FEDERAL ACCOUNTING STANDARDS ADVISORY BOARD FASAB Statements of Federal Financial Accounting Standards June 2004 SFFAS Nos. 1-25 Interpretations Nos. 1-6 Technical Bulletin No. 2003-1 Technical Release Nos. 1-6 Volume II, Current Text

Transcript

FEDERAL ACCOUNTING STANDARDS ADVISORY BOARD

FASAB

Statements of FederalFinancial Accounting Standards

Consolidated Financial Report of the U.S. Government—C60 53

Deferred Maintenance—D20 68

Entity and Non-Entity Assets—E30 77

Federal Debt—F10 79

Fund Balance with Treasury—F50 85

General Property, Plant, and Equipment—G20 91

Goods Held under Price Support and Stabilization Programs—G40 109

Governmental and Intragovernmental Assets and Liabilities—G60 114

Heritage Assets—H20 116

Human Capital—H60 128

Insurance and Guarantee Programs—I40 135

Interest Payable—I50 150

Inventories Including Inventory Held for Sale; Inventory Held in Reserve; Excess, Obsolete and Unserviceable Inventory—I60 151

Investment in Treasury Securities—I80 160

Land—L10 179

Leases—L20 186

Liabilities—L40 191

Loans and Loan Guarantees—L60 218

Management’s Discussion and Analysis—M10 360

Managerial Cost Accounting—M20 364

Non-Federal Physical Property—N60 417

Non-Recourse Loans & Purchase Agreements—N80 420

Operating Materials and Supplies—O20 423

Other Current Liabilities—O40 430

Page i FASAB: Current Text, Version 2 (06/2004)

Contents

Pensions, Other Retirement Benefits, and Other Post-Employment Benefits—P20 432

Software—S50 650

Stewardship Land—S60 671

Stewardship Reporting—S70 680

Stockpile Materials—S80 697

Transactions Not Recognized As Revenue, Gains, or Other Financing Sources—T30 700

Appendix A: Topical Index 708Appendix B: Effective Dates of Statements, Interpretations, and

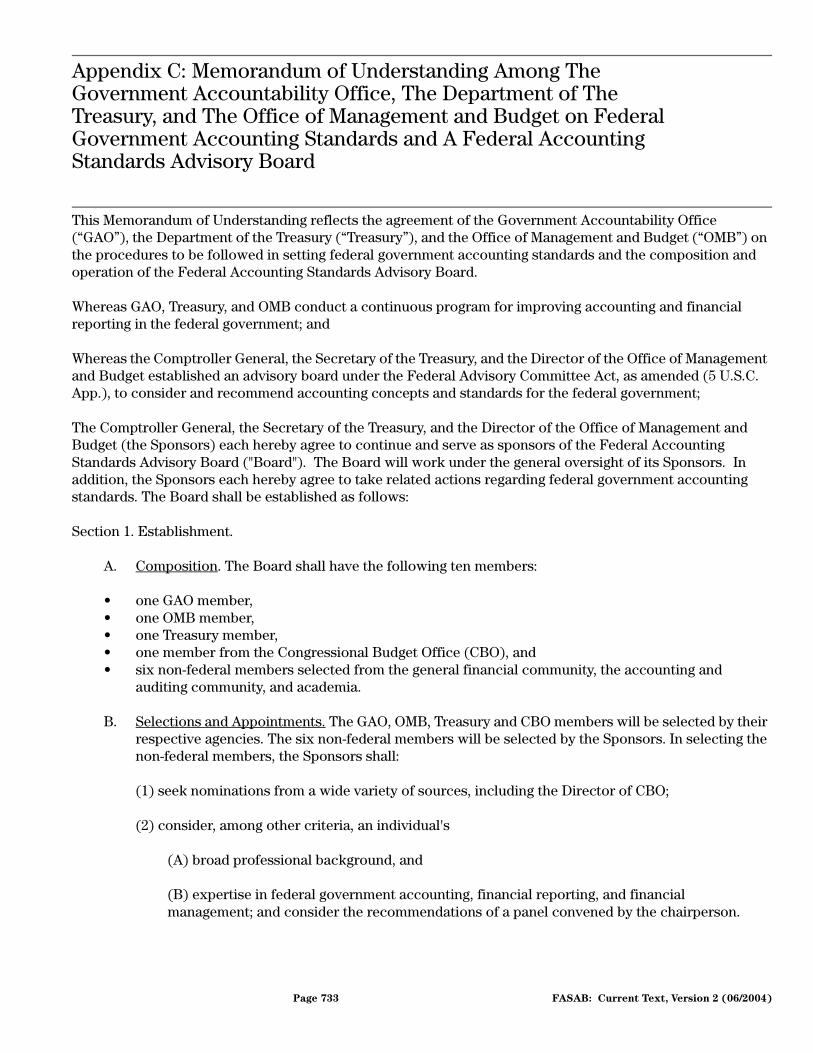

Technical Releases 731Appendix C: Memorandum of Understanding Among The Government

Accountability Office, The Department of The Treasury, and The Office of Management and Budget on Federal GovernmentAccounting Standards and A Federal Accounting Standards Advisory Board 733

Appendix D: Federal Accounting and Auditing Resources 737Appendix E: Cross-Reference Table Original Pronouncements

to Current Text 738

Page ii FASAB: Current Text, Version 2 (06/2004)

Foreword Foreword

The Statements of Federal Financial Accounting Standards, Current Text (“Current Text”) is a FASAB Staff document that compiles the original text that currently constitutes the body of accounting standards for the U.S. government in a major topic format.

The Current Text incorporates the following documents published through June 30, 2004:

• Statements of Federal Financial Accounting Standards 1-25,• Interpretations 1-6,• Technical Bulletin 2003-1 and• Technical Releases 1-6.

Origins of the Documents

The standards, interpretations, technical bulletins, and technical releases presented in the Current Text were issued in accordance with policies and procedures approved by the Department of the Treasury (Treasury), the Office of Management and Budget (OMB), and the Government Accountability Office (GAO) at the time of their issuance. These three central agencies, referred to collectively as the “sponsors,” established the Federal Accounting Standards Advisory Board (FASAB) in 1990. The mission of the FASAB is to develop accounting standards and principles for the federal government, after considering the financial and budgetary information needs of congressional oversight groups, executive agencies, and the needs of other users of federal financial information.

Standards

Using a due process and a consensus building approach, the Board promulgates accounting standards after considering the financial and budgetary information needs of Congress, executive agencies, other users of federal financial information, and comments from the public. The Memorandum of Understanding dated May 7, 2003, is included in Appendix C and describes the Board's authorities and processes.

Interpretations

Interpretations clarify original meaning, add definitions, and provide other guidance for existing SFFAS. They are narrow in scope. FASAB will respond to requests for guidance by providing technical assistance, including, in some cases, interpretations. When drafting an interpretation the FASAB staff submits the request to the Board and reviews applicable literature and consults with knowledgeable persons, as appropriate. FASAB will consider the draft interpretation at an open meeting. Proposed interpretations are exposed for public comment for at least 30 days. Interpretations approved by a majority of the Board and not objected to by a Board member representing a principal within 45 days are published by FASAB.

Page iii FASAB: Current Text, Version 2 (06/2004)

Foreword

Technical Bulletins

Technical bulletins provide guidance for applying statements and interpretations and resolving issues not directly addressed by them. Technical bulletins are used when the nature of an issue does not warrant more extensive due process. They are generally in question and answer format.

Technical Releases

The Accounting and Auditing Policy Committee (AAPC) provides implementation guidance for accounting standards, for the OMB’s Form and Content guidance, and for audit issues. The AAPC provides guidance through technical releases that are reviewed and published by the FASAB and announced originally in the Federal Register.

GAAP Documents

When adopted and issued, these documents become federal accounting standards and implementation guidance. It is expected that FASAB will continue to issue guidance through the documents described above. As new documents are adopted, the Current Text will be updated. Individual documents issued between updates are available through a variety of sources.

