78

Warm-up to Session 5 On the blank balance sheet you have been given and using the case study in your participant notebooks, bring the fixed cost over from the capital start up budget.

Warm-up to Session 5

On the blank balance sheet you have been given and using the case study in your

participant notebooks, bring the fixed cost over from the capital start up budget.

Session 5: Financial Management

Review Take Home

■ Develop your Enterprise Budgets

■ In AG PLAN

■ Products

■ Services

■ Production systems

■ Customers

Review of Field Day

Refer to the notes you took during the field trip:■ What decision-making processes did the

farmer use that you would use?■ How will you decide on crops, pricing, and

size of enterprise?

[Guest Speaker Details]

Last Session Enterprise Budget

■ Develop enterprise budget■ Decide on Production System■ How did they decide on pricing■ Where will they market

■ Fixed cost

■ Revenue = Price X Quantity

Today’s Goals:

■ What records do you need to keep for good financial management?

■ What are the components of balance sheet, cash flow statement, and income statement?

■ Why do you track cash flow?■ How do you use financial statements?

Farm Goal

We would like our farm to make $35,000 net profit in 2013.

Farm GoalWe would like our farm to make $35,000 net profit in 2013.

■What information do we need to know?■ Gross sales

■ Amount vegetables or animals sold

■ Prices sold each sold

■ Inputs needed for production (Labor, Equipment, Fertilizer, Seed)

■ What machinery and equipment needed?

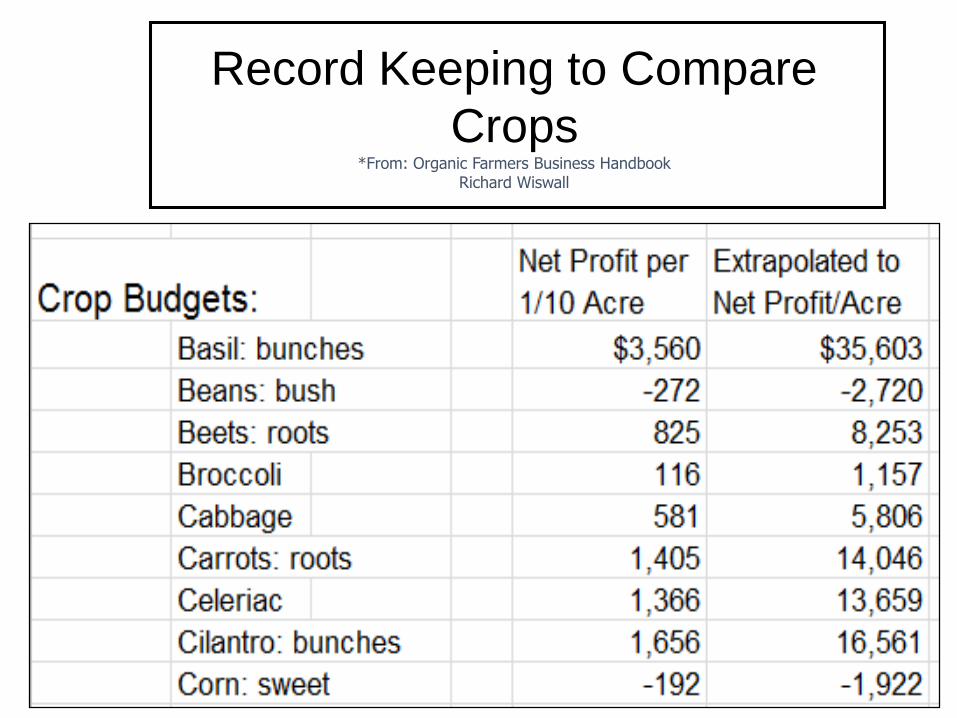

Record Keeping to Compare

Crops *From: Organic Farmers Business Handbook

Richard Wiswall

Record Keeping Allows You See Progress Toward Goals

Record Keeping Basics

■ Why do we keep records?

■ Who should keep your records?

■ Do you need an accountant?

■ What accounting software should you use?

■ When should you start?

Cash vs Accrual Accounting

■ Cash Accounting: Reporting of your revenues and expenses at the time they are actually received or paid

■ Accrual Accounting: The recognition of revenues and expenses at the time they are earned or incurred, regardless of when cash for transaction is received or paid out

Single and Double Entry Systems

■ Single entry system: Using only income and expenses accounts, as well as some of the other records listed on general records.

