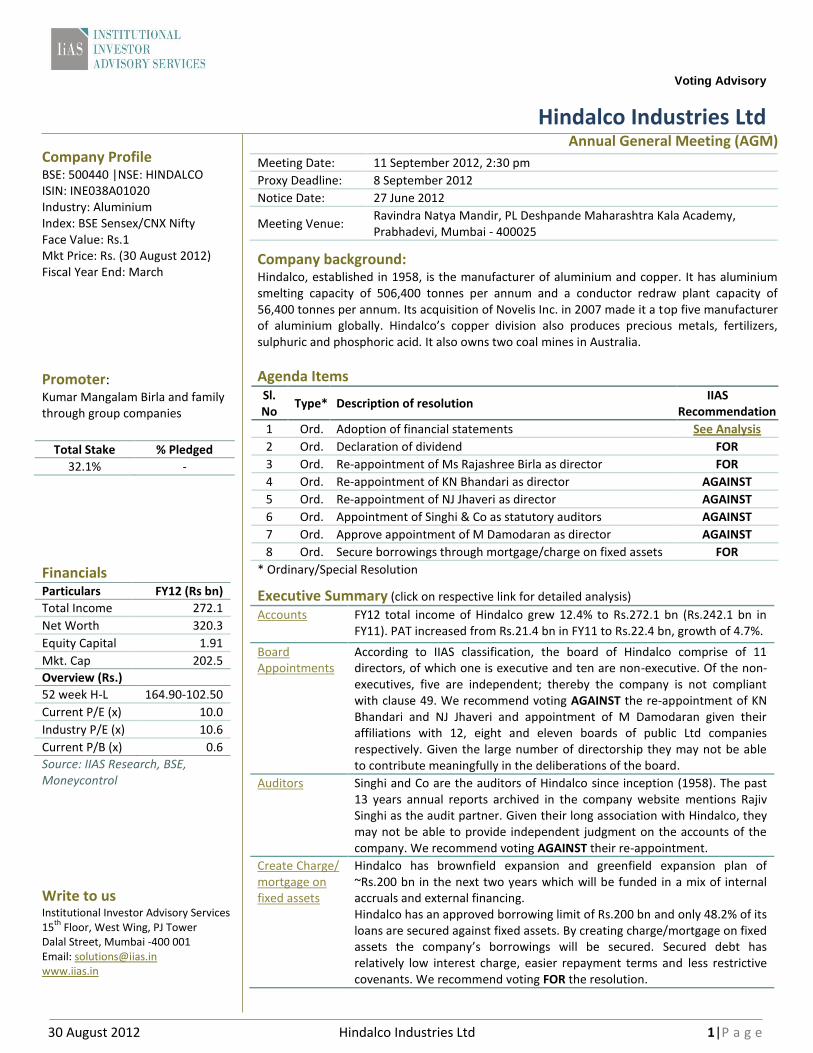

Voting Advisory 30 August 2012 Hindalco Industries Ltd 1|Page Hindalco Industries Ltd Company Profile BSE: 500440 |NSE: HINDALCO ISIN: INE038A01020 Industry: Aluminium Index: BSE Sensex/CNX Nifty Face Value: Rs.1 Mkt Price: Rs. (30 August 2012) Fiscal Year End: March Promoter: Kumar Mangalam Birla and family through group companies Total Stake % Pledged 32.1% - Financials Particulars FY12 (Rs bn) Total Income 272.1 Net Worth 320.3 Equity Capital 1.91 Mkt. Cap 202.5 Overview (Rs.) 52 week H-L 164.90-102.50 Current P/E (x) 10.0 Industry P/E (x) 10.6 Current P/B (x) 0.6 Source: IIAS Research, BSE, Moneycontrol Write to us Institutional Investor Advisory Services 15 th Floor, West Wing, PJ Tower Dalal Street, Mumbai -400 001 Email: [email protected]www.iias.in Annual General Meeting (AGM) Meeting Date: 11 September 2012, 2:30 pm Proxy Deadline: 8 September 2012 Notice Date: 27 June 2012 Meeting Venue: Ravindra Natya Mandir, PL Deshpande Maharashtra Kala Academy, Prabhadevi, Mumbai - 400025 Company background: Hindalco, established in 1958, is the manufacturer of aluminium and copper. It has aluminium smelting capacity of 506,400 tonnes per annum and a conductor redraw plant capacity of 56,400 tonnes per annum. Its acquisition of Novelis Inc. in 2007 made it a top five manufacturer of aluminium globally. Hindalco’s copper division also produces precious metals, fertilizers, sulphuric and phosphoric acid. It also owns two coal mines in Australia. Agenda Items Sl. No Type* Description of resolution IIAS Recommendation 1 Ord. Adoption of financial statements See Analysis 2 Ord. Declaration of dividend FOR 3 Ord. Re-appointment of Ms Rajashree Birla as director FOR 4 Ord. Re-appointment of KN Bhandari as director AGAINST 5 Ord. Re-appointment of NJ Jhaveri as director AGAINST 6 Ord. Appointment of Singhi & Co as statutory auditors AGAINST 7 Ord. Approve appointment of M Damodaran as director AGAINST 8 Ord. Secure borrowings through mortgage/charge on fixed assets FOR * Ordinary/Special Resolution Executive Summary (click on respective link for detailed analysis) Accounts FY12 total income of Hindalco grew 12.4% to Rs.272.1 bn (Rs.242.1 bn in FY11). PAT increased from Rs.21.4 bn in FY11 to Rs.22.4 bn, growth of 4.7%. Board Appointments According to IIAS classification, the board of Hindalco comprise of 11 directors, of which one is executive and ten are non-executive. Of the non- executives, five are independent; thereby the company is not compliant with clause 49. We recommend voting AGAINST the re-appointment of KN Bhandari and NJ Jhaveri and appointment of M Damodaran given their affiliations with 12, eight and eleven boards of public Ltd companies respectively. Given the large number of directorship they may not be able to contribute meaningfully in the deliberations of the board. Auditors Singhi and Co are the auditors of Hindalco since inception (1958). The past 13 years annual reports archived in the company website mentions Rajiv Singhi as the audit partner. Given their long association with Hindalco, they may not be able to provide independent judgment on the accounts of the company. We recommend voting AGAINST their re-appointment. Create Charge/ mortgage on fixed assets Hindalco has brownfield expansion and greenfield expansion plan of ~Rs.200 bn in the next two years which will be funded in a mix of internal accruals and external financing. Hindalco has an approved borrowing limit of Rs.200 bn and only 48.2% of its loans are secured against fixed assets. By creating charge/mortgage on fixed assets the company’s borrowings will be secured. Secured debt has relatively low interest charge, easier repayment terms and less restrictive covenants. We recommend voting FOR the resolution.