Purpose of the Current Text

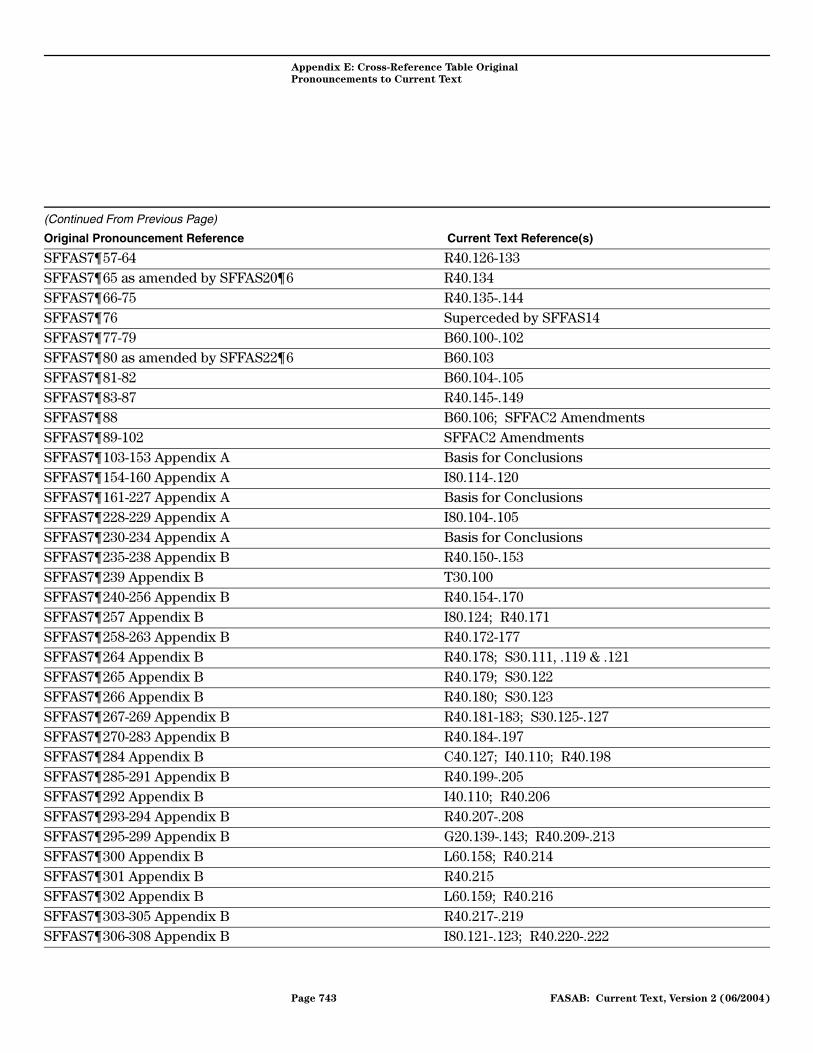

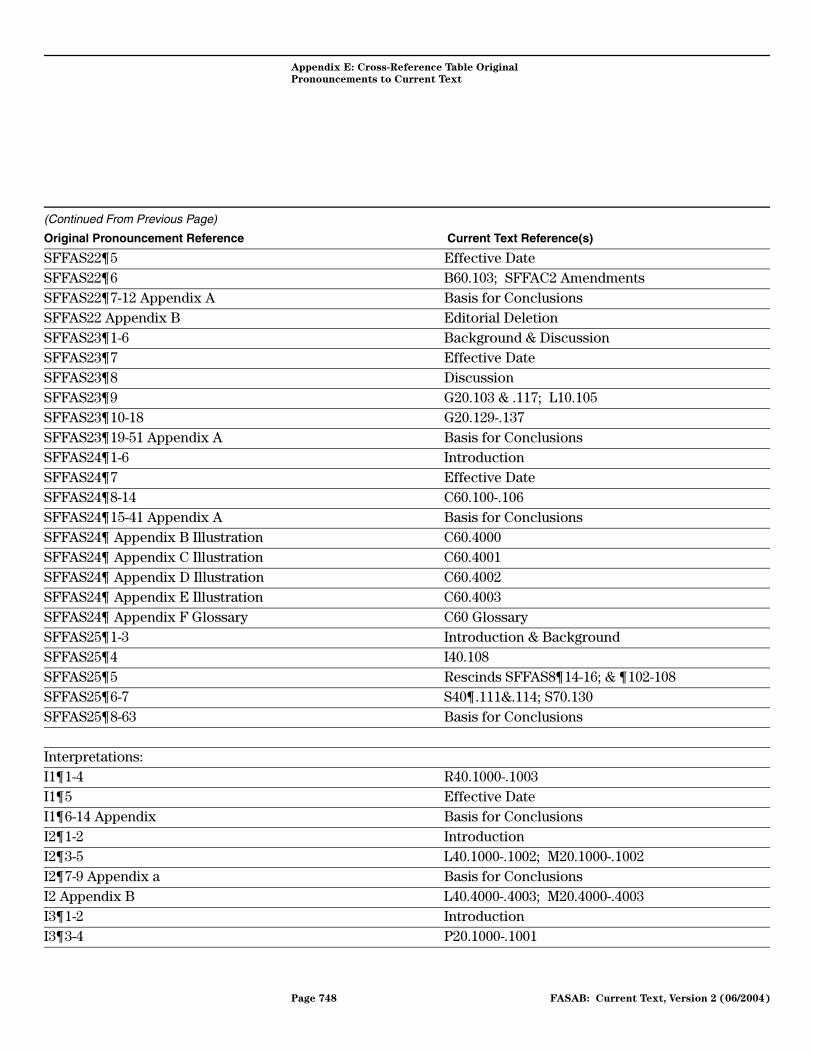

FASAB Staff provides the Current Text (also referred to as Volume II) as a compilation of the currently effective guidance promulgated by the FASAB. The Current Text presents the authoritative portions of the Original Pronouncements in a topical arrangement. Volume II also includes some non-authoritative portions of the FASAB guidance (i.e., illustrations, appendices, etc.). The Current Text is a resource for preparers and auditors, but is not an authoritative reference since it does not undergo Board level review for accuracy. Included in the Current Text are several appendices, such as an extensive topical index (Appendix A) and a cross-reference table to the Original Pronouncements (Appendix E).

Page iv FASAB: Current Text, Version 2 (06/2004)

Foreword

Organization of the Current Text

The Current Text combines the FASAB guidance according to the major subject areas to which they apply. The subject areas are arranged in alphabetical sections and each section of the Current Text has been designated with a corresponding alphanumeric code. The numeric part of the code has been arbitrarily selected to allow space for future subject areas. Each section includes the source of the guidance included as well as other related Volume II references. Paragraphs in each section are numbered consecutively, using the following format:

Each paragraph of the Current Text taken from the original pronouncements includes a reference back to the guidance, including the paragraph number of the original pronouncement. All amended and superseded guidance has been deleted and replaced with the new language and a reference noting the changes.

Each topical section includes a separate glossary of terms as used in the original pronouncements compiled into the section.

The Current Text includes the following appendices:

and Technical ReleasesAppendix C: Memorandum of UnderstandingAppendix D: Federal Accounting and Auditing ResourcesAppendix E: Cross-Reference Table - Original Pronouncement to Current Text

Appendix F: Consolidated List of Acronyms

The Current Text does not include the FASAB Statements of Federal Financial Accounting Concepts. The concept statements can be found in the Original Pronouncements document. Also excluded from the Current Text are the background sections of the original documents and their basis for conclusions sections.

Page v FASAB: Current Text, Version 2 (06/2004)

Foreword

Materiality

The Board intends that the standards’ application be limited to items that are material. “Materiality” has not been strictly defined in the accounting community; rather, it has been a matter of judgment on the part of preparers of financial statements and the auditors who attest to them. Presented below is the Board’s position on the issue of materiality at this time.

The accounting and reporting provisions of the Board’s accounting standards need not be applied to immaterial items. The determination of whether an item is immaterial requires the exercise of considerable judgment, based on consideration of specific facts and circumstances.

Hierarchy of Generally Accepted Accounting Principles

The term “generally accepted accounting principles” has a specific meaning for accountants and auditors. The AICPA Code of Professional Conduct prohibits members from expressing an opinion or stating affirmatively that financial statements or other financial data “present fairly... in conformity with generally accepted accounting principles,” if such information contains any departures from accounting principles promulgated by a body designated by the AICPA Council to establish such principles. The AICPA Council has designated FASAB as the body that establishes accounting principles for federal entities. The AICPA’s hierarchy of generally accepted accounting principles in Statement of Auditing Standards (SAS) No. 69, The Meaning of

Present Fairly in Conformity With Generally Accepted Accounting Principles in the Independent Auditor’s

Report, governs what constitutes GAAP for all U.S. government reporting entities. The hierarchy lists the priority sequence of sources that an entity should look to for accounting and reporting guidance.

The FASAB standards provide GAAP covering most transactions for the federal government. However, agencies may engage in transactions that are not addressed by these standards. In that event, agencies should view the hierarchy as providing sources of GAAP for the federal government.

Page vi FASAB: Current Text, Version 2 (06/2004)

Accounts Payable—A10

Source: SFFAS1

Related Reference(s): G60 Governmental and Intragovernmental Assets and Liabilities; O40 Other Current Liabilities; L40 Liabilities

Summary Accounts Payable are to be recognized for an entity’s liability for goods and services received, or work progress made by a contractor, for which payment has not been made. Accounts Payable for intragovernmental transactions are reported separately from amounts owed to the public.

Accounts Payable .100 Accounts payable are amounts owed by a federal entity for goods and services received from, progress in contract performance made by, and rents due to other entities. [SFFAS1, ¶74]

.101 Accounts payable are not intended to include liabilities related to on-going continuous expenses such as employees' salary and benefits, which are covered by other current liabilities. (See recommended standard for Other Current Liabilities O40.) [SFFAS1, ¶75]

.102 Amounts owed for goods or services received from federal entities represent intragovernmental transactions and should be reported separately from amounts owed to the public. [SFFAS1, ¶76]

.103 When an entity accepts title to goods, whether the goods are delivered or in transit, the entity should recognize a liability for the unpaid amount of the goods. If invoices for those goods are not available when financial statements are prepared, the amounts owed should be estimated. [SFFAS1, ¶77]

.104 When a contractor provides the government with goods that are also suitable for sale to others, the liability usually arises when the contractor physically delivers the goods and the government receives them and takes formal title. However, when a contractor builds or manufactures facilities or equipment to the government's specifications, formal acceptance of the products by the government is not the determining factor for accounting recognition. Constructive or de facto receipt occurs in each accounting period, in accordance with the following paragraph. [SFFAS1, ¶78]

Page 1 FASAB: Current Text, Version 2 (06/2004)

Accounts Payable—A10

.105 For facilities or equipment constructed or manufactured by contractors or grantees according to agreements or contract specifications, amounts recorded as payable should be based on an estimate of work completed under the contract or the agreement. The estimate of such amounts should be based primarily on the federal entity's engineering and management evaluation of actual performance progress and incurred costs. [SFFAS1, ¶79]

.106 The reporting entity should disclose accounts payable not covered by budgetary resources. [SFFAS1, ¶80]

Page 2 FASAB: Current Text, Version 2 (06/2004)

Advances and Prepayments—A30

Source: SFFAS1

Related Reference(s): G60 Governmental and Intragovernmental Assets and Liabilities; O40 Other Current Liabilities; L40 Liabilities

Summary Advances and prepayments are cash outlays made before expenses are incurred. They should be recorded as assets and reduced when the goods and services are received and expenses incurred.

Advances and Prepayments

.100 Advances are cash outlays made by a federal entity to its employees, contractors, grantees, or others to cover a part or all of the recipients' anticipated expenses or as advance payments for the cost of goods and services the entity acquires. Examples include travel advances disbursed to employees prior to business trips, and cash or other assets disbursed under a contract, grant, or cooperative agreement before services or goods are provided by the contractor or grantee. [SFFAS1, ¶57]

.101 Prepayments are payments made by a federal entity to cover certain periodic expenses before those expenses are incurred. Typical prepaid expenses are rents paid to a lessor at the beginning of a rental period. Progress payments made to a contractor based on a percentage of completion of the contract are not advances or prepayments. [SFFAS1, ¶58]

.102 Advances and prepayments should be recorded as assets. Advances and prepayments are reduced when goods or services are received, contract terms are met, progress is made under a contract, or prepaid expenses expire. A travel advance, for example, should be initially recorded as an asset and should be subsequently reduced when travel expenses are actually incurred. Amounts of advances and prepayments that are subject to refund (for example, a settled travel claim indicating the traveler owes part of the advance to the government) should be transferred to accounts receivable. [SFFAS1, ¶59]

.103 Advances and prepayments paid out by an entity are assets of the entity. On the other hand, advances and prepayments received by an entity are liabilities of the entity. (See O40 Other Current Liabilities).

