81

CBIZ & MHM Executive Education Series™ Key Tax & Compensation Complexities Facing Not-for-Profit Organizations Presented by: Joseph Giso & Priya Kapila Dates: December 4 and 10, 2014

| Date post: | 11-Jul-2015 |

| Category: |

Documents |

| Upload: | mayer-hoffman-mccann-pc |

| View: | 151 times |

| Download: | 1 times |

CBIZ & MHM Executive Education Series™ Key Tax & Compensation Complexities Facing

Not-for-Profit Organizations

Presented by: Joseph Giso & Priya Kapila

Dates: December 4 and 10, 2014

2 #CBIZMHMwebinar #CBIZMHMwebinar

To view this webcast in full screen mode, click on view options in the upper right hand corner.

Click the Support tab for technical assistance.

If you have a question during the presentation, please use the Q&A feature at the bottom of your screen.

Before We Get Started…

3 #CBIZMHMwebinar #CBIZMHMwebinar

This webcast is eligible for CPE credit. To receive credit, you will need to answer periodic participation markers throughout the webcast.

External participants will receive their CPE certificate via email immediately following the webcast.

CPE Credit

4 #CBIZMHMwebinar

Today’s Presenters

Joseph Giso, CPA Managing Director, CBIZ MHM 617.761.0623 | [email protected] Located in our Boston office, Joe has nearly 30 years of experience working exclusively with not-for-profit organizations in the education, healthcare, human services, and cultural sectors. He provides tax consulting services that are dedicated to improving the accountability and efficiency of tax-exempt organizations, including federal, state, local and various other regulatory agencies.

Priya Kapila Manager, CBIZ Benefits & Insurance Services 314.692.2249 | [email protected] Priya is a manager in the compensation consulting division at CBIZ Human Capital Services. She has participated in the development of compensation plans for numerous organizations across the US. During her time with CBIZ, she has gain significant experience in designing market-and job evaluation-based salary structures, drafting job documentation and compensation plan policies, and creating performance-based salary increase and incentive programs.

5 #CBIZMHMwebinar #CBIZMHMwebinar

Today’s Agenda

1

2

3

4

Definition of Unrelated Business Income (UBIT)

Alternative Revenue Sources

Executive Compensation in Not-for-Profit Organizations

5

6

Federal and State Regulatory Developments How to Protect Your Executives and Board Members

How to Protect Your Executives and Board Members

Trends in Not-for-Profit Compensation

EXECUTIVE COMPENSATION IN NOT-FOR-PROFIT ORGANIZATIONS

7 #CBIZMHMwebinar #CBIZMHMwebinar

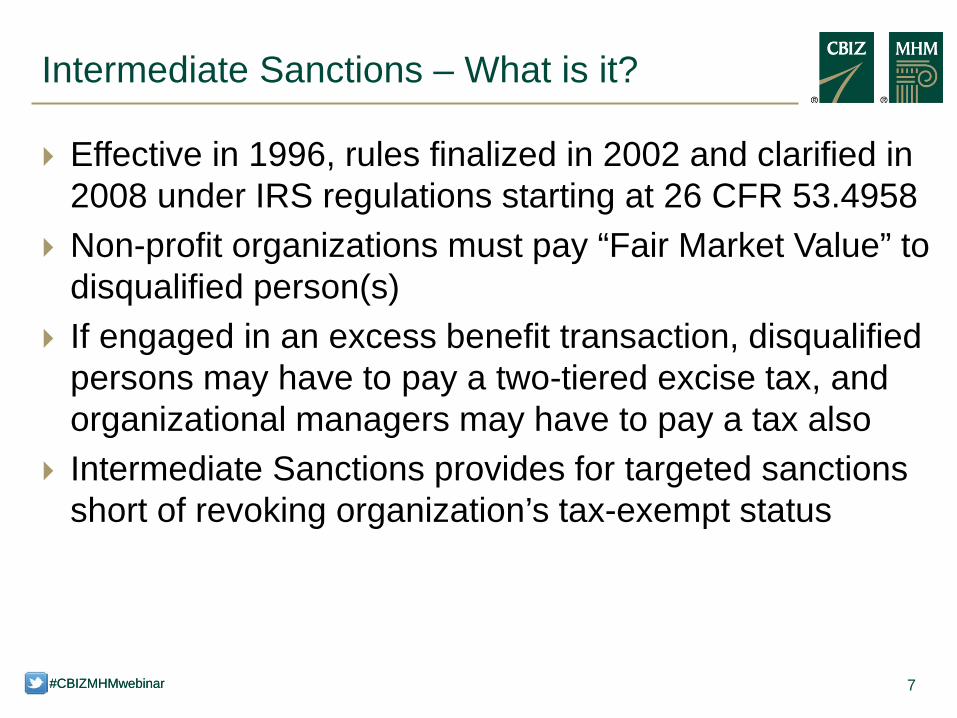

Effective in 1996, rules finalized in 2002 and clarified in 2008 under IRS regulations starting at 26 CFR 53.4958

Non-profit organizations must pay “Fair Market Value” to disqualified person(s)

If engaged in an excess benefit transaction, disqualified persons may have to pay a two-tiered excise tax, and organizational managers may have to pay a tax also

Intermediate Sanctions provides for targeted sanctions short of revoking organization’s tax-exempt status

Intermediate Sanctions – What is it?

8 #CBIZMHMwebinar #CBIZMHMwebinar

IRS is focusing on compensation issues IRS is staffing offices and adding personnel to question

excessive compensation State Attorneys General beginning to review as well

Violations (even inadvertent) can mean embarrassment for nonprofits and affect ability to raise funds

Personal liability for “disqualified persons” and "organization managers"

Form 990 changes

Intermediate Sanctions – Why Should You Care?

9 #CBIZMHMwebinar #CBIZMHMwebinar

25% penalty imposed on “disqualified person,” which may be increased to 200% if not corrected

10% penalty imposed on “organizational managers,” capped at $20,000 per transaction

Penalty applied to the amount of “excess benefit” Joint and several liability for all penalties Risk of losing tax exempt status

Intermediate Sanctions – Penalties

10 #CBIZMHMwebinar #CBIZMHMwebinar

Excess benefit transactions can include: Compensation, Sale, exchange or use of assets, Loan, or Any other form of compensation

In which the organization receives less than the value in return

Excess Benefit Transactions

11 #CBIZMHMwebinar #CBIZMHMwebinar

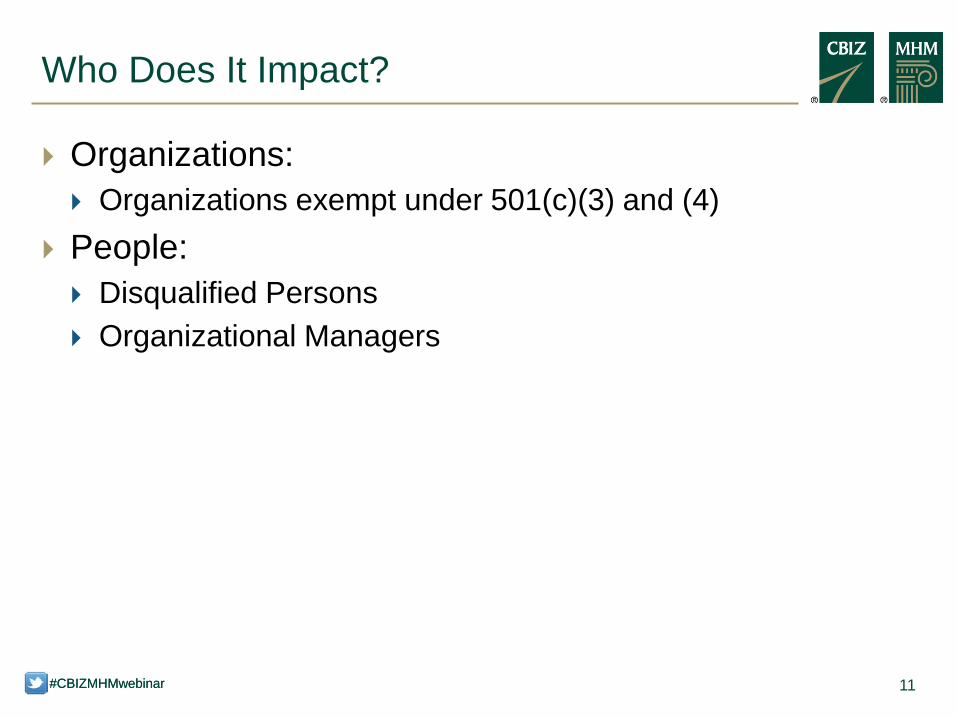

Organizations: Organizations exempt under 501(c)(3) and (4)

People: Disqualified Persons Organizational Managers

Who Does It Impact?