Transcript

Voting Advisory

30 August 2012 Hindalco Industries Ltd 1|P a g e

Hindalco Industries Ltd

Company Profile BSE: 500440 |NSE: HINDALCO ISIN: INE038A01020 Industry: Aluminium Index: BSE Sensex/CNX Nifty Face Value: Rs.1 Mkt Price: Rs. (30 August 2012) Fiscal Year End: March

Promoter: Kumar Mangalam Birla and family through group companies

Total Stake % Pledged

32.1% -

Financials Particulars FY12 (Rs bn)

Total Income 272.1

Net Worth 320.3

Equity Capital 1.91

Mkt. Cap 202.5

Overview (Rs.)

52 week H-L 164.90-102.50

Current P/E (x) 10.0

Industry P/E (x) 10.6

Current P/B (x) 0.6

Source: IIAS Research, BSE, Moneycontrol

Write to us Institutional Investor Advisory Services 15

Company background: Hindalco, established in 1958, is the manufacturer of aluminium and copper. It has aluminium smelting capacity of 506,400 tonnes per annum and a conductor redraw plant capacity of 56,400 tonnes per annum. Its acquisition of Novelis Inc. in 2007 made it a top five manufacturer of aluminium globally. Hindalco’s copper division also produces precious metals, fertilizers, sulphuric and phosphoric acid. It also owns two coal mines in Australia.

Agenda Items Sl. No

Type* Description of resolution IIAS

Recommendation

1 Ord. Adoption of financial statements See Analysis

2 Ord. Declaration of dividend FOR

3 Ord. Re-appointment of Ms Rajashree Birla as director FOR

4 Ord. Re-appointment of KN Bhandari as director AGAINST

5 Ord. Re-appointment of NJ Jhaveri as director AGAINST

6 Ord. Appointment of Singhi & Co as statutory auditors AGAINST

7 Ord. Approve appointment of M Damodaran as director AGAINST

8 Ord. Secure borrowings through mortgage/charge on fixed assets FOR

* Ordinary/Special Resolution

Executive Summary (click on respective link for detailed analysis)

Accounts FY12 total income of Hindalco grew 12.4% to Rs.272.1 bn (Rs.242.1 bn in FY11). PAT increased from Rs.21.4 bn in FY11 to Rs.22.4 bn, growth of 4.7%.

Board Appointments

According to IIAS classification, the board of Hindalco comprise of 11 directors, of which one is executive and ten are non-executive. Of the non-executives, five are independent; thereby the company is not compliant with clause 49. We recommend voting AGAINST the re-appointment of KN Bhandari and NJ Jhaveri and appointment of M Damodaran given their affiliations with 12, eight and eleven boards of public Ltd companies respectively. Given the large number of directorship they may not be able to contribute meaningfully in the deliberations of the board.

Auditors Singhi and Co are the auditors of Hindalco since inception (1958). The past 13 years annual reports archived in the company website mentions Rajiv Singhi as the audit partner. Given their long association with Hindalco, they may not be able to provide independent judgment on the accounts of the company. We recommend voting AGAINST their re-appointment.

Create Charge/ mortgage on fixed assets

Hindalco has brownfield expansion and greenfield expansion plan of ~Rs.200 bn in the next two years which will be funded in a mix of internal accruals and external financing. Hindalco has an approved borrowing limit of Rs.200 bn and only 48.2% of its loans are secured against fixed assets. By creating charge/mortgage on fixed assets the company’s borrowings will be secured. Secured debt has relatively low interest charge, easier repayment terms and less restrictive covenants. We recommend voting FOR the resolution.

3 Yrs: 11 August 2009 to 10 August 2012 5 Yrs: 11August 2007 to 10 August 2012 Source: IIAS Research

Public Shareholders >1%

Sl. No. Name of the Shareholder No. of Shares held

(millions) Shares as % of Total No.

