65

The better the question. The better the answer. The better the world works. Welcome DACT Workshop IFRS 9, IFRS 13 and regulatory developments Amsterdam, March 9 th , 2016

The better the question. The better the answer.�The better the world works.

Welcome DACT Workshop

IFRS 9, IFRS 13 and regulatory developments

Amsterdam, March 9th, 2016

Page 2

Agenda today

15:40 – 16:55 IFRS 9 by Sander de Ruiter

16:55 – 17:25 IFRS 13 by Floris van de Loo

17:25 – 17:45 Other regulation by Ruud Bulkmans

15:30 – 15:40 Kick-off by André ten Damme

Page 3

The challenges for 2016 and ahead..

Page 4

EY Treasury Services locations

USA

Brazil

Argentina

Germany

Switzerland

Dubai

Turkey

The Netherlands Denmark

Belgium

UK

France

Spain

Italy

Portugal

South Africa

Austria

Nordics (Sweden)

Russia

Poland

India

Hong Kong

Singapore

South Korea

Japan

Shanghai

Australia

• Our global Centre of

Excellence Corporate Treasury offers you a focused expert knowledge

• More than 300 specialized consultants assist our customer in Treasury projects worldwide

• It is our aim to provide you with tailor-made and high-performance solutions.

Countries with EY presence

Countries without EY presence

Page 5

EY Global Treasury Services

What makes EY different? ► Cross-functional and integrated team including tax,

accounting and regulatory, IT, corporate finance, and finance transformation

► Dedicated team includes former practitioners in the treasury and finance areas of major global corporations

► Strong credentials and success stories demonstrate our ability to successfully effect change

Page 6

Increasing scope of a corporate Treasury

Common

Selective

Corporate finance ► Capital Structure ► WACC ► M&A and Post Deal Integration

Insurance ► Credit insurance ► Insurance of goods shipments ► General insurance

EWRM ► Quantitative/Qualitative ► Risk Management Framework ► Reporting

Accounting ► For own activities ► Signing the accounts

Credit risk ► Counterparty limits ► Country limits ► Commercial credit ► Credit insurance ► Trade finance/ LCs

Working capital management ► Evaluation of projects ► Monitoring KPIs

Commodity risk ► Purchase/Sale contracts ► Commodity futures and options

Pension fund management ► Risk Management ► ALM ► Selection process

Bank relationship management

Treasury technology

Debt management and financing activities

Interest rate risk management

Foreign exchange risk management

Cash & liquidity management

Tax ► Tax considerations ► Tax planning ► Base erosion and profit shifting

The better the question. The better the answer.�The better the world works.

Dutch Association of Corporate Treasurers Supporting accounting change: IFRS 9

Page 8

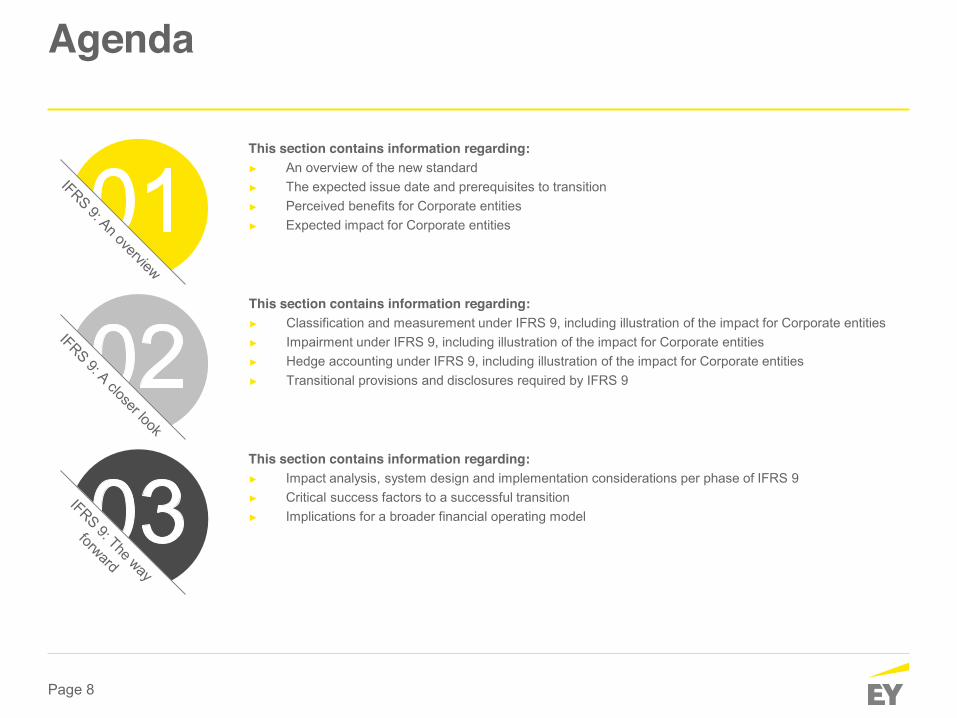

Agenda

This section contains information regarding: ► An overview of the new standard ► The expected issue date and prerequisites to transition ► Perceived benefits for Corporate entities ► Expected impact for Corporate entities

This section contains information regarding: ► Classification and measurement under IFRS 9, including illustration of the impact for Corporate entities ► Impairment under IFRS 9, including illustration of the impact for Corporate entities ► Hedge accounting under IFRS 9, including illustration of the impact for Corporate entities ► Transitional provisions and disclosures required by IFRS 9

This section contains information regarding: ► Impact analysis, system design and implementation considerations per phase of IFRS 9 ► Critical success factors to a successful transition ► Implications for a broader financial operating model

Page 9

IFRS 9: An overview

Page 10

IFRS 9 An overview

IFRS 9 is the new financial instruments standard, and will replace IAS 39. Endorsement by the EU is expected by H2 2016, after which adoption is permitted. While the standard is not effective until 1 January 2018, implementation is expected to require a significant investment of time and resources, resulting in many entities already commencing diagnostic and pre-implementation activities. In addition, while IFRS 9 may not be applied until endorsed by the EU, the transition provisions require all preparation be completed prior to adoption. As such, entities who foresee benefits in application of the new standard may wish to perform analysis now, ahead of an anticipated early adoption from January 2017 onwards.

