid by the Jolle Udyog

Samuh, taking this step further; They have formed a un-organized construction and worker

association. Members registered under this scheme get number of benefits.

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 25

A STUDY ON LOANS AND ADVANCES

We are into this service sector since long time; They have a tie-up with Axis Bank,

Corporate Bank for DD facilities. This group is corporate agent of SBI life, Tata ALG, NIC,

Bajaj Allianz, and Reliance Life Insurance. SBCS are also in transaction with western union

money and express money transfer to receive foreign exchange from any country. Apart

from this Organisation is also in Airport and Rail buy ticketing service. DTH and mobile

recharging service is available at all over branches. The main collaboration with reliance

money is providing vital information about the stocks and share market.

In the FMCG sector our Jyoti Multipurpose sahakari ltd is providing service to the

consumers through cloth shops, super markets and medicine divisions at affordable price.

Jyoti has 9 super markets, 3 credit branches and medical stores. They want to expand our

operations through Jyoti Bazar across North Karnataka.

The oil seed’s Grower co-operative society is providing agricultural equipment at

subsidy rate, training farmers about the cropping system and the use of pesticides,

fertilizers, soil erosion, and society is providing excellent services to the farmers in this part

of state.

Sahakar Educational and social welfare society is yet another wing of Jolle Udyog

samuha that is fulfilling in aspirations of thousands of student. Once the child takes

admission in either English medium (CBSE) or Kannada medium Nursery class he has the

all options open in front of him. They have pre-university (Arts/Commerce/Science), BCA

and BSW colleges in integrated campus, state of art infrastructure like hostel, kitchen,

interactive classes, laboratories, indoor and outdoor sports complex are already functional

and in the days to come SBCS adding much more amenities to the complex. Basavjyoti

Garment Training, Nipani and Knitting Centre at Galtaga are doing fine.

Sahakar Education and social welfare society’s family counseling centre, chikode

and is on the mission to join the broken relations and families, mahinal Kendra, athani, is

working 24 hours through women helpline.

Under this Amruta Self help Federation our 1200 self-help groups are on a mission

of women empowerment. As usual they are proving them with the market through chain of

Jyoti Bazars. This year various SHGs from Gokak Raibag, Bailhongal etc, visited Exmba to

see the functioning of their federation.

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 26

A STUDY ON LOANS AND ADVANCES

With the intension of providing employment to rural women and empowering the

financially a micro loan scheme is designed by the name Amulya. Under this scheme the

member of SHG are getting a loan up to Rs.20,000 with insurance facility, till now more

than Rs.66 crores loan distributed.

India is rural and agricultural based country. Government of Karnataka has

introduced ‘Yashwini’- a farmer health insurance scheme, our sahakari has made 500

policies under this scheme. The 500 families are secured under this scheme.

SBCCS is the ever growing organization and this year they opened our 75 th branches

in Karnataka. They have acquired ISO-9001-2008 certification. They are providing fully

computerized banking services to our customer, 17 branches are providing e-stamping

facility. They are continuously striving hard to uplift the economy and financial status of

their members, customers through all branches. To this date SBCCS has 51388+ members

with Rs.541 crore share capital. Our deposits have grown to Rs377 crores and the loan

advances are Rs.298,71,87,477.77. Our working capital is Rs.408,31,67,653.77 and this

year the profit is Rs.3,81,38,138.13 through Beereshwar, their main is to be provide

financial services under one roof.

As usually they are totally committed to serve the society through various ventures.

Under Jolle Udyog Samuh, They assure you of giving our best in the days to come so that

the overall standard of living of the people raises more than expected.

They have tied up with Axis bank for their ATM reward card for their members and

customers. ATM will be installed soon at our head office. There is no need to open new

account in Axis Bank but the same SB account holder’s sahakari will eligible to operate

using the cards; further information is available at nearest branch.

They have set up a separate department to look in to the matters of claim

settlements. This year 262 families have got the death claim settled through our sahakari,

the amount of settlement was Rs.106 crore.

