25

| Date post: | 02-Jul-2015 |

| Category: |

Investor Relations |

| Upload: | vivo-investor-relations |

| View: | 240 times |

| Download: | 0 times |

Vivo Participações S/AFebruary 21, 2008

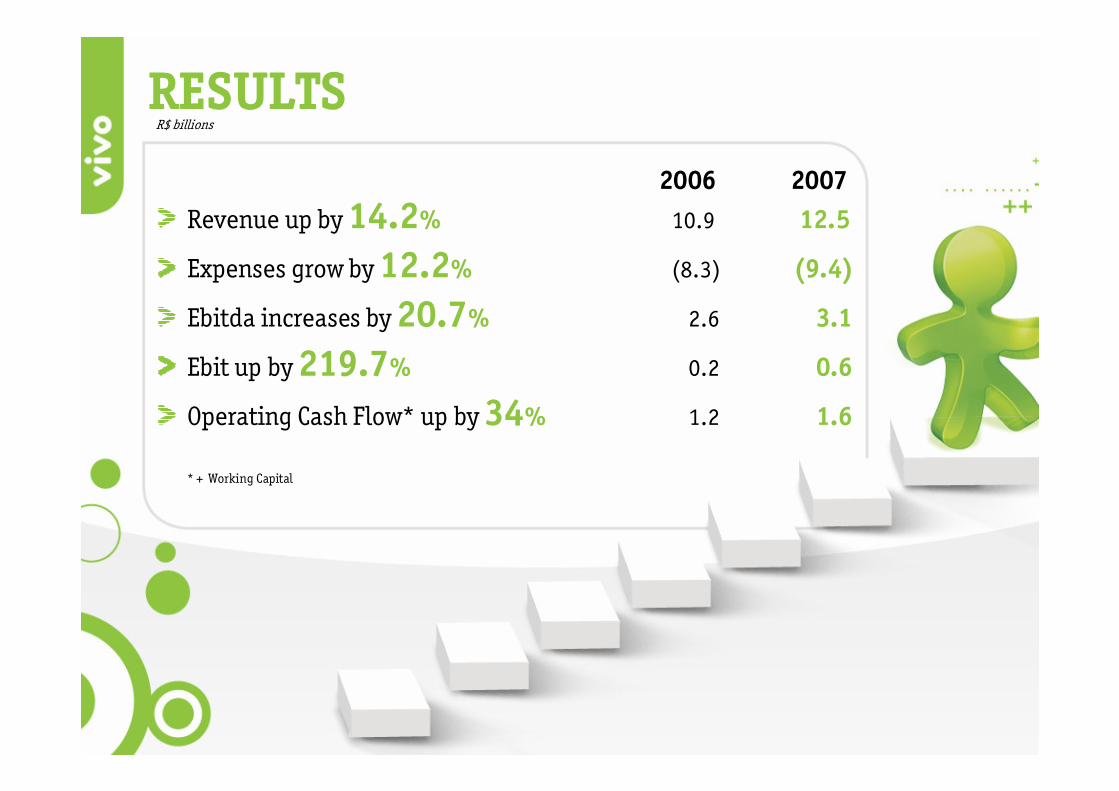

RESULTS

Revenue up by14.2% 10.9 12.5

Expenses grow by12.2% (8.3) (9.4)