While implementation of IFRS 9 brings with it a number of challenges, it is also being more frequently acknowledged as providing many benefits, including:

IFRS contains three modules: classification

and measurement, impairment and hedge

accounting

While the impact upon on each organization will differ (depending upon their risk management strategy of portfolio of financial instruments), the following demonstrates the bearing upon a ‘typical’ Dutch Corporate Treasury:

Enhanced data

analytics Alignment with other

regulations

Greater operational oversight

Benefits

Greater alignment between

finance and risk

Improved hedge

accounting framework

Expected relative impact (for corporate entity)

Classification &Measurement

Impairment Hedge Accounting

Implementation

System design

Impact assessment

Page 11

IFRS 9: A closer look

Page 12

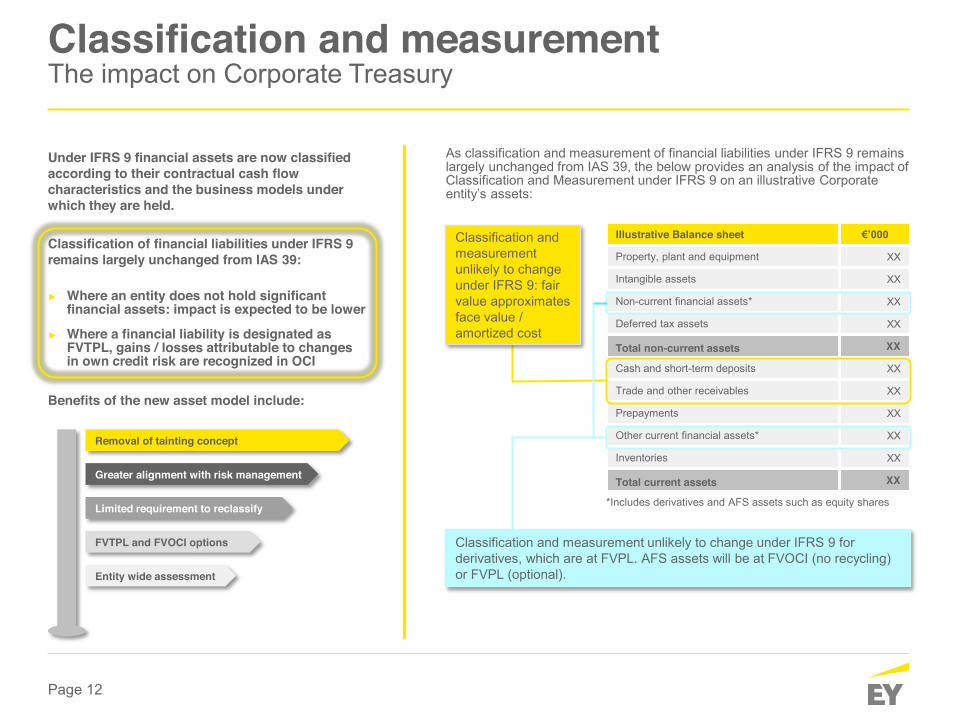

Classification and measurement The impact on Corporate Treasury

Under IFRS 9 financial assets are now classified according to their contractual cash flow characteristics and the business models under which they are held. Classification of financial liabilities under IFRS 9 remains largely unchanged from IAS 39: ► Where an entity does not hold significant

financial assets: impact is expected to be lower

► Where a financial liability is designated as FVTPL, gains / losses attributable to changes in own credit risk are recognized in OCI

Removal of tainting concept

Greater alignment with risk management

Limited requirement to reclassify

FVTPL and FVOCI options

Entity wide assessment

Benefits of the new asset model include:

Illustrative Balance sheet €’000

Property, plant and equipment XX

Intangible assets XX

Non-current financial assets* XX

Deferred tax assets XX

Total non-current assets XX

Cash and short-term deposits XX

Trade and other receivables XX

Prepayments XX

Other current financial assets* XX

Inventories XX

Total current assets XX

*Includes derivatives and AFS assets such as equity shares

Classification and measurement unlikely to change under IFRS 9: fair value approximates face value / amortized cost

Classification and measurement unlikely to change under IFRS 9 for derivatives, which are at FVPL. AFS assets will be at FVOCI (no recycling) or FVPL (optional).

As classification and measurement of financial liabilities under IFRS 9 remains largely unchanged from IAS 39, the below provides an analysis of the impact of Classification and Measurement under IFRS 9 on an illustrative Corporate entity’s assets:

Page 13

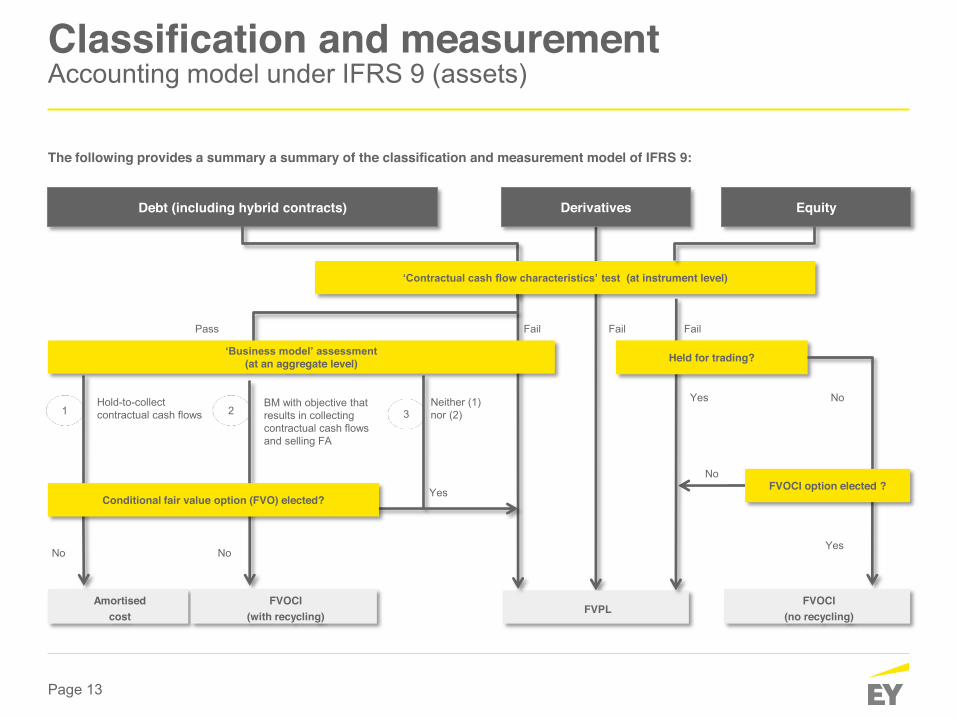

Classification and measurement Accounting model under IFRS 9 (assets)

The following provides a summary a summary of the classification and measurement model of IFRS 9:

Debt (including hybrid contracts)

Pass

No

Neither (1) nor (2)

BM with objective that results in collecting contractual cash flows and selling FA

1 3 2

No

Yes

Derivatives Equity

No

Yes

Amortised cost FVPL

FVOCI (with recycling)

FVOCI (no recycling)

‘Contractual cash flow characteristics’ test (at instrument level)

Fail

Hold-to-collect contractual cash flows

Conditional fair value option (FVO) elected?

Fail Fail

Held for trading?

Yes No

FVOCI option elected ?