Page 3 FASAB: Current Text, Version 2 (06/2004)

Advances and Prepayments—A30

In financial reports of an entity, advances and prepayments the entity paid out (assets) should not be netted against advances and prepayments that the entity received (liabilities). [SFFAS1, ¶60]

.104 Advances and prepayments made to federal entities are intragovernmental items and should be accounted for and reported separately from those made to nonfederal entities. [SFFAS1, ¶61]

Page 4 FASAB: Current Text, Version 2 (06/2004)

Budgetary Information—B60

Source: SFFAS7; SFFAS22

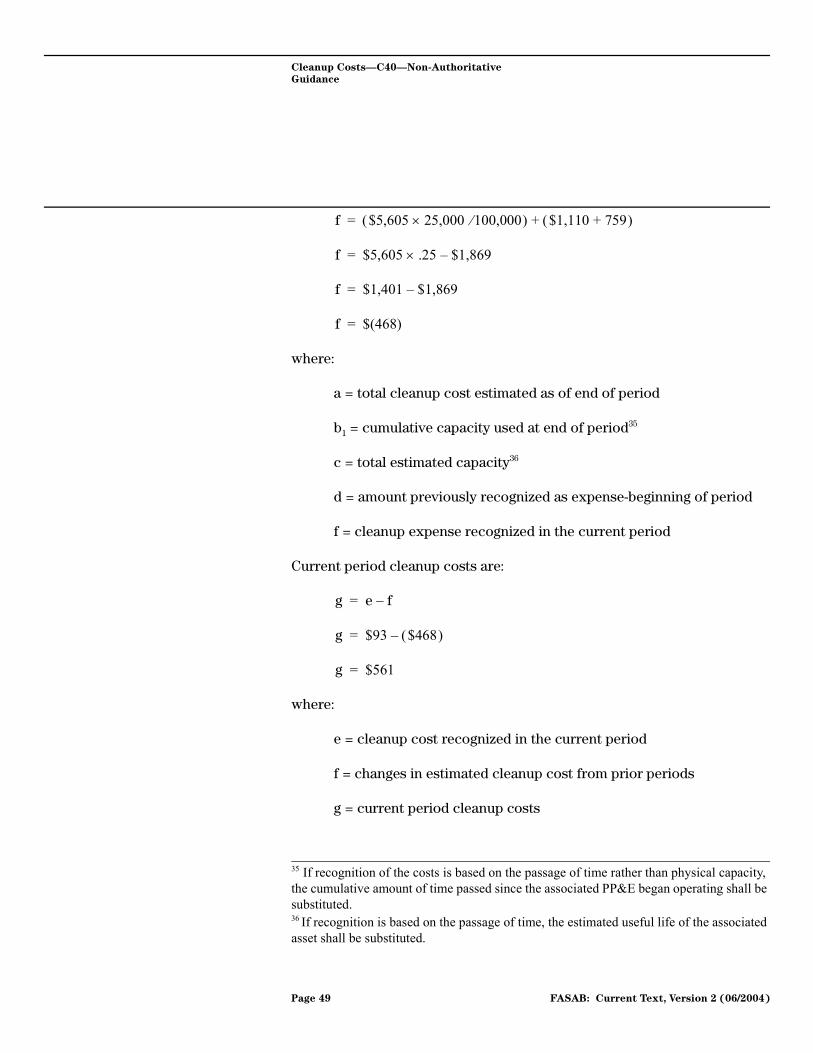

Related Reference(s): R40 Revenue, Gains & Losses, and Other Financing Sources

Summary Both budget information and operating performance (i.e., proprietary) information is required to meet the needs of users and the objectives of reporting. The budget information focuses on the obligation and outlay of financial resources to acquire or provide goods and services as defined by budget concepts. Operating performance information focuses on the cost of resources used as defined by accrual accounting standards. Budgetary and financial accounting information are complementary, but both the types of information and the timing of their recognition is necessarily different because of the difference in focus. To better understand the differences and make better use of the complementary information provided, information needs to be provided to reconcile the use of budgetary resources to acquire or provide goods and services with the net cost of using those goods and services. FASAB, therefore, amended Concept Statement 2, “Entity and Display” to include in its concepts the need to communicate information about the differences between the use of resources as reported in the budget and in the net cost of operations. 1 As a result of the amendments, budgetary Information is recognized and reported in both the Statement of Budgetary Resources and the new statement, the Statement of Financing.

This section includes the provisions of SFFAS7 that relate to budgetary information and a glossary of budgetary terms used in this and other sections of this volume. For further information, see SFFAC 2.

Budgetary Information .100 The budget is the primary financial planning and control tool of the government. For this reason, and because of the importance of this information to users of federal financial information, the following material budgetary information should be presented by reporting entities whose financing comes wholly or partially from the budget:

1 SFFAS7 amends the FASAB’s Concepts Statement 2 by adding Concepts for Reconciling Budgetary and Financial Accounting. See SFFAC 2’s Section, “Displaying Financial Information.”

Page 5 FASAB: Current Text, Version 2 (06/2004)

Budgetary Information—B60

(a) total budgetary resources available to the reporting entity during the period;

(b) the status of those resources (including “obligations incurred”);

(c) outlays. [SFFAS7, ¶77]

.101 Recognition and measurement of budgetary resources should be based on budget concepts and definitions contained in OMB Circulars A-11, Preparation and Submission of Budget Estimates. In addition, the reporting entity should provide this information for each of its major budget accounts as supplementary information. Small budget accounts may be aggregated. [SFFAS7, ¶78]

.102 The following information about the status of budgetary resources should be disclosed.

(a) the amount of budgetary resources obligated for undelivered orders at the end of the period;

(b) available borrowing and contract authority at the end of the period;

(c) repayment requirements, financing sources for repayment, and other terms of borrowing authority used;

(d) material adjustments during the reporting period to budgetary resources available at the beginning of the year and an explanation thereof;

(e) existence, purpose, and availability of permanent indefinite appropriations;

(f) information about legal arrangements affecting the use of unobligated balances of budget authority such as time limits, purpose, and obligation limitations;

(g) explanations of any material differences between the information required by paragraph .103 and the amounts described as “actual” in the Budget of the United States

Government;

Page 6 FASAB: Current Text, Version 2 (06/2004)

Budgetary Information—B60

(h) the amount, and an explanation that includes identification of balance sheet components, when recognized unfunded liabilities do not equal the total financing sources yet to be provided; and

(i) the amount of any capital infusion received during the reporting period. [SFFAS7, ¶79]

.103 Budgetary and financial accounting information are complementary, but both the types of information and the timing of their recognition are different, causing differences in the basis of accounting. To better understand these differences, a reconciliation should explain the relationship between budgetary resources obligated by the entity during the period and the net cost of operations. It should reference the reported “obligations incurred” and related adjustments as defined by OMB Circular A-11. It also should include other financing sources not included in “obligations incurred” such as imputed financing, transfers of assets, and donations of assets not included in budget receipts. [SFFAS7, ¶80, as amended by SFFAS22, ¶6]

.104 This total should then be adjusted by:

(a) Resources that do not fund net cost of operations (e.g., changes in undelivered orders, appropriations received to pay for prior period costs, capitalized assets),

(b) Costs included in net cost of operations that do not require resources (e.g., depreciation and amortization expenses of assets previously capitalized), and

(c) Financing sources yet to be provided (those becoming available in future periods which will be used to finance costs recognized in determining net cost for the present reporting period). [SFFAS7, ¶81]

.105 The adjustments should be presented and explained in appropriate detail and in a manner that best clarifies the relationship between the obligations basis used in the budget and the accrual basis used in financial (proprietary) accounting. [SFFAS7, ¶82]

Page 7 FASAB: Current Text, Version 2 (06/2004)

Budgetary Information—B60

Reconciling Budgetary and Financial Accounting

.106 The Statement of Federal Financial Accounting Concepts (SFFAC) No. 2, Entity and Display2, was issued to provide conceptual guidance as to what would be encompassed by a federal entity's financial report. It identifies the types of financial information to be communicated to users and suggests the types of information to be included in an entity's report to help meet the objectives of federal financial reporting. Among other things, SFFAC No. 2 supports reporting both budget information and operating performance (i.e., proprietary) information3 to meet the needs of users and the objectives of reporting. The budget information focuses on the obligation and outlay of financial resources to acquire or provide goods and services as defined by budget concepts. Operating performance information focuses on the cost of resources used as defined by accrual accounting standards. [SFFAS7, ¶88]

2 See SFFAC 2, Entity and Display.

3 SFFAC 2 includes example formats for the Statement of Financing.

Page 8 FASAB: Current Text, Version 2 (06/2004)

Budgetary Information—B60—Glossary

Glossary Apportionment – A distribution made by OMB of amounts available for obligation in an appropriation or fund account into amounts available for specified time periods, programs, activities, projects, objects, or combinations thereof. The apportioned amount limits the obligations that may be incurred. (OMB Circular A-11, Preparation and Submission of Budget Estimates)

Appropriation – In most cases, appropriations are a form of budget authority provided bylaw that permits federal agencies to incur obligations and make payments out of the Treasury for specified purposes. An appropriation usually follows enactment of authorizing legislation. An appropriation act is the most common means of providing budget authority, but in some cases the authorizing legislation itself provides the budget authority.

Authority To Borrow – Authority to borrow is a subset of budget authority. (See budget authority.)

Basic Financial Statements – As used in SFFAS7, the basic financial statements are those on which an auditor would normally be engaged to express an opinion. The term “basic” does not necessarily mean that other financial information not covered by the auditor’s opinion is less important to users than that contained in the basic statements; it merely connotes the expected nature of the auditor’s review of, and association with, the information. The basic financial statements in financial reports prepared pursuant to the Chief Financial Officers Act, as amended, are called the “principal financial statements.” The Form and Content of these statements are determined by OMB.

Budget Authority – The authority provided by Federal law to incur financial obligations that will result in immediate or future outlays. Specific forms of budget authority include:

• appropriations, which may be provided in appropriations acts or other laws and which permit obligations to be incurred and payments to be made;

• borrowing authority, which permits obligations to be incurred but requires funds to be borrowed to liquidate the obligation;

• contract authority, which permits obligations to be incurred but requires a subsequent appropriation or offsetting collections to liquidate the obligations; and

Page 9 FASAB: Current Text, Version 2 (06/2004)

Budgetary Information—B60—Glossary

• spending authority from offsetting collections, which permits offsetting collections to be credited to an expenditure account and permits obligations and payments to be made using the offsetting collections (the offsetting collections credited to an account are deducted from gross budget authority of the account.)

• Budget authority may be classified by period of availability (one year, multiple-year, or no year), by nature of the authority (current or permanent), by the manner of determining the amount available (definite or indefinite), or as gross (without reduction of offsetting collections) and net (with reductions of offsetting collections). (OMB Circular A-11; and GAO, A Glossary of Terms Used in the Federal Budget Process, Exposure Draft, January 1993.)

Budgetary Accounting – Budgetary accounting is the system that measures and controls the use of resources according to the purposes for which budget authority was enacted; and that records receipts and other collections by source. It tracks the use of each appropriation for specified purposes in separate budget accounts through the various stages of budget execution from appropriation to apportionment and allotment to obligation and eventual outlay. This system is used by the Congress and the Executive Branch to set priorities, to allocate resources among alternative uses, to finance these resources, and to assess the economic implications of federal financial activity at an aggregate level. Budgetary accounting is used to comply with the Constitutional requirement that “No Money shall be drawn from the Treasury, but in Consequence of Appropriations Made by Law; and a regular Statement and Account of the Receipts and Expenditures of all public Money shall be published from time to time.” (See Statement of Federal Financial Accounting Concepts No. 1, Objectives of Federal Financial Reporting, September 1993, Paragraphs 45-46, 112-114, and 186-191.)

Budgetary Resources – The forms of authority given to an agency allowing it to incur obligations. Budgetary resources include the following: new budget authority, unobligated balances, direct spending authority, and obligation limitations. (GAO Budget Glossary)

Collections – Amounts received by the federal government during the fiscal year. Collections are classified as follows: — Budget receipts or off-budget receipts are collections from the public based on the government's exercise of its sovereign powers, including collections from participants in

Page 10 FASAB: Current Text, Version 2 (06/2004)

Budgetary Information—B60—Glossary

compulsory social insurance programs. — Offsetting collections are collections from government accounts (intragovernmental transactions) or from the public that are offset against budget authority and outlays rather than reflected as receipts in computing the budget and off-budget totals. They are classified as (a) offsetting receipts (i.e., amounts deposited to receipt accounts), and (b) collections credited to appropriation or fund accounts. The distinction between these two major categories is that collections credited to appropriation or fund accounts are offset within the account that contains the associated disbursements (outlays), whereas offsetting receipts are in accounts separate from the associated disbursements. Offsetting collections are deducted from gross disbursements in calculating net outlays. (Budget Glossary.)

