10

Weekly Market Review September 20, 2015 – September 26, 2015 September 27, 2015

Weekly Market Review September 20, 2015 – September 26, 2015

September 27, 2015

Page I 2

CONTENTS

International Equity Markets

GCC Equities

Currencies

Commodities

Interest Rates

Equity Markets - Top Most & Bottom Most

Commodity Markets - Top Most & Bottom Most

Page I 3

US GDP expanded 3.9% in 2Q2015, faster than 3.7% estimated earlier on stronger consumer spending, construction

Fed chief Janet Yellen said she expects interest rates to increase in 2015, easing global growth concerns

US existing home sales dropped 4.8% in Aug, giving a cautionary sign for the otherwise strong US housing market

Markit’s flash US services PMI slipped to 55.6 in Sep from 56.1 in Aug as new business expansion slowed

Manufacturing PMI by Markit stood at 53 in Sep, the same as in Aug which was weakest in almost 2 years

University of Michigan’s final consumer sentiment index fell to 87.2 in Sep from 91.9 in Aug

Markit’s Eurozone flash composite PMI dipped to 53.9 in Sep vs. 54.3 in Aug indicating business growth slowed

Lending to Eurozone households & corporate inched up sluggishly by 1.0% & 0.4% YoY, respectively in Aug

German real wages rose by 2.7% in 2Q2015 aided by low inflation, the strongest increase on records since 2008

Alexis Tsipras got re-elected as Greece’s PM; vowed to quickly implement measures needed for 3rd bailout

Japan’s core consumer prices fell 0.1% YoY in Aug, marking 1st fall since BoJ deployed its massive stimulus program

Shinzo Abe vowed to raise Japan’s GDP by nearly a quarter to ¥600tn, without setting a timeframe

Manufacturing activity expansion slowed as Markit/Nikkei flash PMI slid to 50.9 in Sep vs. 51.7 in Aug

Japan lowered its economic assessment due to risks posed by China and a US interest rate hike

Asian Development Bank cut Asia’s growth forecast to 5.8% & 6.0% from 6.1% & 6.2% in 2015 & 2016, respectively

China said economy is expected to grow around 7% in 3Q2015 as impact from stock market plunge will be limited

China will cut administration fees worth up to yuan 4bn including real estate sector to prop economy

Caixin/Markit China flash manufacturing PMI unexpectedly fell to 47 in Sep, the worst since Mar 2009

Brazilian Central Bank’s economic activity index fell at a slower than expected pace by 0.2% MoM in July

Brazil revised its 2015 recession estimate to2.44% from 1.49%, in-line with market expectations

Myanmar opened $1.5bn manufacturing complex before elections, aimed at luring investments & creating jobs

