Volume Seven, Number Two Winter 2005 C ENTER F OR E CONOMIC S ELF -R ELIANCE MARRIOTT S CHOOL BRIGHAM YOUNG UNIVERSITY PROVO, UT of Journal Microfinance S CHOOL OF B USINESS BRIGHAM YOUNG UNIVERSITY–HAWAII LAIE, HI

Transcript

Volume Seven, Number Two

Winter 2005

CENTER FOR ECONOMIC

SELF-RELIANCE

MARRIOTT SCHOOLBRIGHAM YOUNG UNIVERSITY

PROVO, UT

ofJournalMicrofinance

SCHOOL OF BUSINESSBRIGHAM YOUNG UNIVERSITY–HAWAII

LAIE, HI

The Journal of Microfinance thanks the following for their contributions:

The Marriott School at Brigham Young University

The BYU Humanities Publication Center, for editing and production services.Director: Professor Melvin J. Thorne; Student Assistants: Alicia Owings, LuciNielsen, Megan Hale, and Geneil Johnson

Journal of Microfinanceis a joint publication of

The Center for Economic Self-Reliance,Marriott School,

at Brigham Young UniversityProvo, UT, USA

and the School of BusinessBrigham Young University–Hawaii

This will be the final issue of the Journal of Microfinance before it changesits title and focus as explained below. As we mark this transition, we lookback with appreciation on the genesis of the journal. Particular thanks goto Gary Woller and Warner Woodworth for their vision in seeing the needfor a journal that would formalize microfinance as a serious topic of aca-demic research.

This vision of a journal that would open the dialogue between practi-tioners and academics on the topic of microfinance was only realizedthrough the hard work and support of many individuals and institutions.Gary Woller is especially deserving for his efforts as editor in the earliestyears of the journal. He worked tirelessly to create awareness of the Journalof Microfinance, recruiting a strong group of reviewers as well as establish-ing the journal’s reputation among researchers. As a result of his efforts, thejournal reached a point where only about twenty-five percent of articlessubmitted were accepted for publication, putting the Journal of Microfinanceon par with other top journals in the field.

Gary was supported in this effort by the George W. Romney Institutefor Public Management and the Center for Economic Self-Reliance of theMarriott School at Brigham Young University. Additional support camefrom the School of Business at Brigham Young University–Hawaii, bothfinancially and editorially through Beth Haynes, who served as BookReview Editor, while I served as co-editor of the journal.

Of course, additional thanks go out to our fine editorial board, con-sisting of many leaders in the field of microfinance. I also wish to expressgratitude for the fine work of our many volunteer reviewers, who workedhard to ensure the quality of the articles that appeared in the journal.

Finally, to the authors of the research appearing in the Journal ofMicrofinance, I wish to extend my congratulations for having made thejournal into a demanding and innovative publication. Your efforts have ledus all to think about the practice of microfinance in ways that will push themovement forward for years to come. In fact, the journal’s shift from amore narrow focus on microfinance to a broader focus on economic self-reliance is indicative of the lessons we have learned as we have sought bet-ter ways to reduce poverty throughout the world.

Again, I thank all who have been involved in trying to make this worlda better place through the use of microfinance. Your work continues to bevaluable in the push toward greater economic self-reliance and will find a

welcoming home in the new publication, Advances in Economic Self-Reliance.

Norman WrightEditor, Journal of Microfinance

With the next issue, the name, focus, and format of the Journal ofMicrofinance will change—the new name will be Advances in Economic Self-Reliance. In March of 2003, the Center for Economic Self-Reliance was for-mally established at the Marriott School of Management at Brigham YoungUniversity. The Center was founded on a vision of improving the economicself-reliance of individuals and families around the world by bringingresearchers, practitioners, and donors together through action research.

Microfinance deals with the provision of financial services to the poorto establish and sustain microenterprises, thus improving their earningcapabilities. As such, the principles and practices of microfinance representone important vehicle through which people can improve their economicself-reliance. Economic self-reliance is a broader concept that includes edu-cation, work within traditional employment relationships, principles ofpersonal prudence and discipline such as budgeting or resource manage-ment, and concerns such as risk management through social networks orinsurance. Each of these components, coupled with individual initiative,works to create or improve self-reliance. The name change of the journalsignifies our willingness to publish articles on these important broadertopics as well as continuing to support microenterprise efforts.

The focus of the journal will be broader than before, and the writingstyle and article selection policies will change as we attempt to reach out topractitioners and donors as well as researchers. The initial issues willinclude pieces from thought leaders in the area of economic development,a theory article that outlines new and important concepts in the field, aresearch and case study section, a short description of best practices in theareas of self-reliance or NGO organizational management, and a bookreview. We expect the format and content of the journal to evolve as webetter understand and model the processes of economic self-reliance. Weinvite you to evolve with us and hope you will continue to see this publi-cation as valuable to your efforts to build a better world.

Paul C. GodfreyEditor, Advances in Economic Self-Reliance

SUBSCRIPTIONS AND SUBMISSIONS

Journal of Microfinance (ISSN 0360-151X) is published semiannually byBrigham Young University. Second-class postage paid at Provo, Utah, and atadditional mailing offices. Postmaster: please send address changes to Journalof Microfinance, 712 TNRB, Marriott School of Management, BrighamYoung University, Provo, UT 84602.

2006 Subscriptions: The subscription rate for subscribers in the U.S. andCanada for two issues of Advances in Economic Self-Reliance is the following(in U.S. Dollars):

Add $10 for non-U.S./Canada hard copy or combination subscriptions.Please send all correspondence regarding subscriptions to [email protected] Journal of Microfinance, 712 TNRB, Marriott School of Management,Brigham Young University, Provo, UT 84602; call (801) 422-9009; or visit usonline at http://www.microjournal.com.

Submissions: Since Advances in Economic Self-Reliance is a practitioner-oriented journal, we welcome article proposals dealing with various aspects ofself-reliance from thoughtful practitioners, researchers, and donors. Pleaseemail a one page article proposal to the editor at [email protected] to begin thesubmission process, or mail your proposal to: Advances in Economic Self-Reliance, BYU Center for Economic Self-Reliance, 712 TNRB, Provo, UT84602.

Content: Views expressed herein are to be attributed to their authors and notto Journal of Microfinance or Brigham Young University unless otherwiseindicated.

Copyright: Except as otherwise noted, Journal of Microfinance is pleased togrant permission for copies of articles to be made for classroom use, providedthat (1) a proper notice of copyright is affixed to each copy, (2) the author andsource are identified, (3) copies are distributed at or below cost, and (4)Journal of Microfinance is notified of the use.

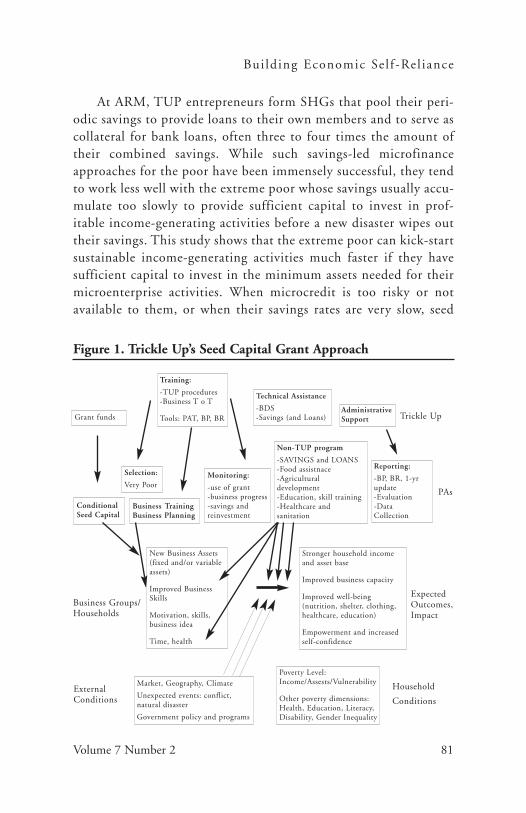

Asubstantial track record of accomplishment and a significantbody of empirical studies worldwide together underline thesignificance of microfinance as an effective antipoverty and

development strategy (Wright, 2000; Zaman, 2000; Khandker,

A Case from India

K. K. Kaushal and J. C. Kala

Abstract: India has embarked upon a community involvement process to restock

the state-owned forests through a recent approach called Joint Forest

Management. But the success of the Joint Forest Management program lies in

the provision of alternative livelihoods to woodcutters and grazers. This article

presents how the forest department of a southern state of India devised a potent

tool of microfinance promotion for weaning those who are dependent on the

forest by implementing a massive externally aided Joint Forest Management

Project. Based on a study of 27 program villages in the Tamilnadu state, this

paper proves that the success of Joint Forest Management is dependent on and

directly linked to the provision of microfinance to villagers through a people’s

representative body—the Village Forest Council. The forest department was suc-

cessful in this unusual task of promoting microfinance even in villages where

formal microfinance institutions have failed, which corroborates an earlier find-

ing that microfinance is more workable and successful if it is properly packaged

in a locally suitable development program.