Contract Authority – Contract authority is a subset of budget authority. (See budget authority.)

Expended Appropriations – The dollar amount of appropriations used to fund goods and services received or benefits or grants provided.

Expenditure – With respect to provisions of the Antideficiency Act (31 U.S.C. 1513-1514) and the Congressional Budget and Impoundment Control Act of 1974 (2 U.S.C. 622(i)), a term that has the same definition as outlay. (GAO Budget Glossary)

Expired Appropriations (Accounts) – Appropriation accounts in which the balances are no longer available for incurring new obligations because the time available for incurring such obligations has expired. (JFMIP Standardization Project)

Obligated Balances – The net amount of obligations in a given account for which payment has not yet been made. (JFMIP Standardization Project)

Obligations – Amounts of orders placed, contracts awarded, services received, and other transactions occurring during a given period that would require payments during the same or a future period. (JFMIP Standardization Project)

Offsetting Receipts – Offsetting receipts are a subset of offsetting collections. (See collections.)

Outlay – The issuance of checks, disbursement of cash, or electronic transfer of funds made to liquidate a Federal obligation. Outlays also occur

Page 11 FASAB: Current Text, Version 2 (06/2004)

Budgetary Information—B60—Glossary

when interest on the Treasury debt held by the public accrues and when the Government issues bonds, notes, debentures, monetary credits, or other cash-equivalent instruments in order to liquidate obligations. Also, under credit reform, the credit subsidy cost is recorded as an outlay when a direct or guaranteed loan is disbursed. (GAO Budget Glossary)

Reappropriation – Enacted legislation that continues the availability of unexpended funds that expired or would otherwise expire. (JFMIP Standardization Project)

Transfers Between Appropriation/Fund Accounts – Occur when all or part of the budget authority in one account is transferred to another account when such transfers are specifically authorized by law. The nature of the transfer determines whether the transaction is treated as an expenditure transfer or a non-expenditure transfer. (JFMIP Standardization Project)

Treasury Warrant – An official document that the Secretary of the Treasury issues pursuant to law and that establishes the amount of monies authorized to be withdrawn from the central accounts that Treasury maintains. Warrants for currently unavailable special and trust fund receipts are issued when requirements for their availability have been met. (GAO Budget Glossary)

Unobligated Balances – Balances of budgetary resources that have not yet been obligated. Unobligated balances expire (cease to be available for obligation) for: — 1-year accounts at the end of the fiscal year; — multiple-year accounts at the end of the period specified; — no-year accounts only when they are 1) rescinded by law, 2) purpose is accomplished, or 3) when disbursements against the appropriation have not been made for 2 full consecutive years. (JFMIP Standardization Project and Budget Glossary)

Page 12 FASAB: Current Text, Version 2 (06/2004)

Cash—C20

Source: SFFAS1

Related Reference(s): E30 Entity and Non-Entity Assets; F50 Fund Balance with Treasury; G60 Governmental and Intragovernmental Assets and Liabilities

Summary Cash, including imprest funds, should be recognized as an asset.

Cash .100 Cash, including imprest funds, should be recognized as an asset. Cash consists of:

(a) coins, paper currency and readily negotiable instruments, such as money orders, checks, and bank drafts on hand or in transit for deposit;

(b) amounts on demand deposit with banks or other financial institutions; and

(c) foreign currencies, which, for accounting purposes, should be translated into U.S. dollars at the exchange rate on the financial statement date. [SFFAS1, ¶27]

Entity Cash .101 Entity cash is the amount of cash that the reporting entity holds and is authorized by law to spend. [SFFAS1, ¶28]

Non-Entity Cash .102 Non-entity cash is cash that a federal entity collects and holds on behalf of the U.S. government or other entities. In some circumstances, the entity deposits cash in its accounts in a fiduciary capacity for the U.S. Treasury or other entities. Non-entity cash should be reported separately from entity cash. [SFFAS1, ¶29]

Page 13 FASAB: Current Text, Version 2 (06/2004)

Cash—C20

Restricted Cash .103 Cash may be restricted. Restrictions are usually imposed on cash deposits by law, regulation, or agreement. Non-entity cash is always restricted cash. Entity cash may be restricted for specific purposes. Such cash may be in escrow or other special accounts. Financial reports should disclose the reasons and nature of restrictions. [SFFAS1, ¶30]

Page 14 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40

Source: SFFAS5, SFFAS6; TR2

Related Reference(s): L40 Liabilities; G20 General Plant, Property, and Equipment

Summary Cleanup costs are the costs associated with hazardous waste removal, containment, or disposal. In some instances, the Federal Government incurs liabilities1 for cleaning up hazardous waste at sites or facilities it operates or has operated. Generally, cleanup cannot be, or is not, done until permanent or temporary closure or shutdown of sites or facilities. The FASAB’s standards for liabilities (SFFAS5) which address liabilities for environmental cleanup resulting from an accident, natural disaster, or other one-time occurrence do not address inter-period cost allocation when cleanup relates to operations that span many periods. Therefore, the Board chose to provide additional guidance relative to cleanup costs in SFFAS6. The additional standards in SFFAS6 provide for the timing of recognition of the liability and related operating expense.

For cleanup costs associated with general PP&E, probable2 and measurable cleanup costs shall be allocated to operating periods benefiting from operations of the general PP&E. This allocation shall be based on a systematic and rational method. For example, the estimated cost could be allocated to operating periods based on the expected physical capacity of the PP&E and the amount of capacity used each period. In addition, disclosure of the total estimated cost is required.

1 FASAB's Statement of Recommended Accounting Standards No. 5, Accounting for Liabilities of the Federal Government, recommends the following definition for liability: a probable future outflow or other sacrifice of resources as a result of past transactions or events. The standards require recognition, in general purpose Federal financial reports, of probable and measurable liabilities arising from past exchange transactions; government-related injuries or damage; or non-exchange amounts that, according to current law and applicable policy, are due and payable to the ultimate recipient. The standards also provide guidance for disclosures related to liabilities that are not both probable and measurable at the balance sheet date.

2 The term “probable” means that which can reasonably be expected or believed to be more likely than not on the basis of available evidence or logic but which is neither certain nor proven. For example, cleanup costs would be probable if (1) laws and regulations that have been approved as of the balance sheet date, regardless of the effective date of those laws and regulations, require cleanup or (2) compliance agreements (e.g., agreements with state or local authorities relating to the extent and the timing of remedial action) had been entered into by a Federal entity.

Page 15 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40

For cleanup costs associated with stewardship PP&E,3 probable and measurable liabilities shall be recognized when the stewardship PP&E is placed in service. Simultaneous to recognizing the liability, the related expense for cleanup cost shall be recognized.

This section also includes non-authoritative guidance related to recognition and reporting of cleanup costs.

Cleanup Costs .100 Cleanup costs are the costs of removing, containing, and/or disposing of (1) hazardous waste (See paragraph .101) from property, or (2) material and/or property that consists of hazardous waste at permanent or temporary closure or shutdown of associated PP&E. [SFFAS6, ¶85]

.101 Hazardous waste is a solid, liquid, or gaseous waste, or combination of these wastes, which because of its quantity, concentration, or physical, chemical, or infectious characteristics may cause or significantly contribute to an increase in mortality or an increase in serious irreversible, or incapacitating reversible, illness or pose a substantial present or potential hazard to human health or the environment when improperly treated, stored, transported, disposed of, or otherwise managed. [SFFAS6, ¶86]

.102 Cleanup may include, but is not limited to, decontamination, decommissioning, site restoration, site monitoring, closure, and post closure costs. [SFFAS6, ¶87]

.103 SFFAS6 provisions related to cleanup costs apply to cleanup costs from Federal operations known to result in hazardous waste which the Federal Government is required by Federal, state and/or local statutes and/or regulations that have been approved as of the balance sheet date, regardless of the effective date, to cleanup (i.e., remove, contain or dispose of).4 These cleanup costs meet the

3 Stewardship PP&E, consists of heritage assets (Section H20), and stewardship land (Section S60).

4 Accounting for environmental liabilities such as cleanup costs is currently undergoing change—due to both improved measurement techniques and increased attention from the accounting community. FASAB plans to monitor these changes and revisit these standards as needed.

Page 16 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40

definition of liability provided in Statement of SFFAS5, Accounting

for Liabilities of the Federal Government. (See Volume 2, L40.)

[SFFAS6, ¶88]

.104 However, due to the nature of the liability and the timing associated with cleanup costs, additional guidance is provided in SFFAS6 on the recognition of cleanup costs over the life of the related PP&E. Guidance is required since cleanup can not occur until the end of the useful life of the PP&E or at regular intervals during that life. [SFFAS6, ¶89]

.105 The guidance in SFFAS6 is intended to supplement the accounting requirements for liabilities in SFFAS5. That standard defines liabilities as a “probable future outflow or other sacrifice of resources as a result of past transactions or events.” Further, SFFAS5 requires recognition of liabilities that are probable and measurable. Measurable means that an item has a relevant attribute that can be quantified in monetary units with sufficient reliability to be reasonably estimable. [SFFAS6, ¶90]

.106 The recognition and measurement standards provided in SFFAS6 are subject to the criteria for recognition of liabilities included in SFFAS5.5 That is, liabilities shall be recognized when three conditions are met:

• a past transaction or event has occurred,• a future outflow or other sacrifice of resources is probable,6

and• the future outflow or sacrifice of resources is measurable.7

[SFFAS6, ¶91]

5 SFFAS5 guidance applies to Government-related events including cleanup from federal operations resulting in hazardous waste that the federal government is required by statutes and/or regulations, that are in effect as of the Balance Sheet date. See Section L40, paragraphs 109-.112 in this Volume.

6 Probable means that the future confirming event or events is more likely than not to occur.

7 The unit of analysis for estimating liabilities can vary based on the reporting entity and the nature of the transaction or event. The liability recognized may be the estimation of an individual transaction or event; or a group of transactions and events. For example, an estimate of the cleanup costs could be made on a facility by facility basis, or an entity by entity basis.