S&P 500 – 1 year performance Euro Stoxx 600 – 1 year performance

Source: Bloomberg, Mashreq Private Banking; *Current

INTERNATIONAL EQUITY MARKETS

Last Close 5 Day % YTD % P/E (2015) *Div. Yield

S&P 500 1,931.34 -1.36 -6.20 16.36 2.24

DJI 16,314.67 -0.43 -8.46 14.91 2.62

Nasdaq Comp 4,686.50 -2.92 -1.05 20.49 1.32

Euro Stoxx 600 349.28 -1.55 1.97 15.07 3.66

FTSE 100 6,109.01 0.08 -6.96 15.17 4.27

Dax 9,688.53 -2.30 -1.19 11.79 3.06

CAC 40 4,480.66 -1.22 4.87 14.58 3.36

Nikkei 225 17,880.51 -1.05 2.46 16.88 1.66

Hang Seng 21,186.32 -3.35 -10.25 10.57 4.04

Brazil - Bovespa

44,831.46 -5.15 -10.35 12.53 4.44

Russia - Micex 1,639.64 -4.16 17.40 5.73 5.08

BSE Sensex 25,863.50 -1.36 -5.95 16.29 1.44

Shanghai Comp 3,092.35 -0.18 -4.40 13.11 1.98

Source: Bloomberg, Mashreq Private Banking

Page I 4

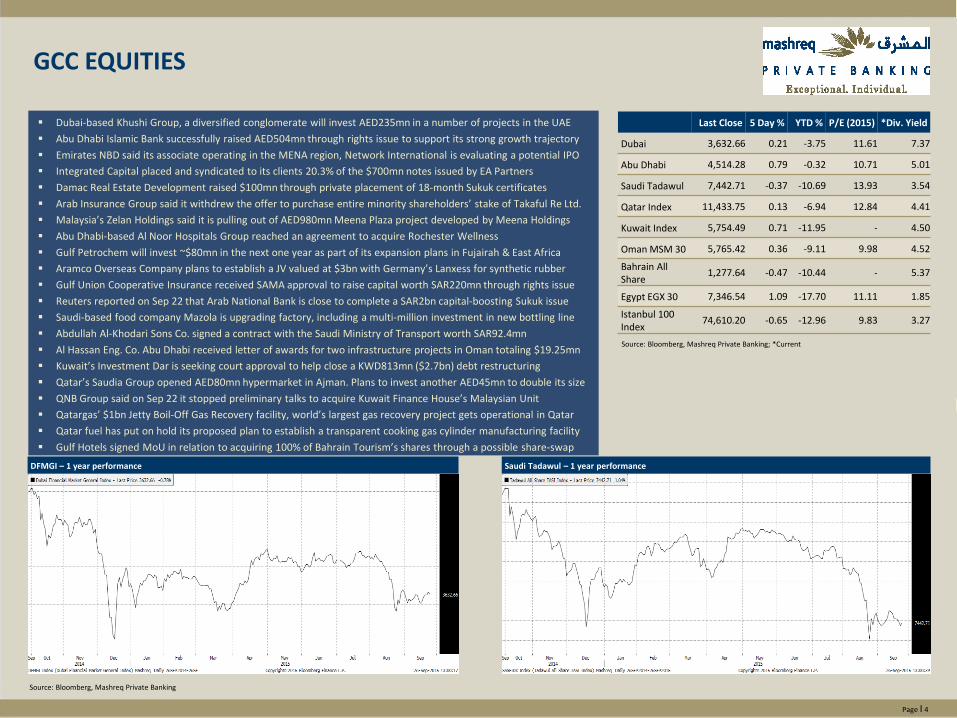

Dubai-based Khushi Group, a diversified conglomerate will invest AED235mn in a number of projects in the UAE

Abu Dhabi Islamic Bank successfully raised AED504mn through rights issue to support its strong growth trajectory

Emirates NBD said its associate operating in the MENA region, Network International is evaluating a potential IPO

Integrated Capital placed and syndicated to its clients 20.3% of the $700mn notes issued by EA Partners

Damac Real Estate Development raised $100mn through private placement of 18-month Sukuk certificates

Arab Insurance Group said it withdrew the offer to purchase entire minority shareholders’ stake of Takaful Re Ltd.

Malaysia’s Zelan Holdings said it is pulling out of AED980mn Meena Plaza project developed by Meena Holdings

Abu Dhabi-based Al Noor Hospitals Group reached an agreement to acquire Rochester Wellness

Gulf Petrochem will invest ~$80mn in the next one year as part of its expansion plans in Fujairah & East Africa

Aramco Overseas Company plans to establish a JV valued at $3bn with Germany’s Lanxess for synthetic rubber

Gulf Union Cooperative Insurance received SAMA approval to raise capital worth SAR220mn through rights issue

Reuters reported on Sep 22 that Arab National Bank is close to complete a SAR2bn capital-boosting Sukuk issue

Saudi-based food company Mazola is upgrading factory, including a multi-million investment in new bottling line

Abdullah Al-Khodari Sons Co. signed a contract with the Saudi Ministry of Transport worth SAR92.4mn

Al Hassan Eng. Co. Abu Dhabi received letter of awards for two infrastructure projects in Oman totaling $19.25mn

Kuwait’s Investment Dar is seeking court approval to help close a KWD813mn ($2.7bn) debt restructuring

Qatar’s Saudia Group opened AED80mn hypermarket in Ajman. Plans to invest another AED45mn to double its size

QNB Group said on Sep 22 it stopped preliminary talks to acquire Kuwait Finance House’s Malaysian Unit

Qatargas’ $1bn Jetty Boil-Off Gas Recovery facility, world’s largest gas recovery project gets operational in Qatar

Qatar fuel has put on hold its proposed plan to establish a transparent cooking gas cylinder manufacturing facility

Gulf Hotels signed MoU in relation to acquiring 100% of Bahrain Tourism’s shares through a possible share-swap

