61

Together we make a world of difference 2006: First Edition Sowing the Seeds of Change: Weaving Innovation and Integrity into Organic Agriculture

Together we makea world of difference

2006: First Edition

Sowing the Seeds of Change:Weaving Innovation and Integrityinto Organic Agriculture

Copyright © 2006 by Organic ExchangePrinted in the United States of AmericaFirst Edition

Extracts from this book may be reproduced for non-commercial purposes without permission, provided fullacknowledgement is given to the authors and publishersas listed.We do request you send us a copy of the relevant publication,article or website for our own reference purposes.

Organic Exchange5332 College Ave., Suite 203Oakland, CA 94618www.organicexchange.org

Together we makea world of difference

Sowing the Seedsof Change:Weaving Innovationand Integrity intoOrganic Agriculture

Acknowledgements:Thanks to the Organic Exchange Farm Development Team, Prabha Nagarajan, SilvereTovignan, Alfonso Lizárraga, and Kathleen Wood

Thanks to Dr Georg Birbaummer Of GTZ Paraguay; GTZ Paraguay who funded SimonFerrigno’s visit to Arasy in October 2005

And Alfonso Lizarraga Travaglini, of RAAA Peru and Organic Exchange Regional Coordinatorfor contributing to the introduction to the Peru section

Parts of this publication are adapted from the Organic Exchange Spring 2006 Fibre Report,by Simon Ferrigno, Organic Exchange: Oakland, 2006

Parts of the Africa section are adapted and extracted from 'Organic Cotton: a new developmentpath for African smallholders', Ferrigno et al., Gatekeeper Series 120, IIED: London 2006,by kind permission of the publisher, www.iied.org

Many thanks to the farmers whose stories we tell in this book and to the many otherfarmers whose stories we will tell in the future. Keep on growing!

Subhash Sharma, Sadashiv Devrao Korpe, Manish Sadashiv Korpe, Kapil Dev, AbhjitDevoke, Pradeep Bayaskar, Kapil Deoke, and others from Jainpur, Bala sahib Wankhedeand all the farmers from the group at Amla in the EcoFarms project, Maharashtra, India

Karshan Bai Choudary, Tulsi Bai Manji Bai Choudary, Narmada Ben Hari lal Choudary,Sathbir Singh ram Swarup Choudury, Wagji Rajabhai Walan, Parbhat Bhai, Savji Bhai inthe Agrocel project, Gujarat, India

The farmers of Chetna Organic, Andhra Pradesh, India

Organic Farms, India

In Benin, the farmers from Nizoumey, Michel Atekokale, Vigue Atekokale, Evelyne Atekokale,Colette Seque, Paul Atekokale, Gogan Atchodo, and the other farmers and residents inNizoumey, as well as Nicholas Abigognan, Vigue and Marcelline and others in Mangassavillage, two truly inspirational groups of farmers, and the farmers from the Pendjari parkarea, who will hopefully become organic soon

In Paraguay, Andres Garay, and other farmers and staff at Arasy, as well as staff andmembers of Altervida

In Peru, Rodolpho Piscoya and all the farmers of Moroppe and the APAEM association,as well as Liliana Llontop, a true field agent

Many thanks as well to those organisations and individuals who facilitated our fieldvisits and showed amazing hospitality:Helene Ecklin and Olga Segovia of Arasy, Paraguay, Dr Georg Birbaummer, GTZ Paraguay,Omprakash and Anand Mor, and staff at ECOFARMS, India, Hasmukh Patel and all atAgrocel, India, Dr CS Pawar, VRTI and University of Hyderabad, Arun Ambatipudi at ETCIndia and Gijs Spoor, ETC/Solidaridad, India, Simplice Davo Vodouhe, Delphine Bodjrenou,Laurent Glin and all at OBEPAB, Benin, Fabrice Vodouhe, Organic Benin, Karina Nikov,Bernard Agbo and all at GTZ Benin, as well as staff of the Pendjari Park Pro-CGRN project,James Vreeland and all at Peru Natuurtex, Peru, Gonzalo LaCruz, Oro Blanco, Peru

Thanks to all others who provided information and insights we have used:Bo Weevil, Netherlands, Dennis Ochwada, Kenya Cotton Growers Association, PaulDesmarais, Kasisi Agricultural Training Centre, Zambia, Pratiba Syntex, India, Joerg Johnand ENDA Pronat, Senegal, Jens Soth of Helvetas and staff at Helvetas Mali and BurkinaFaso, Altervida, Paraguay, Fundeca, Paraguay, Daniel Campos, Paraguay, SNV Kandi,Benin, Pilar, Olympic, and Lioplant, Paraguay, Oro Blanco, Peru, Stephan Bergman, theWhite Cotton Project, Peru, Esplar, Brazil, ICCOA, India, Remei, Switzerland, BioRe Tanzaniaand Maaikal BioRe, India, Pesticide Action Network UK, Afforest, Zimbabwe, PAN Togo, andRob Morrison of Leopold Ketel

The participants in the Organic Exchange regional workshops in Peru and Africa in April andJuly 2006 and participants at the ETC workshops and ICCOA India Organic seminars inIndia in November 2005, and to their sponsors and organisers, including OBEPAB, GTZBenin, ETC India, ICCOA and Hialpesa

I hope I have not forgotten anyone, and apologise if this is the case. Any other errors oromissions are the responsibility of the author! And thanks to Heidi, for having the vision topush this project.

Thanks to the Farm Development Program donors:

This publication funded by ICCO, with many thanks.

Sowing the Seeds of Change: Weaving Innovation and Integrity into Organic Agriculture

Author: Simon Ferrigno with support from Prabha Nagarajan (India section) and AlfonsoLizarraga Travaglini (Peru)Editor: Heidi McCloskeyPhotographer: Simon FerrignoDesigner: Peter Rossing

Table of Contents

Breaking withConvention:Making an ImpactOne Fibre at a Time

I. Global Overview: “Breaking with Convention:Making an Impact One Fibre at a Time” 1

1. Tradition or Innovation? 22. Organic Cotton in 2006 32.1. A Look at Global Organic Cotton Production 32.2. Regional Changes 5

II. Africa 7III. India 21IV. Latin America 37V. Ensuring Supply: Considerations

for Brands and Other Investors 53VI. Contacts 54

The growth of the organic cotton sector has been considerable over the pastfive years. The positive environmental and social benefits at the farm level havebecome increasingly apparent to non-governmental organizations, government bodiesand brands while becoming of greater importance to the general public. No longeris organic cotton a story of lower yields for higher incomes; it’s a story of innovationand discovery. It’s a story that is just beginning – one that clearly demonstrates thehealthy alternatives to conventional agriculture that do not involve the use of harmfulchemicals.

For many early innovators in the organic movement, there was nothing quite likeexperiencing firsthand the contrast between conventional farmers who live day today under a mountain of debt and health problems, and organic farmers who empowerthemselves and their families within a few short years and develop amazing joy,humour, and confidence in their ownership of a healthy, collaborative solution.

1

1. Tradition or Innovation?In the not-so-distant past, farming without syntheticchemicals was considered to be the standardmethod of farming and was practised around theworld for hundreds of years before the advent ofmodern agricultural chemicals. After syntheticchemicals were introduced to farmers, old farmingmethods were quickly subsumed by what is nowtermed “conventional” farming. Farmers saw andenjoyed a seemingly easy way to eradicate insects,weeds and other pests. What conventional farmingfailed to consider were the short, medium and longterm effects of chemical exposure on people andthe environment. As the effects of agriculturalchemical exposure have not been well documenteduntil fairly recently, the conventional cotton industryhas easily been able to position modern organicfarming as the same traditional, untried, unstable,and unaffordable production system, unable toprovide adequate fibre volume to meet customerdemand, despite its many success stories.

While that position has provided a convenientmethod of promoting conventional cotton fibre formany years, more and more brands have becomewell versed and highly experienced in social andenvironmental responsibility, including specificareas like textile chemistry and farming practices.Equipped with this knowledge, brands and theirsupply chains are now able to make informedsourcing choices. The choice to use organic versusconventional cotton is just that: a choice. But it’sone that, like organic farming, works with instead

of against nature and one that aligns with theevolving environmental and social values of anincreasing number of brands, organisations andconsumers.

Organic farmers are true innovators in today’sagricultural world, often working with extremelylimited funds, without sophisticated scientists andlaboratories and without ready access to orinfluence on corporate boardrooms. Even withthese limitations, they produce high quality foodand fibre without damaging their productive base.These farmers often achieve impressive results inwater conservation (see examples in the Indiasection) and the restoration of soil fertility, anddevelop an intimate understanding of how theircrops interact with the wider farm environment.

Organic farmers usually achieve higher incomesthan their conventional counterparts. On a trip toIndia in 2006, Organic Exchange staff asked sevengroups of farmers to compare their experiencesbefore and after transitioning to organic cotton withregard to income, personal health, environmentalhealth, and social development. Six farm groupsreported much higher incomes and similar or higheryields per acre. The seventh farm group reportedthe same level of income as with conventional, butlower health costs from reduced exposure topesticides.

One of these groups has also developed asuccessful water harvesting and conservationsystem, generating hundreds of thousands of litresof water each year, which provides more thanenough for its irrigation needs (see India section).

Sowing the Seeds of Change: Weaving Innovation and Integrity into Organic Agriculture

The organic crop yields reported in this bookcurrently include farmers in conversion, whichoccurs over a period of three years, and thus mayseem lower than conventional yields. A quick glanceat accomplished organic farmers tells a differentstory. Experienced, innovative organic farmersachieve similar or higher yields, although manychoose to emphasise diversity of crops, and thusmore secure income, over a single cash crop.

An extensive review of yields over time might alsoshow that organic fields stay productive longer andthat after five to seven years, most organic cottonfarmers obtain similar yields as conventionalfarmers.

