Analysis of the Sanitation Supply Chain in Rural and Small Towns in Uganda Final Report from PATH to the World Bank’s Water and Sanitation Program June 2012 2201 Westlake Avenue Suite 200 Seattle, WA 98121 206.258.3500 P.O. Box 900922 Seattle, WA 98109 >>PROJECT REPORT

Transcript

Analysis of the

Sanitation Supply

Chain in Rural and

Small Towns in

Uganda

Final Report from PATH to the

World Bank’s Water and

Sanitation Program

June 2012

2201 Westlake Avenue

Suite 200

Seattle, WA 98121

206.258.3500

P.O. Box 900922

Seattle, WA 98109

>>PROJECT REPORT

ii

THE REPUBLIC OF UGANDA

Analysis of the Sanitation Supply Chain in Rural and Small

Towns in Uganda

This report was prepared with financial support from WSP and research by PATH

iii

Table of Contents Table of Contents ............................................................................................................................... ii

Acronyms ......................................................................................................................................... vi

Stakeholder MoH, Ministry of Water and Environment

3

The study aggregated data from these various activities to create a high-level review of the market

situation and potential in Uganda for the expansion of sanitation services. Furthermore, the study

analyzed the limitations and level of interconnectedness of the various supply chain elements to initiate

the process of identifying and addressing gaps in the system and suggest focus areas for future capacity

building and market-development efforts.

4.0 Study limitations as they pertain to the analysis It should be noted that this study was designed as a rapid, qualitative assessment of the market for

household sanitation in rural and small towns in Uganda. The study was not designed to be

representative of the entire country in terms of geography, population, sanitation solutions, or supply

chain entities. The findings reflect high-level conversations with an extremely small sample of value

chain actors and households across multiple districts, complemented by past studies carried out by the

Hygiene Improvement Project/Plan International–Uganda in Tororo and a demand driver study by

Nuwagaba. Most, but not all, of the individuals and organizations in our originally proposed sample fell

into our final sample of respondents (Table 1). Thus, the analysis and recommendations incorporate

10

reasonable assumptions based upon the themes of information expressed by respondents and may not

fully represent the market situation in every region or community in the country.

As mentioned above, the original terms of reference from WSP were to examine the supply chain actors

and business models for providing sanitation goods and services to rural households. The study was not

meant to focus on gathering extensive, quantitative data from the household perspective. Therefore,

the inclusion of limited information from qualitative household discussions is merely meant to provide

additional perspective on supply chain findings rather than serve as representative characteristics of

low-income, rural households across Uganda.

In addition, not all respondents were completely forthcoming with information asked of them during the

field surveys. Some reasonable assumptions were made, and gaps in information and analysis were filled

in some areas of the study based on comparisons to similar market conditions in other regional settings

in East Africa. While many commonalities exist between countries such as Uganda, Kenya, and Tanzania,

it is understood that underlying socioeconomic and cultural factors play differing but substantial roles in

shaping behaviors and perceptions around sanitation, and those factors affect market conditions in

unique ways in each setting.

Finally, the design and timeline for the study allowed for a limited exploration of select issues related to

household sanitation in Uganda. The findings from the study point to certain recommendations but are

not meant to indicate a finite set of solutions to addressing the need for improved sanitation at the

household level. Any approach to solving the challenges of increased access to sanitation requires an

extensive examination of multiple complex and interwoven issues, and this report attempts to address

only a subset of issues related to leveraging better market mechanisms for household sanitation

provision in rural and small towns in Uganda.

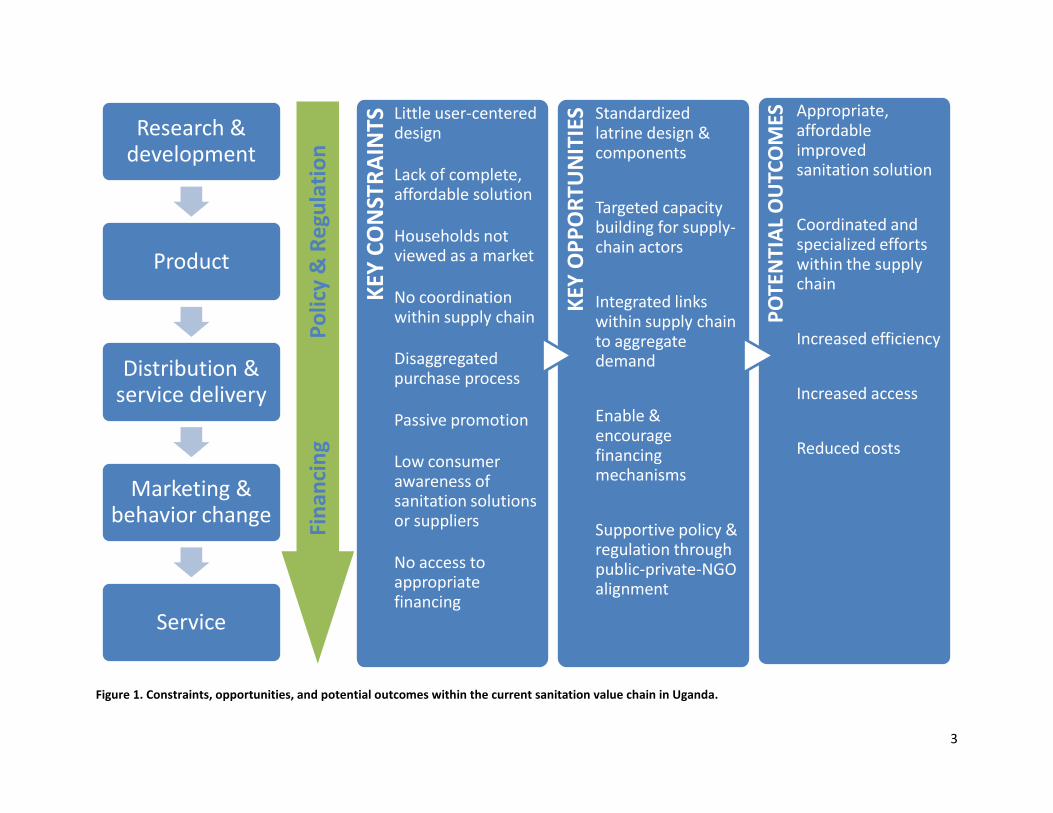

5.0 The sanitation value chain: A framework for analysis Understanding the elements of the value chain begins with examining the interactions among the

system players involved in the distribution and delivery of sanitation products and services. Entities such

as product designers, manufacturers, distributors, retailers, and service providers all serve as individual

links in an interdependent system (i.e., “value chain”) of service provision, which can function under a

variety of public-sector, private-sector, or combined approaches (Figure 3). The efficiency and

effectiveness of the value chain, however, depends upon the strength of the connections between each

link.

Figure 3. Value chain framework for the study.

The initial link in the chain, and one of the most critical factors for uptake by the consumer, is product or

service research and development. If a product or service aimed at households at the base of the

pyramid (BOP) does not easily integrate into their daily “ecology” of surroundings and routines, product

11

adoption often suffers. Thus, user-centered research and development that takes into account

consumer preferences, practices, and beliefs lays the foundation for establishing the rest of the value-

chain elements.

Appropriate design then leads to products or services, preferably sourced through local means in order

to ensure low-cost delivery and market sustainability. Products or services must also be of a high enough

quality to withstand the challenging conditions in which most BOP households live, while maintaining a

simplicity of elements that accommodates easy transport, assembly, repair, replacement, or upgrading.

In addition, products or services must allow for reasonable manufacturing scale in order to ensure

volumes necessary for sufficient profitability.

Distribution provides the access to meet consumer demand for products or services. However, this link

is often the weakest in market-based value chains in low-resource settings. Poor infrastructure,

disaggregated groups of potential consumers, and a lack of specialized training are some of the

numerous challenges to successful service delivery that can reach large numbers of BOP consumers.

Marketing and behavior change communication serve as the bridge to bring demand from consumers

together with product or service supply. Demand generation must balance between providing sufficient

general education and information about a product or service (i.e., category-level promotion or

behavior change communication), while emphasizing the appealing aspects and features of a specific

product (i.e., branded promotion). This is particularly important in the context of BOP markets, where

consumers may be inexperienced purchasers but still have aspirations for products or services that

improve their quality of life. In low-resource settings, NGOs and other public-sector entities often

shoulder the burden of demand generation and behavior change communication. Private-sector players

must also find ways to tie into these efforts or conduct independent marketing campaigns in order to

ensure success for market-based approaches.

Product purchase or service acquisition occurs at the point where demand generation meets access, but

after-sales service is essential for sustaining the connections between value-chain elements. Service may

involve simple follow-up visits from salespeople to gauge consumer satisfaction, or more extensive

interactions with individual or groups of consumers to provide further education, repairs, or upgrades.

