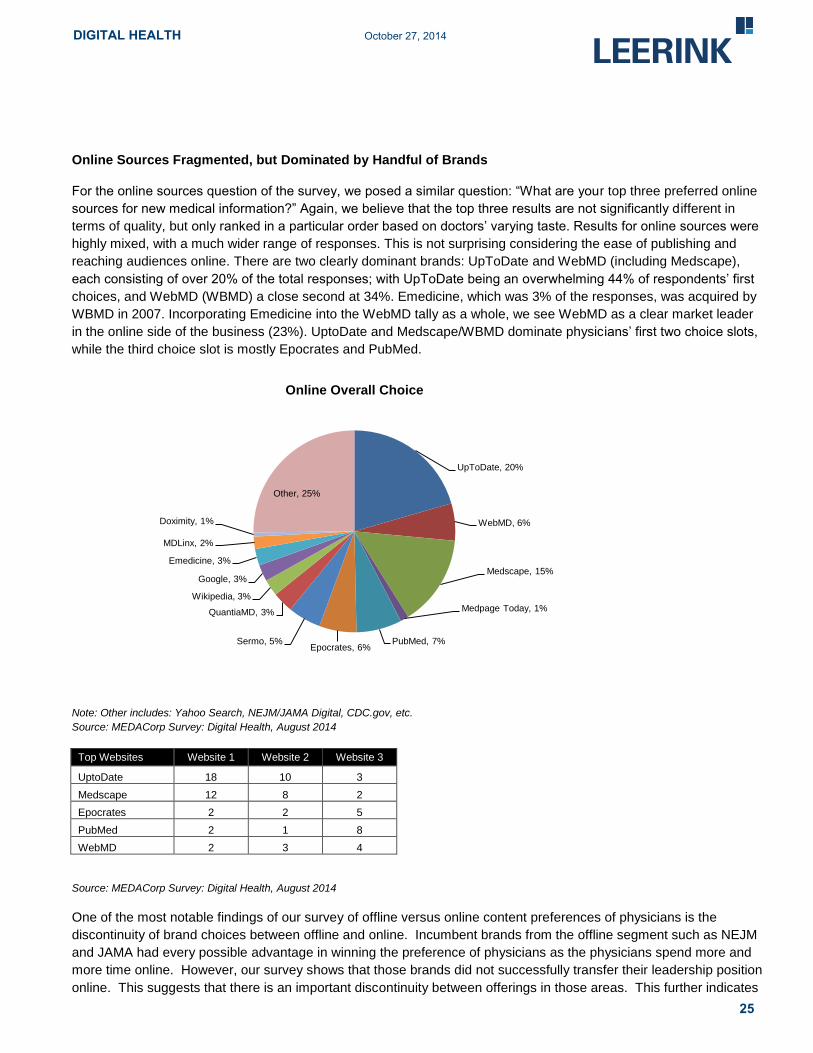

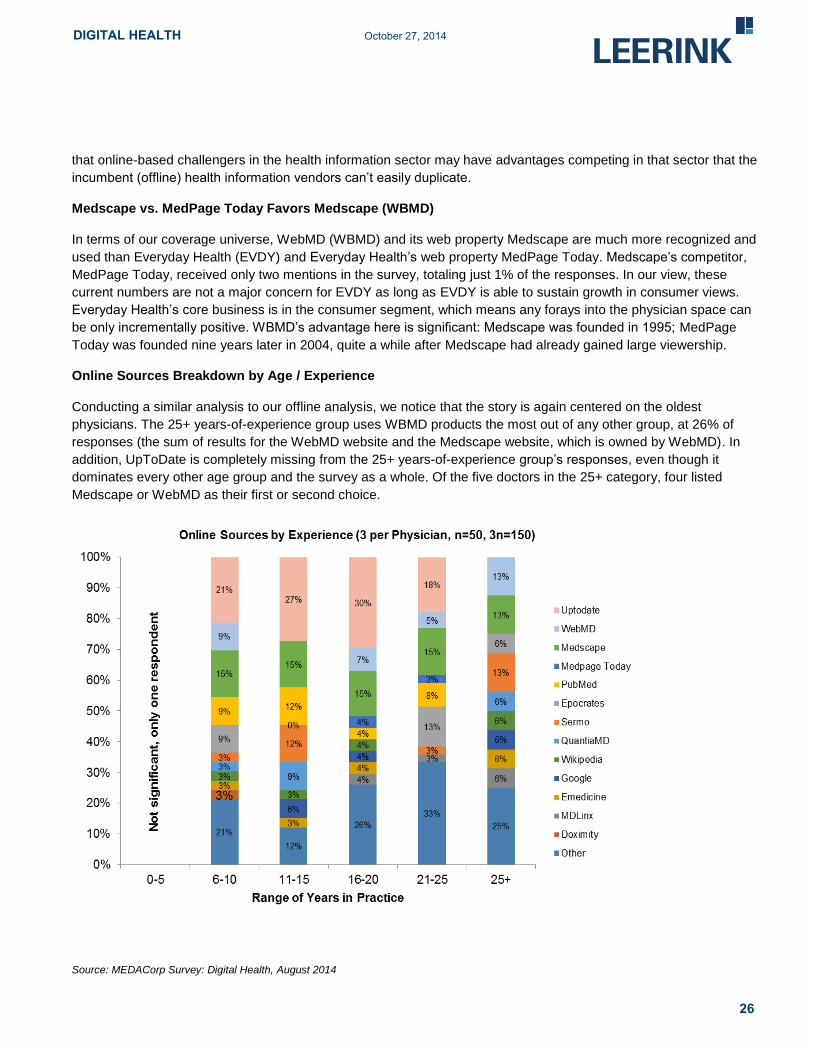

October 27, 2014 Reason for report: PROPRIETARY INSIGHTS Steven Wardell (617) 918-4097 [email protected]DIGITAL HEALTH Future of Digital Health • Bottom Line: We are initiating coverage of the Digital Health sector. The same digital revolution that re-ordered the media sector has now arrived at the healthcare sector, creating winners and losers. We believe healthcare is entering the same digital productivity curve as the technology sector. We have identified 6 important Digital Health investment themes and the many social, industry, policy, and technological drivers behind them. We initiate coverage of CSLT, EVDY, IMPR, WAGE, and WBMD at Outperform, with a Market Perform rating on VEEV. Investment in the Digital Health sector has grown meaningfully over the past two years. But at the same time, while the S&P 500 Healthcare Index returned about 23% over the last 12 months and the NASDAQ Biotechnology Index returned over 36%, the Leerink Digital Health EW39 Index has returned only about 1%. Channel checks within our MEDACorp network point to increased physician adoption of digital content, while cost-shifting from employers to employees increases consumer demand for online media and Consumer Directed Benefits management. • Healthcare is undergoing a digital transformation, and we highlight six key themes powering investment opportunities in the emerging Digital Health Sector: Consumer Empowerment, Automation, Connected Health, Population Health, Big Data, and Healthcare IT. We define Digital Health as the convergence of the healthcare system with digital technology. We see a vast opportunity for Digital Health in the near term, as consumers take charge of their healthcare, technological shocks present opportunities for IT improvement, healthcare reform (the ACA) challenges the status quo, aging Baby Boomers and the hyper-connected Millennials demand increased involvement in their own care, and rising healthcare costs shift to consumers. We have already seen growing interest in the sector, with private and public investments totaling $2.3b in 1H14, up from $2b in 2013 and $1.4b in 2012, and 7 IPOs this year. However, the Leerink Digital Health EW39 Index of 39 public pure-play Digital Health stocks had a return of only 1% over the past 12 months, while the S&P 500 Healthcare returned ~23% and the NASDAQ Biotech index returned over 36% – suggesting to us there is room for valuation upside in the Digital Health sector, with compelling societal, technological, sector, and policy drivers fueling this growth. • Now is different: the post-2010 healthcare industry is poised for adoption of new technologies to enhance productivity, control spending, and improve outcomes. Despite technological improvements propelling US business productivity and collaboration through enhanced IT systems in the late 20th and early 21st centuries, healthcare lagged well behind. The Affordable Care Act of 2010 opened up the healthcare system to adoption of technological improvements due to a convergence of factors - namely, an estimated ~10m newly insured individuals entering the system in 2014, and a shift from volume- to value-based payment, placing importance on outcomes and cost management. On the manufacturing side, increasingly stringent FDA regulation and legislation S&P 500 Health Care Index: 775.27 Companies Highlighted: CSLT, EVDY, IMPR, VEEV, WAGE, WBMD Please refer to Pages 102 - 104 for Analyst Certification and important disclosures. Price charts and disclosures specific to covered companies and statements of valuation and risk are available at https://leerink2.bluematrix.com/bluematrix/Disclosure2 or by contacting Leerink Partners Editorial Department, One Federal Street, 37th Floor, Boston, MA 02110.

• Bottom Line: We are initiating coverage of the Digital Health sector. Thesame digital revolution that re-ordered the media sector has now arrived atthe healthcare sector, creating winners and losers. We believe healthcareis entering the same digital productivity curve as the technology sector.We have identified 6 important Digital Health investment themes andthe many social, industry, policy, and technological drivers behind them.We initiate coverage of CSLT, EVDY, IMPR, WAGE, and WBMD atOutperform, with a Market Perform rating on VEEV. Investment in theDigital Health sector has grown meaningfully over the past two years. Butat the same time, while the S&P 500 Healthcare Index returned about23% over the last 12 months and the NASDAQ Biotechnology Indexreturned over 36%, the Leerink Digital Health EW39 Index has returnedonly about 1%. Channel checks within our MEDACorp network point toincreased physician adoption of digital content, while cost-shifting fromemployers to employees increases consumer demand for online mediaand Consumer Directed Benefits management.

• Healthcare is undergoing a digital transformation, and we highlightsix key themes powering investment opportunities in the emergingDigital Health Sector: Consumer Empowerment, Automation,Connected Health, Population Health, Big Data, and Healthcare IT.We define Digital Health as the convergence of the healthcare system withdigital technology. We see a vast opportunity for Digital Health in the nearterm, as consumers take charge of their healthcare, technological shockspresent opportunities for IT improvement, healthcare reform (the ACA)challenges the status quo, aging Baby Boomers and the hyper-connectedMillennials demand increased involvement in their own care, and risinghealthcare costs shift to consumers. We have already seen growinginterest in the sector, with private and public investments totaling $2.3bin 1H14, up from $2b in 2013 and $1.4b in 2012, and 7 IPOs this year.However, the Leerink Digital Health EW39 Index of 39 public pure-playDigital Health stocks had a return of only 1% over the past 12 months,while the S&P 500 Healthcare returned ~23% and the NASDAQ Biotechindex returned over 36% – suggesting to us there is room for valuationupside in the Digital Health sector, with compelling societal, technological,sector, and policy drivers fueling this growth.

• Now is different: the post-2010 healthcare industry is poised foradoption of new technologies to enhance productivity, controlspending, and improve outcomes. Despite technological improvementspropelling US business productivity and collaboration through enhancedIT systems in the late 20th and early 21st centuries, healthcare laggedwell behind. The Affordable Care Act of 2010 opened up the healthcaresystem to adoption of technological improvements due to a convergenceof factors - namely, an estimated ~10m newly insured individualsentering the system in 2014, and a shift from volume- to value-basedpayment, placing importance on outcomes and cost management. On themanufacturing side, increasingly stringent FDA regulation and legislation

Please refer to Pages 102 - 104 for Analyst Certification and important disclosures. Price charts and disclosures specific tocovered companies and statements of valuation and risk are available athttps://leerink2.bluematrix.com/bluematrix/Disclosure2 or by contacting Leerink Partners Editorial Department, OneFederal Street, 37th Floor, Boston, MA 02110.

requiring tracking of physician compensation is creating a need for datamanagement and process automation in the pharmaceutical industry.

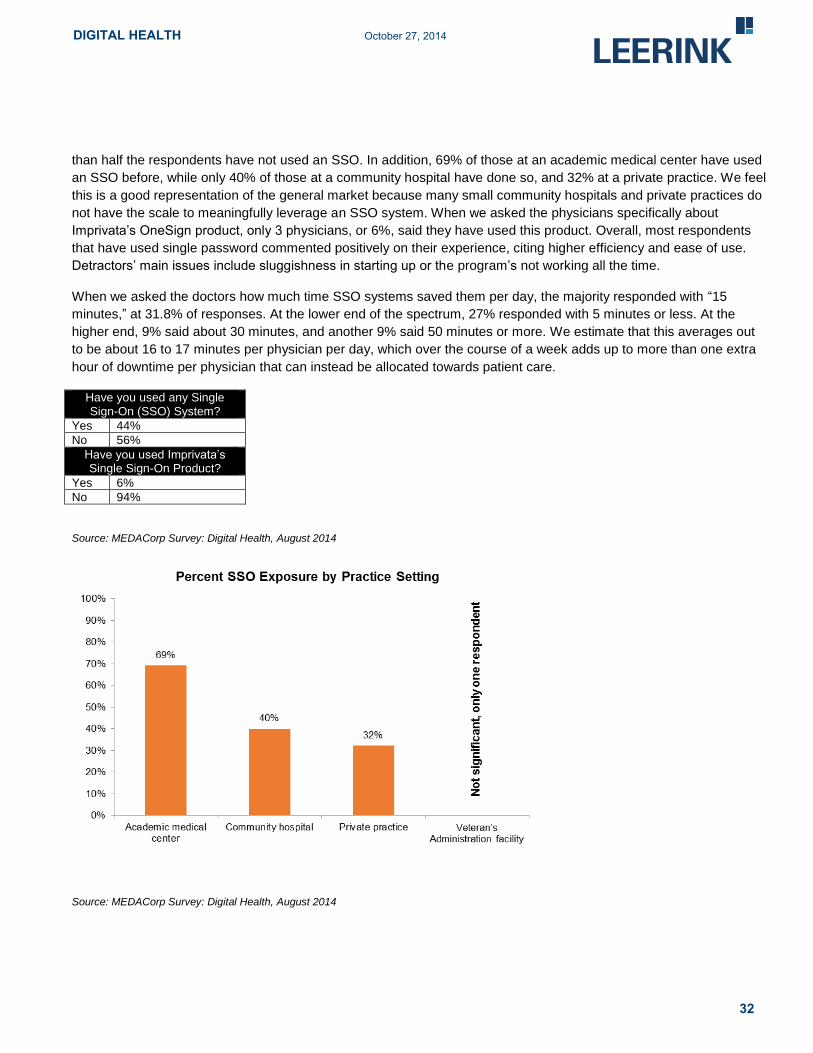

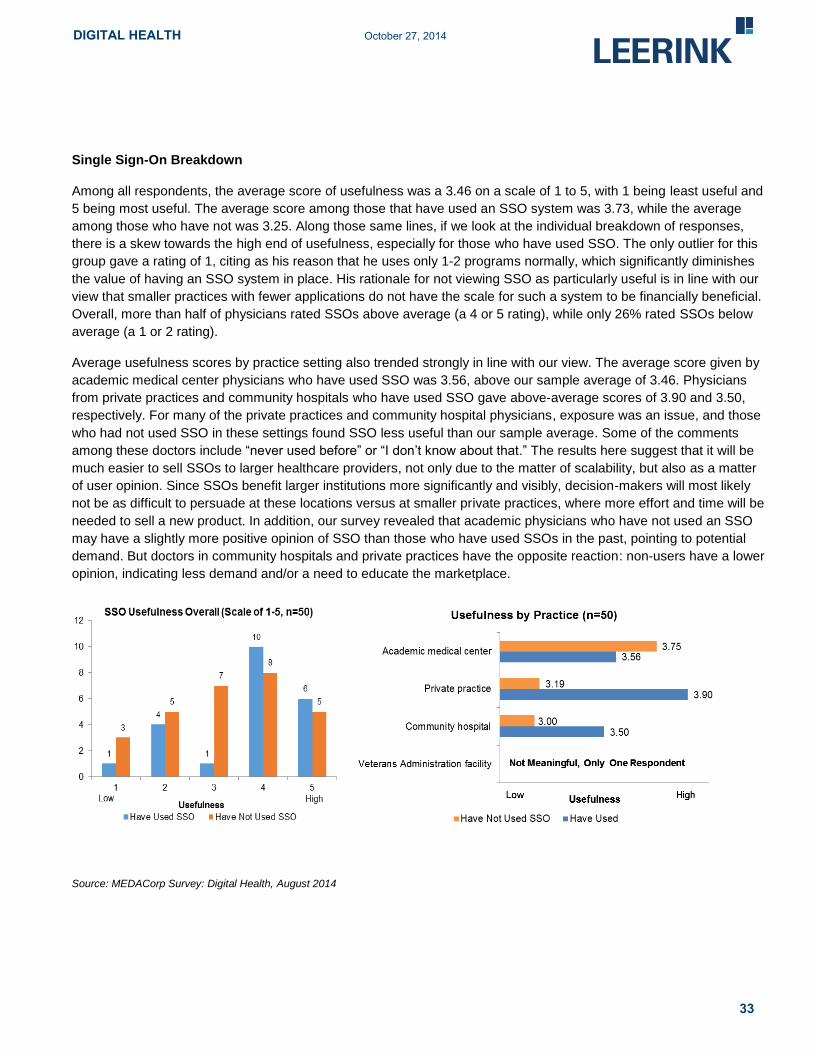

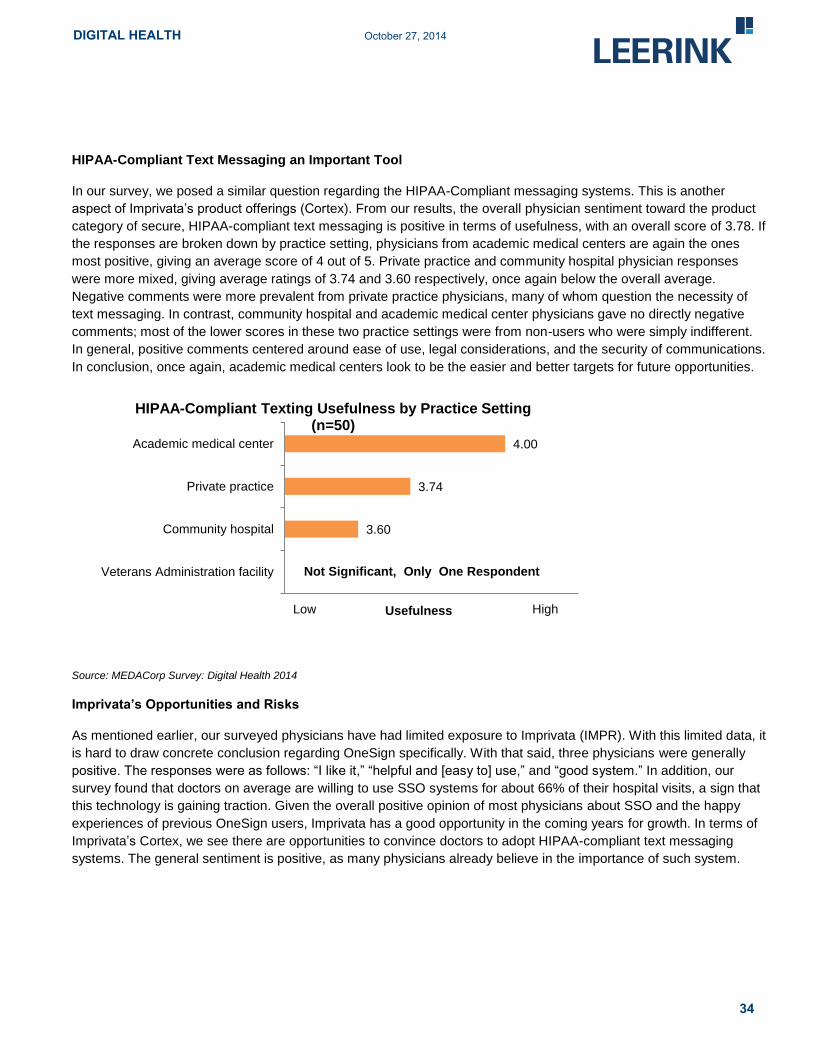

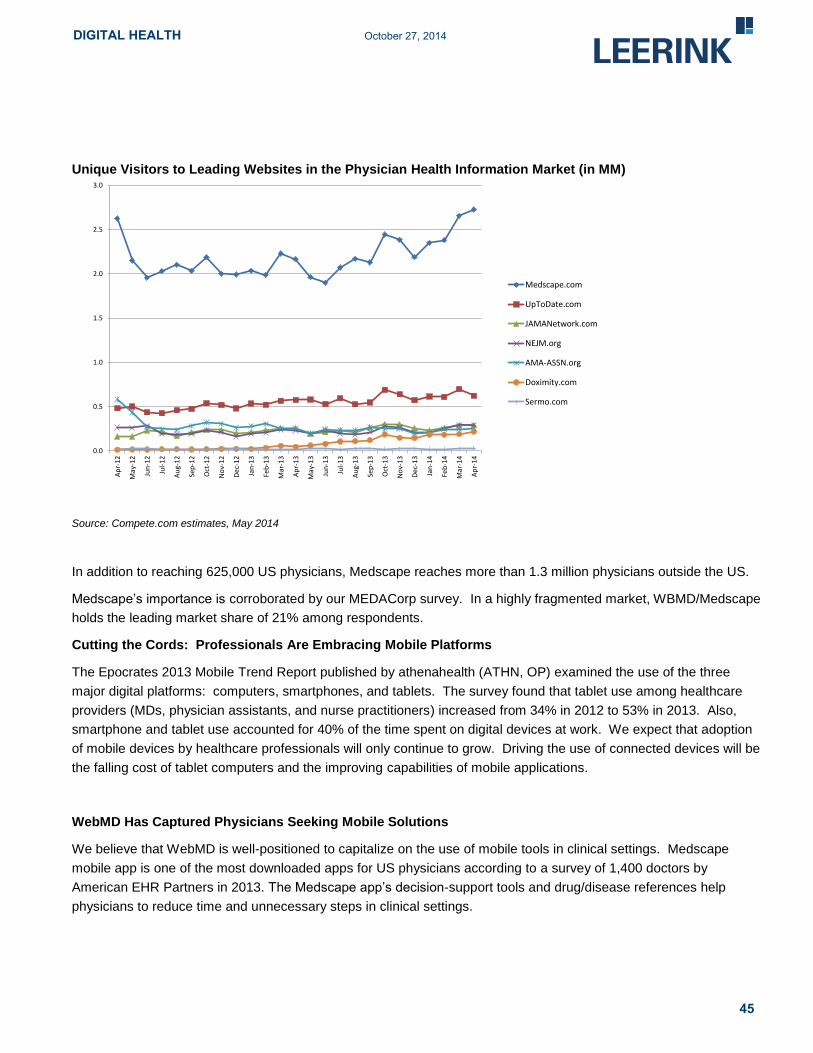

• Our MEDACorp survey of 50 physicians across the U.S. pointsto growing demand for digital content, which in turn presentsan opportunity for content providers to profit from increasedpharmaceutical advertising. While older generations of physiciansmay prove “sticky” to old habits, we found that, overall, physicians areincreasing their use of web and mobile (online) sources, single sign-onsystems (SSOs), and HIPAA-compliant texting in their daily practice. Thisincreasing interest in online sources presents the biggest opportunityfor WBMD and EVDY, which stand to benefit from increased advertisingspend as physician demand increases and pharma ad spend continues togrow.