2

2. Organic Cotton in 20062.1. A Look at Global OrganicCotton ProductionThe global organic cotton fibre supply has increased292% 1 from a 2000-01 harvest of 6,480 metric tonnesto the 2004-05 harvest of 25,394 metric tonnes.Supplies are projected to grow to 31,017 metrictonnes (68,237,400 pounds or 142,161 bales) by theend of the 2005-06 harvest, reflecting an annualgrowth rate of 22%.

During the 2004-05 harvest, cotton was produced intwenty-two countries with Turkey growing 40%, India25%, the United States 7.7% and China 7.3%respectively. In 2005-06, these four countriescombined are projected to produce 79% of the globalorganic cotton fibre crop.2

All existing organic cotton producer groups areexpected to maintain or slightly expand productionfor the 2006-07 harvest, and a small number of newprojects growing cotton for the general market areexpected to begin organic production in 2006-07.Additional projects that currently grow cottonexclusively for specific customers are expected toexpand their customer base beginning with the 2007-08 harvest.

Organic cotton fibre supply and demand has gonethrough several phases of development in the pastfifteen years. These phases included: enthusiasticgrowth in the early 1990s, re-orientation in the earlyto mid 1990s, then the laying of a more structuredand professional approach in the late 1990s andearly 2000s.3 The current phase of developmentshows increased organic cotton production and trade,

improved supply chains and fibre quality and rapidgrowth in demand.

The first phase of organic fibre production began inthe United States and Turkey in the late 1980s.4

These countries were soon followed by Sub-SaharanAfrica, predominantly Egypt and Uganda, India, and

Global Overview

1. See Organic Exchange 2006 Spring Fibre Report for more information2. Ibid3. Ton, 2002, Myers and Stolton 19994. Ton, 2002

1992-2001 Organic Cotton Production Worldwide by Country (in metric tonnes)

Source: Ton (2002) updated in Ferrigno et al., 2006

Argentina - - 75 75 - - - - -Australia 500 500 750 400 300 300 - - -Brazil - 1 5 1 1 1 5 10 20Benin - - - - 1 5 20 20 30Egypt 50 150 600 650 625 500 350 200 200Greece - - 300 150 125 100 75 50 50India 200 250 400 925 850 1,000 825 1,150 1,000Israel - - - 50 50 20 140 180 530Kenya - - - - - 5 5 5 -Mozambique - - - 100 75 50 - - -Nicaragua - - 20 20 20 20 - - -Paraguay - 100 75 50 50 50 - - -Peru 200 675 900 900 600 650 650 500 550Senegal - - - 1 10 10 50 125 200Tanzania - - - 10 100 100 100 200 250Turkey 125 200 600 725 850 1,000 1,200 2,000 1,750Uganda - - 25 75 300 450 250 200 275USA 1,000 1,950 2,400 3,350 1,550 1,300 1,900 2,900 1,625Zimbabwe - - - - - 1 5 5 -Total in 2,075 3,826 6,150 7,482 5,507 5,562 5,575 7,545 6,480Metric TonnesTotal in Bales 9,510 17,535 28,188 34,292 25,240 25,493 25,552 34,581 29,700

1992-93 1993-94 1994-95 1995-96 1996-97 1997-98 1998-99 1999-2000 2000-01

Conversion Note: 2,200 pounds are in a Metric Tonne,and 480 pounds in a bale.

Peru. Some production was initiated bycompanies seeking to create new models ofdoing business; some were started by farmersseeking new markets and better ways of living; andseveral were started as development projects by anassortment of non-governmental organizations.

3

2004-05 Organic Cotton Stocks and Fibre Production by Country(in metric tonnes)

Benin 199 67 230 36 0.26% Medium*Burkina Faso 0 45 30 15 0.18% MediumKenya 0 2 0 2 0.01% MediumMalawi 0 0 0 0 0.00% —Mali 0 296 296 0 1.17% MediumSenegal 5 27 14 17 0.11% MediumTanzania 0 1,213 1,213 0 4.78% MediumTogo 0 0 0 0 0.00% MediumUganda 400 900 500 800 3.54% MediumZambia 0 2 0 2 0.01% MediumZimbabwe 0 0 0 0 0.00% MediumIndia 930 6,320 5,213 2,037 24.89% MediumPakistan 0 600 600 0 2.36% MediumIsrael 0 436 436 0 1.72% MediumEgypt 0 240 240 0 0.95% ELS**Nepal 0 0 0 0 0.00% Short***Kyrgyzstan 0 65 65 0 0.26% MediumChina 20 1,870 1,470 420 7.36% MediumParaguay 34 70 70 34 0.28% MediumPeru 100 813 775 138 3.20% Medium & ELSTurkey 0 10,460 10,460 0 41.19% MediumUSA 0 1,968 1,968 0 7.75% Medium & ELS

Total 1,683 25,394 23,580 3,502 100.00%

% OFPRODUCTION

BEGINNINGSTOCK

AUGUST 1HARVEST SALES /

COMMITMENTSENDINGSTOCK

FIBRETYPE

Southeast Asia 2,037.00 10,834.86 11,835.00 1,036.86 34.93%(Pakistan/India)Middle East 0.00 10,760.00 10,700.00 60.00 34.69%(Turkey, Israel)China 420.00 2,531.60 2,630.00 321.60 8.16%Other Africa 804.38 2,469.60 2,859.00 414.98 7.96%North America 0.00 1,867.64 1,868.00 0.00 6.02%(USA)Latin America 172.00 1,188.00 1,035.00 325.00 3.83%Africa CFA zone 68.50 1,014.95 1,049.00 34.45 3.27%North Africa 0.00 240.00 240.00 0.00 0.77%CIS 0.00 110.00 110.00 0.00 0.35%(Commonwealth ofIndependent States)EU, Central Europe 0.00 0.00 0.00 0.00 0.00%Central America 0.00 0.00 0.00 0.00 0.00%East Asia / Australia 0.00 0.00 0.00 0.00 0.00%

Total in Metric Tonnes 3,501.88 31,016.65 32,326.00 2,192.89 100.00%

Total in Bales 16,050.28 142,159.65 148,160.83 10,050.75

% OFPRODUCTION

BEGINNINGSTOCK

AUGUST 1HARVEST SALES /

COMMITMENTSENDINGSTOCK

2005-06 Organic Cotton Stocks and Fibre Production by Region(in metric tonnes, predicted)

Sowing the Seeds of Change: Weaving Innovation and Integrity into Organic Agriculture

4

* Medium Staples are 24-30mm in length.** ELS stands for Extra Long Staples such as Tangus, Pima and Egyptian with staple

lengths over 30mm.*** Short Staples are less than 24mm.

2.2. Regional Changes

On a regional level, major organic productionincreases have occurred from highest to lowestrespectively in Southeast Asia (India and Pakistan)at 692%; the Middle East (Turkey and Israel) at478%; and Africa at 403%.

Other regions have also seen growth with thelowest recorded data in North Africa at 120%followed by North America at 121%. Growth inAfrica has been mostly in East Africa in the non-CFA* region where conventional cotton productionis simultaneously decreasing.

Based on current projections, the Southeast Asiaregion will overtake the Middle East as the leadingproduction region in 2005-06, with China overtakingAfrica’s non-CFA region as the world’s third largestproducer of certified organic cotton.

Some countries, Greece in particular, haveappeared to cease organic cotton production. Newproduction countries include Pakistan andKyrgyzstan along with African countries Mali,Burkina Faso, Togo, Kenya and Zambia. BothTanzania and Uganda have seen major growth.In Latin America, production is now underway againin Paraguay. China is now also a major organiccotton grower, and organic cotton trials in Spainare commencing in 2006.

Global Overview

5

* CFA refers to the CFA Franc Zone including Benin,Burkina Faso, Mali, Ivory Coast, Togo, Niger, and otherFrancophone West and Central African Countries.

Together we makea world of difference

Africa

Organic cotton projects in Africa combine innovative approachesto farmer participation with strong social programs, an attention tofibre quality, and a diversity of interesting cultures and productionareas, offering unique products and programs for a variety ofcompanies.

While each project is different, visitors to organic cotton farms willalways see amazing colour, traditional dress and smiles, and willoften be greeted, quite literally, with a song and dance about organiccotton.

Communities at theHeart of Organic CottonFarming in Africa

1. Cotton in Africa 82. History of Organic Cotton in Africa 93. Sourcing Potential in Africa 104. Focus on Benin 154.1. Nizoumey Village 164.2. Benin Supply Chain Map 184.3. Rotation Crops 184.4. Proposed Pendjari Production Project 195. Processing and the Future:

Cotonou Workshop July 2006 20

7

1. Cotton in Africa †

Cotton is an important cash crop for many Africancountries. It accounts for 50% to 70% of exportrevenues in Benin and is the second largestexport earner in Tanzania1. Some 10 millionpeople in Central and West Africa depend oncotton revenues2. However, African cottonexports are affected by subsidies paid by theUnited States, European Union and Chinesegovernments, a practice that undermines worldmarket prices3 . It also increases the impactsof agrochemicals on human and environmentalhealth4. According to a global study, cotton uses22% of all insecticides applied in agriculture and11% of all pesticides5.

Because of these economic pressures, manyAfrican smallholders are being driven to themargins of economic viability or out of cottonaltogether with few alternative cash crops6.

While conventional cotton production hascontributed positively to economies in sub-Saharan Africa7, it has not been cost-free8.Synthetic inputs (fertilisers and pesticides) needto be bought on credit (deducted from a farmer’searnings after harvest); farmers gamble ongaining sufficient yields to pay for the inputs,and conventional farming practices damageecosystems and human and animal health9. Inaddition, food security is reduced10, andliberalisation exposes producer countries and

farmers to unstable world market prices, whichfor decades have been fluctuating but generallydeclining11.

African cotton production is based on smallholderfamily farming. In West Africa, units averageeight to nine people who farm ten or fewerhectares12. The same pattern is true for organiccotton farming, with a tendency for the smallestand poorest farmers to be more represented13.

