Friday, March 25, 2022 Friday, March 25, 2022 1 Crisis Crisis Presentation to Presentation to Students & Friends of Rensselaer Students & Friends of Rensselaer Hartford Hartford Hartford, CT Hartford, CT James Stodder, (Ph.D., Economics, Yale 1990) Lally School of Management & Technology Rensselaer Polytechnic Institute at Hartford Hartford, Connecticut, USA

Transcript

Wednesday, April 19, 2023Wednesday, April 19, 2023 11

Understanding the Financial CrisisUnderstanding the Financial Crisis Presentation toPresentation to

Students & Friends of Rensselaer HartfordStudents & Friends of Rensselaer HartfordHartford, CTHartford, CT

James Stodder, (Ph.D., Economics, Yale 1990)Lally School of Management & Technology

Rensselaer Polytechnic Institute at HartfordHartford, Connecticut, USA

Outline of TalkOutline of Talk

1.1. Keynes on Credit Cycles: Keynes on Credit Cycles: - Why we need Regulation- Why we need Regulation

2.2. Where is the Bottom?Where is the Bottom?

3.3. Connecticut is “Middle of the Pack”Connecticut is “Middle of the Pack”

4.4. Government Deficit SpendingGovernment Deficit Spendinga.a. Needed in the Short-termNeeded in the Short-term

b.b. But a Big Problem Long-termBut a Big Problem Long-term

Wednesday, April 19, 2023Wednesday, April 19, 2023 22

(1) Biz & Credit Cycles (1) Biz & Credit Cycles J. M. Keynes: 1883-1946J. M. Keynes: 1883-1946

Wednesday, April 19, 2023Wednesday, April 19, 2023 33

Wednesday, April 19, 2023Wednesday, April 19, 2023 44

US Macro-Stability: US Macro-Stability: Better, Room for Improvement Better, Room for Improvement

Source: http://www.nber.org/cycles.html

45% 55%

66%34%

Bad News: Bubbles are Bad News: Bubbles are EndemicEndemic

Wednesday, April 19, 2023Wednesday, April 19, 2023 55

Wednesday, April 19, 2023Wednesday, April 19, 2023 88

““A sound banker, alas, is not one A sound banker, alas, is not one who foresees danger and avoids who foresees danger and avoids

it, but one who, when he is ruined, it, but one who, when he is ruined, isis ruined in a conventional way,ruined in a conventional way, along with his fellows,along with his fellows, so that no so that no one can really blame him.” one can really blame him.”

- J.M. Keynes (1931)- J.M. Keynes (1931)

Wednesday, April 19, 2023Wednesday, April 19, 2023 99

“Paradox of Thrift” Keynes noted:

Consumers cut back on their spending and save more during a recession. This only makes the recession worse.

Similarly for Banks, Loan Loss Reserves (LLR) are often raised in a recession, just when households and businesses most need credit –ensuring more collapses and worsening the recession.