Journal of Microf inance

Volume 7 Number 22

2001). However, even a well-designed microfinance program isunlikely to have a positive impact on the poorest unless it specifi-cally seeks to reach them through appropriate product design andtargeting (Wright, 2000). It is clear from various reports that thereare strong potential synergies between microfinance and the provi-sion of basic social services to clients. However, the services providedneed to be relevant to the needs of the target groups and not just anadd-on that is of poor quality (Marcus, Portes, & Harper, 1999).

Of the 63.72 million hectares (ha) of actual forest area of India(most of which is state owned) almost 38% is degraded, with acanopy density1 of less than 40% (FSI, 2000). This degradation offorests is mainly ascribed to the rigid state control and the result-ing disempowerment and displacement of indigenous tribal andhill communities, accompanied by the disintegration of community-based resource management (Fernandes & Menon, 1987; Guha,1991; Kelkar & Nathan, 1991; Gadgil & Guha, 1992).Consequently the Government of India made a major policy shiftin 1988 and switched over to Joint Forest Management (JFM).JFM is an evolving policy-based program, which sets out to estab-lish management “partnerships” between local forest-dependentcommunities and the state for the sustainable management andjoint benefit-sharing of public forest land (Sarin, 1995). To accom-plish this, JFM seeks to shift the existing inequitable distributionof management control by directly involving local people andinstitutions in forest management (Campbell, 1996). JFM doesnot involve the transfer of ownership over forests, but attemptsinstead to restructure the formal system of access, decision-making,and sharing of benefits to account for the needs of local communi-ties. So far, 22 state governments have issued orders to implementJFM and the states have evolved their own mechanisms of involv-ing local communities in conformity with the proclaimed policy.

K. K. Kaushal is Deputy Conservator of Forests in Madurai District of Tamilnadu State for theIndian Forest Service. Email: [email protected]

J. C. Kala is Principal Chief Conservator of Forests, Tamilnadu State Government, IndianForest Service. Email: [email protected]

Nurtur ing Joint Fores t Management

Volume 7 Number 2 3

About 36,130 Village Forest Councils are managing a total of10.25 million ha of forest area in the country (FSI, 2000).

It is a known fact that during the last 140 years of state con-trol, most of the land with the potential for agriculture was clearedof forests. The remaining forest in India is now concentrated inrugged and inaccessible areas, and this reduces the potential to har-vest and manage the forest for production purposes. The abuttingpopulation has increased manifold; their needs have also multi-plied. It is impossible to create forest-based livelihoods for all theabutting population. Consequently, most of the states are follow-ing a two-pronged approach to involve communities: increasingthe stake of the neighboring communities in the management andutilization of the forests, and creating alternative sources ofemployment to reduce the pressure on forests (Kumar, Naresh,Yogindra, & Kinsuk, 2000). But the resources to promote alterna-tive income are limited and cannot wean all forest dependents(Kaushal & Kala, 2004). However, if the limited available fundsare used for the creation of a revolving fund for microfinance pro-vision instead of providing doles to a few individuals, then theimpact can be larger and more sustainable also.

This paper seeks to present how microfinance as a componentof the Joint Forest Management project has emerged as a potenttool for the development of forest villages in Tamilnadu and isreducing people’s dependence on forests to nontimber forest prod-ucts and indirect benefits. Further it substantiates with field datathat the regeneration of forests is directly linked to the successfulworking of microfinance.

Tamilnadu Forestry Project

Tamilnadu, the southern state of India, has a geographic area of 13million hectares, which constitutes 3.96% of the land area of thecountry. The total population of the state is 55.86 million (1991census), accounting for 6.60% of the country’s population. Therecorded forest area2 is 2.26 million hectares, which constitutes17.40% of the land area of the state. But the actual forest cover3

as assessed through remote sensing is only 1.71 million hectares—a mere 13.13% of the land area. Furthermore, half of this actual for-

est cover is degraded and has a canopy density of less than 40%(FSI, 2000).

There are 15,822 villages in the state, of which 1405 are forestabutting. The total population of these forest villages is estimatedto be 3.11 million. No separate consumption or income data areavailable, but it is a known fact that forest communities are thepoorest of the poor (Tiwari, 1994; Kaushal & Kala, 2004). Becauseof remoteness and a thin and scattered population, modern develop-ment and amenities have not reached them. Moreover, the devel-opment departments hardly reach these areas. Likewise, thecooperative banks and grameen banks restrict their operations tothe villages in the plains, which have more productive lands thatallow their people to make gainful use of loans.

The Tamilnadu Forestry Project (TFP) is a Joint ForestManagement (community forestry) Project that is funded by theJapan Bank for International Cooperation at a level of US$100million.4 This project has been implemented in Tamilnadu statesince 1997–98. In the Project, degraded forest microwatersheds alongwith abutting habitations are selected. The forest area is divided intothree zones—Lower zone or Utility zone, Middle zone or Asset cre-ation zone, and Upper zone or Eco-restoration zone. Normally, thearea for all three zones is 250 ha, in which the zone-wise gap plant-ing is taken up. The unique feature of the Project is that it has aprovision of $12,000 for the development of abutting village pop-ulation over a period of three years. The aim is to reduce thedependence of villagers on forests by initiating alternate activitiesfor generating income.

In each of the identified management units, the people’s repre-sentative body, called a Village Forest Council (VFC), is formedwhich is fully involved in the planning and execution of works, pro-tection, harvesting, and benefit sharing, with focus on degradedforests. One man and one woman from each household, providedthat they are willing, are enrolled as its members. Any person whoopts out from the membership of VFC is not entitled to any benefits.The VFC meets as and when called for, but in any case at least oncein three months.

Journal of Microf inance

Volume 7 Number 24

Nurtur ing Joint Fores t Management

Volume 7 Number 2

Each Village Forest Council elects an Executive Committee,with each hamlet electing at least two members; each VFC elects aminimum of 5 and a maximum of 15 members to the ExecutiveCommittee. The panchayat5 members of the management unit areco-opted as ex-officio members of the Executive Committee (EC).The members of the Executive Committee elect a President fromamong themselves who is also President of the VFC. The ForestRanger concerned is the Member Secretary of the ExecutiveCommittee, who facilitates the election of the members andPresident of the Executive Committee. The Executive Committeeis responsible for the day-to-day activities of the VFC and meets atleast once a month. A Memorandum of Understanding is signed inthe beginning between the Divisional Forest Officer (on behalf ofForest Department) and the VFC President. This gives the detailsof the roles and responsibilities of the Forest Department andVFC—the partners in Joint Forest Management. All the VFCshave been registered under the Societies Registration Act 1975.