Page 17 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40

.107 SFFAS5 also provides for disclosure of liabilities that do not meet all of the above criteria; these standards apply to cleanup costs as well. [SFFAS6, ¶92]

.108 Certain other cleanup costs, such as those resulting from accidents or where cleanup is an ongoing part of operations, are to be accounted for in accordance with liability standards and are not subject to the recognition guidance provided in SFFAS6. SFFAS6’s guidance does not apply to these other types of cleanup since the cleanup effort is not deferred until operation of associated PP&E ceases either permanently or temporarily.8 [SFFAS6, ¶93]

Recognition and Measurement

Estimation Methods .109 Cleanup costs, as defined above, shall be estimated when the associated PP&E is placed in service . The estimate shall be referred to as the “estimated total cleanup cost.” There are two approaches to recognizing this total—one applies to general PP&E and another to stewardship PP&E. [SFFAS6, ¶94]

.110 The estimate shall contemplate:

• the cleanup plan, including level of restoration to be performed, current legal or regulatory requirements,9 and current technology; and

• current cost which is the amount that would be paid if all equipment, facilities, and services included in the estimate were acquired during the current period. [SFFAS6, ¶95]

8 Cleanup may be deferred for other reasons, such as availability of resources. However, this type of deferral does not affect the recognition of the liability.

9 Laws and regulations approved as of the balance sheet date, regardless of the effective date of those laws and regulations, shall be considered.

Page 18 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40

.111 Estimates shall be revised periodically to account for material changes due to inflation or deflation and changes in regulations, plans and/or technology.10 New cost estimates should be provided if there is evidence that material changes have occurred; otherwise estimates may be revised through indexing. [SFFAS6, ¶96]

Cleanup Cost for General PP&E

.112 A portion of estimated total cleanup costs shall be recognized as expense during each period that general PP&E is in operation. This shall be accomplished in a systematic and rational manner based on use of the physical capacity of the associated PP&E (e.g., expected usable landfill area) whenever possible. If physical capacity is not applicable or estimable, the estimated useful life of the associated PP&E may serve as the basis for systematic and rational recognition of expense and accumulation of the liability. [SFFAS6, ¶97]

.113 Recognition of the expense and accumulation of the liability shall begin on the date that the PP&E is placed into service, continue in each period that operation continues, and be completed when the PP&E ceases operation. [SFFAS6, ¶98]

.114 As re-estimates (See paragraph .115) are made, the cumulative effect of changes in total estimated cleanup costs related to current and past operations shall be recognized as expense and the liability adjusted in the period of the change in estimate. [SFFAS6, ¶99]

.115 As cleanup costs are paid, payments shall be recognized as a reduction in the liability for cleanup costs. These include the cost of PP&E or other assets acquired for use in cleanup activities. [SFFAS6, ¶100]

10 SFFAS4, Managerial Cost Accounting, discusses costs related to facility abandonments in paragraph 104 of the statement: “A responsibility segment may incur and recognize costs that are linked to events other than the production of goods and services. … Other non-production costs include reorganization costs, and nonrecurring cleanup costs resulting from facility abandonments that are not accrued. Since these costs are recognized for a period in which a particular event occurs, assigning these costs to goods and service produced in that period would distort the production costs. In special purpose cost studies, management may have reasons to determine historical output costs by distributing some of these costs to outputs over a number of past periods. Such distribution may be appropriate when: (a) experience shows that the costs are recurring in a regular pattern, and (b) a nexus can be established between the costs and the production of outputs that may have benefited from those costs. (See Subject Area Section M20.141.)

Page 19 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40

Cleanup Cost for Stewardship PP&E

.116 Consistent with the treatment of the acquisition cost of stewardship PP&E (i.e., expensing in the period placed in service), the total estimated cleanup cost shall be recognized as expense in the period that the stewardship asset is placed in service and a liability established. [SFFAS6, ¶101]

.117 The liability shall be adjusted when the estimated total cleanup costs are re-estimated as described in paragraph .115. Adjustments to the liability shall be recognized in expense as “changes in estimated cleanup costs from prior periods.” [SFFAS6, ¶102]

.118 As cleanup costs are paid, payments shall be recognized as a reduction in the liability for cleanup costs. These include the cost of PP&E or other assets acquired for use in cleanup activities. [SFFAS6, ¶103]

Implementation Guidance

.119 Two implementation approaches have been provided for liabilities related to general PP&E in service at the effective date of SFFAS6:

• A liability shall be recognized for the portion of the estimated total cleanup cost that is attributable to that portion of the physical capacity used or that portion of the estimated useful life that has passed since the PP&E was placed in service. The remaining cost shall be allocated as provided in paragraphs .116 through .118.

• If costs are not intended to be recovered primarily through user charges, management may elect to recognize the estimated total cleanup cost as a liability upon implementation. In addition, in periods following the implementation period, any changes in the estimated total cleanup cost shall be expensed when re-estimates occur and the liability balance adjusted. The provisions for cost allocation provided in paragraphs .116 through .118 shall not apply under this implementation method. [SFFAS6, ¶104]

.120 The offsetting charge for any liability recognized upon implementation shall be made to Net Position of the entity. The amount of the adjustment shall be shown as a “prior period adjustment” in any statement of changes in net position that may be required. No amounts shall be recognized as expense in the period of

Page 20 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40

implementation. The amounts involved shall be disclosed and to the extent possible the amount associated with current and prior periods should be noted. [SFFAS6, ¶105]

.121 For stewardship PP&E that are in service at the effective date of this standard, the liability for cleanup costs shall be recognized and an adjustment made to the Net Position of the entity. The amount of the adjustment shall be shown as a “prior period adjustment” in any statement of changes in net position that may be required. The amounts involved shall be disclosed. [SFFAS6, ¶106]

Disclosure Requirements

.122 The sources (applicable laws and regulations) of cleanup requirements. [SFFAS6, ¶107]

.123 The method for assigning estimated total cleanup costs to current operating periods (e.g., physical capacity versus passage of time). [SFFAS6, ¶108]

.124 For cleanup cost associated with general PP&E, the unrecognized portion of estimated total cleanup costs (e.g., the estimated total cleanup costs less the cumulative amounts charged to expense at the balance sheet date). [SFFAS6, ¶109]

.125 Material changes in total estimated cleanup costs due to changes in laws, technology, or plans shall be disclosed. In addition, the portion of the change in estimate that relates to prior period operations shall be disclosed. [SFFAS6, ¶110]

.126 The nature of estimates and the disclosure of information regarding possible changes due to inflation, deflation, technology, or applicable laws and regulations. [SFFAS6, ¶111]

Page 21 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40

Revenue Recognition .127 SFFAS7 addresses reimbursement for cleanup costs and provides that “The Coast Guard or other Federal entities may incur costs to clean up environmental hazards caused by private parties and, in some cases, require these private parties to reimburse it for the costs incurred. Notwithstanding that the Government demands the revenue under its power to compel payment, the revenue arises from the action of the private parties and is closely related to the cost of operations incurred as a result of that action. Therefore, the revenue is an exchange revenue of the entity that incurs the cost.” [SFFAS7, ¶292]

Page 22 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40—Technical Guidance

Cleanup Costs—Technical Guidance

Federal Financial Accounting and Auditing Technical Release No. 2: Determining Probable and Reasonably Estimable for Environmental Liabilities in the Federal Government

.3000 Federal agencies are required to recognize a liability when a future outflow or other sacrifice of resources as a result of past transactions or events is “probable” and “reasonably estimable.” Technical Release is intended to assist federal agencies in determining probable and reasonably estimable liabilities related to their environmental cleanup responsibilities.

.3001 This technical release includes two sections and an appendix. Section 1 will help an agency determine whether its environmental contamination meets the definition of probable (i.e., a future outflow of resources will be required to clean up the contamination). Section 2 offers guidance in quantifying an agency’s liability for cleanup. Appendix I lists key laws and regulations relating to environmental contamination.

Description of Issue .3002 An agency is required to recognize a liability for environmental cleanup costs as a result of past transactions or events when a future outflow or other sacrifice of resources is probable and reasonably estimable.

Page 23 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40—Technical Guidance

.3003 Concerns have been raised about when costs associated with environmental damage meet the probable and reasonably estimable criteria. Probable is related to whether a future outflow will be required.11 This section12 addresses only the “probable” part of this requirement; reasonably estimable will be addressed in Section 2.

Key Determinants and Positions

.3004 Various key factors (tests) must be considered in determining whether a future outflow of resources from a federal agency for environmental cleanup is probable. The factors are:

1. Likely Contamination,

2. Government Related and Legally Liable,

3. Government Acknowledged Financial Responsibility, 3a. Monies Appropriated/Transaction Occurred, and

4. No Known Remediation Technology Exists.

11 SFFAS4, Managerial Cost Accounting, discusses costs related to facility abandonments in paragraph 104 of the statement: “A responsibility segment may incur and recognize costs that are linked to events other than the production of goods and services. … Other non-production costs include reorganization costs, and nonrecurring cleanup costs resulting from facility abandonments that are not accrued. Since these costs are recognized for a period in which a particular event occurs, assigning these costs to goods and service produced in that period would distort the production costs. In special purpose cost studies, management may have reasons to determine historical output costs by distributing some of these costs to outputs over a number of past periods. Such distribution may be appropriate when: (a) experience shows that the costs are recurring in a regular pattern, and (b) a nexus can be established between the costs and the production of outputs that may have benefited from those costs. (See Subject Area Section M20.141.)

12 SFFAS4, Managerial Cost Accounting, discusses costs related to facility abandonments in paragraph 104 of the statement: “A responsibility segment may incur and recognize costs that are linked to events other than the production of goods and services. … Other non-production costs include reorganization costs, and nonrecurring cleanup costs resulting from facility abandonments that are not accrued. Since these costs are recognized for a period in which a particular event occurs, assigning these costs to goods and service produced in that period would distort the production costs. In special purpose cost studies, management may have reasons to determine historical output costs by distributing some of these costs to outputs over a number of past periods. Such distribution may be appropriate when: (a) experience shows that the costs are recurring in a regular pattern, and (b) a nexus can be established between the costs and the production of outputs that may have benefited from those costs. (See Subject Area Section M20.141.)

