42

Business Unit PCS Polycarbonate Update Visit to Customer Place September 7, 2004

Business Unit PCS

Polycarbonate Update

Visit to CustomerPlace

September 7, 2004

September 7, 2004 • Seite 2Business Unit PCS

Organizational Overview

September 7, 2004 • Seite 3Business Unit PCS

Bayer MaterialScienceA Core Business of Bayer

HealthCare

MaterialScience

CropScience

September 7, 2004 • Seite 4Business Unit PCS

• Butadien- & Butyl Rubber• Rubber Products• Rubber Chemicals• Fibers• Rhein Chemie• Semi Crystalline Products

Bayer MaterialScience & LanxessFormation of Two New Companies

• Polycarbonat• PC Sheets• TDI• MDI• Polyether• Base- und modified

Isocyanates• Thermoplastic

Polyurethanes• Inorganic Base Chemicals

• Basic Chemicals• Functional Chemicals• Fine Chemicals• Inorganic Pigments• Ion Exchange Resins• Leather Chemicals• Material Protection• Paper Chemicals• Textile Processing

Chemicals

• H.C. Starck• Wolff

Walsrode

• PC/ABSBlends

• StyrenicsABS/SAN

Bayer Bayer MaterialScienceMaterialScience LanxessLanxess

Bayer Polymers Bayer Chemicals

September 7, 2004 • Seite 5Business Unit PCS

• New customers• New applications• Regional expansion

• Displacement• Consolidation• Different business

models

• Product and processinnovation

Development Growth “Mature” markets

Growthdriver

Successfactors

Product properties• Technology leadership• Application know-how

Market access• Marketing and fulfillment• Financial muscle

Cost leadership• Processing technology• World-scale plants• Sites / Portfolio

Controlling Profitable growth Capital productivity

Market stage

Time

BayerLanxess

Bayer MaterialScience and LanxessDifferent Business Characteristics

September 7, 2004 • Seite 6Business Unit PCS

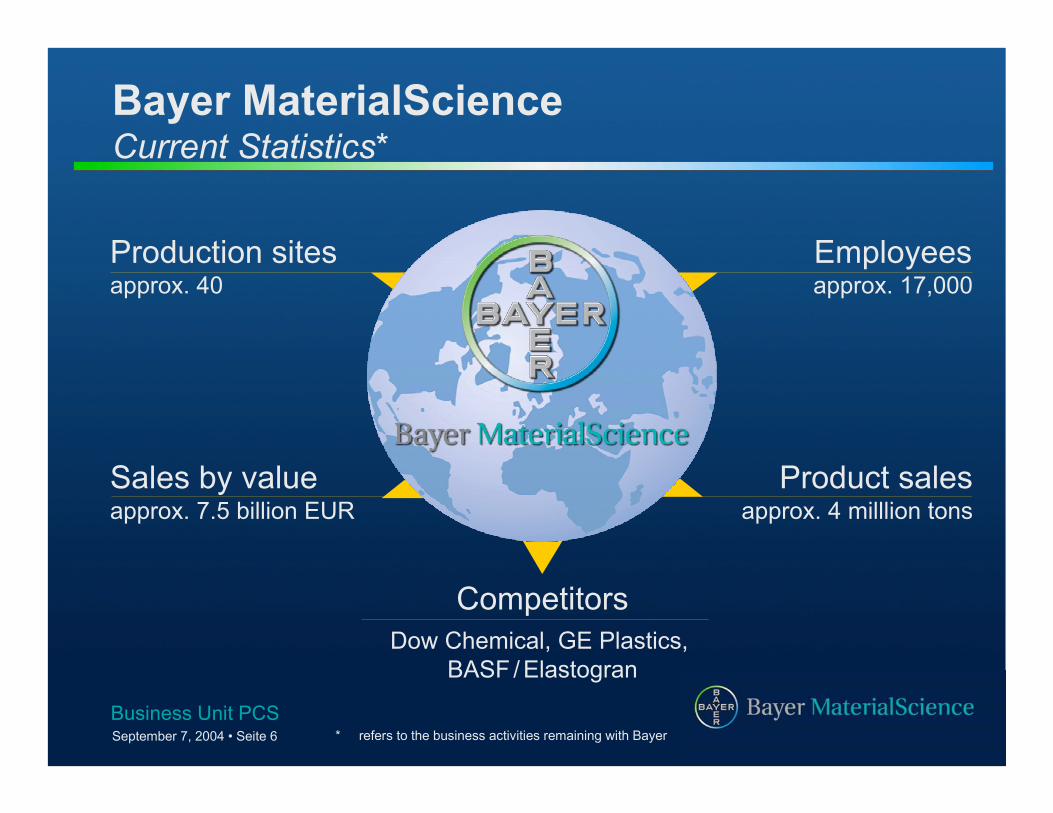

Bayer MaterialScienceCurrent Statistics*

Production sitesapprox. 40

Employeesapprox. 17,000

Product salesapprox. 4 milllion tons

Sales by valueapprox. 7.5 billion EUR

CompetitorsDow Chemical, GE Plastics,

BASF / Elastogran

* refers to the business activities remaining with Bayer

September 7, 2004 • Seite 7Business Unit PCS

Bayer MaterialScienceBusiness Units and Sales Share

42%23%

18%2%3%4% 8%

PolyurethanesPolycarbonate

Coating RawMaterialsWolff Walsrode

H.C. StarckThermoplasticPolyurethanes

Umsatz7.5 Mrd. €

InorganicBasic Chemicals

September 7, 2004 • Seite 8Business Unit PCS

Bayer MaterialSciencePortfolio Driven by Growth and Market Leadership

PolycarbonatesPolycarbonates(PCS)(PCS)