The government order sanctioning funds from JBIC soft loandefined the objective of the program as increasing the tree coverthrough the involvement of people. But once the program waslaunched, it was continuously reviewed, modified, and broadenedin consonance with the feedback from the people and the fieldofficers. The amount for development of forest dependents wasincreased to $12,000 from $6000. The individual grants were con-verted into interest free loans so that the VFC can build up itscorpus fund and extend loans to the remaining forest dependentsfor acquiring productive assets. The VFC President was made thejoint signatory for the withdrawl of funds and the submission ofaccounts. State Government ordered the involvement of all otherline departments, like Public Works Department, Electricity,Health, Agriculture, Animal husbandry, and Tribal Development,etc., for the holistic development of these microwatersheds on apriority basis. Thus the Project has come to acquire a multidisci-plinary approach in which the promotion of microfinance plays thelead role.

5

TFP and Microfinance

Each VFC opens an account with the nearest post office and bank,which account is jointly operated by the President and MemberSecretary. Income from the following sources accrue into thataccount:

1. Fines imposed for offenses (like grazing or illicit removal)in the JFM area.

2. Recovery of loans.

3. Income from the sale of nontimber forest products6

(NTFPs).

4. Membership fees.

Out of $12,000 meant to be spent on the buffer zone in eachvillage, about 30% is spent on village development and communityassets like threshing floors, community halls, etc. The remainingamount is given to individuals for acquiring productive assets.Soon after the launching of the Project, this amount was declaredas a loan, which individuals have to pay back to the VFC so that itcan give loans to other people, as well as later further assistance tothe same individuals. In fact, this buffer zone amount is the majorsource of VFC fund, as income from the sale of NTFPs will takemany more years to be significant.

Presently, extending credit is the main financial activity of theVFC. But the term microfinance has been applied to the VFC becauseit arranges insurance for the cattle purchased through its loans. SomeVFCs have also taken group insurance policies for their members.Further, NTFP sales are done by the VFC only.

Methodology

Study Area

There are 48 field-level implementing units called Forest Divisionsin Tamilnadu State Forest Department which have been imple-menting TFP. Plantation Division, Madurai is undertaking TFP

Journal of Microf inance

Volume 7 Number 26

Nurtur ing Joint Fores t Management

Volume 7 Number 2

implementation in Madurai and Theni districts of TamilnaduState. So far 27 villages have been brought under the Project in thisdivision and this study was conducted in the 27 villages of thePlantation Division, Madurai.

Procedural Description and Results

Data regarding the financial position and recycling of money werecollected from the records of each VFC, since each VFC maintainsthe loan disbursement and loan recovery registers and cashbook.Recovery and recycling were separately rated on a scale of 0 to 1. Ifloan recovery for the village showed 100% recovery, we gave it avalue of 1, and if loan recovery was less, then the decimal valuecorresponding to the loan recovery percentage was assigned. Foranalyzing recycling, evaluation considered whether the funds afterrecovery were kept in a bank account or given as fresh loans to newindividuals within a reasonable period, with a value from 0 to 1assigned. We allowed a period of 1 month and an accumulation ofup to Rs 50000 for giving fresh loans. As per expectations, the val-ues were almost the same as the better recovery villages for earlydisbursal. The average of loan recovery and recycling values wastaken to arrive at the value of the combined parameter of loanrecovery and recycling.

Then a team of three Forest Range Officers assessed the protec-tion and regeneration status of each program area. Better protectionthrough effective social fencing was reflected in the growth ofplanted seedlings, the regeneration of existing rootstock, and theabsence of goat or cattle dung on the forest floor. The team per-ambulated the forest area of each of the 27 forest villages to assesthe protection and regeneration status and independently rated thesame on a scale of 0 to 1. The average of the ratings assigned bythe three rangers was taken as the value of forest protection statusfor the respective villages.

Data regarding the financial position of each village is pre-sented in Table 1, which shows the year of the formation of theVillage Forest Council, the amount extended as loan, along withthe ratings of the VFC fund and forest protection.

7

Table 1: Village Forest Councils’ Fund Working as of 31-03-2004 inPlantation Division, Madurai, India

Year S. No. Name of Total Rating of Rating ofTFP Village Loan Loan Recovery Forest and

given and Recycling Protection (0 to 1 scale) Regeneration

Income from fines, membership fees, and NTFP sales is almostnegligible in all the villages and has not been shown. The mainsource of VFC funds is the amount given by the department toindividual beneficiaries for alternative income promotion, whichthey pay back to the VFC concerned. Most of the loans are for pur-chasing hybrid cattle, because cattle rearing comes naturally tothem, and if a village has 20 cattle, the milk procurement societygets started at the nearest road head. Hybrid cattle are notamenable to grazing and have to be stall-fed. They yield 10–12litres of milk per day in comparison to 1–2 liters from indige-nously bred cattle. In some cases artisans have taken loans toimprove their profession. In Rangarampatti village, people havetaken up iron file making, and as many as 102 men and women aregainfully engaged in that trade (Kaushal, 2004). The forest depart-ment has not imposed an alternative income generation activityand the people decide on their own. Almost all the successful VFCshave voluntarily imposed an interest rate of 1% per month on allthe loans given by them. For instance, in Naurjinagar village onlyRs 4 Lakhs was given from the project fund, but with 1% permonth interest, the total amount has grown to Rs 7.5 Lakhs. Ascan be seen in columns 5 and 6 of Table 1, there is a direct corre-spondence between the VFC fund working and forest protection;this shows that once the people get alternate livelihoods they neednot do woodcutting and consequently forest protection improves.In the villages where loan recovery is poor, the remaining forestdependents could not be provided with productive assets and theycontinue to indulge in the grazing of goats or the removal of fire-wood from the forest. In successful villages, the people receivedloans two times and are therefore able to engage themselves in othervocations. The social fencing of the forest area is complete in suchvillages and there is no reason why it should not sustain itself infuture. The concept of Joint Forest Management hinges on socialfencing, which means the local people agree through their localinstitutions and mechanisms not to indulge in grazing and wood-cutting and to ensure that others also comply with it.

9

The VFC President handles the loan collection and only incase of default is persuasion by the VFC members and forest staffadopted, because most of the people do not have collateral securitiesand even when they do, the tedious legal process of loan recoveriescannot be pursued by the VFC President or Member Secretary.Since the Forest Ranger enjoys a tremendous amount of respectand fear in forest villages, his persuasive role, if enacted sincerely,is enough to keep people paying on their loans even in villageswhere formal financial institutions have failed.

The results are the poorest in 1997–98 villages, because theProject was launched hastily and initially loan recovery was notenvisaged. Only in February 1998 was it announced that individualbeneficiaries have to pay back the loan amounts to the concernedVFCs. The results are better in recent years due to better interesttaken by a fresh set of Rangers in the latter years. Nurturant style ofForest Ranger is more successful in JFM (Rishi, 2003). Also, theDepartment personnel have learned the technique of fosteringthe VFCs in the latter years.

The efficient working of a VFC fund is reflected not only inforest protection but also in the improvement of the living stan-dards of the people, as evidenced through the increase in thenumber of concrete houses, people switching over to the use ofcooking gas from firewood, number of cycles and mopeds, etc.

Conclusions

1. In Joint Forest Management programs, forest regenerationand a profit yield from NTFPs will take years; hence thepeople have to be compensated for the lost opportunitycost of grazing and illicit removal to ensure effective socialfencing of the forests. If properly applied, microfinance isa potent tool in this regard.

2. In Joint Forest Management Program villages, forestregeneration and protection show a direct correspondencewith the working of Village Forest Councils as microfi-nance institutions.

Journal of Microf inance

Volume 7 Number 210

Nurtur ing Joint Fores t Management

Volume 7 Number 2

3. Microfinance is more successful if it is launched as a com-ponent of a development package relevant to the peopleand the area.

4. In forest villages, the Forest Department has more interac-tion and rapport with the people. Hence any developmentinitiative including microfinance implemented by theforest department has a better chance of success.

5. The post-Project sustainability of the program is assuredin all such villages, where microfinance has been wellestablished, because the people need not revert to grazingand illicit woodcutting and can pursue alternative liveli-hoods through microfinance. Also, the Village ForestCouncils in such villages acquire more popularity andauthority, which further helps in forest protection.

Notes

1. Canopy density indicates the extent to which sunlight is prevented from falling

on the ground by tree crowns. Canopy density of 40% and above is taken as dense

forest whereas 10–39% is taken as degraded.