1. Ton, 2002a2. Watkins, 20023. Linard, 2002; Goreux, 2003; Watkins, 20024. Ton, 2002a; PAN UK, 2003; Williamson, 2003a5. Allan Woodburn Associates, 19956. PAN UK, 2003; Ton, 2002a7. Ton, 2001; Minot and Daniels, 20028. Ton, 20019. Ton, 2001

10. PAN UK, 200311. Gibbon, 200112. Minot and Daniels, 2002; Toulmin and Gueye, 200313. Ton, 2002a

i. For a more detailed view of cotton in Africa as wellas a history of organic cotton in Africa, see Ferrignoet al., Organic Cotton: a new development path forAfrican smallholders, Gatekeeper Series 120, IIED:London 2005, from which this section is extracted.

Breaking with Convention: Making an Impact One Fibre at a Time

8

2. History of Organic Cotton in AfricaOrganic cotton production began in 1994 in Tanzaniaand Uganda, with Senegal and Zimbabwe joiningin 1995 and Benin in 1996. Organic production alsorecently started in Togo, Kenya and Zambia.

Organic cotton production in Africa continues to bestrong, and is over three times higher now than in2000-01. Production is still concentrated mostly inthe East; however, production in West Africa hasgrown, especially in Mali, through support from buyers

trading company, may restart organic cottonproduction.

A small project in Togo is ongoing, with 300 farmerstrained, although the fibre is currently uncertifieddue to lack of both funding and buyers.

New production and trials have begun in Zambiaand Kenya. Production is also planned in Malawi.A small number of uncertified producers remain inZimbabwe together with a support structure thatalso trains other producers in Southern Africa.Senegal, while still producing little organic cotton,has the potential to transition 2,000 hectares, alreadycertified organic for other crops, to organic cotton.

in Switzerland, while production in Benin hasbecome more secure and has gained access toexport markets through new ties with buyers andthe creation of a new trading company. Another newfactor in Africa is the growth of Fairtrade cotton,beginning in Senegal and extending now to Mali.Some of the Fairtrade cotton is jointly certified asorganic. Thus far, only one project in Senegal hasceased organic cotton production since 2000-01.

Tanzania is currently the largest producer in Sub-Saharan Africa, ahead of Uganda. In Uganda, anew project, NOGAMU, is promoting organic cottonproduction in traditional cotton growing areas suchas Kasese and West Nile. Outspan, a Ugandan

2004-05 Organic Cotton Stocks and Fibre Production in Africa(in metric tonnes, CFA Zone = West African Franc Region)

Benin 199 67 230 36 15%Burkina Faso 0 45 30 15 10%Mali 0 296 296 0 68%Senegal 5 27 14 17 6%Togo 0 0 0 0 0%Total 204 435 570 68 100%

% OFPRODUCTION

AFRI

CACF

A ZO

NE

BEGINNINGSTOCK

AUGUST 1HARVEST SALES /

COMMITMENTSENDINGSTOCK

OTH

ERAF

RICA

Kenya 0 2 0 2 0.09%Malawi 0 0 0 0 0%Tanzania 0 1,213 1,213 0 57%Uganda 400 900 500 800 43%Zambia 0 2 0 2 0.09%Zimbabwe 0 0 0 0 0%Total 400 2,117 1,713 804 100%

Benin 36 58 94 0 6%Burkina Faso 15 200 200 15 20%Mali 0 722 722 0 71%Senegal 17 33 33 18 3%Togo 0 2 0 2 0%Total 68 1015 1049 35 100%

% OFPRODUCTION

AFRI

CACF

A ZO

NE

BEGINNINGSTOCK

AUGUST 1HARVEST SALES /

COMMITMENTSENDINGSTOCK

OTH

ERAF

RICA

Kenya 2 6 0 8 0%Malawi 0 4 0 4 0%Tanzania 0 1336 1336 1 54%Uganda 800 1100 1500 400 45%Zambia 2 23 23 2 1%Zimbabwe 0 0 0 0 0%Total 804 2469 2859 415 100%

2005-06 Organic Cotton Production Projections and Stocks in Africa(in metric tonnes, CFA Zone = West African Franc Region)

Africa

9

Breaking with Convention: Making an Impact One Fibre at a Time

Zambia

HUB 1

Uganda

Tanzania

Kenya

Mozambique

Zimbabwe

South AfricaLesotho

Mali

Senegal

HUB 2

HUB 3

HUB 4

10

3. Sourcing Potential inAfricaThere is strong organic cotton expansionpotential in several countries that are looselycentred around two continental hubs, East andWest, each with two distinct geographicalregions, as follows:

East Africa:Hub 1: Uganda, Tanzania, Kenya, ZambiaHub 2: Zambia, Mozambique, Lesotho, South

Africa, Zimbabwe

West Africa:Hub 3: Benin, Burkina Faso, Togo, Ghana,

Nigeria, CameroonHub 4: Senegal, Mali

note:The capacity and growth of these hubs arediscussed in more detail in the following sections.All growth projections are based on the need tosimultaneously increase production and the capacityof projects to deliver continued support and trainingto farmers while developing their management andmarketing capabilities. The estimates used hereare minimum estimated potential growth. The morehuman and financial capital that is invested, thehigher production can grow.

Nigeria

CameroonBenin

Ghana

BurkinaFaso

Togo

East Africa Hub 1:Uganda, Zambia, Kenya,Tanzania

Fibre ProductionUganda currently has the largest number of bothexisting and prospective organic cotton farmers.Since 1994, 15,000 farmers have been growingorganic cotton and sesame in the northern regionof Lira. Two other projects in the same area haveproduced organic cotton in the past or plan to doso, and one company, Phenix Logistics, alreadymanufactures organic cotton garments.

Some processing also exists in Kenya, where organic

Conservative Estimate for Additional Organic CottonFibre Production, 2010-11 (in metric tonnes)

Africa

cotton fibre production is now in its second year.

Tanzania is currently the largest producer of organiccotton fibre in this hub; however, the group organisingthis project has high demand and all cotton producedis processed through their supply chains. This makesit difficult for companies who design their ownproducts and utilize a set supply chain to accessthis fibre supply. Currently this can be negotiated ona case by case basis and may change in the future. A second project set up in Tanzania has so farfailed to properly get off the ground.

Zambia can be counted in either East African hub,as it is possible for its fibre to be processed in eitherKenya or Uganda. Zambia is another new project,with highly promising early results in yields.

Uganda 300.00 600.00 600.00 700.00 700.00 700.00Zambia 23.00 100.00 200.00 250.00 300.00 350.00Kenya 5.00 20.00 50.00 100.00 150.00 200.00

Total 328.00 720.00 850.00 1,050.00 1,150.00 1,250.00

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11

A conservative estimate for this hub is thata further 1,250 tonnes of organic cottonfibre could be sourced from this region by the 2010-11 growing season.

A higher estimate for organic cotton production basedon sufficient investments, appropriate contracts andpre-financing for farmers could see over 7,000 metrictonnes of fibre produced. This is based on potentialgrowth rates of existing projects coupled with thedevelopment of some new projects and does notrepresent the region’s full capacity.

Of the various existing projects, Lango in Ugandais thought to be applying for Fairtrade status, andothers have the potential to aim for this.

Actors in Hub 1

Bo Weevil Uganda/Netherlands

Lango Organic Cotton Ugandapromotion

Phenix Logistics Uganda

NOGAMU Uganda

EPOPA Uganda

KATC Zambia

Cotton Growers Union Kenya

Wildlife Works Kenya/USA

Chresma Kenya

ACTOR COUNTRY FARM TRADER / SPINNER MANUFACTUREREXPORTER

11

note: Farms aside, this table onlylists those actors mentioned inthis document. For a morecomprehensive list see OrganicExchange's Sourcing Guide.

Conservative Estimate for Additional Organic CottonFibre Production, 2010-11 (in metric tonnes)

East Africa Hub 2:Zambia, Mozambique, Lesotho,South Africa, Zimbabwe

Fibre and Textile ProductionThis hub can also include Zambia, as can Hub 1.While we have no current information about Zambia'stextile industry, past surveys by Pesticide ActionNetwork UK indicated several potential companies

Breaking with Convention: Making an Impact One Fibre at a Time

East Africa Hub 1:Uganda, Zambia,Kenya, Tanzania

Processing and transportBesides being one of the largestorganic cotton fibre producers inAfrica, Uganda also has the mostadvanced fibre processing industry,with Phenix Logistics producingorganic cotton garments for the localmarket. Kenya's organic cotton couldeither be processed completely inKenya or spun in Uganda and wovenin Kenya. Zambia is a newcomer toorganic cotton production with greatpromise, and would be a central partof any East or Southeast African hub.It is possible also that some spinningcapacity could be developed basedon customer demand.

Neither Uganda or Zambia have seaports, so processed yarn and rawfibre would need to betransported to Tanzania orKenya for shipping.

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11

Zambia 23.00 100.00 200.00 250.00 300.00 350.00Mozambique 0.00 50.00 100.00 200.00 300.00 300.00

Total 23.00 150.00 300.00 450.00 600.00 650.00

Actors in Hub 2

that could produce organic cotton textiles.

Mozambique has not yet begun production but hasa lot of promise. Furthermore, production could restartin Zimbabwe, particularly once the political situationchanges. Production potential also exists in SouthAfrica.

In terms of fibre production, this hub is still in itsdevelopment phase, but we estimate it could eventuallysupply 650 tonnes of organic cotton fibre, andpossibly more if Zimbabwe comes back into play.

12

KATC Zambia

Auxmoz MozambiqueFarmholdings

African Organic South AfricaFarming Foundation

Afforest Zimbabwe

ACTOR COUNTRY FARM TRADER / SPINNER MANUFACTUREREXPORTER

note: Farms aside, this table only lists those actors mentioned in this document. For a more comprehensive listsee Organic Exchange's Sourcing Guide.