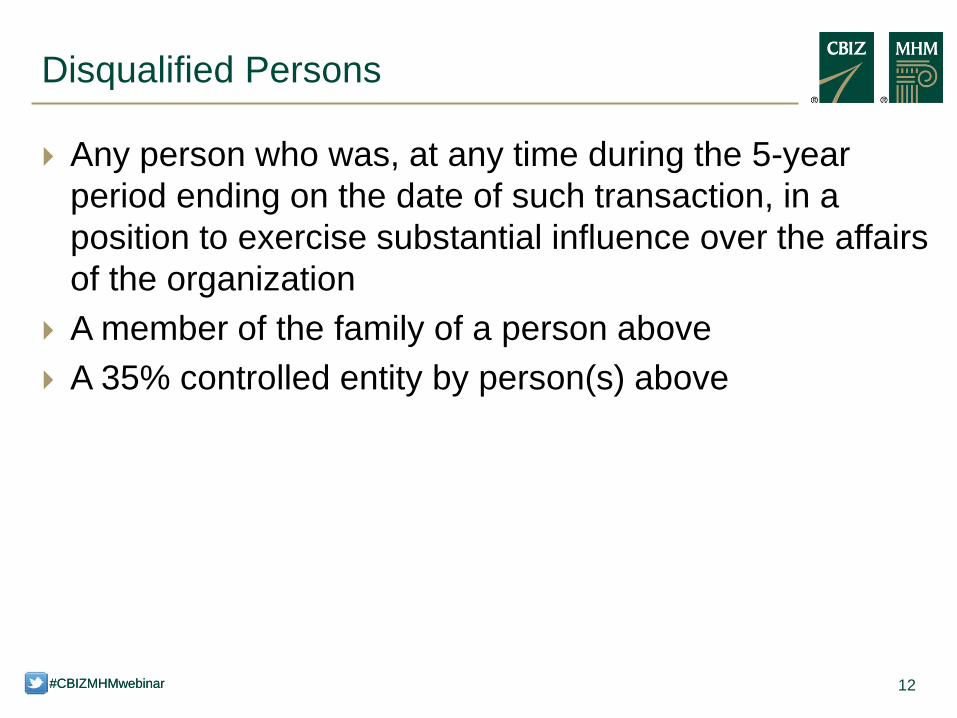

12 #CBIZMHMwebinar #CBIZMHMwebinar

Any person who was, at any time during the 5-year period ending on the date of such transaction, in a position to exercise substantial influence over the affairs of the organization

A member of the family of a person above A 35% controlled entity by person(s) above

Disqualified Persons

13 #CBIZMHMwebinar #CBIZMHMwebinar

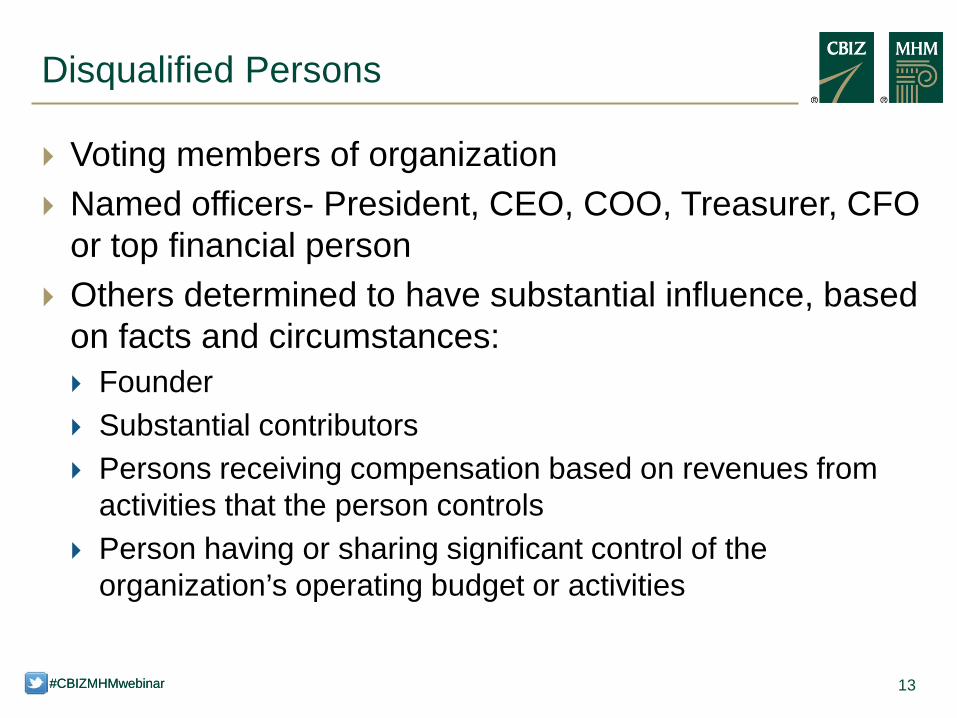

Voting members of organization Named officers- President, CEO, COO, Treasurer, CFO

or top financial person Others determined to have substantial influence, based

on facts and circumstances: Founder Substantial contributors Persons receiving compensation based on revenues from

activities that the person controls Person having or sharing significant control of the

organization’s operating budget or activities

Disqualified Persons

14 #CBIZMHMwebinar #CBIZMHMwebinar

Receives compensation less than $115,000 Is not a family member of a disqualified person Is not specifically a named officer or voting member,

and Is not a significant contributor

Deemed Not to Have Substantial Influence

15 #CBIZMHMwebinar #CBIZMHMwebinar

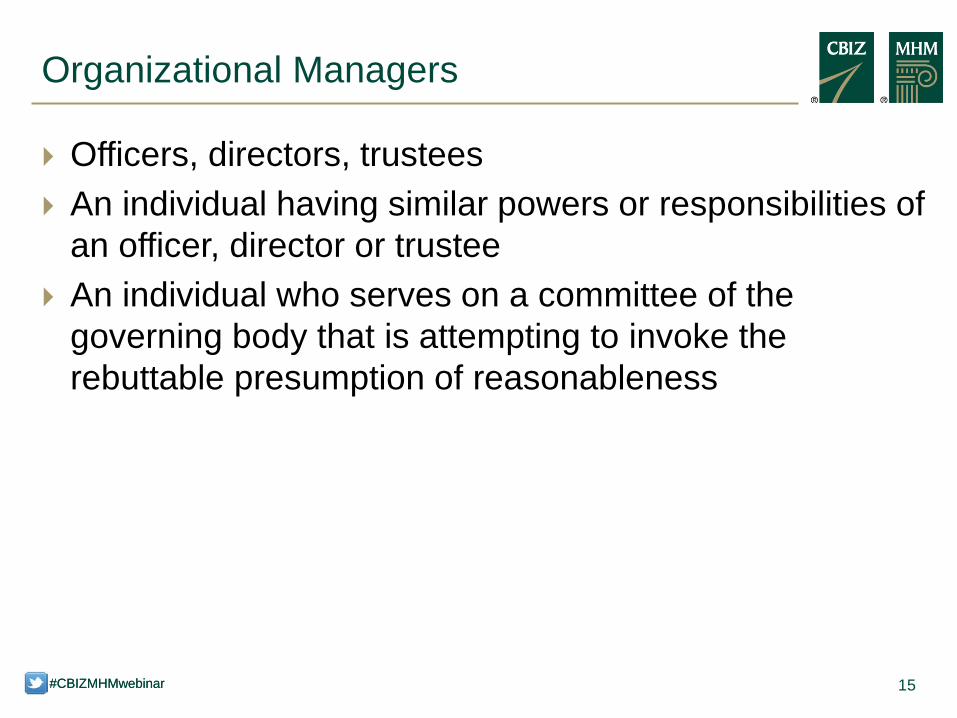

Officers, directors, trustees An individual having similar powers or responsibilities of

an officer, director or trustee An individual who serves on a committee of the

governing body that is attempting to invoke the rebuttable presumption of reasonableness