2. Forest areas in all lands statutorily classified as forest, though they may not

necessarily bear tree cover.

3. Forest cover is all lands with a tree canopy density of more than 10%, though

they may not be statutorily classified as forestland.

4. US$1 = 45 Indian National Rupees.

5. The panchayat is the lowest tier of local self-government in India.

6. NTFPs are goods of biological origin other than wood that are derived from

the forests. These include fruits, nuts, tubers, mushrooms, essential oils, medicinal

herbs, spices, resins, and gums.

References

Campbell, J. Y. (1996). The power to control versus the need to use: A pragmatic view

of Joint Forest Management. Common Property Resource Digest, 37 (March

1996), 9–10.

Fernandes, W., & Menon, G. (1987). Tribal women and forest economy, deforestation,

exploitation and status change. New Delhi: Indian Social Institute.

11

Forest Survey of India (FSI). (2000). State of Forest Report 1999, Ministry of

Environment and Forests, Dehradun, India.

Guha, R. (1991). The unquiet woods: Ecological change and peasant resistance in the

Himalaya. New Delhi: Oxford University Press.

Gadgil, M., & Guha, R. (1992). This fissured land: An ecological history of India. New

Delhi: Oxford University Press.

Kaushal, K. K. (in press). Alternate livelihood promotion in Rangarampatty village

through JFM Project: A case study. Kurukshetra.

Kaushal, K. K., & Kala, J. C. (2004). Joint Forest Management in India—Need for

sustainable livelihood approach. International Forestry Review, 6 (1), 13–18.

Kelkar, G., & Nathan, D. (1991). Gender and tribe: Women, land and forests in

Jharkhand. New Delhi: Kali for Women.

Khandker, S. (2001). Does micro-finance really benefit the poor? Evidence from

Bangladesh. Paper presented at Asia and Pacific Forum on Poverty: Reforming

Policies and Institutions for Poverty Reduction, held by the Asian Development

Bank. Manila.

Kumar, N., Naresh, S., Yogindra, A., & Kinsuk, M. (2000). India alleviating poverty

through forest development (Evaluation country case study series). Washington,

DC: World Bank.

Marcus, R., Porter, B., & Harper, C. (1999). Money matters: Understanding microfi-

nance. London: Save the Children.

Rishi, P. (2003). Leading JFM through nurturance: An Indian Scenario. International

Forestry Review, 4 (2), 143–148.

Sarin, M. (1995). Joint Forest Management in India: Achievements and unaddressed

challenges. Unasylva, 26 (180), 30–36.

Tiwari, D. D. (1994). Developing and sustaining non–Tiber Forest products: Policy

issues and concerns with special reference to India. Journal of World Forestry

Resource Mangement 7, 151–178.

Wright, G. A. N. (2000). Microfinance Systems: Designing Quality Financial Services

for the Poor. London & New York: Zed Books Ltd., and Dhaka: The University

Press Limited.

Zaman, H. (2000). Assessing the poverty and vulnerability impact of micro-credit in

Bangladesh: A case study of BRAC. World Bank. Retrieved from

There have been government policies on the role of microfi-nance in the rural development process for more than fourdecades. In the 1960s and 1970s, the policies focused on

the provision of agricultural credit as a necessary support to theintroduction of new, more productive agricultural technologies

A Long-Term Perspective

Henk A. J. Moll

Abstract: The long-term perspective on microfinance starts with a discussion of

three central issues: first, views and policies, with two opposing views: “credit for

target group” and “pushing the financial frontier”; second, the performance of

microfinance institutions measured via two objectives: outreach and financial

sustainability; third, microfinance and rural development. This latter issue is

approached through analyses of the effects of financial services on rural house-

holds and analyses of long term national financial development. Both micro and

macro studies show positive effects of an expansion of savings and lending services,

financial deepening. The negative side of financial deepening, the apparently

unavoidable occurrence of bank insolvancies, is also reviewed. The concluding

section argues that the microfinance sector should be guided by “stability and

expansion”: stability to withstand shocks and to maintain the relationships estab-

lished between rural households and microfinance institutions, and expansion to

include more people within the financial frontier.

Journal of Microf inance

Volume 7 Number 214

that would simultaneously improve farmers’ incomes and feed thenation. Later, the focus broadened to include credit provision tothe rural population engaged in other enterprises, such as trade,handicrafts, and small-scale industry. Presently the internationaldevelopment agenda is dominated by the Millennium Goals, withpoverty eradication heading the list of goals, and with microfi-nance firmly linked to this goal.

The implementation of rural credit policies through financialinstitutions has been debated internationally. What triggered thisdebate was the publication of the “Spring Review,” an evaluationof small-farmer credit programs by USAID in the 1970s (Donald,1976), which made available world wide experience on the achieve-ments and failings of credit programs supported by governmentsand donors. In the 1970s, the discussion shifted from “lack of cap-ital” and consequently “the need for cheap credit,” to “cost-coveringinterest rates” that would enable financial institutions to continueto operate (Adams & Von Pischke, 1992). Later, the discussionwidened to include imperfect information as one of the distinctivecharacteristics of rural credit markets (Hoff & Stiglitz, 1993) thatleads to insight into the screening, monitoring, and enforcementproblems that rural microfinance institutions face. Presently we seea sort of consensus about the operations of microfinance institutions:they should strive towards both outreach and financial sustainability.

The debate on microfinance largely assumes a micro perspec-tive, with a short- to medium-term horizon. From this perspective,assumptions about the behavior of farmers, the rural population,or the poor, and about the constraints these groups face lead topolicies to be implemented by financial institutions. These institu-tions measure the effects of access to finance on their target groupafter a couple of years. Finally, the objective to become financiallysustainable is to be reached in a few years’ time. Long-term analysesof the role of microfinance institutions in rural development arescarce. Mellor (1966) and Timmer (1988) deal in macro terms with

Henk A. J. Moll is associate professor in the Development Economics Group of WageningenUniversity, the Netherlands. Email: [email protected]

Microf inance and Rura l Development

Volume 7 Number 2 15

the role of the agricultural sector in national development and dis-cuss the transfer of people and capital from the agricultural (orrural) sector to the services and industrial sectors in the urbanareas. They do not, however, discuss the mechanisms for such atransfer of capital. McKinnon (1973) and Shaw (1973) deal explic-itly with the development of the financial sector within economicdevelopment and plead for financial liberalization to enable sav-ings to be mobilized, followed by an efficient banking system thatlends to investors with expected high return investments. Morerecently, financial development and the links with economicgrowth and with poverty reduction have been discussed by Kingand Levine (1993) and Li, Squire, and Zou (1998). Though theseauthors make no distinction between the rural and urban sectors,their analyses are relevant for the rural sector too.

The three issues introduced above, views and policies regard-ing microfinance; the operations of microfinance institutions; andthe position of microfinance in rural development, are linked. Inthis article I will discuss these issues and then draw overall conclu-sions regarding the long-term role of microfinance institutions inrural areas.

The reason for focusing on rural microfinance is because thisdiffers from microfinance in urban areas in several ways. The mostobvious difference is that the dominant economic enterprise inrural areas is agriculture, with known seasonality and unpre-dictable climatic conditions. This results in similar cash flowrequirements for many households and in co-variant risk.Additionally, in many rural areas the population is widely dis-persed, which means high transaction costs for clients and possiblylow volumes of services per microfinance location. These aspectsrequire specific attention from microfinance institutions operatingin rural areas, in addition to the general microfinance problem ofhandling financial transactions for the small sums low-incomeclients require.