Ebitda increases by20.7% 2.6 3.1

Ebit up by219.7% 0.2 0.6

Operating Cash Flow* up by34% 1.2 1.6

* + Working Capital

2006 2007

R$ billions

AgendaOperating PerformanceFinancial Performance

Vivo Participações S/AFebruary 21, 2008

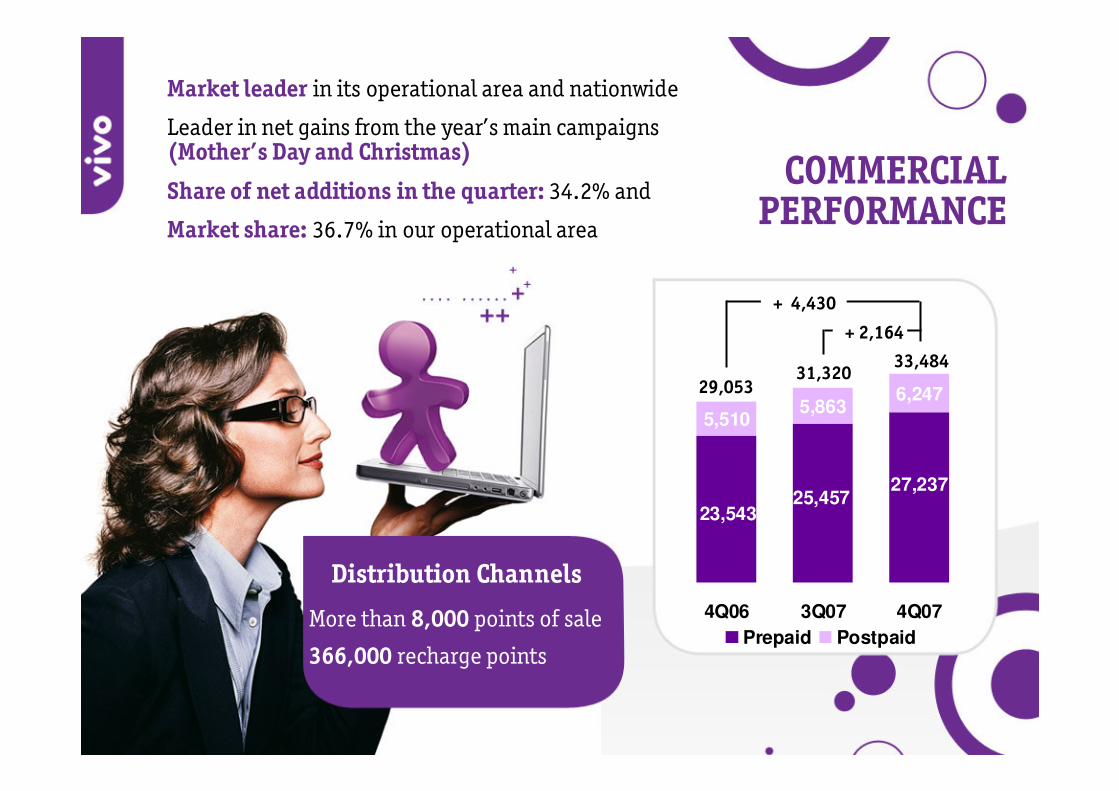

+ 2,164

+ 4,430

33,48431,320

29,053

More than 8,000 points of sale

366,000 recharge points

Distribution Channels

Market leader in its operational area and nationwide

Leader in net gains from the year’s main campaigns(Mother’s Day and Christmas)