of Shares

1 Life Insurance Corporation Of India & Its associate Funds 192.6 10.1

2 Franklin Templeton Investment Funds 72.4 3.8

3 Bajaj Allianz Life Insurance Company Ltd 36.6 1.9

4 Vanguard Emerging Markets Stock Index Fund 19.9 1.0

Total 321.6 16.8

Source: BSE

Change in Shareholding Pattern (%) Period Promoter DII FII Others

Jun-12 32.1 15.3 25.8 26.9

Mar-12 32.1 14.9 26.9 26.2

Dec-11 32.1 15.6 26.5 25.9

Mar-11 32.1 13.0 30.9 24.1

Mar-10 32.1 15.7 28.9 23.3

Mar-09 36.1 18.6 10.3 35.0

Mar-08 31.4 15.1 13.0 40.4

Mar-07 27.1 14.7 18.6 39.7

Source: BSE

Shareholding Pattern

Source: BSE, as at 30 June 2012

-2.0%

-27.0%

-2.2% -12.7%

21.9% 19.1%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

3 YR 5 YR

Hindalco Sensex Nifty

Promoter, 32.1

DII, 15.3 FII, 25.8

Others, 26.9

Voting Advisory

30 August 2012 Hindalco Industries Ltd 3|P a g e

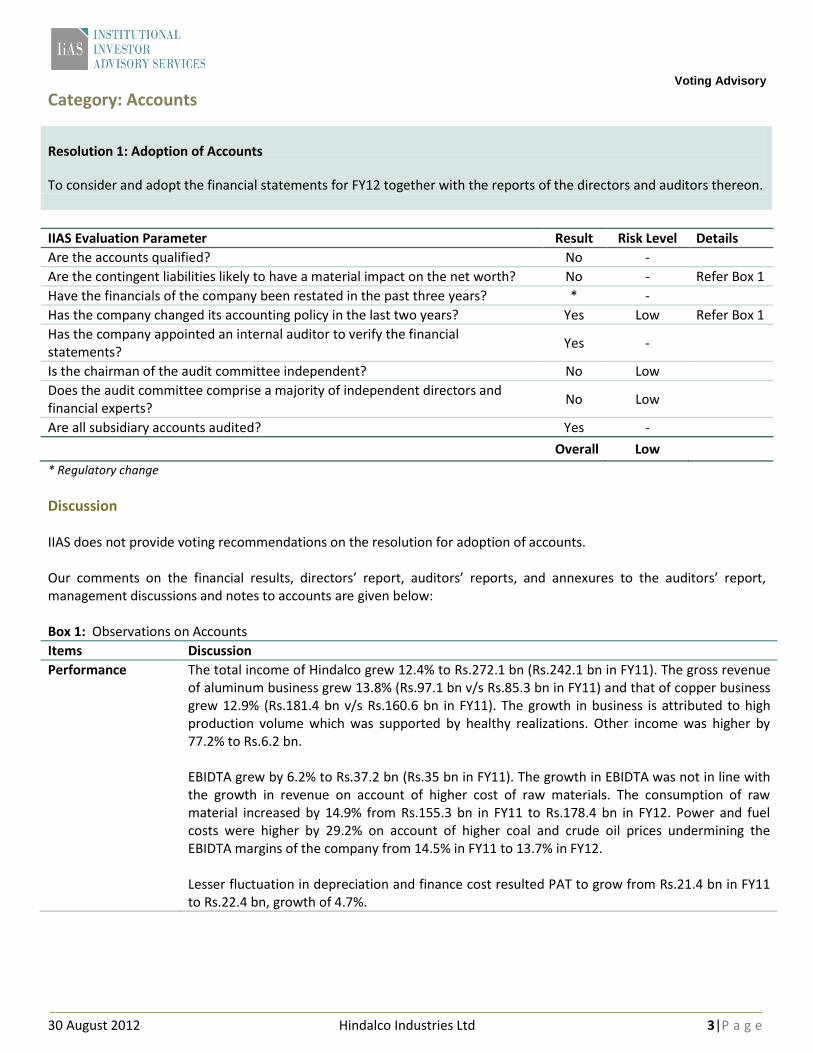

Category: Accounts

IIAS Evaluation Parameter Result Risk Level Details

Are the accounts qualified? No -

Are the contingent liabilities likely to have a material impact on the net worth? No - Refer Box 1

Have the financials of the company been restated in the past three years? * -

Has the company changed its accounting policy in the last two years? Yes Low Refer Box 1

Has the company appointed an internal auditor to verify the financial statements?

Yes -

Is the chairman of the audit committee independent? No Low

Does the audit committee comprise a majority of independent directors and financial experts?

No Low

Are all subsidiary accounts audited? Yes -

Overall Low * Regulatory change

Discussion IIAS does not provide voting recommendations on the resolution for adoption of accounts. Our comments on the financial results, directors’ report, auditors’ reports, and annexures to the auditors’ report, management discussions and notes to accounts are given below: Box 1: Observations on Accounts

Items Discussion

Performance The total income of Hindalco grew 12.4% to Rs.272.1 bn (Rs.242.1 bn in FY11). The gross revenue of aluminum business grew 13.8% (Rs.97.1 bn v/s Rs.85.3 bn in FY11) and that of copper business grew 12.9% (Rs.181.4 bn v/s Rs.160.6 bn in FY11). The growth in business is attributed to high production volume which was supported by healthy realizations. Other income was higher by 77.2% to Rs.6.2 bn. EBIDTA grew by 6.2% to Rs.37.2 bn (Rs.35 bn in FY11). The growth in EBIDTA was not in line with the growth in revenue on account of higher cost of raw materials. The consumption of raw material increased by 14.9% from Rs.155.3 bn in FY11 to Rs.178.4 bn in FY12. Power and fuel costs were higher by 29.2% on account of higher coal and crude oil prices undermining the EBIDTA margins of the company from 14.5% in FY11 to 13.7% in FY12. Lesser fluctuation in depreciation and finance cost resulted PAT to grow from Rs.21.4 bn in FY11 to Rs.22.4 bn, growth of 4.7%.

Resolution 1: Adoption of Accounts

To consider and adopt the financial statements for FY12 together with the reports of the directors and auditors thereon.