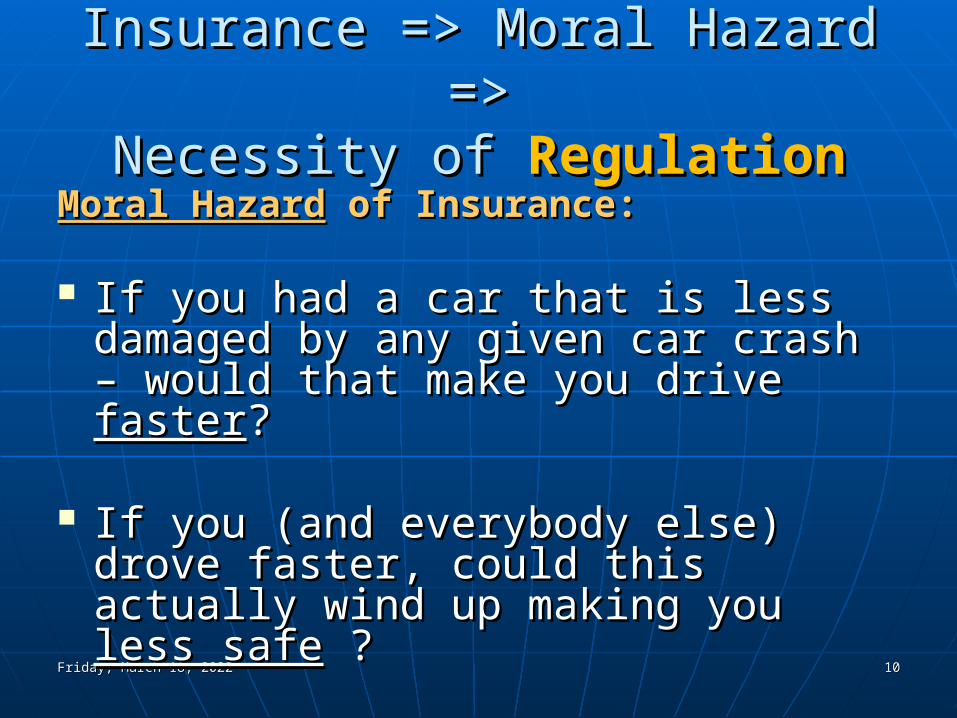

Insurance => Moral Hazard =>Insurance => Moral Hazard =>Necessity of Necessity of RegulationRegulation

Wednesday, April 19, 2023Wednesday, April 19, 2023 1010

Moral HazardMoral Hazard of Insurance: of Insurance:

If you had a car that is less damaged If you had a car that is less damaged by any given car crash – would that by any given car crash – would that make you drive make you drive fasterfaster??

If you (and everybody else) drove If you (and everybody else) drove faster, could this actually wind up faster, could this actually wind up making you making you less safeless safe ? ?

Wednesday, April 19, 2023Wednesday, April 19, 2023 1111

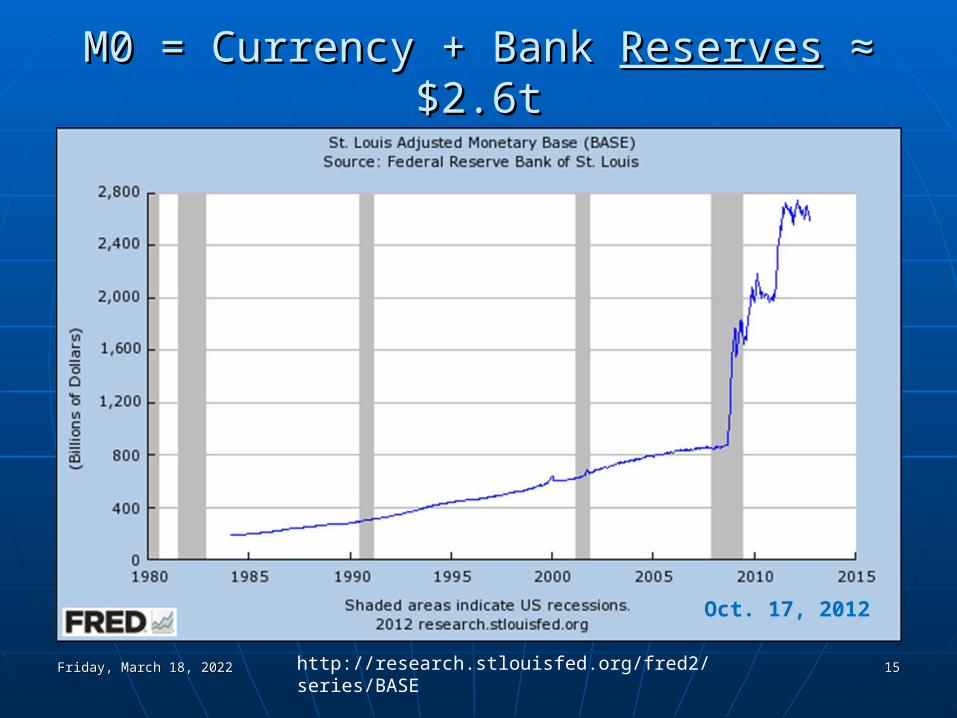

i.e., i.e., %%∆∆M + M + %∆%∆V = V = %%∆∆P + P + %%∆∆Y over Y over timetime

Wednesday, April 19, 2023Wednesday, April 19, 2023 2323

Apr 19, 2023Apr 19, 2023 2424

%∆ Money Turnover [ %∆ Money Turnover [ = %∆ (= %∆ (MMoney x oney x VVelocity) elocity) ] ] is Too is Too ProPro-Cyclical because of -Cyclical because of VelocityVelocity