Last Close 5 Day % YTD % P/E (2015) *Div. Yield

Dubai 3,632.66 0.21 -3.75 11.61 7.37

Abu Dhabi 4,514.28 0.79 -0.32 10.71 5.01

Saudi Tadawul 7,442.71 -0.37 -10.69 13.93 3.54

Qatar Index 11,433.75 0.13 -6.94 12.84 4.41

Kuwait Index 5,754.49 0.71 -11.95 - 4.50

Oman MSM 30 5,765.42 0.36 -9.11 9.98 4.52

Bahrain All Share

1,277.64 -0.47 -10.44 - 5.37

Egypt EGX 30 7,346.54 1.09 -17.70 11.11 1.85

Istanbul 100 Index

74,610.20 -0.65 -12.96 9.83 3.27

Source: Bloomberg, Mashreq Private Banking; *Current

DFMGI – 1 year performance Saudi Tadawul – 1 year performance

GCC EQUITIES

Source: Bloomberg, Mashreq Private Banking

Page I 5

The US dollar index gained 1.48% in the week after Federal Reserve Cheif Janet Yellen said she expected the central bank to hike rates in 2015, appeared to be supported by stronger 2Q2015 GDP growth

Canadian dollar weakened 0.84% against US dollar in the past five days on concerns that a weakening global economic growth will derail the country’s plan for an export-led recovery

Chinese President Xi Jinping pledged to avoid further lowering the value of the yuan against the US dollar after abruptly devaluing the currency in Aug as yuan lost 0.16% against US dollar from Sep 18

Brazil’s real slipped 0.76% against US dollar this week on speculation the government will struggle to pull Brazil out of its longest recession since the 1930s and narrow the budget deficit to avoid further cuts to its credit rating

Russian ruble appreciated 1.63% against US dollar in the week ended Sep 25 as crude oil prices appeared more upwardly mobile and companies convert export earning to pay taxes

Australian dollar lost 2.34% this week against US dollar on a speech by US Fed chief about raising US interest rates in 2015 coupled with the worries related to China slowdown

Indian rupee edged down 0.73% during the week against US dollar as the US started discussions on an interest rate hike and global recessionary fears prompt risk aversion by investors

Last Close 5 Day % 1 Mth. % YTD % 1 Year %

USD Index 96.2690 1.48 1.84 6.65 13.00

EUR/USD 1.1195 -0.91 -2.80 -7.46 -12.20

GBP/USD 1.5180 -2.29 -3.23 -2.55 -6.97

USD/JPY 120.5900 0.51 1.48 0.68 10.89

USD/CHF 0.9795 1.08 4.29 -1.49 3.48

USD/CAD 1.3337 0.84 0.01 14.77 20.05

USD/BRL 3.9755 0.76 9.91 49.59 63.75

USD/RUB 65.4095 -1.63 -5.24 7.69 69.97

USD/INR 66.1563 0.73 0.09 4.94 7.84

USD/CNY 6.3745 0.16 -0.60 2.72 3.88

USD/AUD 1.4231 2.34 1.45 16.28 25.05

EUR/USD – 1 year performance GBP/USD – 1 year performance

Source: Bloomberg, Mashreq Private Banking

CURRENCIES

Source: Bloomberg, Mashreq Private Banking

Page I 6

Brent and US crude futures gained more than 2% in the week as upbeat comments on the US economy from Federal Reserve Chairwoman Janet Yellen helped provide a boost to the outlook for crude demand

Spot gold prices edged up 0.65% in the week, helped by the momentum in the wake of the surprisingly dovish rates call by the Federal Reserve last week even as Fed chief discussed raising rates later in 2015

Spot palladium prices jumped 9.5% this week, supported by the emissions scandal raging around Volkswagen AG. The German car maker apologized for inserting software into 11mn of its diesel-engine cars to cheat strict US auto-pollution regulations and its CEO, Martin Winterkorn, stepped down

LME copper futures lost 4.4% during the week as RBC Capital markets said data from the International Copper Study Group showed Chinese demand fell 1% in 1H2015 and imports fell 10%

Malaysian palm oil futures climbed ~10% as the Malaysian ringgit slumped and as concerns built up that El Nino weather and a haze that has engulfed parts of Southeast Asia will curb output

ICE sugar futures strengthened 7.1% from Sep 18 after Brazil's Unica cane group data showed cane crushing and sugar output dropped steeply in the first half of September as rains hampered harvesting

ICE orange juice futures slumped 10.1% in the past five days with positive growing conditions in Florida boosting orange crop prospects. Florida is the source of most oranges used for juice in the US