Views and Policies

Nowadays microfinance enjoys widespread support from govern-ments, development agencies and nongovernmental organizations.The reasons for this support are, however, diverse, and the termmicrofinance is linked with very different views and assumptionsabout the relationship between finance and development. Variousauthors have attempted to classify these views. Krahnen andSchmidt (1994), for example, distinguish four views by tracingdevelopment thinking from the 1950s: capital as the engine foreconomic growth, financing specific target groups, the focus onfinancial systems, and, from the 1990s onwards, the insights fromthe new institutional economics emphasizing the dominant role ofinstitutions in development and with specific views on the pecu-liarities of financial institutions. Robinson (2001) distinguishestwo approaches to microfinance: the poverty lending approach andthe financial system approach. Different views or approaches haveconsequences for the policies shaping the environment of micro-finance institutions, the financial services provided, and microfi-nance institutions themselves. Below I will discuss two opposingviews and their resulting policies. The consequences for microfi-nance institutions and for the role of microfinance in rural areaswill be discussed in the sections that follow.

The two opposing views are: (a) credit for target group and (b)pushing the financial frontier. Based on Robinson’s poverty lendingapproach, the first view is defined in a wider sense, with the poorbeing replaced by any target group. The phrasing of the secondview echoes Von Pischke (1991), who refers to the financial fron-tier as the dividing line between the established formal financialinstitutions with their large-scale business and private clients, andthe majority of the rural population without access to formalfinance.

Credit for target group is the oldest view and can be summa-rized as follows: A specified group of people lacks the capital toundertake certain enterprises that would lead to development. Thegroup of people and their enterprises can be specified to a greateror lesser degree: small farmers, fishermen, market women, or

Journal of Microf inance

Volume 7 Number 216

Microf inance and Rura l Development

Volume 7 Number 2

small-scale entrepreneurs with their respective enterprises in agri-culture, fishing, trade, and industry. The specification of develop-ment too may differ: improved health, food security, povertyreduction, or improvement in general welfare. The perspective onthe financial environment of the specified group is limited: theonly way the target group can access credit is through privatemoneylenders whose interest rates are unacceptably high andwould nullify any positive effect of the credit.

It was this view that led many governments in the 1960s and1970s to provide targeted credit with or without support fromdonors; for example, to enable small farmers to use modern pro-duction technologies, such as hybrid seeds or imported dairy cows.This credit would increase their incomes and provide enough andsufficiently diversified food for the domestic market. The credit fortarget group view is still widespread and nowadays is generally tar-geted at “the poor,” in line with the international attention forpoverty eradication. The micro-credit summit (not microfinancesummit) held in Washington in 1997, for example, advocated pro-viding credit to the world’s poor to enable them to shed theirpoverty. Barrett (2003) mentions targeted microfinance (togetherwith land reform, targeted school meals programs, and subsidiesfor agricultural inputs) as one of the “cargo net policies” that canlift people out of poverty. In short, the credit for target group viewis based on the following two central assumptions:

1. The factor constraining development is capital.2. The target group is unable to mobilize this capital under

acceptable conditions.

The policy implication of these assumptions is straight-forward: lend capital to the target group.

The pushing the financial frontier view developed in the 1970sto the 1990s from an increasing understanding of the financialcapabilities of low-income rural households and the existing formaland informal financial institutions in rural financial markets.According to this view, rural households are economic units thatmake daily decisions about production, consumption, and the

17

resource base under conditions that are characterised by (a) sea-sonality that rules rural economic life, (b) uncertainty about futureproduction and consumption requirements, and (c) income levelsthat are generally not far above subsistence. The decisions arereflected internally in the size and composition of the household’sassets and in the enterprise choice, and externally in the house-hold’s participation as buyer and seller of financial assets in ruralfinancial markets (Moll, 1989).

This sharper focus on rural households was accompanied byinsight into the rural financial markets (Von Pischke et al., 1983),defined as the totality of relationships between buyers and sellersof financial assets who are active in rural economies. Rural finan-cial markets are characterized by having a range of institutions thatare usually divided into formal institutions, such as state or privatebanks, semiformal institutions such as cooperatives and NGOsinvolved in financial services, and informal institutions, ranging fromprivate moneylenders and traders to relatives and friends and groups.Despite the wide range of institutions present, individual rural house-holds generally have access to only some of the institutions and theproducts these institutions provide, as rural financial markets arehighly segmented (Moll, Ruben, Mol & Sanders, 2000).

New, comprehensive explanations for the observed segmenta-tion in rural financial markets have been offered by Bell (1988),Hoff and Stiglitz (1993), and others. These focus on the informa-tion asymmetry between lender and borrower as a central issue incredit provision, with as consequences the absence of credit rela-tionships where information on borrowers was perceived as insuf-ficient, and the failure of government-supported financialinstitutions if these information asymmetries were neglected.

The insights gained firstly contradict the two assumptions ofthe credit for target group view: (a) low-income rural householdscan and do save both in kind and in financial assets through a vari-ety of informal arrangements, and (b) the existing savings capacityin rural financial markets refutes the assumption that capital assuch is the major factor constraining rural development. Secondly,the insights into rural households and the rural financial market

Journal of Microf inance

Volume 7 Number 218

Microf inance and Rura l Development

Volume 7 Number 2

institutions revealed the limitations of the informal financial insti-tutions in mobilizing and storing savings, dealing with co-variantrisk, and transforming small, short-term savings into larger loansof medium-term duration. In this way, these insights revealed anunfulfilled demand for financial services that formal institutionscan address more readily than informal ones:

1. Mobilizing savings together with providing unrestrictedwithdrawal.

2. Short-term lending for working capital, as and whenrequired.

3. Medium- and long-term lending for investments.

The overall conclusion was that rural households would benefitfrom the presence of formal financial institutions with servicesadjusted to their capabilities. The policy implications are twofold:(a) government policy attention for rural finance was vindicated,though not policies with the aim to provide capital, but policies toenable formal financial institutions to intermediate between saversand borrowers; and (b) policies should encourage financial institu-tions to participate in pushing the financial frontier to includenew, low-income rural households as their clients, by tackling theinformation problem through innovative screening, monitoring,and enforcement procedures.

The Performance of Microfinance Institutions

The views and policies described above translate into the operationsof microfinance institutions and thereafter into the assessment oftheir performance. The credit for target group view results in micro-finance institutions that focus on providing loans, generally in spec-ified quantities and possibly provided in kind and earmarked for aspecific enterprise. These loans are provided to the defined targetgroup, to be used to attain the specified development goals. Theloans are generally at subsidized interest rates, as the target group ispoor—in whatever terms poverty is defined. The assessment of theperformance initially focuses on the number of loans provided, orthe number of people who have received one or more loans,

19

because this number of people is assumed to reach the anticipateddevelopment goal. The latter assumption can be tested throughimpact assessment,1 for which elaborate methodologies have beendeveloped. This operational approach can be summed up as “supplyleading finance.” Adams and Von Pischke (1992) are among thosewho have analyzed this approach in detail and shown that govern-ment interference adversely influences lending and causes the basiceconomics of banking to be bypassed. The consequences of thesefailings have been that microfinance institutions incurred lossesand sooner or later ceased operating—but not before destroyingrepayment morale in the population and giving bank staff wrongideas about banking. Most importantly, the target group was onlypartly and temporarily reached, and after the demise of the finan-cial institution was again left without financial services.

Two developments in the 1980s and 1990s changed the situa-tion. The emerging pushing the financial frontier view showed theimportance of permanent financial relationships for rural house-holds, and thereby the permanence of financial institutions. The“cost-covering interest rates” for microfinance institutions (insteadof the subsidized interest rates) advocated by Adams and VonPischke were a major step towards achieving such permanence.Financial sustainability became part of the microfinance discussionand Yaron (1992) made this operational by devising the subsidydependence index with two levels of achievement: operational sus-tainability and financial sustainability, whereby the latter indicatesthe total independence from subsidies. New microfinance institu-tions took on board the increased insight and the attention forfinancial sustainability and used new approaches to reach peoplewho had previously lacked access to institutional financial services.

The emergence and expansion of microfinance institutions wasgreatly facilitated by a second development: financial liberaliza-tion. This meant a reduced role for government in the allocation ofcapital, less interference with banking, and thus new opportunitiesfor banks and microfinance institutions to engage in the centralfunction of financial institutions: intermediating between saversand borrowers. Less interference with banking generally meant the

Journal of Microf inance

Volume 7 Number 220

Microf inance and Rura l Development

Volume 7 Number 2

abandonment of interest rate control on savings and credit, andthat enabled the microfinance institutions to pay attention tofinancial objectives.