■ Double entry system: Every transaction is records as a debit and credit. A sale could be both a delivery and a receipt of payment

What will you use your records for?

■ For taxes■ For management

decisions■ What equipment you

need?■ When should you

buy machinery?■ Keeping up with

labor

■ Keeping up with feed costs

■ If you are borrowing money

Essential Records for Business

■ Business checkbook■ Record Book (receipts and

expenses record)■ Inventory reports■ Market sales

■ Production Records■ Labor records■ Depreciation schedule

■ Accounts payable■ Accounts receivable■ Family Living Expense

records■ Financial Statements

■ Balance sheet■ Income statements■ Cash Flow statements

Keep your records as simple as possible

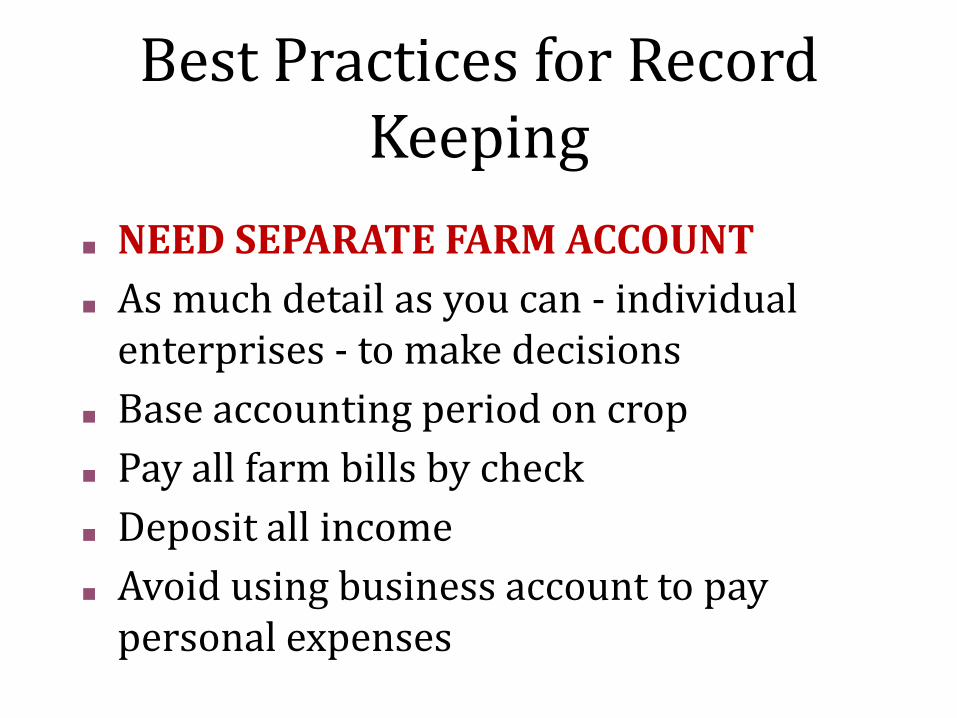

Best Practices for Record Keeping