VolumeVolumeGrowthGrowth

2004-062004-06

Our Our PositionPosition

EMEAEMEA AmericasAmericas APACAPAC

PolyurethanesPolyurethanes(PUR)(PUR)

Coating RawCoating RawMaterials*Materials*

(CAS)(CAS)

+8% p.a.

+5% p.a.

+5% p.a.

GlobalGlobal

#1(ms > 40%)

#1 #1 #1

#1(ms = 26%)

#1 #1 #1

#2(ms = 30%)

#1 #2 #2

EMEA: Europe, Middle East, AfricaAPAC: Asia Pacific*) arom. and aliph. Isocyanates

September 7, 2004 • Seite 9Business Unit PCS

Bayer MaterialScience Organziation

NoerenbergNoerenbergVV Bayer MaterialScienceVV Bayer MaterialScience

PlumpePlumpeAdministrationAdministration

Van Van OsselaerOsselaerP&TP&T

PatersonPatersonMarketing & InnovationMarketing & Innovation

J. WolffJ. WolffBU BU CoatingsCoatings, , Adhesives Adhesives &&

SealantsSealants

G. HilkenG. HilkenBU PolycarbonatesBU Polycarbonates

P. P. VanackerVanackerBU BU PolyurethanesPolyurethanes

T. T. BielfeldtBielfeldtBU BU ThermoplasticThermoplastic

PolyurethanesPolyurethanes

C. OhmC. OhmBU BU Inorganic Inorganic BasicBasic

ChemicalsChemicals

D. HerzogD. HerzogWolff WalsrodeWolff Walsrode

H. HeumüllerH. HeumüllerH.C. StrackH.C. Strack

Bayer MaterialScienceBoard of Management

BMS ServicesBMS Services

September 7, 2004 • Seite 10Business Unit PCS

Global Leadership Team BU Polycarbonates

Klaus-Patrick MichaelBusiness Planning &

Administration

Dirk Van MeirvenneProduction &Technology

Hartmut LöwerGlobal Innovations &Product Management

Dennis McCulloughMarketing / BD

EMEA & LA

Rainer SchorrMarketing / BD

NAFTA

Jürgen RaabMarketing / BD

APAC

Günter HilkenHead ofBU PCS

Customer Focus with ~3,000 employees world-wide!

September 7, 2004 • Seite 11Business Unit PCS

Polcarbonate Market Update

September 7, 2004 • Seite 12Business Unit PCS

Consumption World: approx. 13 Mio.t (Value: > 25 Mrd. Euro)

Growth: approx. +6% p.a. (2003-2007)

