1 Wages Owed to Deceased Employees Kristine K. Willson, CPP Kristine K. Willson, CPP – [email protected]Agenda Coordinating efforts with other departments Issuing the payments State laws and resources Best practices Resources

Coordinating efforts with other departments Issuing the payments State laws and resources Best practices Resources

2

Coordinating Efforts with Other Departments Who needs to be involved?

Accounts Payable Benefits Human Resources Legal Payroll Stock/Equity

Checklist

Develop a checklist of each department’s responsibilities

HR Make note of relatives working at company Notify department where employee worked Identify contact to determine family needs Send flowers/memorial contribution Coordinate communications regarding funeral arrangements Request onsite EAP support if appropriate Send customized condolence letter to family, include life insurance claim forms, COBRA

forms, contact name and phone number Recover company assets: cell phone, laptop, etc.

Benefits

Validate beneficiary forms for accuracy upon receipt Send annual reminders to employees to update beneficiary forms Research benefits options for the employee’s dependents Obtain certified copy of death certificate – may take several weeks Was employee on disability? Notify insurance company. Was death work-related? Notify workers’ compensation insurance company Was employee traveling on business? Is there travel insurance? Notify administrator to transfer 401(k) to beneficiary

Payroll and Accounts Payable

Update payroll/HR system with termination Review residential state law of decedent Determine payments to be made in year of death and year(s) following. Who will issue

payments? Obtain Form W-9. Need to report payments on Form 1099-MISC even if amount is less

than $600.00 Does decedent have uncashed paychecks? Suspend direct deposit Does payroll need to set up unique earnings code? Notify agencies if employee had involuntary deductions

3

Equity Determine stock value at date of death Initiate required distributions Notify broker of date of death How to report income recognized for an NQSO exercise (or vesting/release of restricted

stock/units) that occurs after an employee’s death? o If transaction occurs in same calendar year as employee’s death, report income

recognized on W-2 as: Box 3, SS Wages/tips (up to annual maximum) Box 4, SS tax withheld Box 5 Medicate wages/tips Box 6, Medicare tax withheld

o Also report income on 1099-MISC issued to estate or beneficiary o If transaction occurs after the calendar year of employee’s death:

No W-2 reporting 1099-MISC reporting

Legal

May need to be involved. Ask if unsure Collaboration

Create one letter/packet for family Include details about each benefit Forms to complete/return envelopes Contact information if family has questions Payments yet to be paid and approximate date(s)

All departments have better understanding of others’ role

Issuing the Payments Scenario 1: Employee dies after receiving a paycheck but before cashing it:

Reissue the net pay to the employee’s spouse, personal representative/executor, per state law

Report the wages paid and taxes withheld on the decedent’s Form W-2. No Form 1099-MISC issued

Scenario 2: Wages payable after employee dies, but within the same calendar year:

Both forms W-2 and 1099-MISC will be generated For W-2 purposes, wages and taxes will be reported in boxes 3 – 6.

o Do not report in Box 1; do not withhold federal income tax o State laws typically follow federal law for SIT & SUI, but research

FUTA taxable On Form 1099-MISC report gross payment in box 3. In name and TIN of

beneficiary/executor. Refer to Form W-9.

4

5

Scenario 3: Wages payable after employee dies, but after the calendar year of death:

No Form W-2. No reporting in payroll records. On Form 1099-MISC report gross payment in box 3. In name and TIN of

beneficiary/executor. Refer to Form W-9.