‘Business model’ assessment (at an aggregate level)

Page 14

Impairment The impact on Corporate Treasury

Under IFRS 9, financial assets are subject to a revised impairment model; focusing on expected rather than incurred losses. The impact on Corporate entities is expected to be reduced where: ► The fair value of the portfolio of financial

assets held approximates their book value

► Financial assets are already carried at fair value (either through P&L or OCI)

Benefits of the new impairment model include:

Illustrative Balance sheet €’000

Property, plant and equipment XX

Intangible assets XX

Non-current financial assets* XX

Deferred tax assets XX

Total non-current assets XX

Cash and short-term deposits XX

Trade and other receivables XX

Prepayments XX

Other current financial assets* XX

Inventories XX

Total current assets XX

*Includes derivatives and AFS assets such as equity shares

Impairment unlikely to change under IFRS 9: fair value approximates book value / amortized cost (presuming receivables are short term)

Impairment unlikely to change under IFRS 9: derivatives are currently carried at FVPL, and AFS assets will be at FVOCI (no recycling) or FVPL (optional).

As impairment under IFRS 9 does not impact financial liabilities, the below provides an analysis of the impact of impairment under IFRS 9 on an illustrative Corporate entity’s assets:

More insights in credit risk of portfolios

Greater Operational Oversight

More alignment Finance and Risk

Alignment regulations

Enhanced data analytics

Page 15

Impairment Accounting model under IFRS 9 (assets)

The following provides a summary a summary of the impairment model of IFRS 9:

Page 16

Hedge accounting The impact on Corporate Treasury

The objective of the IFRS 9 hedge accounting framework is to simplify application, align accounting outcomes to economic realities, and provide useful information regarding risk management activities. Development of the revised framework involved ongoing industry consultation to address as many concerns of information preparers and users as possible. This yielded a more practical standard, which streamlines implementation for those already applying hedge accounting, and incentivizes those not to reconsider.

Benefits of the new hedge accounting model include:

Illustrative Balance sheet €’000

Property, plant and equipment XX

Derivative assets XX

Cash and short-term deposits XX

Total assets XX

Trade payables XX

Deferred revenue XX

External borrowings XX

Derivative liabilities XX

Total liabilities XX

Hedge reserve XX

Total equity XX

As hedge accounting under IFRS 9 impacts both financial assets and liabilities, the below provides an analysis of the impact of impairment under IFRS 9 on an illustrative corporate entity’s (selected) assets and liabilities:

Due to differences in effectiveness testing and accounting models, as well as the items qualifying for hedge accounting, IFRS 9 has the potential to cause significant changes to an entity’s balance sheet

IFRS 9 also has the potential to effect the timing of revenue recognition and presentation within an entity´s Profit or Loss

Less P&L volatility

Additional qualifying exposures

Simplified testing model

Less breakage of hedges

Less clerical burden

Unrecognized future cash flows arising from FX and commodity exposures will also be impacted

Page 17

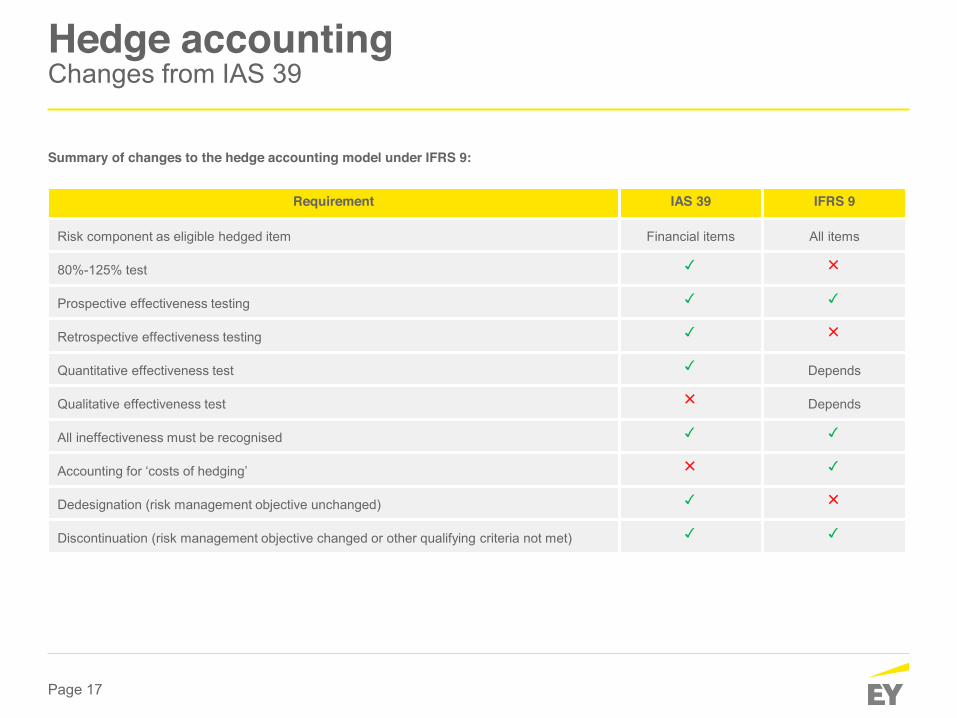

Hedge accounting Changes from IAS 39

Summary of changes to the hedge accounting model under IFRS 9:

Requirement IAS 39 IFRS 9

Risk component as eligible hedged item Financial items All items

80%-125% test 3 5

Prospective effectiveness testing 3 3

Retrospective effectiveness testing 3 5

Quantitative effectiveness test 3 Depends

Qualitative effectiveness test 5 Depends

All ineffectiveness must be recognised 3 3

Accounting for ‘costs of hedging’ 5 3

Dedesignation (risk management objective unchanged) 3 5

Discontinuation (risk management objective changed or other qualifying criteria not met) 3 3