* w/o PC for blends

PBT4%

PA 6.68%

PET eng.1%

Blends7%

PMMA9%

POM5%

H T Polymers2% ABS, ASA

38%

SAN3%

PC straight *14%

PA 69%

World Market Engineering Thermoplastics2003

September 7, 2004 • Seite 13Business Unit PCS

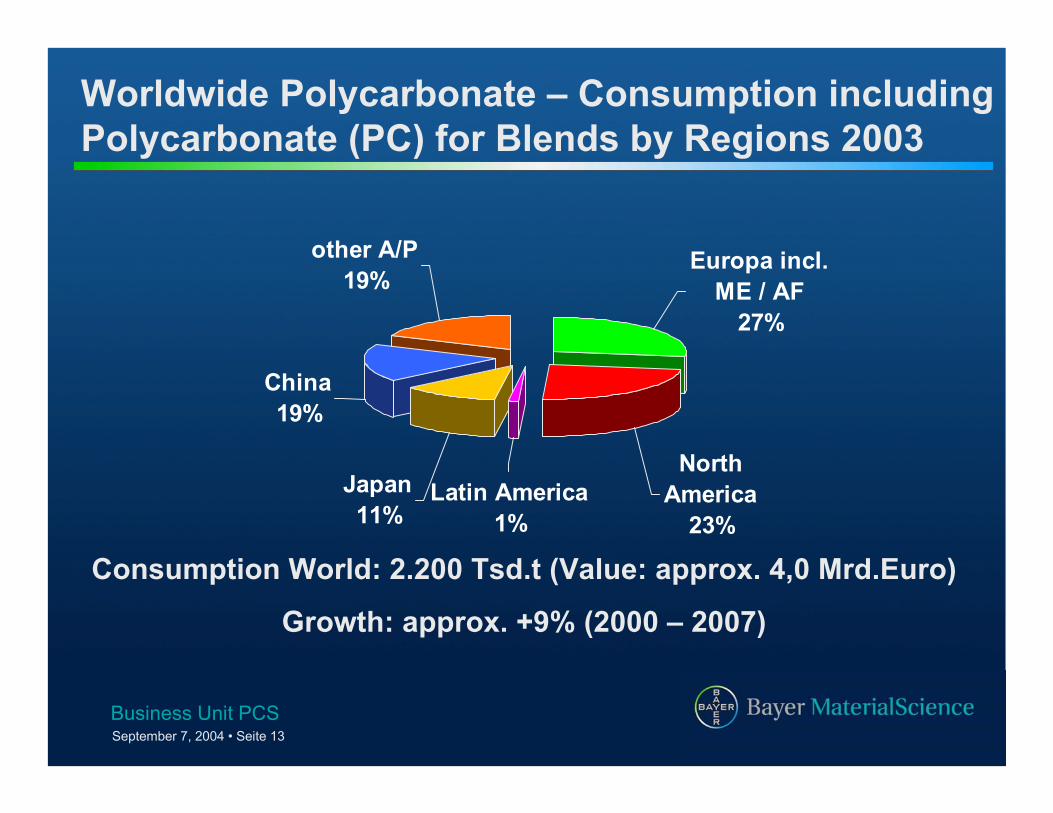

Europa incl. ME / AF

27%

other A/P19%

China19%

Japan11%

Latin America1%

North America

23%

Consumption World: 2.200 Tsd.t (Value: approx. 4,0 Mrd.Euro)

Growth: approx. +9% (2000 – 2007)

Worldwide Polycarbonate – Consumption includingPolycarbonate (PC) for Blends by Regions 2003

September 7, 2004 • Seite 14Business Unit PCS

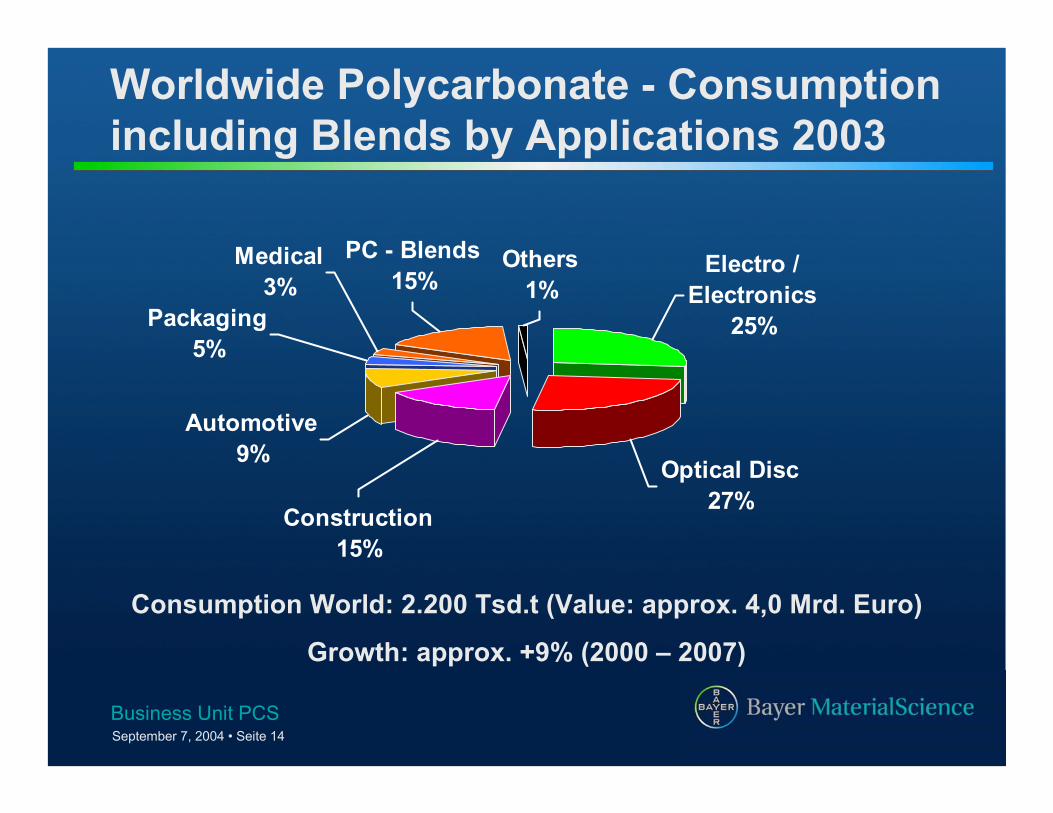

PC - Blends15%

Others1%

Electro / Electronics

25%

Medical3%

Packaging5%

Automotive9%

Construction15%

Optical Disc27%

Consumption World: 2.200 Tsd.t (Value: approx. 4,0 Mrd. Euro)

Growth: approx. +9% (2000 – 2007)

Worldwide Polycarbonate - Consumptionincluding Blends by Applications 2003

September 7, 2004 • Seite 15Business Unit PCS

610 660865

1.000

1.300

1.900 2.0502.200

2.400

0

500

1000

1500

2000

2500

1990 1992 1994 1996 1998 2000 2002 2003 2004

World Consumption Polycarbonate (PC) includingPolycarbonate for Blends from 1990 to 2003 (Tsd.t)

September 7, 2004 • Seite 16Business Unit PCS

-10%

0%

10%

20%

30%

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

Market Growth

Economic Cycles: 7 to 10 years

Polycarbonate Market Growth versusPrevious Year

September 7, 2004 • Seite 17Business Unit PCS

• Europe (incl. ME/AF) ~ + 6% p.a.