FUTURE PLANS OF SBCCS LTD:

1. Opening their branches across Karnataka

2. Implementing ABB/core banking system from 2012-13

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 27

A STUDY ON LOANS AND ADVANCES

3. Converting the sahakari to multistate co operate society

4. Starting chit-fund balances for members

5. The organisation are trying to create own infrastructure for all their branches.

2.13 ORGANIZATION STRUCTURE:

FOUNDER

CHAIRMAN

ACCOUNTANT

VICE-CHAIRMAN

SENIOR ASSISTANT

JUNIOR ASSISTANT

MANAGER

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 28

A STUDY ON LOANS AND ADVANCES

EMPLOYEES

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 29

A STUDY ON LOANS AND ADVANCES

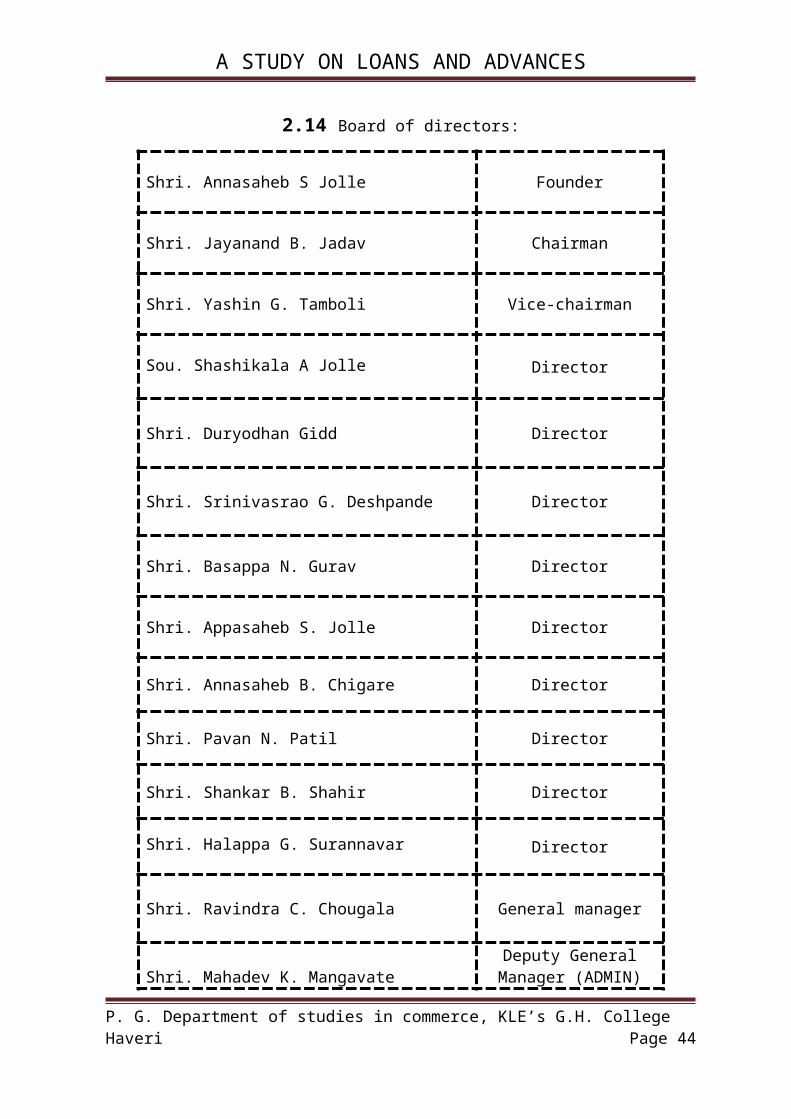