By the end of the 1980s, case studies had become available onmicrofinance institutions that had succeeded in reaching low-income households with savings and credit services (Moll, 1989;Patten & Rosengard, 1991; Yaron, 1992) and that showed a widevariety of organizational structures and operations. These casestudies provided the material for comparative analyses and theemergence of “best practices” in microfinance literature. These bestpractices offer a wealth of experience, but as the description of thebackground that shaped the specific institutions is generally lim-ited, these best practices need to be tested, assessed, and adapted tothe individual circumstances.

Presently there seems to be consensus on at least the objec-tives of microfinance institutions: outreach towards low-incomepeople and financial sustainability. Given these two objectives,microfinance institutions must deal with two central issues intheir day-to-day operations:

(a) the information issue: how to establish borrowers’ abilityand willingness to repay; and

(b) the cost issue: how to handle cost-effectively the smallfinancial transactions with a short duration generallyrequired by low-income people.

The first issue requires screening, monitoring, and enforcementprocedures that comply with the specific circumstances of low-income people and that deviate widely from the usual bankingpractices. The second issue requires operating with transactioncosts (including information costs and risk) that necessarily lead tointerest rates that are well above commercial bank rates, but thatare nevertheless still competitive and thus attractive for themicrofinance institution’s clients.

Microfinance institutions generally experience a trade-off intheir operations between the two objectives: a focus on the some-what better known clients who require somewhat larger loans eases

21

the cost issue and brings financial sustainability closer. This,however, leaves the smaller clients outside the financial frontier.Conversely, a focus on new clients with small financial capacitieswho require small loans does bring new clients inside the frontier,but also brings more costs and risk due to an initial shortage ofinformation on the new clients. The consequence is that it is moredifficult to achieve financial sustainability. It is in this trade-offbetween the two objectives that the two views sketched in the pre-vious section have maintained their roles up until today. The creditfor target group view complies directly with the outreach objective,as outreach can be made operational in terms of reaching a specifictarget group. Successfully reaching the target group with loans,possibly measured through impact studies, may easily provide ajustification for slackening the financial sustainability objective byaccepting “structural subsidies” or by postponing the date forachieving sustainability. The pushing the financial frontier viewoffers more opportunity for a better balance between the twoobjectives, as financial sustainability is required to keep low-income people inside the financial frontier. The resulting greateremphasis on financial sustainability may, however, slow the flow ofnew people across the frontier.

The balance between the two objectives often remains hiddenin management decisions on organization, operations, and thefinancial products offered. The consequences of these decisionsare, however, reflected in the annual accounts; whether or notthese are considered acceptable depends on the views of the gov-erning body of the microfinance institution.

Microfinance and Rural Development

No studies have been done on the long-term effect of microfi-nance, most likely due to the relative youth of many microfinanceinstitutions and the generally still limited coverage within theirareas of operation. However, an exploration of studies on theeffects of microfinance on rural households and studies on the roleof finance at national level provides indications of what the long-term effect might be. As a start, an overview of the position of a

Journal of Microf inance

Volume 7 Number 222

Microf inance and Rura l Development

Volume 7 Number 2

microfinance institution in the rural financial market is given inFigure 1.

The potential demand for formal financial services by the ruralpopulation is depicted by the triangular segments. The populationin the lowest income quintile has a demand for saving services andshort-term credit. Higher income quintiles require more types ofservices and a larger volume of these services, with the volumesmeasured along the Y-axis. The position of commercial banks is onthe left: serving the highest income groups with a range of services.Microfinance institutions focus on the population in the lowerquintiles and offer a limited range of services. Over time, success-ful microfinance institutions will reach a steadily increasing shareof the rural population and most likely will expand the range ofservices offered. Commercial banks may also expand their presenceby offering services to somewhat less well-off people. In the longrun we can envision a gradual change from complementarity tocompetition between the two types of financial institutions.

23

Figure 1. Formal Financial Services in the Rural FinancialMarket: Demand and Supply

The effect of microfinance on individual low-income house-holds has been studied through microeconomic impact studies.Three aspects are generally highlighted. Firstly, there is an increasedcapacity to deal with risk through the withdrawal of savings orobtaining credit in the case of an emergency. This may mean thatproductive assets (machinery, inventory, land, livestock) need notbe sold during an emergency and thus that the flow of income isnot interrupted. Secondly, there is an improved management ofconsumption requirements over the year, to maintain adequatelevels of food intake (Pitt & Khandker, 1998). This is of majorimportance, as labor is often the main resource of low-incomehouseholds. Thirdly, opportunities to invest in productive enter-prises increase. These increased capabilities of rural households toproduce, consume, and invest may be reflected only partly in theactual credit and savings relationships with microfinance institu-tions, because reliable access to microfinance forms a potentialthat can be tapped if and when required. This potential may, forexample, mean that the household’s own resources will be utilizedmore fully for production, with access to microfinance being reliedon if there is an emergency.

Extrapolating the effects of microfinance on individual house-holds to rural areas in total gives some idea of the overall conse-quences. The increased individual capacity to deal with shocksreduces the effects of a co-variant shock for the rural population asa whole, at least when a substantial proportion of the population iswithin the financial frontier. Further, increased saving in financialassets means a shift away from storing wealth in assets with zero orlow productivity. The financial savings become available for invest-ment in agriculture, in agriculture-related trade and processing,and in a host of other enterprises with expected benefits for tech-nological progress and rural employment. In a later stage, whenremunerative investment opportunities in rural areas become lim-ited and the volume of savings overtakes the volume of credit,excess capital can be channelled via microfinance institutions andthe national banking system to urban areas where large-scale indus-tries and services offer extensive investment opportunities. In this

Journal of Microf inance

Volume 7 Number 224

Microf inance and Rura l Development

Volume 7 Number 2

way, rural savers will benefit from those investments and the chil-dren of the savers might find the urban jobs they are looking for.

The above process of increased saving in financial assets fol-lowed by intermediation by the banking system and investmentby borrowers has been studied extensively at the national level.In their theory of financial development, Shaw (1973) andMcKinnon (1973) describe this process as financial deepening.This theory was developed in the 1960s when governments usedthe banking system to support investment in their priority sectors(often industry), thereby bypassing efficiency considerations inmany cases and neglecting domestic savings. Since the 1980s, manycountries have shifted policy from financial repression towardsfinancial liberalization, or from shallow finance to deep finance.

The relationship between financial development and economicgrowth at the national level has received renewed attention nowthat databases covering many countries over prolonged periodshave become available. In a cross-country sample of 80 countriesover the period 1960 to 1989, King and Levine (1993) found apositive relationship between financial depth, measured throughfour indicators,2 and economic growth. They also showed thatfinancial development has predictive power for future growth,indicating a causal relationship between financial development andgrowth. Khan and Senhadji (2000) reviewed methodological issuesregarding the relationship between financial development andgrowth and applied these insights to a data set covering 159 coun-tries over the period 1960–1999. Their results are in line with thefindings of King and Levine, and they conclude that financialdepth is an important determinant of economic growth.

The analysis of the relationships between financial develop-ment and economic growth has been expanded to include poverty.Li, Squire, and Zou (1998) studied income inequality in a largedata set from 112 developed and developing countries for the years1947–1994. They found that financial deepening helped reduceinequality and raise the income of the lower 80% of the popula-tion. Honohan (2004) gives a recent overview of financial development, economic growth, and poverty and concludes that

25

finance-intensive growth is empirically associated with lowerpoverty ratios.