Page 18

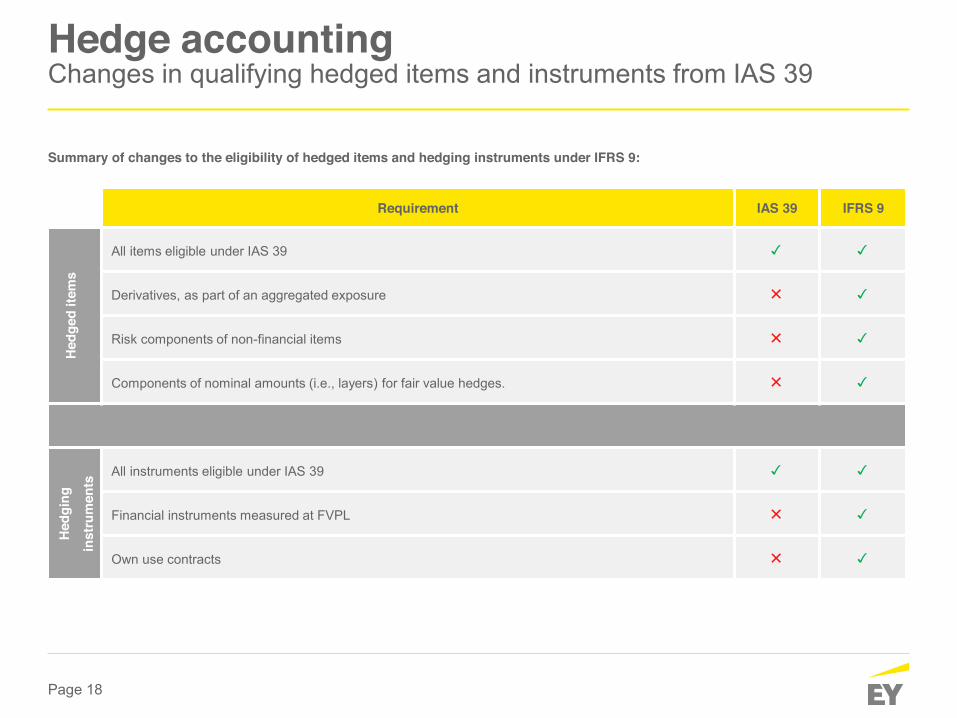

Hedge accounting Changes in qualifying hedged items and instruments from IAS 39

Summary of changes to the eligibility of hedged items and hedging instruments under IFRS 9:

Requirement IAS 39 IFRS 9

Hed

ged

item

s

All items eligible under IAS 39 3 3

Derivatives, as part of an aggregated exposure 5 3

Risk components of non-financial items 5 3

Components of nominal amounts (i.e., layers) for fair value hedges. 5 3

Hed

ging

inst

rum

ents

All instruments eligible under IAS 39 3 3

Financial instruments measured at FVPL 5 3

Own use contracts 5 3

Page 19

Hedge accounting Risk management objectives

Item Risk strategy Risk objective

Description ► Established at a high level ► Identifies risks and how

entity responds to them ► Typically in place for

longer period ► May include flexibility ► Often a formal policy

document ► Part of hedge

documentation

► Applies at level of particular hedging relationship

► Describes how a particular hedging instrument is used to hedge a particular exposure designated as the hedged item

► Part of hedge documentation

Examples ► Maintain 40% of liabilities at floating interest rate

► Assure long-term price stability of commodity purchases

► Hedge foreign currency risk of all forecast purchases in USD up to 12 months

► Designate an interest rate swap as a fair value hedge of a GBP 100m fixed rate liability

► Designate a coal forward contract to hedge the first 100 tones of coal purchases in March 2016

► Designate a foreign exchange forward contract to hedge the foreign exchange risk of the first USD100 purchases in March 2016

Risk management activity

Accounting for risk management

activity

Risk management strategy

Risk management objective

What is the significant of risk management strategies and objectives? ► Link between risk management activity and

accounting ► Affects discontinuation of hedge accounting

Page 20

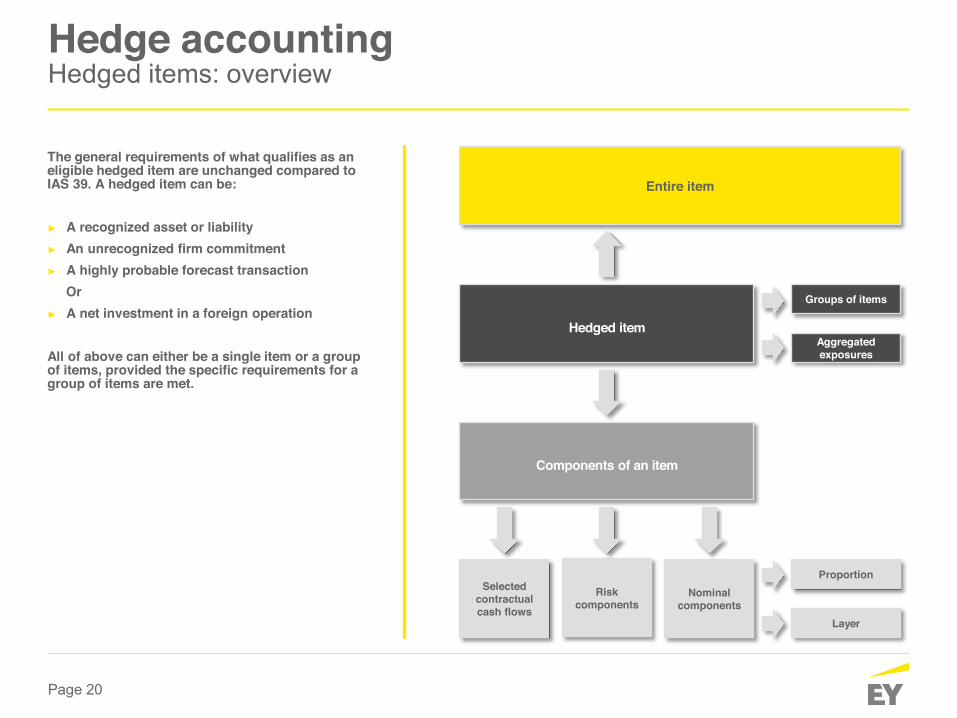

Hedge accounting Hedged items: overview

The general requirements of what qualifies as an eligible hedged item are unchanged compared to IAS 39. A hedged item can be: ► A recognized asset or liability ► An unrecognized firm commitment ► A highly probable forecast transaction

Or ► A net investment in a foreign operation

All of above can either be a single item or a group of items, provided the specific requirements for a group of items are met.

Entire item

Hedged item

Groups of items

Aggregated exposures

Components of an item

Selected contractual cash flows

Risk components

Nominal components

Proportion

Layer

Page 21

Hedge accounting Hedged items: risk components

IAS 39 did not allow the designation of risk components for non-financial items. IFRS 9 creates parity between financial and non-financial hedged items and consequently also allowed risk components of non-financial items to be designated as hedged items, provided that the risk component can be separately identified and reliably measured.

Criteria for designation

Separately identifiable

Reliably measurable

Contractually specified

Other components

Rebuttable presumption: inflation risk

Mar

ket s

truc

ture

Illustrative Example ► Purchasing coffee from a specific area in Columbia ► Hedge expected coffee purchases for the next 12months, by entering into a

futures contract with Arabica coffee as underlying instrument. ► Coffee is purchased in Columbia via physical supply contracts that are

entered into up to 6 months in advance. ► Supply contracts are variable rate, however the benchmark is Arabic Coffee

and the price differential from to the local market is fixed

The entity enters into coffee futures to lock in the coffee benchmark price for the next year. Six months later, when entering into the supply contracts, the price differential between the coffee benchmark and local price is also fixed. The Arabica benchmark price is a non-contractually specified risk component, designated as the hedged risk in the item.