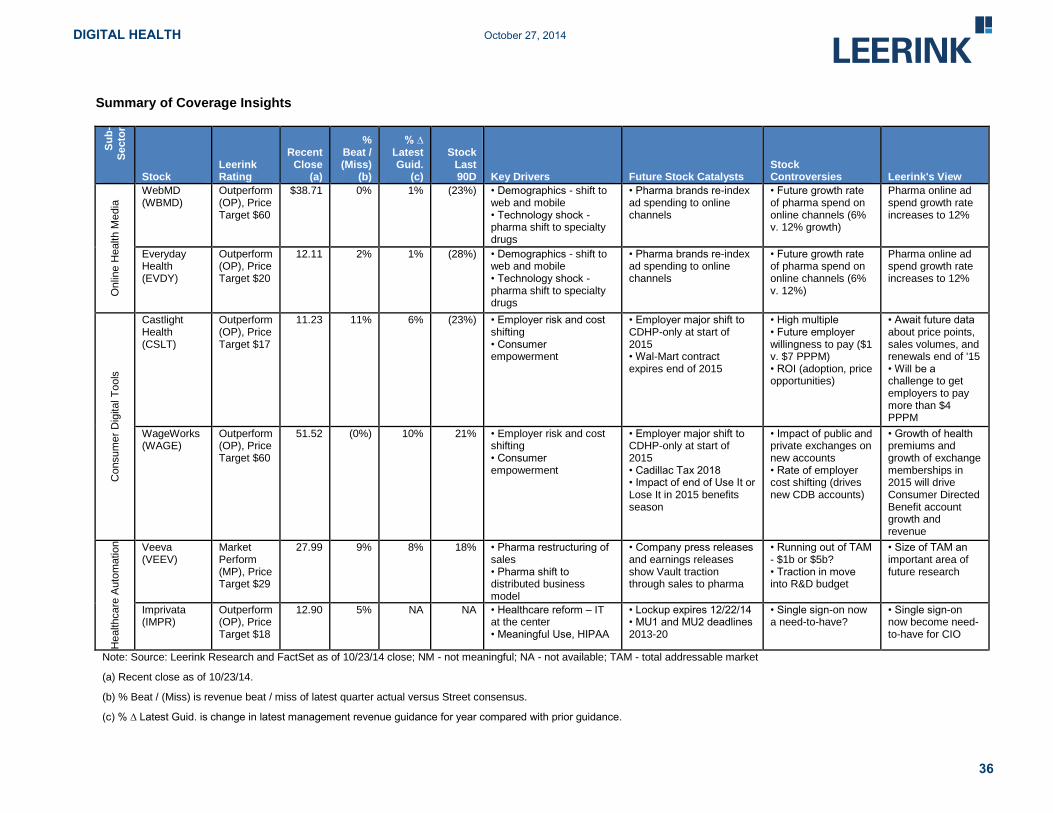

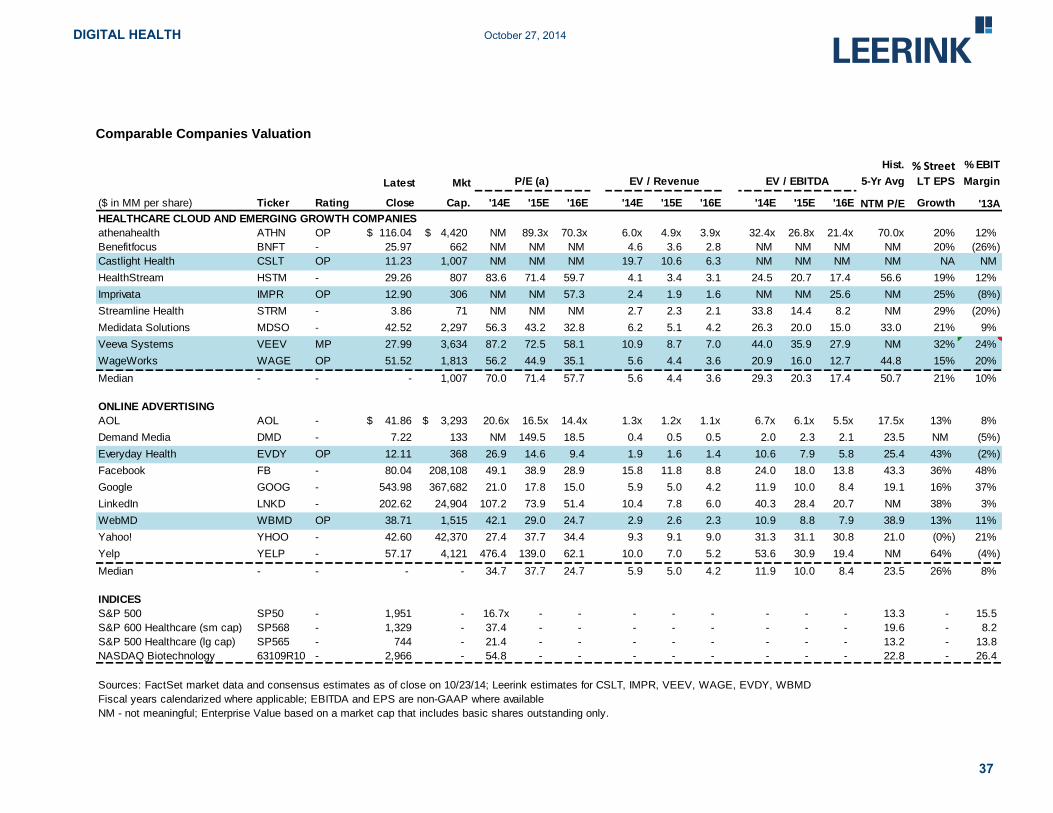

• We initiate coverage of 6 companies, with Outperform ratings onCSLT, EVDY, IMPR, WAGE, and WBMD and a Market Perform ratingon VEEV. Our coverage companies range in primary function from OnlineHealth Media (WBMD, EVDY) to Consumer Digital Tools (CSLT, WAGE)and Healthcare Automation (VEEV, IMPR).

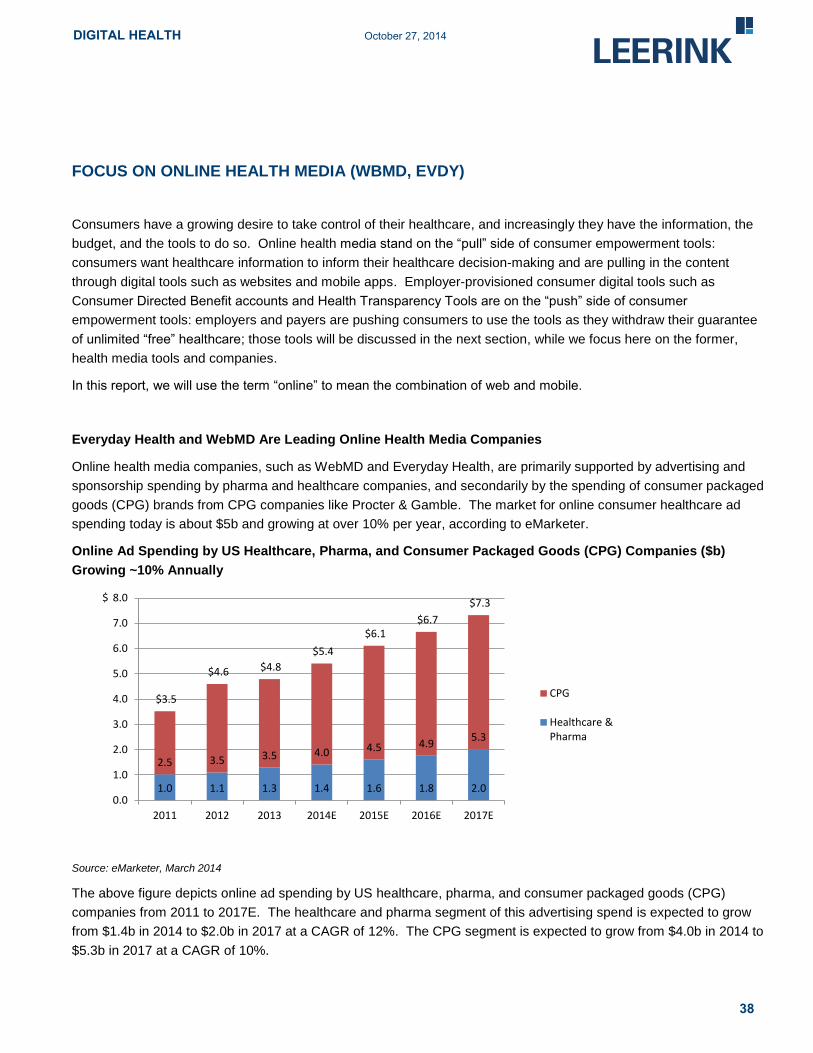

• In online media, we see a $5b market growing at 10% per year,with physicians increasingly transitioning to digital platforms aswell. Pharmaceutical advertising spend increased 17% in 2013, and weforecast this trend continuing with spend growing at 12% over the nextfew years. We see WBMD as best positioned to take advantage of trendsshifting consumption by both patients and physicians to online, followed byEVDY, an up-and-comer in mobile.

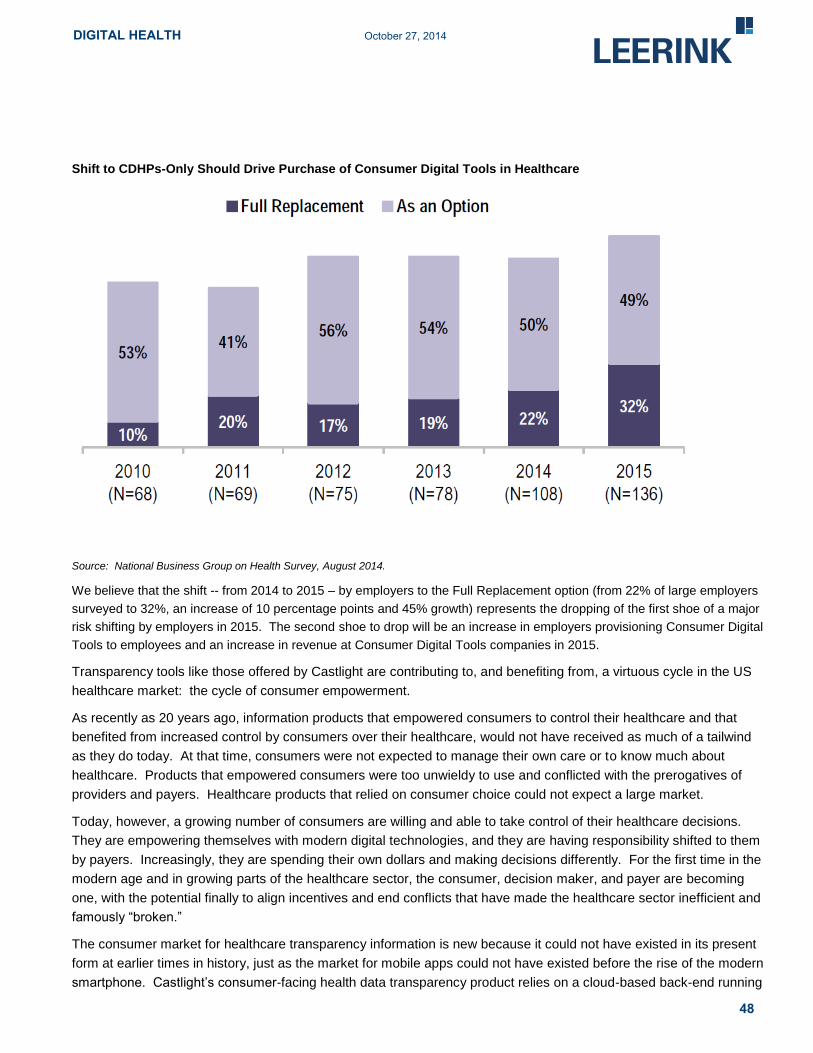

• As benefit costs are shifted from employers to employees,consumers are empowered to take control of their healthcare tominimize spend while maximizing quality of care. We see 2015 asa big year for employer risk shifting, with WAGE and CSLT poised tocapitalize on increased demand for transparency and management ofHigh Deductible Health Plans and Consumer Directed Benefit accounts.

• Healthcare has lagged in purchasing and adopting automationtechnologies, but we see opportunity for providers andmanufacturers to invest in IT. In automation, VEEV and IMPR standto benefit from trends toward IT upgrades that take advantage of cloudsystems and mobile technology.

2

TABLE OF CONTENTS

CHAPTER 1: OVERVIEW OF THE DIGITAL HEALTH SECTOR, ITS DRIVERS, AND COMPANIES ........................................... 4

DIGITAL HEALTH INVESTMENT THEMES ....................................................................................................................... 4

PERFORMANCE OF PUBLIC PURE-PLAYS IN DIGITAL HEALTH ...................................................................................... 5

APPENDIX A: DIGITAL HEALTH DEFINITIONS ................................................................................................................. 57

APPENDIX B: THE LEERINK DIGITAL HEALTH EW39 INDEX AND LEERINK RATINGS ...................................................... 59

APPENDIX C: THE LEERINK DIGITAL HEALTH LANDSCAPE (TABULAR FORMAT) …………………………………………………………61

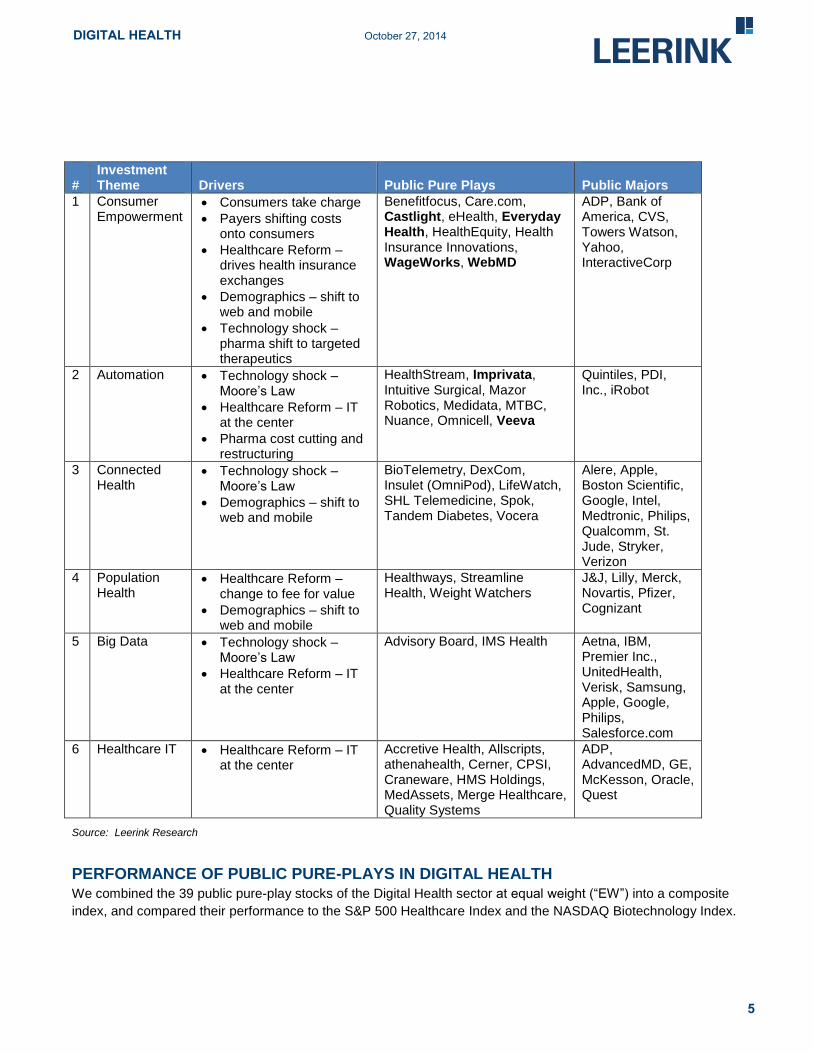

Alere, Apple, Boston Scientific, Google, Intel, Medtronic, Philips, Qualcomm, St. Jude, Stryker, Verizon

4 Population Health

Healthcare Reform – change to fee for value

Demographics – shift to web and mobile

Healthways, Streamline Health, Weight Watchers

J&J, Lilly, Merck, Novartis, Pfizer, Cognizant

5 Big Data Technology shock – Moore’s Law

Healthcare Reform – IT at the center

Advisory Board, IMS Health Aetna, IBM, Premier Inc., UnitedHealth, Verisk, Samsung, Apple, Google, Philips, Salesforce.com

6 Healthcare IT Healthcare Reform – IT at the center

Accretive Health, Allscripts, athenahealth, Cerner, CPSI, Craneware, HMS Holdings, MedAssets, Merge Healthcare, Quality Systems

ADP, AdvancedMD, GE, McKesson, Oracle, Quest

Source: Leerink Research

PERFORMANCE OF PUBLIC PURE-PLAYS IN DIGITAL HEALTH

We combined the 39 public pure-play stocks of the Digital Health sector at equal weight (“EW”) into a composite

index, and compared their performance to the S&P 500 Healthcare Index and the NASDAQ Biotechnology Index.

5

DIGITAL HEALTH October 27, 2014

The resulting chart of the Leerink Digital Health EW39 Index (below) shows that over the last 12 months, while the

S&P 500 Healthcare Index returned about 23% and the NASDAQ Biotechnology Index returned over 36%, the Digital

Health EW39 Index had returns of only about 1%. Digital Health stocks were strongly negatively-affected by the 2014

Spring Growth Stock Correction, as was the NASDAQ Biotechnology Index. In the wake of that correction, Digital

Health stocks have picked back up – however, not as much as the NASDAQ Biotechnology Index. This lag suggests

that, at the present time and with continued lift from societal and technological megatrends, we believe the stocks in

our Digital Health Index have room to rise, and new buyers can buy below historical highs.

Source: Latest twelve month performance per FactSet 10/23/14 close. The Leerink Digital Health EW39 Index is comprised of 39 pure-play Digital

Health stocks with equal weighting. IPOs added during the year are treated in the Digital Health Index through rebalancing (includes Benefitfocus,

Care.com, Castlight, Everyday Health, HealthEquity, Imprivata, IMS Health, MTBC, Tandem Diabetes, and Veeva).

6

DIGITAL HEALTH October 27, 2014

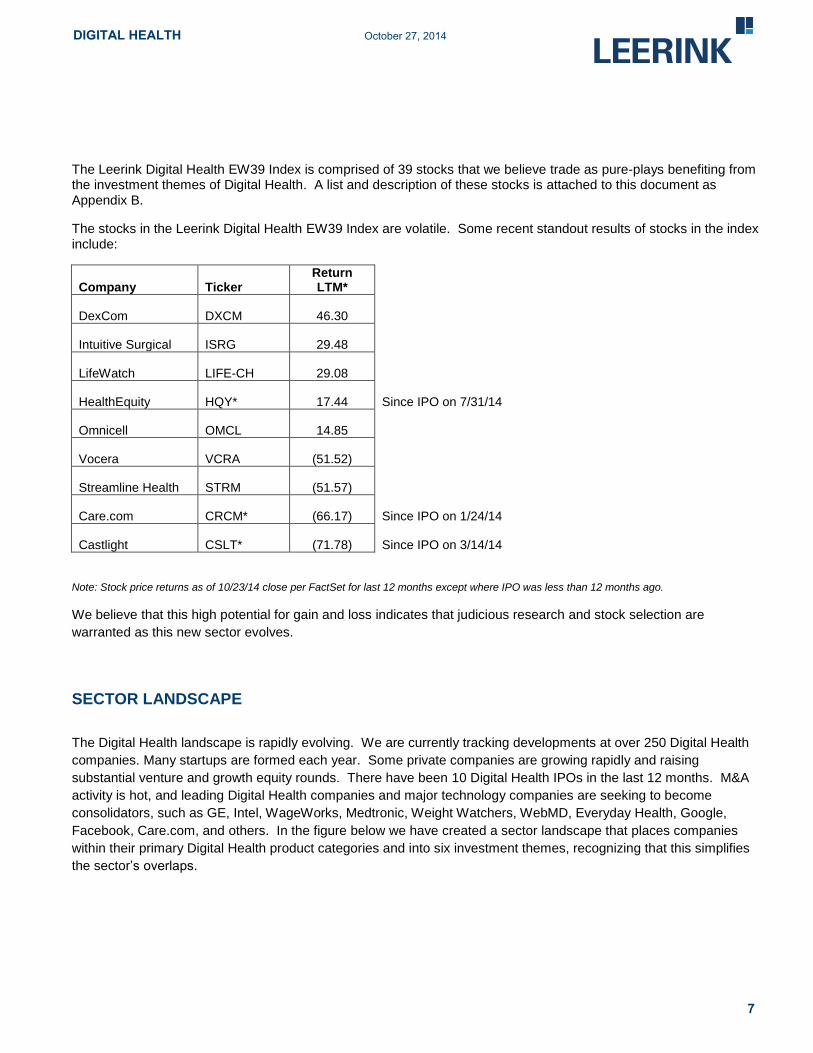

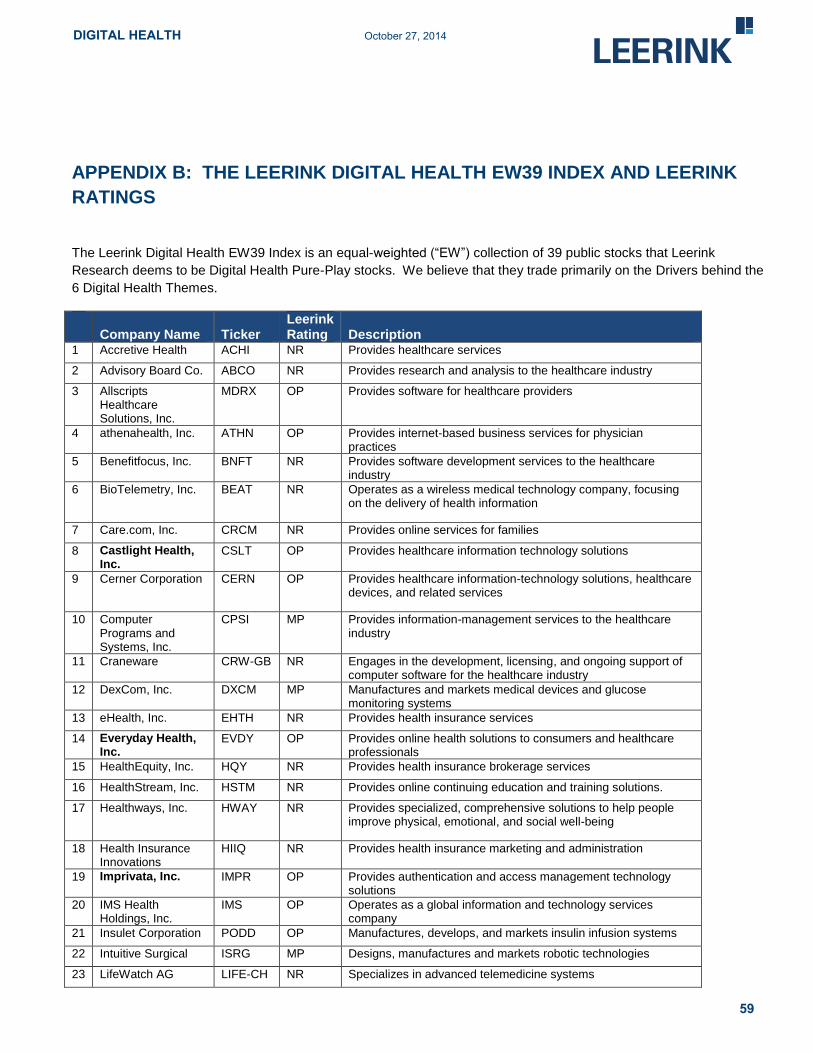

The Leerink Digital Health EW39 Index is comprised of 39 stocks that we believe trade as pure-plays benefiting from the investment themes of Digital Health. A list and description of these stocks is attached to this document as Appendix B.