2.14 Board of directors:

Shri. Annasaheb S Jolle Founder

Shri. Jayanand B. Jadav Chairman

Shri. Yashin G. Tamboli Vice-chairman

Sou. Shashikala A Jolle Director

Shri. Duryodhan Gidd Director

Shri. Srinivasrao G. Deshpande Director

Shri. Basappa N. Gurav Director

Shri. Appasaheb S. Jolle Director

Shri. Annasaheb B. Chigare Director

Shri. Pavan N. Patil Director

Shri. Shankar B. Shahir Director

Shri. Halappa G. Surannavar Director

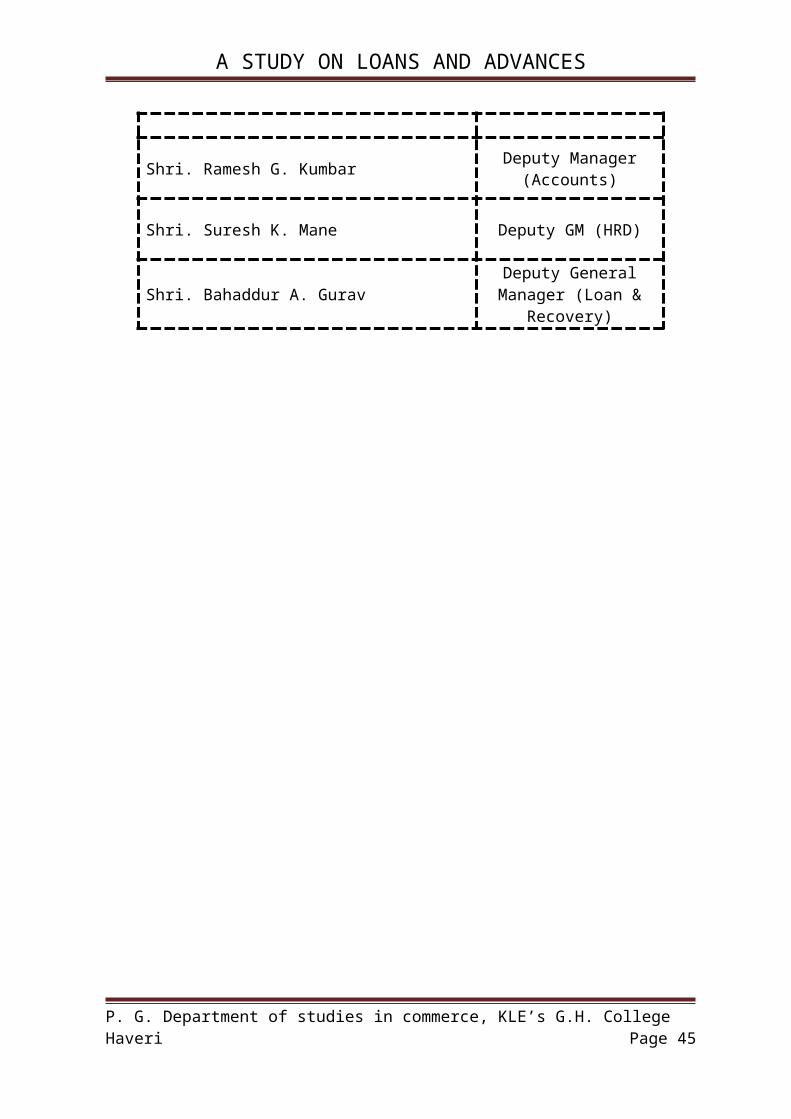

Shri. Ravindra C. Chougala General manager

Shri. Mahadev K. Mangavate Deputy General Manager (ADMIN)

Shri. Ramesh G. Kumbar Deputy Manager (Accounts)

Shri. Suresh K. Mane Deputy GM (HRD)

Shri. Bahaddur A. GuravDeputy General Manager

(Loan & Recovery)