Organizational Managers

HOW TO PROTECT YOUR EXECUTIVES AND BOARD

MEMBERS

17 #CBIZMHMwebinar

Rebuttable Presumption

Compensation will be presumed to be reasonable if the organization has followed the rebuttable presumption procedures, shifting the burden of proof to the IRS

Requirements Compensation arrangement is approved in advance by an

independent authorized body without conflicts of interest Authorized body obtained and relied upon appropriate data

prior to making determination (i.e., compensation consultant’s data)

Authorized body concurrently and adequately documented the basis for making determination of compensation

18 #CBIZMHMwebinar

Reasonable Compensation

Reasonable compensation is based on: Nature of duties Background and experience Size of organization Time devoted Economic conditions in general and locally The amount paid by similarly situated organizations to those

performing similar services

19 #CBIZMHMwebinar

Appropriate Data

Compensation paid by similar organizations, tax exempt and taxable Base Salary Bonus Perquisites Long-Term Incentives

Current compensation surveys Written offers to disqualified person

20 #CBIZMHMwebinar

Reliability of Data

Reliable Data Published survey data

Major consulting and surveying firms Statistically validated Standard deviation analysis of data

Unreliable data examples: Self-reported data DOL Data from one or two competitors

21 #CBIZMHMwebinar

• National Executive Survey - AAIM Management Association

• Policies and Benefits Survey - AAIM Management Association

• Salary Survey - AAIM Management Association • Wage Survey - AAIM Management Association • Compensation in Non-Profit Organizations - Abbott-Langer • Compensation of Non-Profit Chief Executive Officers -

Abbott-Langer • Executive Compensation Report - Aspen Publishing/A

Panel Publication • Not-for-Profit Compensation and Benefits - Buck

Consultants • Top Management Compensation Survey - Buck

Consultants • Survey of Employee Benefits - Business and Legal

Reports, Inc. • Survey of Exempt Compensation - Business and Legal

Reports, Inc. • Executive Benefits - A Survey of Current Trends -

Clark/Bardes Consulting • Board of Directors Comp., Policies, Practices - Towers

Watson Data Services • Survey Report on Top Management Compensation -

Towers Watson Data Services • Hospital and Health Care Management Compensation

Report - Towers Watson Data Services • Sales and Marketing Personnel Compensation Report -

Towers Watson Data Services • Management Compensation Report for Not-For-Profit

Organizations - PRM Consulting Group • Compensation Report - Guidestar

• Survey Report on Non-Qualified Benefits & Perquisites Practices - Towers Watson Data Services

• Economic Research Institute - Survey Database • Executive TCM - Hewitt • Management and Professional TCM - Hewitt • Executive Compensation Survey - William M Mercer • Finance, Accounting and Legal Compensation Survey -

William M Mercer • Metropolitan Benchmark Compensation Survey - North

Central Region - William M Mercer • Information Technology Compensation Survey - William M.

Mercer • Salary Budget Survey - WorldatWork • Executive Compensation Data - CompData Surveys • Benefits USA - CompData Surveys • Engineering Executive Compensation Survey - Dietrich and

Associates • PSMJ A/E Management Salary Survey - PSMJ • PSMJ A/E Financial Performance Survey Engineering - PSMJ • Director Compensation Report - National Association of

Corporate Directors • Human Services Compensation in the United States -

Alliance • Compensation Policies and Practices - Watson Wyatt Data

Services • Executive Compensation Analyst - Salary.com • Not For Profit Compensation Survey - Total Compensation

Solutions • Nonprofit Organizations Salary & Benefits Report – Bluewater

Nonprofit Solutions/The NonProfit Times

Sample of CBIZ Survey Library

22 #CBIZMHMwebinar

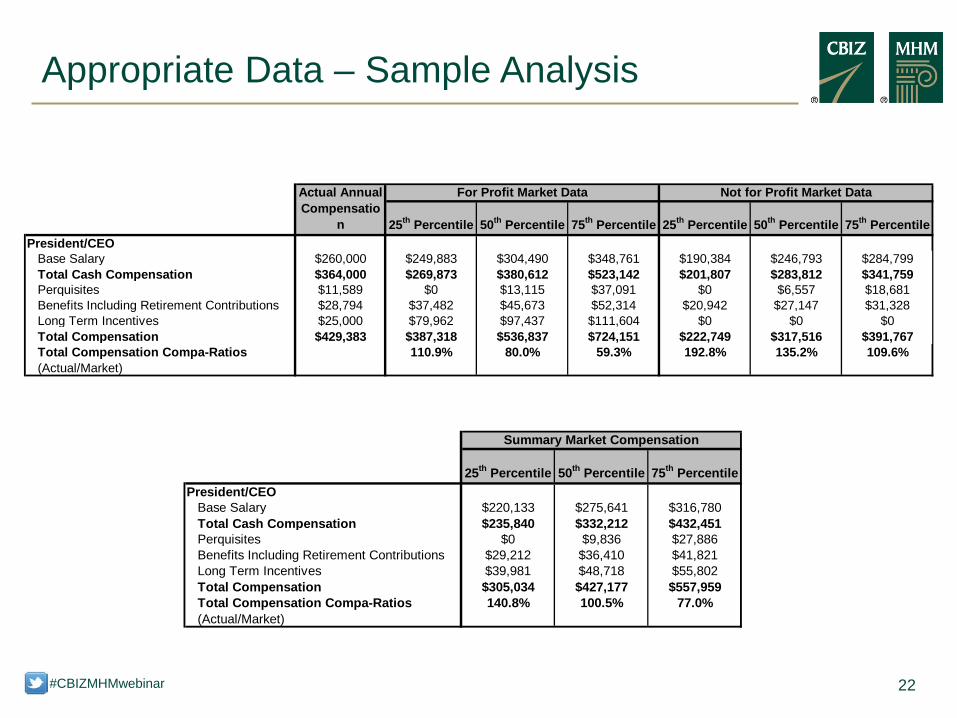

Appropriate Data – Sample Analysis

25th Percentile 50th Percentile 75th Percentile 25th Percentile 50th Percentile 75th PercentilePresident/CEO

Base Salary $260,000 $249,883 $304,490 $348,761 $190,384 $246,793 $284,799Total Cash Compensation $364,000 $269,873 $380,612 $523,142 $201,807 $283,812 $341,759Perquisites $11,589 $0 $13,115 $37,091 $0 $6,557 $18,681Benefits Including Retirement Contributions $28,794 $37,482 $45,673 $52,314 $20,942 $27,147 $31,328Long Term Incentives $25,000 $79,962 $97,437 $111,604 $0 $0 $0Total Compensation $429,383 $387,318 $536,837 $724,151 $222,749 $317,516 $391,767Total Compensation Compa-Ratios (Actual/Market)

110.9% 80.0% 59.3% 192.8% 135.2% 109.6%

Actual Annual Compensatio

n

For Profit Market Data Not for Profit Market Data

25th Percentile 50th Percentile 75th PercentilePresident/CEO

Base Salary $220,133 $275,641 $316,780Total Cash Compensation $235,840 $332,212 $432,451Perquisites $0 $9,836 $27,886Benefits Including Retirement Contributions $29,212 $36,410 $41,821Long Term Incentives $39,981 $48,718 $55,802Total Compensation $305,034 $427,177 $557,959Total Compensation Compa-Ratios (Actual/Market)

140.8% 100.5% 77.0%

Summary Market Compensation

23 #CBIZMHMwebinar

Form 990 Compensation Sections

Form 990 Part VI, Section B, 15 – “rebuttable presumption” question Part VII – Compensation table and related questions