Share of net additions in the quarter: 34.2% and

Market share: 36.7% in our operational area

COMMERCIAL PERFORMANCE

27,237 25,457

23,543

6,2475,863

5,510

4Q06 3Q07 4Q07

Prepaid Postpaid

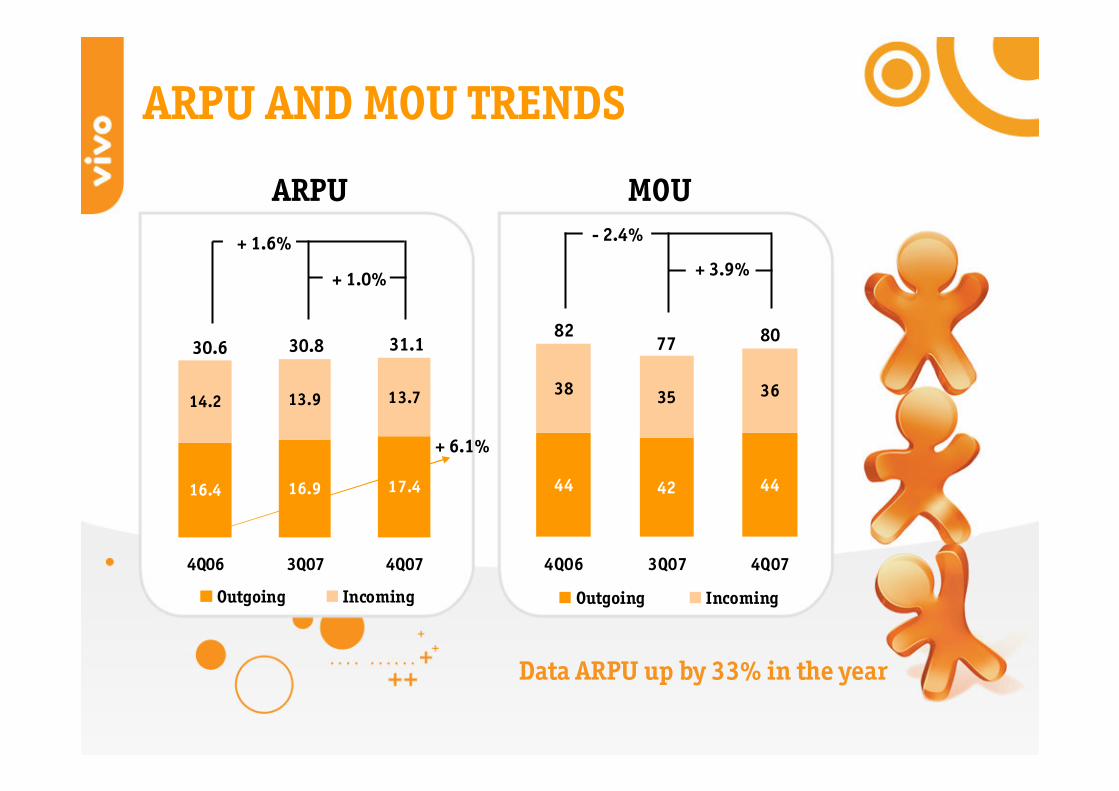

ARPU AND MOU TRENDS

ARPU MOU

+ 6.1%

31.130.830.6

+ 1.0%

+ 1.6% + 3.9%

- 2.4%

44 42 44

38 35 36

4Q06 3Q07 4Q07

Outgoing Incoming

807782

Data ARPU up by 33% in the year

17.416.916.4

13.713.914.2

4Q06 3Q07 4Q07

Outgoing Incoming

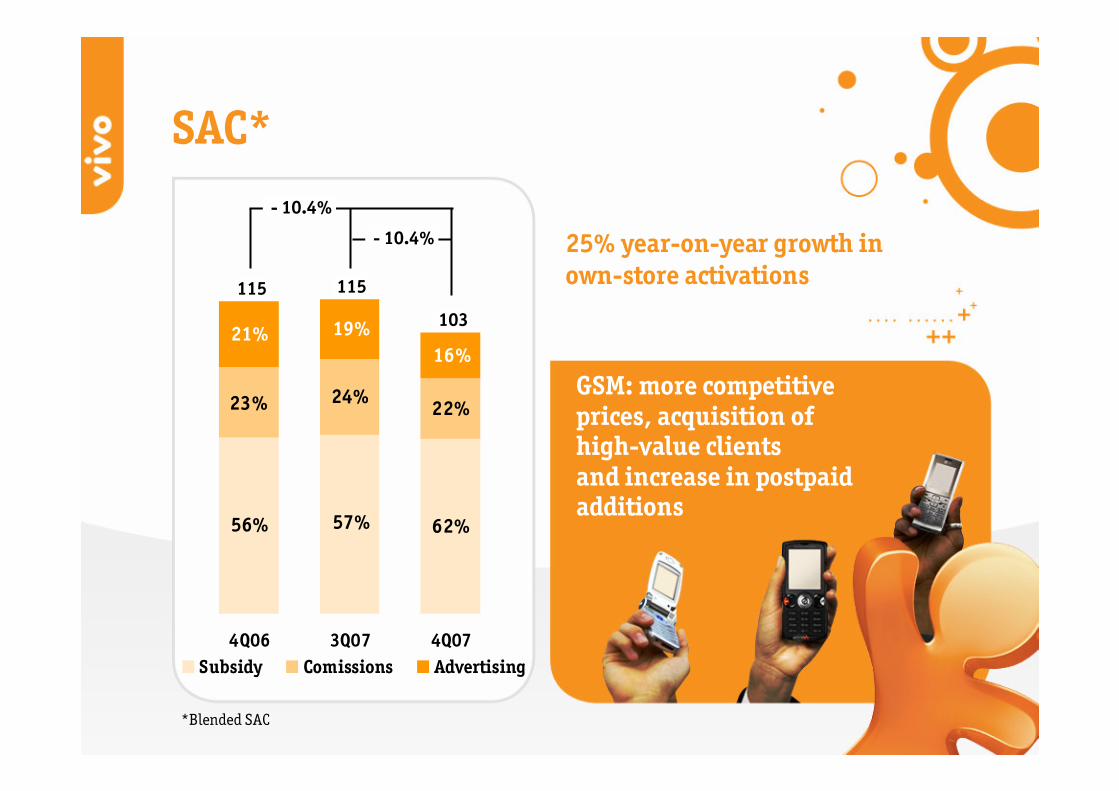

SAC*

GSM: more competitive prices, acquisition of high-value clients and increase in postpaid additions

- 10.4%

- 10.4%

115 115

103

*Blended SAC

25% year-on-year growth in own-store activations

57% 56% 62%

24% 22% 23%

16% 19% 21%

4Q06 3Q07 4Q07Subsidy Comissions Advertising

LOYALTY BUILDING AND RETENTION

InitiativesPoints Program

Customer recapture

Restructuring of plans

Recovery of suspended customers

Alteration of recharge mix

Recharge incentives

Results

2.1% Churn

PRODUCTS AND SERVICES Launch of exclusive partnership with Positivo

Informática, Brazil’s biggest computermanufacturer.

Launch of broadband solutions in the PlanoControle.

Launch of new smartphones: allowing increasedpenetration of the Vivo Smart Mail service in VIVO’s customers base

Increase in interactivity initiatives via SMS

National and international roaming.

More than 400,000 broadband users

More than 4 million Value Added Servicessold in the year, growth of 132%

CUSTOMER SATISFACTION

Vivo ‘s rating is higher thanthemarket average

8.41

8.33

Market Average Vivo

The number of “extremelysatisfied” clients (score of10) grew from 33% to 39%

“How would you rate your operator on a scale of 0 to 10, where 0 indicates that you are extremely unsatisfied and 10 that you are extremely satisfied?”