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 30

A STUDY ON LOANS AND ADVANCES

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 31

A STUDY ON LOANS AND ADVANCES

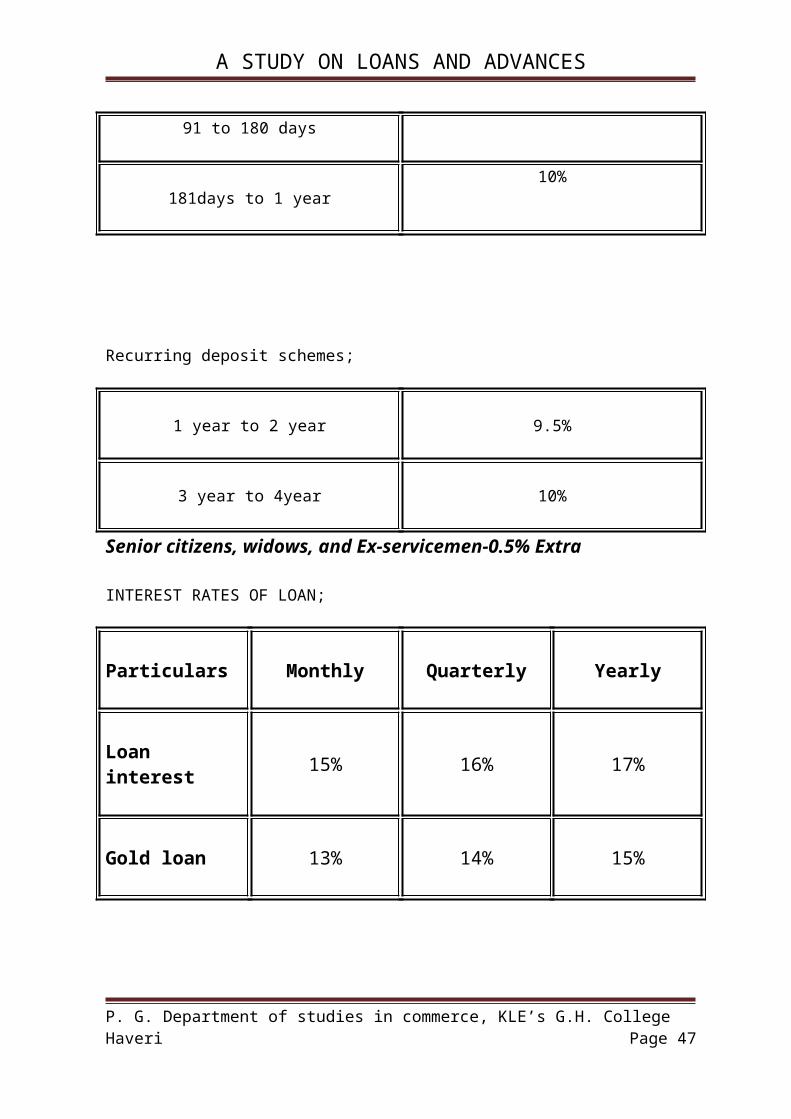

2.15 INTEREST RATE STRUCTURE IN SBCSS LTD

Basava jyoti deposit (monthly interest scheme)

30 days to 1 year 8%

3 year fixed period 9%

5 year fixed period 10%

Fixed deposit schemes;

1 year to 2 year 11.5%

2 year above upto 5 year 12%

Jyoti deposit schemes;

15 to 29 days5%

30 to 45 days7%

46 to 90 days9%

91 to 180 days9.5%

181days to 1 year10%

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 32

A STUDY ON LOANS AND ADVANCES

Recurring deposit schemes;

1 year to 2 year 9.5%

3 year to 4year 10%

Senior citizens, widows, and Ex-servicemen-0.5% Extra

INTEREST RATES OF LOAN;

Particulars Monthly Quarterly Yearly

Loan interest 15% 16% 17%

Gold loan 13% 14% 15%

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 33

A STUDY ON LOANS AND ADVANCES

CHAPTER-IIICONCEPTUAL FRAMEWORK

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 34

A STUDY ON LOANS AND ADVANCES

3.1 INTRODUCTION OF LOANS AND ADVANCES:

Any amount borrowed or lent is called loan. If money is borrowed it is debt of

business and if loan is given, it is receivable for the business.

Loan is a method of lending under which bank gives credit to a borrower for a fixed

period and for a specific purpose. Loan are promises for future payment, they have to be

repaid in periods beyond a year and are therefore long term liabilities.

In other words “when a banker makes an advance in a lump sum which cannot be

paid wholly or partly and which the customer has permission to withdraw subsequently it is

called loan.

Profit is the pivot on which the entire business activity rotates. Banking is a

essentially a business dealing with money and credit. Like a every other business activity,

banks are profit oriented a bank invest its funds in many ways to earn incomes. The bulk of

its income is dividend from loans and advances.

Banks makes loans and advances to traders, business and industrialist against the

security of some assets are on the basis of the personal security of the borrower in either

case, the banks run the risk of the default in repayment therefore, banks have to follow

caution policy and sound lending principle in the matter of lending. Banks in India have to

consider the national interest along with their own interest determining the lending policy.

Many times a borrowers need funds fixed asset on non-respective types of activities and

thus, seeks money from the bank that bank in one lump-sum. The loan amount is normally

repaid in installment. Loan may be short terms, medium or long-terms.

3.2 PRINCIPLES OF SOUND LENDING:

Traditionally, the banks follow three principles of lending viz.,

1. Safety

2. Liquidity

3. Profitability and

4. Security.

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 35

A STUDY ON LOANS AND ADVANCES

1. Safety: A bank lends what it receives from the public as deposits. The success of the

bank depends upon confidence of the depositing public. Confidence could be infused in the

depositories by the investing the money in safe and sound security. Safety depends upon:

The security offer by the borrower

The repaying capacity and willingness of the debtors to repay the loan with interest.

2. Liquidity: It refers to the ability of asset to convert into cash without loss within a short

time. The liabilities of bank are repayable on demand are at a short notice. To meet the

demand of the depositories in the time, the banks should keep its funds in liquid state.