Non-contractually specified risk component

1-year Coffee futures contract on Arabica coffee

Physical contract: benchmark + differential

6 months 12 months t0

Page 22

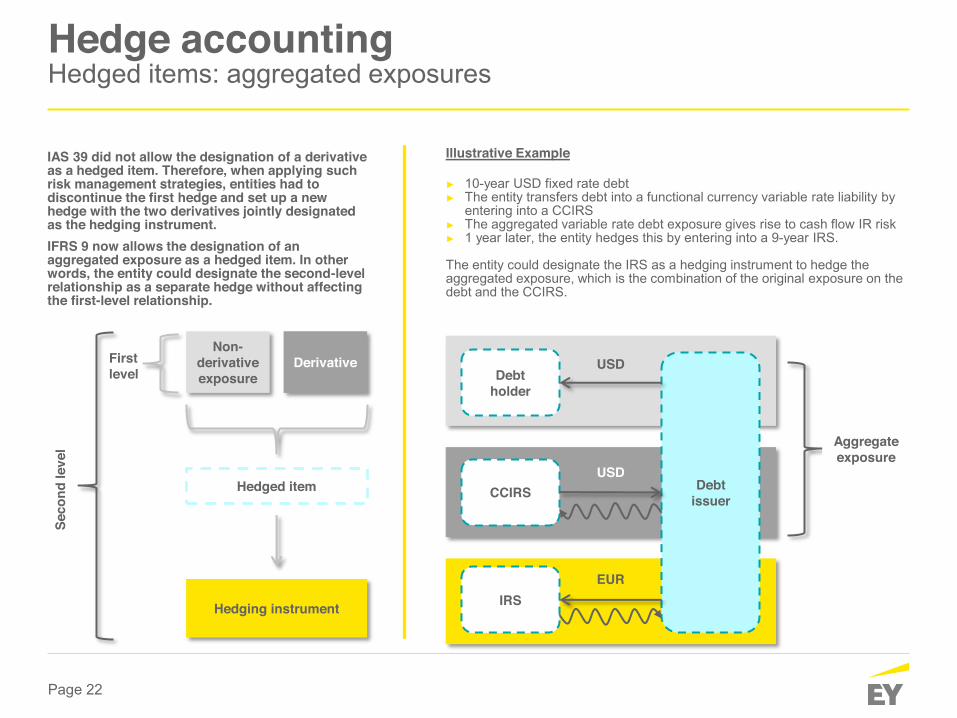

Hedge accounting Hedged items: aggregated exposures

IAS 39 did not allow the designation of a derivative as a hedged item. Therefore, when applying such risk management strategies, entities had to discontinue the first hedge and set up a new hedge with the two derivatives jointly designated as the hedging instrument. IFRS 9 now allows the designation of an aggregated exposure as a hedged item. In other words, the entity could designate the second-level relationship as a separate hedge without affecting the first-level relationship.

First level

Non-derivative exposure

Derivative

Hedging instrument

Hedged item

Seco

nd le

vel

Illustrative Example ► 10-year USD fixed rate debt ► The entity transfers debt into a functional currency variable rate liability by

entering into a CCIRS ► The aggregated variable rate debt exposure gives rise to cash flow IR risk ► 1 year later, the entity hedges this by entering into a 9-year IRS. The entity could designate the IRS as a hedging instrument to hedge the aggregated exposure, which is the combination of the original exposure on the debt and the CCIRS.

Aggregate exposure

Debt issuer

Debt holder

CCIRS

IRS

USD

USD

EUR

Page 23

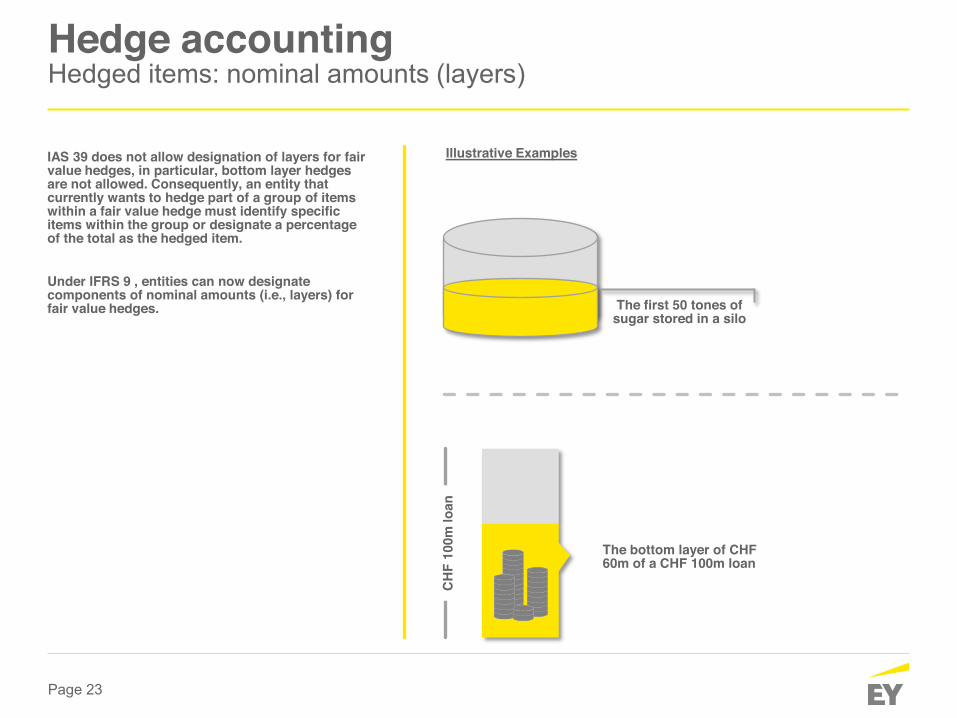

Hedge accounting Hedged items: nominal amounts (layers)

IAS 39 does not allow designation of layers for fair value hedges, in particular, bottom layer hedges are not allowed. Consequently, an entity that currently wants to hedge part of a group of items within a fair value hedge must identify specific items within the group or designate a percentage of the total as the hedged item. Under IFRS 9 , entities can now designate components of nominal amounts (i.e., layers) for fair value hedges.