• North America ~ + 6% p.a.

• Latin America ~ + 7% p.a.

• Japan ~ + 3% p.a.

• China ~ + 18% p.a.

• other Asia / Pacific ~ + 8% p.a.

• World (average) ~ + 8-9% p.a.*) forecast

Polycarbonate (PC) – Average MarketGrowth 2003 – 2007 *

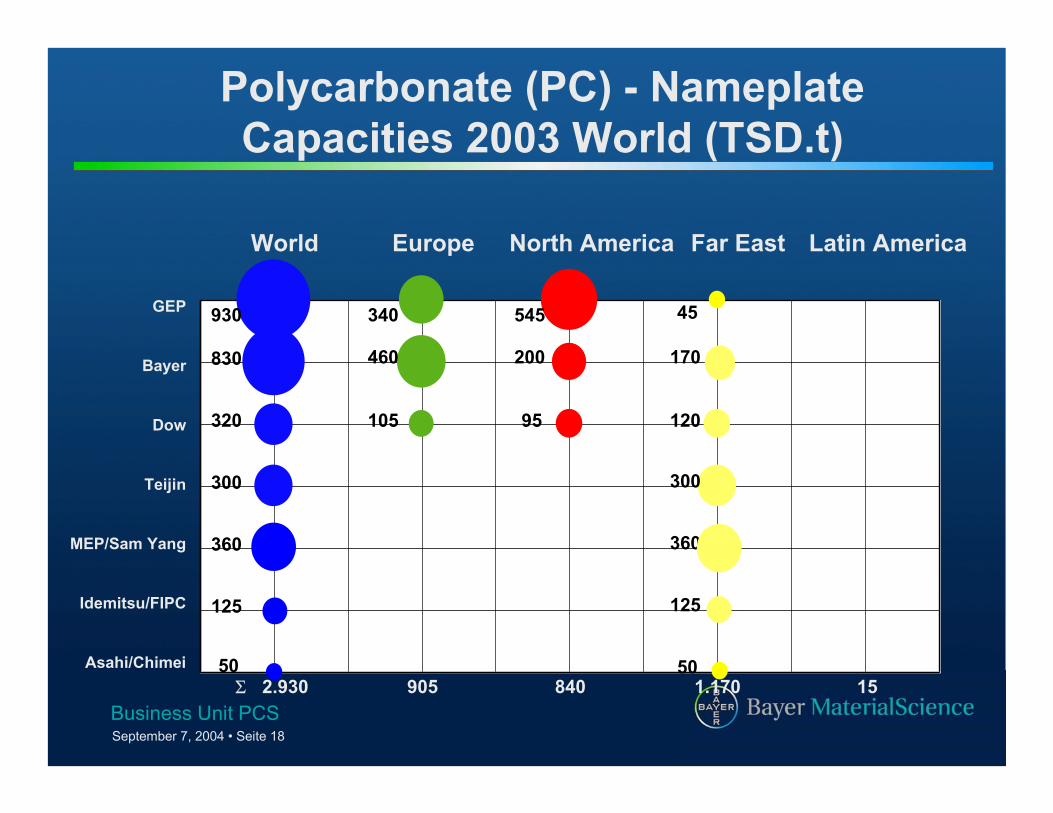

September 7, 2004 • Seite 18Business Unit PCS

930

830

320

300

360

125

50

340

460

105

545

200

95

45

170

120

300

360

125

Σ 2.930 905 840 1.170 15

World Europe North America Far East Latin America

GEP

Bayer

Dow

Teijin

MEP/Sam Yang

Idemitsu/FIPC

Asahi/Chimei 50

Polycarbonate (PC) - NameplateCapacities 2003 World (TSD.t)

September 7, 2004 • Seite 19Business Unit PCS

Polycarbonate Capacity Shares

Bayer Sites

GE Sites

DOW Sites

Mitsubishi Sites

Teijin Sites

Idemitsu / FPIP Sites

Chimei Sites

Polycarbonatos do Brasil

Bayer 29%

GE31%

Dow10%

Teijin10%

others1%

Chimei2%

MEP/Samyang12%

Idemitsu5%

2003

September 7, 2004 • Seite 20Business Unit PCS

Total: 830 kt/a

Plan 2006: 930 kt/a

Baytown, TX200 kt/a

Uerdingen,Germany260 kt/a

Map Ta Phut,Thailand170 kt/a

Shanghai, China200kt/a

(1. Phase 100 kt/a Start 2Q./2006)

Antwerp, Belgium200 kt/a

PCS wet side facilities

Baytown, USA

Map Ta Phut, Thailand

Uerdingen, GermanyAntwerp, Belgium

.........The Heritage after 50 Years of Makrolon

PCS dry side & blends facilities

Newark, OHFilago, IT

Uerdingen, D

Map Ta Phut, TH

Caojing, China

September 7, 2004 • Seite 21Business Unit PCS

InnovativeApplications

Electrically Insulated Components

Twin-wall sheetCrystal-clear Solid Sheet

Water Bottles

CD, DVD,Blu Ray Disc

GlazingSystems

Blends for Automotive Applications and Computer Housings

Time

The Future has a Name....