Voting Advisory

30 August 2012 Hindalco Industries Ltd 4|P a g e

Business Segment The company has three reporting business segments, viz, aluminium, copper and others. ‘Aluminium’ business comprises hydrate & alumina, aluminium and other aluminium products. ‘Copper’ business comprises continuous cast copper rods, copper cathode, sulphuric acid, DAP & complexes, gold and silver. ‘Other’ business comprises caustic and others. Table 1: FY12 Contribution to revenue and EBIT

Particulars (Rs bn) Aluminium Copper Others Total

Revenue 621.2 183.8 6.1 811.1

Contribution to revenue 76.6% 22.7% 0.8%

EBIT 45.0 11.2 0.8 57.0

Contribution to EBIT 78.9% 19.6% 1.5%

Source: Company

Other observations 1. Issuance of warrants on preferential basis: On 22 March 2012, Hindalco allotted 150 mn warrants on preferential basis to IGH Holdings Private Ltd, Surya Kiran Investments Private Ltd, TGS Investment & Trade Private Ltd and Umang Commercial Company Ltd (promoter group companies) at Rs.144.35 per warrant. The company received Rs.5.4 bn as 25% of the amount to be received upfront and the balance is received before 22 September 2012. The objective for the issuance is to fund the brownfield expansion and greenfield projects of the company. In the previous instance (warrants issued in April 2007) the promoters of the company did not honor the obligation by not opting to convert the warrants into equity shares as the conversion price of warrants was 116% premium to the share price at the date of conversion. If Hindalco forfeits the warrants issued in March 2012, it may impact its capital expenditure plans. 2. Issuances of debentures: In April 2012, Hindalco raised Rs.30 bn through the issuance of secured non-convertible debentures on private placement basis. These debentures carry an interest rate of 9.55% and have a maturity period of 10 years. 3. Concerns (consolidated) a. Changes in accounting policy with respect to recognition of actuarial losses: Until FY11, Hindalco expensed actuarial losses/profits. However the company changed its accounting policy related to recognition of actuarial losses (along with the related deferred tax) of Novelis Inc. by adjusting it from reserves and surplus of the company. The change in accounting is not impacting the cash position. However, if these losses were provided from profit and loss account the employee benefit expenses would have been higher by Rs.10.1 bn and tax expense would have been lower by Rs.3 bn. Simultaneously, net profit for the year would have been lower by Rs.7.2 bn and foreign currency translation reserve would have been lower by Rs.0.4 bn. b. Loss on exiting foil and packing business was provided from reconstruction reserve: Hindalco in FY12 consolidated accounts has provided for cost related to exiting foil and packaging business from Business Reconstruction Reserve. Had this amount been expensed, other expenses would have been higher by Rs.5 bn and Business Reconstruction Reserve would have been higher by equivalent amount. Simultaneously, the net profit of the company would have been lower by Rs.5.4 bn and deferred tax assets would have been higher by Rs.0.4 bn. c. Non consolidation of its share of profit in Idea Cellular Ltd: in FY11, Hindalco did not consolidate its share of profits in Idea Cellular. The same was done in FY12, resulting in the net profits of the company higher by Rs.0.6 bn. Collectively, the above three observations have resulted in the net profit of the company being higher by Rs.12.8 bn. Auditors, Singhi and Co have raised concern on the above observations.

Source: Company Filings, IIAS Research

Voting Advisory

30 August 2012 Hindalco Industries Ltd 5|P a g e

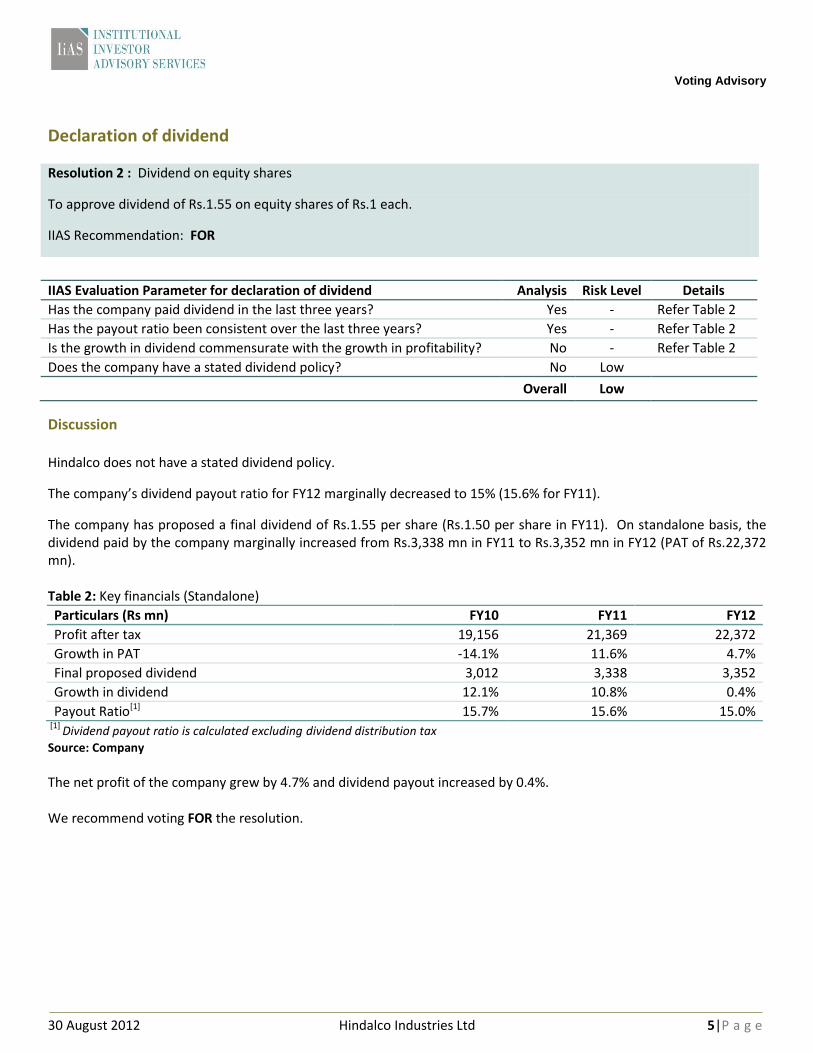

Declaration of dividend

IIAS Evaluation Parameter for declaration of dividend Analysis Risk Level Details