The discussion of financial deepening, economic growth, andpoverty cited above considers these issues at the national level.However, the central tenet of financial deepening, a shift to savingin financial assets followed by intermediation by the banking systemand investment by borrowers, has direct relevance for microfinancein rural areas, since providing rural households for the first timewith access to savings and credit through local intermediation isthe core of financial deepening. The effects of financial deepeninggo beyond the individual links between microfinance institutionsand households, because a reduction of the capital locked up inpoorly productive assets and the availability of capital for new,trustworthy clients with productive uses fundamentally affectseconomic relationships in rural areas. Rajan and Zingales (2003),for example, state: “a healthy financial system can be a powerfulanti-monopoly tool, providing the lubrication for the emergence ofcompetitors that can undermine the power of incumbent firms,and the means for poor households and small-scale producers toescape the tyranny of exploitative middlemen.” Microfinance thuspositively affects economic life in rural areas; expanding outreach,enlarging the microfinance oval in Figure 1 to include a substantialproportion of the rural population, will make these effects morevisible.

The review of long-term financial development at the nationallevel also provides a perspective on a potentially negative side offinancial deepening: the occurrence of bank insolvency. Caprioand Klingebiel (1996) give an overview of bank insolvencies in 69countries since the late 1970s. The list includes countries from allfive continents and covers industrialized, transitional, and alsodeveloping countries. A number of countries saw more than onecrisis in the period covered. The crises involved governmentbanks, private banks, savings banks, and rural banks and rangedfrom a few banks to the entire banking sector in a country. Thecosts or losses ranged from less than 1% of GDP to as much as55% of GDP and were borne by taxpayers, savers, or a combina-

Journal of Microf inance

Volume 7 Number 226

Microf inance and Rura l Development

Volume 7 Number 2

tion of both. The factors cited as reasons for the crises range frommacroeconomic factors, through weak incentives for banks to actprudently, to lack of managerial skill and fraud.

The widespread occurrence of national bank crises means thatviewed from a long-term perspective, financial institutions are atrisk irrespective of current apparently stable situations. Formicrofinance institutions this risk has special dimensions. A pos-sible collapse of a microfinance institution in a national bankingcrisis means a loss of savings for their low-income clients, andthis is the more damaging as a financial crisis is usually followedby a period of economic recession. Less visible, but with similargrave consequences, is the loss of the relationship-specific socialcapital built up between the microfinance institution and clients.This social capital cannot be replaced without again overcomingthe information gap and building up new confidence betweenfinancial institution and clients—a costly affair that will takeyears. Finally, in a national banking crisis the government’s pri-orities are usually with the larger commercial banks. These banksare more likely to be rescued in the name of national interest andwith taxpayers’ money than the smaller, less visible, rural micro-finance institutions.

The exploration of microfinance and rural development showsa potentially positive impact of microfinance institutions on ruraleconomic life, as they are the primary vehicles for the process offinancial deepening in rural areas. This process is not without risk,however, as a failure of a microfinance institution, whetherinduced by a national bank crisis or by the institution’s ownactions, will result in a loss of both financial capital and the rela-tionship-specific social capital built up between institution andclient.

Discussion

The foregoing review of views and policies on microfinance andthe operations of microfinance institutions vis-à-vis the position ofmicrofinance in the long-term process of rural development leadsto the conclusions given below.

27

First, the generally accepted objective of microfinance institu-tions—financial sustainability, or independence from subsidies—seems to be outdated. It was certainly relevant in the 1980s and 1990swhen microfinance institutions were struggling into existence.Nowadays, many microfinance institutions are operational and theestablished relationships with clients deserve to be safeguarded. Thisis the more relevant as history has shown that bank crises are therule rather than the exception. The financial objective must there-fore be raised towards financial stability, defined as the ability towithstand financial shocks, whether the shocks come from insidedue to the adverse conditions of clients or from outside, transmittedthrough the financial links with the national economic and finan-cial sectors. Financial stability must be approached from two sides:diversification of the loan portfolio to minimize the negativeeffects of co-variant risks facing the rural population, and buildingup reserves. The latter means making a profit, not as an objectiveas such, but as a requirement for continuation.

Second, outreach in the sense of reaching a more or less nar-rowly defined group is, in the long run, not justified. First, a focuson one group of clients makes a microfinance institution vulnerable,thereby endangering financial stability. Second, a focus on onetype of clients overlooks the indirect positive effects of wider accessto financial services for the rural population as a whole. Therefore,the objective that is beneficial for all rural households in the longrun is expansion towards new clients and the provision of newfinancial services. Profit comes in again for two additional reasons:profitable microfinance institutions are more likely to be able todraw capital from the national market for expansion, and profit isrequired for experiments to include new groups of clients and todevelop new financial products to serve old clients better.

The two opposing views on microfinance, credit for targetgroup and pushing the financial frontier can be united into one newperspective for policy formulation: stability and expansion. Fromthis perspective the first priority is to achieve financial stability tomaintain what has been achieved; the second is to expand towardsnew clients. It is interesting to note that from a long-term perspective,

Journal of Microf inance

Volume 7 Number 228

Microf inance and Rura l Development

Volume 7 Number 2

there is no trade-off between stability and expansion, as financialstability is a necessary condition for an expansion of services.

Government policies that are based on stability and expansionmust support microfinance institutions in two ways. First, they mustpass legislation that allows microfinance institutions to mobilizesavings, to provide credit, and to undertake other services, such asinsurance and money transfers. This combination of servicesresults in economies of scale and scope, which strengthens thefinancial position of individual microfinance outlets and thusallows geographical expansion and financial deepening in ruralareas. Second, prudent regulations are required that buttress thefinancial stability of microfinance institutions in their specificcircumstances.

Notes

This article is based on a paper presented at the International Seminar on BRI

Microbanking System, Bali, Indonesia, 1–3 December 2004.

1. Impact assessment may include an assessment of the effect of credit on clients

as well as a study of the appropriateness of credit services.

2. (1) The ratio of liquid liabilities (M3) of the financial system to GDP; (2) the

ratio of deposit money bank domestic assets to deposit money bank assets plus cen-

tral bank domestic assets; (3) the ratio of claims on the nonfinancial private sector to

total domestic credit; and (4) the ratio of claims on the nonfinancial private sector to

GDP.

References

Adams, D. W., & Von Pischke, J. D. (1992). Microenterprise credit programs: Déjà

vu. World Development 20 (10): 1463–1470.

Barret, C. B. (2003). Rural poverty dynamics: Development policy implications. Paper

presented at the 25th International Conference of Agricultural Economists,

Durban, South Africa.

Bell, C. (1988). Credit markets and interlinked transactions. In H. Chenery and

T. N. Srinivasan (Eds.), Handbook of development economics (Vol. I, pp.

763–772). Amsterdam: North-Holland.

Billah, P. (1984). Report on indigenous savings and credit arrangements in Lombok.

Unpublished manuscript.

Bouman, F. J. A. (1977). Indigenous savings and credit societies in the third world: A

message. Savings and Development, 1(4), 181–218.

29

Caprio, G. Jr., & Klingebiel, D. (1996). Bank insolvencies: Cross-country experience

(Policy Research Working Paper 1620). Washington DC: World Bank.

Donald, G. (1976). Credit for small farmers in developing countries. Boulder, Colorado:

Westview Press.

Hoff, K., & Stiglitz, J. E. (1993). Imperfect information and rural credit markets:

puzzles and policy perspectives. In: K. Hoff, A. Braverman, & J. E. Stiglitz. The

economics of rural organization, theory, practice, and policy. Oxford: Oxford

University Press.

Honohan, P. (2004). Financial development, growth and poverty: How close are the

links? (Policy Research Working Paper 3203). World Bank.

Khan, M. S., & Senhadji, A. S. (2000). Financial development and economic growth:

An overview (IMF Working Paper).

King, R. G., & Levine, R. (1993). Finance and growth: Schumpeter might be right.

The Quarterly Journal of Economics, 108(3), 717–737.

Krahnen, J. P., & Schmidt, R. H. (1994). Development finance as institution building:

A new approach to poverty-oriented banking. Boulder: Westview Press.

Li, H., Squire, L., & Zou, H. (1998). Explaining international and intertemporal

variations in income inequality. The Economic Journal, 108 (446), 26–43.

Mellor, J. W. (1966). The economics of agricultural development. Ithaca: [publisher]

McKinnon, R. I. (1973). Money and capital in economic development. Washington,

DC: Brookings Institution.