Finding ways to enable the consumer to continue to interact with the product or service aids in weaving

it more completely into their daily lives, and it builds a relationship between the customer and each

piece of the value chain.

The need for access to business capital and other financing mechanisms underlies every link in the value

chain. Small entrepreneurs must have the ability to develop their products and build their stocks from

adequate working capital, while BOP consumers require access to financing in order to afford products

or services amid their often fluctuating income streams. Financing for low-resource settings involves

risks on both the supply and demand side of BOP markets (e.g., informal, unregistered small enterprises;

small loan amounts with long-term borrowing horizons for consumer purchase), but catalyzing the

growth and sustainability of market-based value chains cannot flourish without it.

12

6.0 Country background

6.1 Household demographics Across Uganda, the current average population density is nearly 170 people per square kilometer (as of

2010), but density varies fairly widely across many of the districts, especially those covered in this study

(Table 2).

Table 2. Population statistics for study districts. (UBOS 2002)

The average household size throughout Uganda is five members, and living conditions across much of

the country remain rather basic. Standard housing in rural areas typically consists of earthen floors,

walls made from local materials (e.g., mud, poles, stones), and roofs made of grass, leaves, or metal

sheets; more permanent building materials such as cement, tiles, and bricks are more commonly found

among urban households. Although somewhat dated, household construction data from 2002 across

the five districts further speaks to these norms as well as highlights the differences in income classes

across the study sites (Table 4).

Table 4. Construction material used for housing (percentage of households). (UBOS 2002)

Region NORTHERN EASTERN EASTERN CENTRAL WESTERN

District Arua Amuria Tororo Mpigi Bushenyi

Roofed with iron sheets 7.7 3.8 39.4 81.1 75.0

Grass-thatched roof 91.3 95.7 58.8 17.0 24.3 Walls made of mud and poles 21.3 13.9 75.6 43.8 80.2

Floor made of rammed earth 93.4 96.3 85.2 71.4 82.4

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

NORTHERN EASTERN CENTRAL WESTERN

Urban

Rural

14

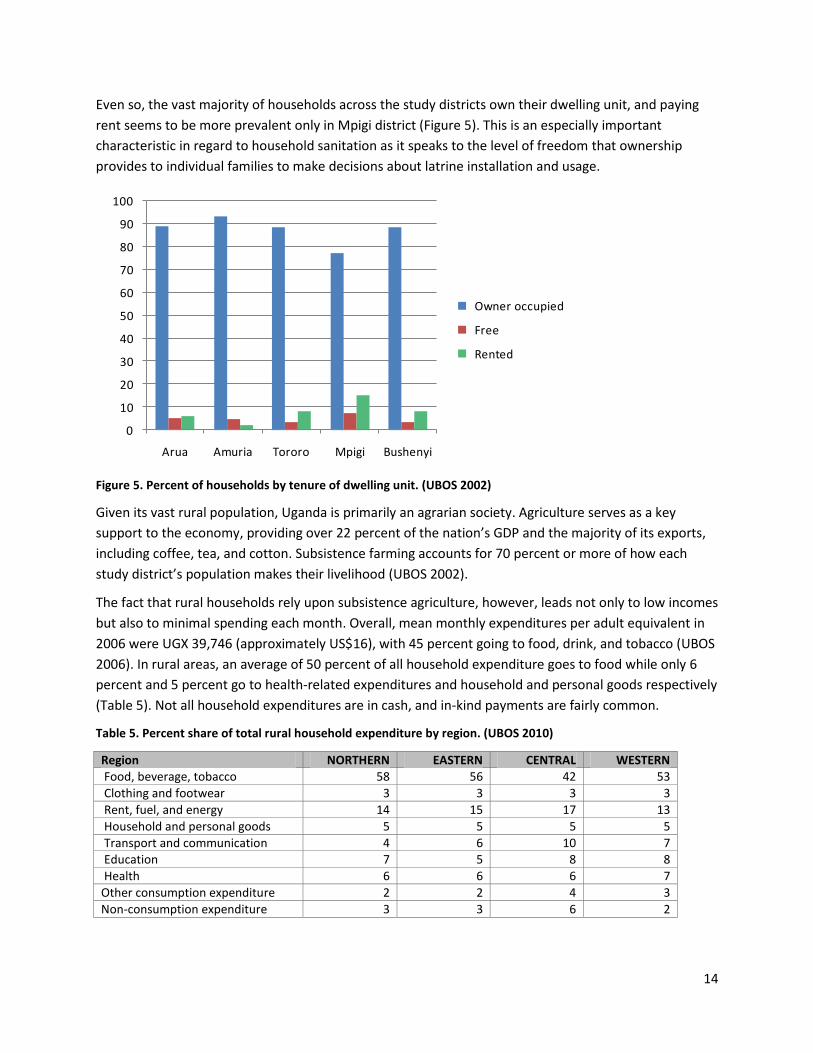

Even so, the vast majority of households across the study districts own their dwelling unit, and paying

rent seems to be more prevalent only in Mpigi district (Figure 5). This is an especially important

characteristic in regard to household sanitation as it speaks to the level of freedom that ownership

provides to individual families to make decisions about latrine installation and usage.

Figure 5. Percent of households by tenure of dwelling unit. (UBOS 2002)

Given its vast rural population, Uganda is primarily an agrarian society. Agriculture serves as a key

support to the economy, providing over 22 percent of the nation’s GDP and the majority of its exports,

including coffee, tea, and cotton. Subsistence farming accounts for 70 percent or more of how each

study district’s population makes their livelihood (UBOS 2002).

The fact that rural households rely upon subsistence agriculture, however, leads not only to low incomes

but also to minimal spending each month. Overall, mean monthly expenditures per adult equivalent in

2006 were UGX 39,746 (approximately US$16), with 45 percent going to food, drink, and tobacco (UBOS

2006). In rural areas, an average of 50 percent of all household expenditure goes to food while only 6

percent and 5 percent go to health-related expenditures and household and personal goods respectively

(Table 5). Not all household expenditures are in cash, and in-kind payments are fairly common.

Table 5. Percent share of total rural household expenditure by region. (UBOS 2010)

Region NORTHERN EASTERN CENTRAL WESTERN Food, beverage, tobacco 58 56 42 53

Clothing and footwear 3 3 3 3

Rent, fuel, and energy 14 15 17 13

Household and personal goods 5 5 5 5

Transport and communication 4 6 10 7 Education 7 5 8 8

Health 6 6 6 7

Other consumption expenditure 2 2 4 3

Non-consumption expenditure 3 3 6 2

0

10

20

30

40

50

60

70

80

90

100

Arua Amuria Tororo Mpigi Bushenyi

Owner occupied

Free

Rented

15

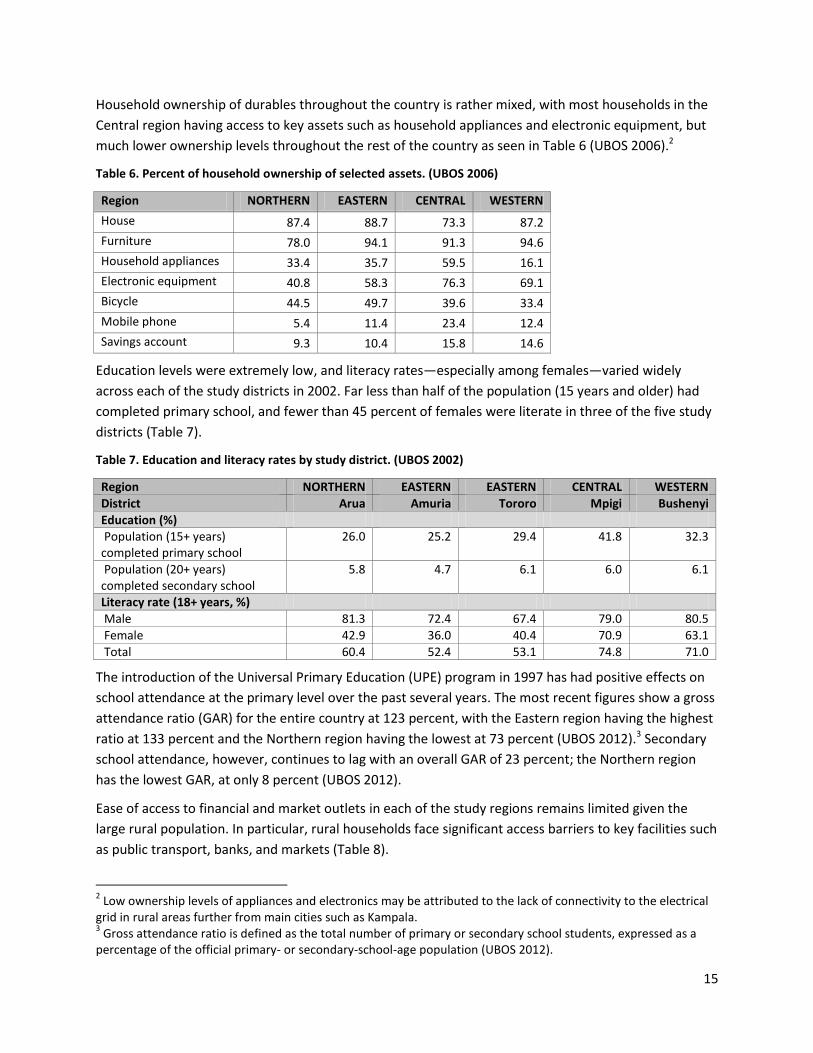

Household ownership of durables throughout the country is rather mixed, with most households in the