Has the company paid dividend in the last three years? Yes - Refer Table 2

Has the payout ratio been consistent over the last three years? Yes - Refer Table 2

Is the growth in dividend commensurate with the growth in profitability? No - Refer Table 2

Does the company have a stated dividend policy? No Low

Overall Low

Discussion Hindalco does not have a stated dividend policy.

The company’s dividend payout ratio for FY12 marginally decreased to 15% (15.6% for FY11).

The company has proposed a final dividend of Rs.1.55 per share (Rs.1.50 per share in FY11). On standalone basis, the dividend paid by the company marginally increased from Rs.3,338 mn in FY11 to Rs.3,352 mn in FY12 (PAT of Rs.22,372 mn). Table 2: Key financials (Standalone)

Particulars (Rs mn) FY10 FY11 FY12

Profit after tax 19,156 21,369 22,372

Growth in PAT -14.1% 11.6% 4.7%

Final proposed dividend 3,012 3,338 3,352

Growth in dividend 12.1% 10.8% 0.4%

Payout Ratio[1] 15.7% 15.6% 15.0% [1]

Dividend payout ratio is calculated excluding dividend distribution tax

Source: Company

The net profit of the company grew by 4.7% and dividend payout increased by 0.4%. We recommend voting FOR the resolution.

Resolution 2 : Dividend on equity shares

To approve dividend of Rs.1.55 on equity shares of Rs.1 each.

IIAS Recommendation: FOR

Voting Advisory

30 August 2012 Hindalco Industries Ltd 6|P a g e

Category: Board Appointments

Resolution 3: To re-appoint Rajashree Birla as director Resolution 4: To re-appoint KN Bhandari as director Resolution 5: To re-appoint NJ Jhaveri as director Resolution 7: To approve the appointment of M Damodaran as director

IIAS Recommendation: FOR IIAS Recommendation: AGAINST IIAS Recommendation: AGAINST IIAS Recommendation: AGAINST

IIAS Evaluation Parameters for Board Appointments

Parameter Result Risk Level Details

Is the chairman of the board an independent director? No Moderate Refer Table 3

Is there a separation in the roles between the Chairman and CEO? Yes - Refer Table 3

Proportion of independent directors on the board 45%[2] Moderate Refer Table 3

Proportion of non-executive directors on the board 91% - Refer Table 3

Is there at least one woman director on the board? Yes - Refer Table 3

Does the company have policy on the retirement age of directors? No Low

Does the company have a policy on the tenure of independent directors? No Low

Do all the board committees have at least one independent director? Yes -

Is there any whistleblower policy for the independent directors?

Proportion of promoter and promoter relatives on board 18% Low

Overall Low [2]

as per IIAS classification Source: Company Filings, IIAS Research

Table 3: Board Composition

Sl. No

Name of director Director Category

Occupation Age Tenure (years)

% of attendance

Other directorships

[3]

Compensation/Commission

(Rs.mn)

Executive

1

Debnarayan Bhattacharya

Whole time Managing director 64 4 100% 3 195.0

Non-executive

2 Kumar Mangalam Birla

Promoter Chairman 45 NA 71% 9 130.6

3 Ms Rajashree Birla

Non-independent

Promoter 79 16 29% 6 2.5

4 Chaitan Manbhai Maniar

Non-independent

Advocate and Solicitor 75 30 100% 14 1.5

5 Madhukar Manilal Bhagat

Non-independent

Director, Zenith Exports

79 16 100% 4 1.3

6 Kailash Nath Bhandari

Independent Former CMD, New India Assurance

70 7 100% 11 1.5

7 Askaran Agarwala Non-independent

Former president, President of Aluminum Association of India

Category of Appointment Non-executive Independent Independent Independent

IIAS Director Classification - Independent Independent Independent

Independence & tenure -

Attendance x Other Affiliations x x x

Shares Held 612,470 3,571 5,000 -

Compensation Qualification[4]

IIAS Recommendation FOR AGAINST AGAINST AGAINST [4]

Refer Director Profile section

Director Profiles Ms Rajashree Birla M/s Rajashree Birla, 79, is one of the promoters of Hindalco. She is mother of Kumar Mangalam

Birla, Chairman of the company. She is a bachelor of arts and was appointed on the board of Hindalco in March 1996. She was paid a total remuneration of Rs.2.5 mn, comprising Rs.10,000 as sitting fees and Rs.2.5 mn as commission. She holds 612,470 equity shares of Hindalco. She is also a director in six other group companies, listed below- Box 2: Directorships of Ms Rajashree Birla

Public Companies (group companies): i. Grasim Industries Ltd, ii. Aditya Birla Nuvo Ltd, iii. Essel Mining and Industries Ltd, iv. Unltatech Cement Ltd v. Aditya Birla health Services Ltd and vi. Idea Cellular Ltd

Kailash Nath Bhandari

KN Bhandari, 70, is a bachelor in arts and a law graduate. His expertise lies in the field of insurance. He is the ex CMD of New India Assurance company Ltd from 2000 to 2004 and United India Assurance Co Ltd from 1998 to 2000. He is director of Hindalco since January 2006. He attended all the seven board meetings held during the year. He was paid Rs.1.5 mn as total remuneration for FY12 including Rs.90,000 as sitting fees and Rs.1.4 mn as commission. He holds 3,571 equity shares of the company. He is also a director in 11 other public limited companies, listed below- Box 3: Directorships of Kailash Nath Bhandari

Public Companies: i. Agriculture Insurance Company of India Ltd, ii. Andhra Cements Ltd, iii. Shristi Infrastructure Development Corporation Ltd, iv. Su-Raj Diamonds & Jewellery Ltd, v. Saurashtra Cement Ltd. vi. Credence Logistics Ltd, vii. Magma Fincorp Ltd., viii. Magma HDI General Insurance Company Limited, ix. NRC LTE, x. KSL Industries Ltd and xi. Jay Bharat Textile and Real Estate Ltd.