■ NEED SEPARATE FARM ACCOUNT

■ As much detail as you can - individual enterprises - to make decisions

■ Base accounting period on crop

■ Pay all farm bills by check

■ Deposit all income

■ Avoid using business account to pay personal expenses

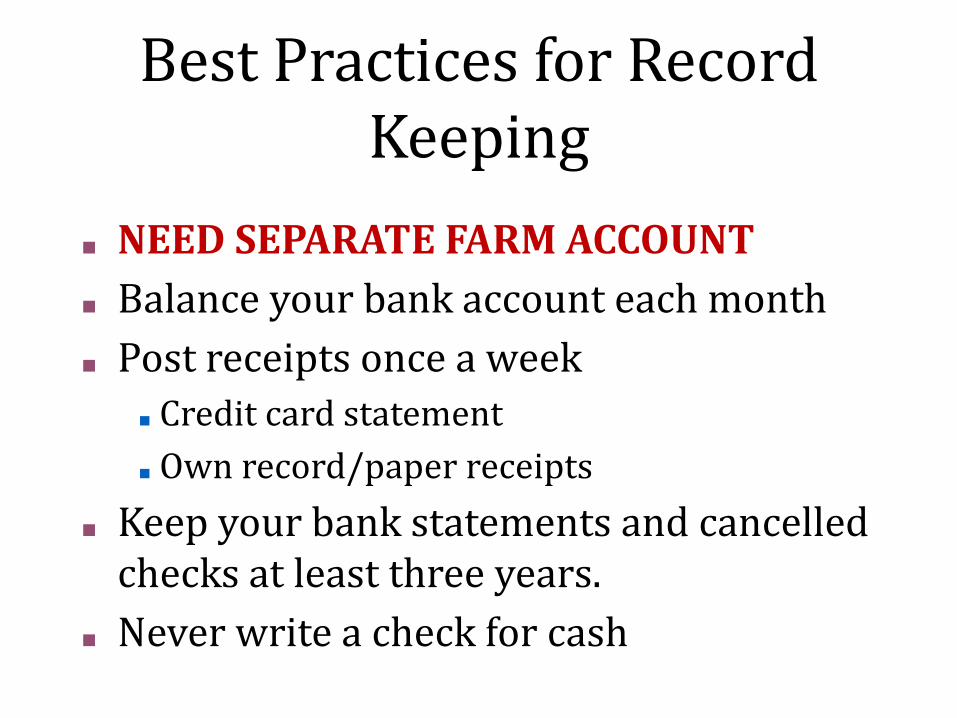

Best Practices for Record Keeping

■ NEED SEPARATE FARM ACCOUNT

■ Balance your bank account each month

■ Post receipts once a week

■ Credit card statement

■ Own record/paper receipts

■ Keep your bank statements and cancelled checks at least three years.

■ Never write a check for cash

From Session 3...

■ Resource Inventory

■ Assets

■ Machinery

■ Buildings

■ Livestock

■ Liabilities

■ List of loans

■ Why Inventory?

Think back to our previous sessions...

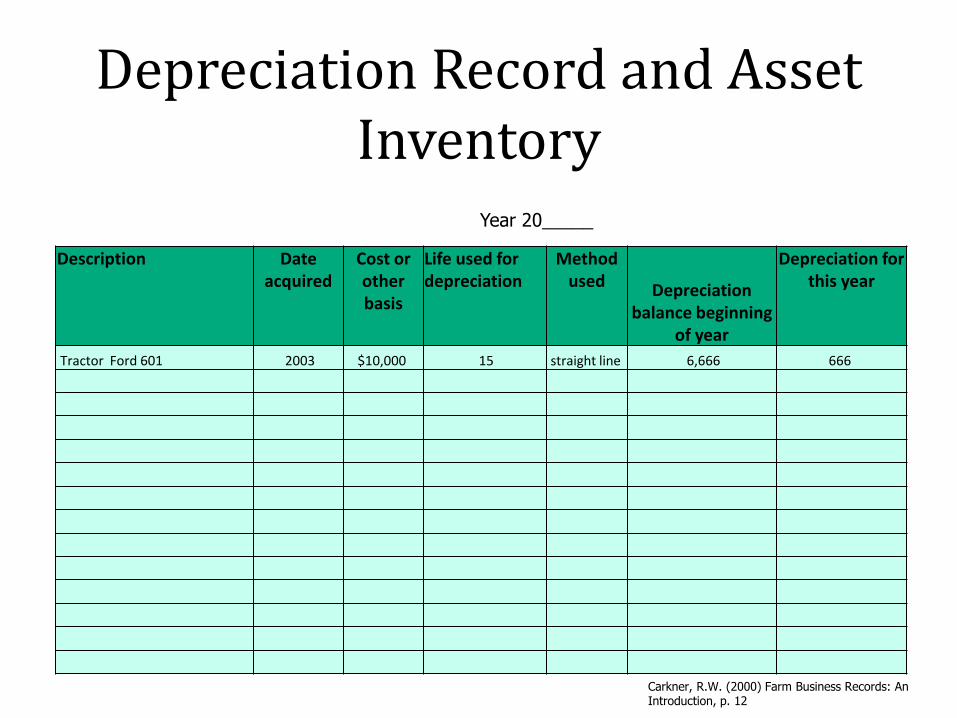

What is depreciation?