The stocks in the Leerink Digital Health EW39 Index are volatile. Some recent standout results of stocks in the index include:

Company Ticker Return LTM*

DexCom DXCM 46.30

Intuitive Surgical ISRG 29.48

LifeWatch LIFE-CH 29.08

HealthEquity HQY* 17.44 Since IPO on 7/31/14

Omnicell OMCL 14.85

Vocera VCRA (51.52)

Streamline Health STRM (51.57)

Care.com CRCM* (66.17) Since IPO on 1/24/14

Castlight CSLT* (71.78) Since IPO on 3/14/14

Note: Stock price returns as of 10/23/14 close per FactSet for last 12 months except where IPO was less than 12 months ago.

We believe that this high potential for gain and loss indicates that judicious research and stock selection are

warranted as this new sector evolves.

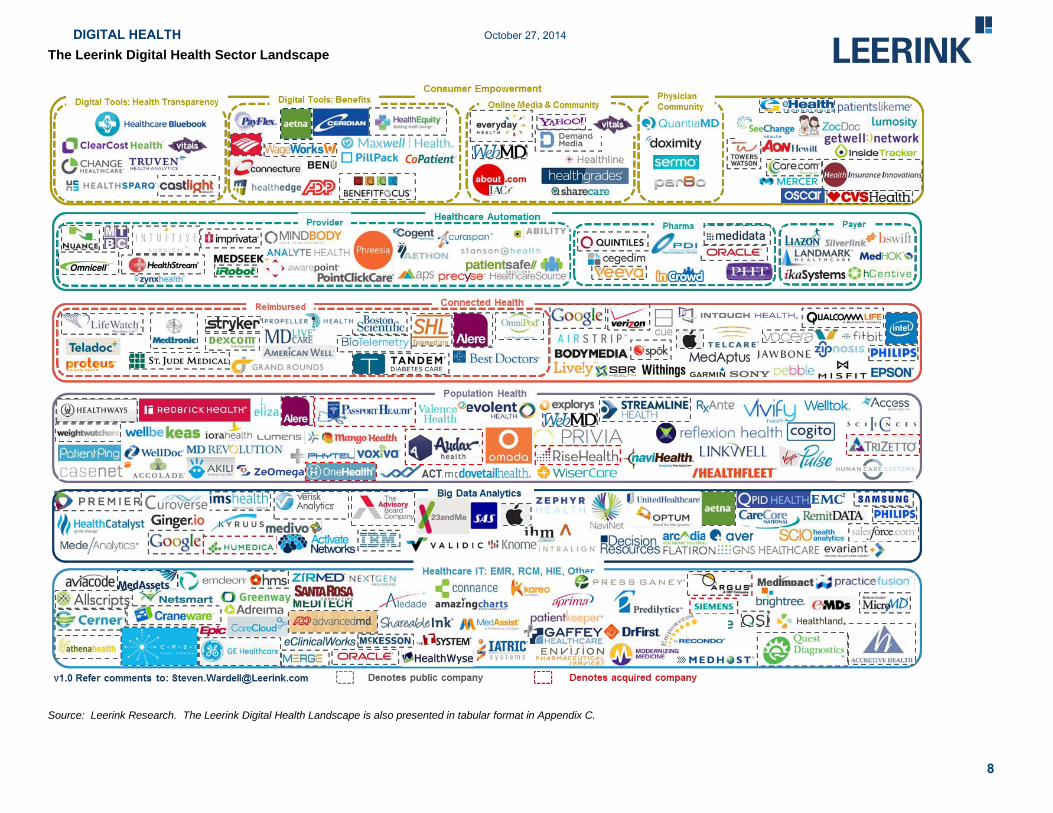

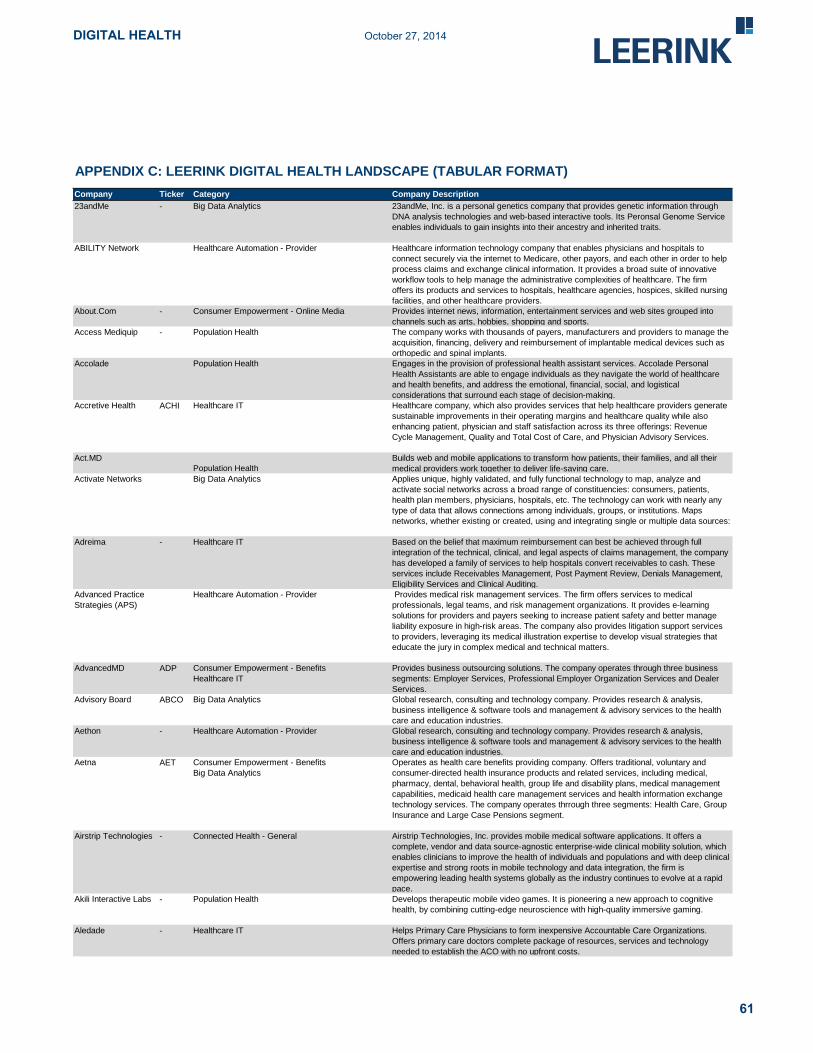

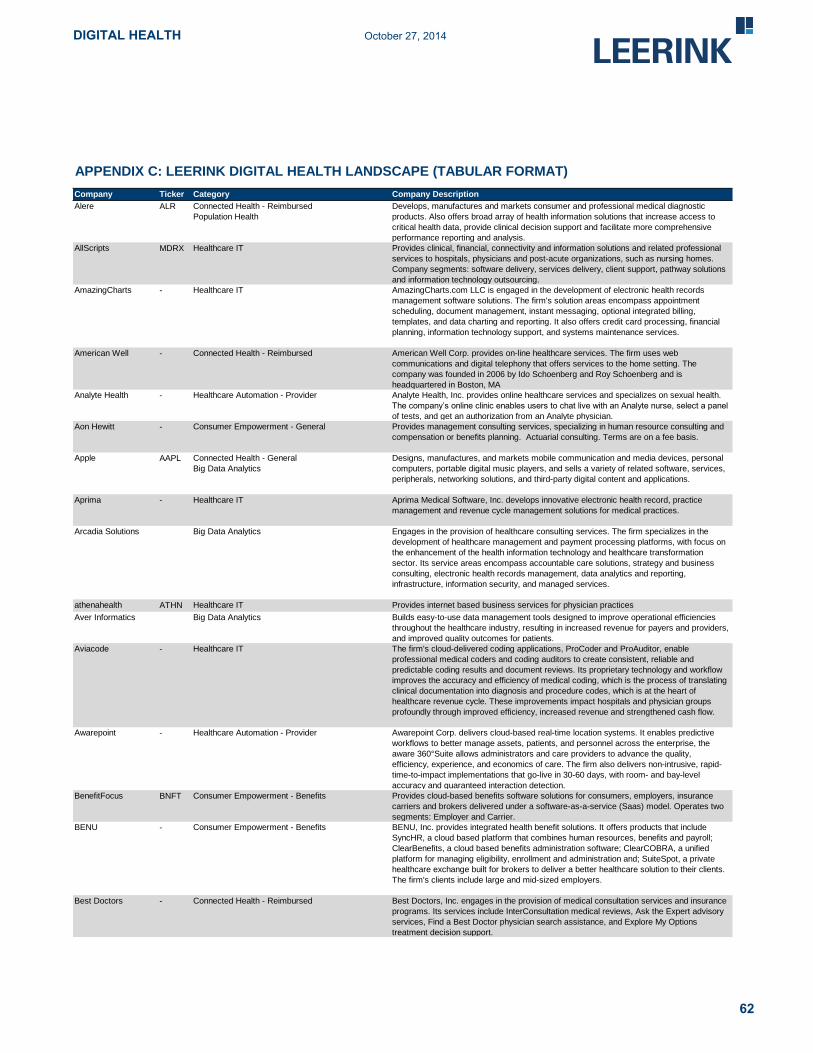

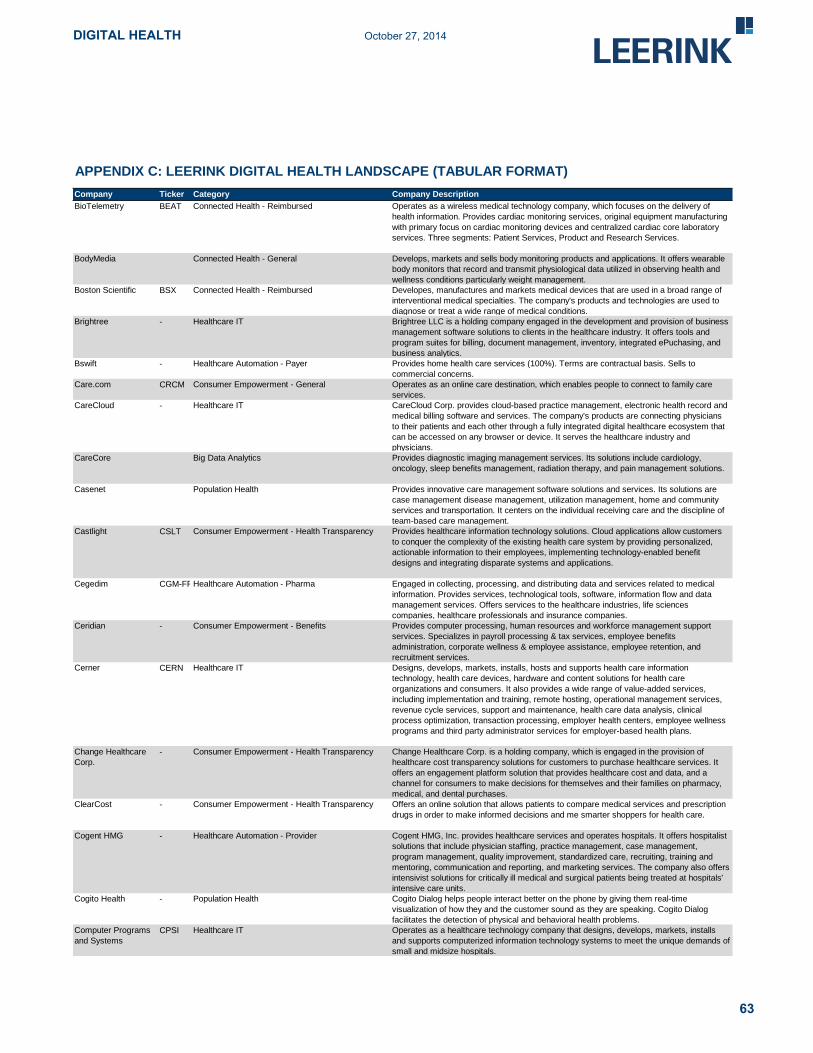

SECTOR LANDSCAPE

The Digital Health landscape is rapidly evolving. We are currently tracking developments at over 250 Digital Health

companies. Many startups are formed each year. Some private companies are growing rapidly and raising

substantial venture and growth equity rounds. There have been 10 Digital Health IPOs in the last 12 months. M&A

activity is hot, and leading Digital Health companies and major technology companies are seeking to become

consolidators, such as GE, Intel, WageWorks, Medtronic, Weight Watchers, WebMD, Everyday Health, Google,

Facebook, Care.com, and others. In the figure below we have created a sector landscape that places companies

within their primary Digital Health product categories and into six investment themes, recognizing that this simplifies

the sector’s overlaps.

7

DIGITAL HEALTH October 27, 2014

The Leerink Digital Health Sector Landscape

Source: Leerink Research. The Leerink Digital Health Landscape is also presented in tabular format in Appendix C.

8

DIGITAL HEALTH October 27, 2014

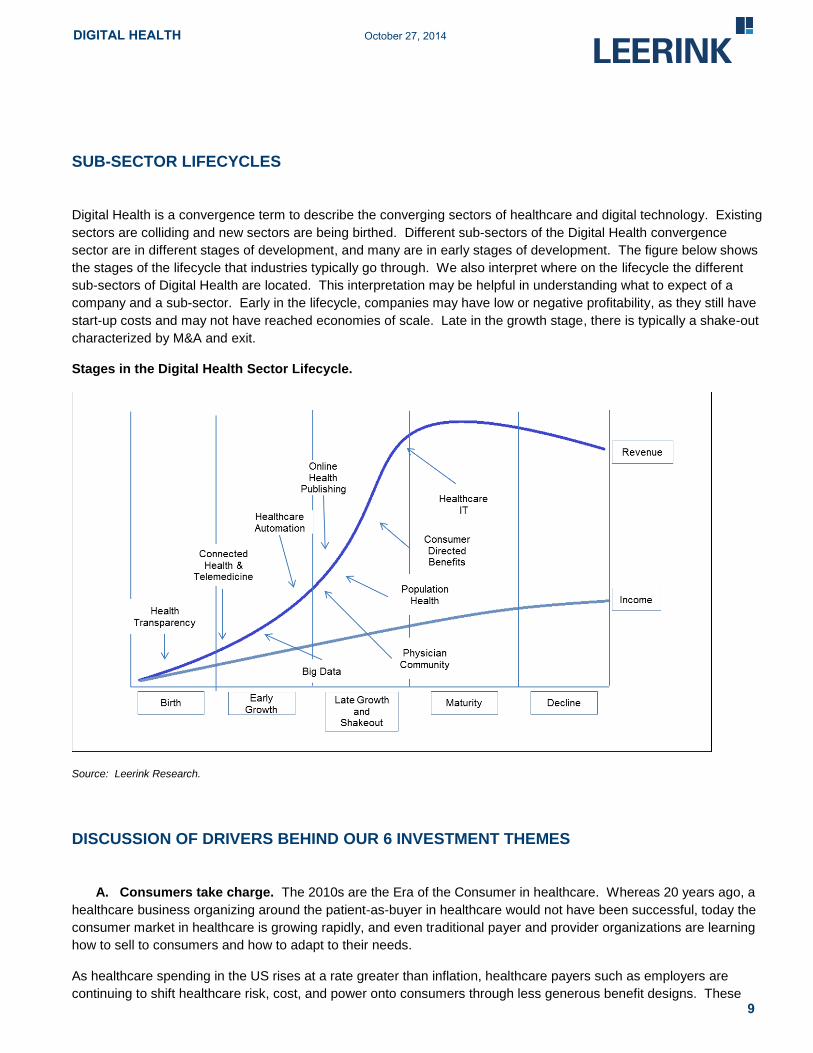

SUB-SECTOR LIFECYCLES

Digital Health is a convergence term to describe the converging sectors of healthcare and digital technology. Existing

sectors are colliding and new sectors are being birthed. Different sub-sectors of the Digital Health convergence

sector are in different stages of development, and many are in early stages of development. The figure below shows

the stages of the lifecycle that industries typically go through. We also interpret where on the lifecycle the different

sub-sectors of Digital Health are located. This interpretation may be helpful in understanding what to expect of a

company and a sub-sector. Early in the lifecycle, companies may have low or negative profitability, as they still have

start-up costs and may not have reached economies of scale. Late in the growth stage, there is typically a shake-out

characterized by M&A and exit.

Stages in the Digital Health Sector Lifecycle.

Source: Leerink Research.

DISCUSSION OF DRIVERS BEHIND OUR 6 INVESTMENT THEMES

A. Consumers take charge. The 2010s are the Era of the Consumer in healthcare. Whereas 20 years ago, a

healthcare business organizing around the patient-as-buyer in healthcare would not have been successful, today the

consumer market in healthcare is growing rapidly, and even traditional payer and provider organizations are learning

how to sell to consumers and how to adapt to their needs.

As healthcare spending in the US rises at a rate greater than inflation, healthcare payers such as employers are

continuing to shift healthcare risk, cost, and power onto consumers through less generous benefit designs. These 9

DIGITAL HEALTH October 27, 2014

benefit design changes include covering fewer employees, increasing deductibles in health plans, increasing co-pays

and co-insurance portions, and, ultimately, reducing and capping the amount of the health insurance benefit premium

that employers will pay. In this way, employers are moving from what has traditionally been a defined-benefit type of

employee benefit toward a defined-contribution benefit, following the path of employee retirement benefits in the late

20th century.

As payers shift healthcare costs onto consumers, they also shift responsibilities and decision-making onto the

consumers. Consumers can now direct healthcare spending as never before, and they are also spending more out-

of-pocket dollars on healthcare than ever before. We have identified 5 growing categories of consumer-empowered

spending in healthcare.

Categories of consumer-empowered healthcare spending:

1. Health plan selection. Consumers have a growing number of health plan options to choose from. Whereas

in the past, a participant in a health benefit might have been able to choose between an HMO and a PPO

from the same carrier, today benefit sponsors may provide to participants several in-house options from

multiple carriers. In addition, still more health plan options are available from private and public exchanges.

Growing consumer choice in health-plan options drives health plans to focus on the consumer as the

customer, instead of the benefit sponsor (such as the employer) as the customer. Carriers must therefore

design plan benefits and costs around the consumer in order to be competitive. All health insurance carriers

are designing plan options to compete in this environment. In addition, employee benefit consulting

companies like Towers Watson (TW) are setting up private insurance exchanges, such as Towers Watson’s

OneExchange, to assist their employer-clients in this transition, while offering multiple plan options to the

employee-participant.

2. Pre-deductible spending. Increasingly, benefit sponsors are shifting healthcare costs onto consumers by

sponsoring low premium / high-deductible health plans (HDHP), including IRS-qualified high-deductible health

plans that are paired with tax-advantaged spending accounts (such as Health Savings Accounts and Flexible

Spending Accounts) that allow employees to spend pre-tax earnings on healthcare. In 2014, the deductible of

a typical single employee in an HDHP was between $1,250 and $6,350 for the year. Consumers control this

healthcare spending (instead of employers) and it hits their wallets on a dollar-for-dollar basis, instead of

being subsidized by their employer. Healthcare providers and vendors who wish to earn the business of

these consumers must sell directly to the consumers. Consumer-directed benefit vendors such as

WageWorks (WAGE) and HealthEquity (HQY) are strongly affected by the shift to high-deductible health

plans. As employers shift health costs onto employees through these high-deductible health plans paired with

tax-advantaged spending accounts, the employers need to set up more consumer-directed benefit accounts

and process more funds through the accounts. Health-transparency data vendors like Castlight (CSLT) also

benefit from this cost shifting by employers, as employers pair the cost-shifting with consumer digital tools that

empower employees to optimize their care decisions.

3. Post-deductible spending. The effect of consumer control of pre-deductible spending in the healthcare

marketplace is multiplied because the spending patterns that consumers develop during the pre-deductible

phase of their health spending (such as using a health-transparency tool to choose one vendor over another

on account of its cost effectiveness) are typically carried over into the post-deductible spending covered by

the health benefit. Potentially all of a consumer’s healthcare spending can be set and directed by the

consumer on the basis of the decisions they made when they were directly spending their own money during

the pre-deductible phase.

10

DIGITAL HEALTH October 27, 2014

4. Consumer-influenced spending. Traditionally, the healthcare marketplace de-emphasized the consumer

because the physician/provider was the decision-maker and the health plan was the payer. Another way that

this traditional structure is now changing is that consumers are gaining additional influence even in areas of

healthcare where that traditional structure still exists. Increasingly, consumers arrive in the doctor’s office with

their own sources of information and opinions about their needs, and treat the physician as a gate-keeper to

the healthcare system rather than as the authoritative decision-maker. Patients may learn about new

pharmaceuticals through pharma direct-to-consumer “ask your doctor” ads for prescription drugs when

seeking information on websites such as Everyday Health (EVDY) and WebMD (WBMD), and go to their

physician requesting the drug (or procedure or device).

5. Direct consumer spending. Consumers are also increasingly willing to spend their post-tax consumer

dollars on healthcare products. A diabetic consumer may receive paper testing strips at no cost through her

health benefit, but may purchase a continuous blood glucose monitor on her own -- with her consumer dollars

-- for the benefits that it offers. A patient with chronic pain may self-manage with OTC drugs bought out of

pocket for the benefits of increased control and convenience and the potential for cost savings. Millions of

Americans have bought activity trackers from companies such as FitBit, Jawbone, and Misfit, or turned on

their smartphone’s activity-tracking settings, using the data from these devices to track their fitness, diet, and

sleep, or to help them self-manage their chronic conditions. Increasingly, health-conscious Americans are

willing to spend their own consumer dollars on health products, and vendors are responding with a wide

variety of consumer-oriented options. Websites such as WebMD (WBMD) and Everyday Health (EVDY) are

popular media channels that health brands turn to for an audience.

Beyond the structural changes described above, a secular social and demographic trend is changing healthcare. The

current generations driving the US economy, from Boomers to Millennials, are taking charge of their healthcare as

prior generations never did. Current generations are likely to question authority, whereas prior generations deferred

to authority. Current generations are likely to develop their own expertise, and they find the tools to accomplish this

readily available, whereas prior generations primarily sought out experts to hand their case over to. Current

generations proactively demand to be involved in their own healthcare, whereas prior generations wanted institutions

to be responsible.

B. Technology shocks. Belatedly, technology is one of the primary drivers of the digital revolution in healthcare.

Over the past 30 years, whereas high-tech sectors of the economy seemed to ride a “digital productivity curve”(driven

by Moore’s Law) of dramatic increases in cost-effectiveness, other sectors of the economy -- especially healthcare,

government, and education -- seemed stuck with slow improvements in productivity, or even negative productivity

trends (sometimes called Eroom’s Law, or Moore’s Law spelled backwards).

However, the last few years have seen breakthroughs in the application of digital technology to healthcare. The

digital revolution that has restructured other industries is finally shaking up healthcare. Health records that used to be

trapped on paper in manila folders in physician practices, or on film at hospitals, are now commonly born digital and

readily shared with members of the care team wherever they are and whenever they need access.

Healthcare products that were once unimaginable, that seemed too expensive for common use, and that were

necessarily controlled by specialty physicians, are now becoming accessible to all. If a component of a healthcare

product can be digitized, then it can follow the same curve of rapid productivity improvement as the rest of the digital

economy.