Conservative Estimates for Additional Organic CottonFibre Production, 2010-11 (in metric tonnes)

Africa

West Africa Hub 3:Benin, Burkina Faso, Togo,Ghana, Nigeria, Cameroon

Fibre ProductionHub 3 in West Africa is the most promising forvolume production after Hub 1 and also hasgreat spinning potential over the long term.Benin and Burkina Faso are the leadingproducers in the region, with Benin havingspinning and finished product manufacturingfacilities for personal care and apparelproducts. Benin has also established a

company to handle the marketing,manufacture and export of organic cottonproducts. Current production in Burkina Fasois handled through the Swiss non-governmental organization (NGO) Helvetasfor a range of Swiss clients. Burkina Fasohas manufacturing potential, particularly inhand-woven textiles.

In Benin, a rapid increase in production isbeing prepared around the area of the PendjariNational Park, for which Organic Exchangewill help find markets. The GermanDevelopment Agency GTZ and OBEPAB aredeveloping the programme on the ground.

This project will explicitly marry theprotection of a wildlife reserve with povertyreduction.

Togo has produced a small quantity of organiccotton, and has some limited hand-wovenprocessing capability. Nigeria is a potentialproducer at present, as is Ghana. Cameroonbegan small experimental production in 2006.

Actors in Hub 3

2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11

Benin 5.00 10.00 50.00 100.00 200.00 400.00 600.00Burkina Faso 30.00 100.00 200.00 250.00 300.00 350.00Nigeria 0.00 0.00 10.00 50.00 100.00 150.00Togo 2.00 10.00 50.00 50.00 75.00 100.00Ghana 0.00 0.00 10.00 50.00 100.00 100.00Total 5.00 42.00 160.00 370.00 600.00 975.00 1,300.00

OBEPAB Benin

Organic Benin Benin

CBT/COTEB Benin

GIETEX Benin

GTZ Benin/Germany

OPCB Burkina Faso

Helvetas Burkina Faso

PAN Togo Togo

Capsard Ghana

Sodecoton Cameroon

ACTOR COUNTRY FARM TRADER / SPINNER MANUFACTUREREXPORTER

13

note: Farms aside, this table onlylists those actors mentioned inthis document. For a morecomprehensive list see OrganicExchange's Sourcing Guide.

Conservative Estimate for Additional Organic CottonFibre Production, 2010-11 (in metric tonnes)

Breaking with Convention: Making an Impact One Fibre at a Time

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11

Senegal 20.00 400.00 500.00 600.00 600.00 600.00Mali 10.00 50.00 100.00 200.00 300.00 400.00

Total 30.00 450.00 600.00 800.00 900.00 1,000.00

West Africa Hub 4:Senegal, Mali

Senegal has been producing organic cottonsince 1994 and now produces both certifiedorganic and Fairtrade cotton, as does Mali.Both have great production capacity.

Senegal has high-end garment productioncapacity for small-volume orders as wellas spinning capacity and is also the exportroute for Malian fibre.

Actors in Hub 4

Helvetas Mali

CMDT Mali

ENDA Pronat Senegal

Cotonneierre du Cap Vert Senegal

Aissa Dionne Textiles Senegal

ACTOR COUNTRY FARM TRADER / SPINNER MANUFACTUREREXPORTER

14

note: Farms aside, this table only lists those actors mentioned in this document. For a more comprehensive listsee Organic Exchange's Sourcing Guide.

West Africa Hub 3:Benin, Burkina Faso,Togo, Ghana, Nigeria,Cameroon

Processing and transportBenin has an excellent port andshipping already takes placeworldwide. Benin also centralisesfibre and textile exports for BurkinaFaso, Togo and Nigeria. Benin hasspinning and some manufacturingcapabilities. Both Ghana and Nigeriahave potential organic processingcapacities in the long-term bytransitioning existing conventionaltextile production.

14. Ferrigno et al., Organic Cotton: a new developmentpath for African smallholders, Gatekeeper Series 120,IIED: London 2005

Africa

4. Focus on Benin

In 1996 two organic cotton projects began inBenin in the central and northern regions,originally managed by the NGOs OBEPAB(Benin) and SNV-Kandi (Netherlands)respectively. OBEPAB has since taken overthe SNV project. By 2001 there were over 300farmers in both projects, and nearly 800 farmersby 2003. Seed cotton production was 72 tonnesin 2001 and 240 tonnes in 2004. As of 2006,some 1,100 farmers are now planting organiccotton.

Yield averages have fluctuated from as low as271 kilograms per hectare (kg/ha) in 1997-98,when organic cotton was affected by outbreaksof aphids that also decimated conventionalproduction, to 562kg/ha in 1999-2000. Yieldaverages do not reflect the good performanceby experienced organic farmers and arelowered by incoming farmers as well as byother circumstances such as weather or pestoutbreaks, both of which affect the conventionalsector.

OBEPAB has recently began using a variationof the Farmer Field School approach wherefield agents and farmers use the fields as thelearning venue and jointly undertake research.

This supplements the work of the field agentsand improves farmer capacities in pest andsoil fertility management and research.Recently, the Beninese Institut National desRecherches Agricoles (INRAB) has becomeinvolved in soil fertility research and thegovernment council of ministers endorsedthe 2002 African Organic Cotton conferenceheld in Cotonou 14.

15

4.1. Nizoumey Village

Farmer Profile – Michel Atekokale:“Organic cotton rewards like a well caredfor baby. When it is done well, it gives goodrevenues and leads us to better times,”

says organic cotton farmer, Michel Atekokale,who has six children in school. Thanks to thebenefits of farming organic cotton, two of themhave been able to study and pass the BEPC thisyear, a designation similar to the UK GCSE orgraduation from Junior High in the United States.His ambition is to see all of his children graduateand then go to university. The oldest, Janvier,wants to study physics, and is about to leave forcollege/high school to study for a D stream orscience Baccalaureate.The income from organic cotton, which is higherthan for conventional cotton, means that theycan rent a house in town for the children inschool. Michel has also built a large house inhis home village for his children, and has boughtbicycles for his school age children. The collegeto which his children are being sent is 35-40kilometres away in Nbega.Michel vows to continue farming organic cottonas long as it is viable. This year he planted fourhectares and will most likely plant one more.His yields have been as high as 1,200 kg/ha,and he hopes for better rain this year, as lastyear’s was poor and negatively impacted his

Breaking with Convention: Making an Impact One Fibre at a Time

16

crop. Michel has been an organic farmer for sevenyears.

There are now twenty organic farmers in Nizoumeyvillage, fifteen having started originally seven yearsago.

This year the village organic cotton association,along with the state, paid the contributory costs fora community well. In previous years, the higherincomes from organic cotton have been used tobuild a health centre and dispensary in the village,and has allowed individual women farmers likeEvelyne Atekokale to celebrate the independencethat the income gives them within the household.

Farmer Profile – Vigue Atekokale:Another woman farmer, Vigue Atekokale, saysshe now makes a significant contribution to bothher family and community:

“When done well, organic cotton revenue isnot bad. It allows me to help my husbandwith the children's needs and look after myown as well, and it helps with family well-being and love.”

It has also allowed her to independently look afterher own self-development, purchase clothing forherself, and buy a motorcycle for one of her sonswho now earns income as a motorcycle taxi driver.She has also been able to purchase new bicyclesfor three of her children who are away at school.Last year she planted one hectare of organic cotton.

Africa

In previous years, one hectare earned herbetween 120,000 and 200,000 CFA francs(between US$ 220 and 360), for a yield of between570 and 1,000 kilograms per hectare. She hasbeen an organic cotton farmer for six years.

Farmer Profile – Colette Segle:Colette Segle says,

“Organic cotton is especially good for womenas there are no more poisonings, and I getmy own income as opposed to conventional.”

The revenue has allowed her to look after herchildren, send them to school, and improve herpersonal financial situation. This year her familyhas sowed organic seeds again and are happywith the earnings they expect to have. They haddebts incurred from conventional farming thatshe can now pay back. She started farmingorganic cotton six years ago and has planted halfa hectare so far already, with more to come. Her

yield last year was 600 kilograms perhectare, which was very high consideringshe thought it was a bad year!

Paul Atekokale says that he values organiccotton as

'We are paid immediately with no longdelays like in conventional.”

He has bought a bicycle so that he can sell hisrotation crops in markets outside the village.

Gogan Atchodo says,

“Organic cotton means you have yourown money; it's beneficial, especiallythe work. The revenue means one cando things like build houses. I have alsogot a pen for my livestock.”

Gogan has also built a house in his home village,which is 30 kilometres away in Nbega.

Organic cotton fibre production in Benin couldeasily reach 200 tonnes of fibre by 2008-09.

17

4.2. Benin Supply Chain MapBenin has changed radically over the past twoto three years in terms of its market links andits capacity to move beyond fibre productionand export to processing. Ginning in West Africahas always been world class, but now they’redeveloping spinning and manufacturingcapabilities.

The first ingredient for change was set whenthe NGO OBEPAB linked up with French investorBIOCOTON and several local companies toestablish a joint-venture trading company,Organic Benin, which now handles processingand exports and liaises with buyers. Around thesame time in late 2004, successful trials hadtaken place with local companies including thespinner, CBT, weaver, COTEB, and local designand production company, GIETEX.

Ginning in Benin takes place in the Sonaprafactories of Bohicon and Kandi. Both factorieshave high ginning outturns of over 40% (ratioof fiber to seed and trash). The Bohicon andKandi factories have a daily capacity of 80 tonnesper day each.

There are also four spinners, including the semi-industrial GIETEX, the Compagnie Béninoisede Textile (CBT, industrial), Echoppe (artisanal)and SASAO. CBT has the capability ofconverting 4,000 tonnes of fibre per year toyarns and fabrics. All fabrics produced through

Organic Benin are made with 100% combedyarn.