Seeking re-appointment Seeking appointment

Voting Advisory

30 August 2012 Hindalco Industries Ltd 8|P a g e

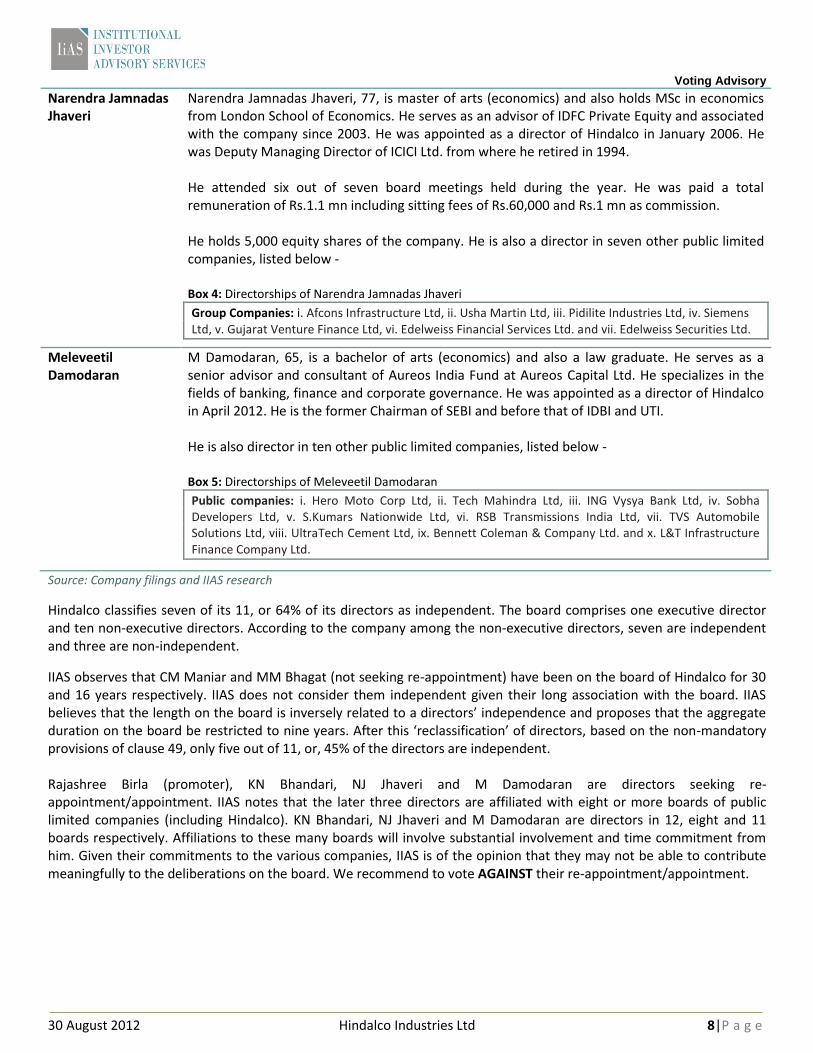

Narendra Jamnadas Jhaveri

Narendra Jamnadas Jhaveri, 77, is master of arts (economics) and also holds MSc in economics from London School of Economics. He serves as an advisor of IDFC Private Equity and associated with the company since 2003. He was appointed as a director of Hindalco in January 2006. He was Deputy Managing Director of ICICI Ltd. from where he retired in 1994. He attended six out of seven board meetings held during the year. He was paid a total remuneration of Rs.1.1 mn including sitting fees of Rs.60,000 and Rs.1 mn as commission. He holds 5,000 equity shares of the company. He is also a director in seven other public limited companies, listed below - Box 4: Directorships of Narendra Jamnadas Jhaveri

Group Companies: i. Afcons Infrastructure Ltd, ii. Usha Martin Ltd, iii. Pidilite Industries Ltd, iv. Siemens Ltd, v. Gujarat Venture Finance Ltd, vi. Edelweiss Financial Services Ltd. and vii. Edelweiss Securities Ltd.

Meleveetil Damodaran

M Damodaran, 65, is a bachelor of arts (economics) and also a law graduate. He serves as a senior advisor and consultant of Aureos India Fund at Aureos Capital Ltd. He specializes in the fields of banking, finance and corporate governance. He was appointed as a director of Hindalco in April 2012. He is the former Chairman of SEBI and before that of IDBI and UTI. He is also director in ten other public limited companies, listed below - Box 5: Directorships of Meleveetil Damodaran

Public companies: i. Hero Moto Corp Ltd, ii. Tech Mahindra Ltd, iii. ING Vysya Bank Ltd, iv. Sobha Developers Ltd, v. S.Kumars Nationwide Ltd, vi. RSB Transmissions India Ltd, vii. TVS Automobile Solutions Ltd, viii. UltraTech Cement Ltd, ix. Bennett Coleman & Company Ltd. and x. L&T Infrastructure Finance Company Ltd.