11

DIGITAL HEALTH October 27, 2014

Technology forces driving improvement in Digital Health include the following:

1.) Moore’s Law. The original Moore’s Law, which applied to the cost effectiveness of microprocessors, is now

joined by a cloud-computing variation of Moore’s Law. Both are now delivering technology shocks to the US

healthcare sector. The cost-effectiveness of cloud computing is growing, both on an absolute basis to users

and also in comparison to traditional enterprise-software infrastructure costs, as economies of scale play out

around cloud storage, transport, processing, and maintenance costs. Cloud-based companies in healthcare

like Benefitfocus (BNFT), Castlight Health (CSLT), athenahealth (ATHN), CareCloud, WageWorks (WAGE),

Veeva (VEEV), Medidata (MDSO), HealthEquity (HQY), and others are riding this curve, as do automation

companies like Omnicell (OMCL), Intuitive Surgical (ISRG, maker of the Da Vinci surgical robotics system),

and Imprivata (IMPR, which automates sign-on and authentication management across complex hospital

systems).

2.) Smartphones. The innovation curve of Digital Health is also being driven by the cost-effectiveness curve of

the smartphones in our pockets, as mass-market demand for these devices drives ever-lower per-unit costs

and ever more pervasive infrastructure support for components like video cameras, cellular radios, GPS

receivers, mobile processors, and body sensors. Companies propelled by these technology shocks include

companies with important mobile apps like WebMD (WBMD) and Everyday Health (EVDY) in the online

health publishing sub-sector; consumer digital tools companies like WageWorks (WAGE) and Castlight

(CSLT); and population health management companies like MDRevolution. In addition, activity tracker

companies like FitBit and Jawbone benefit, as do wearable medical device companies like DexCom (DXCM)

and Insulet (PODD), both of which make advanced diabetes medical devices.

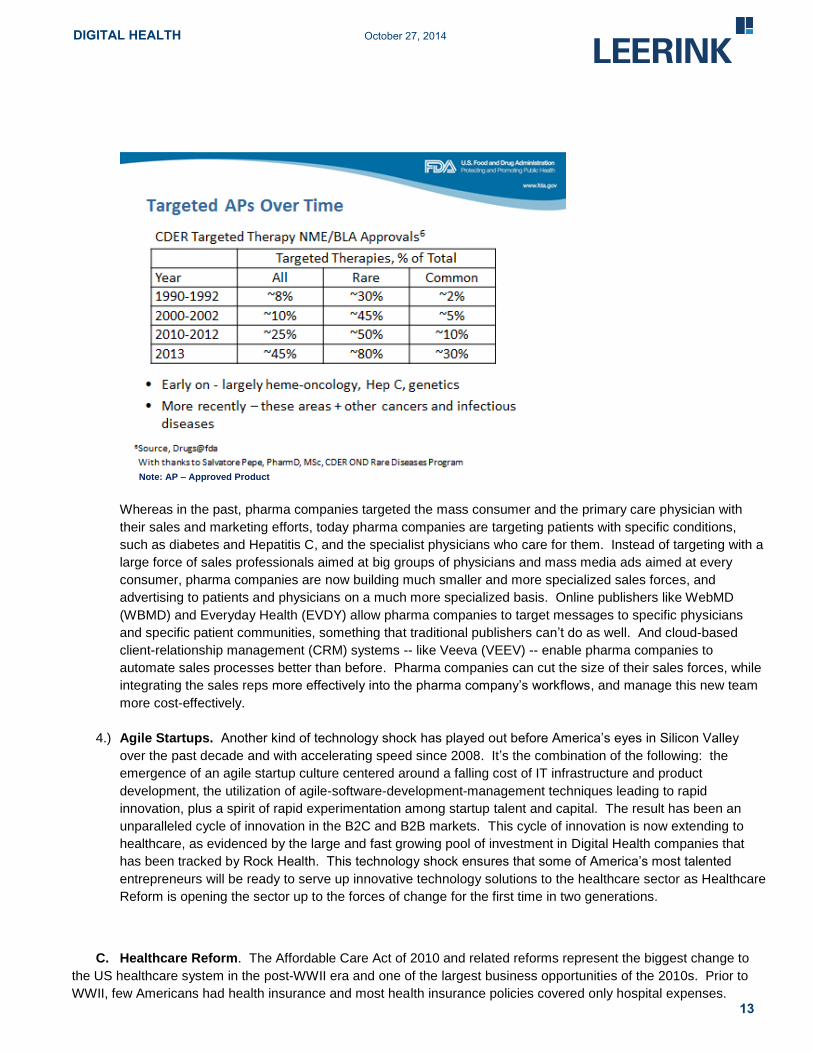

3.) Targeted Therapeutics. A third technology shock to hit the healthcare system is the progress of drug

development from primary-care blockbuster drugs -- such as ibuprofen-class drugs for pain relief and statin

drugs for high cholesterol -- to targeted therapeutics, which have the potential to stop the progression of major

diseases that have hitherto eluded successful treatment. Building on advances in the study of disease and in

the capabilities to manipulate biology, targeted therapeutics allow us to more effectively treat Crohn’s disease,

infertility, hepatitis C, cancer, growth-hormone deficiency, and other conditions. Over the past 10 years,

pharmaceutical companies have seen their primary-care blockbuster drugs go off-patent, as part of the

ongoing Patent Cliff, which peaked in the early 2010s. Pharma companies have adapted strategically by

shifting drug development to targeted therapeutics and restructuring the way that they sell and market the

drugs.

12

DIGITAL HEALTH October 27, 2014

Note: AP – Approved Product

Whereas in the past, pharma companies targeted the mass consumer and the primary care physician with

their sales and marketing efforts, today pharma companies are targeting patients with specific conditions,

such as diabetes and Hepatitis C, and the specialist physicians who care for them. Instead of targeting with a

large force of sales professionals aimed at big groups of physicians and mass media ads aimed at every

consumer, pharma companies are now building much smaller and more specialized sales forces, and

advertising to patients and physicians on a much more specialized basis. Online publishers like WebMD

(WBMD) and Everyday Health (EVDY) allow pharma companies to target messages to specific physicians

and specific patient communities, something that traditional publishers can’t do as well. And cloud-based

client-relationship management (CRM) systems -- like Veeva (VEEV) -- enable pharma companies to

automate sales processes better than before. Pharma companies can cut the size of their sales forces, while

integrating the sales reps more effectively into the pharma company’s workflows, and manage this new team

more cost-effectively.

4.) Agile Startups. Another kind of technology shock has played out before America’s eyes in Silicon Valley

over the past decade and with accelerating speed since 2008. It’s the combination of the following: the

emergence of an agile startup culture centered around a falling cost of IT infrastructure and product

development, the utilization of agile-software-development-management techniques leading to rapid

innovation, plus a spirit of rapid experimentation among startup talent and capital. The result has been an

unparalleled cycle of innovation in the B2C and B2B markets. This cycle of innovation is now extending to

healthcare, as evidenced by the large and fast growing pool of investment in Digital Health companies that

has been tracked by Rock Health. This technology shock ensures that some of America’s most talented

entrepreneurs will be ready to serve up innovative technology solutions to the healthcare sector as Healthcare

Reform is opening the sector up to the forces of change for the first time in two generations.

C. Healthcare Reform. The Affordable Care Act of 2010 and related reforms represent the biggest change to

the US healthcare system in the post-WWII era and one of the largest business opportunities of the 2010s. Prior to

WWII, few Americans had health insurance and most health insurance policies covered only hospital expenses. 13

DIGITAL HEALTH October 27, 2014

However, during WWII the War Labor Board ruled that the ongoing wage freeze didn’t apply to fringe benefits, and

employers responded by using health benefits to compete for workers during a time of labor shortages. This change

kicked off the modern American healthcare payment system – with employers providing health insurance as a tax-

advantaged fringe benefit. Government reinforced this system both as a conventional employer and also as the

insurer of the old (Medicare) and the poor (Medicaid).

Many of the modern healthcare system’s much-observed ailments have been attributed over time to its fundamental

fee-for-service payment structure. Healthcare’s expensive procedures and suspected overutilization of care is

attributed to the system’s bias to pay for procedures but not to pay for quality, or thinking about options, or prevention,

or waiting to take action, or maintaining wellness. The system’s lack of a true marketplace is attributed to

misalignment of incentives among the user (the patient), the decision maker (the provider / physician), and the payer

(the insurance carrier). Due to the healthcare system’s decentralized nature, it has proven difficult to improve any one

part without reforming all of the healthcare system (and the healthcare payment system too). And payment reform

ultimately required changes in healthcare policy and law that the political system couldn’t deliver until recently.

Under the traditional healthcare system, the misalignment among payers, providers, and patients often punished

innovation:

Prospective innovators found that they had to bear all the cost of innovation, while the benefits were spread

diffusely among other participants, without enough of the benefits accruing to the innovator to justify the cost.

Thus physicians rejected electronic medical records at their practices because they would have to bear the

cost of the system in time and money -- with not enough benefit accruing to their practice, they felt, to justify

the cost.

Innovations that required different sector participants to adopt their innovation withered because of lack of

agreement on priorities among participants.

Vendors would find their innovative product rejected by otherwise-receptive physicians because the

innovators needed to get assurance of reimbursement from payers first before physicians would prescribe or

use the innovative products.

Clinicians weren’t allowed to use basic productivity technology in the practice of medicine because it didn’t

meet HIPAA standards. And lack of critical mass in electronic clinical systems caused sector participants to

default to paper and physical mediums of collaboration, denying the collaborative benefits of electronic

systems to the participants who adopted them early.

Payers refused to reimburse an innovative product because the costs were too high to cover the innovation

for members who could be changing carriers within a couple of years anyway.

Wellness products were rejected by the healthcare system because of a traditional agreement to reimburse

for sick care but not for population health.

Providers who innovated to develop higher-quality procedures found the system didn’t reward high-quality

care and didn’t punish low-quality care.

Patients over-consumed expensive care because they didn’t have to pay the bills.

The consequences of the healthcare system’s misalignments could fill many pages and have contributed to America’s

having the highest per-capita healthcare expenses in the world with sometimes less-than-the-best outcomes. The

result of these problems in the US healthcare system was that throughout the late 20th and early 21

st centuries, while

US businesses were pioneering world-class productivity, collaboration, and automation systems in offices and

factories, healthcare’s payers and providers seemed stuck in a darkly-humorous parallel universe of old and kludgey

technology, including telephone answering services, color-coded manila folders, large film negatives, paper clips,

monochrome computer screens, multiple computer key-function codes from 1980s DOS manuals, handwritten phone

messages on pink sheets of paper, and deliveries of critical workflow documents through the postal system. Our 21st

century brain surgeons are still wearing beepers and reading faxes. 14

DIGITAL HEALTH October 27, 2014

The healthcare reforms of the 2010s have opened up the healthcare system -- the largest single component of the US

economy -- to the adoption of the same wave of productivity, collaboration, and automation systems as the rest of the

economy. Like a third-world country in the 1990s that could skip over the building of a copper-line telephone network

in favor of going straight to the latest mobile phone system, the US healthcare sector now has the opportunity to adopt

the latest cloud-based systems while skipping over the prior generation of enterprise systems built by pioneers in the

business sector. The US healthcare sector can now jet straight to Malibu without having to trek for weeks in

Conestoga wagons through a technological Death Valley.

15

DIGITAL HEALTH October 27, 2014

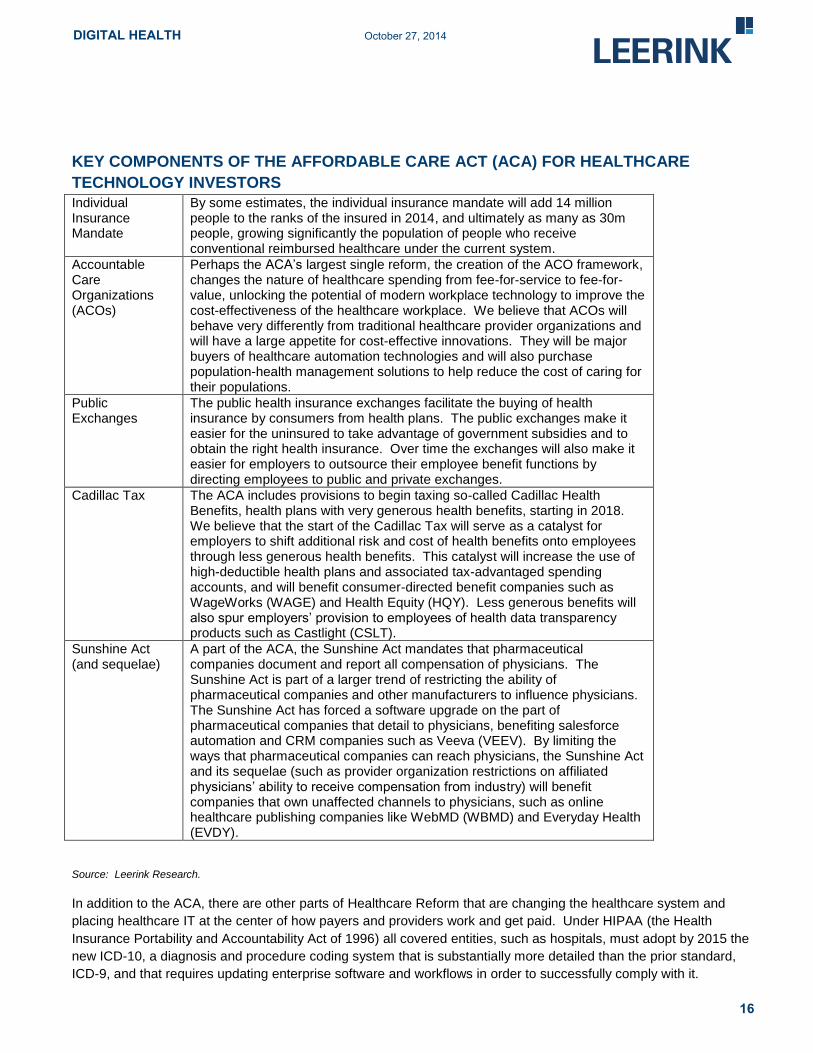

KEY COMPONENTS OF THE AFFORDABLE CARE ACT (ACA) FOR HEALTHCARE

TECHNOLOGY INVESTORS

Individual Insurance Mandate

By some estimates, the individual insurance mandate will add 14 million people to the ranks of the insured in 2014, and ultimately as many as 30m people, growing significantly the population of people who receive conventional reimbursed healthcare under the current system.

Accountable Care Organizations (ACOs)

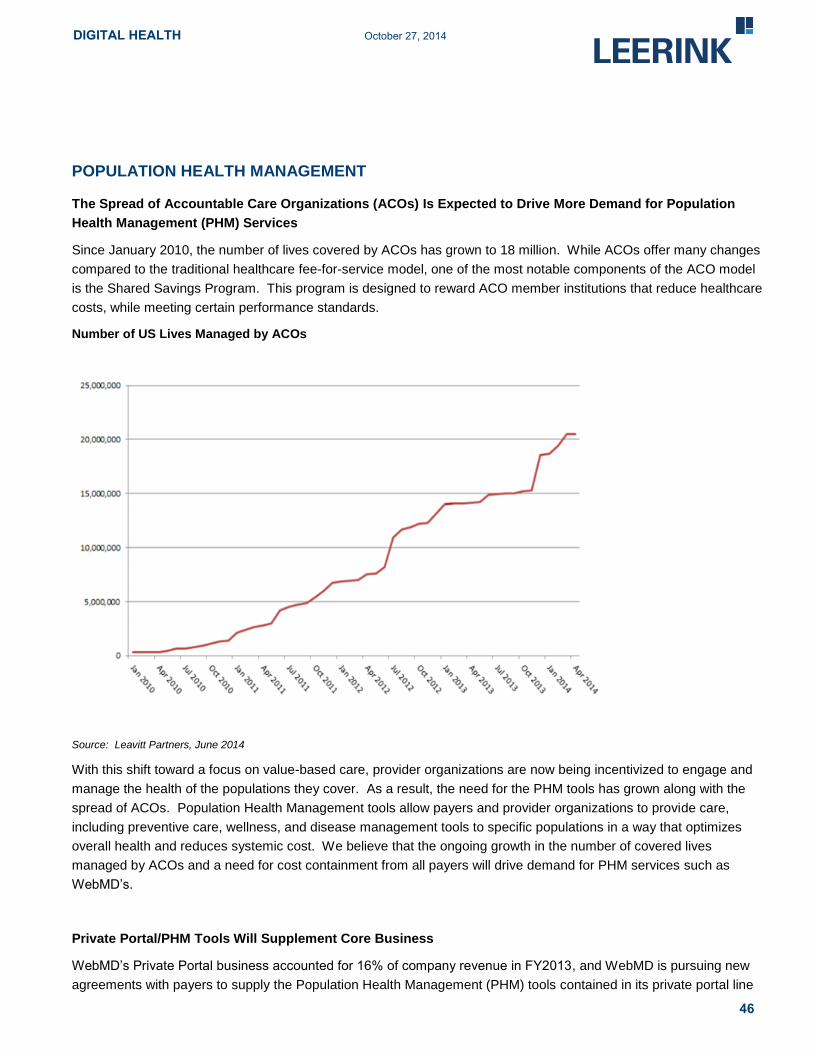

Perhaps the ACA’s largest single reform, the creation of the ACO framework, changes the nature of healthcare spending from fee-for-service to fee-for-value, unlocking the potential of modern workplace technology to improve the cost-effectiveness of the healthcare workplace. We believe that ACOs will behave very differently from traditional healthcare provider organizations and will have a large appetite for cost-effective innovations. They will be major buyers of healthcare automation technologies and will also purchase population-health management solutions to help reduce the cost of caring for their populations.

Public Exchanges

The public health insurance exchanges facilitate the buying of health insurance by consumers from health plans. The public exchanges make it easier for the uninsured to take advantage of government subsidies and to obtain the right health insurance. Over time the exchanges will also make it easier for employers to outsource their employee benefit functions by directing employees to public and private exchanges.

Cadillac Tax The ACA includes provisions to begin taxing so-called Cadillac Health Benefits, health plans with very generous health benefits, starting in 2018. We believe that the start of the Cadillac Tax will serve as a catalyst for employers to shift additional risk and cost of health benefits onto employees through less generous health benefits. This catalyst will increase the use of high-deductible health plans and associated tax-advantaged spending accounts, and will benefit consumer-directed benefit companies such as WageWorks (WAGE) and Health Equity (HQY). Less generous benefits will also spur employers’ provision to employees of health data transparency products such as Castlight (CSLT).

Sunshine Act (and sequelae)

A part of the ACA, the Sunshine Act mandates that pharmaceutical companies document and report all compensation of physicians. The Sunshine Act is part of a larger trend of restricting the ability of pharmaceutical companies and other manufacturers to influence physicians. The Sunshine Act has forced a software upgrade on the part of pharmaceutical companies that detail to physicians, benefiting salesforce automation and CRM companies such as Veeva (VEEV). By limiting the ways that pharmaceutical companies can reach physicians, the Sunshine Act and its sequelae (such as provider organization restrictions on affiliated physicians’ ability to receive compensation from industry) will benefit companies that own unaffected channels to physicians, such as online healthcare publishing companies like WebMD (WBMD) and Everyday Health (EVDY).

Source: Leerink Research.

In addition to the ACA, there are other parts of Healthcare Reform that are changing the healthcare system and

placing healthcare IT at the center of how payers and providers work and get paid. Under HIPAA (the Health

Insurance Portability and Accountability Act of 1996) all covered entities, such as hospitals, must adopt by 2015 the

new ICD-10, a diagnosis and procedure coding system that is substantially more detailed than the prior standard,

ICD-9, and that requires updating enterprise software and workflows in order to successfully comply with it.

16

DIGITAL HEALTH October 27, 2014

Also, under the American Recovery and Reinvestment Act of 2009 (ARRA) and its included HITECH Act, healthcare

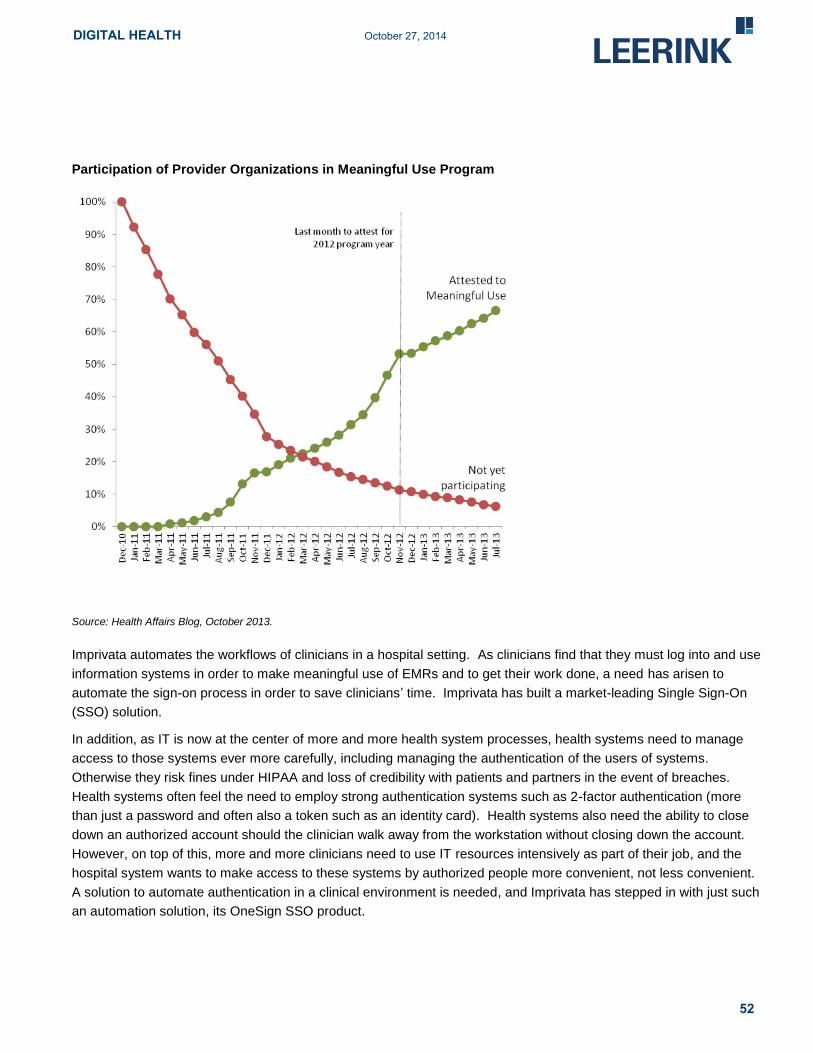

providers can receive financial rewards for the Meaningful Use of Electronic Health Records. Currently, providers

must meet additional use requirements under Stage 2 of Meaningful Use in the 2014-15 timeframe in order to

continue to receive these rewards. Provider organizations that decline to participate in the Meaningful Use program

initially forgo its financial rewards, and later are subject to reimbursement penalties from CMS for not satisfying its

billing requirements.

The combination of these policies has triggered multiple waves of healthcare IT software upgrades and put healthcare

IT in 2014 at the center of how healthcare payers and providers improve care, cut costs, and get paid. Instead of

necessarily defaulting to the lowest common technological standard of paper documentation and communication,

healthcare participants can now train and organize around advanced electronic systems. A critical mass of

participants in healthcare online has been reached, and participants can now count on doing their work digitally.

Laggard provider organizations must also make deferred investments in IT systems in order to stay current and

interoperate with their peers and payers. The emergence of IT at the center of healthcare is benefiting automation

companies like Imprivata (IMPR), which automates the sign-on and authentication process for healthcare providers

across multiple healthcare IT systems, and Omnicell (OMCL), which automates the hospital pharmacy.