The using up of a capital asset (something that will last more than one year)

Land can never be depreciated

Depreciation Record and Asset Inventory

Description Date acquired

Cost or other basis

Life used for depreciation

Method used Depreciation

balance beginning of year

Depreciation for this year

Tractor Ford 601 2003 $10,000 15 straight line 6,666 666

Year 20_____

Carkner, R.W. (2000) Farm Business Records: An Introduction, p. 12

You need to track income...

And to do that, you need a map and standardized units

Production Units■ Field Map

■ Greenhouse sqft

■ For record keeping and analysis

■ Standardize bed size

■ Ex: 300 feet long raised bed and 5.5 ft wide.

■ How many beds per acre?

■ 1,650 sqft each bed

■ Divide area of acre (43,560 sqft) by bed area

■ 26.40 beds per acre

Tracking Income

■ How much of product harvested by crop

■ How much of product leaves farm

■ What is sales value

■ Detail…by crop or total, sales by market?

■ Farmers market beginning inventory and end of market

■ Compile all market outlets sales

Production Records

Harvest Records

Unit? lbs may need scale

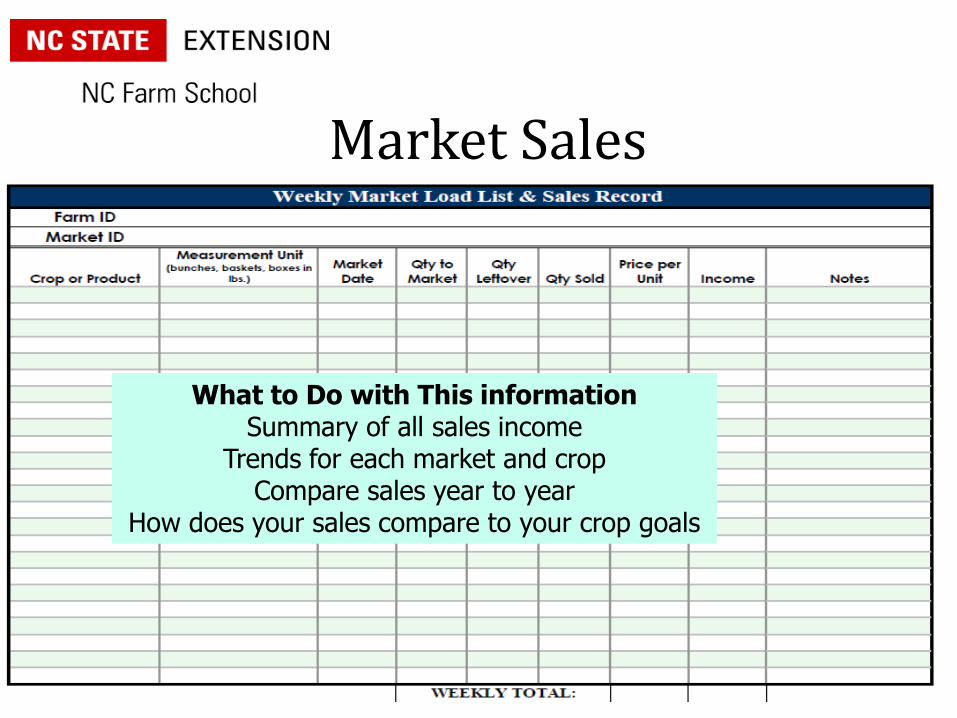

Market Sales

One sheet for each marketAdd up total sales for the year for each product

Add up total sales for each marketTotal quantity sold

CSA

Market Sales

What to Do with This informationSummary of all sales income

Trends for each market and cropCompare sales year to year

How does your sales compare to your crop goals

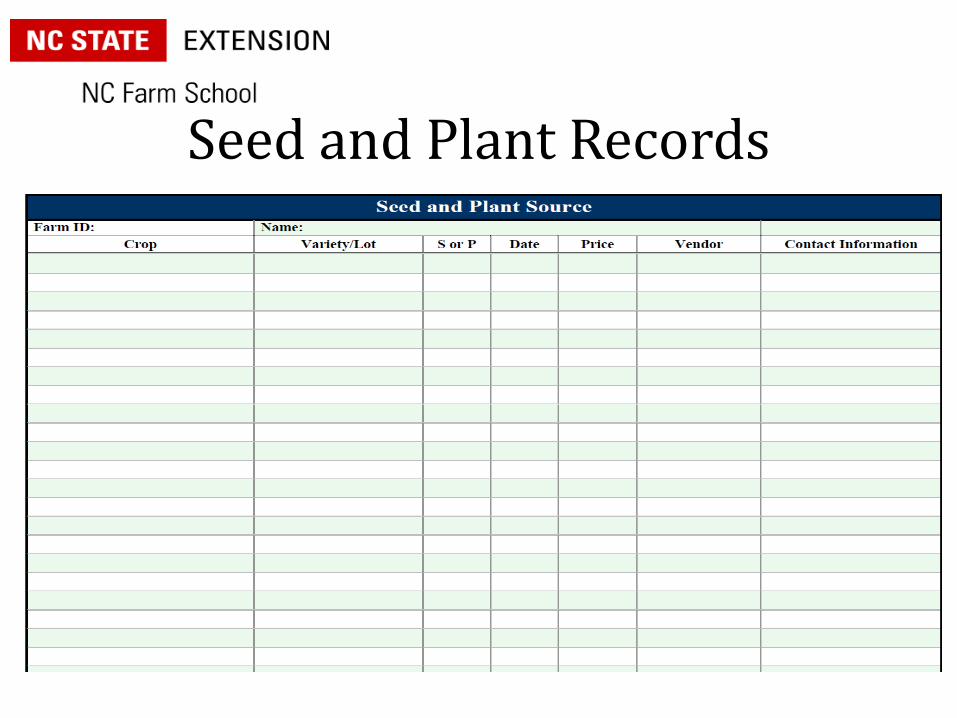

Seed and Plant Records

Tracking Expenses

Types of expenses

Deductible Expenses■ Deductible expenses are expenses that are

allowed by IRS when computing taxable income at end of your business tax year

■ Two categories

■ Fully deductible

■ Depreciable

Overhead Costs

Expense Description Cost

Mortgage annual

payment

Farm % of total, not house &

house portion

600

Depreciation to account for replacement 2000

Property taxes Farm % 800

Insurance Health & Fire 4000

Office Supplies 1100

Website Subscription & Fees 400

Expense Categories

• Fertilizer• Fuel & oil• Propane• Truck gas• Greenhouse supplies• Insurance• Interest