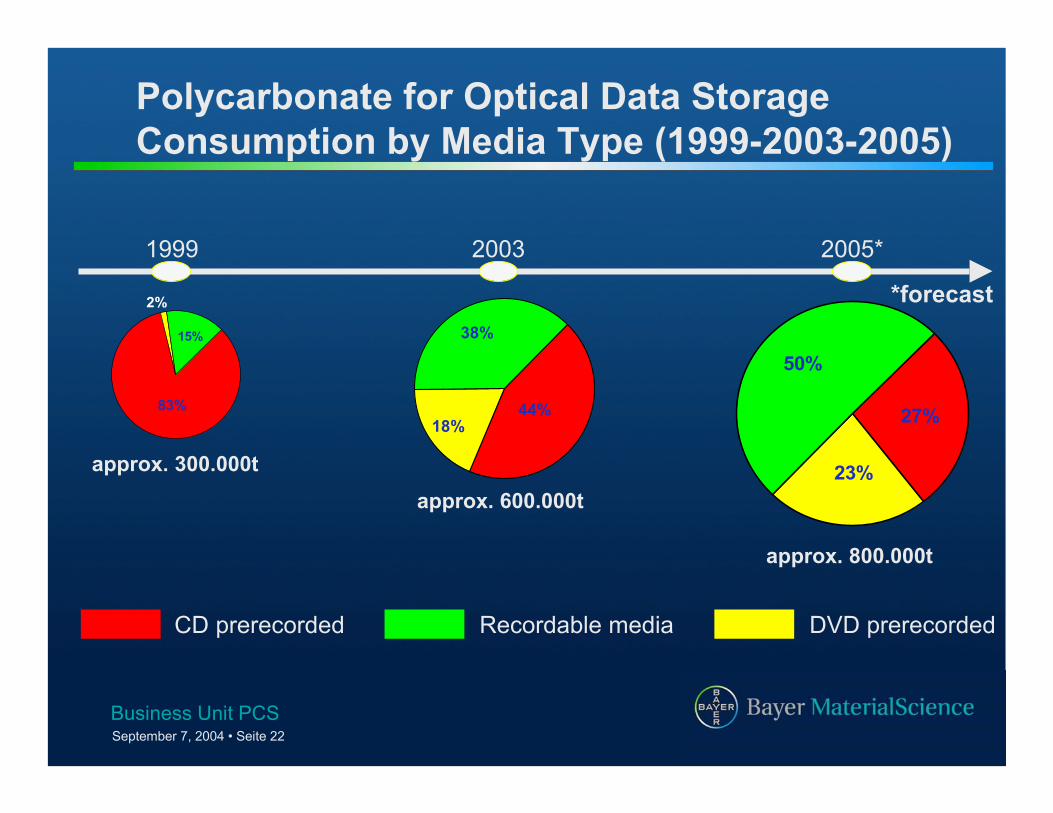

September 7, 2004 • Seite 22Business Unit PCS

18%44%

38%

1999 2003 2005*

CD prerecorded Recordable media DVD prerecorded

approx. 600.000t

approx. 800.000t

Polycarbonate for Optical Data StorageConsumption by Media Type (1999-2003-2005)