D. Demographics. Major demographic trends are boosting demand for digital solutions to healthcare

challenges. At the older end of the demographic spectrum, Boomers are retiring in vast numbers and becoming major

consumers of healthcare services, triggering a number of changes. Healthcare has long been viewed as a labor-

intensive service sector that has resisted automation. But as the Boomers enter retirement at a time of

unprecedentedly high healthcare spending and a growing gap in the adequate supply of healthcare providers,

Boomers are increasingly demanding healthcare and eldercare services. In addition, unlike prior generations who

saw themselves as recipients of care from institutions and authorities, Boomers are taking charge of their care

through their own spending and demanding that their care be customized to them. In order for their care to be

convenient, personalized and affordable, there’s an increased need for automation.

Earlier along the demographic spectrum are the Millennials, a generation that was “born digital” and that turns first to

internet-connected mobile devices for information, connection, work, and play. Businesses that want to serve

Millennials will need to figure out how to serve them on their mobile devices.

In between the Boomers and the Millennials, the rest of America is responding to the technological shocks of the past

30 years by changing how they spend their time and how they want to receive care. They are consuming information

from online sources such as the web and mobile apps. And they too are changing how they want to interact with their

healthcare vendors and providers, switching from offline activities, such as calling a doctor’s office, to online activities,

such as finding a provider and booking a visit through a mobile app.

These demographic changes are boosting healthcare benefit vendors that engage with their members through web

and mobile: vendors such as WageWorks (WAGE), Health Equity (HQY), and Castlight (CSLT). The trend to online

activities also benefits healthcare publishers with a strong web and mobile presence such as WebMD (WBMD) and

Everyday Health (EVDY), and population health vendors with mobile apps such as Weight Watchers (WTW) and

Healthways (HWAY). This web and mobile trend also helps medical device companies that are building brands in the

hearts of consumers, such as DexCom (DXCM) and Insulet (PODD).

We believe that the convergence of positive technology shocks powered by Moore’s Law with demographic shifts

such as retiring boomers and provider shortages, plus the world’s highest healthcare costs, is spawning an

unprecedented wave of automation in healthcare. Increasingly we’re receiving our healthcare in new ways – such as

at home, through connected devices, and with the assistance of automation.

17

DIGITAL HEALTH October 27, 2014

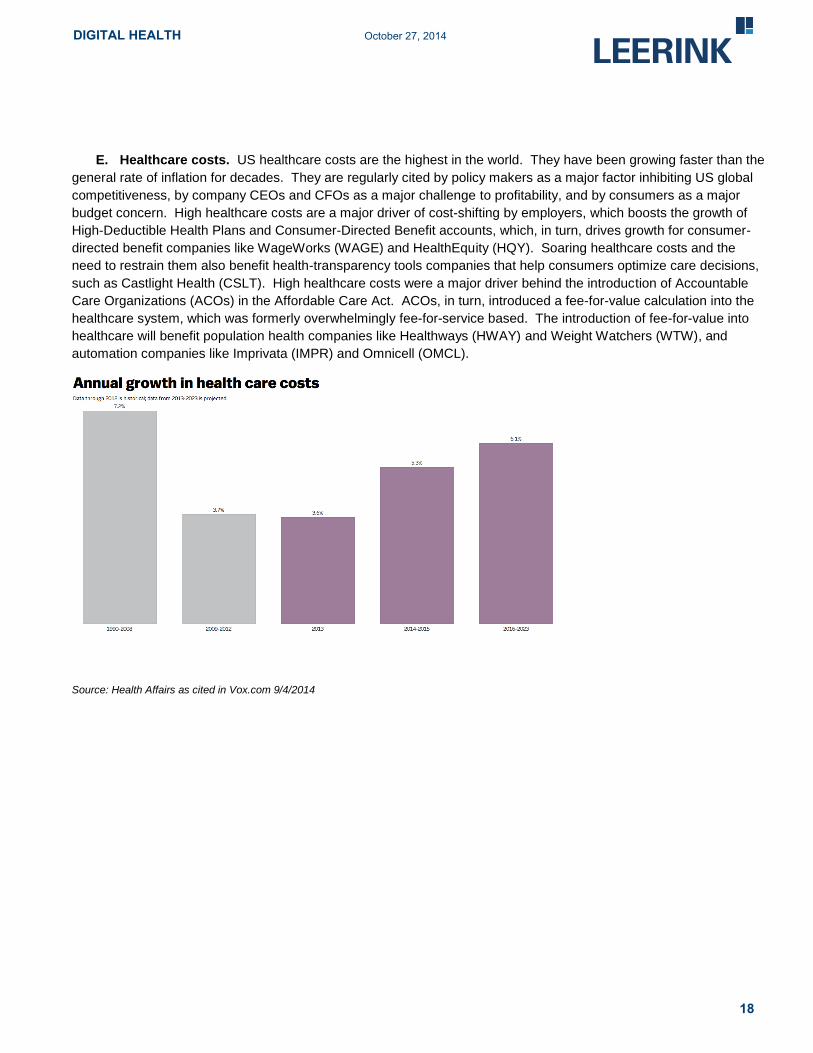

E. Healthcare costs. US healthcare costs are the highest in the world. They have been growing faster than the

general rate of inflation for decades. They are regularly cited by policy makers as a major factor inhibiting US global

competitiveness, by company CEOs and CFOs as a major challenge to profitability, and by consumers as a major

budget concern. High healthcare costs are a major driver of cost-shifting by employers, which boosts the growth of

High-Deductible Health Plans and Consumer-Directed Benefit accounts, which, in turn, drives growth for consumer-

directed benefit companies like WageWorks (WAGE) and HealthEquity (HQY). Soaring healthcare costs and the

need to restrain them also benefit health-transparency tools companies that help consumers optimize care decisions,

such as Castlight Health (CSLT). High healthcare costs were a major driver behind the introduction of Accountable

Care Organizations (ACOs) in the Affordable Care Act. ACOs, in turn, introduced a fee-for-value calculation into the

healthcare system, which was formerly overwhelmingly fee-for-service based. The introduction of fee-for-value into

healthcare will benefit population health companies like Healthways (HWAY) and Weight Watchers (WTW), and

automation companies like Imprivata (IMPR) and Omnicell (OMCL).

Source: Health Affairs as cited in Vox.com 9/4/2014

18

DIGITAL HEALTH October 27, 2014

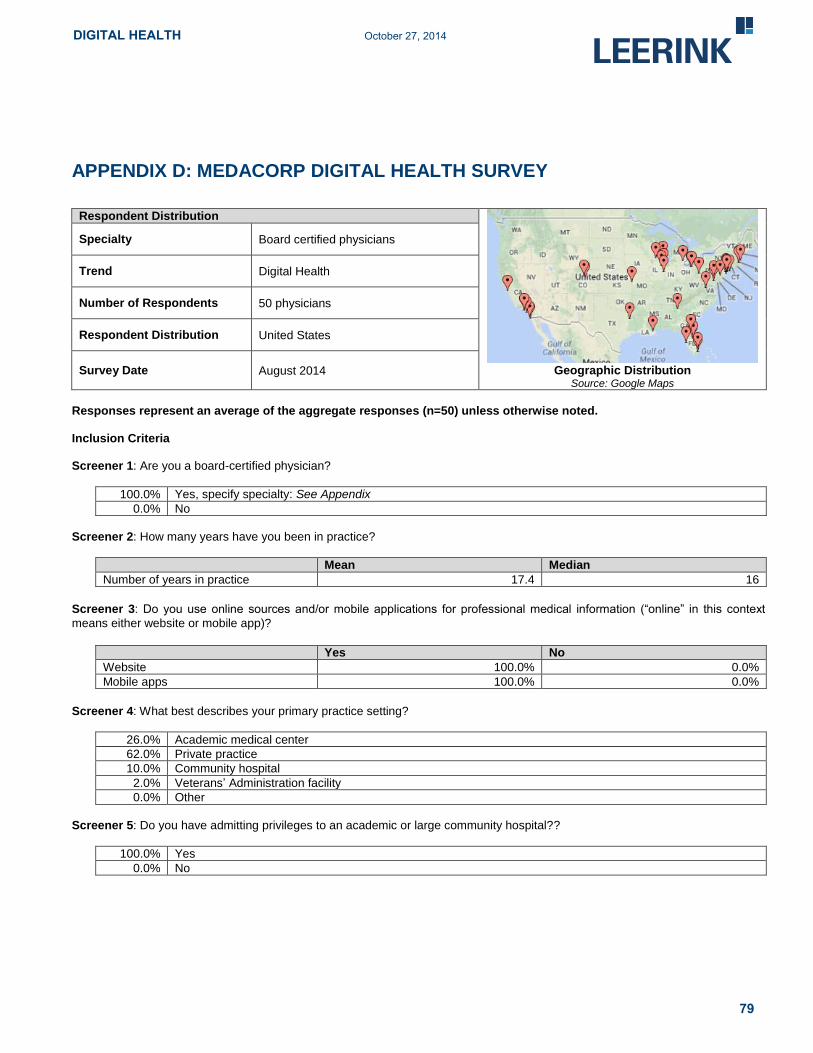

MEDACORP SURVEY REVEALS CHANGE IN PHYSICIAN BEHAVIOR

Digital Health Survey Points to Increase in Online Content Demand

Our recent survey of 50 board-certified physicians reveals fundamental changes in physician behavior in terms of how

new digital technology is used in their everyday practice. The focus of this survey was centered on digital content

distribution, advertisements, and the single sign-on (SSO) system. Among our Digital Health coverage universe, the

companies that will be most impacted by content and advertisement decisions and trends are WebMD (WBMD) and

Everyday Health (EVDY). Data from the survey suggest that within the next ~3-5 years, there will be significant growth

in demand for digital content, especially for the mobile health segment. Advertisers will see opportunities as a result.

And the increasing interest in and adoption of single sign-on will benefit Imprivata (IMPR).

Usefulness of SSO Is Above Average, According to Results

Demand by physicians for single sign-on products will most directly impact Imprivata (IMPR). The general sentiment

of our surveyed physicians is that SSO’s usefulness is above average, and time saved can be up to an hour per shift,

but mostly hovers around 10-15 minutes per day. The market opportunity for Imprivata is presently narrow due to the

SSO product category’s low visibility and limited exposure among physicians. However, there could be significant

market upside to Imprivata given the growing interest in the product category combined with barriers to entry to new

competition, due to the need to integrate with many other software systems in order to sell a viable product.

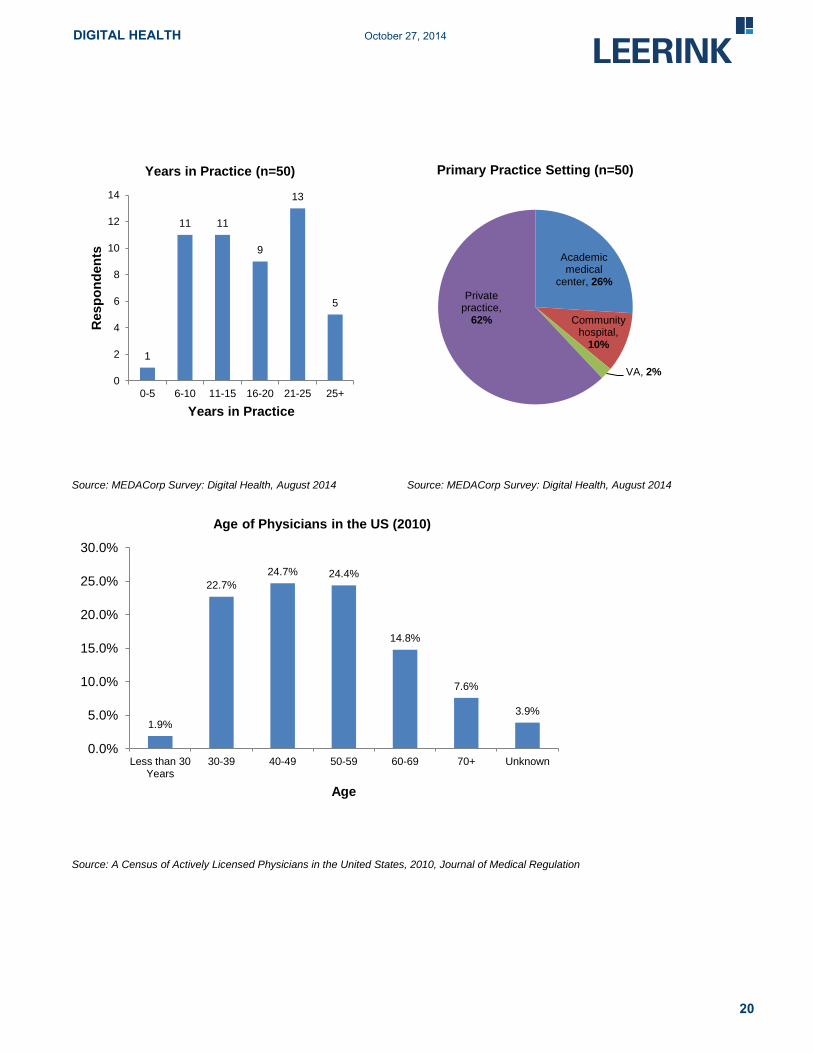

Demographics: Survey Respondents Skew to a Younger Group

Among MEDACorp’s 50 surveyed physicians, the majority work in private practice, followed by academic medical

centers, community hospitals, and Veterans Administration facilities. By comparing our survey sample with the survey

results from the Center for Studying Health System Change (below), we believe that academic medical centers could

be over-represented in the MEDACorp survey. In terms of experience, almost all MEDACorp respondents have been

practicing for at least 5 years, and all use online or mobile apps at least one hour a week. The average number of

years in practice is ~17, with the lowest being 3 years and highest being 40. The distribution of our MEDACorp survey

leans towards the younger side of the spectrum, however, and therefore could show a skew toward use of technology,

especially mobile technology. In our survey, 62% of respondents have <20 years’ experience, in contrast with ~50% in

the chart from the Journal of Medical Regulation also cited below. MEDACorp respondents were mostly located in the

Northeast, Florida, the Illinois/Chicago area, and the California coast, with a scattering throughout the Midwest.

19

DIGITAL HEALTH October 27, 2014

Source: MEDACorp Survey: Digital Health, August 2014 Source: MEDACorp Survey: Digital Health, August 2014

Source: A Census of Actively Licensed Physicians in the United States, 2010, Journal of Medical Regulation

1

11 11

9

13

5

0

2

4

6

8

10

12

14

0-5 6-10 11-15 16-20 21-25 25+

Resp

on

den

ts

Years in Practice

Years in Practice (n=50)

Academic medical

center, 26%

Community hospital,

10%

VA, 2%

Private practice,

62%

Primary Practice Setting (n=50)

1.9%

22.7%

24.7% 24.4%

14.8%

7.6%

3.9%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Less than 30Years

30-39 40-49 50-59 60-69 70+ Unknown

Age

Age of Physicians in the US (2010)

20

DIGITAL HEALTH October 27, 2014

Source: Center for Studying Health System Change: 2008 Health Tracking Physician Survey

Geographic Distribution of Physicians in MEDACorp Digital Health Survey

Symbols represent responding physicians

Source: Google Maps, MEDACorp Survey: Digital Health, August 2014

21

DIGITAL HEALTH October 27, 2014

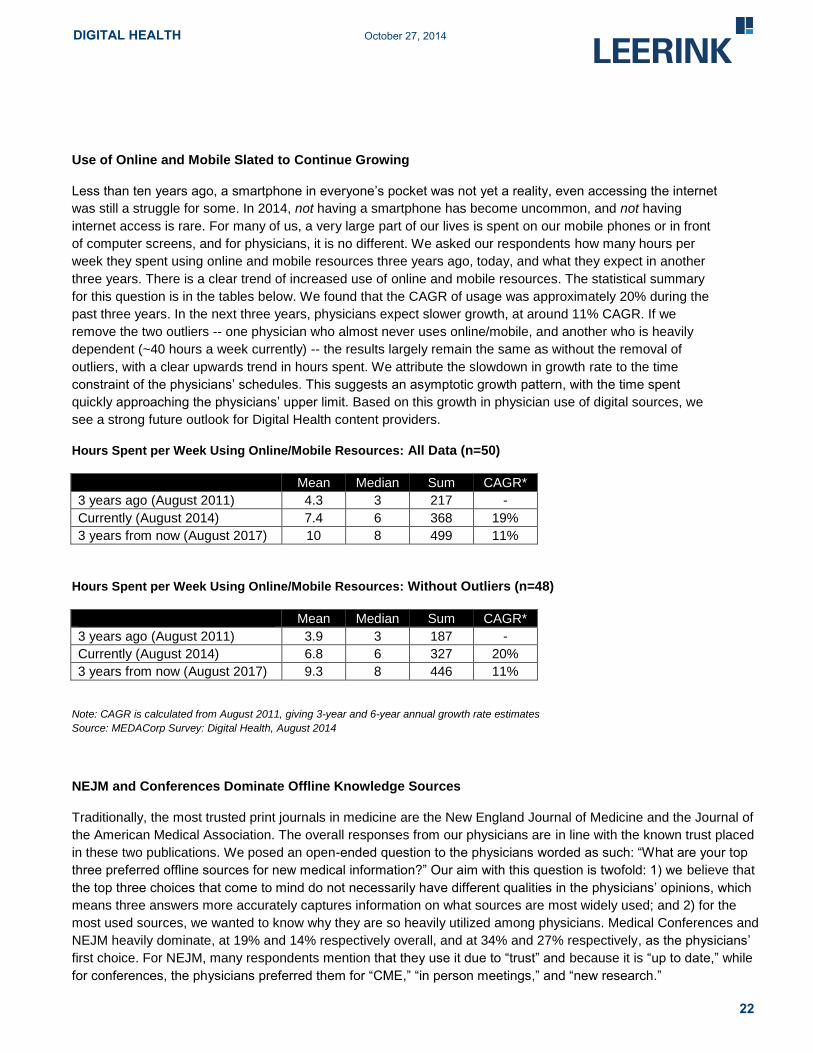

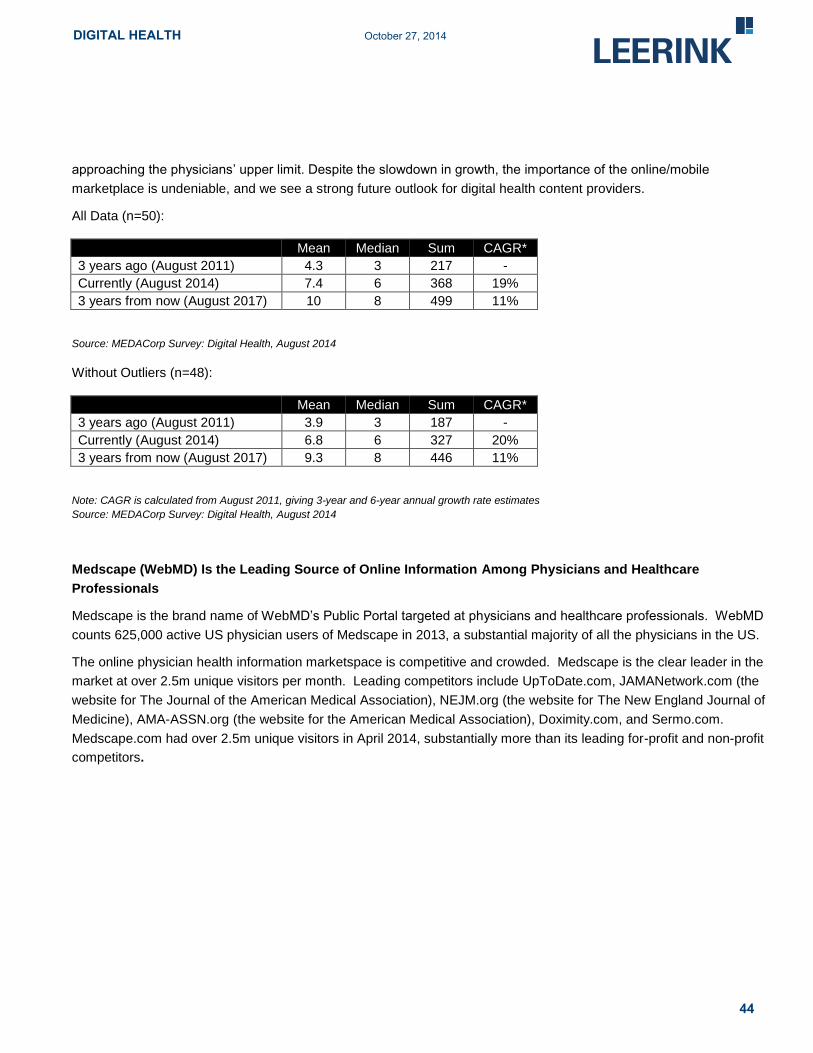

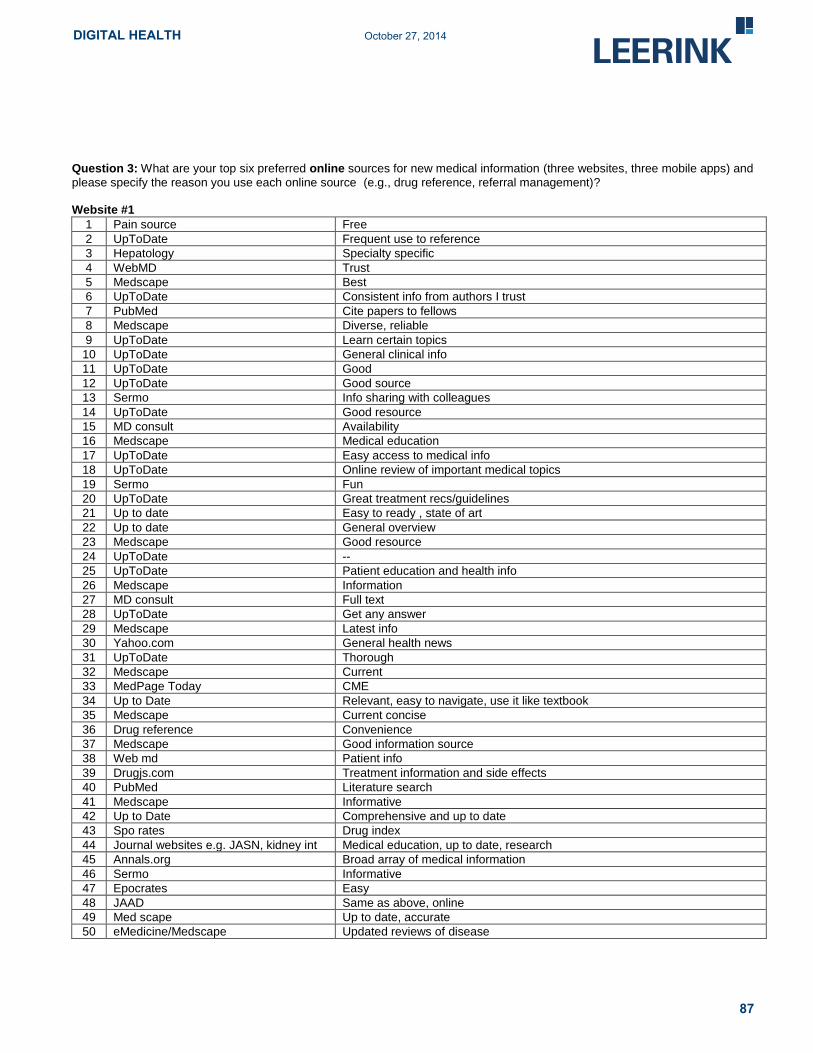

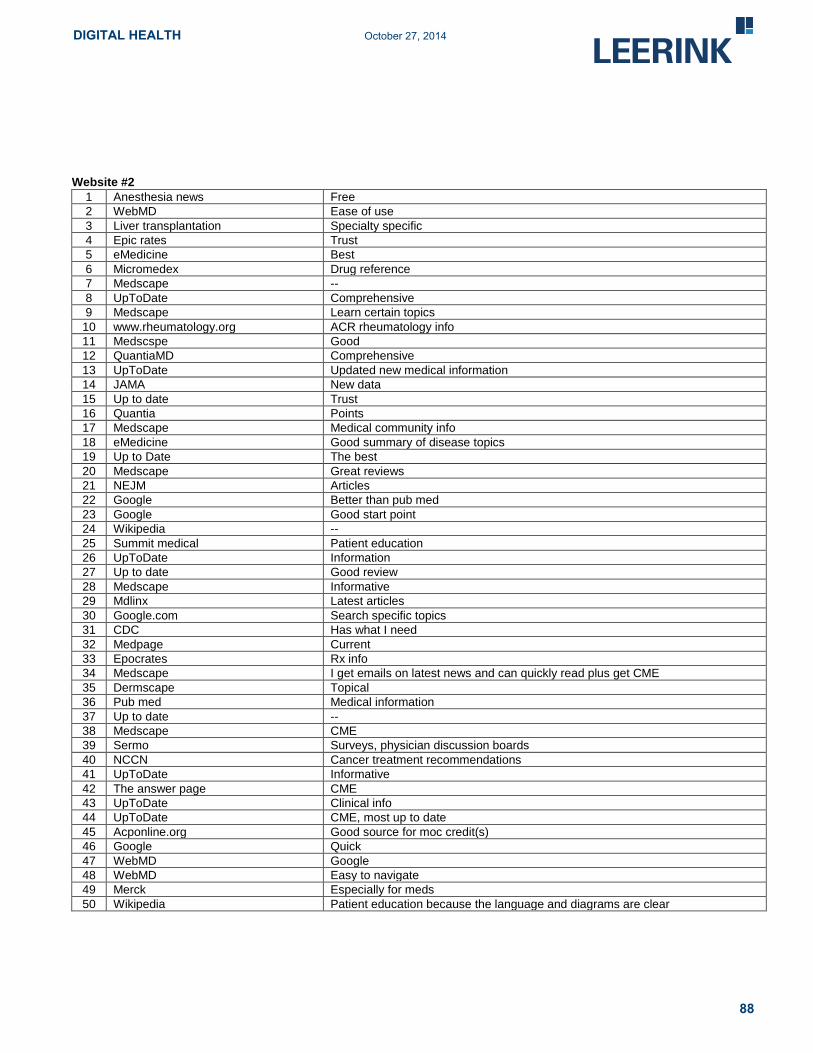

Use of Online and Mobile Slated to Continue Growing

Less than ten years ago, a smartphone in everyone’s pocket was not yet a reality, even accessing the internet