% ∆ (M x V)

% ∆ V

% ∆M

Wednesday, April 19, 2023Wednesday, April 19, 2023 2525

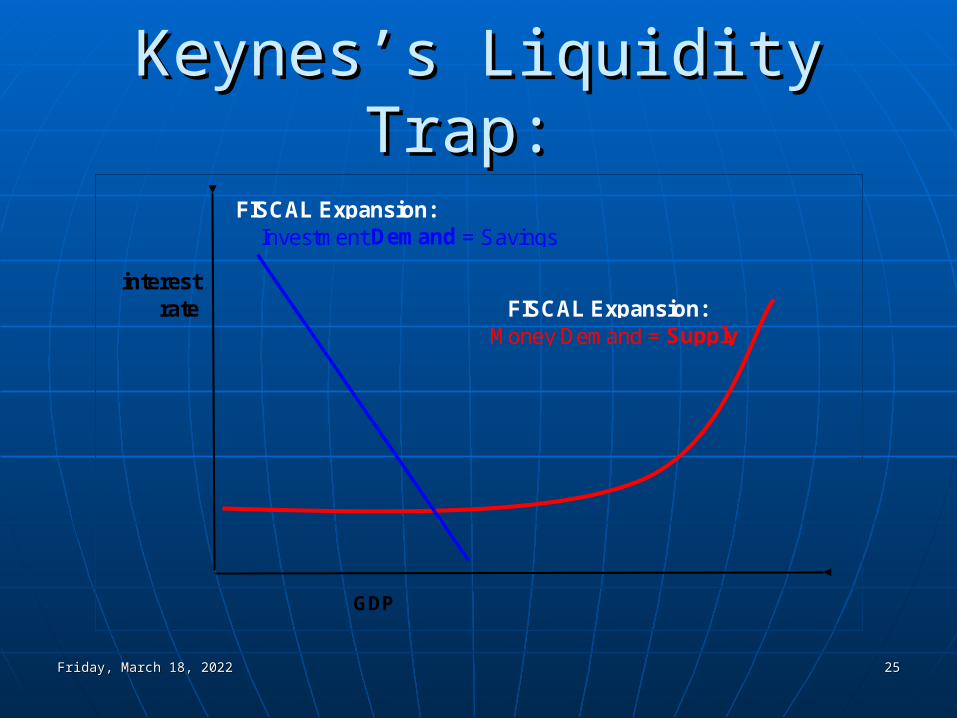

FISCAL Expansion: Investment Demand = Savings

interest rate FISCAL Expansion:

Money Demand = Supply

GDP

Keynes’s Liquidity Trap: Keynes’s Liquidity Trap:

Wednesday, April 19, 2023Wednesday, April 19, 2023 2626

Investment Demand = Savings

interest rate

Money Demand = Supply

GDP

FISCAL Expansion: Investment Demand = Savings

interest rate MONETARY Expansion:

Money Demand = Supply

GDP

Keynes’s Liquidity Trap: Keynes’s Liquidity Trap:

Wednesday, April 19, 2023Wednesday, April 19, 2023 2727

FISCAL Expansion: Investment Demand = Savings

interest rate FISCAL Expansion:

Money Demand = Supply

GDP

Keynes’s Liquidity Trap: Keynes’s Liquidity Trap:

Wednesday, April 19, 2023Wednesday, April 19, 2023 2828

Wednesday, April 19, 2023Wednesday, April 19, 2023 3535

(2) Bottom Still a Ways Off(2) Bottom Still a Ways Off Okun’s Law, and Slow RecoveryOkun’s Law, and Slow Recovery Housing RecoveryHousing Recovery probably still a year probably still a year

away.away. Credit Markets Credit Markets still very weak.still very weak. Stock Market Valuation Ratios Stock Market Valuation Ratios like P/E like P/E

and Tobin’s Q are now only at and Tobin’s Q are now only at historical historical averagesaverages..