Source: Company filings and IIAS research

Hindalco classifies seven of its 11, or 64% of its directors as independent. The board comprises one executive director and ten non-executive directors. According to the company among the non-executive directors, seven are independent and three are non-independent.

IIAS observes that CM Maniar and MM Bhagat (not seeking re-appointment) have been on the board of Hindalco for 30 and 16 years respectively. IIAS does not consider them independent given their long association with the board. IIAS believes that the length on the board is inversely related to a directors’ independence and proposes that the aggregate duration on the board be restricted to nine years. After this ‘reclassification’ of directors, based on the non-mandatory provisions of clause 49, only five out of 11, or, 45% of the directors are independent. Rajashree Birla (promoter), KN Bhandari, NJ Jhaveri and M Damodaran are directors seeking re-appointment/appointment. IIAS notes that the later three directors are affiliated with eight or more boards of public limited companies (including Hindalco). KN Bhandari, NJ Jhaveri and M Damodaran are directors in 12, eight and 11 boards respectively. Affiliations to these many boards will involve substantial involvement and time commitment from him. Given their commitments to the various companies, IIAS is of the opinion that they may not be able to contribute meaningfully to the deliberations on the board. We recommend to vote AGAINST their re-appointment/appointment.

Voting Advisory

30 August 2012 Hindalco Industries Ltd 9|P a g e

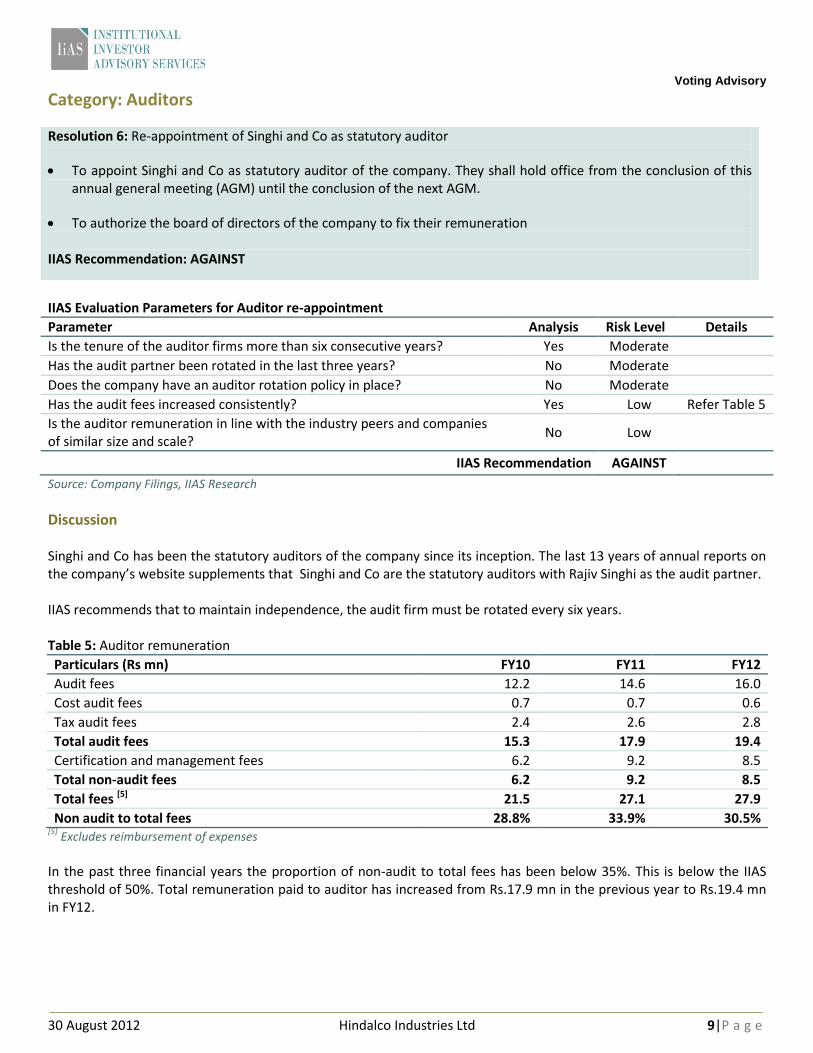

Category: Auditors

IIAS Evaluation Parameters for Auditor re-appointment

Parameter Analysis Risk Level Details

Is the tenure of the auditor firms more than six consecutive years? Yes Moderate

Has the audit partner been rotated in the last three years? No Moderate

Does the company have an auditor rotation policy in place? No Moderate

Has the audit fees increased consistently? Yes Low Refer Table 5

Is the auditor remuneration in line with the industry peers and companies of similar size and scale?

No Low

IIAS Recommendation AGAINST Source: Company Filings, IIAS Research

Discussion Singhi and Co has been the statutory auditors of the company since its inception. The last 13 years of annual reports on the company’s website supplements that Singhi and Co are the statutory auditors with Rajiv Singhi as the audit partner. IIAS recommends that to maintain independence, the audit firm must be rotated every six years. Table 5: Auditor remuneration

Particulars (Rs mn) FY10 FY11 FY12

Audit fees 12.2 14.6 16.0

Cost audit fees 0.7 0.7 0.6

Tax audit fees 2.4 2.6 2.8

Total audit fees 15.3 17.9 19.4

Certification and management fees 6.2 9.2 8.5

Total non-audit fees 6.2 9.2 8.5

Total fees [5] 21.5 27.1 27.9

Non audit to total fees 28.8% 33.9% 30.5% [5]

Excludes reimbursement of expenses

In the past three financial years the proportion of non-audit to total fees has been below 35%. This is below the IIAS threshold of 50%. Total remuneration paid to auditor has increased from Rs.17.9 mn in the previous year to Rs.19.4 mn in FY12.