was still a struggle for some. In 2014, not having a smartphone has become uncommon, and not having

internet access is rare. For many of us, a very large part of our lives is spent on our mobile phones or in front

of computer screens, and for physicians, it is no different. We asked our respondents how many hours per

week they spent using online and mobile resources three years ago, today, and what they expect in another

three years. There is a clear trend of increased use of online and mobile resources. The statistical summary

for this question is in the tables below. We found that the CAGR of usage was approximately 20% during the

past three years. In the next three years, physicians expect slower growth, at around 11% CAGR. If we

remove the two outliers -- one physician who almost never uses online/mobile, and another who is heavily

dependent (~40 hours a week currently) -- the results largely remain the same as without the removal of

outliers, with a clear upwards trend in hours spent. We attribute the slowdown in growth rate to the time

constraint of the physicians’ schedules. This suggests an asymptotic growth pattern, with the time spent

quickly approaching the physicians’ upper limit. Based on this growth in physician use of digital sources, we

see a strong future outlook for Digital Health content providers.

Hours Spent per Week Using Online/Mobile Resources: All Data (n=50)

Mean Median Sum CAGR*

3 years ago (August 2011) 4.3 3 217 -

Currently (August 2014) 7.4 6 368 19%

3 years from now (August 2017) 10 8 499 11%

Hours Spent per Week Using Online/Mobile Resources: Without Outliers (n=48)

Mean Median Sum CAGR*

3 years ago (August 2011) 3.9 3 187 -

Currently (August 2014) 6.8 6 327 20%

3 years from now (August 2017) 9.3 8 446 11%

Note: CAGR is calculated from August 2011, giving 3-year and 6-year annual growth rate estimates

Source: MEDACorp Survey: Digital Health, August 2014

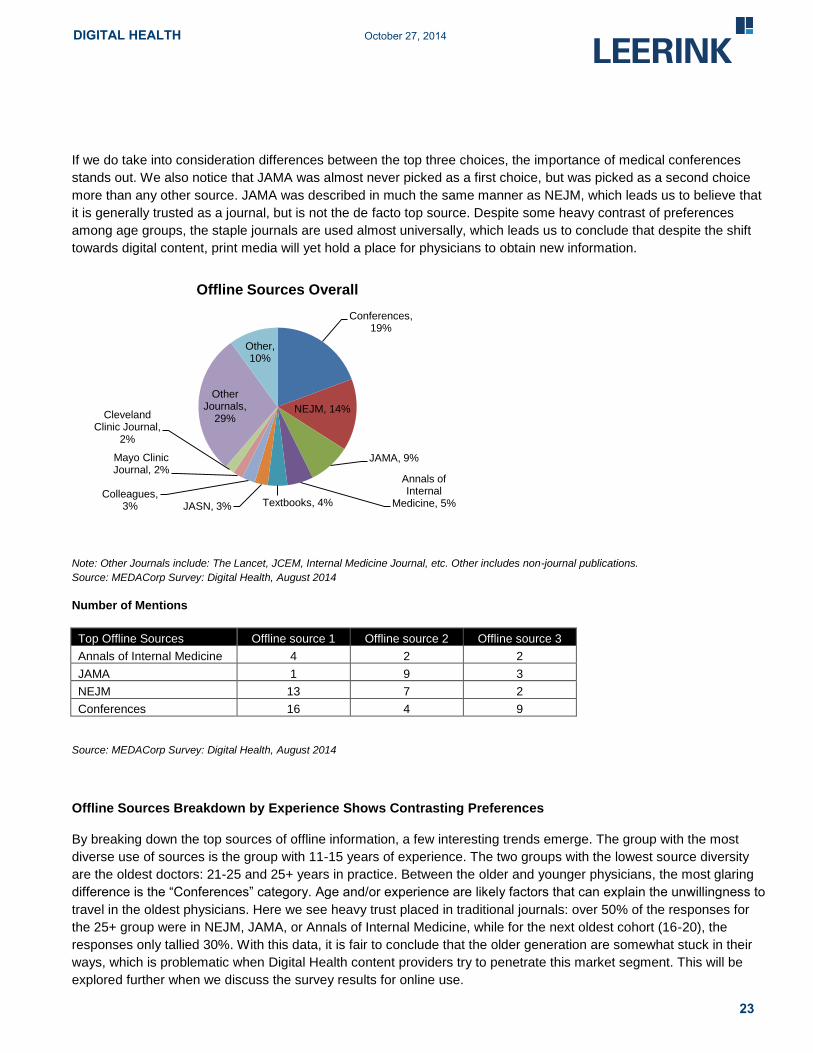

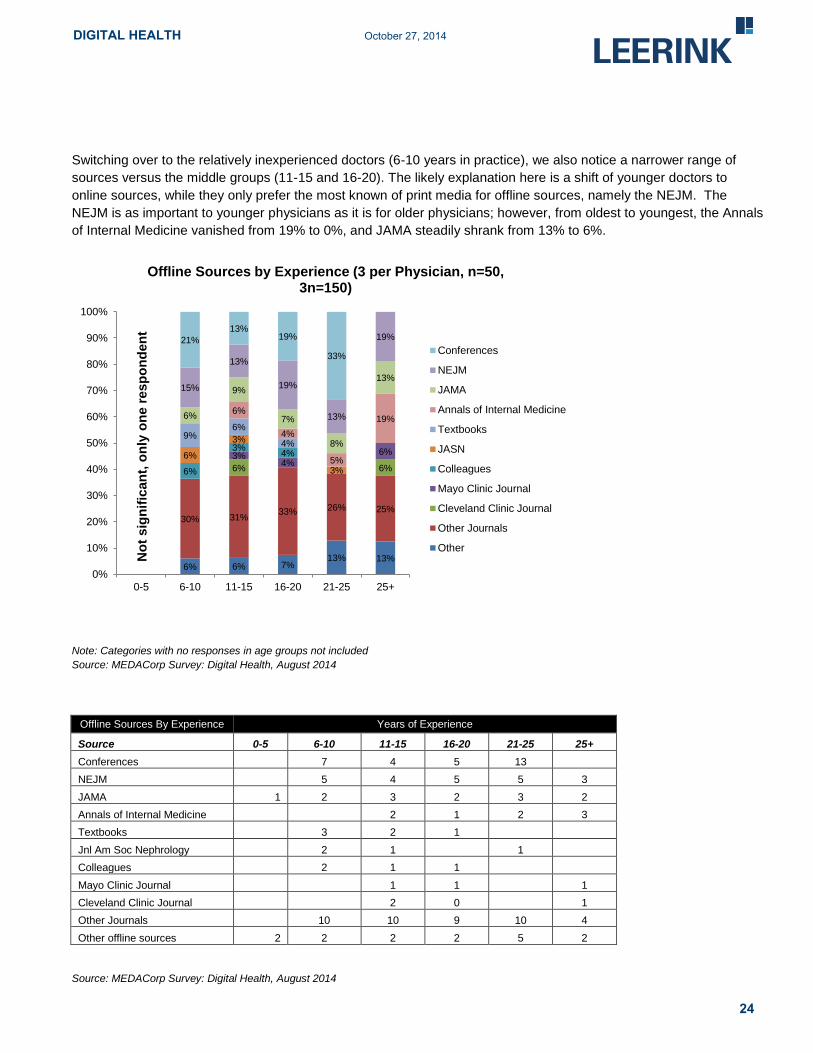

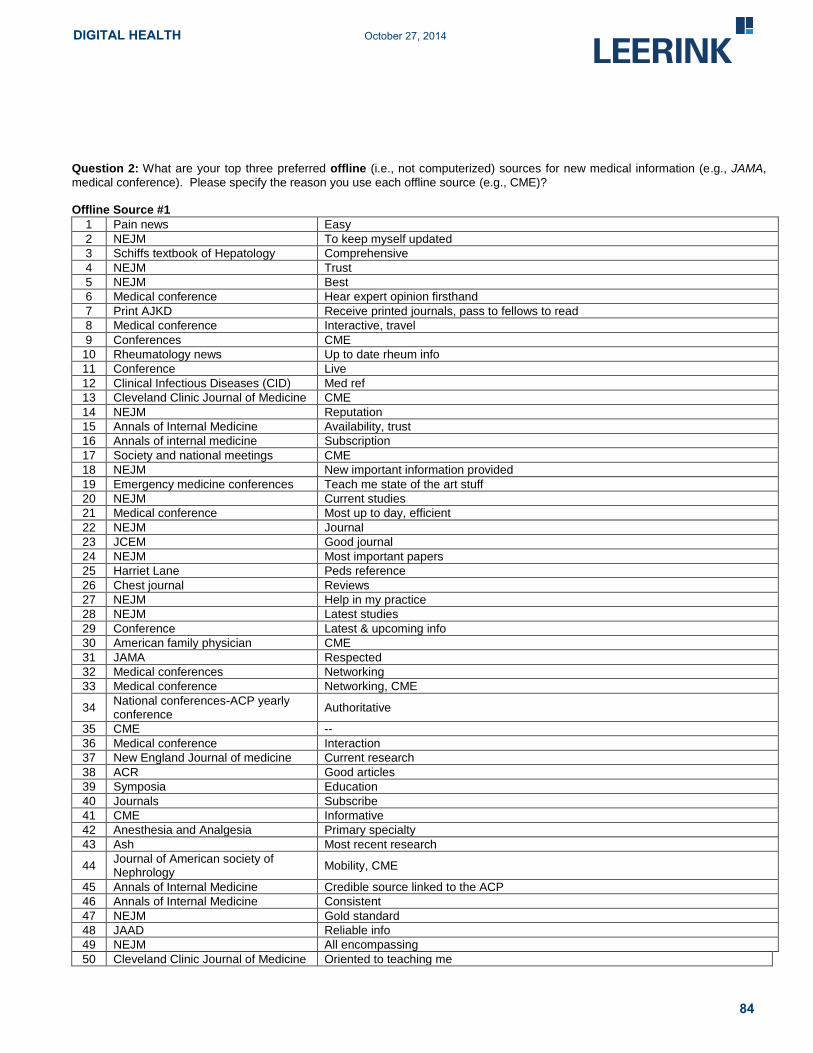

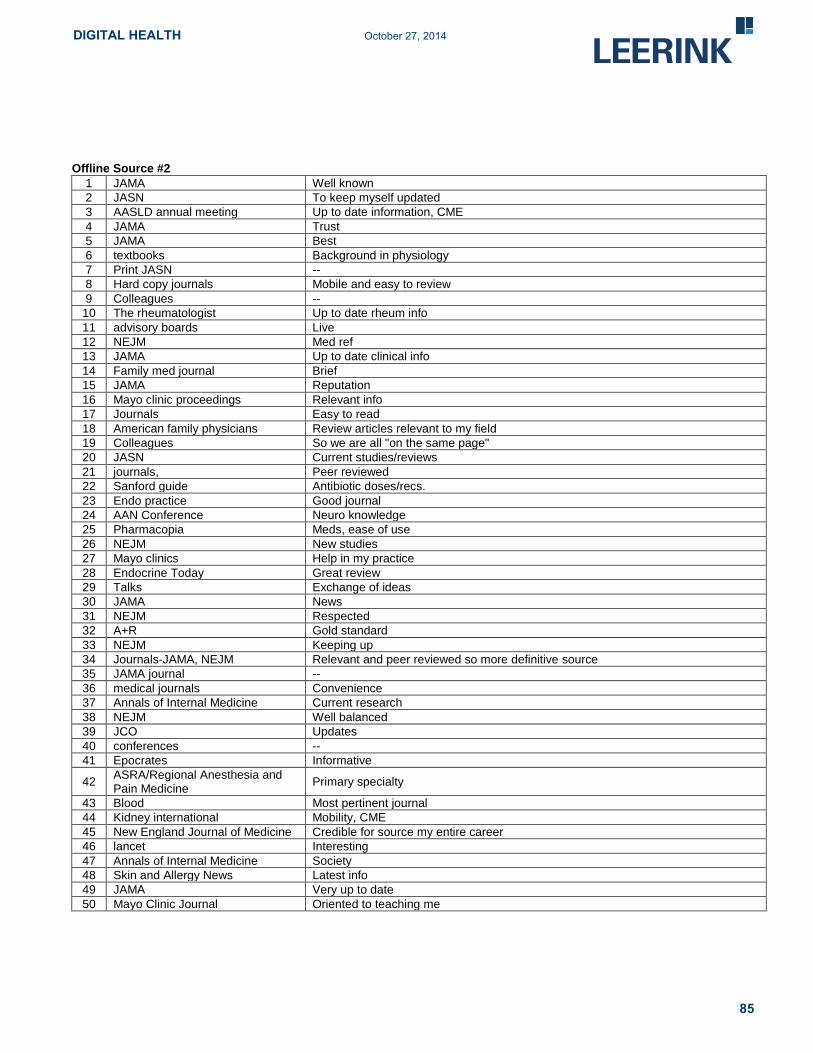

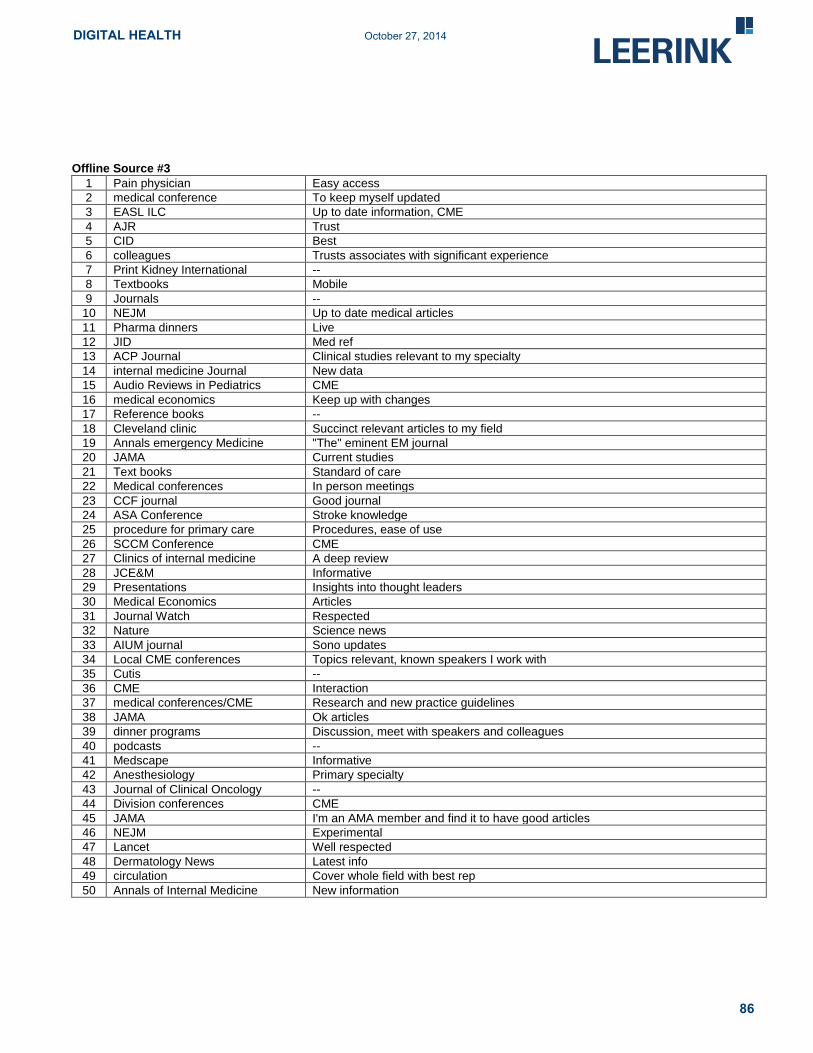

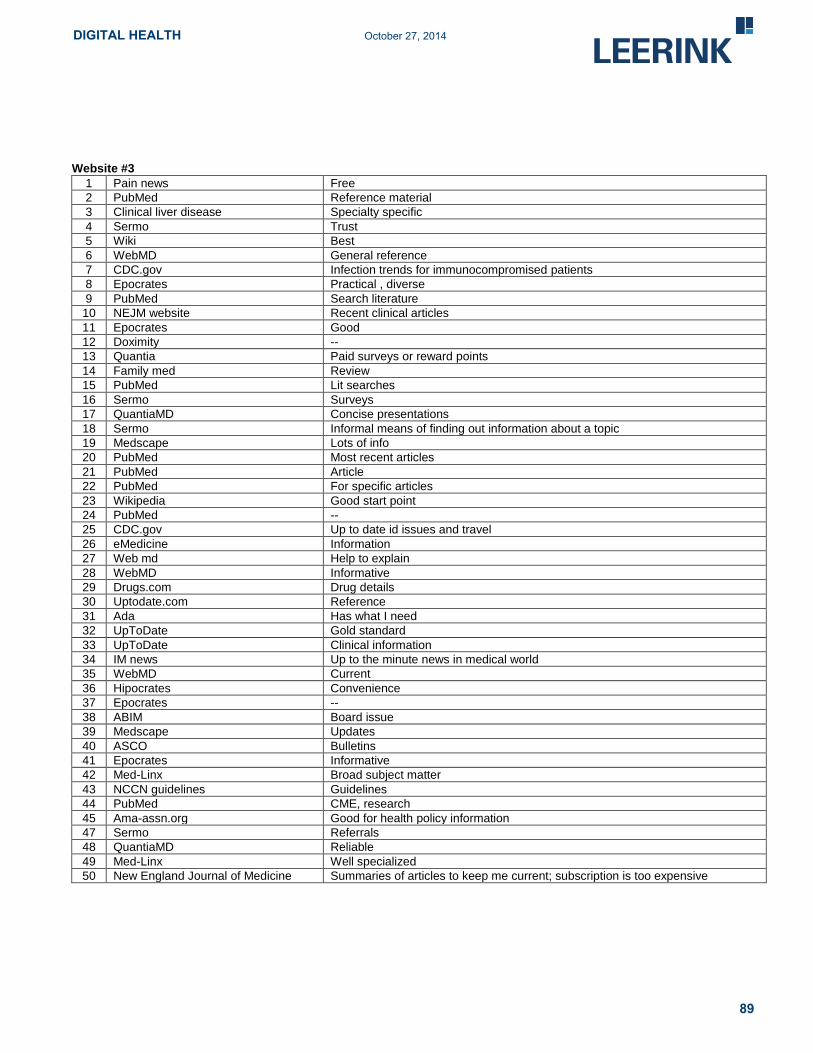

NEJM and Conferences Dominate Offline Knowledge Sources

Traditionally, the most trusted print journals in medicine are the New England Journal of Medicine and the Journal of

the American Medical Association. The overall responses from our physicians are in line with the known trust placed

in these two publications. We posed an open-ended question to the physicians worded as such: “What are your top

three preferred offline sources for new medical information?” Our aim with this question is twofold: 1) we believe that

the top three choices that come to mind do not necessarily have different qualities in the physicians’ opinions, which

means three answers more accurately captures information on what sources are most widely used; and 2) for the

most used sources, we wanted to know why they are so heavily utilized among physicians. Medical Conferences and

NEJM heavily dominate, at 19% and 14% respectively overall, and at 34% and 27% respectively, as the physicians’

first choice. For NEJM, many respondents mention that they use it due to “trust” and because it is “up to date,” while

for conferences, the physicians preferred them for “CME,” “in person meetings,” and “new research.”

22

DIGITAL HEALTH October 27, 2014

If we do take into consideration differences between the top three choices, the importance of medical conferences

stands out. We also notice that JAMA was almost never picked as a first choice, but was picked as a second choice

more than any other source. JAMA was described in much the same manner as NEJM, which leads us to believe that

it is generally trusted as a journal, but is not the de facto top source. Despite some heavy contrast of preferences

among age groups, the staple journals are used almost universally, which leads us to conclude that despite the shift

towards digital content, print media will yet hold a place for physicians to obtain new information.

Note: Other Journals include: The Lancet, JCEM, Internal Medicine Journal, etc. Other includes non-journal publications.