Money locked up in the long term such as land, building, plants, machineries etc cannot be

received in bank and show less liquid.

3. Profitability: like all other commercial banks are run for the profit even government

owned is not exception to this. Banks earn profit to pay interest to depositories, declared

dividends to shareholders and meet establishment changes and other expenses, provide for

the reserve for bad and doubtful debts, description, maintenance of the improvement of

property owned by the bank and sufficient resource to the meet the contingent loss. So

profit is an essential consideration.

4. Security: consumer may offer different kinds of securities viz, land, building, machinery,

goods and raw materials to get advance. The securities of the customers are insurance and

banker can back upon than in times of necessity. Securities which could be marketed easily,

quickly and without less should be preferred.

3.3 PURPOSES OF THE LOAN:

Before sanctioning loans a banker should enquire about the purpose for which it is

needed loans for undesirable activities such as speculation and hording should be

discouraged. Banks readily allow borrowings for productive purposes. It is also equally

important on part of banks to insure that a loan is utilized for the proposed for which it is

granted so that repayment will be prompt.

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 36

A STUDY ON LOANS AND ADVANCES

Proposed of the loan has assumed a special significance in the present day concept

of banking it is equally important to insure that the loan is utilized for the proposed for

which it is granted.

Sources of repayment:

Before giving a financial accommodation, a banker should consider the source from

which repayment is promised.

Diversifications of risk:

The security conciseness of a banker and the integrity of the borrower are not

adequate factors to keep the bankers on safe side, what are important the diversifications of

risk. So that a bank should follow wise-policy for ‘do not lay all the eggs in the same basket

bank must advance moderate some to a large number of spread over a wide area and

belonging to different industries.

RECEIPT CONCEPT OF SOUND LENDING:

A sound credit is one their timely repayment is assumed. This largely depends on

the earning power of the business units. And repaying capacity of the borrowers so great

emphasis is laid on the productivity of loan. Since the banks have should earned and

additional responsibility of keeping the tempo of development of an economy. They should

consider productivity of loans as the cheap criterion for advising loan.

3.4 TYPES OR FORMS OF ADVANCES:

Bank offers different types of borrowing facilities to their customer. The credit

facility may be broadly into four types.

1. Loan:

2. Cash credit system

3. Overdraft

4. Bills purchase and discount

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 37

A STUDY ON LOANS AND ADVANCES

1. Loans: In case of loans banker advance a lump-sum for a certain period at an agreed rate

of interest. The entire amount is paid on occasion either in cash or credit in his current

account, which he can drawn at any time the interest is charged for the full amount for

sanction whether he withdraws the money from his account or not. The loan may be repaid

in installment or at expire of certain paid. The loan made with or without security. A loan

once rapid in a full or in part cannot be withdrawn again by the customer. In case of

borrower, wants to further loan and he has to arrange for the fresh loan.

Loan may be demand or term loan. A demand loan is payable on the demand for a

short period. Usually granted to meet working capital needs for the borrower. The term loan

may be medium or long term loan. The medium term loans granted for a period of ranging

from 1 year to 5 years for the purchase of vehicles, tractors and tools and equipments. Long

term loans are granted for capital expenditure such as purchase of land, construction of

factory, building, purchase of new machinery and modernization of plants etc.

Advantages of Loan System:

Financial discipline on the borrower

Periodic review of local account

Profit liability

Limitation of Loan:

Inflexibility: Every time loan is required it is to be negotiated with the banker to

avoid its borrower, may borrow in excess of their extent requirement contingencies.

Though loans are fixed periods: But in practice their role over, that is, they are

renewed frequently

Loan documentation: It is more comprehensive as compare to each credit

system.