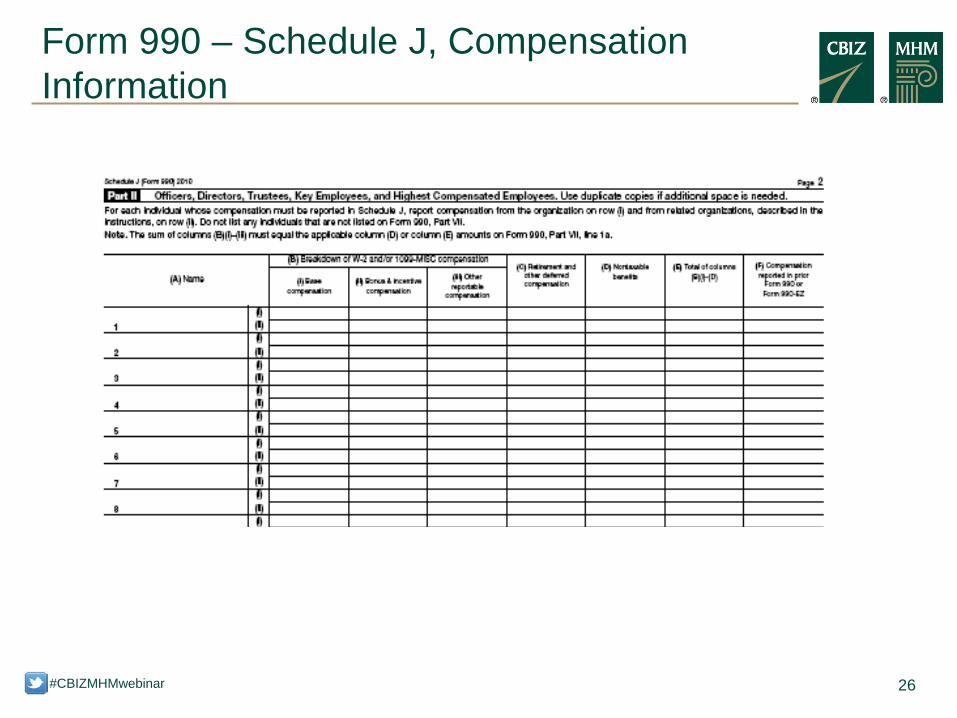

Schedule J – Compensation Information Must be completed if current or former employee being paid over

$150,000 or if Officer or Director receiving compensation from unrelated organization for services rendered to the organization

Requests greater detail regarding types and amounts of compensation paid (including base, bonus, deferred compensation, nontaxable benefits, specific types of perquisites, etc.) and how compensation decisions are made

Schedule O Referenced throughout compensation sections, blank page for

providing greater detail on many compensation and other matters

24 #CBIZMHMwebinar

Form 990 – Rebuttable Presumption

The Form 990 Part VI, Section B, question 15 asks whether or not the organization has made efforts to fulfill the rebuttable presumption standard:

25 #CBIZMHMwebinar

Form 990 – Compensation Information

The Form 990 Part VII requests detailed information regarding compensation:

26 #CBIZMHMwebinar

Form 990 – Schedule J, Compensation Information

27 #CBIZMHMwebinar

Form 990, Schedule O

FEDERAL AND STATE REGULATORY DEVELOPMENTS

29 #CBIZMHMwebinar

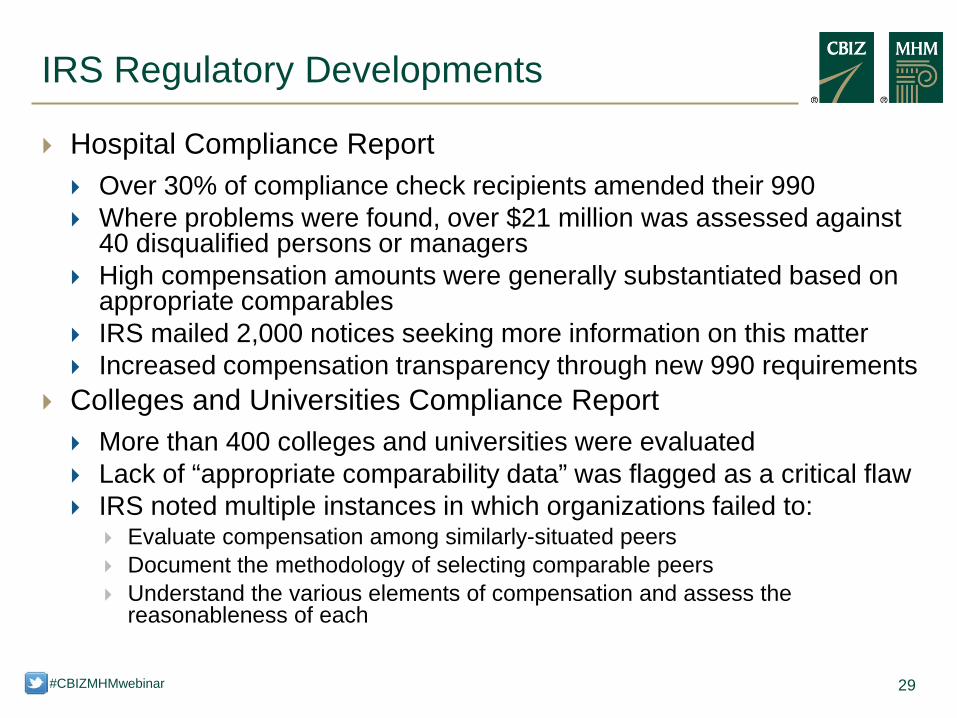

IRS Regulatory Developments

Hospital Compliance Report Over 30% of compliance check recipients amended their 990 Where problems were found, over $21 million was assessed against

40 disqualified persons or managers High compensation amounts were generally substantiated based on

appropriate comparables IRS mailed 2,000 notices seeking more information on this matter Increased compensation transparency through new 990 requirements

Colleges and Universities Compliance Report More than 400 colleges and universities were evaluated Lack of “appropriate comparability data” was flagged as a critical flaw IRS noted multiple instances in which organizations failed to:

Evaluate compensation among similarly-situated peers Document the methodology of selecting comparable peers Understand the various elements of compensation and assess the

reasonableness of each

30 #CBIZMHMwebinar

State Regulatory Environment

Several States have proposed regulations on executive compensation in nonprofit organizations:

New York Implemented Regulations (EO38) For nonprofits that receive more than $500,000 in state

support each year and receive at least 30% of their annual funding from the state, no more than $199,000 in state funds can be used to compensate any executive. At least 75% of state-provided funds must go toward program services. By 2015, at least 85% of funds must be used for program services.

Status: Took effect in January 1, 2013. Currently being challenged successfully and unsuccessfully in court.

TRENDS IN NOT-FOR-PROFIT COMPENSATION

32 #CBIZMHMwebinar #CBIZMHMwebinar

A number of forces are impacting compensation levels in not-for-profits:

Trends

Factors Decreasing Compensation

Factors Increasing Compensation

• Regulatory scrutiny • Public outcry • EO38

• For-profit executives moving into tax-exempt world • Transparency ("me too" affect) • Inclusion of for-profit data in comparisons

33 #CBIZMHMwebinar #CBIZMHMwebinar

Rely on professionals to alleviate Board members’ risk via the “Rebuttable Presumption”

Have the Board approve, in advance, any contract for a suspected disqualified person, relying on appropriate data with documentation of conclusion

Make sure to disclose any and all compensation on 990. Otherwise it may be an automatic excess benefit transaction

Summary – Protect the Organization

DEFINITION OF UNRELATED BUSINESS INCOME (UBIT)

35 #CBIZMHMwebinar #CBIZMHMwebinar

July, 25, 2012 – Second in its series of hearings on tax-exempt organizations, this time examining the revised Form 990, reasons for the increasing organizational complexity of public charities, including unrelated business income tax (UBIT) issues

IRS “College and University Compliance Project Final Report” – April 2013 Analysis of the questionnaire responses on governance, executive compensation, endowments, and unrelated business income: 40 percent on UBIT

May 2013 – Hearing on the IRS’s final report on its Colleges and Universities Compliance Project

Advisory Committee on Tax Exempt and Government Entities – June 11 2014. “Analysis and Recommendation Regarding Unrelated Business Income Tax Compliance of Colleges and Universities”

History and Background

35

36 #CBIZMHMwebinar #CBIZMHMwebinar

UBIT is income from a regularly-carried-on trade or business that is not substantially related to the organization’s exempt purpose

To find out if an activity generates UBIT, conduct the UBIT test Three-part test:

1. A trade or business 2. Regularly carried on 3. Not substantially related

Watch out for The “Fragmentation” Rule

Basic Principles

36

37 #CBIZMHMwebinar #CBIZMHMwebinar

The key issue: Is revenue substantially related to its exempt purpose?