Source: MEDACorp Survey: Digital Health, August 2014

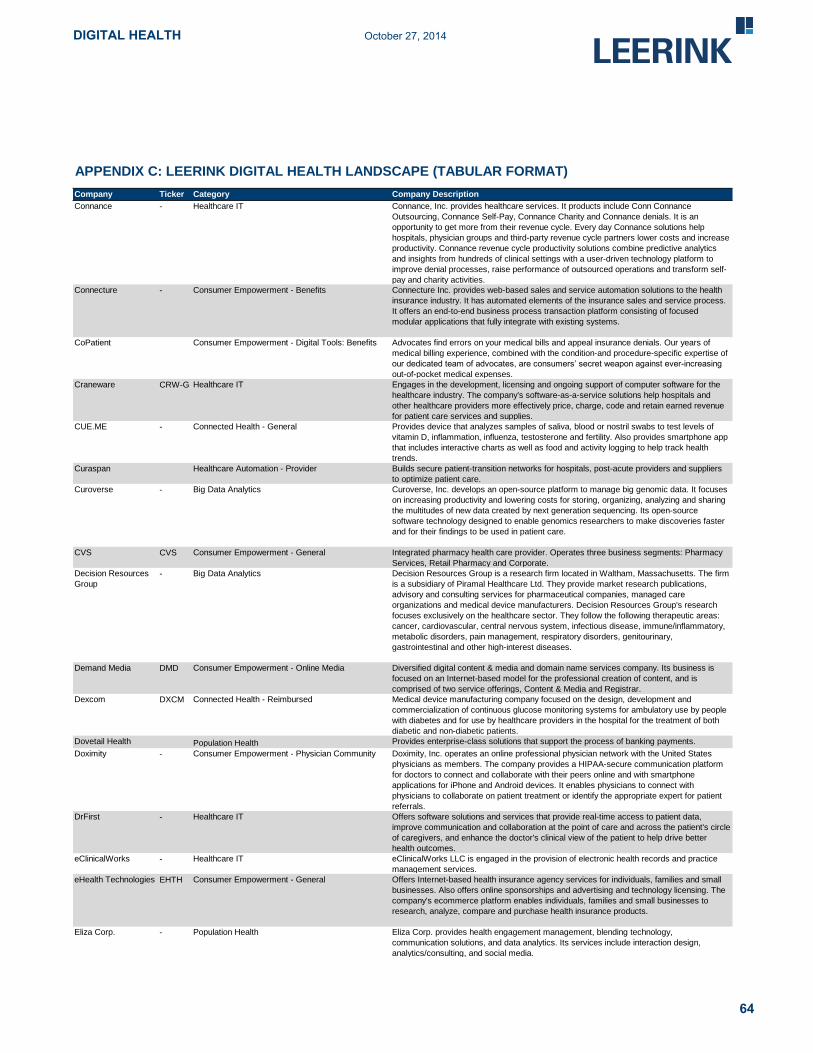

gastrointestinal and other high-interest diseases.

Demand Media DMD Consumer Empowerment - Online Media Diversified digital content & media and domain name services company. Its business is

focused on an Internet-based model for the professional creation of content, and is

comprised of two service offerings, Content & Media and Registrar.

Dexcom DXCM Connected Health - Reimbursed Medical device manufacturing company focused on the design, development and

commercialization of continuous glucose monitoring systems for ambulatory use by people

with diabetes and for use by healthcare providers in the hospital for the treatment of both

diabetic and non-diabetic patients.

Dovetail Health Population Health Provides enterprise-class solutions that support the process of banking payments.

Doximity - Consumer Empowerment - Physician Community Doximity, Inc. operates an online professional physician network with the United States

physicians as members. The company provides a HIPAA-secure communication platform

for doctors to connect and collaborate with their peers online and with smartphone

applications for iPhone and Android devices. It enables physicians to connect with

physicians to collaborate on patient treatment or identify the appropriate expert for patient

referrals.

DrFirst - Healthcare IT Offers software solutions and services that provide real-time access to patient data,

improve communication and collaboration at the point of care and across the patient's circle

of caregivers, and enhance the doctor's clinical view of the patient to help drive better

health outcomes.

eClinicalWorks - Healthcare IT eClinicalWorks LLC is engaged in the provision of electronic health records and practice

management services.

eHealth Technologies EHTH Consumer Empowerment - General Offers Internet-based health insurance agency services for individuals, families and small

businesses. Also offers online sponsorships and advertising and technology licensing. The

company's ecommerce platform enables individuals, families and small businesses to

research, analyze, compare and purchase health insurance products.

Eliza Corp. - Population Health Eliza Corp. provides health engagement management, blending technology,

communication solutions, and data analytics. Its services include interaction design,

analytics/consulting, and social media.

64

DIGITAL HEALTH October 27, 2014

Company Ticker Category Company Description

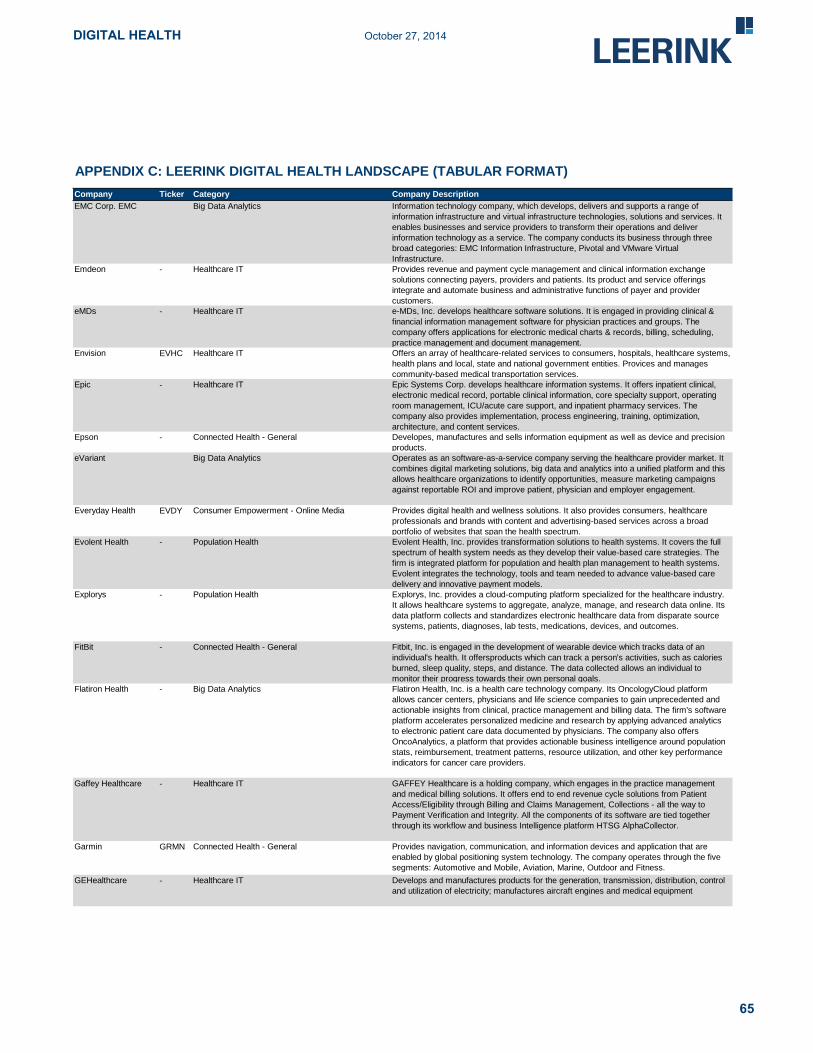

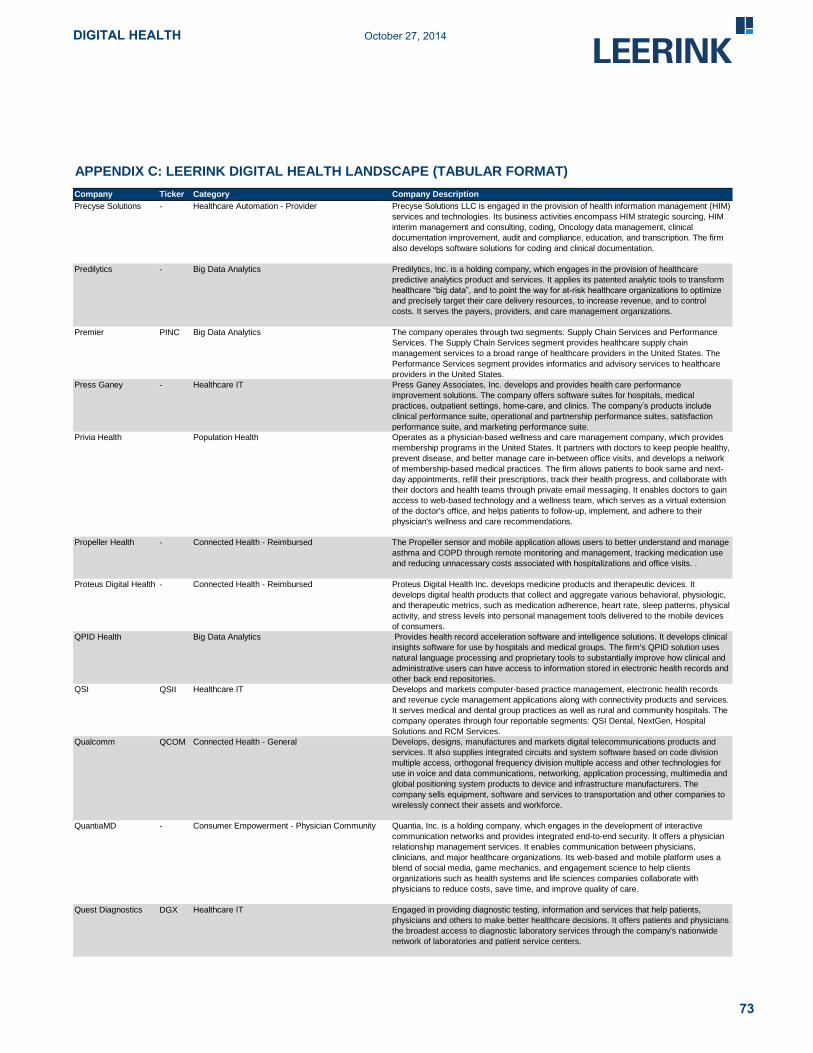

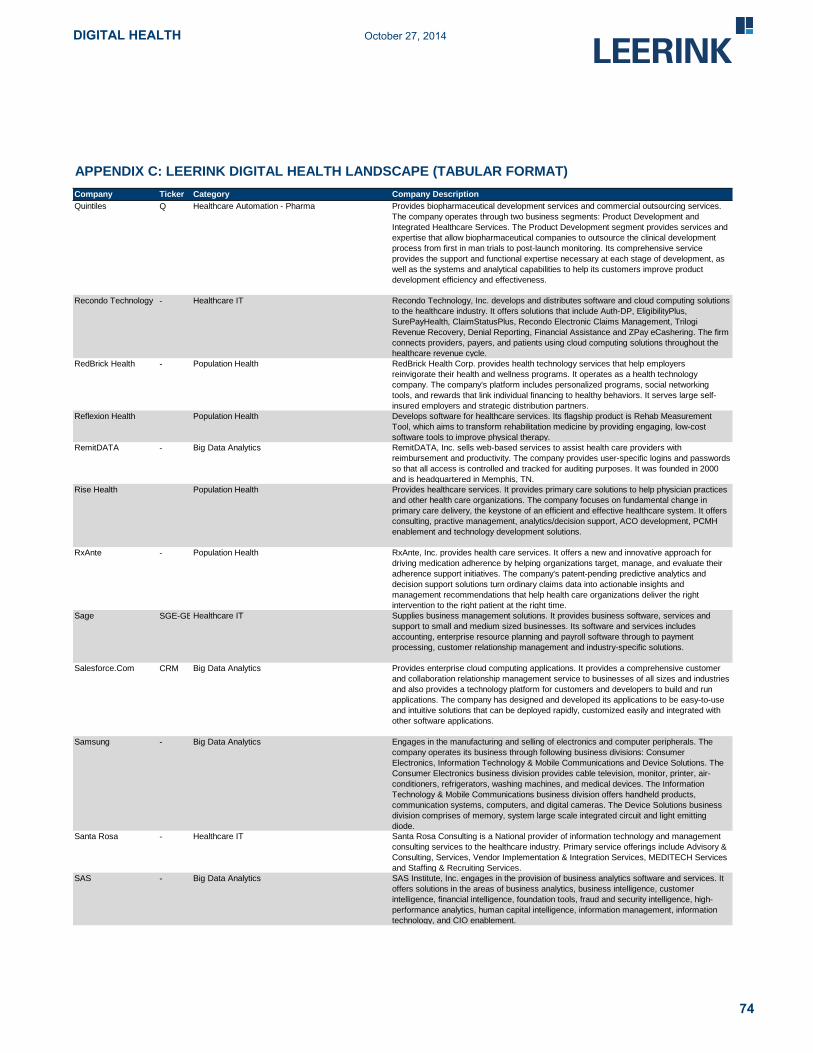

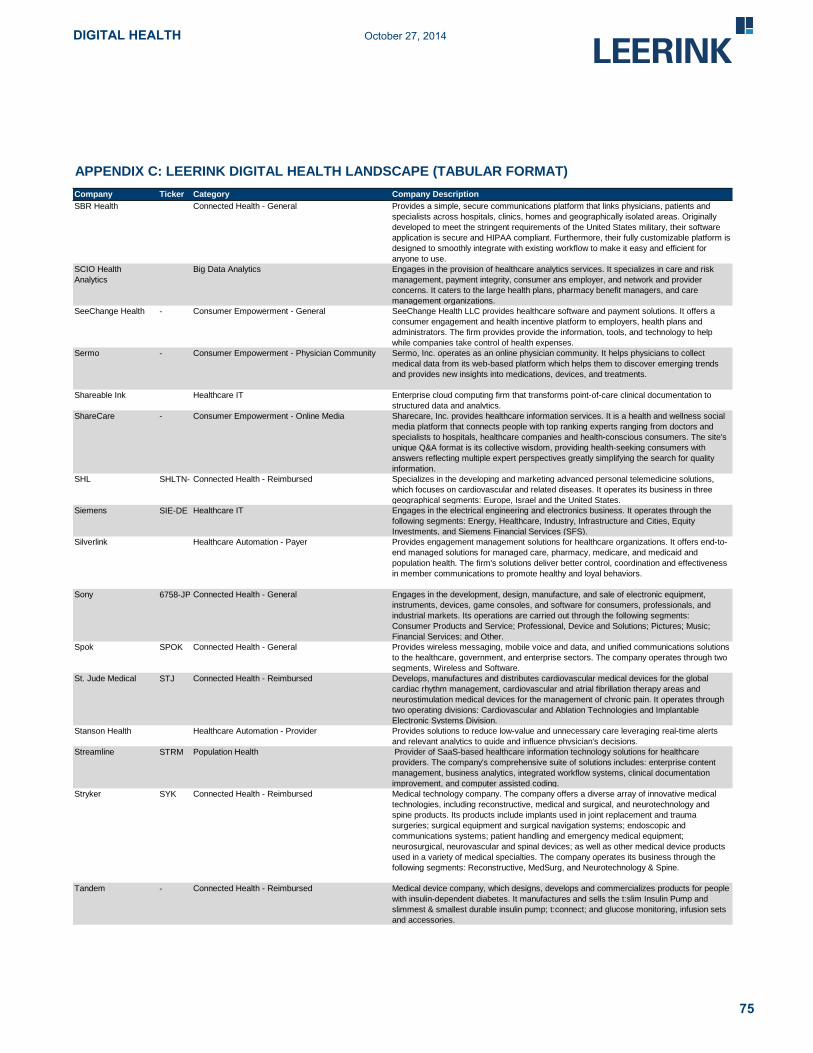

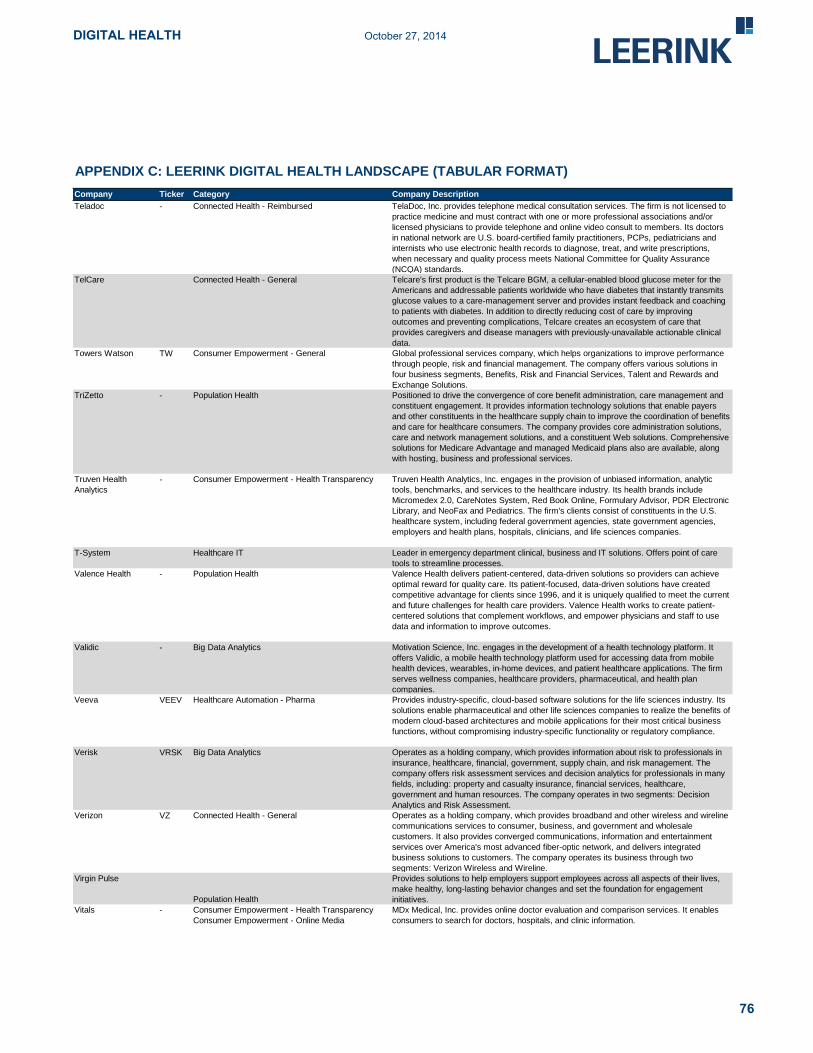

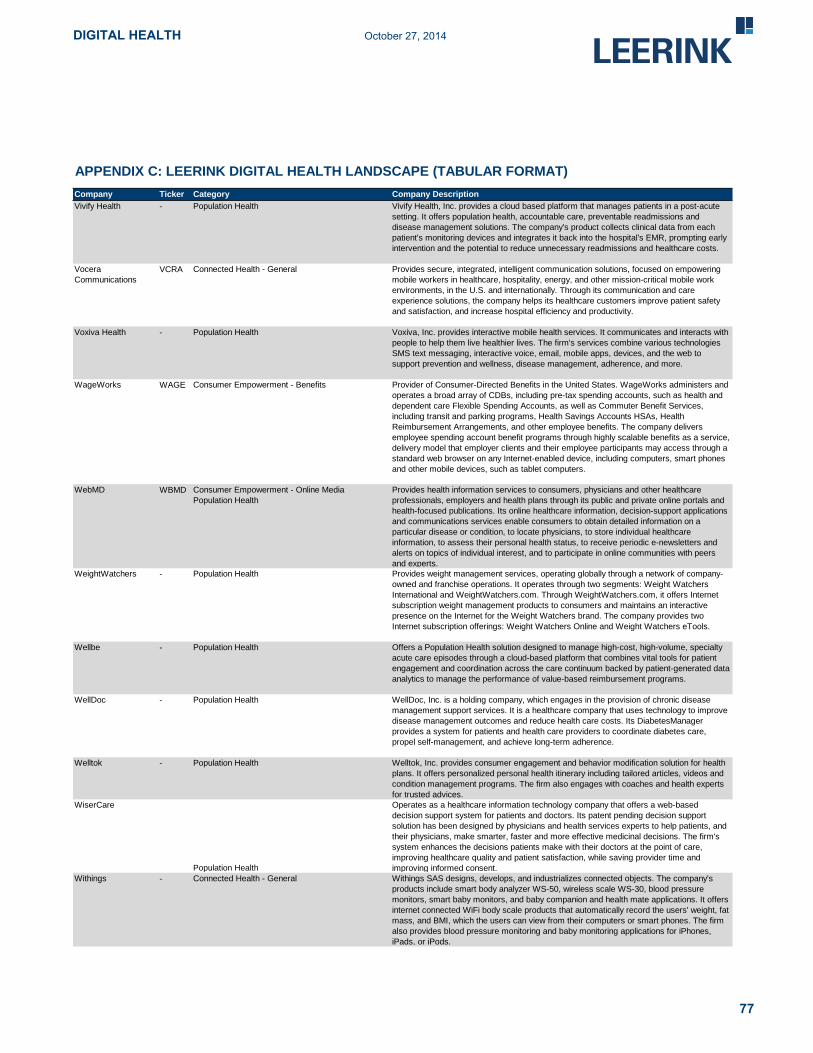

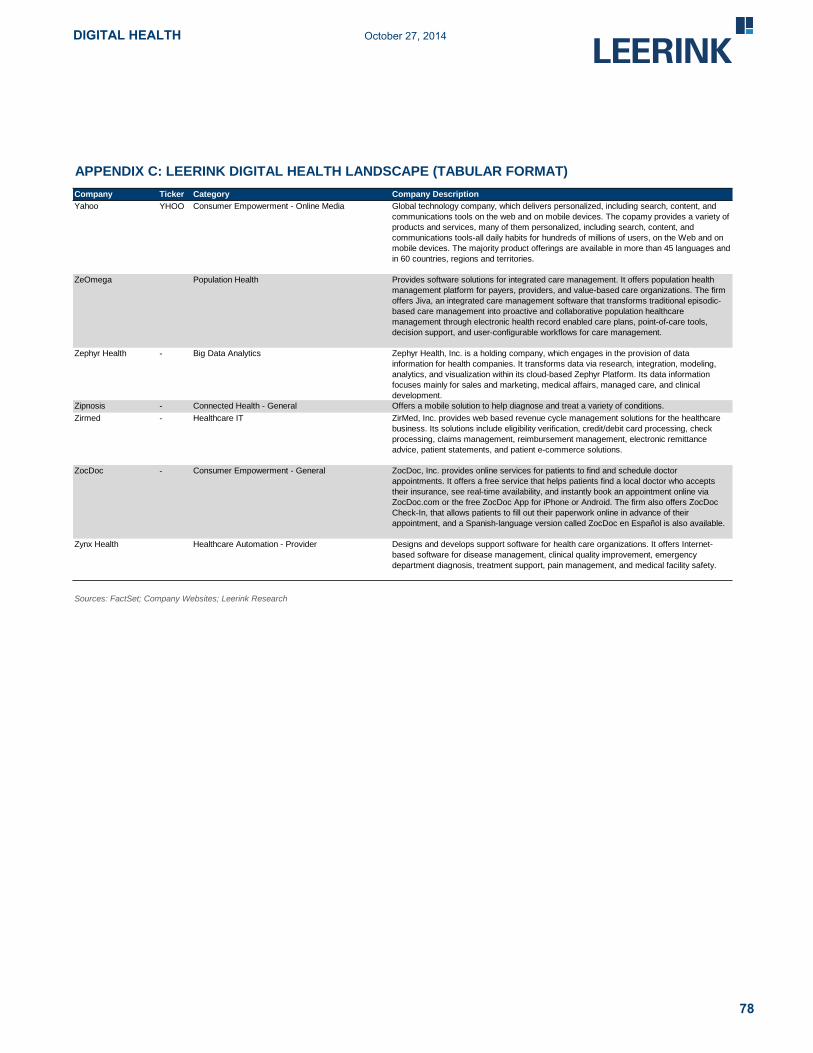

APPENDIX C: LEERINK DIGITAL HEALTH LANDSCAPE (TABULAR FORMAT)

EMC Corp. EMC Big Data Analytics Information technology company, which develops, delivers and supports a range of

information infrastructure and virtual infrastructure technologies, solutions and services. It

enables businesses and service providers to transform their operations and deliver

information technology as a service. The company conducts its business through three

broad categories: EMC Information Infrastructure, Pivotal and VMware Virtual

Infrastructure.