Central region having access to key assets such as household appliances and electronic equipment, but

much lower ownership levels throughout the rest of the country as seen in Table 6 (UBOS 2006).2

Table 6. Percent of household ownership of selected assets. (UBOS 2006)

Region NORTHERN EASTERN CENTRAL WESTERN

House 87.4 88.7 73.3 87.2

Furniture 78.0 94.1 91.3 94.6

Household appliances 33.4 35.7 59.5 16.1

Electronic equipment 40.8 58.3 76.3 69.1

Bicycle 44.5 49.7 39.6 33.4

Mobile phone 5.4 11.4 23.4 12.4

Savings account 9.3 10.4 15.8 14.6

Education levels were extremely low, and literacy rates—especially among females—varied widely

across each of the study districts in 2002. Far less than half of the population (15 years and older) had

completed primary school, and fewer than 45 percent of females were literate in three of the five study

districts (Table 7).

Table 7. Education and literacy rates by study district. (UBOS 2002)

Region NORTHERN EASTERN EASTERN CENTRAL WESTERN

District Arua Amuria Tororo Mpigi Bushenyi

Education (%) Population (15+ years) completed primary school

26.0 25.2 29.4 41.8 32.3

Population (20+ years) completed secondary school

5.8 4.7 6.1 6.0 6.1

Literacy rate (18+ years, %)

Male 81.3 72.4 67.4 79.0 80.5

Female 42.9 36.0 40.4 70.9 63.1

Total 60.4 52.4 53.1 74.8 71.0

The introduction of the Universal Primary Education (UPE) program in 1997 has had positive effects on

school attendance at the primary level over the past several years. The most recent figures show a gross

attendance ratio (GAR) for the entire country at 123 percent, with the Eastern region having the highest

ratio at 133 percent and the Northern region having the lowest at 73 percent (UBOS 2012).3 Secondary

school attendance, however, continues to lag with an overall GAR of 23 percent; the Northern region

has the lowest GAR, at only 8 percent (UBOS 2012).

Ease of access to financial and market outlets in each of the study regions remains limited given the

large rural population. In particular, rural households face significant access barriers to key facilities such

as public transport, banks, and markets (Table 8).

2 Low ownership levels of appliances and electronics may be attributed to the lack of connectivity to the electrical

grid in rural areas further from main cities such as Kampala. 3 Gross attendance ratio is defined as the total number of primary or secondary school students, expressed as a

percentage of the official primary- or secondary-school-age population (UBOS 2012).

16

Table 8. Access to selected social and economic outlets. (UBOS 2006)

Region NORTHERN EASTERN CENTRAL WESTERN

Access to transport facilities (% of communities)

All season feeder

roads 48.9 61.0 81.0 66.4

Bus stop 11.5 20.1 12.6 15.6

Taxi/matatu stop 22.0 26.7 38.0 38.4

Access to banking facilities (% of communities)

Bank branch office 0.3 0.2 0.2 0.8

Microcredit institution 0.2 4.6 3.9 7.5

Distribution of markets in communities

Consumer products markets

64.1 49.3 61.7 57.2

Furthermore, regardless of household access to banking facilities, the overwhelming majority of people

in each of the study regions have never opted to borrow money through formal or informal means

(Table 9).

Table 9. Percent of households that have ever applied for a loan. (UBOS 2010)

Region NORTHERN EASTERN CENTRAL WESTERN

Formal 2.7 3.1 5.5 3.5

Semi-formal 2.6 3.2 5.0 3.9

Informal 2.6 3.2 5.0 3.9

For the few Ugandan households that have applied for a loan, most of them utilized it to purchase

inputs or working capital for a business, as seen in Figure 6.

Figure 6. Purpose of loan by percent of households having applied (all Uganda). (UBOS 2010)

0 5 10 15 20 25 30

Purchase inputs/working capital

Buy consumption goods

Pay for education expenses

Pay for health expenses

Pay for building materials

17

6.2 Household sanitation status

The Joint Monitoring Program (JMP) for the World Health Organization and United Nations Children’s

Fund estimated in 2010 that just over a third (34 percent) of the Ugandan population was using

improved sanitation, with as many as 10 percent (primarily rural inhabitants) still resorting to open

defecation (JMP 2012). The number of households using open defecation as their sanitation solution has

dropped significantly since 1990, when the proportion was 28 percent. Some of this drop may be the

result of large-scale integrated rural water and sanitation programs, many of which offered subsidized

latrine platforms, as well as the enforcement by various local governments of the Public Health Act to

mobilize communities to end open defecation practices (WSP 2011). For the most part, however,

Uganda remains a country reliant upon traditional pit latrines, especially across the four regions of the

study (Table 10).

Table 10. Percent of households by type of toilet facility. (UBOS 2010)

Region NORTHERN EASTERN CENTRAL WESTERN

Flush toilet 0.3 0.6 14.1 0.8

VIP latrine 1.9 1.9 10.0 1.2

Pit latrine 72.9 86.1 75.9 95.7

Bush/no toilet 24.9 11.4 0 2.3

Many of the households with access to a latrine share that facility with other households, which equates

to unimproved sanitation access under JMP standards. JMP data from 2010 estimated that 20 percent of

the total population shared their sanitation facility with at least one other household (JMP 2012). The

Demographic and Health Survey (DHS) in 2006 revealed that 43 percent of all respondents (37.3 percent

in rural areas) indicated they used a latrine facility that was shared with at least one other household

(Uganda 2007).

Little data exists on the quality of latrines found throughout the country. While DHS data collection

indicated that 40.8 percent of rural households utilized a pit latrine without a slab, no delineation is

given regarding the shared facilities, and few other studies have been conducted to extensively assess

the status of traditional latrines across Uganda.4 It is reasonable to assume from statistics related to

household facilities and the overall rural nature of Ugandan society, however, that most latrines are

constructed with simple materials. These basic-style latrines often have makeshift walls and roofs, but

rarely are the superstructures made from permanent materials, and few latrines offer full doors for

privacy. Grass, mud, dirt, wood, fabric, and other improvised materials that can be cheaply and locally

sourced are common building elements, particularly in rural areas. However, even these materials are

becoming increasingly scarce due to poor land-use methods, unsustainable harvesting of materials, and

deforestation (USAID 2009). Bricks, cement or plastic, and metal may also be utilized for walls, slabs, and

roofs respectively, but are much more expensive and difficult to access for low-income households.

4 For example, a qualitative study of 30 households by the United States Agency for International Development

Hygiene Improvement Project in Tororo district revealed that of the 16 households using latrines, 14 latrines were of a traditional style with mud slabs and grass-thatched roofs (USAID 2009).

18

Movement toward the initial rungs of the sanitation ladder

(Figure 7) has seen some positive progress in Uganda over

the past several years. Between 1990 and 2005, an average

of 3.96 percent of the population per year reported a

change in sanitation coverage to a traditional latrine

(Morella 2009). Improvements beyond traditional latrines,

however, have been extremely limited with only 0.2

percent of the population annually moving to an improved

latrine (Table 11).

Table 11. Annualized change in sanitation coverage (percent of

population) from 1990–2005. (Morella 2009)

Septic tank Improved latrine

Traditional latrine

Urban 0.5 0.7 4.4

Rural 0 0.1 3.9

Total 0.1 0.2 3.96

6.3 Household segmentation The country background data begins to paint a picture of

some key characteristics of the target market for potential

demand-responsive business approaches to household

sanitation provision. Overall, the market appears somewhat

homogeneous, but there are particular nuances that may

be critical to ensuring the success of certain approaches.