There must be causal relationship between the activities of producing or distributing the goods or performing the services involved and the accomplishment of the entity’s exempt purpose.

What is the primary purpose of sale? “Merely imprinting an object with the museum's name was

insufficient to establish a substantial causal relationship.” (TAM 9550003, 9/18/1995)

Basic Principles

37

38 #CBIZMHMwebinar #CBIZMHMwebinar

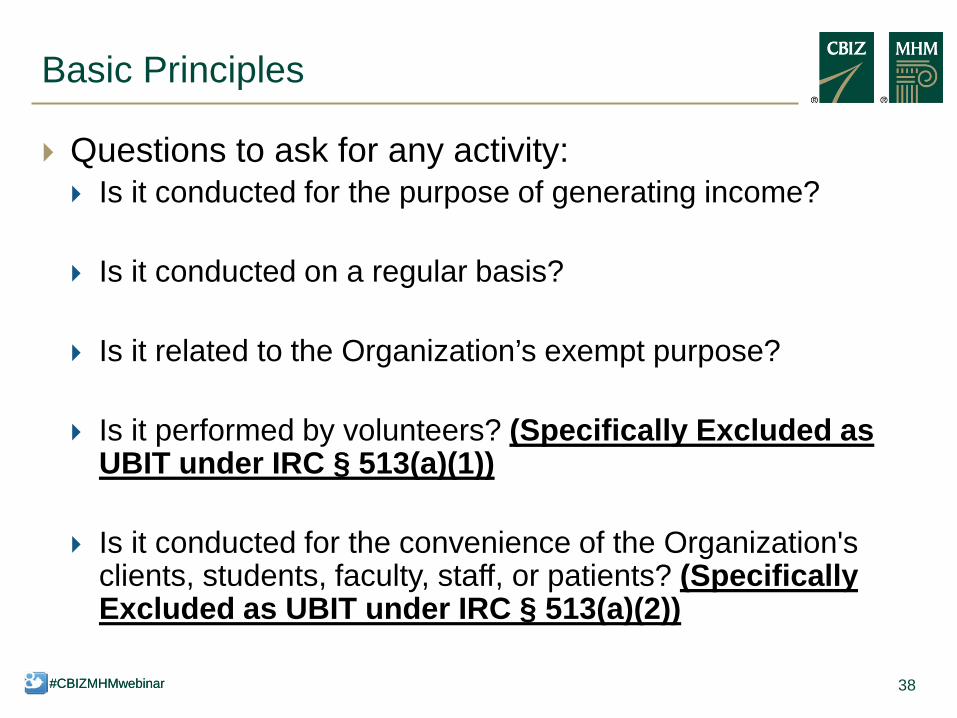

Questions to ask for any activity: Is it conducted for the purpose of generating income?

Is it conducted on a regular basis?

Is it related to the Organization’s exempt purpose?

Is it performed by volunteers? (Specifically Excluded as

UBIT under IRC § 513(a)(1))

Is it conducted for the convenience of the Organization's clients, students, faculty, staff, or patients? (Specifically Excluded as UBIT under IRC § 513(a)(2))

Basic Principles

38

39 #CBIZMHMwebinar #CBIZMHMwebinar

Examples: Hospital pharmacy furnishes supplies to the hospital, but it

also sells to the general public. Sales made to the public are treated as an unrelated trade or business. Regs. 1.513–1(b)

Religious order operated a commercial farm. Operated by the organization’s Brothers, who take a vow of poverty. St. Joseph Farms of Indiana v. Commissioner, 85 T.C. 9 (1985)

Rev. Rul. 76-94, Operation of a retail grocery store by a not-for-profit

Basic Principles

39

ALTERNATIVE REVENUE SOURCES

41 #CBIZMHMwebinar 41

Colleges and Universities Project Final Report

Key Focus Areas – (Applicable to all Tax-Exempt organizations) Unrelated Business Taxable Income (UBTI) Compensation Employment Tax and Retirement Plans

Unrelated Business Taxable Income Thirty-four examinations have resulted in:

Increases to UBTI for 90% of colleges/universities examined, totaling about $90 million

Disallowance of more than $170 million in losses and net operating losses (NOLs)

Primary reasons: Disallowing expenses Errors in computation or substantiation Reclassifying exempt activities as unrelated

42 #CBIZMHMwebinar 42

Colleges and Universities Project Final Report

Alternative Investments another name for “Alternative Revenue” “Colleges and universities are not taxed on income from

activities that are substantially related to their exempt purpose even if the activity is a trade or business.” Many organizations generate UBIT but pay no tax on that income IRS focused on how organizations report their business activities

including the characterization of activities as “exempt” or “unrelated”

The IRS looked at a wide variety of activities including advertising and exclusive provider arrangements, sports management agreements, facility rentals, arenas, food service, golf courses, hotels, recreation centers and programs, parking lots, commercial research and bookstores

43 #CBIZMHMwebinar #CBIZMHMwebinar

Activities

43

Colleges and Universities Project Final Report

44 #CBIZMHMwebinar

Activities

44

Colleges and Universities Project Final Report

45 #CBIZMHMwebinar 45

Colleges and Universities Project Final Report

Activities Top UBIT Loss-Generating Activities

46 #CBIZMHMwebinar

Colleges and Universities Project Final Report

Activities Advertising/Sponsorship Facility Rental Conference Centers Catering/Food Services

46

47 #CBIZMHMwebinar

Colleges and Universities Project Final Report

47

Advertising/Sponsorship Acknowledgements must have the effect of identifying the sponsor

without promoting the sponsor’s products, services or facilities A “qualified sponsorship payment” is a payment in exchange for

which the corporate sponsor neither gets nor expects any return benefit other than: Goods or services, or other benefits, the total value of which does not

exceed two percent of the sponsorship payment; or Recognition (i.e., use or acknowledgment of the sponsor’s name, logo,

or product lines in connection with the nonprofit’s activities) “Advertising” includes any message containing an endorsement,

qualitative or comparative language, price information, other indications of savings or value, or any inducement to purchase, sell, or use the sponsor’s products or services

48 #CBIZMHMwebinar

Colleges and Universities Project Final Report

48

Advertising/Sponsorship The regulations provide six acceptable actions that would

avoid the “substantial benefits realm:” 1. Listing the name or logo or product line of sponsor; 2. Awarding exclusive sponsorship award; 3. Providing logos or slogans that do not contain any qualitative

language or comparative description of the products; 4. Listing of payor's locations, addresses, phone numbers, and

internet addresses; 5. Providing value-neutral descriptions of the sponsor’s product

displays; and 6. Listing sponsor’s brands or trade names.

49 #CBIZMHMwebinar

Colleges and Universities Project Final Report

49

Advertising/Sponsorship There are four items that are prohibited. If any of these items

are done, then you are relegated to traditional UBIT analysis: 1. advertising; 2. designating a sponsor as an exclusive provider; 3. providing facilities, services or other privileges to the sponsor

unless they are of “insubstantial value”; and 4. granting of either exclusive or nonexclusive rights to use

sponsor’s intangible asset (e.g., name or logo)