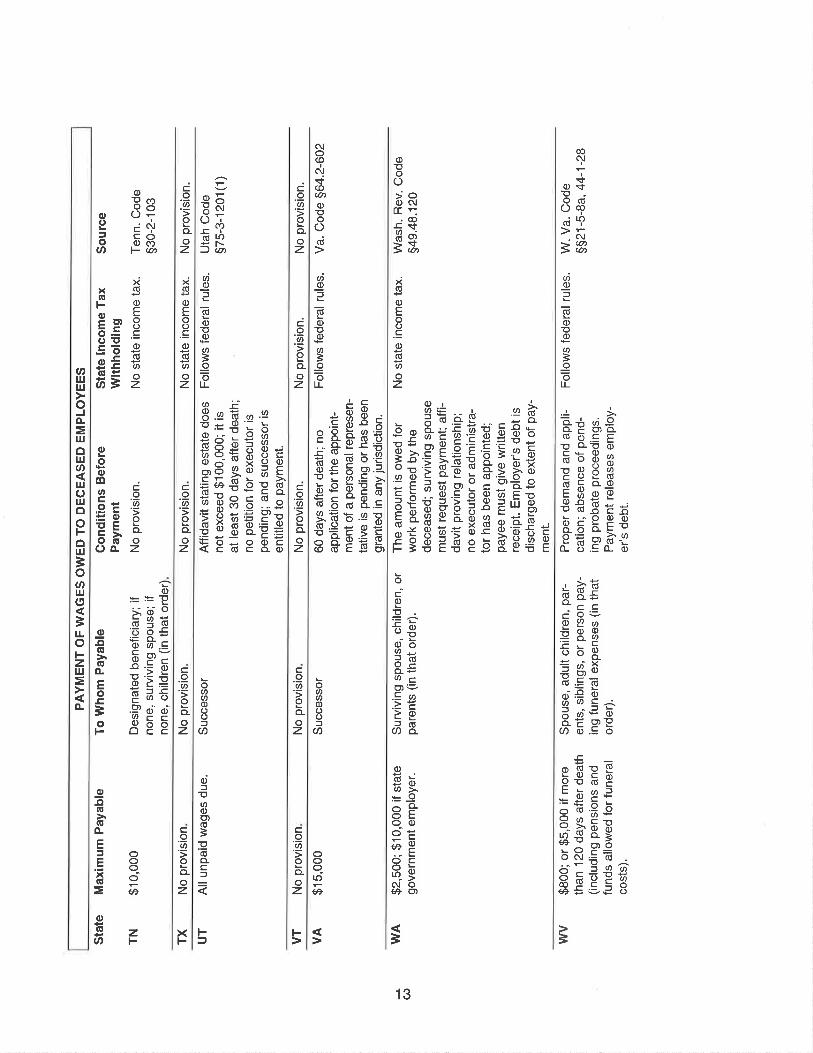

State Laws Follow state law where employee resided State laws dictate:

The maximum amount payable To whom payable Any special conditions before payment can be made If state income taxable

6

Best Practices Ensure beneficiary forms are accurate and attempt to keep current Coordinate communication to family through one channel Review federal and state rules before issuing payments Stop direct deposit Obtain written acknowledgement payments were received Each situation is unique but be reasonably consistent in responses and support

Resources

www.irs.gov o Instructions for Forms W-2 and W-3 under ‘Special Reporting Situations’ o Instructions for Form 1099-MISC

APA’s The Payroll Source® APA’s Guide to State Payroll Laws Your payroll service provider Payroll library subscriptions (such as Bloomberg BNA, Thomson Reuters, Wolters Kluwer,

etc.) State laws, state government websites Corporate attorney

7

Sample letter to send with payment Date RE: Wage and vacation payment for John Dear Mrs. Smith, Enclosed is a check for $6,659.86 which represents the following:

Wages earned for period February 1 ‐ 5, 2016: 1,442.31

20 days unused vacation: 5,769.23

Gross pay 7,211.54

Less taxes: social security (447.12)

Medicare (104.57)

Net payment: 6,659.86

We will mail the following 2016 tax forms to you on or before January 31, 2017: 1) Form W‐2 in John’s name for all taxable wages paid during 2016. 2) Form 1099‐MISC will be issued in your name for the above payment. Box 3 will list the gross

amount of $7,211.54. Please keep us informed if your address should change. If you have any questions, feel free to contact me. Kind regards, Name Title Address Phone number Email address

![IN THE EMPLOYMENT RELATIONS AUTHORITY AUCKLAND I TE … · 2020-06-11 · Arrears of wages [15] The second to ninth applicants claim they are owed arrears of wages for overtime, payment](https://static.documents.pub/doc/80x56/5f2ddf04737f7663497ed389/in-the-employment-relations-authority-auckland-i-te-2020-06-11-arrears-of-wages.jpg)