Source: Total Satisfaction Survey in the 2H07 undertaken by the Instituto GFK

SURVEY

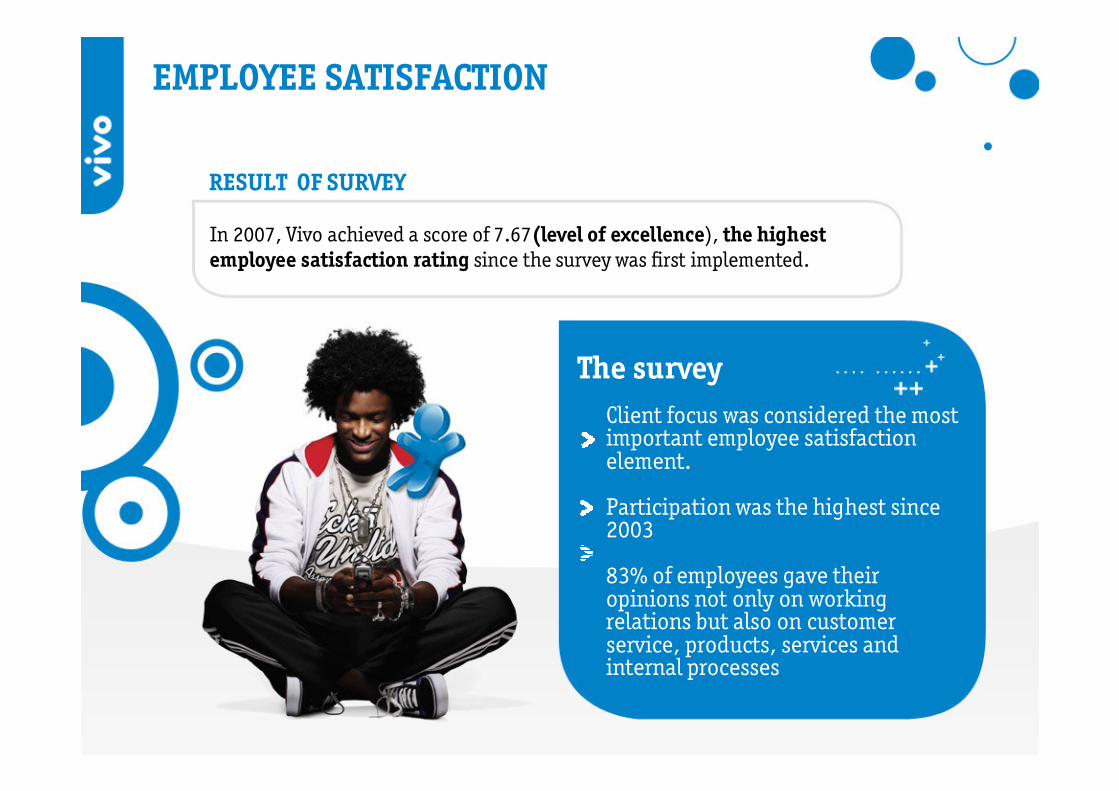

EMPLOYEE SATISFACTION

In 2007, Vivo achieved a score of 7.67(level of excellence), the highestemployee satisfaction rating since the survey was first implemented.

RESULT OF SURVEY

Client focus was considered the mostimportant employee satisfactionelement.

Participation was the highest since2003

83% of employees gave theiropinions not only on working relations but also on customerservice, products, services andinternal processes

The survey

Brand strengthening/repositioning

Acquisition of Telemig, gaining entry to Brazil’s 3rd largest state

Acquisition of 10MHz of additional 1.9 spectrum throughout Brazil, particularly in the 6 states where we had no previous footprint

Acquisition of 20MHz of 2.1 frequencies in all our operational areas.

All this Increase the Company’s capacity to offer the best services of the market

STRATEGIC POSITIONING

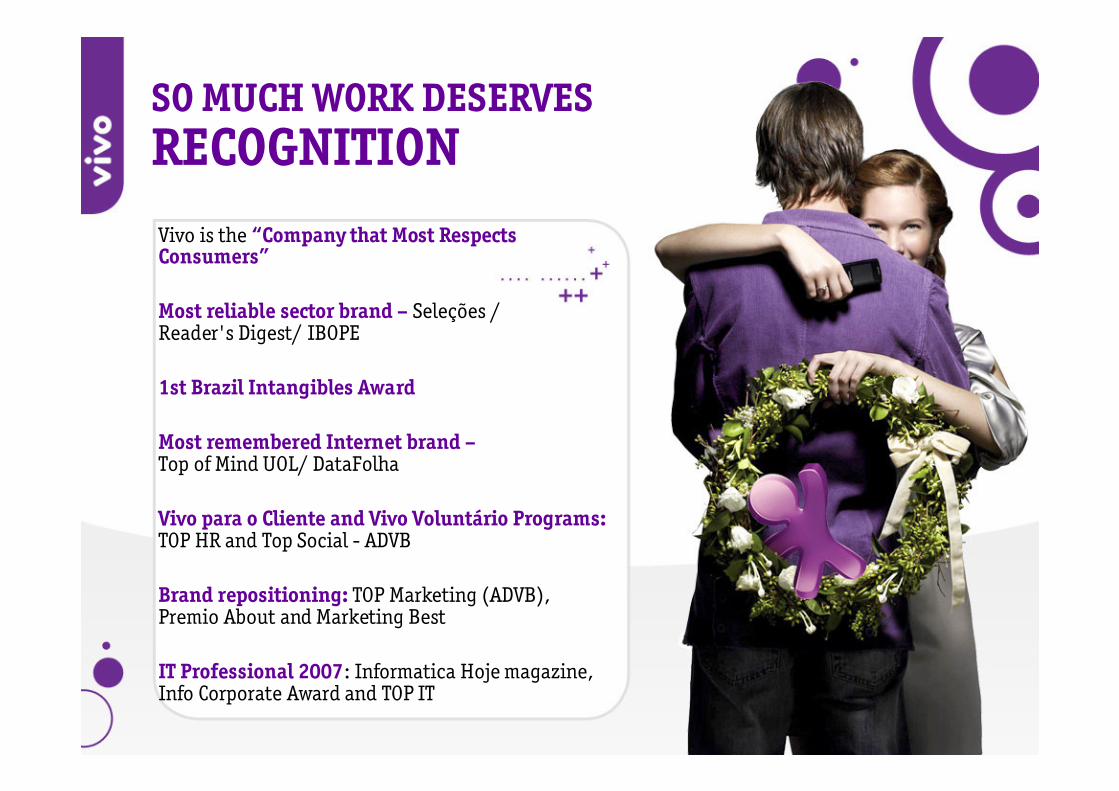

SO MUCH WORK DESERVESRECOGNITION

Vivo is the “Company that Most RespectsConsumers”