• Repairs & maintenance

• Seed & supplies• Taxes• Utilities• Rent paid

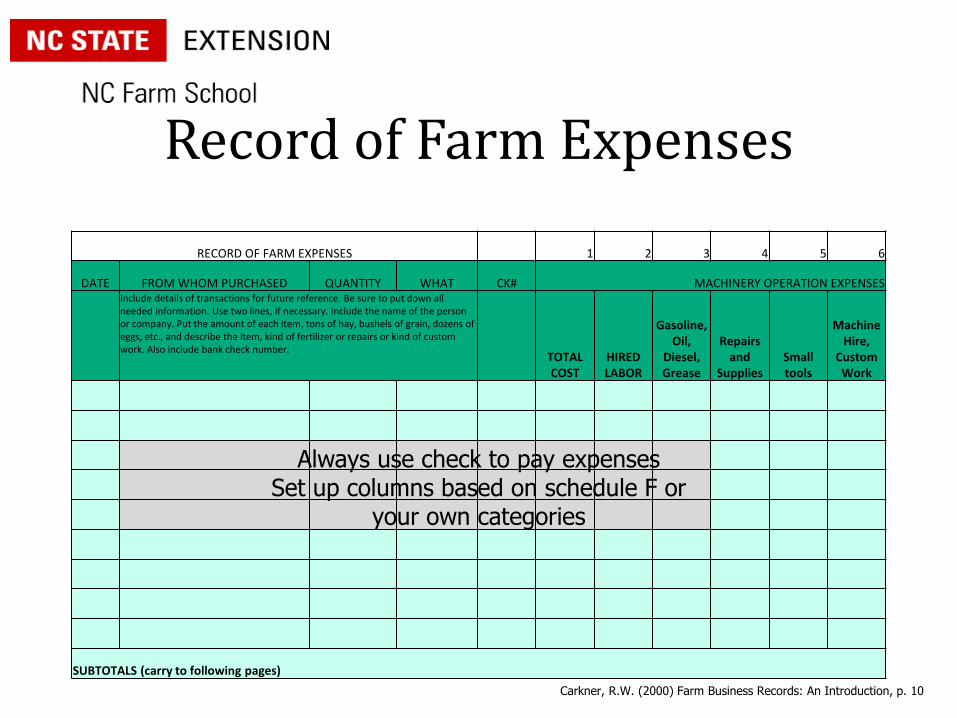

Record of Farm Expenses

RECORD OF FARM EXPENSES 1 2 3 4 5 6

DATE FROM WHOM PURCHASED QUANTITY WHAT CK# MACHINERY OPERATION EXPENSESInclude details of transactions for future reference. Be sure to put down all needed information. Use two lines, if necessary. Include the name of the person or company. Put the amount of each item, tons of hay, bushels of grain, dozens of eggs, etc., and describe the item, kind of fertilizer or repairs or kind of custom work. Also include bank check number.

TOTAL COST

HIRED LABOR

Gasoline, Oil,

Diesel, Grease

Repairs and

SuppliesSmall tools

Machine Hire,

Custom Work

SUBTOTALS (carry to following pages)

Carkner, R.W. (2000) Farm Business Records: An Introduction, p. 10

Always use check to pay expensesSet up columns based on schedule F or

your own categories

Expense Ledger

Some expense are more easily documented that otherOut of pocket expenses ( variable expenses)

Labor: hired and familyAllocating over head costs to crops

Tracking Labor

Best Practices for Tracking Labor

■ Set up a work order■ Estimate time per task

■ Occasionally have employee record

■ Track difference in employee work time per task

■ Track hours per employee

Independent Contractors

■ Independent contractors

■ not eligible for unemployment, disability or workers compensation benefits.

■ Do not need to pay employee taxes to independent contractors

Financial Management

Financial Management

■ Start up Costs

■ Balance Sheet

■ Income Statement

■ Cash Flow

■ Financial Statement Analysis

■ Breakeven Analysis

Balance Sheet

■ Defining the entity

■ Personal assets and liabilities included

■ Business only

■ Valuation methods

■ Market based

■ Book value

Balance Sheet■ A balance sheet shows the financial

position of a business as of a fixed date

■ It is a picture of what your business owns and owes at a particular given moment

■ Balance sheet example

Balance Sheet

Net Worth

Assets Liabilities

● Current○ Cash○ Savings○ Inventory○ Growing Crop

● Long Term○ Equipment○ Buildings○ Land

Beef Balance Sheet example

What happens when we add animals as assets? And when we add the liability for buying them?

LiquidityLiquidity is the availability of a business to generate enough cash to pay bills without disrupting the business.

Current Ratio = CA/CL

CA=current assets

CL= current liabilities

LiquidityNet capital ratio shows whether or not the total assets are adequate to cover total liabilities.

Net Capital Ratio = TA/TL

SolvencyDebt-equity ratio shows the relationship between owned and borrowed capital

Debt to Equity = TL/OE

TL = total liabilities

OE = owners equity

Ten Minute Break

In-Class Activity

In-Class ExerciseThe Thomas family started “New Farms” a year

ago. They have heard that you went through NC

Farm School and they asked you for help in

developing what their balance sheet should

look like for their “New Farms”. You asked them

to make a list of all the items that will need to

be included on the balance sheet.

Current Assets

Cash in Bank $ 30,000

Long-Term (Fixed and Intermediate) Assets

Farmland and Improvements (not including residence and three acres) Pasture: 20 acres @ $2,500 $ 50,000Timber: 20 acres @ $1,500 $ 30,000Barn, coop and well About 3 acres $ 8,000Used Machinery & Equipment $ 15,000