The majority of the population in these districts consists of

rural, low-income households dependent upon agriculture

for their way of life. The level of sophistication in their daily life is rather limited. Most households live in

primarily temporary dwellings constructed of basic materials and rely upon basic sanitation solutions

such as pit latrines or open defecation, and they have limited access to market infrastructure and the

tools necessary to engage in market activity—either as suppliers or consumers. Furthermore, there has

been little progression toward improved latrines over the last several years, and the status and quality

of the current traditional pit latrines remains questionable. This might indicate that the market need

may not necessarily be a new latrine design, especially for a population with constrained income and

limited access to finance. Piecemeal latrine upgrades and retrofitting of what households currently have

in place could be more appropriate approaches in the near term. All of these factors must be taken into

account for any market development activity, and all speak to the need to design relatively basic

interventions that can aid the majority of the population in gaining familiarity with both improved

sanitation and market mechanisms that might increase access to it.

Beyond the broad characteristics across all study sites, there are some differences between districts that

are particularly important to highlight for any future sanitation market development opportunities. The

data show higher average monthly incomes and a greater proportion of households in the higher

Figure 7. The sanitation ladder.

Open defecation: When human waste is disposed of in fields, forests, bushes, open bodies of water, beaches, or other open spaces, or disposed of with solid waste.

Unimproved facilities: Do not ensure hygienic separation of human excreta from human contact. Unimproved facilities include pit latrines without a slab or platform, hanging latrines, and bucket latrines.

Shared facilities: Sanitation facilities of an otherwise acceptable type shared between two or more households. Only facilities that are not shared or not public are considered improved.

Improved sanitation facilities: Ensure hygienic separation of human excreta from human contact. Such facilities

include: Flush or pour/flush latrines to piped sewer, septic system , or pit latrine; ventilated improved pit latrine; pit latrine with slab; or composting toilet.

Un

imp

rove

d s

anit

atio

nIm

pro

ved

san

itat

ion

19

income classes in both the Central and Western regions (where Mpigi and Bushenyi districts respectively

are located). Mpigi and Bushenyi also display higher rates of education (percent of population having

completed primary school) and literacy from the 2002 data. These factors may indicate a population not

only better able to consider market-based interventions requiring parting with their expendable income,

but also one better able to connect with marketing efforts for new household sanitation product

offerings.

Lower average monthly household incomes and household income classes are found in the Northern

and Eastern regions (where Arua and Amuria/Tororo districts respectively are located). Only one-quarter

of the population in Arua and Amuria have completed primary school, and only 36 to 43 percent of

females in Arua, Amuria, and Tororo are literate (UBOS 2002). Furthermore, approximately 25 percent

of the population still resorts to open defecation in the Northern region, and over 10 percent defecate

in the open in the Eastern region. These factors point to the need for a very different approach than that

applied in other locations of Uganda. A low-cost, basic improved sanitation solution communicated

through simple means may be the most appropriate approach.

6.4 Regulatory and policy environment for sanitation

The Government of Uganda has committed to achieving the Millennium Development Goals to address

issues related to the high poverty rates within the country and has incorporated many of these targets

into the 2010 National Development Plan. The government’s current policy objectives for the water and

sanitation sector are to address poor sanitation and hygiene to move households up the sanitation

ladder to facilities that can be cleaned and have hand-washing facilities next to them. The specific target

is to increase the proportion of households in Uganda with pit latrines from the current 70 percent in

2011 in rural areas to 77 percent by the year 2015 (UMoH 2010). The government’s approach has

progressed through several policy development and iteration processes including:5

Kampala Declaration on Sanitation of 1997

Ministerial Memorandum of Understanding of 2001

Formation of the National Sanitation Working Group of 2003

Environmental Health Policy of 2005

Improved Sanitation and Hygiene Financing Strategy of 2006

Each policy has incorporated a stronger focus on bridging existing gaps in sanitation access and

provision; however, it should be noted that Uganda still has no specific national sanitation policy.

Instead, sanitation is managed under a broad network of laws, regulations, by-laws, and policies spread

among numerous agencies and governing bodies. While there is no single institution with a direct

mandate to authoritatively deal with all aspects of sanitation in Uganda, the MoH is widely viewed as

the acknowledged lead, especially in the realm of policy development, but continues to be hampered by

a lack of resources (Table 12). Furthermore, local governments struggle with sanitation law enforcement

due to political interference at various levels and difficulty in getting by-laws approved which causes

5 Several other policy documents have also been written and are at various levels of implementation such as the 1

st Health

Sector Strategic Plan in 2005, the National Health Policy and 2nd

Health Sector Strategic Plan in 2010, and the Improved Sanitation and Hygiene Promotion Financing Strategy in 1997.

20

increased difficulty in the improvement of access to safe sanitation services at the household level.

Stakeholders under the National Sanitation Working Group have supported different aspects of the

sector, with WSP supporting policy development and nongovernmental organizations (NGOs) such as

Plan International–Uganda introducing new methodologies.

Table 12. Institutional responsibilities in the Uganda sanitation sector. (The Water Dialogues 2008)

Institution Responsible department/division Specified role

Ministry of Health Environmental Health Promote household hygiene and sanitation.

Ministry of Water and Environment Directorate of Water Development and National Water and Sewerage Corporation

Plan investments in sewerage services and public toilet facilities in urban areas.

Ministry of Finance, Planning, and Economic Development

N/A Allocate sanitation sector budget.

Ministry of Gender, Labor, and Social Development

Community Development Department

Develop policies and guidelines with respect to community mobilization and empowerment, gender responsiveness, coordinating and mentoring community development workers, and coordinating cross-cutting development areas.

Ministry of Local Government N/A Inspect, monitor, advise, and provide technical assistance to local governments.

Local governments District Health Inspectorates Enforce laws and provide sanitation services at the local level.

National Sanitation Working Group N/A Coordinate ministries responsible for sanitation and sanitation promotion activities.

District Water and Sanitation Working Groups

N/A Coordinate sanitation-promotion activities at the district level.

Setting funding priorities for water supply, sanitation, and primary health care interventions has largely

been ceded to local governments, with budget-making and control designated at the district levels.

However, the central government retains the roles of policymaking, standard setting, technical

oversight, and overall program supervision (USAID 2007). Funding for rural sanitation activities at the

district level depends on national-level allocations from within ministerial budgets, known as on-budget

funding. Districts decide how to spend these allocated funds, within guidelines and restrictions imposed

from the national level. Off-budget funding from nongovernmental sources can be provided directly to

districts, but more often bypasses district budgeting and expenditure mechanisms, going directly to pay

for implementation activities designed and run by NGOs themselves, often at the sub-county or village

levels (USAID 2007).

At the national level, government funding for sanitation still lags far behind funding for the water

supply. A key funding problem has been the general marginalization of sanitation and hygiene activities

at the district level, particularly the general lack of district-level attention to rural household sanitation

(USAID 2007).

21

The Ugandan government has attempted to use innovative approaches including incentives and

competition to encourage districts. Potential sources of off-budget financing (decided at national and

district budgets) for household sanitation and hygiene promotion have included household investment

in sanitation facilities, microfinance available to communities and consumers (thus far fairly minor, but

increasing), grants and subsidies from NGOs and donor projects, and private-sector investments (also

very limited to date). However, neither microfinance nor private-sector investments have been

mobilized directly for rural sanitation thus far (USAID 2007).

Uganda’s rich policy context with various regulations, declarations, and legal instruments intended to

achieve its health and sanitation objectives, however, has not translated into substantial progress in

provision of improved sanitation—especially in rural and small towns—or tangible health outcomes.

Inadequate resources, high levels of poverty, inadequate awareness and poor enforcement of public

health by-laws are major challenges that have affected the implementation of environmental health

strategies (UMoH 2010).

According to a 2008 report published by The Water Dialogues:

Perhaps the biggest obstacle to progress in improved sanitation in Uganda is the lack of a specific

sanitation policy under the current institutional and policy arrangements. Implementation of

interventions relies on inferences from other policies like the national Environmental Policy and

the Water Policy, which are not adequate to address the needs of the sanitation sector. This

explains why even progressive strategies like the Improved Sanitation and Hygiene Financing

Strategy, which is championed by the National Sanitation Working Group (NSWG) as the

preferred approach to sanitation improvement, remains difficult to implement and monitor, as

they have no institutional home, but largely rely on the goodwill of various agencies and persons,

and often the short-term pressure of development partners, especially through the NSWG.

Unfortunately such goodwill does not provide an adequate anchor for private sector

participation or a guarantee of security for their investments (The Water Dialogues 2008).