Illustrative Examples

The first 50 tones of sugar stored in a silo

The bottom layer of CHF 60m of a CHF 100m loan

CH

F 10

0m lo

an

Page 24

Hedge accounting Hedged instruments

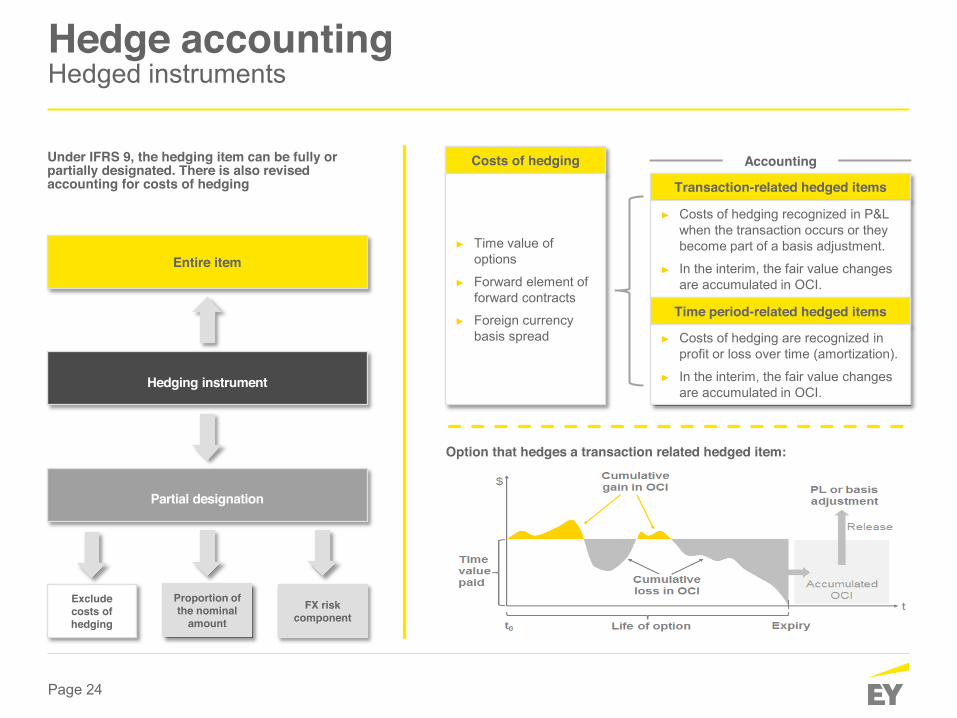

Under IFRS 9, the hedging item can be fully or partially designated. There is also revised accounting for costs of hedging

Entire item

Hedging instrument

Partial designation

Exclude costs of hedging

Proportion of the nominal

amount FX risk

component

Costs of hedging

► Time value of options

► Forward element of forward contracts

► Foreign currency basis spread

Transaction-related hedged items

► Costs of hedging recognized in P&L when the transaction occurs or they become part of a basis adjustment.

► In the interim, the fair value changes are accumulated in OCI.

Time period-related hedged items

► Costs of hedging are recognized in profit or loss over time (amortization).

► In the interim, the fair value changes are accumulated in OCI.

Accounting

Option that hedges a transaction related hedged item:

Page 25

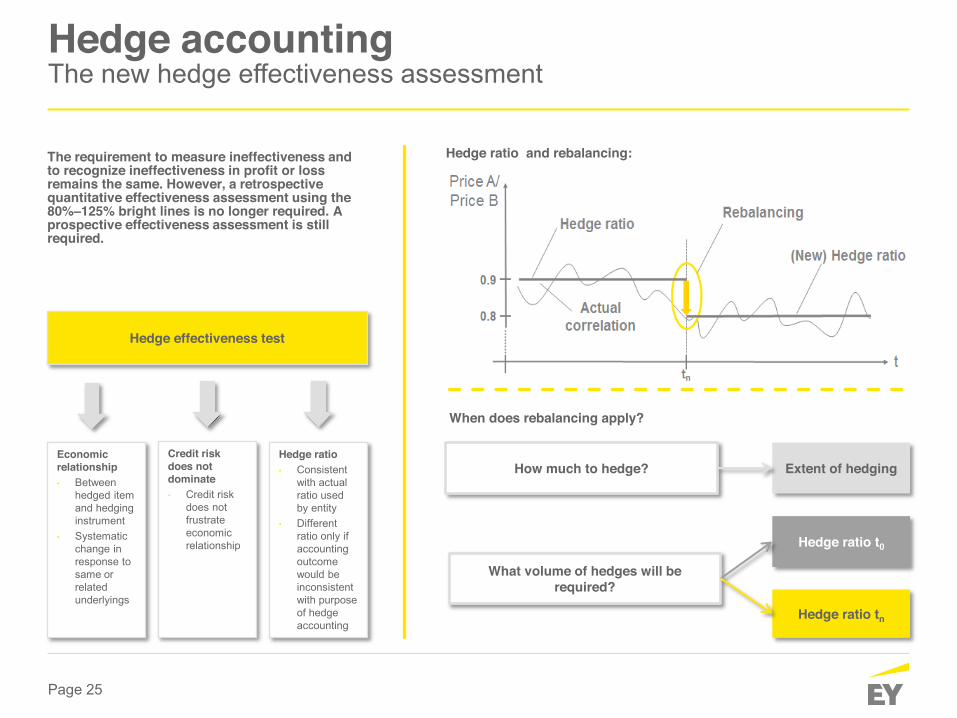

Hedge accounting The new hedge effectiveness assessment The requirement to measure ineffectiveness and to recognize ineffectiveness in profit or loss remains the same. However, a retrospective quantitative effectiveness assessment using the 80%–125% bright lines is no longer required. A prospective effectiveness assessment is still required.

Hedge effectiveness test

Economic relationship • Between

hedged item and hedging instrument

• Systematic change in response to same or related underlyings

Credit risk does not dominate • Credit risk

does not frustrate economic relationship

Hedge ratio • Consistent

with actual ratio used by entity

• Different ratio only if accounting outcome would be inconsistent with purpose of hedge accounting

Extent of hedging

Hedge ratio t0

Hedge ratio tn

Hedge ratio and rebalancing:

When does rebalancing apply?

How much to hedge?

What volume of hedges will be required?

Page 26

On transition to IFRS 9, entities can apply the fair value option on an all-or-nothing basis for

(already existing) own use contracts.

Fail

Hedge accounting Fair value option for ‘own use’ contracts IFRS 9 Financial Instruments extends the fair value option to ‘own use’ contracts. When applying the fair value option an entity may make an irrevocable designation to measure an own use contract at FVTPL, where it eliminates or significantly reduces an accounting mismatch.

Illustrative Example ► An entity is in the business of procuring, transporting, storing, processing

and merchandising soybeans and sunflower seeds. ► The inputs and the outputs are agricultural commodities which are traded in

liquid markets. ► The entity has both a broker business and a processing business, which are

operationally distinct. ► The entity analyses and monitors its net commodity risk position,

comprising inventories, physically settled forward purchase and sales contracts and exchange traded futures and options. The target is to keep the net fair value risk position close to nil.

Under IAS 39, the physically settled forward contracts from the processing business have to be accounted for as own use contracts, whereas all other contracts are accounted for at fair value through profit or loss. The resulting accounting mismatch does not reflect how the entity is managing the overall fair value risk of those contracts.