1st Brazil Intangibles Award

Most remembered Internet brand –Top of Mind UOL/ DataFolha

Most reliable sector brand – Seleções / Reader's Digest/ IBOPE

Vivo para o Cliente and Vivo Voluntário Programs: TOP HR and Top Social - ADVB

Brand repositioning: TOP Marketing (ADVB), Premio About and Marketing Best

IT Professional 2007: Informatica Hoje magazine, Info Corporate Award and TOP IT

Operating PerformanceFinancial Performance

Agenda

Vivo Participações S/AFebruary 21, 2008

AgendaOperating PerformanceFinancial Performance

Vivo Participações S/AFebruary 21, 2008

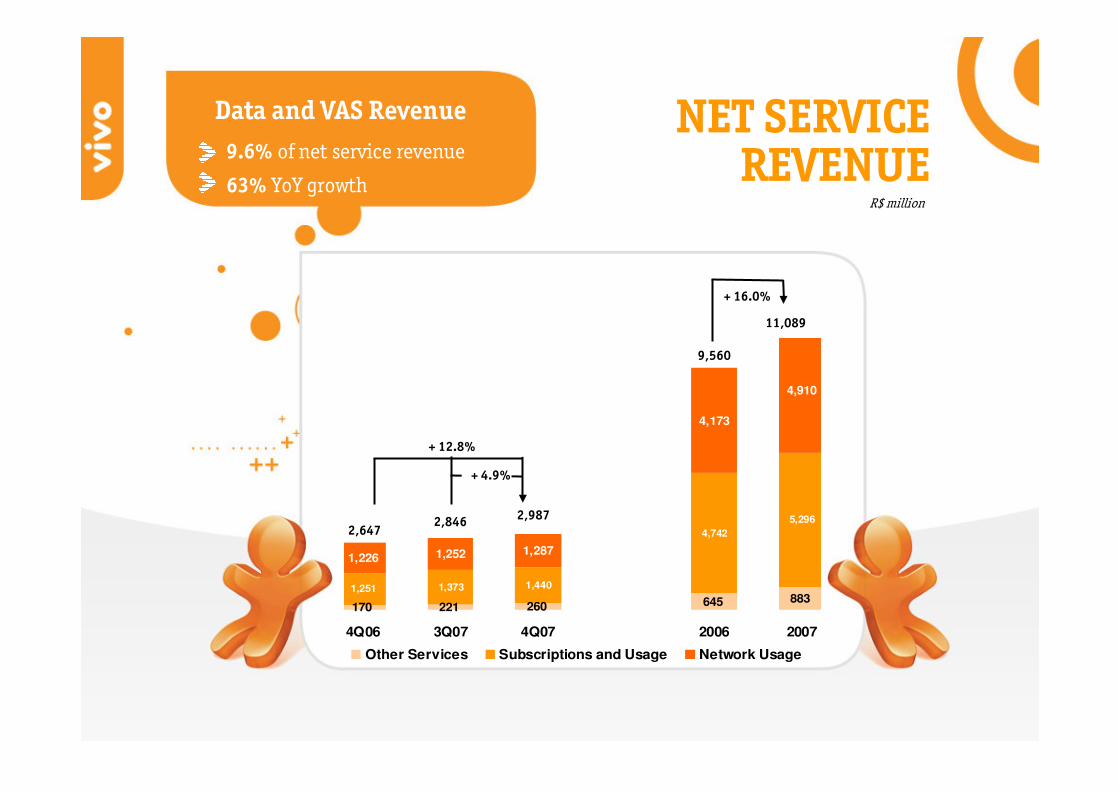

NET SERVICE REVENUE

170 221 645 883260

5,296

1,440 1,3731,251

4,742

1,226 1,252 1,287

4,910

4,173

4Q06 3Q07 4Q07 2006 2007

Other Services Subscriptions and Usage Network Usage

+ 16.0%

9,560

11,089

2,6472,9872,846

+ 12.8%

+ 4.9%

9.6% of net service revenue

63% YoY growth

Data and VAS Revenue

R$ million

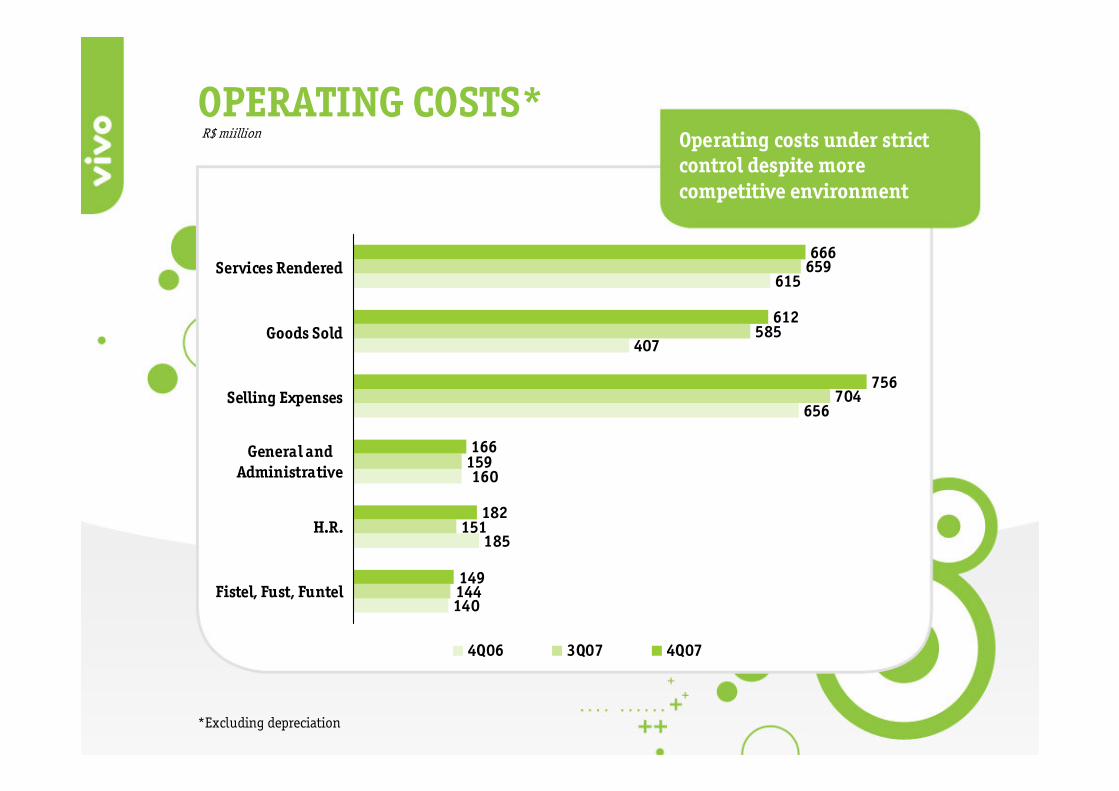

Operating costs under strict control despite more competitive environment

*Excluding depreciation

R$ miillion

140

185

656

407

615

144

151

159

704

585

659

149

182

166

756

612

666

160

Fistel, Fust, Funtel

H.R.