CBT also manufactures finished goods. Arange of small manufacturing units is beingorganised by Organic Benin and BIOCOTON. Echoppe also manufactures both garmentsand textiles.

4.3. Rotation cropsAvailable rotation crops in Benin include:

Cashew nuts: 50 tonnes per year. The nutscan be shelled by a locally based Dutch-Beninese company.Groundnut/peanut: 25 tonnes per yearMaize: 100 tonnes per yearShea nut and shea nut butter

Breaking with Convention: Making an Impact One Fibre at a Time

18

Africa

4.4. Proposed PendjariProduction ProjectAs well as the current and potential fibreproduction mentioned previously, furtherincreases in production could come from theproposed organic cotton farming area aroundthe Pendjari National Wildlife Park, in NorthWest Benin on the border with Burkina Faso.The park was registered as a biosphere reserveby UNESCO in 1986, and some 4,000 touristsvisit each year.

The park includes a conservation area, a mixedconservation-hunting area and a mixed usezone where rural populations practiceagriculture on some 3,460 hectares of land.Lions, elephants, tigers, crocodiles, antelopeand other animals are all found within the park.

Conventional cotton is grown here as this isone of the few cash crop activities available tofarmers in Benin. However, the use of chemicalpesticides and fertilisers has caused a rangeof well documented problems. Endosulfanresidues have been detected in the park'swaterways and in aquatic species such as fishand amphibians.

However, rather than restrict the livelihoodoptions of local farmers, who are typical of therural poor in Benin (average incomes aroundEuros 115 per year), conversion of this area

to organic farming is currently beingconsidered as it would promote botheconomic opportunity and wildlifeconservation.

Conservative estimates envisage a transitionof at least 1,200 hectares to organic cottonwithin four years, and optimistic projectionsestimate at least double that figure. Theproliferation of organic cotton would allowimproved incomes and ensure the future ofthe Wildlife Park.

19

5. Processing and the Future:Organic Exchange Workshop, July2006, Cotonou

Organic Exchange, together with the BenineseNGO OBEPAB, and supported by ICCO andGTZ, organised a workshop in Cotonou, Beninin July 2006 to look in depth at organic cotton inAfrica and help determine its future.

Participants came from Benin, Burkina Faso,Ghana, Kenya, Zambia, Togo, Senegal, India,Lesotho, Taiwan, Mali, United Kingdom, TheNetherlands, Uganda, France, Italy, United States,Australia, and Ethiopia and represented farmers,farmer organisations, NGOs, manufacturers,designers, government organisations, agriculturalministry, extension agents, donors, and journalists.

The participants were uniformly positive aboutthe future of organic cotton in Africa, and ambitiousto use organic cotton as a strategy to make uplost ground in textile processing. By focusing onhigher-end textiles, the groups felt that they couldgain a competitive advantage in specialised areas,rather than trying to compete against cheapervolume production.

The textile sector in Africa is required to meethigher labour standards and minimum wagesthan many competing regions, but the creationof an ‘Organic Cotton from Africa’ brand and astrong farming standard could turn potential

weaknesses, such as higher costs, into strongselling points.

To back up these ambitious plans, a regionalstructure will be created over the next year andthe sector will develop a plan to significantlyimprove the efficiency and effectiveness of theirinformation systems.

African projects usually emphasise social impactsas much as environmental goals.The strong socialaims of most farming projects also requireinvestors interested in having added-value overand above environmental impacts, willing to beinvolved in the long-term.

Both African companies and projects feel a needto use organic cotton and higher-end markets tomove from commodity production to developinga stronger industrial base, Africans are keenlyaware that they have often gone backward inmanufacturing over recent years, faced with cheap

competition from Asia and dumping on theirmarkets, but are confident that by focusing onhigher end production they can reverse thistrend.

The emphasis in Africa could also be on Fairtradeorganic, perhaps aiming at elite rather than massmarkets.

Breaking with Convention: Making an Impact One Fibre at a Time

20

Together we makea world of difference

India

India has taken to organic cotton in a big way. The principles of organiccotton strike a chord with many Indian farmers who are steeped in a holistictradition that sees the relationship between humans and their environmentand respects natural processes in a way that is unique. Indian projects areoften characterised by an enormous respect for the environment, a wealthof natural approaches to pest management and soil fertility, and a strongspiritual philosophy. Buyers in this region will also find a high degree ofprofessionalism and a variety of regional differences in culture, food anddress.

Organic Cotton in India:Passion, Entrepreneurship,and Vitality

1. Introduction 222. Agrocel 24

2.1. Organic Farmers in Gujarat 242.2. Choudary Family, Mandvi District 252.3. Sathbir Singh ram Swarup Choudury 262.4. Rotation Crops and other Local Developments 272.5. Wagji Rajabhai Walan’s Farm, Bhutakiya Village,

Rapar Taluk 282.6. Fairtrade 292.7. Parbhat Bhai Savji Bhai Patel’s Farm,

Padampur Village, Kutch 293. EcoFarms India 30

3.1. Origins 303.2. Mr. Subhash Sharma's Farm, Dorli Village, Yavatmal 313.3. Jainpur Village, Farmer Group, Amaravathi 323.4. Amla Village, Dharyapur Taluk, Amaravathi 333.5. EcoFarms and Supply Chain Requirements 34

4. Chetna Organic 354.1. Processing 35

5. Organic Farms Company 356. Processing Options and Vertical Suppliers 35

21

Sowing the Seeds of Change: Weaving Innovation and Integrity into Organic Agriculture

22

1. IntroductionOrganic cotton production in India has increasedsignificantly since 2000-01. As of 2006, India is thesecond largest producer of organic cottonworldwide, with eleven known active projects. Thelargest projects are Pratibha Syntex, EcoFarmsand Maikaal BioRe. Most production for the 2005-06 harvest is already sold or committed althoughsome open stocks exist for several fibre qualities.It is possible that total production is slightly higherthan stated here.

Pakistan is a newcomer to the organic cottonproduction scene and is set to grow rapidly in thecoming seasons.

Some production, located on farms with permanentcrop rotation systems (also known as permaculturesystems) also occurs in Nepal although it is verysmall and currently uncertified.

The bulk of organic cotton production in India occursin the following states: Gujarat, Madhya Pradhesh,Maharashtra, Orissa, and Andhra Pradesh. Indiais rapidly increasing organic cotton fibre, textileand garment production to meet growing customerdemands. India also has a mature, global textileindustry with links to major international marketsas well as access to a potentially enormousdomestic market.

India

Pakistan 0 600 600 0 8.67%India 930 6,320 5,213 2,037 91.33%

Total 930 6,920 5,813 2,037 100.00%

% OFPRODUCTION

BEGINNINGSTOCK

AUGUST 1HARVEST SALES /

COMMITMENTSENDINGSTOCK

2004-05 Organic Cotton Stocks and Fibre Production inIndia and Pakistan (in metric tonnes)

India 2,037 9,835 10,835 1,037 91%Pakistan 0 1,000 1,000 0 9%

Total 2,037 10,835 10,835 1,037 100%

% OFPRODUCTION

BEGINNINGSTOCK

AUGUST 1HARVEST SALES /

COMMITMENTSENDINGSTOCK

2005-06 Organic Cotton Production Projection inIndia and Pakistan (in metric tonnes)

23

note: Farms aside, this table only lists those actors mentioned in this document.For a more comprehensive list see Organic Exchange's Sourcing Guide.

Actors in India

Agrocel (some)

Pratibha Syntex

EcoFarms

Chetna Organic

Organic Farms

VOFA

ETC India

Super Spinning Mills

Arvind Mills

GTC

Maikaal Fibres

Rajlaksmi Centre

Maikaal BioRe

ACTOR FARM TRADER / MANUFACTUREREXPORTER

Authority of Gujarat. They reserve 25% of theirorganic cotton fibre and a 25% mix of otherorganic crops for the rapidly growing domesticmarket.

Agrocel’s predicted harvest for 2005-06 is 800-850 tonnes of certified organic fibre and 600tonnes of certified organic, Fairtrade fibre.

2.1. Organic farmers in GujaratThere are currently twelve organic farmerslocated around the Mandvi centre, and some1,200 certified organic and/or Fairtrade farmersin the Rapur zone, a marginal area with manytribal farmers. This area has relatively low yieldsdue to lower rainfall.

Field officers are employed by Agrocel to supportfarmers on a one-to-one basis as they transitionto or increase their current organic cropproduction. Soils are light with low waterretention, and landholdings are small.

A third district in Dhrangadhra has farmers on16,000 acres with progressive approaches, goodsoil, irrigation, and good farm practices. In total,4,000 farmers are certified organic across thefour districts where Agrocel are present.

Sowing the Seeds of Change: Weaving Innovation and Integrity into Organic Agriculture

2. AgrocelAgrocel Industries are one of the pioneers ofboth certified organic and certified Fairtradeorganic cotton production in India. Most of theirorganic production takes place in Gujarat.

Their organic production was an outgrowth oftheir interest in the environmental, social andeconomic aspects of farming. Hence, the grouphas also done a great deal of work on watermanagement and was also involved in helpingthe rebuilding efforts after the earthquake inKaatch in 2001. Fifty-seven villages were rebuiltand eighteen thousand temporary houses wereconstructed.

The Shrujan project, a high quality, handwoventextile centre was founded by Chanda BenShroff, a member of the family behind Agrocel,and employs 3,500 women in 110 villages inGujarat which supplements incomes of farmingfamilies during their lean periods.

Established in 1941, Agrocel has eighteenresearch and development centres in six states,helping farmers with such varied issues astaxation, accounts, audits, personal finance, aswell as agronomic issues and food and cottonsales and exports.