50 #CBIZMHMwebinar

Colleges and Universities Project Final Report

50

Facility Rental Exceptions noted in Study:

the rental income is excluded by IRC §512(b)(3); (not debt financed) the income was substantially related to the college‘s or university‘s

exempt purpose; and the rental activity was conducted primarily for the convenience of

the college’s or university‘s student body or faculty

51 #CBIZMHMwebinar

Colleges and Universities Project Final Report

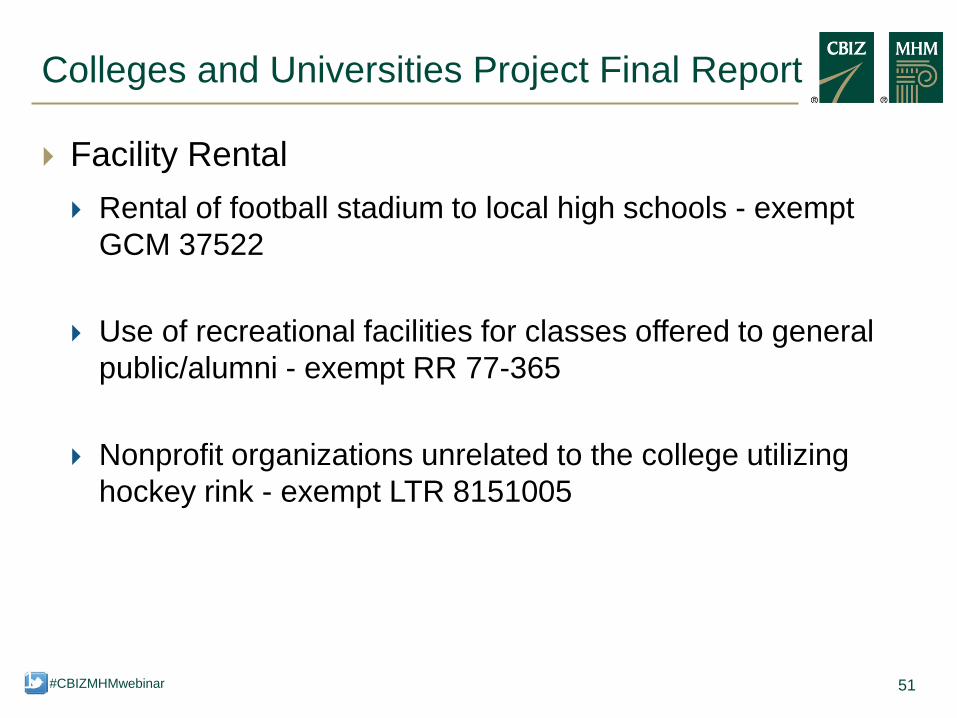

Facility Rental Rental of football stadium to local high schools - exempt

GCM 37522

Use of recreational facilities for classes offered to general public/alumni - exempt RR 77-365

Nonprofit organizations unrelated to the college utilizing hockey rink - exempt LTR 8151005

51

52 #CBIZMHMwebinar

Colleges and Universities Project Final Report

52

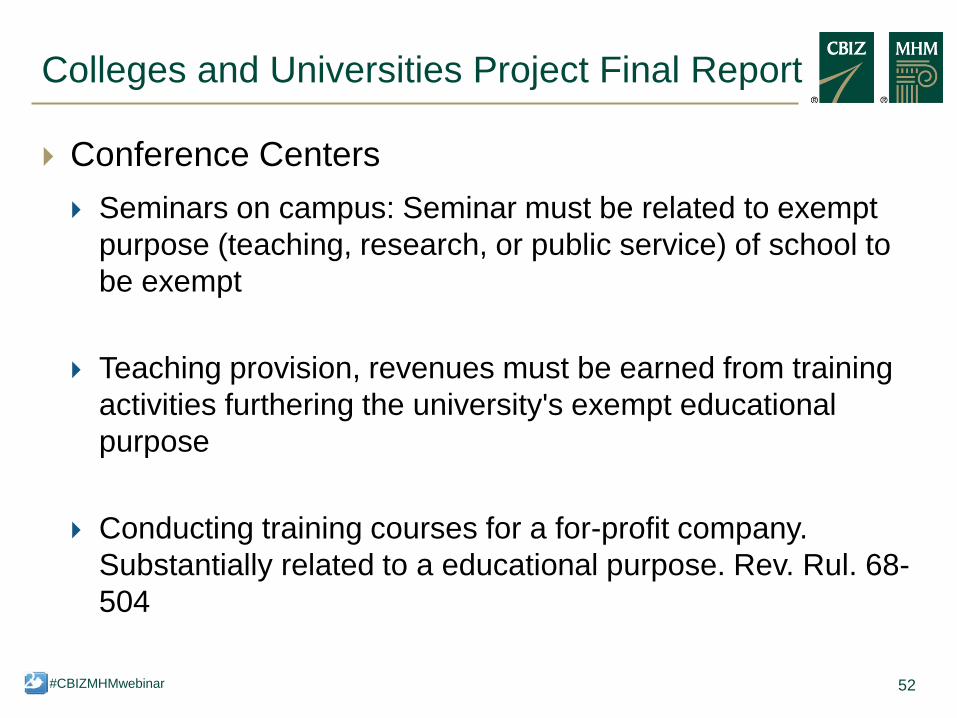

Conference Centers Seminars on campus: Seminar must be related to exempt

purpose (teaching, research, or public service) of school to be exempt

Teaching provision, revenues must be earned from training activities furthering the university's exempt educational purpose

Conducting training courses for a for-profit company. Substantially related to a educational purpose. Rev. Rul. 68-504

53 #CBIZMHMwebinar

Colleges and Universities Project Final Report

53

Catering/Food Services A college owns and operates a hotel and restaurant located

close to school Located in a remote area and there are no other reasonably

available food and lodging facilities to serve visitors to the college Special circumstances may exist bringing the operation of the hotel

and restaurant within the convenience exception (IRS 1980 EO CPE)

54 #CBIZMHMwebinar

Advisory Committee on Tax Exempt and Government Entities

Analysis and Recommendations Regarding Unrelated Business Income Tax Compliance of Colleges and Universities – June 11, 2014

The Exempt Organizations Division should expeditiously formalize and adopt a new Form 990-T “The IRS EO Division should recommend that Chief Counsel and

Treasury open a regulation project so that profits from a substantial commercial activity will not preclude exemption…”

“The EO Division should….to publish a comprehensive revenue ruling on a range of UBI issues. The ruling should provide categories of activities that will be considered related and unrelated.”

54

Colleges and Universities Project Final Report

55 #CBIZMHMwebinar

Advertising Arena Rental Athletic Facility Usage Book Store Catalog Sales Catering Services Commercial Research Computer Services Conference Center Operation Credit Card Promotion Debt Financed Income Exclusive Use Contracts Exploited Exempt Activity Income Facility Rental Food Services Golf Course Hotel Operation

Income from Controlled Organizations Intellectual Property Internet Sales Parking Lot Operations Partnership Allocations Patents Personal Property Rentals Power Generations Recreation Center Usage Restaurant Operation S-Corp Allocations Sale of Space in Periodicals Telecomm Related Rentals Travel Tours Working Interest in Oil, Gas, etc. "List of other UBIT activities below" There are more?

Colleges and Universities Project Final Report

55

56 #CBIZMHMwebinar

Rents From Real Property

56

Normally exclude rents from real property, including elevators and escalators, when calculating UBIT For example, 501(c)(3) rents out an assembly hall for special

events. Provide no additional services such as bartending, you can exclude the rental income.

However, the exclusion does not apply to: Rents from debt-financed real property

Under § 514(c)(9), exempt organizations are excused from the debt-financed property. The following organizations (three others not covered) are qualified: Educational organizations described in § 170(b)(1)(A)(ii); and, Qualified trusts under § 401

57 #CBIZMHMwebinar

Rents From Real Property

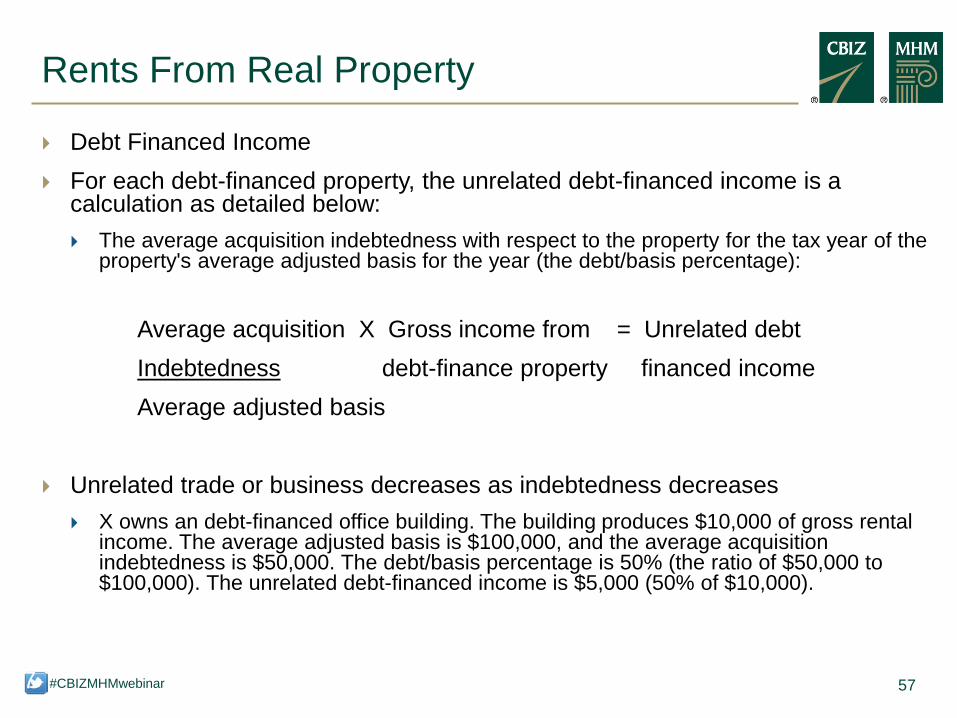

Debt Financed Income For each debt-financed property, the unrelated debt-financed income is a

calculation as detailed below: The average acquisition indebtedness with respect to the property for the tax year of the

property's average adjusted basis for the year (the debt/basis percentage):