Non-financial item

Financial instrument

Right of cash settlement

Practice of cash settlement

Pass

Pass

Business purpose of contract Pass

Own use contract

Fail

Fail

Own use contracts

Page 27

Hedge accounting Discontinuation Under IFRS 9 an entity would have to discontinue hedge accounting if the qualification criteria are no longer met. This includes if the risk management objective for the hedging relationship has changed. IFRS 9 now introduces partial discontinuation of hedge accounting, which means that hedge accounting continues for the remaining part of the hedging relationship.

Scenario Discontinuation • The risk management objective has

changed • Full or partial

• No longer an economic relationship between the hedged item and the hedging instrument

• Full

• The effect of credit risk dominates the value changes of the hedging relationship

• Full

• When rebalancing, the volume of the hedged item or the hedging instrument is reduced

• Partial

• The hedging instrument expires • Full

• The hedging instrument is (in full or in part) sold, terminated or exercised

• Full or partial

• The hedged item (or part of it) no longer exists or is no longer expected to occur

• Full or partial

The option to voluntary revoke a hedge relationship under IAS 39 has been removed

Page 28

Hedge accounting Disclosures The disclosure requirements for entities applying hedge accounting are set out in IFRS 7. In order to maximize the effectiveness of its disclosures, an entity must consider the necessary level of detail, the balance between different disclosure requirements, the appropriate level of disaggregation and whether additional explanations are necessary. The IASB has made it clear that disclosures with respect to risk management activities should be specific to the entity rather than generic or ‘boiler plate’.

Disc

losu

re o

bjec

tives

Risk management strategy

Effects of hedging on future cash flows

Effects of hedging on financials

Activity specific matters

The following provides an extract of IFRS 9 transition disclosures with respect to hedge accounting in the context of a Corporate entity:

Consideration Disclosure • Hedge

relationships • Transactions previously de-designated from fair value hedge

relationships relating to a portion of our borrowing portfolio have been re-instated in fair value hedges from the application date. These transactions were and continue to be in effective economic relationships based on contractual amounts and cash flows over the life of the transaction, however previously they did not satisfy the requirements for hedge accounting.

• We have redefined our hedge relationships relating to the portion of our offshore borrowing portfolio in fair value hedges to exclude borrowing margins from the hedged risk. This has resulted in de-designating our existing fair value hedge relationships and re-designating from the application date without any change to the underlying economic objective of the hedging.

• Foreign currency basis spreads and forward

• We have elected to separate and exclude foreign currency basis spreads from instruments designated as hedging instruments.

• The cumulative change in fair value of the foreign currency basis spreads is recognized in a separate component of equity. Cross currency basis spreads are included in interest on borrowings in the income statement over the life of the borrowing.

• Upon transition to IFRS 9, the balance of foreign currency basis spread was a loss of xx. We have elected not to retrospectively apply the provisions in relation to the accounting treatment of foreign currency basis spread. Accordingly, this amount will be unwound partly to the P&L and partly to the cash flow hedging reserve over the remaining life of the associated borrowing.

Page 29

IFRS 9: The way forward

Page 30

Preparation timelines should maintain flexibility in order to

permit early adoption

Sophisticated Approach Simplified Approach Month

Impact assessment (C&M) April

Impact assessment (Impairment) May

System design (C&M and Impairment) Jun

Parallel run, including IFRS 9 disclosures Jan

Impact assessment (hedge accounting) Sept

System design (hedge accounting) Oct

Build test & deploy (hedge accounting) Nov

Go Live Jan

Implementation approach Scoping and timeline

2018 2017

2016

Scoping Determining the implementation timeline of IFRS 9 for a corporate is highly dependent upon the nature of financial instruments held by the entity: ► Significant portfolio of non core financial

assets such as bonds etc. (referred to as the ‘Sophisticated Approach´): comparative disclosures (1 Jan 2017) required in order to show changes in classification / measurement and impairment. This will increase lead time.

► Insignificant portfolio of non core financial assets (referred to as the ‘Simplified Approach´): only transitional disclosures required in order to demonstrate changes in hedge accounting (impact disclosures for FY17 expected to be insignificant).

Page 31

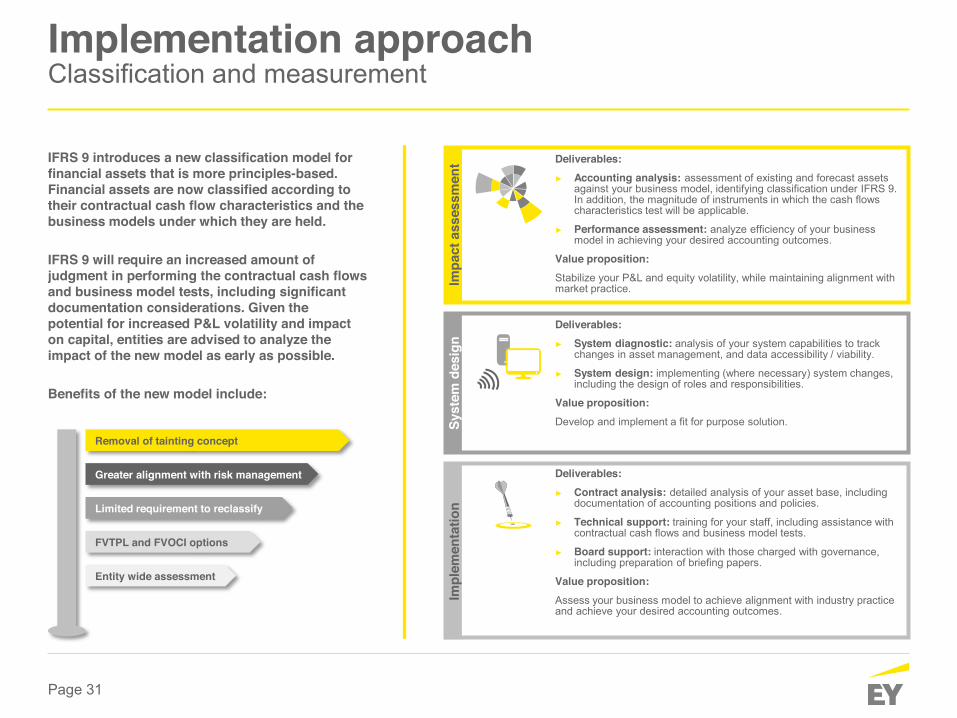

Implementation approach Classification and measurement

IFRS 9 introduces a new classification model for financial assets that is more principles-based. Financial assets are now classified according to their contractual cash flow characteristics and the business models under which they are held. IFRS 9 will require an increased amount of judgment in performing the contractual cash flows and business model tests, including significant documentation considerations. Given the potential for increased P&L volatility and impact on capital, entities are advised to analyze the impact of the new model as early as possible. Benefits of the new model include:

Deliverables: ► Accounting analysis: assessment of existing and forecast assets

against your business model, identifying classification under IFRS 9. In addition, the magnitude of instruments in which the cash flows characteristics test will be applicable.