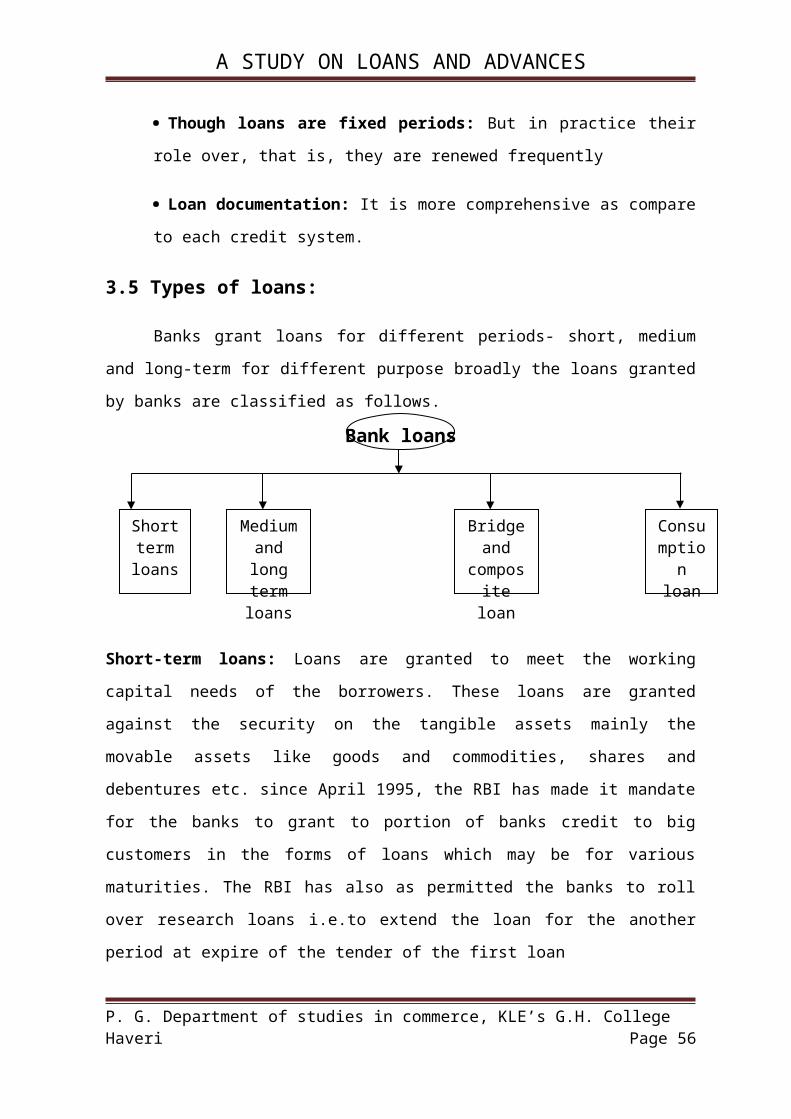

3.5 Types of loans:

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 38

Short term loans

Medium and long

term loans

Bridge and

composite loan

Consumption

loan

A STUDY ON LOANS AND ADVANCES

Banks grant loans for different periods- short, medium and long-term for different

purpose broadly the loans granted by banks are classified as follows.

Bank loans

Short-term loans: Loans are granted to meet the working capital needs of the borrowers.

These loans are granted against the security on the tangible assets mainly the movable assets

like goods and commodities, shares and debentures etc. since April 1995, the RBI has made

it mandate for the banks to grant to portion of banks credit to big customers in the forms of

loans which may be for various maturities. The RBI has also as permitted the banks to roll

over research loans i.e.to extend the loan for the another period at expire of the tender of the

first loan

Term loans: Term loans are given for medical and loan periods, and loans are used for

acquiring for fixed asset or for not modernization and expansion of the existing units. They

may also be used for working capital requirements. An important feature of the term loan is

the felt that they are repayable in yearly or half-yearly installments over a period of time.

Payment is to be made according to specified schedule, extending up to 15 years which

imposes a short off financial discipline on borrowing concern. The amortization gradually

starts two to three years after the sanction of the loan.

Bridge Loan: Bridge loan are essentially short-term loans which are granted to industrial to

meet their urgent and essential needs during the period in formalities for the availing of the

term loans sanctioned by the financial institutions are being fulfilled or necessary steps are

being taken to raise the capital market. These loans are granted by financial institutions.

Composite loan: When a loan is granted both for buying capital asset and for working

capital purposes, it is called composite loans. Such loans are granted to small borrower,

such as artisans, farmers and industries etc.

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 39

A STUDY ON LOANS AND ADVANCES

Consumption Loan: The normally banks provide loans for productive purpose only, but as

an exception loans are also granted on the limited scale to meet the medical needs or

educational expenses or expenses relating to marriages and other social care monies etc.

Classifications of Loans and advances:

Secured loan

Unsecured loan

Secured loans: According to section 5A of Banking Regulation Act , 1949, a secured loans

are advances or a loan advance made on the security of the asset, the market value of the

market which is not yet many time less than the amount. Such loans and advances and

unsecured loans are advances are means a loan or advance so not secured.