General andAdministrative

Selling Expenses

Goods Sold

Services Rendered

4Q06 3Q07 4Q07

OPERATING COSTS*

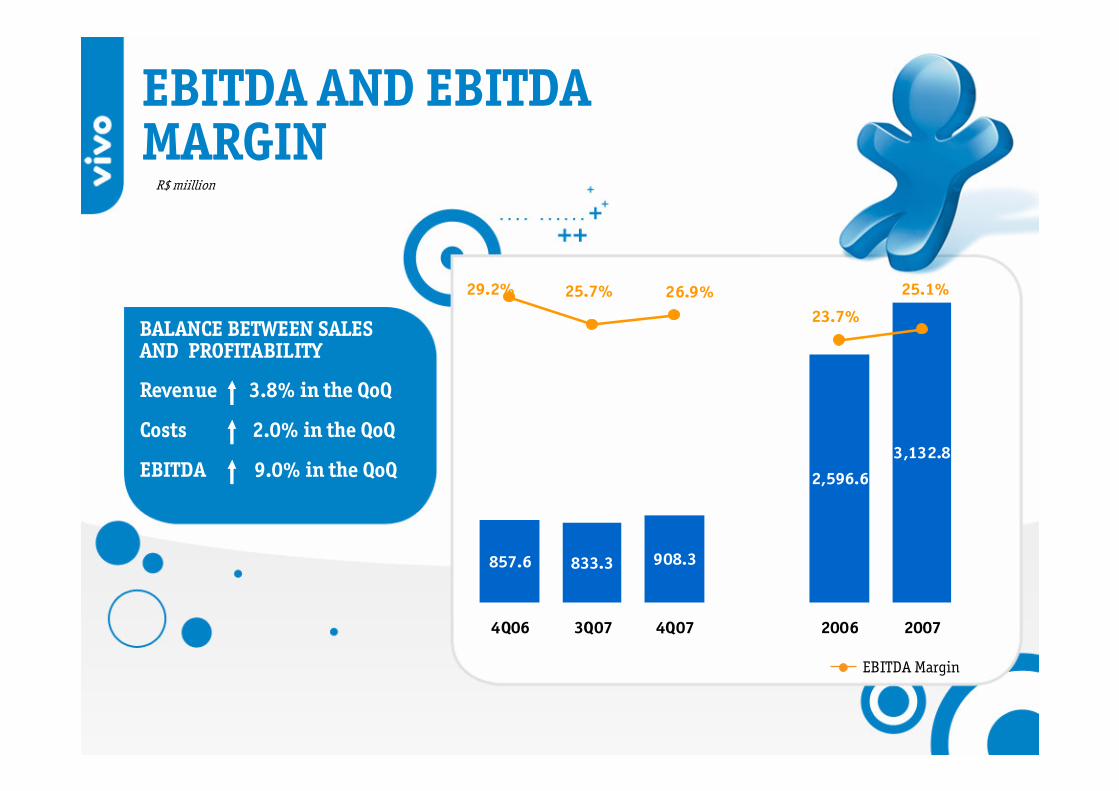

BALANCE BETWEEN SALES AND PROFITABILITY

Revenue 3.8% in the QoQ

Costs 2.0% in the QoQ

EBITDA 9.0% in the QoQ

EBITDA Margin

3,132.8

2,596.6

908.3857.6 833.3

25.7% 26.9%29.2%

23.7%

25.1%

4Q06 3Q07 4Q07 2006 2007

EBITDA AND EBITDA MARGIN

R$ miillion

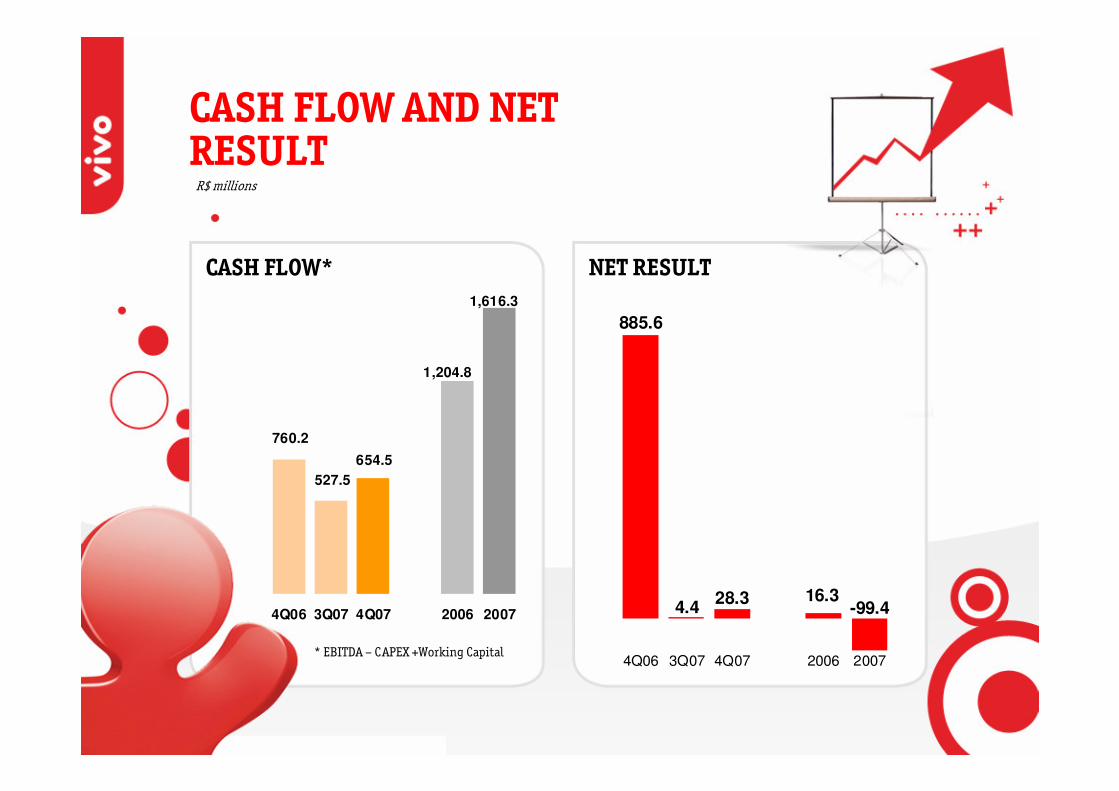

* EBITDA – CAPEX +Working Capital

R$ millions

CASH FLOW* NET RESULT

-99.416.3

885.6

28.34.4

4Q06 3Q07 4Q07 2006 2007

CASH FLOW AND NET RESULT

1,616.3

1,204.8

654.5

527.5

760.2

4Q06 3Q07 4Q07 2006 2007

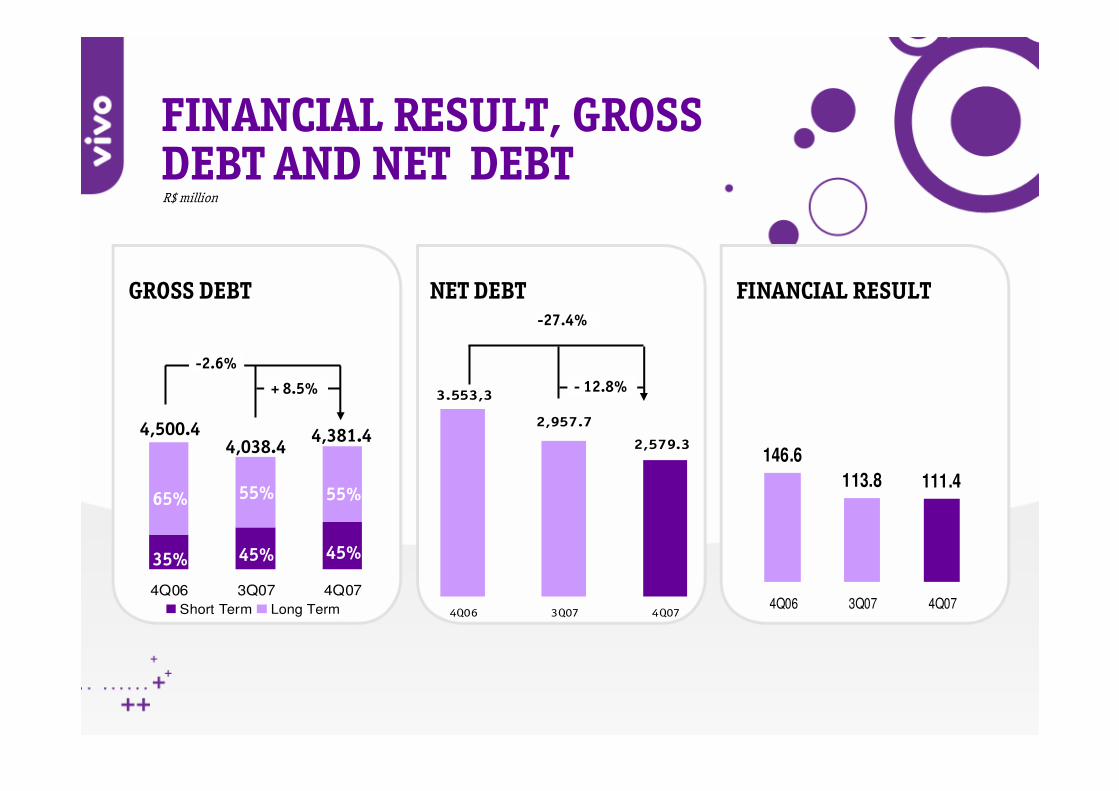

2,957.7

2,579.3

3.553,3

4Q06 3Q07 4Q07

4Q06 3Q07 4Q07

Short Term Long Term

4,038.44,500.4

65%

35%

55%

45%

55%

45%

4,381.4

111.4113.8

146.6