In addition to organic fibre production, Agrocelhas the capacity to produce small garment ordersfor basic knits like t-shirts in the 1,000-2,000unit range and has produced such for the Sports

24

India

Choudary Family Farm Budget

Input Costs 309.52 119.05 38.46%Labour CostsAverage Yields (kg/acre) 1,400.00 900.00 64.29%Premium (%) 8.00Price (kg) 0.48 0.48

Total Income (Dollars) 666.67 462.86 69.43%Costs 309.52 119.05 38.46%

Net Income 357.14 343.81 96.27%

PER ACRE (IN US $)

CONVENTIONAL ORGANIC DIFFERENCES

This is a rare example of an organic farm budget showinga loss of income, although it is very slight, and if costssuch as health care from pesticide exposure are takeninto account, it would show a gain. What is interestingto note is the major reduction in production costs, whichwill significantly reduce this family's debt.

2.2. Choudary Family, MandviDistrictA joint family holding of twenty-seven acres ofinherited farmland is owned and managed byKarshan Bai Choudary, Tulsi Bai Manji BaiChoudary, and Narmada Ben Hari lal Choudary.Since their original inheritance, they have increasedtheir holdings to a total of forty-five acres. Each ofthe three members farm a portion of the land asindividual farmers and receive a share of the profits.

Growing organic cotton has helped Agrocel solvea significant soil salinity problem (too much salt inthe soil). Some 50% of the land is under cottonat any time, with an average staple length of over28 millimetres. The balance of the land is on rotationwith castor, bajra, wheat, dill, green gram andgroundnut, and 25% of the land is reserved for

growing food for family consumption.

The nine-month cotton season begins in May whenthe crops are sown and ends with a three month,three-pick harvest beginning in September.

Irrigation

25

The Gujarat government offers a subsidy to farmers to install drip irrigation systems. Because the Choudary family saw irrigationas a solid investment in the improvement of cropyields, they borrowed the necessary finance andhave since paid it back. In addition, they harvestrain water using tube wells, of which they havethree; they also have three ordinary wells on thefarm. The water table is 400 feet deep in thislocation, but the lack of rainfall is threatening cottonproduction, and the family have irrigated only 13acres so far.

Organic InputsThe family use mostly inputs gathered and grownon the farm, such as neem seed and cow urine,which act as natural pesticides, as well asbuttermilk, datura, and neem cake. They also use

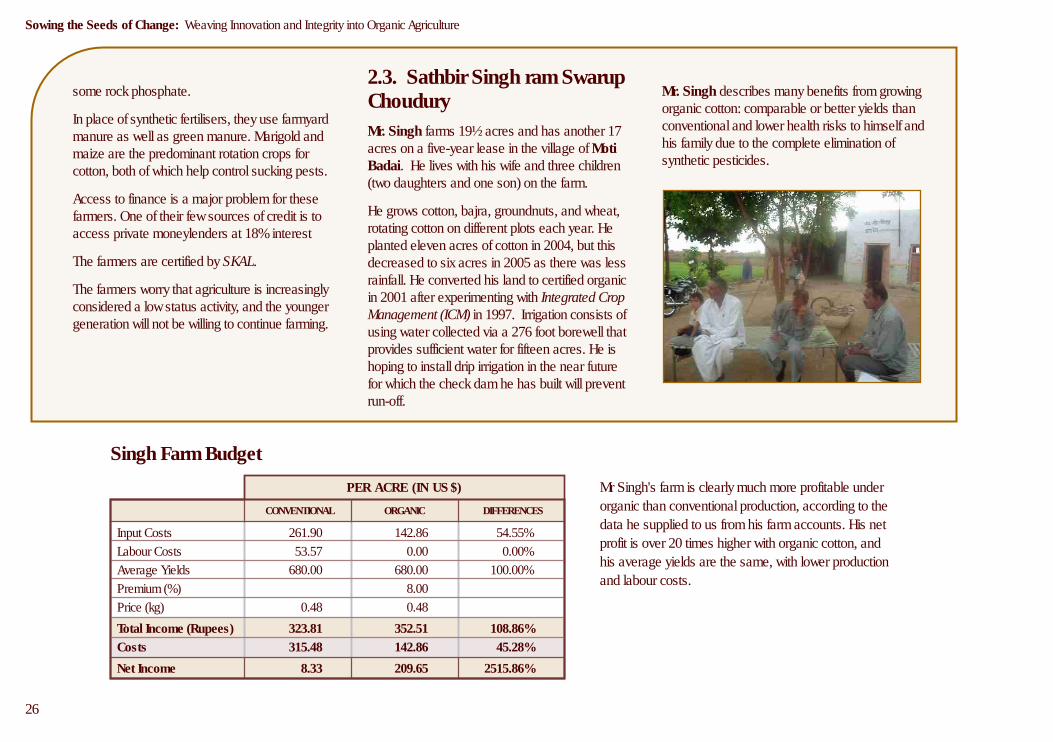

Mr. Singh describes many benefits from growingorganic cotton: comparable or better yields thanconventional and lower health risks to himself andhis family due to the complete elimination ofsynthetic pesticides.

Sowing the Seeds of Change: Weaving Innovation and Integrity into Organic Agriculture

2.3. Sathbir Singh ram SwarupChouduryMr. Singh farms 19½ acres and has another 17acres on a five-year lease in the village of MotiBadai. He lives with his wife and three children(two daughters and one son) on the farm.

He grows cotton, bajra, groundnuts, and wheat,rotating cotton on different plots each year. Heplanted eleven acres of cotton in 2004, but thisdecreased to six acres in 2005 as there was lessrainfall. He converted his land to certified organicin 2001 after experimenting with Integrated CropManagement (ICM) in 1997. Irrigation consists ofusing water collected via a 276 foot borewell thatprovides sufficient water for fifteen acres. He ishoping to install drip irrigation in the near futurefor which the check dam he has built will preventrun-off.

Singh Farm Budget

Input Costs 261.90 142.86 54.55%Labour Costs 53.57 0.00 0.00%Average Yields 680.00 680.00 100.00%Premium (%) 8.00Price (kg) 0.48 0.48

Total Income (Rupees) 323.81 352.51 108.86%Costs 315.48 142.86 45.28%

Net Income 8.33 209.65 2515.86%

PER ACRE (IN US $)

CONVENTIONAL ORGANIC DIFFERENCES

Mr Singh's farm is clearly much more profitable underorganic than conventional production, according to thedata he supplied to us from his farm accounts. His netprofit is over 20 times higher with organic cotton, andhis average yields are the same, with lower productionand labour costs.

some rock phosphate.

In place of synthetic fertilisers, they use farmyardmanure as well as green manure. Marigold andmaize are the predominant rotation crops forcotton, both of which help control sucking pests.

Access to finance is a major problem for thesefarmers. One of their few sources of credit is toaccess private moneylenders at 18% interest

The farmers are certified by SKAL.

The farmers worry that agriculture is increasinglyconsidered a low status activity, and the youngergeneration will not be willing to continue farming.

26

India

In addition to the pesticide elimination, thefertilisers used on organic cotton are animalmanure and agricultural crop waste, as opposedto synthetic fertilisers. A number of bugs, suchas sucking pests and bollworm, are effectivelycontrolled with neem oil, which he mixes withbuttermilk.

Cotton provides 50% of farm and householdcash income. In fact, the environmental, socialand economic benefits from organic farminghave inspired his son, who now wants to be afarmer, in a time when the younger generationis seeking work in more highly perceived sectorslike law and medicine.

The farm is self-sufficient in food, a strongmotivation for the family, who are concernedabout the spread of genetically modified seed.They buy only luxuries like sugar from othersources.

The local Agrocel field officer is present duringsowing to ensure the proper seeds are planted,help with soil and water testing, and monitor thefarm once a week through harvest.

27

2.4. Rotation Crops andOther Local DevelopmentsRecently, organic sesame, a common rotationcrop, was exported for the first time fromNavalgud in the Surendra Nagar district, thefunds from which allow eighty-five local familiesto get power from Biogas. Four other villageshave solar tube lights, and fourteen others willbe receiving them in 2006.

However, Agrocel feel more connections needto be made by consumers between health, food,farming and traditional knowledge. There is aneed to reach out to appropriate sectors whocan then distribute these messages, such asAyurvedic and holistic practitioners, health andbeauty practitioners, as well as Ashrams. Thereare several key states which are ideal forlaunching this type of grassroots marketingcampaign: Gujarat, Madhya Pradesh,Maharashtra, and Rajastan as their consumerbase is already ecologically and socially aware.

Walan Farm Budget

Input Costs 190.48 142.86 75.00%Labour CostsAverage Yields 880.00 880.00 100.00%Premium (%) 0.00 17.75Price (kg) 0.51 0.51

Total Income (Rupees) 445.24 524.27 117.75%Costs 190.48 142.86 75.00%

Net Income 254.76 381.41 149.71%

PER ACRE (IN US $)

CONVENTIONAL ORGANIC DIFFERENCES

The Walan farm budget shows a much higher incomefor the farmer under organic than conventional practices,with similar yields and lower production costs.

Sowing the Seeds of Change: Weaving Innovation and Integrity into Organic Agriculture

2.5. Wagji Rajabhai Walan’sFarm, Bhutakiya Village, RaparTalukMr. Walan owns 7.5 acres on uneven terrain. Heis married with two sons and three daughters andlives on the farm with his family. The farm is certifiedas both organic and Fairtrade.

Mr. Walan converted to organic farming in 2003.His organic yields are very similar to hisconventional output, but he needs far less water.He sees both his individual farm’s and his region’sorganic production increasing steadily based onlocal and international brand demand. He putsout bird food and bird baths and is happy that thebirds contribute to natural pest control methods.He also makes his own natural pesticides fromneem and buttermilk and uses animal manure,

green manure, castor cake, neem oil, and otherorganic inputs. He rotates his organic cotton withcastor, bhadja, and dill.

He usually grows cotton on 50% of his land,although poor rainfall in 2005 meant that he wasonly able to grow it on 20%. He also grows bajra,til, and some vegetables.