Uganda primarily follows a private-sector-led economic system, with the government serving to provide

policy and regulatory support. Private provision of sanitation services in Uganda has a long history

stemming from the Public Health Act of 1964 (and refreshed in 2000), which places the responsibility for

obtaining sanitation facilities with individual households.6 Still, a substantial proportion of the

development programs stemming from the Poverty eradication Action Plan (PEAP) are financed by

donors. This has consequently distorted the potential for market development and prohibited private-

sector entry into sectors such as sanitation by creating unrealistic expectations, most likely within the

supply chain, that services will be provided to households for free or via subsidies through government,

donor, or NGO funding (The Water Dialogues 2008).7

6 Furthermore, the Public Health Act provides that any dwelling without proper sanitation facilities should be

closed down and or its owner prosecuted (The Water Dialogues 2008). 7 While the Environmental Health Policy states that no subsidies shall be offered for household sanitation, the

funding of development programs by donors can foster a discouraging signal to private-sector players that they might not be able to obtain a profitable return on their participation in the sector.

22

6.5 Key sanitation stakeholders

While local government entities, donors, international NGOs, civil society organizations, private-sector

players, and individual communities all play an important role in health, the Ministry of Health has

overall authority over the household sanitation sector in terms of promulgating regulations and

implementing programs. According to a 2011 study in which stakeholders were ranked according to

influence, the MoH/Environmental Health Department was said to be the most powerful and influential

with regard to community-led total sanitation (CLTS) and sanitation marketing (SANMARK) (J. Birungi,

unpublished data, 2011). The Ministry of Water and Environment (MWE)/Directorate of Water

Development (DWD) was said to be the second most powerful due to its responsibility for urban

sanitation and hygiene promotion among safe water user communities. The MWE allocates funds to

local governments for sanitation under the District Water and Sanitation Conditional Grant and provides

capacity building through Technical Support Units. District local governments were identified as key in

the implementation of CLTS/SANMARK as they are responsible for service delivery including sanitation,

formulating policies and by-laws, and planning and locating resources for sanitation at the district level.

The study attempted to visually represent a continuum

of influence based upon the interpretation of the major

actors within the sanitation sector (Figure 8).

The continuum illustrates some of the key issues

currently contributing to the development of better

mechanisms for delivering household sanitation within

Uganda. Government entities maintain high influence,

but without particularly clear lines of coordination and

few resources. International and local organizations

find themselves clumped somewhere in the middle, all

experiencing various levels of success amid different

implementation efforts. Meanwhile, the private sector

and media sit at the lowest levels of influence within

the sector, either through circumstance or by choice.

A separate, similar mapping exercise was carried out by

WSP to assess the level of influence of each stakeholder

based upon its amount of resources, policy mandate,

and/or authority to make decisions. The full table of

stakeholders can be found in Appendix A. The results

were fairly similar in that it displayed the various

degrees of influence and support across the sector,

and seems to point towards the need for consolidation

of sanitation policy and alignment of key contributors

for pursuing market provision of sanitation.

Figure 8. Continuum of influence of sanitation

sector actors in Uganda. (J. Birungi,

unpublished data, 2011)

MoHMWE

Districts

MoFPEDWorld Bank/WSP,

DANIDA, AfDB, UNICEF

Plan, Water Aid, NETWAS, SNV, Technical Support

Units, UWASNET

MediaPrivate sector

Low

Hig

h

23

7.0 Study findings: The sanitation value chain in Uganda

7.1 Summary Secondary data reflect a population generally aware of the need for household sanitation solutions, but

unable to meet the proper threshold for improved latrine designs due to any number of reasons.

Households may choose to construct everything themselves or hire a local laborer to assist with portions

or all of the construction. The building process and materials, however, most often do not comply with

any sort of specifications or regulations for ensuring a safe and improved sanitation solution. A

collection of improvised, makeshift latrines built through informal means has resulted from a market

that basically does not acknowledge the presence of sanitation service provision as a subset of need or

opportunity.

The market for household sanitation in Uganda is undefined and undeveloped. At the most basic level

this is evident in the fact that Crestanks—a local manufacturer of ready-made, plastic latrine

components—does not sell directly to the consumer.8 As for the actors within the supply chain that do

interact directly at the household level (e.g., masons), they do so in a one-off, disaggregated fashion and

do not currently possess the correct training, tools, or approaches to take their operations to scale in

any meaningful way. Instead, they focus on “easy win” opportunities such as government and school

contracts for latrines and other construction projects. Households are not seen as consumers for

improved latrines and this philosophy appears to permeate the small service providers within the supply

chain, from hardware stores who sell traditional latrine components to the masons who build them. At

this point in time, many low-income Ugandan households are not considered to be a revenue-

generating market and therefore the supply chain has not invested in building appropriate sanitation

solutions for this segment of the population. However, a USAID study from 2009 posited that if demand

were stronger and year round, the development of specialized latrine contractors may be viable (USAID

2009).

It appears that there is a lack of coordination along the sanitation supply chain in Uganda and entities

are acting in isolation. From manufacturers to distributors to sales, installation, and services, the players

do not seem to be in communication or have aligned incentives. This creates gaps that unnecessarily

increase the financial and time resources needed to deliver a complete solution to the end user,

therefore further constricting the development of a sophisticated household sanitation market.

Until gaps along the entire value chain are addressed, the household sanitation industry will remain

immature and will inhibit the creation of safe, culturally-relevant solutions for low-income markets. This

endeavor will take great coordination and investment in order to strengthen supply, build demand, and

sustain a competitive business environment that fosters synergies and innovation and allows for

expansion.

8 This supports findings from a 2007 study by USAID that found that “while Crestanks remains hopeful and believes

sales to households is ultimately where it wants its market to develop, the company currently has neither the market reach, distribution, capacity, nor the ability to invest in direct promotion and sales to households” (USAID 2007).

24

While the constraints within the household sanitation value chain in Uganda are significant, they are not

insurmountable, and they point toward clear opportunities for laying a solid foundation for the

development of the sanitation market. The fact that little market infrastructure currently exists in the

household sanitation space allows for broad and potentially sweeping innovation across the entire value

chain.

Certain aspects of any household sanitation market creation effort will present much more complex

challenges than others, and will require coordination, partnership, and patience. Still, some initial

components for high-potential market-based approaches to household sanitation in Uganda are already

in place, and stakeholders appear to be engaged and established within the sector. The key will be

integrating and aligning current and future efforts accordingly to ensure both scalability and

sustainability.

For example, organizations such as Plan International–Uganda have begun to build a foundation for

improved access to better household sanitation through training masons, behavior change

communication, community-led total sanitation (CLTS), and hand washing initiatives. However, the next

step is to create an environment that encourages efficiency as well as building and delivering market-

based solutions at scale. Properly establishing a household sanitation industry will require specialization

and vertical integration.

7.2 Research and development

7.2.1 Current status

Broad research and development efforts around household sanitation in Uganda appear to be virtually

non-existent, apart from a few targeted efforts such as the Network for Water and Sanitation Uganda

(NETWAS) Action Research Project carried out with a few designs in four districts. While some

manufacturers have worked with local and international NGOs on targeted (primarily in terms of

geographic locations and specific populations) sanitation-related projects, few have taken the initiative

to design sanitation products or latrine elements geared toward broad acceptance by low-income

households across the country. Organizations such as Plan International–Uganda have instituted

projects around new styles of latrine slabs and other organizations have introduced Ecosan

technologies, but these efforts have been limited to a small number of districts and have shown little

success in terms of uptake.9 Evidence exists within Uganda of multiple household sanitation-related

products (primarily in the plastics category), but there appears to be no proactive effort on the part of

manufacturers or other product design entities to better understand user needs and desires for

acceptable and affordable household sanitation solutions.

7.2.2 Constraint: Lack of a standardized, culturally appropriate sanitation solution

The study encountered a wide range of definitions of what materials are needed to construct an

improved latrine. Of all the groups interviewed, masons seem to have the clearest idea of what they

require, but there were discrepancies in the exact materials, the amount of materials, and the time

9 Plan noted in an interview that since inception, 90 Plan-sponsored masons have sold only about 40 to 50 latrines

over a three-year timeframe.

25

needed for construction. The study was unable to discern a widely-used, standard package of latrine

construction materials (e.g., cement, iron bar, wire mesh, etc.), and therefore, was unable to get an

accurate idea of the total price of an improved household latrine.10

The lack of standardization inhibits the ability of the supply chain to gravitate toward an optimized

business model to deliver better sanitation products and services. Understanding what the consumer

wants in design, function, and health/safety benefits serves as the first step to being able to offer a

range of desirable technologies and services, at various price points, to meet the demands of

households.

At the current time, there are no consumer brands for household latrine products or complete solutions.