Average acquisition X Gross income from = Unrelated debt Indebtedness debt-finance property financed income Average adjusted basis Unrelated trade or business decreases as indebtedness decreases

X owns an debt-financed office building. The building produces $10,000 of gross rental income. The average adjusted basis is $100,000, and the average acquisition indebtedness is $50,000. The debt/basis percentage is 50% (the ratio of $50,000 to $100,000). The unrelated debt-financed income is $5,000 (50% of $10,000).

57

58 #CBIZMHMwebinar

Rents From Real Property

Arena Rental Most universities have athletic facilities (tennis courts,

gymnasiums, canoe rentals, etc.) that are used in physical education programs/college athletic events. Exempt purpose. Often the school allows the general public to use these facilities for a

fee Use by faculty and staff will be considered related, however use by

alumni and the general public may result in unrelated business income, unless it meets the Real Property Rental Income exclusion or any other exception

Entertainment events conducted by a university in which the school’s own students put on the event (e.g., play, recital or ballet) are treated as a related activity, even if a substantial portion of the audience and revenues come from the general public

58

59 #CBIZMHMwebinar

Rents From Real Property

Arena Rental Regulation 1.513-1(d)(4)(iv) example (2) holds that a university

sponsoring professional theater companies and symphony orchestras does not have unrelated income from the conduct of the performances. “....the presentation of such drama and music events contributes importantly to the overall educational and cultural function of the university.”

Entertainment events involving professional entertainers. Examples of these events include rock concerts, tractor pulls, and string quartets. The distinguishing characteristic is not the “cultural” nature of the event (or lack thereof) but rather whether it is a professional performance involving paid performers.

The IRS views these paid entertainment activities as being related only if they are “operated as an integral part of the educational program of the university, but are unrelated if operated in substantially the same manner as a commercial operation.”

59

60 #CBIZMHMwebinar

Rents From Real Property

Telecomm Related Rentals Broadcast towers are classified as personal property, thus

rental income received from lease of space on the towers to other not-for profit, governmental, and other for-profit groups will be UBIT

A broadcast tower, which was leased by an EO to a company providing paging services, was tangible personal property. LTR 200104031

Solution: Lease the space for the tower and let the communication company build and maintain tower

60

61 #CBIZMHMwebinar

Internet Sales

IRS personnel have been trained to look at your website for unrelated business income and other tax and non-tax issues

No restrictions on access – agents can audit you from virtually anywhere!

Internet issues: Website “advertising” vs “corporate sponsorships” Website solicitation of contributors Links (such as, to a business) and banners Merchant affiliate programs Lobbying Unrelated Business Income Tax – Online Stores

Note: The IRS has stated, “the use of the Internet to accomplish a particular task does not change the way the tax laws apply to that task. Advertising is still advertising, and fundraising is still fundraising.”

61

62 #CBIZMHMwebinar

Internet Sales

Merchant affiliate programs A link from the NFP website to a merchant’s web page can be

characterized only specific facts and circumstances Some links simply state that “We receive a royalty on ...books

purchased through X bookseller.” The exempt organization earns a percentage of sales of exempt

books as well as a lesser commission on other purchases via the link

An NFP’s commissions from sales by affiliated merchants can be analyzed using rules similar to those for merchandise sales

Merchandise sales items are looked at from the point of view of whether they contribute to the NFP’s exempt purpose

62

63 #CBIZMHMwebinar

Internet Sales

Unrelated Business Income Tax – Online Stores Sales of Merchandise via Website – PLR 200722028

M’s exempt purpose is to educate the general public about breast cancer

M also offers R merchandise via its website. R is the universal symbol of breast cancer. The color of R is also recognized as the universal color denoting breast cancer awareness.

The merchandise ranges from apparel, jewelry and other items that can be worn to promote awareness and early detection of breast cancer

Merchandise sales items are looked at from the point of view of whether they contribute to the NFP’s exempt purpose.