For irrigation, he has one 75 foot open well, butno drip irrigation as yet, as he cannot afford thecost. His well can provide water for up to four hoursa day, which is sufficient for healthy organic cottonfarming. At present, he does little water harvestingbut does practice contour banding to reduce waterloss. In Mr. Walan's experience, organic farminguses less water due to the elimination of thesynthetic fertilisers that had previously depletedhis soil’s mineral content.

Cotton represents some 50% of his farm income.The adult members of his family work the land,and many farmers in the area often help eachother on an as needed basis.

The family are food self-sufficient except for luxurieslike sugar.

28

til and some vegetables. They have one borewellwith rain supplying the rest of their waterrequirements. Labour is a mixture of adult familymembers and outside labour, which is used atharvest time. They use animal manure and greenmanure for fertilisation, and neem, castor andbuttermilk for pest control. Pigeon pea is also usedto nourish the soil.

Patel Farm Budget

Input Costs 214.29 154.76 72.22%Labour Costs 71.43 71.43Average Yields 700.00 700.00 100.00%Premium (%) 17.58Price (kg) 0.51 0.51

Total Income (Rupees) 354.67 419.76 118.35%Costs 285.71 226.19 79.17%

Net Income 68.95 193.57 280.73%

PER ACRE (IN US $)

CONVENTIONAL ORGANIC DIFFERENCES

The family farm budgetshows that their net incomeis much higher under theorganic system, with similaryields to conventional.

India

2.6. FairtradeMr. Walan has been part of a Fairtrade group sinceearly 2006, the Agrocel Pure and Fair CottonGrowers Association, which currently has 340members. His wife, Amrutha ben, is the VicePresident of the association. As part of requiredFairtrade activities, a sewing class also takes placein one room of their home.

2.7. Parbhat Bhai Savji BhaiPatel’s Farm, Padampur Village,KutchThis 70-acre farm is held jointly by three brothers.Mr. Patel is President of the Agrocel Pure andFairtrade Cotton Growers Association.

They grow mostly cotton along with wheat, maize,

29

The Patel family prefers organic cotton toconventional as they find it less waterintensive and healthier for the soil. With theprofits they receive from organic and Fairtrade,the family is mostly food self-sufficient, only buyinga few things like tea, oil, sugar and rice.

Support Structures forFairtradeThere is one field agent per every47 farmers and 900 acres offarmland. The 340 Fairtrade farmersare in the pipeline for organic cottonconversion, with 160 ready forconversion now. Their total organiccotton production is approximately900,000 kilogrammes or 900 tonnes.The internal control system is entirelyrun by field agents without any farmerinvolvement.

The field agent decides whichadditional farmers join the projectbased on a set of establishedFairtrade criteria.

issue contracts to buy both their food and cottoncrops. Approximately 600 farmers are involvedin this project and span all three districts ofMaharashtra, with sixty of these farmers residingin the Amaravathi district.

The average land holding is fifty acres per farmeras the maximum legal holding per farmer is fifty-two acres. There are few small farmers in thisdistrict.

Sowing the Seeds of Change: Weaving Innovation and Integrity into Organic Agriculture

3. EcoFarms in India

3.1. OriginsEcoFarms was established by Mr. OmprakashMor in Yavatmal, Maharashtra. Mr. Mor hasbeen farming 40 years and converted completelyto organic in 1990. He runs the trading company,EcoFarms, with the help of his son, Anand.Farming in this area is mostly rain fed, with onlyabout 10% of the farms being irrigated. Rainfallis an average of 800 to 900 millimetres per yearalthough in 2005 they received over 2,000millimetres of rainfall.

Most farmers employ 50% of their land to growcotton and 50% to grow food crops. Averageyields are approximately 800 kilograms per acre.EcoFarms promote their own package of organicpractices with an emphasis on total farm self-sufficiency, i.e., no use of external organic inputs.

FarmersEcoFarms operate out of Maharashtra inMadhya Pradesh and have now expanded toOrissa. There are four external farm inspectorsfrom Eco Cert (Germany) who certify the farmersfrom the Maharashtra district.

Farmers who wish to grow organic crops firstenter into a formal contract with EcoFarms, whothen help each farmer in planning his crops, andoffer technical support including guidance forsourcing seeds and organic inputs. They also

Organisational StructureThe organisational structure of EcoFarms isoptimised to manage both the collection and saleof food and fibre from those farmers with whomthey have pre-existing contracts. EcoFarms hashelped connect a total of two thousand farmersaltogether.

30

India

EcoFarms is now a state-registered serviceprovider under the state project on organic farming.As an organic farming service provider, EcoFarmshost farmer field days, where meetings are heldon such topics as seed selection, marketdevelopment and farming techniques. In addition,they provide training and distribute informationand booklets in local languages for groups of 50-80 farmers. They also have regular meetings withfarmers, and their field agents visit each farmeron a monthly basis.

In 2003, EcoFarms began working withmarginalized tribal farmers in Orissa. In 2006,there will be 150,000 certified organic acres, ofwhich 30,000 acres will be organic cotton with anapproximate yield of 800 kilogrammes per acre.EcoFarms pay a 25% premium for organic cottonover conventional cotton.

EcoFarms are concerned about potential volatilityin the organic cotton sector, as experienced in theearly 1990s when organic was a cool, but shorttrend that disappeared abruptly. They wantcustomers and consumers to understand thatorganic farming is both a growing method and away of life Each business is a real family full ofreal people who invest everything they have inorganic conversion because they want a better,healthier way of life. EcoFarms act as an advocatefor these farmers and seek to build collaborationbetween the different farmer groups in order tostrengthen their collective bargaining power,something farmers find difficult to do on their own.

31

EcoFarms also manage some seedbanks and provide seed at no cost tofarmers. They also voluntarily advise onthe pros and cons of different seed varieties. Inseeking to provide their farmers with research anddevelopment services, they are also consideringbreeding different seeds from high performingorganic varieties. Orissa, even with limitedresearch to date, already has 30 millimetre staplelengths.

Their irrigation efforts focus on water harvestingusing wells and boreholes. Drip irrigation receivesa 25% subsidy for installation.

3.2. Mr. Subhash Sharma's farm,Dorli village, YavatmalMr. Sharma cultivates 30 acres of organic cropswith his farm help and their families who live onthe farm in lodging he provides. At present, hefarms three acres of organic cotton and growsseveral food crops including various vegetables,maize, rice, and wheat.

Mr. Sharma converted to organic farming in 1994.He was fairly skeptical about organic farming inthe beginning but is now totally convinced of itsbenefits. He is a model farmer, serving as a rolemodel to others and is frequently visited bygovernment officials, scientists and visiting farmergroups.

He is an incredibly progressive farmer who haswon the President’s award twice for innovative

Sowing the Seeds of Change: Weaving Innovation and Integrity into Organic Agriculture

Farm Budget, Mr. Sharma

Input Costs 257.14 128.57 50.00%Labour CostsAverage Yields 450.00 450.00 100.00%Premium (%) 25.00Price (kg) 0.48 0.48

Total Income (Rupees) 214.29 233.28 108.86%Costs 257.14 128.57 50.00%

Net Income -42.86 104.71

PER ACRE (IN US $)

CONVENTIONAL ORGANIC DIFFERENCES

From his farm budget, the benefits of organic cotton areclear. From being a loss-maker under conventionalproduction, the crop is now profitable.

farming and several awards from the Maharashtragovernment as well as the Tata Fellowship Award.One of the areas in which Mr. Sharma is particularlyinnovative is in the area of irrigation. He traps therain water that falls on his farm through wells andcontour farming. He says one centimetre of rainfallcan generate 100,000 litres of ground water, andthat organic farming has resulted in at least a 20%water savings.

He has pits that measure 10 feet wide by 20 feetlong by 10 feet deep in each field, from whichrainwater is channelled towards 75-foot borewells.He collects up to 36,000 litres of water per hourand has some 800 hours of water use availableeach year. Even with a 30% water evaporationrate, he estimates that his water needs are 50%lower with organic farming due to improved soilsand land management.

32

The farm uses no mechanical equipment exceptfor transport to market. All field operations aremanual or animal powered.

For inputs he uses neem, castor, buttermilk, farmmanure and green manure. He has developed aunique way of adding liquid manure to his dripirrigation process, and has planted several treesbetween the plots which serve as bunds (low ridgesto help prevent flooding) and house several speciesof birds, which act as natural pest controllers. Inaddition, the trees provide shade which helpsregulate crop temperatures.

3.3. Jainpur Village, FarmerGroup, AmaravathiThere are many organic farms in this Maharashtranvillage, some new and some long established. Thefarmers regularly meet at the home of SadashivDevrao Korpe, an organic cotton farmer, and hisson, Manish Sadashiv Korpe, an engineer byeducation who has now returned to farming. Otherfarmers nearby include Kapil Dev and AbhjitDevoke from Kalamgovan Village, and PradeepBayaskar from Narsinghpur.

Mr. Korpe's farm is considered large at 110 acres.The family farm is predominantly organic cottonwith some food grains and oil crops. They oftenuse external workers during busy times like plantingand harvesting. Their soil quality is excellent, beingpredominantly robust black soil, and is augmented

Jaipur Village Farm Budget

Input Costs 95.24 47.62 50.00%Labour Costs 69.05 69.05Average Yields 850.00 850.00 100.00%Premium (%) 25.00Price (kg) 0.48 0.48

Total Income (Rupees) 408.00 440.64 108.00%Costs 164.29 116.67 71.01%

Net Income 243.71 323.97 132.93%

PER ACRE (IN US $)

CONVENTIONAL ORGANIC DIFFERENCES

India

The combined farm budget from farmers in this villageshows that yields are the same between conventionaland organic cotton, with incomes in organic much higherdue to the premiums and lower input costs. Labour costsremain the same between both systems.

Those farmers who can afford to educate theirchildren in order to provide them with an escapefrom the risks of conventional farming. Manyfamilies have moved to more populous towns inorder to provide their children with better accessto education and healthcare.