When a household approaches a mason or hardware store to inquire about latrine construction, there is

no one set of materials that serves as a reference point. Variable inflationary price fluctuations and

product stock-outs across hardware suppliers also make estimating a guaranteed total cost for a latrine

extremely difficult once a household attempts to assemble the necessary materials. The result is a

convoluted and confusing latrine construction decision and purchase process for the household. The

simple addition of a single, bundled product/service solution at the point of sale could make all the

difference in generating increased consumer demand for improved household latrine solutions.

While the MoH has design standards for latrine pits, these do not seem to be followed on a wide scale at

the household level. Pits depths can vary from 15 to 40 feet, and any official guideline for optimization,

safety, or compliance does not seem to be recognized by the majority of informal service providers. The

dimensions of the pit partially dictate the amount of materials needed to construct the remaining

components of the entire latrine, and so from the very beginning, there are variances, which further

complicate the industry.

With no standard for either materials or construction pricing, coupled with inflation and stock-outs, the

task of quoting the exact total cost of an improved latrine to a household is difficult. The inability to

clearly communicate aspects of materials, labor, and total cost to households affects the overall

perception of improved sanitation and makes access and uptake even more challenging. Once a

common solution set to meet demand for household sanitation products and services is established, the

natural forces of competition and specialization can smooth out issues of pricing and eventually lay the

foundation for a package of solutions aimed at various niche markets.

7.2.3 Opportunity: Documenting user input and feedback on latrine design and functionality

The critical gap in the initial link of the value chain is a lack of knowledge of what households might

desire for their sanitation solutions. There appears to be little to no investment on the part of plastics or

cement manufacturers on specialization, innovation, or product development related to household

sanitation. Although plastics manufacturers currently produce products that can be used in household

sanitation settings as well as engage in small-scale, coordinated product development, most of this

activity appears to be tied to NGO initiatives and distribution efforts. Such efforts, however, do little to

drive a market for household sanitation forward. Without competition from elsewhere in the sector,

10

However, cost estimates from the Network for Water and Sanitation (NETWAS) estimate slab construction with a similar set of materials at a cost of approximately between UGX 40,000 and UGX 50,000 (NETWAS 2012).

26

manufacturers have little incentive to explore lower-cost product designs or broaden their distribution

channels. That type of market structure means that consumers will never have the opportunity to

provide their input and feedback to market actors, especially in critical areas such as product design and

functionality.

The opportunity exists for better understanding of household sanitation needs and desires in Uganda,

and then introducing or developing a latrine that fulfills that need. The Ugandan Network for Water and

Sanitation (NETWAS) is already helping to address this opportunity through the Action Research sub-

component if the Learning for Policy and Practice in Rural Household and Primary School Sanitation and

Hygiene (LeaPPS) project (Box 1). The project has taken current basic, improved latrine designs and has

worked with communities to adapt them for the local context. This iterative process continues, and

challenges remain especially in terms of cost of construction, but findings thus far indicate that the

potential is high for replication in other locations over time.

Box 1. Action Research with latrine designs under the LeaPPS project.

Since 2008, Simavi has supported SNV, IRC and NETWAS to implement the Action Research for Learning for Policy and Practice in Rural Household and Primary School Sanitation and Hygiene (LeaPPs) project which focuses on local learning around cost-efficient and effective sanitation and hygiene programs, sustainable facilities, and behaviors in primary schools and households (NETWAS 2012).

This initiative aims at synthesizing sanitation and hygiene issues derived from the previous action research to streamline further learning towards more effective and pro-poor sustainable sanitation technologies and approaches in households and primary schools in the districts (NETWAS 2012).

Under LeaPPS, the Action Research sub-component brought four sanitation technology solutions (the fossa alterna, spiral fossa alterna, two-in-one fossa alterna, and arborloo latrine designs) to communities with poor soil formation and termite infestation that did not favor construction of the commonly used traditional pit latrines (NDCL 2012). The technologies are also a deterrent to wastage of arable land and promote organic farming through provision of compost manure in predominantly agriculture areas.

The latrine designs were meant to address specific geological difficulties faced by certain communities in Uganda. For example, the latrines incorporate shallower pit designs and composting strategies to alleviate the difficulty of having to dig a deep pit in rocky soil. However, the designs for each latrine have been altered over time to suit individual community and socio-economic needs. These adaptations have resulted in improved perception of the latrines and increased interest in how to construct them by community members.

Overall, many stakeholders are also satisfied with the designs, but challenges related to the cost of construction remain. Households seem unwilling to invest their own money in sanitation despite being interested in the technologies, and the initial costs of construction (UGX 248,400 for a fossa alterna latrine, and UGX 117,450 for an arborloo latrine) have discouraged local community uptake (NETWAS 2012). In addition, there is limited access to non-local construction materials such as cement, iron bars, and iron sheets.

Still, the project continues to work with the local communities to incorporate their ideas and concerns into additional improvements to the design to bring down construction costs and increase access and uptake. The project plans to undertake pilot construction of fossa alterna sub-structures with locally-sourced soils and treated logs to test for appropriateness and durability.

The project acknowledges that further time is required to continue to build awareness about the different technologies and educate the communities about the design aspects. However, current recommendations point towards extending the project in order to continue to learn from current progress and better determine the best course for future replication.

27

An additional opportunity lies at an even more basic level of gathering more insight into more specific

user preferences related to sanitation at a broad, country-wide level (Box 2). Similar to the process of

tweaking current designs as done in the LeaPPS Action Research, more can be done to completely

understand the nuances of sanitation practices and preferences to ensure those details are considered

in the initial design of new sanitation solutions (or redesigns of old ones).

The challenge is not necessarily to design the cheapest latrines and superstructures possible, but to

create designs that fit the reality and desires of the target audience, to make valued latrine products,

including superstructures that can be a major part of the cost (USAID 2007). In-depth research and

development with users (i.e., households) to move toward lower-cost designs and production of

improved latrine components should be encouraged in order to aid in building a brand and business

model to deliver that product, increasing local production of latrine components, eliminating the need

to transport supplies or products over long distances, and driving down costs across the entire value

chain.

Box 2. PATH’s user-centered design approach and latrine user-needs assessment in Cambodia and Kenya.

To date, there has been limited involvement of end-users in the design of improved sanitation solutions in spite of evidence demonstrating higher uptake and sustained use of technologies that incorporate user experience through iterative feedback loops based on human-centered design theory. Factors such as attitudes about human feces—including those of very young children—or women’s needs for privacy and security are often mentioned, but they are poorly understood and rarely considered in design. Furthermore, few designs for high-volume production currently exist that focus on user experience or include input from users themselves. Locally designed and site-constructed latrines that involve communities and users provide an important starting point for additional learning and research.

To that end, PATH conducted qualitative user-needs assessments in Cambodia and Kenya focusing on the preferences and priorities of low-income latrine users. The objective of the assessments was to explore how users’ norms, preferences, and priorities around sanitation may impact their use and demand for an improved, upgradeable latrine platform.

The study consisted individual interviews with opinion leaders, service providers, and users, as well as hardware inventories in multiple communities in each country. The structured interviews explored the current behaviors, preferences, priorities, and barriers to healthy sanitation practices for users of latrines and covered topics such as desired ideal profile-specific features, comparative standards, motivation to change behavior, and hygiene.

Findings from the research highlighted critical issues for user acceptability related to latrine design in Kenya, which may impact the uptake and continued use of latrines. The research also revealed the importance of pairing the platform component of the latrine with a structurally sound enclosure and weather/flood resistant collection pit.

In Cambodia, the large amount of user-feedback data generated from focus groups allowed for the drafting of initial engineering design plans for a latrine slab or platform. These designs incorporate user preferences such as ease of cleaning, material composition, and layout of slab features with production requirements for interoperability with standard construction processes, structural requirements, and ventilation. The end result was an alpha design that meets baseline criteria for the target audience and is ready to be transitioned to physical prototyping and testing in a forthcoming PATH project. The availability of this prototype opens the door to end-user experience research, the crucial next step in ensuring that the product can combine effectiveness, appropriateness, and desirability.

28

7.3 Products

7.3.1 Current status

The supply chain interviews make it fairly apparent that households view certain aspects of a latrine as

completely separate entities, whether due to costs, labor, or other factors. Pits seem to be thought of as

a facet of the latrine construction process that is independent from slabs and/or superstructures.

Therefore, while usually not requiring physical materials, the pit can be considered an individual product

in the household latrine value chain. From the field work, it appears that most pits are dug to an

impressive and expensive depth, and then usually left unlined, which can make them susceptible to

collapse, especially during the rainy season. References were made by several respondents to formal pit

regulations that are broadly known by households and often followed for fear of financial penalties.

Households appear to hire informal laborers to dig pits and pay cash upon completion, or in increments

as able with the laborer digging in a meter-by-meter fashion upon payment.