Page 24 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40—Technical Guidance

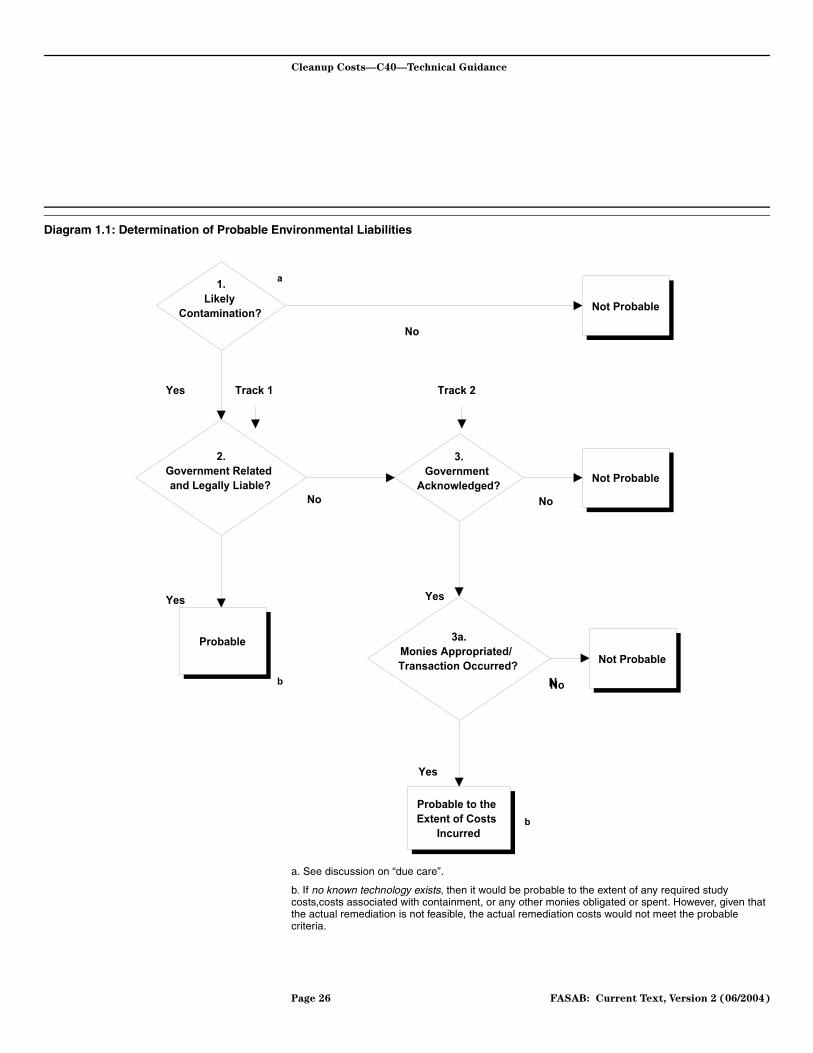

.3005 Diagram 1.1 illustrates the above tests. These tests for probability assume that a past transaction or event has occurred (i.e., past or present operation, contribution and/or transportation of waste), and apply to both active and closed sites. A narrative discussion of each of these tests for probability follows on Diagram 1.1.

Page 25 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40—Technical Guidance

Diagram 1.1: Determination of Probable Environmental Liabilities

a. See discussion on “due care”.

b. If no known technology exists, then it would be probable to the extent of any required study costs,costs associated with containment, or any other monies obligated or spent. However, given that the actual remediation is not feasible, the actual remediation costs would not meet the probable criteria.

��

������

�� ��� ������ ��� ���

�

��

��������� ��� ���

�� ��� ��� �� ����

���

�

��� ���

���

��

���������

�������������� ��� ���

�

� �

���� �!!�!�� ���"

#� �� ���� $��%�����

���

��� ��� � �&�

'(���� ) ���

*��%����

���

�� ��� ���

��

�

#� �� � #� �� �

�

Page 26 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40—Technical Guidance

.3006 Diagram 1.1 shows that there are two primary tracks for determining whether a federal agency’s environmental responsibilities meet the probable criterion. The first track is when contamination is known, is related to federal government operations, and represents a legal liability. The second track is when the federal government knows of contamination, and although the contamination is not government related and the government is not legally liable, the government acknowledges financial responsibility for cleanup. For both tracks, if no known technology exists, then the probability criterion is met only to the extent of likely expenditures (e.g., for study costs and containment). A more detailed discussion of the various components of Diagram 1.1 follows.

1. Likely Contamination: If the agency has exercised due care in determining the presence of contamination and as a result, believes it is unlikely that contamination (for which it is responsible) exists, then the probability criterion is not met. However, if the relevant agency is aware of contamination, having used the due care criteria (see below), then the agency must determine whether the contamination is government related and the federal government (i.e., the agency) is legally liable.

Due care refers to a reasonable effort to identify the presence or likely presence of contamination. Due care is considered to be exercised if an agency has effective policies and procedures in place to routinely attempt to identify contamination and forward that information to the responsible agency official. Procedures that are evidence of the exercise of due care may include, but are not limited to, the following:

• review of recorded chain-of-title documents (including restrictions, covenants and any possible liens) and good faith inquiry and investigation into prior uses of the property

• investigation of aerial photographs that are available

through government agencies that may reflect prior uses;

• analyses to estimate the existence of uninvestigated sites based on information from known sites;

• inquiry into records that are available from federal, state, and/or local jurisdictions that show whether

Page 27 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40—Technical Guidance

there has been a release or potential release of hazardous substances on the property (and adjacent property, if suspected contaminators exist);

• visual site inspection of any portions of the property where environmental contamination is likely or suspected, and

• investigation of complaints regarding abnormal health conditions.

2. Government Related and Legally Liable13: As it relates to environmental damage/contamination, government related events are those where a governmental entity either caused

contamination (i.e., contribution of waste)or is otherwise related to it in such a way that it is legally liable to clean up the contamination. If the agency believes it is more likely than not that it will be legally liable, then the probability criterion is met.14

3. Government Acknowledged Financial Responsibility: If environmental contamination is not government related, then the agency, under its statutory programmatic authority, must determine whether it is authorized to formally accept financial responsibility for cleanup.15 If the government does not accept financial responsibility, then the probability criterion is not met.

13 Legally liable is defined, generally, as any duty, obligation or responsibility established by a statute, regulation, or court decision, or where the agency has agreed, in an interagency agreement, settlement agreement, or similar legally binding document, to assume responsibility for cleanup costs. Legal liability should be determined in consultation with the entity’s legal counsel. [See American Bar Association’s (ABA) Statement of Policy Regarding Lawyers Responses to Auditors’ Request for Information (December 1975). Also see American Institute of Certified Public Accountants (AICPA) Professional Standards, Auditing Standards (AU) Section 337C — source SAS No. 12.] See Subject Area Section L40 in this Volume.

14 Federal entities should consider the Environmental Protection Agency’s (EPA) National Priorities List [which identifies “potentially responsible parties” (PRP)] when determining probability.

15 The Federal government has broad responsibility to provide for the public’s general welfare. The Federal government has established programs to fulfill many of the general needs of the public and often assumes responsibilities for which it has no prior legal obligation. SFFAS5,¶ 30.

Page 28 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40—Technical Guidance

3a. Monies Appropriated/Transaction Occurred: If an agency accepts financial responsibility under No. 3 above,16 then the agency determines the extent of probability based on appropriation or authorization legislation and whether a transaction has occurred causing another party to expect payment (e.g., contractor has performed cleanup of a site). For example, if the federal government has acknowledged responsibility for cleaning up a site, the cost of which is at $10 million, and $2 million has been appropriated but only $1 million in services have been rendered, probable is only met to the extent of $1 million. In the case of government acknowledged events, both conditions (i.e., appropriations or authorization and transaction executed) must exist for the probability criterion to be met.

4. No Known Remediation Technology Exists: In the case of a government related event, where there is no known technology to clean up a particular site, then known costs, for which the entity is responsible, such as a remedial investigation/feasibility study (RI/FS) and/or costs to contain the contamination, meet the probability test. With no known remediation technology, actual remediation is not feasible and therefore the outflow of resources for remediation is not probable.

16 This Technical Release does not propose a position regarding environmental contamination caused by natural disasters which may become the responsibility of the Federal Emergency Management Agency (FEMA).

Description of Issue .3007 An agency is required to recognize a liability for environmental cleanup costs resulting from past transactions or events when a future outflow or other sacrifice of resources is probable and reasonably estimable. Concerns have been raised about when costs associated with environmental damage meets the probable and reasonably estimable criteria. Reasonably estimable relates to the ability to reliably quantify in monetary terms the outflow of resources that will be required. This section addresses only the “reasonably estimable” part of this requirement; probable was addressed in Section 1.17

Key Determinants and Positions

.3008 Various key factors (tests) should be considered in determining whether future outflows of resources can be reasonably estimated. The factors are:

1. Completion of a Remedial Investigation/Feasibility Study (RI/FS)18 or other Study,

2. Experience with Similar Site and/or Conditions, and

3. Availability of Remediation Technology.

17 Disclosure requirements when the criteria for reasonably estimable are not met are as follows:

– the nature of the environmental damage and– an estimate of the possible liability, an estimate of the range of the possible liability,

or a statement that such an estimate cannot be made.

18 A remedial investigation/feasibility study (RI/FS) is a comprehensive environmental data collection and site characterization study (RI) that evaluates alternative cleanup actions and recommends one (FS).

Page 30 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40—Technical Guidance

.3009 These tests for reasonably estimable are applied after a transaction or event has occurred that meets the definition of “probable” as discussed in Section 1; tests apply to both active and closed sites. The analysis should consider all significant sites, with the information rolled up into an entity wide estimate. Cost estimates should be based on current technology. Diagram 2.1, below, illustrates the application of these tests. A discussion of each of the three tests follows Diagram 2.1. The discussion concludes with issues related to quantification of the estimate and guidance for active sites. Overall, it must be emphasized that every effort should be made to develop an estimate.

Page 31 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40—Technical Guidance

Diagram 2.1: Determination and Quantification of Reasonably Estimable Environmental Liabilities

a Probable refers to track 1 (government related) which is found in Section 1. Track 2 (government acknowledged) is not applicable.b With all tracks, see SFFAS #6 PAR. 107-111 and SFFAS #5 par. 40-42 for disclosure requirements.

1. RI/FS or other

Study Completed?

2. Experience w/

Similar Site and/or Conditions?

Not Currently Reasonably

Estimable

Reasonably Estimable

4. Recognize Best Estimate or Low End of Range* at

Current Cost

Recognize Estimated Cost of Study, if required

3. Technology Available to Remediate?

Remediation Not Reasonably

Estimable

Recognize Estimated

Cost to Contain

ProbableFrom

Probable Section

b

a

YesNo

Yes

No No Yes

bb

*Low end of range could be containment, if containment is chosen as the option to be pursued.

Page 32 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40—Technical Guidance

.3010 Diagram 2.1 begins with the assumption that costs associated with environmental damage has already met the test for probable. This is a direct continuation of the left-side track of Diagram 1.1 on the definition of probable (i.e., the agency has met probable under government related and is legally liable; see Section 1). As it relates to the “probable” second track (i.e., government acknowledged), probable is only met to the extent that monies have been appropriated or authorized (through authorization legislation) and costs have been incurred (e.g., services rendered). In these situations, a definitive dollar figure has already been determined and an estimate is not required. Therefore, the following discussion refers to determining whether something is “reasonably estimable” only as it relates to government related and legally liable.

1. Completion of RI/FS or other Study: The first test in determining whether costs are reasonably estimable is to ascertain whether there is a completed study upon which to base an estimate. For example, if a remedial investigation/ feasibility study (RI/FS) has been completed for a particular site, the RI/FS would form the basis upon which to begin estimating the liability.

The fact that an agency does not have a department- wide

comprehensive study completed does not exempt an agency from making its best effort to estimate a liability for financial statement purposes, or for recognizing a liability for that portion of its obligation that can be estimated.

If the results of the study indicate that no contamination exists, then probability is not met and the decision process of Diagram 2.1 should be considered complete.

2. Experience With Similar Site and/or Conditions: If no study has been completed, the next test is to determine whether a site appears to be similar to any other site or condition where experience has been gained through either a completed study or actual remediation. Similar sites or conditions could be related to other federal entities or private sector corporations. A “site” is defined as a physical place where contamination has occurred. A “location” can be composed of many sites; a site can contain many “conditions.” It may be practical for an agency to combine similar conditions or sites into one large site or location.