*forecast2%

15%

83%

approx. 300.000t 23%

50%

27%

September 7, 2004 • Seite 23Business Unit PCS

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

0

5.000

10.000

15.000

20.000

Mio Discs

HD-Disc -R,RW DVD-R,RW DVD Prerecorded CD-R,RW CD Prerecorded

* forecast

Optical Data Storage Development

** * * * * *

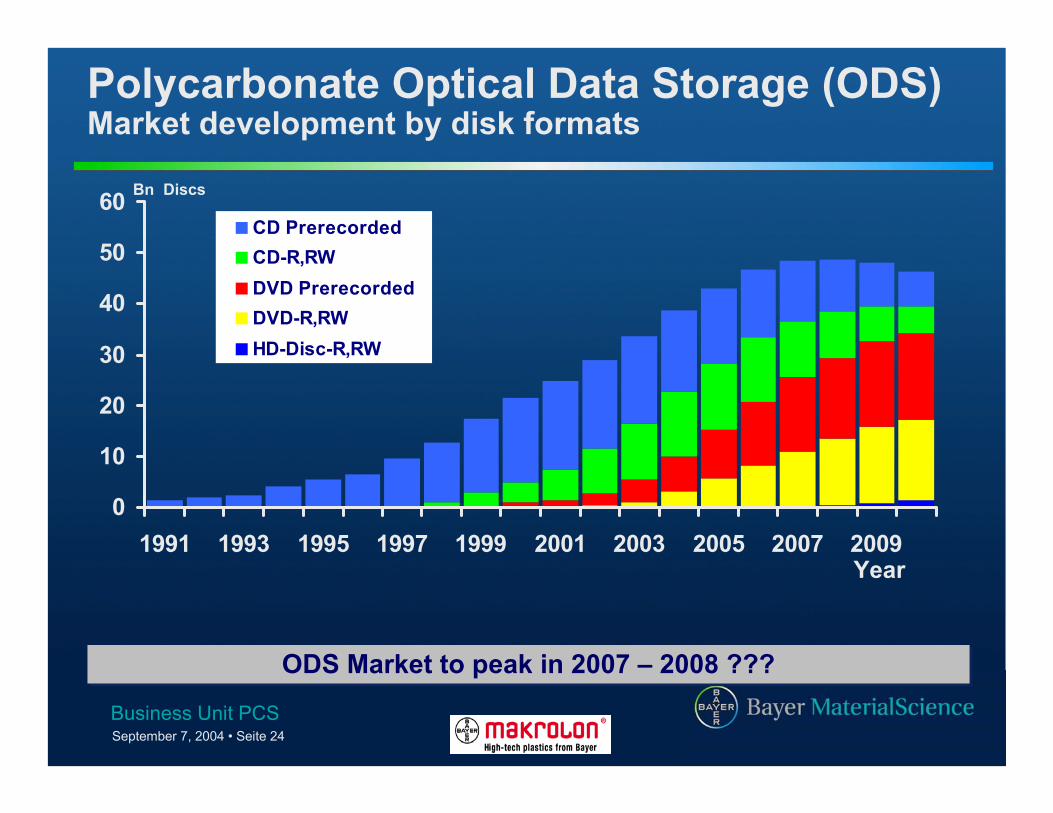

September 7, 2004 • Seite 24Business Unit PCS

0

10

20

30

40

50

60

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

CD PrerecordedCD-R,RWDVD PrerecordedDVD-R,RWHD-Disc-R,RW

Bn Discs

Year

Polycarbonate Optical Data Storage (ODS)Market development by disk formats

ODS Market to peak in 2007 – 2008 ???ODS Market to peak in 2007 – 2008 ???

September 7, 2004 • Seite 25Business Unit PCS

2000 2004* 2008*

Êurope Americas APAC

Globalization and consolidation in the bottled water industry is accelerating

Global PC demand for water bottle expected to grow to 106 Tsd.t in 2008*

87106

65

Market Development PC for water bottle(Tsd.t)

*) forecast

Water Bottle Market: Trends and Development

September 7, 2004 • Seite 26Business Unit PCS

2000 2004* 2008*

Êurope Americas APAC

295332

402(Tsd.t)

The global sheet market is expected to grow in 2004* to 2008* with an average rate of 5 % p.a.Multi wall sheet growing faster than solid sheet. Multi wall sheet is the major product in Europe, solid sheet is dominating in America andin the Far East.

Market development PC for sheet

*) forecast

Sheet Market: Trends and Development

September 7, 2004 • Seite 27Business Unit PCS

September 7, 2004 • Seite 28Business Unit PCS

Advantages of Polycarbonatein Automotive Glazing

•Freedom of design•Integration offunctionalities

•Reduction ofmanufacturing cost

•Burglary protection

•Accident safety

•Weight reduction

•Result: lowering ofcenter of gravity

Fuel savings

Recycling

Design Weight

Safety Environment

September 7, 2004 • Seite 29Business Unit PCS *) forecast

1997 2000 2003

Declining margins in a growing marketrequire strategic repositioning of PCbusiness

Declining margins in a growing marketrequire strategic repositioning of PCbusiness

volumevolume

priceprice

profitprofit

70%

75%

80%

85%

90%

95%

100%

1982 1987 1992 1997 2002

Price increases and good profitabilityare only possible at utilization > 85%Price increases and good profitabilityare only possible at utilization > 85%

Polycarbonate – Economic Environment

September 7, 2004 • Seite 30Business Unit PCS

Bayer MaterialScience

Teijin Chemicals

Idemitsu/Formosa

Bayer MaterialScience

Teijin Chemicals

Idemitsu/Formosa

Mitsubishi

Chimei

DOW Chemicals

Mitsubishi

Chimei

DOW Chemicals

GE AdvancedMaterialsGE AdvancedMaterials

Strategic Responses to Current Market Situation

Remain Core BusinessClear Growth StrategyCont. strategic investment

Remain Core BusinessClear Growth StrategyCont. strategic investment

Abandon Core BusinessFocus on cash generationno strategic investment

Abandon Core BusinessFocus on cash generationno strategic investment

„Wait and See“no further investmentno refocuss

„Wait and See“no further investmentno refocuss

??