Last Close 5 Day % 1 Mth. % YTD % 1 Year %

Brent – ICE 48.60 2.38 12.47 -15.23 -49.90

WTI – Nymex 45.70 2.28 16.26 -14.21 -50.61

Gold Spot 1,146.40 0.65 0.53 -3.25 -6.15

Silver Spot 15.11 -0.45 2.92 -3.76 -13.80

Copper - CMX 229.15 -4.40 -0.95 -18.90 -25.11

S&P GSCI Spot Index

362.01 1.24 6.55 -13.42 -37.69

Baltic Dry Index 943.00 -1.77 0.11 20.59 -9.15

WTI Crude – 1 year performance GOLD – 1 year performance

Source: Bloomberg, Mashreq Private Banking

COMMODITIES

Source: Bloomberg, Mashreq Private Banking

Page I 7

US 10-year bond yield ticked up 2.9 bps in the week to 2.16% after the head of the US central bank signaled that an interest-rate increase remains on track in 2015, which strengthened global stocks while government bonds slipped

UK 10-year gilt yield rose marginally by 1 bps this week to 1.84% after Fed Chief Janet Yellen said the US central bank was on course to raise interest rates this year, boosting speculation that the Bank of England will follow

China’s seven-day repurchase rate declined one basis point in the past 5 days to 2.38% after the central bank added funds to the financial system. The People’s Bank of China injected a net yuan 40bn via open-market operations this week, after withdrawing yuan 140bn last week

South Africa’s central bank kept its benchmark interest rate unchanged at 6% on Sep 23 as lower oil prices gave it room to support an economy weighed down by power cuts and falling metal prices

Norway’s central bank unexpectedly lowered the overnight deposit rate by 25 bps to 0.75% on Sep 24 and said it may ease policy further as it seeks to rescue an expansion in western Europe’s biggest petroleum producer from a plunge in oil prices

Taiwan's central bank reduced its policy rate to 1.750% from 1.875% on Sep 24, the first cut since 2009 as the strength of its currency and China’s slowdown dragged exports into a seven-month slump

The Philippines central bank left its benchmark interest rate unchanged at 4% on Sep 24 for an eighth straight meeting, as the prospect of faster economic growth in 2016 reduces the need for monetary stimulus

Last Close 5 Day % 1 Mth. % YTD % 1 Year %

USD-10yr 2.16 1.35 4.39 -0.41 -13.58

USD-2yr 0.69 2.08 15.20 4.11 25.53

Fed Funds Rate 0.14 0.00 -6.67 133.33 55.56

USD-3m Libor 0.33 2.26 -0.18 27.70 39.73

USD-6m Libor 0.53 0.64 1.33 46.02 59.85

German-10yr 0.65 -2.11 -11.10 19.96 -33.30

UK-10yr 1.84 0.55 -3.46 4.78 -24.74

Japan-10yr 0.32 3.24 -16.05 -0.93 -38.65

AED-3m EIBOR 0.82 -0.17 2.67 21.73 15.86

AED-6m EIBOR 0.95 0.00 2.15 12.69 6.56

US 10 year Generic Yield – 1 year performance UK 10 year Generic Yield – 1 year performance

Source: Bloomberg, Mashreq Private Banking

INTEREST RATES

Source: Bloomberg, Mashreq Private Banking

Page I 8

Ref Country Weekly Change Weekly Change

(USD Adj.)

1 Venezuela -8.61% -8.61%

2 Argentina -7.16% -7.42%

3 Ukraine -6.98% -5.93%

4 Kazakhstan -5.88% -2.75%

5 Brazil -5.15% -5.87%

6 Lithuania -4.95% -5.81%

7 Israel -4.44% -5.12%

8 Namibia -4.15% -8.19%

9 Luxembourg -4.05% -4.92%

10 Indonesia -3.90% -5.99%

Ref Country Weekly Change Weekly Change

(USD Adj.)

1 Slovenia 2.43% 1.50%

2 Latvia 2.08% 1.15%

3 Serbia 1.97% 1.15%

4 Morocco 1.72% 1.08%

5 Egypt 1.09% 1.05%

6 Romania 1.08% 0.38%

7 Slovakia 1.04% 0.12%

8 Abu Dhabi-UAE 0.79% 0.79%

9 Kenya 0.77% 0.43%

10 Vietnam 0.73% 0.66%

WEEKLY

Ref Country YTD Change YTD Change (USD Adj.)