Page 33 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40—Technical Guidance

If there is a similar site or condition with experience gained (through actual cleanup and/or a completed study to compare), the estimate for recognizing a liability for a site could be based on the similar experience or conditions. In addition, the estimated cost of a future study (if required) should be recognized. Future studies could result in improved estimates. If there is no comparable site and/or condition, remediation costs for a site would not be considered reasonably estimable at that time, but the agency would recognize the anticipated cost of conducting a future study, if required, plus any other identifiable costs.

3. Availability of Remediation Technology: Assuming a study has been completed, or an agency or other entity has experience with a similar site and/or condition as noted above, the next test is whether there is technology available to remediate a site. If no remediation technology exists, then remediation costs would not be reasonably estimable, but the agency would be required to recognize the costs to contain the contamination and any other relevant costs, such as costs of future studies. If technology is available, then remediation costs are reasonably estimable, and the agency would recognize the best estimate at current cost. If no amount within a range of estimates is a better estimate than any other amount, the minimum amount in the range would be recognized. If the estimate is based on similar site criteria, the agency would also recognize the anticipated cost of its own RI/FS or other study, if required.

Page 34 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40—Technical Guidance

In certain instances, the RI/FS or other study may conclude that even though technology does exist to remediate, containment should be considered as one of the options by the agency. If the agency has yet to make a decision and they may in fact choose containment rather than remediation, and assuming containment is not precluded by other involved parties (i.e., by EPA, individual states and/or local jurisdictions), the agency would consider the estimated cost of containment when calculating the estimated costs to be recognized or disclosed. The agency would calculate an amount to be recognized based on the type and length of containment required.19

If management has not determined what remedial action should be taken for a contaminated active site, the cost of containment at the end of the facility’s useful life, plus the cost of a study, if not yet done, should be considered as the low end of the range of future estimated cleanup costs.

4. Quantification of the Estimate: According to paragraph 39 of the SFFAS5 on contingent liabilities, the estimated liability may be a specific amount or a range of amounts. If some amount within the range is a better estimate than any other amount within the range, that amount is recognized. If no amount within the range is a better estimate than any other amount, the minimum amount in the range is recognized. According to SFFAS6, ¶95, estimated costs should be based on the cleanup plan, assuming current technology and current cost.

Changes in environmental liability estimates related to PP&E should be accounted for in accordance with SFFAS6. For general PP&E, SFFAS6 requires that the portion of the re-estimate related to current and prior periods be recognized as an expense in the period of the change. For stewardship PP&E, SFFAS6

19 RCRA (Resource Conservation and Recovery Act) regulations require owners of hazardous waste disposal facilities to implement post-closure maintenance and monitoring activities for a minimum of 30 years. When developing estimates of these operation and maintenance (O&M) costs, EPA generally assumes that O&M activities will be required for 30 years. In most instances, containment costs should be determined on the basis of a minimum of 30 years. It would be expected that in the case of nuclear contamination, different tri-party agreements, technical problems, or other circumstances may lead to the use of a substantially longer time frame than for typical RCRA or CERCLA (Comprehensive Environmental Response Compensation and Liability Act of 1980) sites.

Page 35 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40—Technical Guidance

requires that the change in estimate be expensed for the incremental costs identified in the re-estimate and the liability adjusted in the period of the change.

Where an agency is one of several potentially responsible parties (PRP’s) under CERCLA and management has determined that more likely than not the agency is legally liable, the agency should include an estimated liability for its:

1. allocable share of the liability for a specific site, and

2. share of amounts related to the site that will not be paid by other PRP’s.20

If an agency shares responsibility with nongovernmental PRP’s for a government related event, the agency should recognize the share that management believes it is more likely than not the agency is legally liable for.21 Where the federal government shares responsibility with nongovernmental PRP’s and agency management has decided to accept the nongovernmental PRP’s share of the responsibility for the damage (i.e., a government acknowledged event), the agency would also recognize a liability for the PRP’s share once the criteria of appropriation or authorization legislation and a transaction have occurred, causing another party to expect payment (e.g., contractor has performed site cleanup).

20 AICPA Statement of Position (SOP) 96-1, Environmental Remediation Liabilities, page 43 par. 6.2.

21 If management determines that an agency should assume responsibility for a portion of another PRP’s share of the liability, the agency may recognize a receivable from the other PRP when the federal entity establishes a claim to cash or other assets against the other PRP based on the related legal provisions (i.e., a legal instrument, such as a settlement agreement, or other objective, verifiable information). Losses on receivables should be recognized when it is more likely than not that the receivables will not be collected in total.

Page 36 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40—Technical Guidance

Guidance for Active Sites

.3011 Thus far, this technical release has dealt with costs for past

environmental contamination of property, plant, and equipment (PP&E) related to active and closed sites. In addition, SFFAS6 outlines accounting treatment for future environmental contamination of PP&E at active sites. The following shows how environmental cleanup costs22 for active sites should be recognized for general and stewardship PP&E under SFFAS6.

General PP&E .3012 There are two implementation methods for general PP&E in service at the effective date of the standard. Under the first method, the agency would estimate the total cleanup costs (based on current cost to perform the cleanup23) that will be required at the end of the PP&E’s useful life. The agency would recognize the estimated cost as a prior period adjustment for the portion of the total estimated cleanup costs related to that portion of the PP&E’s useful life that

has already expired.

.3013 To illustrate, assume implementation of SFFAS6 on October 1, 1996. Using the illustration below, and assuming a facility was placed in service at the beginning of fiscal year 1992 with a 20-year useful life, the agency would first estimate the total costs (based on current cost) required to clean up the contaminated facility at the presumed plant closure at the end of fiscal year 2011 ($20 billion). From that estimate (as of October 1, 1996), the amount that relates to that portion of the PP&E’s useful life that has already expired (4/20 of $20 billion, or $4 billion) would be charged to net position and the fiscal year 1996 prorata portion would be charged to expense.

22 Costs referred to in this section are for decontamination and decommissioning (D&D) only, not operating costs. D&D costs are those incurred after plants or equipment become inactive and require cleanup. Operating costs are period costs that flow through the Statement of Operations and Changes in Net Position. A liability is not recognized for operating costs.

23 Current cost should be based on existing laws, technology and management plans (SFFAS6, ¶188).

Page 37 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40—Technical Guidance

.3014 Beginning with fiscal year 1997, the agency would annually recognize a prorata portion of the estimated total cleanup costs based on the remaining useful life of the subject PP&E. In our example, for fiscal year 1997, for this plant (with an estimated remaining useful life of 15 years), the agency would recognize 1/15 of the total estimated remaining cleanup cost of $15 billion, or $1 billion. The probable criterion was met under Diagram 1.1 once the PP&E was placed in service. The reasonably estimable criterion was met with the agency’s development of an overall estimate of total cleanup costs using the process indicated in Diagram 2.1. Consequently, each years’ allocation of cleanup costs is both probable and reasonably estimable, thus requiring the agency to recognize a liability. The allocation method used for cleanup costs, as described above, is similar to depreciation of general PP&E.

.3015 Changes in estimates of cleanup costs should be accounted for in accordance with the SFFAS6, which requires that the cumulative effect of changes in total estimated cleanup costs related to current and past operations be recognized as expense, and the liability adjusted in the period of the change in estimate.

Oct 1,1991 1996 2011

1) Estimate total cleanup costs for facility ($20 billion)

Today's Date:

Sept. 30, 1996

2) Book cleanup costs

related to prior useful

life

3) Annually book prorata

portion of cleanup costs for

remaining useful life

Active Facility

General PP&E

Placed in service

Page 38 FASAB: Current Text, Version 2 (06/2004)

Cleanup Costs—C40—Technical Guidance

.3016 SFFAS6 allows a second method for recognizing cleanup cost related to general PP&E in service at the effective date of the standard. The alternative method provides that “if costs are not intended to be recovered primarily through user charges, management may elect to recognize the estimated total [ultimate] cleanup cost as a liability upon implementation of the standard.”24