Profitable Growth Long term exitUndecided

September 7, 2004 • Seite 31Business Unit PCS

50%

60%

70%

80%

90%

100%

110%

1Q 2

001

3Q 2

001

1Q 2

002

3Q 2

002

1Q 2

003

3Q 2

003

Jan

04

Mrz

04

EMEANAFTAAPAC

Market Prices PolycarbonateIndex 1Q2001 = 100%

86%83%

81%

87%

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%

2001 2002 2003 2004

GlobalCapacity Utilization (%)

Turn-Around in Polycarbonate on the Horizon

September 7, 2004 • Seite 32Business Unit PCS

0

20

40

60

80

100

120

140

2002 2003 2004 2005

Bayer GE-P Teijin DOW MEP Chimei Formosa PRC Kosan

Published Capacity Expansion Plans

252 kt

290 kt

200 kt

162 kt

September 7, 2004 • Seite 33Business Unit PCS

Capacity Demand Balance World

91 kt 128 kt - 15 kt - 61 kt

Global Capacity Surplus:

Cartagena Effekt

Delta to previous year

0

50

100

150

200

250

300

350

2002 2003 2004 2005

Europe Cap. Europe Dem. America Cap. America Dem.Asia Cap. Asia Dem. World Cap. World Dem.

September 7, 2004 • Seite 34Business Unit PCS

Raw Material Crisis

September 7, 2004 • Seite 35Business Unit PCS

We are Experiencing a Crisis Situation

Raw material costs have escalated to unprecedented high levels andare affecting margins drastically in the Plastics Industry

Benzene contract prices in September have reached levels of $ 1185/tin the US and € 950/t in Europe!

– Demand is strong and supply will remain tight due to limitedcapacity

– Strong demand in Asia and Europe for polycarbonate and otherplastics derived from benzene has put intense pressure on supply

– Although high crude oil prices have an influence on the price ofbenzene, there is not a direct linked

– Unfortunately, there is no end in sight for price relief in the nearfuture

This is a severe problem that has resulted in drastic pricing measuresin the plastics industry globally..........This not just a Polycarbonate or aBayer problem!

September 7, 2004 • Seite 36Business Unit PCS

Raw Material Flow for Polycarbonate

Propylene

BenzeneCumene

Acetone

PhenolBPA

Chlorine

COPhosgene

PCCaustic

Soda

Solution

(NaBPA)

September 7, 2004 • Seite 37Business Unit PCS

Quart 4 Quart 1 Quart 2 Quart 3 Quart 4 20052003 2004 2004 2004 2004 Forecast

Benzene 376 467 667 882 776 662

Phenol 700 780 923 1186 1140 986

Acetone 483 578 613 660 661 622

Toluene 363 396 462 506 439 452

prices in €/t

source - CMAI WEU Spot Market prices

Raw Material Pricing Overview

September 7, 2004 • Seite 38Business Unit PCS

Benzene Price History by Quarter (WEU)

Source: ICIS NWE Contract Price

0

100

200

300

400

500

600

700

800

900

1000

86/Q1 88/Q1 90/Q1 92/Q1 94/Q1 96/Q1 98/Q1 00/Q1 02/Q1 04/Q1

Euro

/T

Benzene

Q3 Av. = 872 €

September 7, 2004 • Seite 39Business Unit PCS

Benzene Price History (WEU)

BENZENE WEU C.P. Average

313

365

185

595

213

415

521

0 100 200 300 400 500 600 700

1986 YTD

1999 YTD

lowest Q

highest Q

lowest Yr

highest Yr

Average 1H 2004

high

est &

low

est s

ince

198

6

EURO/T

F2005662!