Emdeon - Healthcare IT Provides revenue and payment cycle management and clinical information exchange

solutions connecting payers, providers and patients. Its product and service offerings

integrate and automate business and administrative functions of payer and provider

customers.

eMDs - Healthcare IT e-MDs, Inc. develops healthcare software solutions. It is engaged in providing clinical &

financial information management software for physician practices and groups. The

company offers applications for electronic medical charts & records, billing, scheduling,

practice management and document management.

Envision EVHC Healthcare IT Offers an array of healthcare-related services to consumers, hospitals, healthcare systems,

health plans and local, state and national government entities. Provices and manages

community-based medical transportation services.

Epic - Healthcare IT Epic Systems Corp. develops healthcare information systems. It offers inpatient clinical,

electronic medical record, portable clinical information, core specialty support, operating

room management, ICU/acute care support, and inpatient pharmacy services. The

company also provides implementation, process engineering, training, optimization,

architecture, and content services.

Epson - Connected Health - General Developes, manufactures and sells information equipment as well as device and precision

products.

eVariant Big Data Analytics Operates as an software-as-a-service company serving the healthcare provider market. It

combines digital marketing solutions, big data and analytics into a unified platform and this

allows healthcare organizations to identify opportunities, measure marketing campaigns

against reportable ROI and improve patient, physician and employer engagement.

Everyday Health EVDY Consumer Empowerment - Online Media Provides digital health and wellness solutions. It also provides consumers, healthcare

professionals and brands with content and advertising-based services across a broad

portfolio of websites that span the health spectrum.

Evolent Health - Population Health Evolent Health, Inc. provides transformation solutions to health systems. It covers the full

spectrum of health system needs as they develop their value-based care strategies. The

firm is integrated platform for population and health plan management to health systems.

Evolent integrates the technology, tools and team needed to advance value-based care

delivery and innovative payment models.

Explorys - Population Health Explorys, Inc. provides a cloud-computing platform specialized for the healthcare industry.

It allows healthcare systems to aggregate, analyze, manage, and research data online. Its

data platform collects and standardizes electronic healthcare data from disparate source

systems, patients, diagnoses, lab tests, medications, devices, and outcomes.

FitBit - Connected Health - General Fitbit, Inc. is engaged in the development of wearable device which tracks data of an

individual's health. It offersproducts which can track a person's activities, such as calories

burned, sleep quality, steps, and distance. The data collected allows an individual to

monitor their progress towards their own personal goals.

Flatiron Health - Big Data Analytics Flatiron Health, Inc. is a health care technology company. Its OncologyCloud platform

allows cancer centers, physicians and life science companies to gain unprecedented and

actionable insights from clinical, practice management and billing data. The firm's software

platform accelerates personalized medicine and research by applying advanced analytics

to electronic patient care data documented by physicians. The company also offers

OncoAnalytics, a platform that provides actionable business intelligence around population

stats, reimbursement, treatment patterns, resource utilization, and other key performance

indicators for cancer care providers.

Gaffey Healthcare - Healthcare IT GAFFEY Healthcare is a holding company, which engages in the practice management

and medical billing solutions. It offers end to end revenue cycle solutions from Patient

Access/Eligibility through Billing and Claims Management, Collections - all the way to

Payment Verification and Integrity. All the components of its software are tied together

through its workflow and business Intelligence platform HTSG AlphaCollector.

Garmin GRMN Connected Health - General Provides navigation, communication, and information devices and application that are

enabled by global positioning system technology. The company operates through the five

segments: Automotive and Mobile, Aviation, Marine, Outdoor and Fitness.

GEHealthcare - Healthcare IT Develops and manufactures products for the generation, transmission, distribution, control

and utilization of electricity; manufactures aircraft engines and medical equipment

65

DIGITAL HEALTH October 27, 2014

Company Ticker Category Company Description

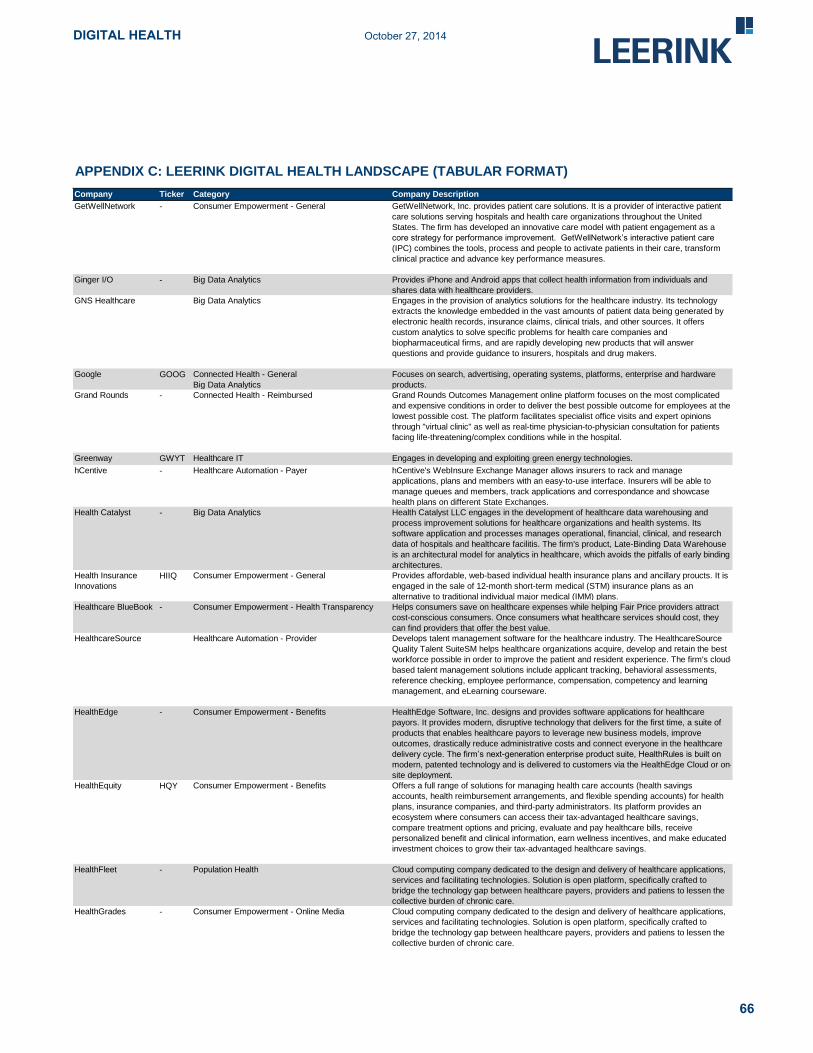

APPENDIX C: LEERINK DIGITAL HEALTH LANDSCAPE (TABULAR FORMAT)

GetWellNetwork - Consumer Empowerment - General GetWellNetwork, Inc. provides patient care solutions. It is a provider of interactive patient

care solutions serving hospitals and health care organizations throughout the United

States. The firm has developed an innovative care model with patient engagement as a

core strategy for performance improvement. GetWellNetwork’s interactive patient care

(IPC) combines the tools, process and people to activate patients in their care, transform

clinical practice and advance key performance measures.

Ginger I/O - Big Data Analytics Provides iPhone and Android apps that collect health information from individuals and

shares data with healthcare providers.

GNS Healthcare Big Data Analytics Engages in the provision of analytics solutions for the healthcare industry. Its technology

extracts the knowledge embedded in the vast amounts of patient data being generated by

electronic health records, insurance claims, clinical trials, and other sources. It offers

custom analytics to solve specific problems for health care companies and

biopharmaceutical firms, and are rapidly developing new products that will answer

questions and provide guidance to insurers, hospitals and drug makers.

Google GOOG Connected Health - General

Big Data Analytics

Focuses on search, advertising, operating systems, platforms, enterprise and hardware

products.

Grand Rounds - Connected Health - Reimbursed Grand Rounds Outcomes Management online platform focuses on the most complicated

and expensive conditions in order to deliver the best possible outcome for employees at the

lowest possible cost. The platform facilitates specialist office visits and expert opinions

through "virtual clinic" as well as real-time physician-to-physician consultation for patients

facing life-threatening/complex conditions while in the hospital.

Greenway GWYT Healthcare IT Engages in developing and exploiting green energy technologies.

hCentive - Healthcare Automation - Payer hCentive's WebInsure Exchange Manager allows insurers to rack and manage

applications, plans and members with an easy-to-use interface. Insurers will be able to

manage queues and members, track applications and correspondance and showcase

health plans on different State Exchanges.

Health Catalyst - Big Data Analytics Health Catalyst LLC engages in the development of healthcare data warehousing and

process improvement solutions for healthcare organizations and health systems. Its

software application and processes manages operational, financial, clinical, and research

data of hospitals and healthcare facilitis. The firm's product, Late-Binding Data Warehouse

is an architectural model for analytics in healthcare, which avoids the pitfalls of early binding

architectures.

Health Insurance

Innovations

HIIQ Consumer Empowerment - General Provides affordable, web-based individual health insurance plans and ancillary proucts. It is

engaged in the sale of 12-month short-term medical (STM) insurance plans as an

alternative to traditional individual major medical (IMM) plans.

Healthcare BlueBook - Consumer Empowerment - Health Transparency Helps consumers save on healthcare expenses while helping Fair Price providers attract

cost-conscious consumers. Once consumers what healthcare services should cost, they

can find providers that offer the best value.

HealthcareSource Healthcare Automation - Provider Develops talent management software for the healthcare industry. The HealthcareSource

Quality Talent SuiteSM helps healthcare organizations acquire, develop and retain the best

workforce possible in order to improve the patient and resident experience. The firm's cloud-

based talent management solutions include applicant tracking, behavioral assessments,

reference checking, employee performance, compensation, competency and learning

management, and eLearning courseware.

HealthEdge - Consumer Empowerment - Benefits HealthEdge Software, Inc. designs and provides software applications for healthcare

payors. It provides modern, disruptive technology that delivers for the first time, a suite of

products that enables healthcare payors to leverage new business models, improve

outcomes, drastically reduce administrative costs and connect everyone in the healthcare

delivery cycle. The firm’s next-generation enterprise product suite, HealthRules is built on

modern, patented technology and is delivered to customers via the HealthEdge Cloud or on-

site deployment.

HealthEquity HQY Consumer Empowerment - Benefits Offers a full range of solutions for managing health care accounts (health savings

accounts, health reimbursement arrangements, and flexible spending accounts) for health

plans, insurance companies, and third-party administrators. Its platform provides an

ecosystem where consumers can access their tax-advantaged healthcare savings,

compare treatment options and pricing, evaluate and pay healthcare bills, receive

personalized benefit and clinical information, earn wellness incentives, and make educated

investment choices to grow their tax-advantaged healthcare savings.

HealthFleet - Population Health Cloud computing company dedicated to the design and delivery of healthcare applications,

services and facilitating technologies. Solution is open platform, specifically crafted to

bridge the technology gap between healthcare payers, providers and patiens to lessen the

collective burden of chronic care.

HealthGrades - Consumer Empowerment - Online Media Cloud computing company dedicated to the design and delivery of healthcare applications,

services and facilitating technologies. Solution is open platform, specifically crafted to

bridge the technology gap between healthcare payers, providers and patiens to lessen the

collective burden of chronic care.

66

DIGITAL HEALTH October 27, 2014

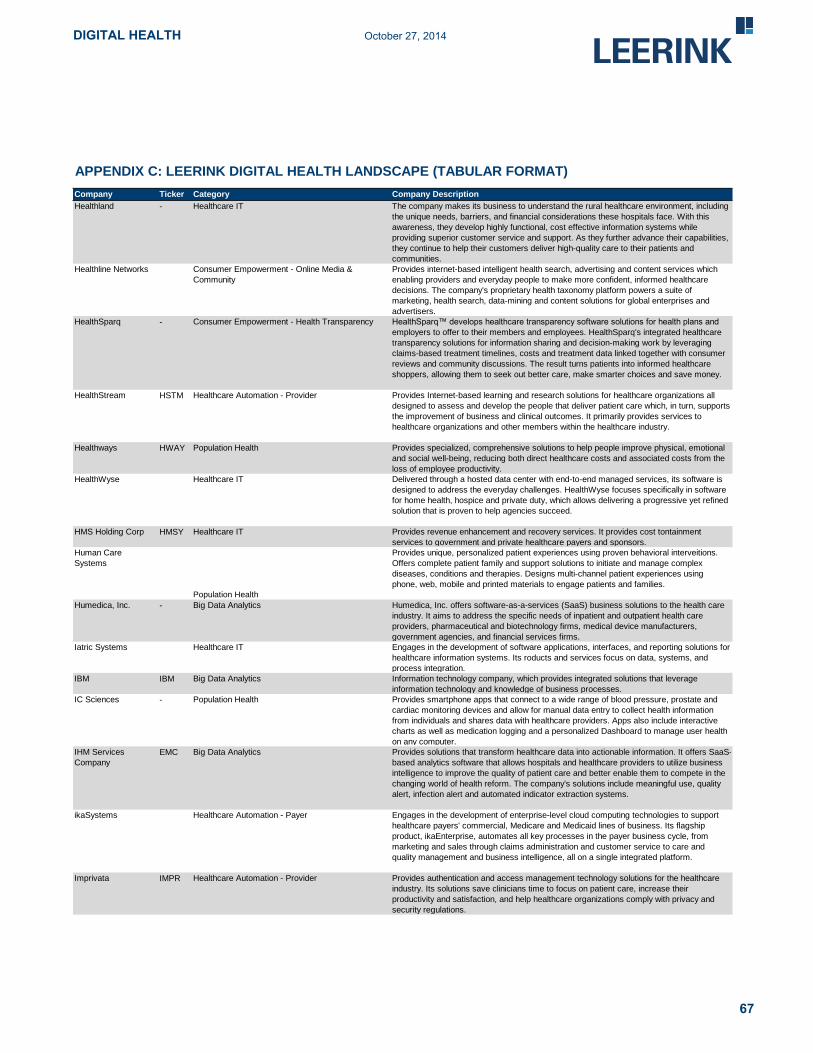

Company Ticker Category Company Description

APPENDIX C: LEERINK DIGITAL HEALTH LANDSCAPE (TABULAR FORMAT)

Healthland - Healthcare IT The company makes its business to understand the rural healthcare environment, including

the unique needs, barriers, and financial considerations these hospitals face. With this

awareness, they develop highly functional, cost effective information systems while

providing superior customer service and support. As they further advance their capabilities,

they continue to help their customers deliver high-quality care to their patients and

communities.

Healthline Networks Consumer Empowerment - Online Media &

Community

Provides internet-based intelligent health search, advertising and content services which

enabling providers and everyday people to make more confident, informed healthcare

decisions. The company's proprietary health taxonomy platform powers a suite of

marketing, health search, data-mining and content solutions for global enterprises and

advertisers.

HealthSparq - Consumer Empowerment - Health Transparency HealthSparq™ develops healthcare transparency software solutions for health plans and

employers to offer to their members and employees. HealthSparq's integrated healthcare

transparency solutions for information sharing and decision-making work by leveraging

claims-based treatment timelines, costs and treatment data linked together with consumer

reviews and community discussions. The result turns patients into informed healthcare

shoppers, allowing them to seek out better care, make smarter choices and save money.

HealthStream HSTM Healthcare Automation - Provider Provides Internet-based learning and research solutions for healthcare organizations all

designed to assess and develop the people that deliver patient care which, in turn, supports

the improvement of business and clinical outcomes. It primarily provides services to

healthcare organizations and other members within the healthcare industry.

Healthways HWAY Population Health Provides specialized, comprehensive solutions to help people improve physical, emotional

and social well-being, reducing both direct healthcare costs and associated costs from the

loss of employee productivity.

HealthWyse Healthcare IT Delivered through a hosted data center with end-to-end managed services, its software is

designed to address the everyday challenges. HealthWyse focuses specifically in software

for home health, hospice and private duty, which allows delivering a progressive yet refined

solution that is proven to help agencies succeed.

HMS Holding Corp HMSY Healthcare IT Provides revenue enhancement and recovery services. It provides cost tontainment

services to government and private healthcare payers and sponsors.

Human Care

Systems

Population Health

Provides unique, personalized patient experiences using proven behavioral interveitions.

Offers complete patient family and support solutions to initiate and manage complex

diseases, conditions and therapies. Designs multi-channel patient experiences using

phone, web, mobile and printed materials to engage patients and families.

Humedica, Inc. - Big Data Analytics Humedica, Inc. offers software-as-a-services (SaaS) business solutions to the health care

industry. It aims to address the specific needs of inpatient and outpatient health care

providers, pharmaceutical and biotechnology firms, medical device manufacturers,

government agencies, and financial services firms.

Iatric Systems Healthcare IT Engages in the development of software applications, interfaces, and reporting solutions for

healthcare information systems. Its roducts and services focus on data, systems, and

process integration.

IBM IBM Big Data Analytics Information technology company, which provides integrated solutions that leverage

information technology and knowledge of business processes.

IC Sciences - Population Health Provides smartphone apps that connect to a wide range of blood pressure, prostate and

cardiac monitoring devices and allow for manual data entry to collect health information

from individuals and shares data with healthcare providers. Apps also include interactive

charts as well as medication logging and a personalized Dashboard to manage user health

on any computer.

IHM Services

Company

EMC Big Data Analytics Provides solutions that transform healthcare data into actionable information. It offers SaaS-

based analytics software that allows hospitals and healthcare providers to utilize business

intelligence to improve the quality of patient care and better enable them to compete in the

changing world of health reform. The company's solutions include meaningful use, quality

alert, infection alert and automated indicator extraction systems.

ikaSystems Healthcare Automation - Payer Engages in the development of enterprise-level cloud computing technologies to support

healthcare payers' commercial, Medicare and Medicaid lines of business. Its flagship

product, ikaEnterprise, automates all key processes in the payer business cycle, from

marketing and sales through claims administration and customer service to care and

quality management and business intelligence, all on a single integrated platform.

Imprivata IMPR Healthcare Automation - Provider Provides authentication and access management technology solutions for the healthcare

industry. Its solutions save clinicians time to focus on patient care, increase their

productivity and satisfaction, and help healthcare organizations comply with privacy and

security regulations.

67

DIGITAL HEALTH October 27, 2014

Company Ticker Category Company Description

APPENDIX C: LEERINK DIGITAL HEALTH LANDSCAPE (TABULAR FORMAT)

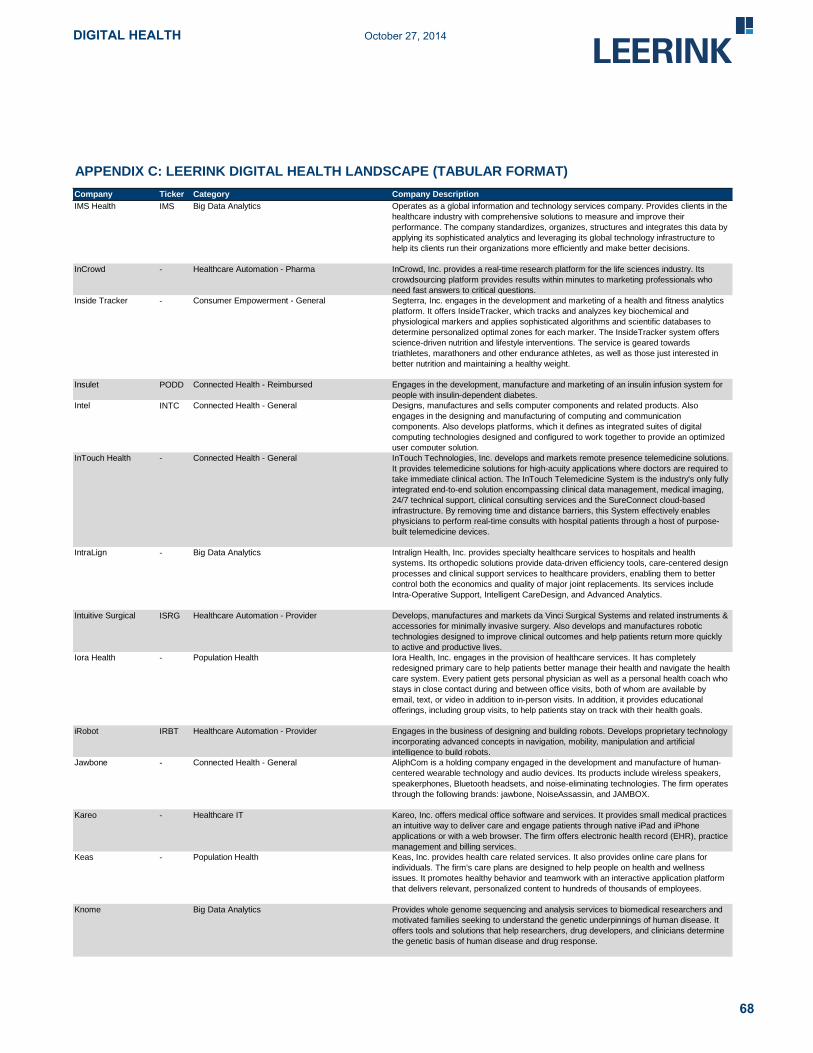

IMS Health IMS Big Data Analytics Operates as a global information and technology services company. Provides clients in the

healthcare industry with comprehensive solutions to measure and improve their

performance. The company standardizes, organizes, structures and integrates this data by

applying its sophisticated analytics and leveraging its global technology infrastructure to

help its clients run their organizations more efficiently and make better decisions.

InCrowd - Healthcare Automation - Pharma InCrowd, Inc. provides a real-time research platform for the life sciences industry. Its

crowdsourcing platform provides results within minutes to marketing professionals who

need fast answers to critical questions.

Inside Tracker - Consumer Empowerment - General Segterra, Inc. engages in the development and marketing of a health and fitness analytics

platform. It offers InsideTracker, which tracks and analyzes key biochemical and

physiological markers and applies sophisticated algorithms and scientific databases to

determine personalized optimal zones for each marker. The InsideTracker system offers

science-driven nutrition and lifestyle interventions. The service is geared towards

triathletes, marathoners and other endurance athletes, as well as those just interested in

better nutrition and maintaining a healthy weight.

Insulet PODD Connected Health - Reimbursed Engages in the development, manufacture and marketing of an insulin infusion system for

people with insulin-dependent diabetes.

Intel INTC Connected Health - General Designs, manufactures and sells computer components and related products. Also

engages in the designing and manufacturing of computing and communication

components. Also develops platforms, which it defines as integrated suites of digital

computing technologies designed and configured to work together to provide an optimized

user computer solution.

InTouch Health - Connected Health - General InTouch Technologies, Inc. develops and markets remote presence telemedicine solutions.

It provides telemedicine solutions for high-acuity applications where doctors are required to

take immediate clinical action. The InTouch Telemedicine System is the industry's only fully

integrated end-to-end solution encompassing clinical data management, medical imaging,

24/7 technical support, clinical consulting services and the SureConnect cloud-based

infrastructure. By removing time and distance barriers, this System effectively enables

physicians to perform real-time consults with hospital patients through a host of purpose-

built telemedicine devices.

IntraLign - Big Data Analytics Intralign Health, Inc. provides specialty healthcare services to hospitals and health

systems. Its orthopedic solutions provide data-driven efficiency tools, care-centered design

processes and clinical support services to healthcare providers, enabling them to better

control both the economics and quality of major joint replacements. Its services include

Intra-Operative Support, Intelligent CareDesign, and Advanced Analytics.

Intuitive Surgical ISRG Healthcare Automation - Provider Develops, manufactures and markets da Vinci Surgical Systems and related instruments &

accessories for minimally invasive surgery. Also develops and manufactures robotic