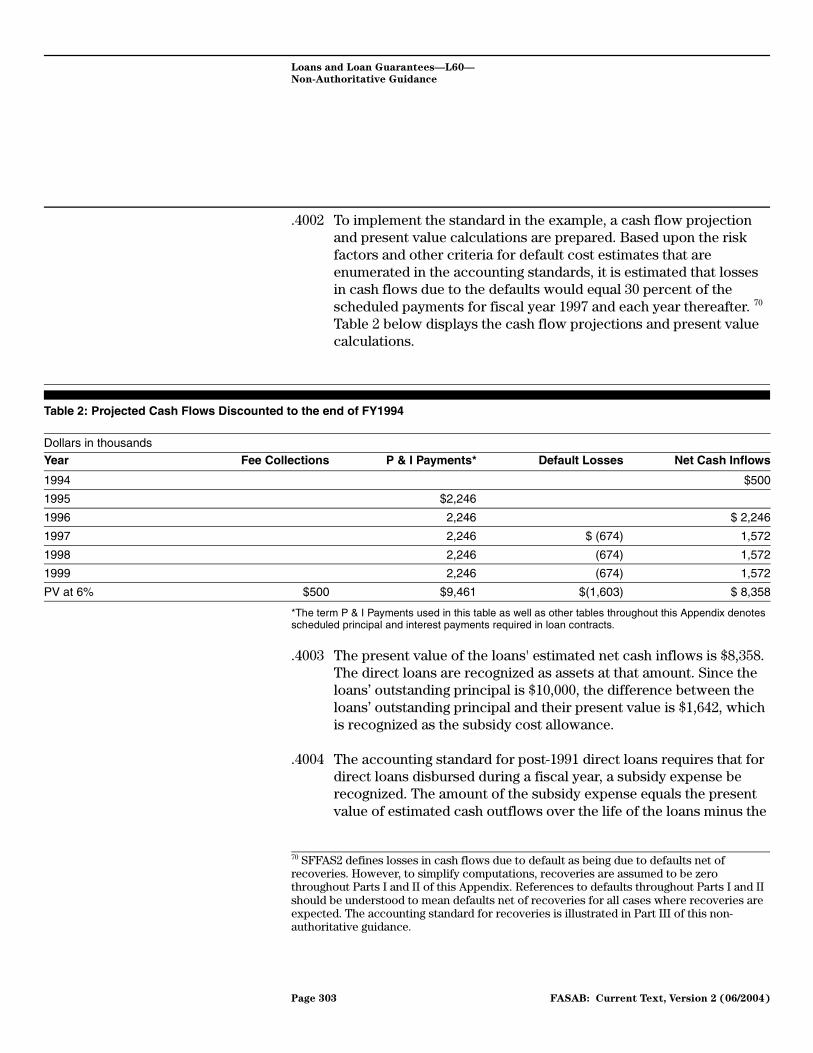

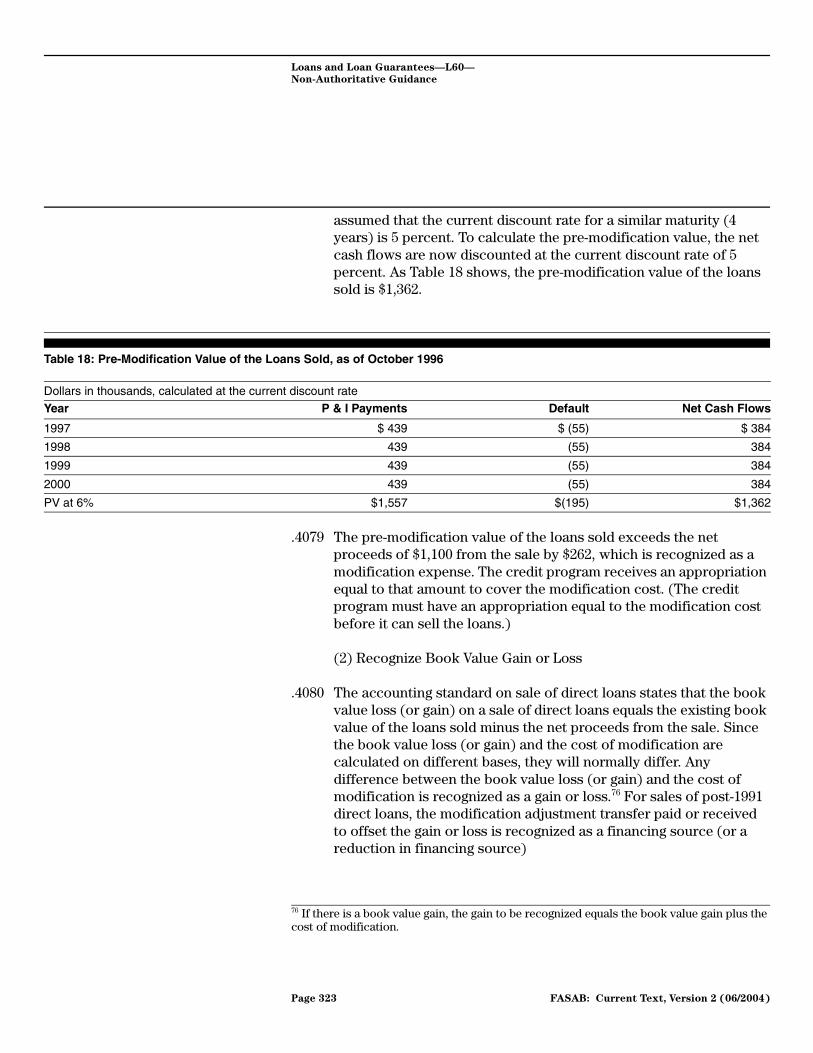

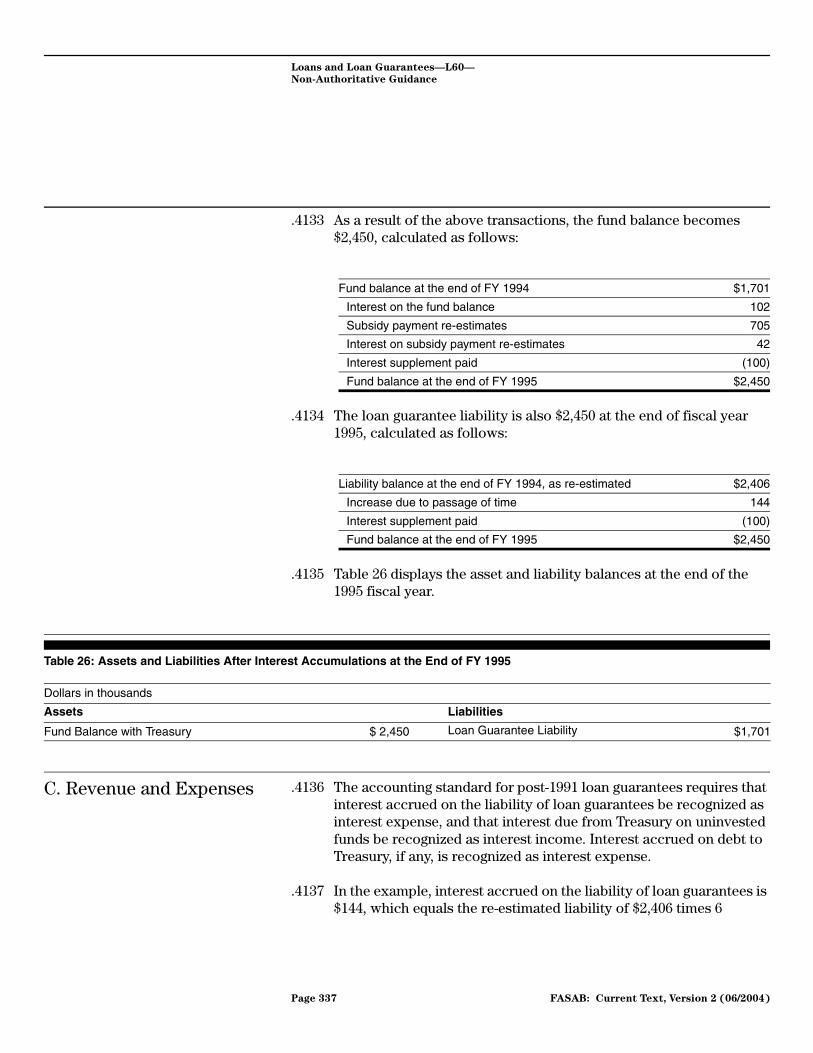

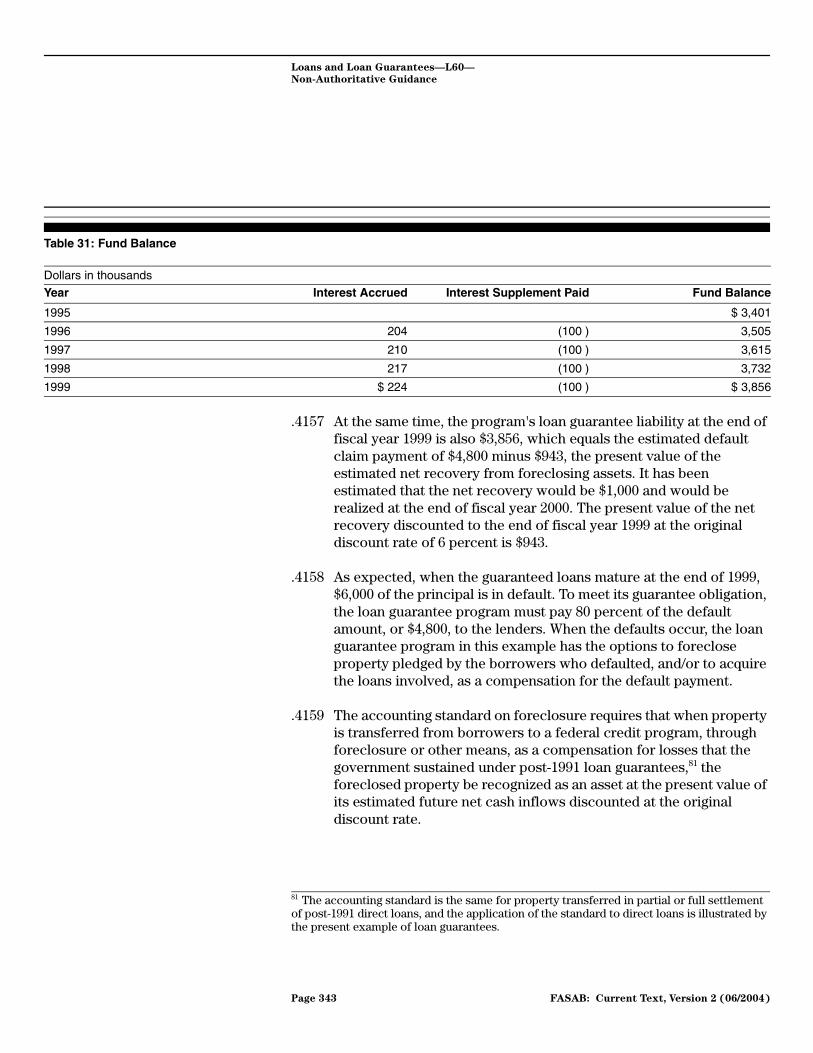

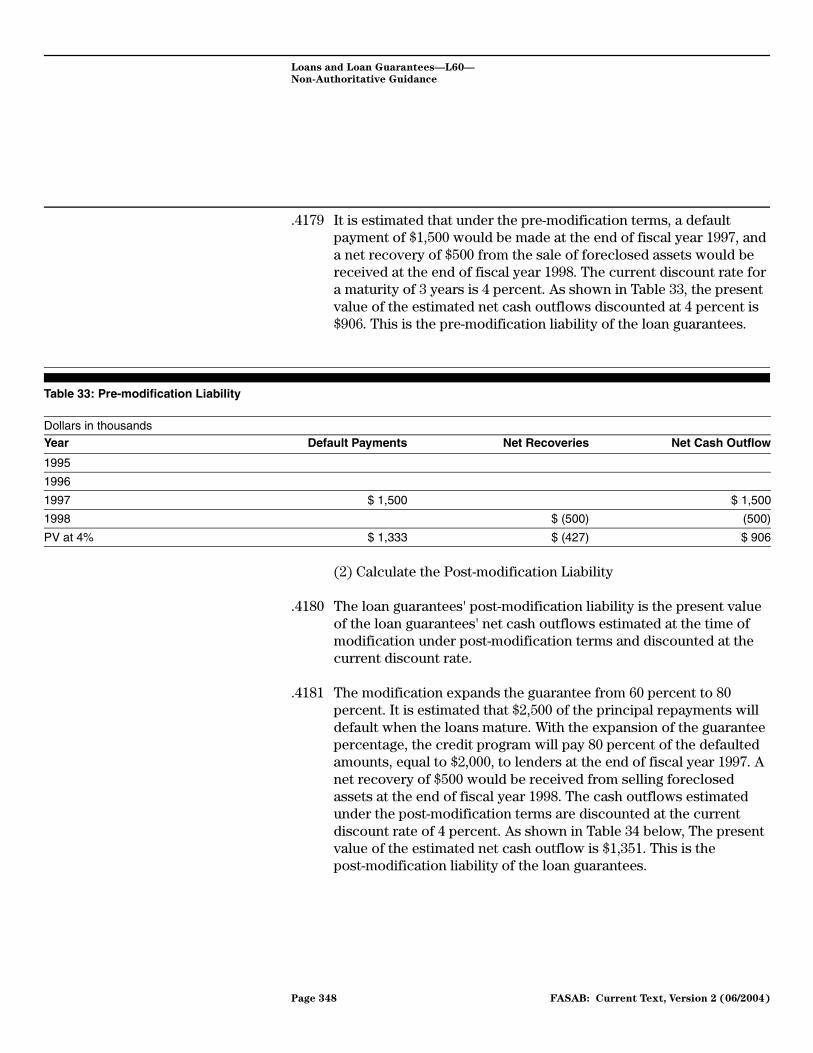

.3017 For general PP&E placed in service after the effective date of the standard, the agency should estimate the total cleanup costs25 related to the PP&E and recognize annually a prorata portion of the costs over the life of the asset. Expense recognition shall begin on the date that the PP&E is placed into service.