September 7, 2004 • Seite 40Business Unit PCS

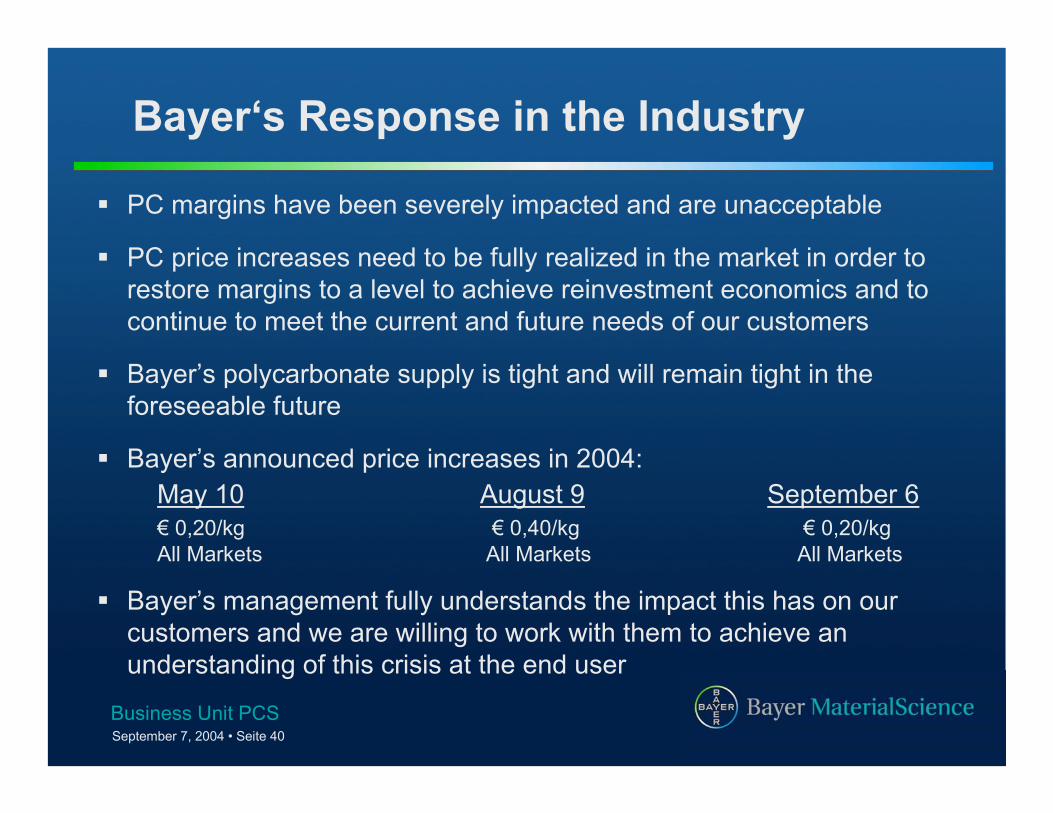

Bayer‘s Response in the Industry

PC margins have been severely impacted and are unacceptable

PC price increases need to be fully realized in the market in order torestore margins to a level to achieve reinvestment economics and tocontinue to meet the current and future needs of our customers

Bayer’s polycarbonate supply is tight and will remain tight in theforeseeable future

Bayer’s announced price increases in 2004:May 10 August 9 September 6€ 0,20/kg € 0,40/kg € 0,20/kgAll Markets All Markets All Markets

Bayer’s management fully understands the impact this has on ourcustomers and we are willing to work with them to achieve anunderstanding of this crisis at the end user

September 7, 2004 • Seite 41Business Unit PCS

Thank you for your attention!

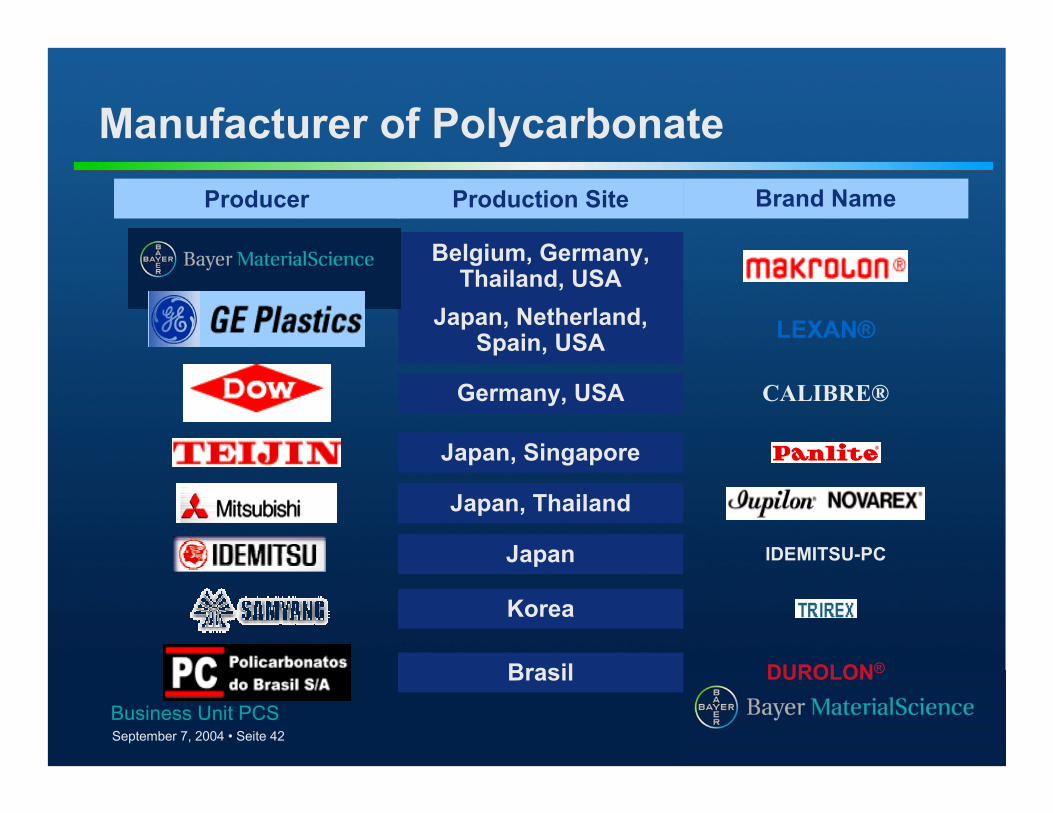

September 7, 2004 • Seite 42Business Unit PCS

Producer Production Site Brand Name

Brasil DUROLON®

Korea

Japan IDEMITSU-PC

Japan, Thailand

Japan, Singapore

Germany, USA CALIBRE®

Japan, Netherland,Spain, USA LEXAN®

Belgium, Germany,Thailand, USA

Manufacturer of Polycarbonate