For households that choose and are able to invest further resources in building a latrine over a newly-

dug pit, or improving a current latrine, the options to do so through the commercial market are fairly

limited and usually revolve around either the slab or the superstructure components. Cement slabs are a

common route for improved pit coverings for households in rural and small towns. Mass-produced,

ready-made, pre-cast cement slabs are virtually nonexistent (however, the study did speak with one

small, independent cement manufacturer in Arua district making cement slabs for purchase; see Box 3).

Thus, households who choose the option of investing in a cement slab sacrifice the investment of time

and energy, in addition to the cost, to obtain and transport the necessary materials on their own and

then hire a mason to construct it for them. No common set of cement slab materials appears to be

established either through regulatory means or from manufacturers, which means households are left

to determine on their own what they think is necessary or simply what they can afford to fashion a

cement latrine slab.

29

Multiple major cement manufacturers exist in Uganda, including Hima Cement and Tororo Cement, but

findings from the study indicate that these manufacturers are not currently offering any specialized

product for use in latrine facilities. They focus their business on large industrial projects such as roads

and simply meeting the increasingly high demand for bagged cement within Uganda as well as in

neighboring countries. None of them are specifically gearing any of their production toward use in the

construction of sanitation facilities.

Plastic slabs are much lighter, more conducive to centralized production, and easier to distribute given

their lighter weight, higher durability, and “nesting” ability for shipping. Both plastic slabs and

superstructures are produced locally in Uganda and come ready-made, but low-income households have

little access to them due to either their relatively high price or lack of commercial distribution.11 One

local company currently manufacturing household sanitation components is Crestanks, a subsidiary of

AquaSan Tec and headquartered in Kampala. The company currently manufactures a full catalog of

sanitation products; however, most of these items seem to be geared primarily toward the needs of and

use by NGOs. In addition, the cost of their products is quite prohibitive to the typical rural household

(WSP 2011). Their products include latrine platforms of various sizes and styles, modular latrine

11

It should be noted that a few of the households from the field survey also mentioned that they did not prefer the look of currently available plastic latrine slabs. Thus, an additional issue may be lack of appeal.

Box 3. WE Concrete in Arua District.

Major manufacturers such as Tororo Cement and Hima Cement primarily produce bagged cement for distribution throughout Uganda, but PATH found little evidence of broad availability of pre-cast cement products for household sanitation. One notable exception is WE Concrete in Arua District. WE Concrete sells multiple concrete products, including pre-made cement latrine slabs of various sizes. They have been in operation now for seven years and also have an additional branch in Gulu District.

WE Concrete currently offers three different sizes of slabs:

80cm x 100cm for UGX 45,000

80cm x 120cm for UGX 60,000

90cm x 120cm for UGX 65,000

They sell the slabs through passive efforts by placing them by the roadside, where customers come to purchase and transport them on their own. Even so, WE Concrete mentioned that all three sizes of slabs “sell a lot” and there are weeks when their stock of slabs sells out.

The company came up with the idea of pre-casting latrine slabs because they realized other materials that households were using for latrines (e.g., wood and mud) easily deteriorated. Pre-fashioned cement slabs provided a cost-effective, durable, and portable solution that could even be re-used if a new latrine became necessary.

WE Concrete currently employs seven laborers who assist in slab production, and one marketing manager. The majority of their customers come from within Arua as well as neighboring districts, but some come from as far away as Kampala, the Democratic Republic of the Congo, and Sudan. The company estimates that 60 percent of their customers are from urban areas, and households that purchase are primarily from middle and upper income classes.

WE Concrete believes that the pre-fabricated slabs are one of their most popular and profitable products. They estimated that sales of the slabs account for an average of 70 percent of their overall monthly business, and they are interested in exploring ways to expand their business.

30

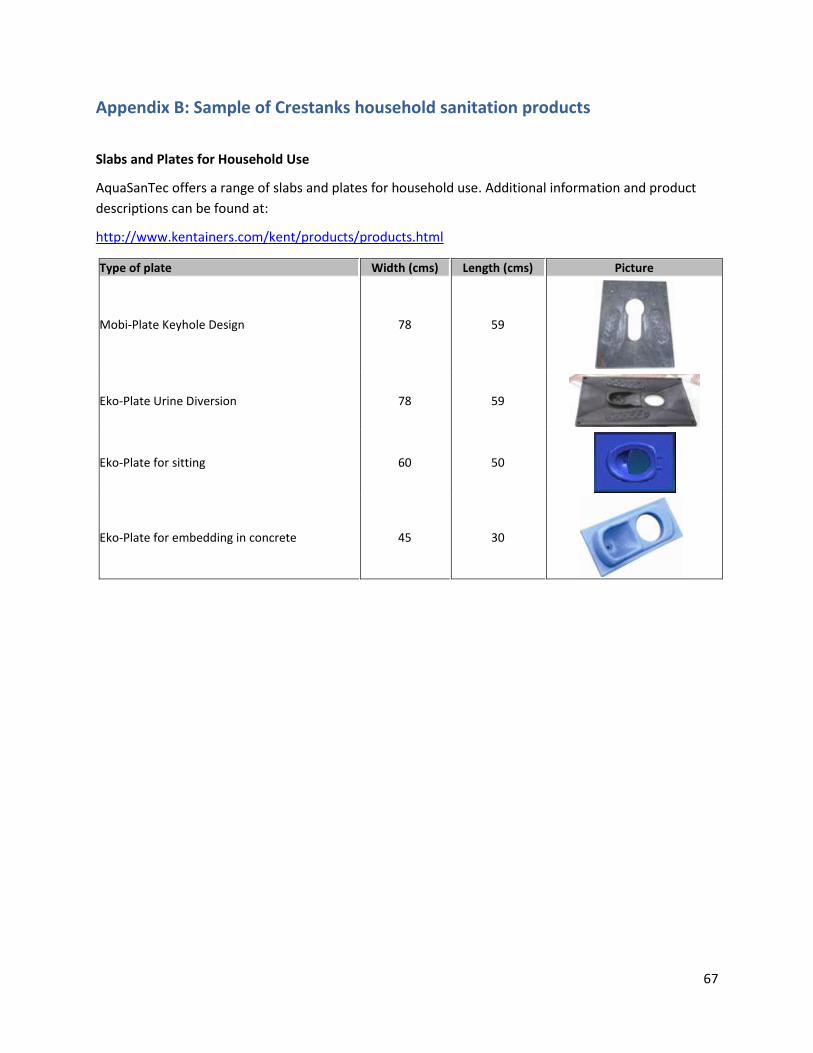

superstructures, waste storage tanks for latrines, and large septic tanks. More about these products can

be found in Appendix B. Prices for these products range from US$35 for a small latrine platform to

US$250 for a septic tank or US$400 for a complete modular latrine including superstructure and slab

(but not including any below-ground storage). Production capacity in the Kampala facility is fairly robust,

but it is not fully utilized at the moment for sanitation-related products due to low demand.12

Mr. N. Suresh, Crestanks’ General Manager, confirmed that the overall demand for their sanitation

products is low, with the company only having generated approximately US$750,000 to US$1 million in

sanitation-related revenue over the past five years. The majority of Crestanks’ sales of latrine products

are to government, NGOs, or religious organizations, while almost none are to consumers. Mr. Suresh

noted that he has been selling to NGOs for eight years now. Crestanks’ only real “outlet” for products

that get close to end users are small hardware shops in rural towns. The sales volume to these outlets,

however, is extremely low. Predominant customer groups in order of size are:

1. Schools

2. Refugee camps

3. Domestic customers (through commercial distribution channels; however, sales in this group are

virtually nonexistent)

7.3.2 Constraints: Pit digging and latrine construction materials

Households independently hire a porter to dig the pit and then hire a separate mason to construct the

latrine. Digging the pit is the first step in the construction process and seemingly the easiest to obtain

due to a large supply of porters. Since this process is not performed by the mason who builds the latrine,

there is a natural break in the momentum of the sales and construction process. One household in this

study, which was considered to be middle class, cited that they had dug a pit but then too much time

elapsed before construction started. The homeowner was concerned with the dangers of an open pit

and having children on site, and therefore decided to have the hole covered, stopping the installation

process. A lack of funds contributed to the decision to halt the process and led to the gap from pit

digging to latrine construction. It is possible that if she had known the total cost up front, she might have

not taken that first step. Alternatively, if a more reasonable pit standard were established, it might have

freed up enough funds to cover both pit digging and subsequent latrine construction. Tangential to this,

masons expressed concern with coming into the construction process and not knowing the details of the

pit digging. If a pit is not reinforced in a timely manner, and depending on the season, masons face the

danger of a pit collapsing. This is especially the case given that the standard guidance on pits across

much of the country stipulates a preferred depth of 15 feet or more. Thus, better pit standardization

and guidance could provide benefits from both a demand and supply perspective.