3.4. Amla village, DharyapurTaluk, AmaravathiThis district has a large group of organic farmerswith an organised meeting room and office at thefarmhouse of Bala sahib Wankhede, the son ofAshkrishna alias Baburaoji Wankkhede whowas a pioneer in organic farming in Mahrashtrain 1975. A whopping 90% of the farmers in Amlaare certified organic. Bala Sahib owns 120 acres,with 60 acres under cotton. The rest of the crops

33

are local vegetables including toor dal,moong, chana, and til. The farmerspractice vermicomposting (composting usingworms) in addition to using other forms ofanimal and green manure. One of the mostcommonly used rotation crops is pigeon pea.Farmers plant three rows of pigeon pea after everytwelve rows of cotton to further enrich the soil.

The farmers here are incredibly committed toorganic farming. Mr. Wankhede is the currentdistrict President of the Youth Congress and VicePresident of the Agri-Produce Marketing Committeein Dharyapur. The farmers would like to put theprofit they receive for organic cotton toward thecreation of computer centres (in order to be ableto check weather forecasts, seed prices, andtechnical information on farming), investment inimproving drinking water facilities, and the buildingof medical facilities for the community.

with cattle manure from the plentiful local livestock.They allow nomadic livestock keepers to grazetheir animals on their fields in the off season wherethey feed on the cotton crop residue.

The farmers here, as in other parts of India, areworried by the loss of status for farming.

Sowing the Seeds of Change: Weaving Innovation and Integrity into Organic Agriculture

34

3.5. EcoFarms and SupplyChain RequirementsMr. Omprakash Mor enjoys an excellent rapportwith the farmers in his project. There are feelingsof mutual respect and trust, and the farmersknow without a doubt that Mr. Mor has theirbest interests in mind.

A major problem faced even by successfulgroups like EcoFarms is access to crop financeand the associated pre-finance rates which canadd up to 30% of the farmer's total contractvalue. Farmers also face interest rates fromlocal banks that are as high as 18-20%. This isan important issue for brands and investors aswell as NGOs to understand. The major problemfaced by many projects in expanding organicfarming is not the difficulty of conversion but the Spinning Capabilities:

EcoFarms can arrange for spinning, in theNE20-40 yarn count range.

Lead Time:A ten-month lead time is required for fibre andyarn orders to allow for adequate crop planning.

EcoFarms pay their farmers within eight to tendays of delivery or collection of harvest, by banktransfer.

cost of growing a business; affordable capital isa major need along with market forecastingsystems and more agronomic research andinformation.

EcoFarms stress the need for better policylobbying and market communication, dispellingwidely believed myths that organic cotton ismore water intensive and less profitable. Thereis also the need to promote organic farming asthe escape route for farmers from debt andsuicide, which is a major issue for areas likeMaharashtra.

India

35

4. Chetna OrganicThis project was started by the consultancy, ETCIndia, in Andhra Pradesh, who implement andcoordinate activities in the field. This project isfunded by ICCO and Solidaridad of theNetherlands and includes seed funding to supportthe farmers in developing their own organisation.There are currently 403 farmers in five differentzones, who produced a total of 40 tonnes of seedcotton in 2005. All the farms are currently ineither their first or second year of organicconversion.

4.1. ProcessingThe ginning outturn is 34%, and is performed byGTC in Nagpur and Vengatesh, Warangal.Spinning is done with Super Spinning Mills andMaikaal Fibres, and the fibre can be spun up toNE40. Both spinners are also able to produceLycra blends, which they currently produce in 4%blends, NE30 for the sock industry. Rajlaksmiproduces knitted fabrics including jersey, ribs,pique, and terry. Some basic wovens are alsopossible and include sheeting and toweling andcome mostly from the Rajlaksmi Centre.

Chetna fibre is certified Fairtrade organic. Themanufacturers, Super Spinning Mills andRajlaksmi, are currently being audited againstthe Ethical Trading Initiative standard. Rajlaksmiare already accredited to the IFAT (InternationalFairtrade Association), Fairwear and Magasinsdu Monde labour standards.

5. Organic FarmsOrganic Farms is a farmer-owned company. TheOrganic Farms structure supports marketing,training, technical advice, and certification for allof its farmers. They have nine trainers who alsomaintain the Internal Control System. At present,the company sells only fibre, and their goal is toproduce 5,000 tonnes of certified organic fibrewithin six years. They sell most of their organicfibre to Assissi Garments, a manufacturer locatedin Tamil Nadu, India, that supplies companiessuch as People Tree in the United Kingdom andJapan. Rotation crops are mostly sold in thedomestic market, but products such as safflower,mangoes and papayas are in demand fromoverseas markets.

6. Processing Optionsand Vertical SuppliersIndia has a wealth of processing options in mostregions as well as organic cotton growing options.There are several other projects in addition tothose previously mentioned. Many of theseprojects, including Maaikaal BioRe and PrathibaSyntex, have fully integrated supply chains allowingsourcing from fibre to finished garment.

Other spinners and weavers are willing and ableto process organic cotton, such as Arvind Mills,

the third-largest denim manufacturer inthe world, with a processing capacity of700,000 bales per year.

Together we makea world of difference

Latin America

An amazingly diverse region, Latin America spans a range of landscapesfrom the Peruvian plains and mountains with their long staple andcoloured cottons and farmers steeped in the long Inca history, to themodern industrial centres of Brazil and the vibrant spirit of land-lockedParaguay. Latin America offers a diversity of choices for small, mediumand large sized companies seeking everything from basic knit andwoven textiles and garments to amazing, complex artisan products –all present in a region of intriguing cultures, cuisine and colour.

Organic Cotton inLatin America:Islands of Uniqueness

1. Introduction 382. Paraguay 40

2.1. Introduction 402.2. Rotation Crops 412.3. Organic Cotton Sector 412.4. Farming Profile: Arasay 422.5. Ginning, Spinning and Weaving 442.6. Dyeing 462.7. Processing and Manufacturing of Handmade

and Artisan Products 462.8. Design and Production Design 472.9. Exports 472.10. Certification 47

3. Peru 483.1. Introduction 483.2. Profile: APAEM Association, Moroppe 493.3. The White Cotton Project 503.4. Oro Blanco 503.5. Processing 50

4. Emerging Countries: Brazil, Columbia, Nicaragua 52

37

Sowing the Seeds of Change: Weaving Innovation and Integrity into Organic Agriculture

38

Peru:- Fibre production- Spinning- Weaving- CMT*

Brazil- Weaving- CMT*- Some farming

Central America:- Some growing andprocessing in Nicaraguaand processing only inColumbia

Paraguay:- Fibre production- Spinning- Weaving- CMT*

*CMT: Cut, Make, and Trim

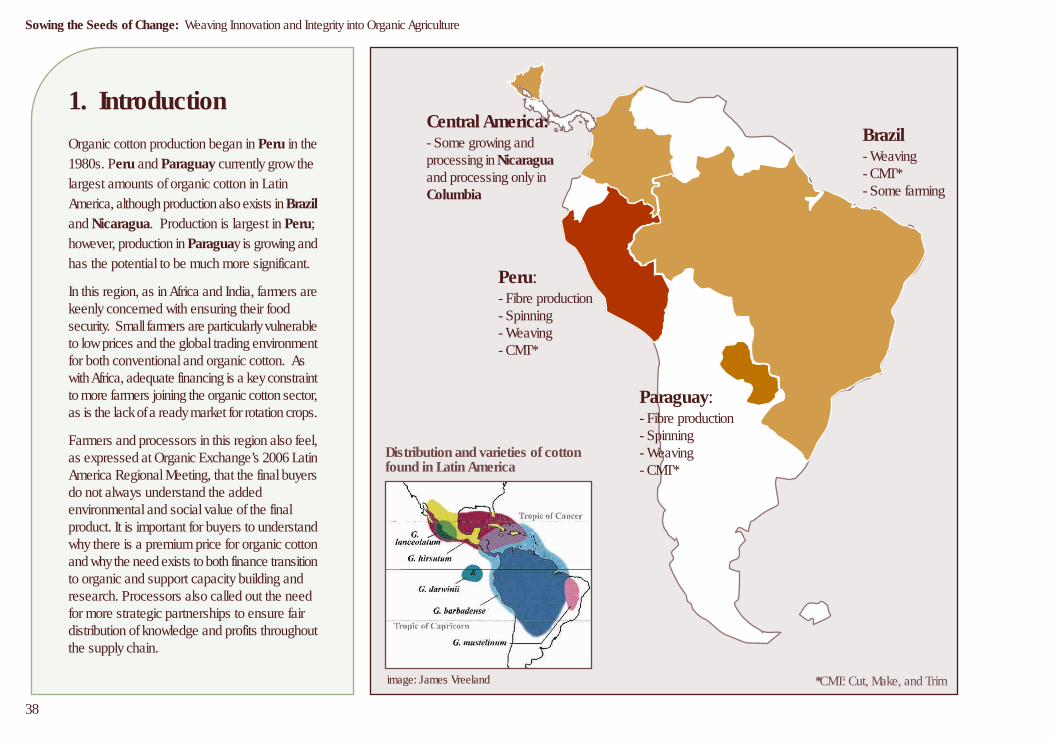

1. IntroductionOrganic cotton production began in Peru in the1980s. Peru and Paraguay currently grow thelargest amounts of organic cotton in LatinAmerica, although production also exists in Braziland Nicaragua. Production is largest in Peru;however, production in Paraguay is growing andhas the potential to be much more significant.

In this region, as in Africa and India, farmers arekeenly concerned with ensuring their foodsecurity. Small farmers are particularly vulnerableto low prices and the global trading environmentfor both conventional and organic cotton. Aswith Africa, adequate financing is a key constraintto more farmers joining the organic cotton sector,as is the lack of a ready market for rotation crops.