TOTAL FARM ASSETS $133,000

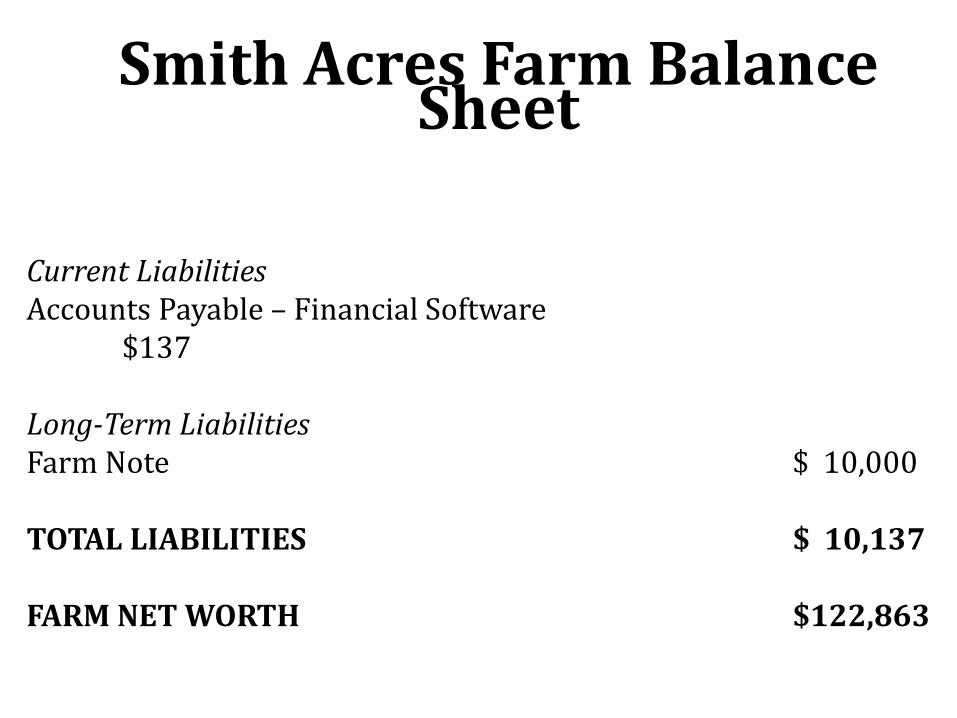

Smith Acres Farm Balance Sheet

Current LiabilitiesAccounts Payable – Financial Software

$137

Long-Term Liabilities Farm Note $ 10,000

TOTAL LIABILITIES $ 10,137

FARM NET WORTH $122,863

Smith Acres Farm Balance Sheet

Smith Balance Sheet

■ Working Capital (Current Assets – Current Liabilities)

$30,000 - $137 = $29,863

■ Current Ratio (Current Assets ÷ Current Liabilities)$30,000 ÷ $137 = 219

■ Debt-to-Equity Ratio (Total Liabilities ÷ Owner’s Equity)$10,000 ÷ $122,863 = 0.083

■ Equity-to-Asset Ratio (Owner’s Equity ÷ Total Assets) $122,863 ÷ $133,000 = 0.924

Income Statement

■ The income statement (profit and loss) shows where your money has come from and where it was spent over a specific period of time usually your tax year.

■ Revenue – Expenses = Net Income

Income Statement Case Study

INCOMECash income from Egg Sales

$625.00

Home value of eggs used (5 dozen @$2.50)12.50

Total income $632.50

Income Statement Case Study

EXPENSESFeed Purchased 1,750 lbs @$0.25

$437.50Plus: Feed on hand at beginning of month 50 lbs @ $0.25

+$ 12.50Less: Ending feed on Hand 300 lbs @ $0.25

-$ 75.00Total feed expense $375

Other production expenses (feed supplements, bedding, cartons) -$100Overhead Expense (utilities, promotion, depreciation)