Thus the distinguish of the secured loan or advance are as follows.

The loan must be made on the security of the tangible asset like goods and

commodities, land and building, gold silver and corporate and government securities etc.

The market value of such security less than the amount of the loan at any time till

the loans is rapid if the farmer falls below the latter because of the decline in the market

price the loan is considering as a partly secured.

2. Cash credit system: It is one of the most important methods of the lending in India

under this method, the banker fix the limits for a customer the cash credit limit. The bank is

generally specified after taking into account the important features of the borrowing

concern, for example production, sale inventory fast credit limits etc.

Advantages:

Flexibility: The borrower need not keep surplus funds idle with themselves. They

can recycle the funds quite efficiently and can minimize interest charges by

depositing all cash accruals in the bank account.

Operative convenience: Banks have maintained one account for all transactions

of customer. The repetitive documentation can be avoided.

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 40

A STUDY ON LOANS AND ADVANCES

Disadvantages:

Fixation of the credit limit

Banks inability to verify the end user of the funds

Lack of proper management of funds

3. OVERDRAFT: Overdraft is an arrangement between the banker and customer by which

the latter is allowed to withdraw over above his credit balance in the current account up to

the agreed limit this is only a temporary accommodation usually granted against security.

The borrower is permitted to draw and repay any numbers of times provide the total

amount of over drawn does not exceed the agreed limit. The interest is charged for the

whole amount sanctioned.

Temporary draft: Banks sometimes grant unsecured overdraft for the small amount

to customer having a current account with them. Such customers may be government

employees with the fixed income or traders. Temporary overdrafts are permitted only where

reliable sources of funds are available to a borrower of repayment.

4. BILL OF PURCHASED AND DISCOUNTED: Banks grant advance to their

customers by discounting bill of exchange or promote the amount of after deducting interest

from the amount of the instrument, is credited in the accounts of the customer. In this form

of lending the banker receiver the interest on advance. Discounting of bills constitutes a

clean and advance, and banks rely on the creditworthiness of parties to the bill.

Advantages:

Safety of bank funds

Certainty of payments

Facility of refinance

Stability in the value of bill

Profitability

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 41

A STUDY ON LOANS AND ADVANCES

3.5 PROCEDURE OF LOAN:

3.6 VARIOUS LOANS SCHEMES:

The bank providing various loan schemes are as follows:

1. Vehicle loan

2. Machinery loan

3. Education loan

4. Consumer loan

5. Staff loan

6. Clean loan

7. Finance for profession person

8. Housing loan

9. Fixed deposit loan

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 42

A STUDY ON LOANS AND ADVANCES

10. NSC KVP loan

11. Purchase bill discounting limits

1) Vehicle Loan: The vehicle loan is provided to customer by purchased a two-

wheeler or four-wheeler vehicles. This loan is providing to individual, partnership

and proprietorship and private limited company. The banks provide a loan before all

papers clear with 24 hours of loans is 60 months. The bank for its security to be

collected by the customer property document.

2) Machinery loan: This loan provides to purchase machinery. New machinery

purchased and hand-over machinery valuation loan. The machinery loan provides to

partnership loan and proprietorship firm etc.

3) Education loan: Education loan is a better facility to the students of higher study in

India or foreign. The bank providing loan according to the students parents income.

The rate of loan is different in India and foreign. This loan is providing after

standard 12th. This facility is could facility students who want study more.

4) Consumer loan: It is providing to purchase a daily use in the house. Banks these

types of loans involve different types of instruments like daily use of house,

television, refrigerator, telephone, computer etc.

5) Staff loan: This loan is provided to bank staff with low rate of interest and loan

margin is also favors for the staff. This loan is provided related to employee’s salary.

This loan is more benefit to the staff and their self use.

6) Clean loan: Personal individual loan is called clean loan on which the rate of

interest is at 14% p.a. this loan is provided to only individual person for use of

personal work.

7) NSC (KVP): RBI suggests to co-operative bank that bank take 25% of margin on

national saving certificate and does not take interest on margin. In this way up to

75% loans granted by the bank.

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 43

A STUDY ON LOANS AND ADVANCES

8) Housing loan: Housing loan is providing to purchase house, plats, shops, office or a

building. The loan providing to individual, partnership and proprietorship, private

limited company to customer etc.

9) FFP loan (Finance for Professional Persons): A FFP loan is finance for

professional persons. A person with the professional degree and engaged in the

professional independently for example doctors, architects, lawyer etc.