Moll, H. A. J. (1989). Farmers and finance: Experience with institutional savings and

credit in West Java. Wageningen: Wageningen Agricultural University.

Moll, H. A. J., Ruben, R., Mol, E. W. G., & Sanders, A. A. (2000). Exploring seg-

mentation in rural financial markets: An application in El Salvador. Savings

and Development, 1(24), 33–54.

Moll, H. A. J. (1994). The performance of banks in rural financial markets. In F. J.

A. Bouman and O. Hospes (Eds.), Financial landscapes reconstructed: The fine

art of mapping development (pp. 71–84). Boulder: Westview Press.

Patten, R. H. & Rosengard, J. K. (1991). Progress with profits: The development of

rural banking in Indonesia. San Fransisco: ICS Press.

Pitt, M. M., & Khandker, S. R. (1998). The impact of group-based credit programs

on poor households in Bangladesh: Does the gender of participants matter? The

Journal of Political Economy, 106(5), 958–996.

Rajan, R., & Zingales, L. (2003). Financial depencence and growth. University of

Chicago, unpublished. Quoted in Khan and Senhadji (2003).

Robinson, M. S. (2001). The microfinance revolution: Sustainable finance for the poor.

Washington, DC: World Bank.

Shaw, E. S. (1973). Financial deepening in economic development. New York: Oxford

University Press.

Journal of Microf inance

Volume 7 Number 230

Microf inance and Rura l Development

Volume 7 Number 2

Timmer, C. P. (1988). The agricultural transformation. In: H. Chenery and T. N.

Srinivasan (Eds), Handbook of development economics (Vol. 1 pp. 275–331).

Amsterdam: Elsevier Science Publishers B.V.

Von Pischke, J. D. (1991). Finance at the frontier: Debt capacity and the role of credit

in the private economy. Washington, DC: EDI Development Studies.

Von Pischke, J. D., et al. (1983). Rural financial markets in developing countries.

Baltimore: Johns Hopkins University Press.

Yaron, J. (1992). Successful rural finance institiutions (World Bank Discussion Paper

No. 150). Washington, DC: World bank.

31

Volume 7 Number 2

Data Standards for Connectingto Commercial Sources ofCapital

Ongoing financial innovations in the microfinance market—equity investments, portfolio securitization, and creditfacilities—demand comprehensive scrutiny of microfi-

nance institutions (MFIs) to ensure that their operational systemsmeet the requirements of such financial instruments. In addition,careful attention must be paid to the value and the quality of thedata MFIs produce.

James Dailey

Abstract: The importance of data interchange between commercial sources of

capital and the microfinance sector is generally acknowledged, if not well

detailed. But microfinance institutions (MFIs) and commercial sources of capital

often need a different depth and breadth of information. As the industry grows

and accesses more commercial capital, there is a need to enable standardized

reporting from multiple MFIs to multiple sources of capital, rather than a pro-

liferation of one-to-one reporting relationships. IT professionals and managers of

microfinance institutions need to recognize this need and push vendors and

industry associations to agree on specific standards of data elements, quality,

and transmission protocols. This paper aims to provide the reader with a grasp

of the issues involved and to recommend a sample set of data standards for MFIs

to use in communicating with commercial sources of capital.

Journal of Microf inance

Volume 7 Number 234

According to an article about financial transparency publishedonline by the World Bank’s Consultant Group to Assist the Poor(CGAP, n.d.),

Only a handful of microfinance providers currently includeenough information to comply with International FinancialReporting Standards (IFRS) and industry-specific disclosureguidelines. Industry-specific disclosure requires certain infor-mation in addition to that required by IFRS to permit a fairassessment of the profitability and asset quality of microfi-nance operations.

The importance of enabling data interchange between com-mercial sources of capital and the microfinance sector has beenunderscored in multiple forums. The microfinance industry needsan estimated US$300 billion to grow to scale. However, this figuremay be too conservative, given that approximately three billionpeople globally do not have regular access to financial services.That number continues to grow.

An analysis of the industry's needs by a group of funders andmicrofinance practitioners shows three related obstacles (personalcommunication, July 28, 2004):

1. Lack of diversified sources of capital for microfinanceinvesting.

2. Lack of sufficient market infrastructure to facilitate efficientinformation and resource flow.

3. Lack of business expertise and capacity among leading MFIsrequired to reach scale.

From these concepts, we can derive broad requirements:• Diversification of portfolio financing by MFIs requires more

sophisticated segmentation of the loan portfolio and loan ser-vicing concepts, better data for regulatory agencies to allow

James Dailey is the Technical Project Manager for Innovations in Microfinance at the GrameenTechnology Center, an initiative of GFUSA located in Seattle, WA. Email: [email protected]

Data Standards

Volume 7 Number 2 35

registered deposit taking, and more customer data to enablethe modeling of the risk profile of any derivative securities.

• The market infrastructure factors that will enable resourcesand information to flow are the ability to send information,the need for data to be understood, and the need to createnorms, audit standards, and mechanisms to comply with therequiremens of rating agencies.

• Organization-wide norms, expressed through systems, are akey part of operational capacity. These systems must alsohave the flexibility to adapt to changing conditions.

This paper proposes an overall strategy to meet the emergingneed for data standards in the microfinance industry. These stan-dards should, nominally, leverage large parts of the existing financialservices standards with some important caveats. However, themicrofinance industry, precisely because it deals with the non-banked, does not always have the same level of information that isfound in the formal sector.

Data standards should cover the following areas:

• Financial reporting, such as those embodied in the MixMarket platform.

• Connections to commercial capital markets (e.g., the securi-tization of portfolio).

• The information needs of credit bureaus and regulatoryplayers.

• Remittances and external payment systems.• Remote transactions and third-party transactions.

The remittance market, which is currently estimated atUS$150 billion annually, is particularly interesting to note as apotential source of capital.

Third-party transactions include connections to global trans-actional systems such as point of sale (POS), automated tellermachine (ATM), credit card, or ACH transactions (an inter-bankautomated clearinghouse system). Such transactional networks typ-ically operate through agreements with regulated banking entitiesin each country, a fast growing market globally. Currently, these

networks are absent in microfinance operations in rural environ-ments, but this seems to be mostly a function of connectivity.

Other reporting standards not covered in this documentinclude those used by credit bureaus and other regulatory or stan-dard financial documents used to evaluate an organization’sstrength.

Microfinance Open Source and Establishing Standards

The microfinance open source project (Mifos) developed byGrameen Foundation USA focuses on integrating data standardsand protocols for financial transactions into an operational system.To maximize the effectiveness of the system and to move towardscommon standards, input from others in the industry is critical,particulary because one effective strategy for pioneering new stan-dards is to encourage partner institutions to adopt them.

Intended Audience

The audience for this paper is composed of those concerned withthe technical interface between the back-office systems used bymicrofinance institutions and those used by banking entities.Vendors of back-office systems for MFIs and the Mifos softwareitself will benefit from having specifications from these importantdata flows.

General Approach

In the context of promoting financial instruments and the infor-mation requirements to enable the aforementioned financialmechanisms, the intent of this report is to look as broadly as pos-sible. Requirements for data standards should reflect currenttrends away from legacy systems in the commercial sector, withtheir strong systems-in-isolation approaches, and toward “market-place” approaches, where interoperability and data exchange arekey drivers. There is probably little need in the microfinance sec-tor to be backwards compatible with legacy systems in the com-mercial sector.

Journal of Microf inance

Volume 7 Number 236

Data Standards

Volume 7 Number 2

There are numerous sources which can be used to determinethe information requirements for back-office systems of microfi-nance institutions. These include work on portfolio managementsystems and financial accountability funded by the World Bank. Asnoted by Dailey and Parekh (2003),

One of the most important kinds of information exchangeconducted at microfinance institutions is basic financialreporting. Many different kinds of financial reports are neededfor the effective functioning of an institution. . . . Thesereports can be intended for a variety of audiences, and encap-sulate different subsets of data for institutional performanceand operations.

The financial reports typically used by MFIs include thefollowing:

• Teller/operational reports guide the teller or loan officer intransactions.