63

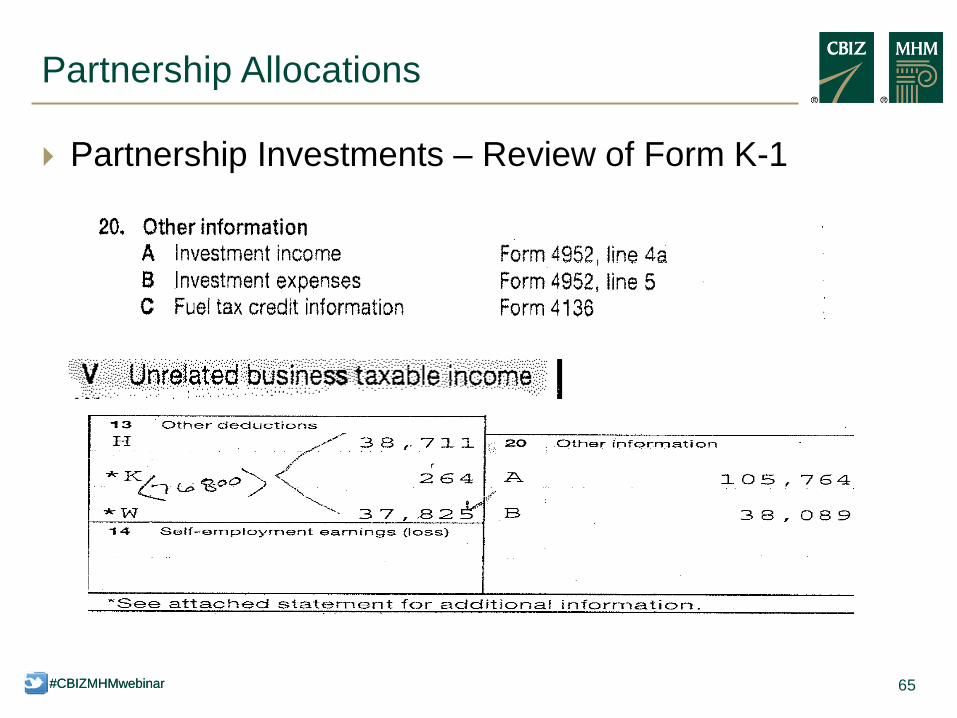

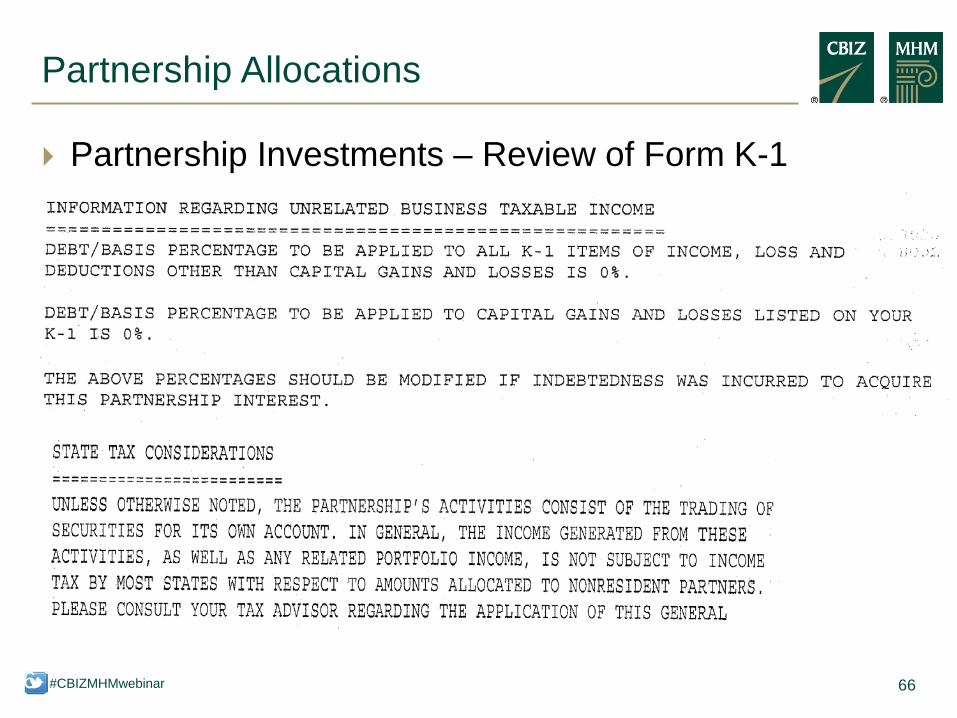

64 #CBIZMHMwebinar 64

Partnership Investments – Review of Form K-1

Partnership Allocations

65 #CBIZMHMwebinar #CBIZMHMwebinar

Partnership Allocations

65

Partnership Investments – Review of Form K-1

66 #CBIZMHMwebinar

Partnership Allocations

66

Partnership Investments – Review of Form K-1

67 #CBIZMHMwebinar

Partnership Allocations

67

Partnership Investments – Review of Form K-1

68 #CBIZMHMwebinar

Partnership Allocations

68

Partnership Investments – Review of Form K-1

69 #CBIZMHMwebinar

Partnership Allocations

69

Current focus of IRS Scrutiny IRS is developing risk models to extrapolate data and target

specific activities IRS is specifically targeting NOL of three years or more Know your activities/investments before undertaking Foreign Account Tax Compliance Act (FATCA) agreements in

the works Take an inventory of investments Prepare a Schedule K-1 summary work paper. Summary

should include: Year-end of investment State filing requirements (nexus)

70 #CBIZMHMwebinar

Partnership Allocations

70

Current focus of IRS Scrutiny (continued) Whether investment is in foreign partnership and foreign

corporation Additional filing requirement may include: Form 926, Return by a U.S. Transferor of Property to a Foreign

Corporation Form 5471, Information Return of U.S. Persons With Respect to

Certain Foreign Corporations Form 5713, International Boycott Report Form 8621, Return by a Shareholder of a Passive Foreign

Investment Company or Qualified Electing Fund Form 8858, Information Return of U.S. Persons With Respect To

Foreign Disregarded Entities

71 #CBIZMHMwebinar

Partnership Allocations

71

Current focus of IRS Scrutiny (continued) Additional filing requirement may include (continued):

Form 8865, Return of U.S. Persons With Respect to Certain Foreign Partnerships

Form 8886, Reportable Transaction Disclosure Statement Form 8886-T, Disclosure by Tax-Exempt Entity Regarding Prohibited

Tax Shelter Transaction TD F 90-22.1, Report of Foreign Bank and Financial Accounts (FBAR)

Substantial penalties for failure to file these additional forms Work closely with investment managers and try obtain periodic

updates on investments Information suitable to calculate the organization’s share of

partnership income must be provided by the investment manager

72 #CBIZMHMwebinar 72

Alternative Revenue - Royalties

The term “royalties” is not defined in either the Internal Revenue Code or the regulations

Royalty, “payment must relate to the use of a valuable right.” Payments for the use of trademarks, trade names, service

marks, or copyrights Royalty treatment will often be precluded where there is

an element of personal services performed in return for the “royalty” and must be passive, such as: Endorse products Services in personal appearances and interviews

73 #CBIZMHMwebinar 73

Alternative Revenue - Royalties

Affinity Fundraising Charity partners with a business or corporation The business enterprise gives the charity a rebate, commission, or

percent of sales in exchange for driving customers to its store or website

The more customers a nonprofit refers, the larger the contribution the company makes

If the agreement is structured properly, the payment constitutes tax free royalty

74 #CBIZMHMwebinar 74

Alternative Revenue - Royalties

Licensing Agreements and Naming Rights Exempt organizations are entitled to a royalty exclusion (not taxed) for

licensing fees As a general rule, passive royalty income is excepted from the definition of

UBIT The payments must be for the use of valuable intangible property rights (i.e.,

use of a name or logo and the charity must maintain a passive role) Logo or Name

An organization’s name and logo have intrinsic value Licensing the organization’s name or logo can generate significant royalties Agreements should state that organization will not require them to provide any

personal services (e.g., promotion of the credit card) Examples

Red Cross licensing of their cross on ambulances and first-aid kits Sierra Club credit card income from affinity card arrangements were royalties and not

subject to UBIT

75 #CBIZMHMwebinar 75

Alternative Revenue - Royalties

Intellectual Property/Patents Software Development – PLR 201024069: An employee of

an exempt church designed computer software for the church’s use For-profit entities purchased the intellectual property rights to the

software Church sold the software to a third-party and received cash

proceeds and a perpetual license in return The IRS stated “sale of the intellectual property rights to Y is not a

continuous and consistent income producing activity because you performed or carried on this activity once.”

76 #CBIZMHMwebinar 76

Alternative Revenue - Royalties

Be Creative! Social Media

Ice Bucket Challenge:

Technology National Museum of the American

Indian Video machine in front lobby or in front

of a new wing

For Profit collaboration Cystic Fibrosis Foundation

Tax Law Exceptions

77 #CBIZMHMwebinar 77

Action Plan

Conduct a Risk Assessment Analysis: The Assessment will help identify risks based upon the recently

completed IRS Compliance Project Inventory your organizations’ revenue producing activities:

Identify any “new” activity during the current year with a potential for generating unrelated business income (Consider relatedness/unrelatedness to mission)

Take a “fresh” look at “old” activities (Consider relatedness/unrelatedness to mission)

Understand the IRS criteria for the activity to considered UBI: The IRS considers an activity to be unrelated if it meets all of the

following criteria: it is not substantially related to the organization’s tax-exempt purposes; it is a trade or business (defined by the IRS as any activity carried on for the

production of income from selling goods or performing services); and, it is regularly conducted (frequency and continuity are key in this assessment).

78 #CBIZMHMwebinar

Action Plan

78

Conduct a Risk Assessment Analysis: With respect to unrelated trade or business, consider:

Methodologies are consistent and reasonable? “Systematic and Rational Method”

Expenses have adequate connections to UBI activities Methodologies should be reviewed on occasion in case of

internal/external changes Risky or IRS scrutinized activities (e.g., advertising,

sponsorship, internet, rental of facilities, joint ventures, printing, etc.) or activities similar to for-profit activities should be reviewed

Appropriate documentation with position/conclusions supported by code section/regulations or IRS rulings should be maintained

Consultation with a Tax Professional

79 #CBIZMHMwebinar #CBIZMHMwebinar

Questions?

80 #CBIZMHMwebinar #CBIZMHMwebinar

Join us for these upcoming courses: 12/11 & 12/16: Fourth Quarter Accounting and Financial Reporting

Issues Update 12/17: Terms and Inherent Risks of Retirement Plan Investments

Read these related publications: Best Practices in the Financial Statement Reporting Process Web Presence & Internet Concerns for Nonprofit Organizations:

Fundraising Five Practices to Improve Your Organization's Governance

Sign up to receive our Not-for-Profit Viewpoint e-newsletter

If You Enjoyed This Webcast…

81 #CBIZMHMwebinar #CBIZMHMwebinar

Connect with Us

linkedin.com/company/ mayer-hoffman-mccann-p.c.

@mhm_pc

youtube.com/ mayerhoffmanmccann

slideshare.net/mhmpc

linkedin.com/company/ cbiz-mhm-llc

@cbizmhm

youtube.com/user/BizTipsVideos

slideshare.net/CBIZInc

MHM CBIZ