Wednesday, April 19, 2023Wednesday, April 19, 2023 4040http://cr4re.com/charts/charts.html

(3) CT & NY in “Middle of Pack”(3) CT & NY in “Middle of Pack”

Financial Sector down, but ..Financial Sector down, but .. Conventional Banking and Insurance Conventional Banking and Insurance

less vulnerable than Investment less vulnerable than Investment Banks, Financial InsuranceBanks, Financial Insurance

Defense industries well insulatedDefense industries well insulated Pharmaceuticals and Biotech have Pharmaceuticals and Biotech have

good long-term prospectsgood long-term prospects House Price Increases near US Avg.House Price Increases near US Avg.Wednesday, April 19, 2023Wednesday, April 19, 2023 4141

International Housing PricesInternational Housing Prices

Wednesday, April 19, 2023Wednesday, April 19, 2023 4242

Wednesday, April 19, 2023Wednesday, April 19, 2023 4343

Sun Belt, Rust Belt ConcentrationSun Belt, Rust Belt Concentration

Wednesday, April 19, 2023Wednesday, April 19, 2023 4444

2006 Peak of Price-to-Rent2006 Peak of Price-to-Rent

Wednesday, April 19, 2023Wednesday, April 19, 2023 4545Source: NY Times, April 20, 2010

(4) More Federal Deficit Spending (4) More Federal Deficit Spending (not Tax Cuts) Necessary(not Tax Cuts) Necessary

Tax cuts to the rich more likely to be Tax cuts to the rich more likely to be saved, not spent or invested.saved, not spent or invested.

Tax cuts don’t have big effect on Tax cuts don’t have big effect on those too poor to pay many taxes.those too poor to pay many taxes.

Unmet needs in Energy, Environment, Unmet needs in Energy, Environment, Health, and Education: good reasons Health, and Education: good reasons to spend.to spend.

Wednesday, April 19, 2023Wednesday, April 19, 2023 4646

Government Must Government Must Increase Increase SpendingSpending in Severe Recession in Severe Recession

“ “ If the Treasury were to If the Treasury were to fill old bottles with fill old bottles with banknotesbanknotes, bury them at suitable depths in , bury them at suitable depths in disused coal mines …disused coal mines …

It would, indeed, be It would, indeed, be more sensible to build more sensible to build

houses houses and the like; but if there are and the like; but if there are political and practical difficulties in the political and practical difficulties in the way of this, the above would be better way of this, the above would be better than nothing.” than nothing.” (Keynes, (Keynes, General TheoryGeneral Theory, 1937), 1937)

Wednesday, April 19, 2023Wednesday, April 19, 2023 4747

But We Need But We Need Foreign Coordination Foreign Coordination for US Expansion to be Successfulfor US Expansion to be Successful

Benefits of lone expansion “leak Benefits of lone expansion “leak out,” other countries free ride.out,” other countries free ride.

Alternatives to joint expansion are Alternatives to joint expansion are protectionism and competitive protectionism and competitive devaluations.devaluations.

US long-term “Fiscal Gap” makes US long-term “Fiscal Gap” makes lone expansion untenable. lone expansion untenable.

Wednesday, April 19, 2023Wednesday, April 19, 2023 4848

Wednesday, April 19, 2023Wednesday, April 19, 2023 4949

Long Term Fiscal Gap: Long Term Fiscal Gap: UnsustainableUnsustainable

• Germany after WWI• Russia after the Revolution• Soviet Union after the Cold War• Many Developing Countries after spending, investment binges

(See L. Kotlikoff & S. Burns, The Coming Generational Storm, 2004)

Wednesday, April 19, 2023Wednesday, April 19, 2023 5454

Inflation/Devaluation Appears Inflation/Devaluation Appears a “Painless” Way Out of Debta “Painless” Way Out of Debt

Summary of ConclusionsSummary of Conclusions RecessionRecession is is long and deeplong and deep: housing slump, : housing slump,

interbank lending, financial markets likely to interbank lending, financial markets likely to “overshoot” on low side.“overshoot” on low side.

CT, NYCT, NY are “ are “middle of the packmiddle of the pack” for housing ” for housing prices and employment stability.prices and employment stability.

Greatly expanded federal spending Greatly expanded federal spending is is needed in the needed in the short-termshort-term..

Long-termLong-term, however, US government , however, US government debt is debt is unsustainableunsustainable..

Wednesday, April 19, 2023Wednesday, April 19, 2023 5555