1 Venezuela 214.13% 214.13%

2 Latvia 40.85% 30.33%

3 Malta 30.41% 20.68%

4 Denmark 26.47% 16.81%

5 Jamaica 26.40% 21.94%

6 Hungary 25.23% 16.47%

7 Slovakia 21.15% 12.10%

8 Ireland 20.67% 11.66%

9 Estonia 15.34% 6.73%

10 Argentina 14.22% 2.80%

YTD

Ref Country YTD Change YTD Change (USD Adj.)

1 Peru -32.48% -37.59%

2 Colombia -19.68% -37.90%

3 Indonesia -19.47% -32.10%

4 Greece -18.28% -24.38%

5 Egypt -17.70% -24.81%

6 Singapore -15.82% -21.72%

7 Bulgaria -15.21% -21.53%

8 Slovenia -14.59% -20.96%

9 Ukraine -14.47% -37.23%

10 Laos -13.08% -13.70%

EQUITY MARKETS - TOP MOST & BOTTOM MOST

Source: Bloomberg, Mashreq Private Banking

Page I 9

Ref Commodity Weekly Change

1 Orange Juice -10.11%

2 Lumber -6.56%

3 Copper -4.40%

4 Feeder Cattle -4.25%

5 Platinum -3.59%

6 Aluminium -3.51%

7 Zinc -3.32%

8 Live Cattle -1.69%

9 Natural Gas -1.57%

10 Steel Rebar -1.53%

Ref Commodity Weekly Change

1 Palm Oil 9.98%

2 Palladium 9.46%

3 Coffee 8.25%

4 Sugar 7.12%

5 Soybean Oil 6.41%

6 Wheat 4.31%

7 Corn 3.11%

8 Nickel 2.84%

9 Soybeans 2.54%

10 Rough Rice 2.47%

WEEKLY

Ref Commodity YTD Pct Change

1 Rough Rice 15.49%

2 Cocoa 12.58%

3

4

5

6

7

8

9

10

YTD

Ref Commodity YTD Pct Change

1 Lumber -34.58%

2 Nickel -34.32%

3 Coffee -26.35%

4 Steel Rebar -25.82%

5 Zinc -25.07%

6 Orange Juice -22.85%

7 Tin -22.16%

8 Platinum -21.64%

9 Live Cattle -19.31%

10 Sugar -19.15%

COMMODITY MARKETS - TOP MOST & BOTTOM MOST

Source: Bloomberg, Mashreq Private Banking

Page I 10

IMPORTANT NOTICE

This report was prepared by the Private Banking Unit of Mashreqbank psc (“Mashreq”) in the United Arab Emirates (“U.A.E.”). Mashreq is regulated by the Central Bank of the U.A.E. This report is provided for informational purposes and private circulation only and should not be construed as an offer to sell or a solicitation to buy any security or any other financial instrument or adopt any hedging, trading or investment strategy. Prior to investing in any product, we recommend that you consult with a professional financial advisor, taking into consideration investment objectives, financial circumstances and tax implication. While based on information believed to be reliable, we do not guarantee and make no express or implied representation as to the accuracy of this report or complete description of the securities markets or developments referred to in this report. The information, opinions, forecasts (if any), assumptions or estimates contained in this report are as of the date indicated and are subject to change at any time without prior notice. The stated price of any securities mentioned in this report is as of the date indicated and is not a representation that any transaction can be effected at this price. The risks related to investment products described in this report are not all encompassing and investors should refer to the relevant investment offer document for detailed information and applicable terms and conditions. Investment products, including treasury products, are not guaranteed by Mashreq or any of its affiliates or subsidiaries unless stated otherwise and are subject to investment risk, including loss of principal. Investment products are not government insured. Past performance is not an indicator of future performance. US persons (US Citizens; US Green Card Holders; Resident Aliens subject to US income taxes for IRS purposes) are not eligible for any of the investment products introduced by Mashreq unless stated otherwise. This report is for distribution only under such circumstances as may be permitted by applicable law. Neither Mashreq nor its officers, directors or shareholders or other persons shall be liable for any direct, indirect, incidental or other damages including loss of profits arising in any way from the information contained in this report. This report is intended solely for the use by the intended recipients and the contents shall not be reproduced, redistributed or copied in whole or in part for any purpose without Mashreq’s prior express consent.