-$ 15TOTAL EXPENSES $490.00NET FARM INCOME $142.50

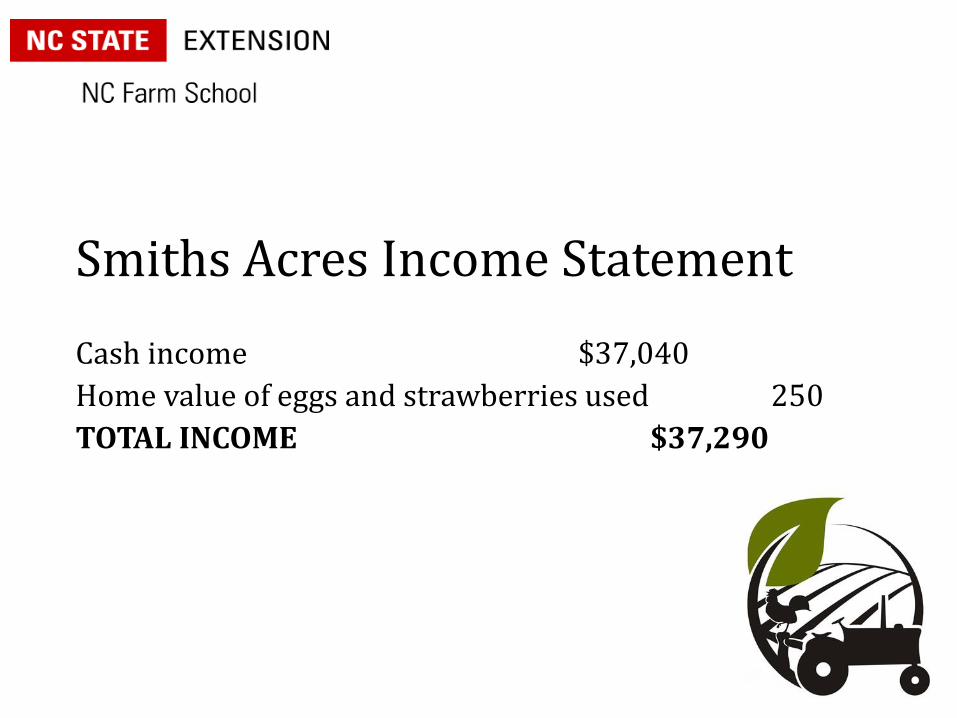

Smiths Acres Income Statement

Cash income $37,040

Home value of eggs and strawberries used 250

TOTAL INCOME $37,290

EXPENSES

Operating Expenses $21,421

Plus: Feed on hand at beginning of year 100 lbs @ $0.25 $ 25

Less: Ending feed on Hand 300 lbs @ $0.25 $ 75

Egg and strawberry cartons on Hand $ 125

Adjusted Operating Expense $21,226

Farm Interest Paid 1,000

Depreciation 4,180

TOTAL EXPENSES $ 26,406

Smiths Acres Income Statement

Smiths Acres Income Statement

NET FARM INCOME $ 10,884Value of Operator Labor $ 5,150

Financial Statement Analysis

Financial Statement Analysis■ Gross Profit Margin is the percentage of each

sales dollar remaining after a business has paid for its goods

■ Gross Profit Margin= Gross Profit / Sales

■ The normal rate depends on the business you are in

Financial Statement Analysis

■ Operating Profit Margin is operating profit margin ignoring taxes and interest.

■ Operating Profit Margin = Income from Operations / Sales

■ The higher the operating profit margin number the better

Financial Statement Analysis

■ Net Profit Margin is measure of success with respect to earnings on sales

■ Net Profit Margin = Net profit / Sales

■ The higher the net profit margin number the better

Financial Statement Analysis

■ Investment Measures

■ Return on Investment isNet Profit / Total Assets

Financial Statement Analysis

■ If the operating profit margin is low ■ Did you have enough mark up on your goods?

■ Are your operating expenses too high?

■ Are your interest expenses too high?

Smith Acres Farm: Sample Cash Flow Projection for Strawberries*

See Handout: Strawberry Cash Flow Statement

Cash Flow Statement

■ A third of businesses fail due to lack of cash flow

■ Historical cash flow similar to a check book

■ Pro Forma Cash Flow Statement – identifies when cash is expected to be received and when it must be spent to pay bills and debts

■ The cash flow statement deals only with actual cash transactions and not with depreciation and other non cash expense items.

Cash Flow and Income Statements

■ Income Statements include only income and deductible expense items

■ Cash Flow reflects all money flowing in and out of the business

Cash Flow and Income Statements

■ Example: Loan payments of $9,000 during the year, $3,000 of which is interest

■ Cash flow statement would include all $9,000

■ Income Statement would record only interest expense

Cash Flow and Income Statements■ Example: Purchase a vehicle for $15,000 cash

■ Cash flow statement would include full $15,000

■ Income Statement would record only projected depreciation for the year

Financial Statement Analysis

■ Financial Statements Analysis

■ Liquidity analysis

■ Profitability analysis

■ Measures of debit

■ Measures of investment

Financial Management

■ Develop your record keeping system

■ Spread sheets

■ Quick books

■ Hand ledgers

■ Financial Statements

How well did we meet today’s goals:

■ What records do you need to keep for good financial management?

■ What are the components of balance sheet, cash flow statement, and income statement?

■ Why do you track cash flow?■ How do you use financial statements?

Homework Explanation

In Ag Plan, develop a Balance Sheet & Cash Flow

Evaluation

Add your evaluation link HERE

Field Day

Take your worksheet for the field day with you to ensure you get the most from the experience!