Resolution 6: Re-appointment of Singhi and Co as statutory auditor

To appoint Singhi and Co as statutory auditor of the company. They shall hold office from the conclusion of this annual general meeting (AGM) until the conclusion of the next AGM.

To authorize the board of directors of the company to fix their remuneration IIAS Recommendation: AGAINST

Voting Advisory

30 August 2012 Hindalco Industries Ltd 10|P a g e

Box 6: Guidelines on auditor appointment

According to MCA, in order to maintain independence of auditors, an audit partner should be rotated every three years and an audit firm should be rotated every five years. A cooling period of three years should elapse before a partner can resume an audit assignment for the company. This period should be five years for the firm. According to IIAS policy, to maintain the independence of auditors – tenure of audit partner should not exceed three years and audit firm should be rotated every six years. According to clause 139 of the new Companies Bill 2011, an auditor will be permitted to hold office for a five year term and can then be reappointed for another five year term. After two consecutive five-year terms, there needs to be a cooling-off period of five years before subsequent reappointments. When the new Companies Bill is passed into law, audit firms would be allowed to hold office for ten consecutive years. Investors should note that IIAS is currently re-evaluating its criteria for auditor tenure and this may change in line with the new

Companies bill.

Considering the tenure of the statutory auditors, we believe that the auditors may not be able to provide an independent judgment on the accounts of the company. We recommend voting AGAINST the resolution.

Category: To create charge/mortgage on assets

Discussion In the annual general meeting held in September 2011, the shareholders of Hindalco gave enabling powers to board of directors to borrow upto Rs.200 bn with an objective to fund its brownfield expansions and greenfield projects. The increase in borrowing limit was over and above the paid up share capital and free reserves of the company. As per section 293 of the Companies Act, shareholders’ approval is essential if the borrowings of the company (apart from temporary loans obtained from the company’s bankers in ordinary course of time) exceeds the aggregate of paid up equity share capital and free reserves.

In the ensuing AGM, the company proposes to create charge and or mortgage its immovable and fixed assets. As at 31 March 2012, Hindalco had outstanding borrowings amounting to Rs.145.7 bn and a debt to EBIDTA ratio of 3.9. Table 6: Debt Ratios and cash flow performance of Hindalco (Standalone)

Particulars FY10 FY11 FY12

Total Debt/ EBITDA 2.0 2.6 3.9

Total Debt/ Equity 0.2 0.3 0.5

Interest Coverage 9.1 20.3 15.3

Net Cash Flow from operations (Rs. bn) 17.2 22.5 21.2

Total Debt (Rs. bn ) 63.6 90.4 145.7

Secured Debt 51.5 51.7 112.8

Fixed assets 114.1 135.9 233.8

Secured loan as % of total debt 81.1% 57.2% 77.4%

Secured Loans as % of fixed assets [6]

45.2% 38.0% 48.2% [6]

Fixed assets includes tangible assets (net block) and capital work in progress

Resolution 8: To secure the borrowings by creating charge/mortgage on assets of the company IIAS Recommendation: FOR

Voting Advisory

30 August 2012 Hindalco Industries Ltd 11|P a g e

Source: Company, IIAS Research

As at 31 March 2012, 77.4% of Hindalco’s debt is secured by providing mortgage or charge on its fixed assets. Even if the company were to borrow upto the maximum approved limit (i.e. Rs.200 bn), the fixed assets of the company can absorb the charge. As at 31 March 2012, secured loans are only 48.2% of the fixed assets. Secured debt typically has easier repayment terms, less restrictive covenants and marginally lower interest rates. We recommend voting FOR the resolution.

Voting Advisory

30 August 2012 Hindalco Industries Ltd 12|P a g e

Disclaimer

This document has been prepared by Institutional Investor Advisory Services India Limited (IIAS). IIAS is a full service Institutional Shareholder Advisory Service Company. The information contained herein is from publicly available data or other sources believed to be reliable, but we do not represent that it is accurate or complete and it should not be relied on as such. IIAS shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. This document is provided for assistance only and is not intended to be and must not alone be taken as the basis for any Voting or investment decision. The user assumes the entire risk of any use made of this information. Each recipient of this document should make such investigation as it deems necessary to arrive at an independent evaluation of the individual resolutions which may affect their investment in the securities of companies referred to in this document (including the merits and risks involved). The discussions or views expressed may not be suitable for all investors. This information is strictly confidential and is being furnished to you solely for your information. This information should not be reproduced or redistributed or passed on directly or indirectly in any form to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject IIAS to any registration or licensing requirements within such jurisdiction. The distribution of this document in certain jurisdictions may be restricted by law, and persons in whose possession this document comes, should inform themselves about and observe, any such restrictions. The information given in this document is as of the date of this report and there can be no assurance that future results or events will be consistent with this information. This information is subject to change without any prior notice. IIAS reserves the right to make modifications and alterations to this statement as may be required from time to time. However, IIAS is under no obligation to update or keep the information current. Nevertheless, IIAS is committed to providing independent and transparent recommendation to its client and would be happy to provide any information in response to specific client queries. Neither IIAS nor any of its affiliates, group companies, directors, employees, agents or representatives shall be liable for any damages whether direct, indirect, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. . The disclosures of interest statements incorporated in this document are provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report. The information provided in these reports remains, unless otherwise stated, the copyright of IIAS. All layout, design, original artwork, concepts and other Intellectual Properties, remains the property and copyright of IIAS and may not be used in any form or for any purpose whatsoever by any party without the express written permission of the copyright holders.