After the pit is dug, construction of the foundation and slab can commence once the household has

hired a mason and the materials are on site. Our interviews with masons demonstrate that households

do not trust them to buy their materials and therefore go directly to the hardware stores and other

12

Mr. Suresh noted that they can produce as many as 750 large latrine platforms per day, but the volume they currently produce is only a fraction of that.

31

suppliers for their latrine construction materials, cutting the mason out of the purchase process.13 This

situation is not ideal because in our observations, the mason is the only entity in the supply chain that

possesses accurate knowledge of what materials are needed in the appropriate quantity, yet is rarely

the one who make the purchases. Occasionally, a mason will give the household a shopping list, but the

household relies on the hardware store to give advice and guide the ultimate material decisions.

However, hardware stores are unable to always clearly and consistently articulate to the consumer what

items are needed to build the latrine, which can lead not only to missed sales opportunities, but to a

delay in the construction process. It can also contribute to households over-purchasing supplies

depending on whose advice they trust, or simply as a result of the overall lack of knowledge within the

supply chain. Masons cited frustrations with having to wait for the household to buy the materials

before they could start construction, often running into issues with not having the correct amount or

type of materials they need, or being unsatisfied or uncomfortable building with low-quality products.

Thus, the resulting quality of a finished latrine may depend more on the materials made available to the

service provider, rather than the service provider’s skills (USAID 2009). Moreover, if a household

purchases the materials in batches or pays in installments, this delays the construction process even

more.

As an added complication, most latrine materials such as cement, wire mesh, and nails are purchased at

the hardware store, but brick, sand, and stones must be purchased separately, and the study did not

uncover any mention of formal or informal connections between these entities.

When considering the total cost of installing an improved latrine, households may easily take into

account the sales prices of the components, but additional hidden cost barriers (e.g., time, effort, and

risk) can disrupt their purchase process. In the case of the current household latrine industry, a decision-

maker may become disconcerted with the process when they realize that they will need to hire a porter

and a mason, buy the materials themselves, and find a way to transport them to the worksite despite

the limited mobility and access they have to modes of transport as noted in Table 8. When the sales

process is disaggregated, a consumer is forced into too many decision points, which may progressively

discourage them from moving toward completion.

7.3.3 Opportunity: Standardized product offering

A critical first step for the household sanitation sector in Uganda is to focus on a specific product

offering for the target market (i.e., households in rural and small towns). While some evidence exists of

specific, complete latrine solutions such as Ecosan latrines offered through NGOs and Crestanks’ Ekoloo,

no simple all-in-one latrine package is currently available for low-income households. Thus, actors within

the supply chain, including households, masons, and hardware shops, must resort to unsystematic

means to resolve the challenges of constructing a latrine.

13

This was also the finding from a USAID study in 2009 in Tororo District, in which it was found that “most clients currently purchase the materials themselves, paying the contractor for labor only” (USAID 2009).

32

As noted above, product development research

need not produce something that is overly

complex, is technologically advanced, or offers an

endless array of options. For example, through

iterative product development research and design

utilizing locally sourced materials, International

Development Enterprises (iDE) in Cambodia was

able to develop the Easy Latrine as a simple,

affordable household latrine option (Figure 9).

Developed through a collaboration between iDE

and multiple partners including WSP, it consists of

a squat pan, concrete slab, prefabricated concrete

chamber, PVC pipe, and concrete rings to line the

pit. Key inputs into the design have helped to

drive down costs and make it easier for suppliers

to purchase the necessary materials and manufacture and transport at-scale. The result has been a

three-fold increase in the number of rings a local, small-scale concrete producer can make in a day (iDE

2011). The Easy Latrine retails at under US$35 and offers poor households—even those in remote, rural

settings—a simplified solution without having to procure or transport any materials themselves.

Limiting the complexity of the design helped iDE simplify the product marketing, sourcing, distribution,

and training, as well as reduce consumer “decision paralysis” about which materials to use for each part

of the latrine. Households may choose to upgrade their latrine with a superstructure on their own, but

the critical elements of safe waste containment are already accounted for in the Easy Latrine design.

Most importantly, it allows for a single product that can be “branded,” marketed, and sold. This allows

producers to create brand awareness and identity, and then sell that brand. This currently cannot be

done in Uganda since no latrine “brand” yet exists.

Development of a complete solution sourced from locally-made materials, such as the Easy Latrine,

along with a range of upgrade products for household latrines means that families would have the

option to consider incremental upgrades as well as more immediate ways to progress up the sanitation

ladder depending on their willingness and ability to invest in latrine improvements. Offering all of these

items under a single brand would help to increase awareness of sanitation solutions for low-income

consumers and build their confidence in being able to seek out appropriate products for their individual

needs and budget.

7.4 Distribution and service delivery

7.4.1 Current status

Materials for latrine construction, whether they are individual components or prefabricated products,

move through a relatively disaggregated supply chain to reach retail outlets and, ultimately, households

in rural and small towns. Stronger, more reliable linkages between supply chain actors currently only

exist within or around larger urban settings within the five study districts, which creates obstacles of

Figure 9. iDE Cambodia Easy Latrine.

33

logistics, lost time, and transport costs for small retailers, masons, and households further afield to

obtain materials for household sanitation.14

Small, local hardware shops basically serve as the primary outlet for all construction-related materials,

including those used for latrines. Most of these shops are located near established small towns or

settlements and operate on an independent basis, although the study found two instances of shops

operating as small franchises in Tororo and Arua districts. The majority of hardware shops surveyed

carry various permutations of inventory and charge differing prices for each type of product. It should be

noted, however, that no hardware shop within the study sample carried any plastic household latrine-

specific (e.g., plastic latrine slabs) products. More information regarding products found in the various

hardware shops from the sample and the corresponding prices of materials can be found in Appendix C.

In addition, nearly every hardware shop owner from the field survey indicated that prices they must pay

for materials often fluctuate, sometimes multiple times a day (e.g., for cement), which further

complicates their overall business operations.

About half of the hardware shops in the sample owned their own vehicles and used these to transport

materials to their shop for sale. The others either rented vehicles or found other means to transport

supplies to their shop. There were only a few instances in which hardware shops referenced suppliers

delivering products to their shops, and in those instances, it was only select products rather than entire

inventories. The shops must pay transport costs for products that are delivered. Some hardware shop

owners also mentioned purchasing stock from “roving salesmen” who sell products on the side of the

road. These “close-in” suppliers help them save transport costs but appear to be used on an irregular

basis.

Most hardware shops did not reference whether specific products were more difficult to source than

others, but a few noted that high demand for cement makes obtaining sufficient supplies rather

challenging. Several hardware shops expressed concerns over appearing to have stock-outs of certain

supplies and admitted to purchasing additional materials at retail price from other nearby hardware

shops just to maintain a minimum level of products for which they had sold out.

Delivery of materials from a hardware shop to a work site is only covered by the hardware shop for large

orders (e.g., for school or industrial sanitation projects and to a few wealthier households). Thus,

masons or individual households must assume the burden of arranging and paying for any transport of

latrine construction materials from hardware outlets to their plot. This is often done via boda-boda

motorcycle taxis for various rates and in stages as materials are often purchased piecemeal rather than

all at once. Table 13 provides a sample of rates quoted by hardware shops for the transport of cement

via boda-boda taxi.

14

This mirrors findings from WSP indicating that, although there are points of sale for sanitation facilities, they are mostly found in urban areas or small towns and not in rural areas (WSP 2011).

34

Table 13. Quoted rates from hardware shops for materials transport via boda-boda taxi.

District Capacity Distance Rate

Bushenyi respondent 1 4 bags of cement 4–5km 1,000 UGX

Bushenyi respondent 2 Not given 1km 3,000–5,000 UGX

Amuria respondent 1 Not given 1km 2,000 UGX

One reason why latrine construction materials are purchased in stages is that there is no known

standardized suggestion of necessary supplies among hardware shops, masons, or households. Masons

seem to hold a bit more knowledge about which materials are most useful for building a latrine

platform, for instance, but households seem to be much less aware and usually resort to asking masons

or hardware shop owners for advice. Meanwhile, hardware shop owners do not currently suggest any

“package” of latrine materials as most insist that every customer’s need is different and because

demand is currently so low. Hardware shop owners also noted that it can be difficult to tell what

customers plan to build with the materials they purchase as the supplies needed for a latrine are similar

to those required to construct a house or a grave. Regardless of the reasons behind a lack of promotion