3.7 RATE OF INTEREST IN DIFFERENT TYPES OF LOANS

TYPE OF LOANS RATE OF INTEREST LIMIT INSTALMENTS

1. Vehicle loanUp to Rs.2L-12%

Up to 2 to 4L-12.5%Above 4L-13%

Maximum 75%of original price

60 months.

2. Machinery loanUp to Rs.5L-12.5%Up to 5 to 15L-13%Above 15L-13.5%

New---80%Old---70% 72 to 73 months

3. Education loan India---10%Outside---12%

India---max-Rs.8L Outside

Rs.10LNA

4. Consumer loan 12.5% 80% on TV, Tel85% on Vehicles 15 monthly

5. Staff loan 6% NA NA

6. Clean loan 14% Max Rs.45,000 50 monthly

7. NSC 9.5% 75% on NSC face value 36 monthly

NA Rs. 5L to 50 Cr More than 10

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 44

A STUDY ON LOANS AND ADVANCES

8. Housing loan years

9. FFP 12.5% NA 72 months

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 45

A STUDY ON LOANS AND ADVANCES

CHAPTER-IVDATA ANALYSIS AND

INTERPRETATION

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 46

A STUDY ON LOANS AND ADVANCES

4.1 INTRODUCTION:

Analysis and interpretation: The term analysis means methodological classification

of data given in the financial statements. The figures given in the financial statements will

not help one unless they are put in simplified form. Interpretation means explain the

meaning and significance of the data so simplified manner.

However, both analysis and interpretation are complimentary to each other.

Interpretation requires analysis, which analysis useless without interpretation. Most of the

user used the term analysis only to cover the meaning of both analysis and interpretation

since analysis involves interpretation.

4.2 RATIO ANALYSIS & INTERPRETATION IN SBCCS:

CURRENT RATIO:

Current ratio is calculated by dividing current assets by current liabilities. Current

assets include cash and other assets that can be converted into cash within in a year, such as

marketable securities, debtors and inventories. Prepaid expenses are also included in the

current assets as they represent the payments that will not be made by the firm in the future.

All obligations maturing within a year are included in the current liabilities. Current

liabilities include creditors, bills payable, accrued expenses, short-term bank loan, income

tax, liability and long-term debt maturing in the current year.

The current ratio is a measure of firm’s short-term solvency. It indicates the

availability of current assets in rupees for every one rupee of current liability. A ratio of

greater than one means that the firm has more current assets than current claims against

them Current liabilities

Current assets . Current liabilities

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 47

CURRENT RATIO =

A STUDY ON LOANS AND ADVANCES

TABLE - 1

GRAPH - 1

INTERPRETATION:

LEVERAGE RATIOS:

The leverage or solvency ratio refers to the ability of a concern to meet its long term

obligations. Accordingly, long term solvency ratios indicate firm’s ability to meet the fixed

interest and costs and repayment schedules associated with its long term borrowings. The

following ratio serves the purpose of determining the solvency of the concern.

PROPRIETORY RATIO:

A variant to the debt-equity ratio is the proprietary ratio which is also known as

equity ratio. This ratio establishes relationship between share holder’s funds to total assets

of the firm.

Shareholders funds Total assets

TABLE: 2

GRAPH-2

CURRENT ASSETS TO FIXED ASSETS RATIO

This ratio differs from industry to industry. The increase in the ratio means that

trading is slack or mechanization has been used. A decline in the ratio means that debtors

and stocks are increased too much or fixed assets are more intensively used. If current assets

increase with the corresponding increase in profit, it will show that the business is

expanding.

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 48

PROPRIETARY RATIO =

A STUDY ON LOANS AND ADVANCES

Current assets Fixed assets

TABLE: 3

GRAPH-3

INTERPRETATION

PROFITABILITY RATIOS:

The primary objectives of business undertaking are to earn profits. Because profit is

the engine, that drives the business enterprise.

Return on total assets

Reserves and surplus to capital ratio

Earnings per share

Operating profit ratio

Price – earnings ratio

Return on investments

RETURN ON TOTAL ASSETS

Profitability can be measured in terms of relationship between net profit and assets.

This ratio is also known as profit-to-assets ratio. It measures the profitability of investments.

The overall profitability can be known.

Net Profit . Total Assets

Net profit = Earnings before interest and tax

P. G. Department of studies in commerce, KLE’s G.H. College Haveri Page 49