4Q06 3Q07 4Q07

FINANCIAL RESULT, GROSS DEBT AND NET DEBTR$ million

+ 8.5%

-2.6%

- 12.8%

-27.4%

GROSS DEBT NET DEBT FINANCIAL RESULT

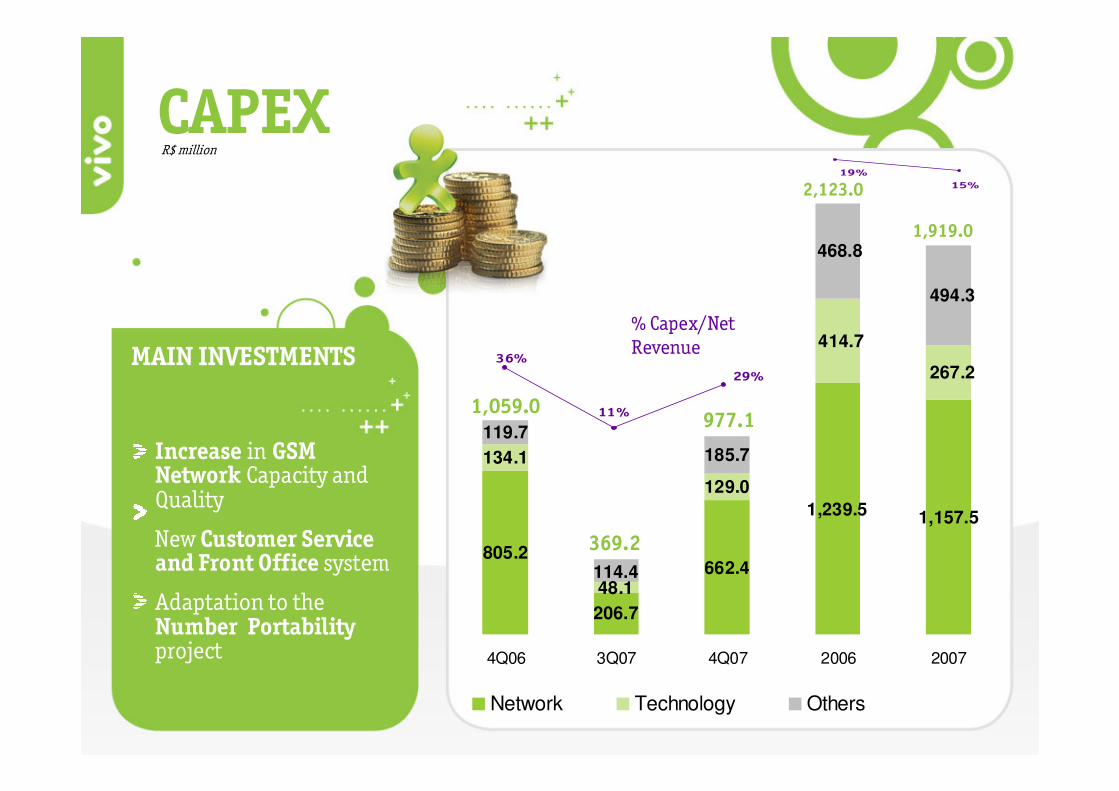

1,157.5 1,239.5

662.4

206.7

805.2

129.0

48.1

134.1

267.2

414.7

185.7

114.4

494.3

468.8

119.7

4Q06 3Q07 4Q07 2006 2007

Network Technology Others

29%

11%

36%

1,059.0977.1

369.2

% Capex/Net Revenue

2,123.0

1,919.0

CAPEX

MAIN INVESTMENTS

Increase in GSM Network Capacity andQuality

New Customer Serviceand Front Office system

Adaptation to theNumber Portabilityproject

R$ million

15%19%

THERE IS ONLY ONE POSSIBLE RESULT OF ALL THIS:

...possesses all the necessaryconditions to ensure its continuousdevelopment in one of the biggest

markets in the world

A COMPANY THAT HAS...

A consistent strategicpositioning with focus on customers

A motivated andcommitted workforce

A highly positive operating and financial performance

DISCLAIMER

• This presentation may contain forward-looking statements concerning future prospects and objectives regarding growth of the subscriber base, a breakdown of the various services to be offered and their respective results. The exclusive purpose of such statements is to indicate how we intend to expand our business and they should therefore not be regarded as guarantees of future performance.

• Our actual results may differ materially from those contained in such forward-looking statements, due to a variety of factors, including Brazilian political and economic factors, the development of competitive technologies, access to the capital required to achieve those results, and the emergence of strong competition in the markets in which we operate.

VIVO PARTICIPAÇÕES S.A.