► Performance assessment: analyze efficiency of your business model in achieving your desired accounting outcomes.

Value proposition: Stabilize your P&L and equity volatility, while maintaining alignment with market practice.

Deliverables: ► System diagnostic: analysis of your system capabilities to track

changes in asset management, and data accessibility / viability.

► System design: implementing (where necessary) system changes, including the design of roles and responsibilities.

Value proposition: Develop and implement a fit for purpose solution.

Deliverables: ► Contract analysis: detailed analysis of your asset base, including

documentation of accounting positions and policies.

► Technical support: training for your staff, including assistance with contractual cash flows and business model tests.

► Board support: interaction with those charged with governance, including preparation of briefing papers.

Value proposition: Assess your business model to achieve alignment with industry practice and achieve your desired accounting outcomes.

Removal of tainting concept

Greater alignment with risk management

Limited requirement to reclassify

FVTPL and FVOCI options

Entity wide assessment

Impa

ct a

sses

smen

t Sy

stem

des

ign

Impl

emen

tatio

n

Page 32

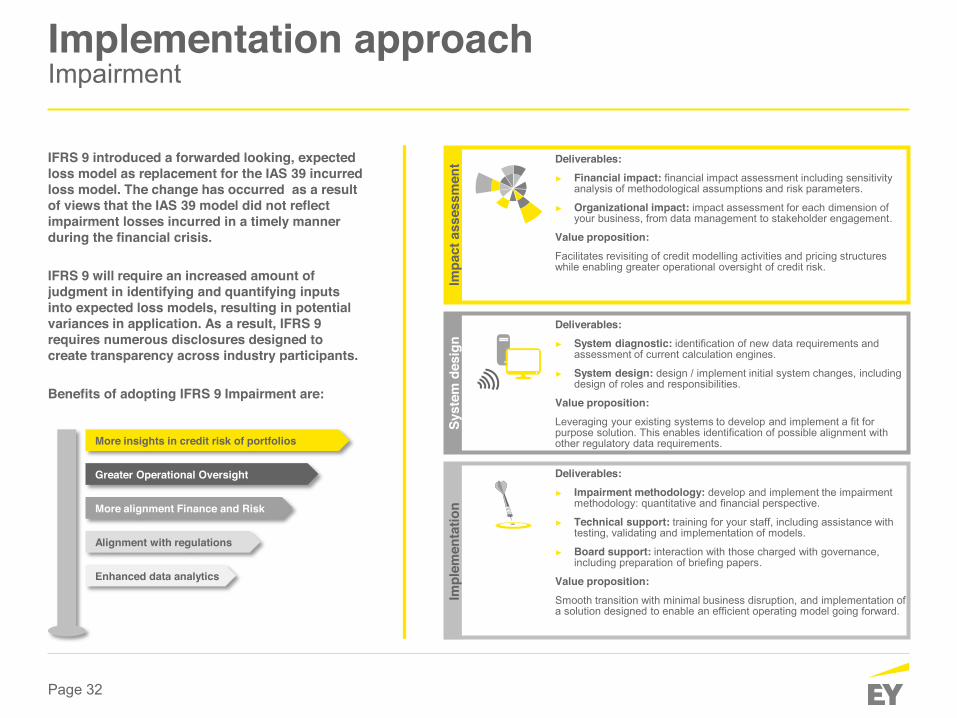

Implementation approach Impairment

IFRS 9 introduced a forwarded looking, expected loss model as replacement for the IAS 39 incurred loss model. The change has occurred as a result of views that the IAS 39 model did not reflect impairment losses incurred in a timely manner during the financial crisis. IFRS 9 will require an increased amount of judgment in identifying and quantifying inputs into expected loss models, resulting in potential variances in application. As a result, IFRS 9 requires numerous disclosures designed to create transparency across industry participants. Benefits of adopting IFRS 9 Impairment are:

Deliverables: ► Financial impact: financial impact assessment including sensitivity

analysis of methodological assumptions and risk parameters.

► Organizational impact: impact assessment for each dimension of your business, from data management to stakeholder engagement.

Value proposition: Facilitates revisiting of credit modelling activities and pricing structures while enabling greater operational oversight of credit risk.

Deliverables: ► System diagnostic: identification of new data requirements and

assessment of current calculation engines.

► System design: design / implement initial system changes, including design of roles and responsibilities.

Value proposition: Leveraging your existing systems to develop and implement a fit for purpose solution. This enables identification of possible alignment with other regulatory data requirements.

Deliverables: ► Impairment methodology: develop and implement the impairment

methodology: quantitative and financial perspective.

► Technical support: training for your staff, including assistance with testing, validating and implementation of models.

► Board support: interaction with those charged with governance, including preparation of briefing papers.

Value proposition: Smooth transition with minimal business disruption, and implementation of a solution designed to enable an efficient operating model going forward.

More insights in credit risk of portfolios

Greater Operational Oversight

More alignment Finance and Risk

Alignment with regulations

Enhanced data analytics

Impa

ct a

sses

smen

t Sy

stem

des

ign

Impl

emen

tatio

n

Page 33

Implementation approach Hedge accounting

The objective of the IFRS 9 hedge accounting framework is to simplify application, align accounting outcomes to economic realities, and provide useful information regarding risk management activities. Development of the revised framework involved ongoing industry consultation to address as many concerns of information preparers and users as possible. This yielded a more practical standard, which streamlines implementation for those already applying hedge accounting, and incentivizes those not to reconsider. Benefits of hedging under IFRS 9 include:

Deliverables: ► Accounting analysis: assessment of the eligibility of your risk

management strategies for hedge accounting under IFRS 9.

► Performance assessment: analysis of the effectiveness of your risk management strategies in achieving your objectives.

Value proposition: Designing of effective hedge structures and aligning accounting outcomes with the economic reality of your risk management strategies.

Deliverables: ► System diagnostic: identification of system requirements, and

assessment against existing capabilities.

► System design: implementing (where necessary) system changes, including the design of roles and responsibilities.

Value proposition: Leveraging your existing systems to develop and implement a fit for purpose solution – identifying common challenges and practical solutions.

Deliverables: ► Hedging framework: identify your risk management objectives,

design testing scripts, and complete documentation.

► Technical support: training for your staff, including assistance with deal setup within your treasury software.

► Board support: interaction with those charged with governance, including preparation of briefing papers.

Value proposition: Smooth transition with minimal business disruption, and implementation of a solution designed to enable an efficient operating model going forward.

Less P&L volatility

Additional qualifying exposures

Simplified testing model

Less breakage of hedges

Less clerical burden

Impa

ct a

sses

smen

t Sy

stem

des

ign

Impl

emen

tatio

n

Page 34

IFRS 9 A practical world view

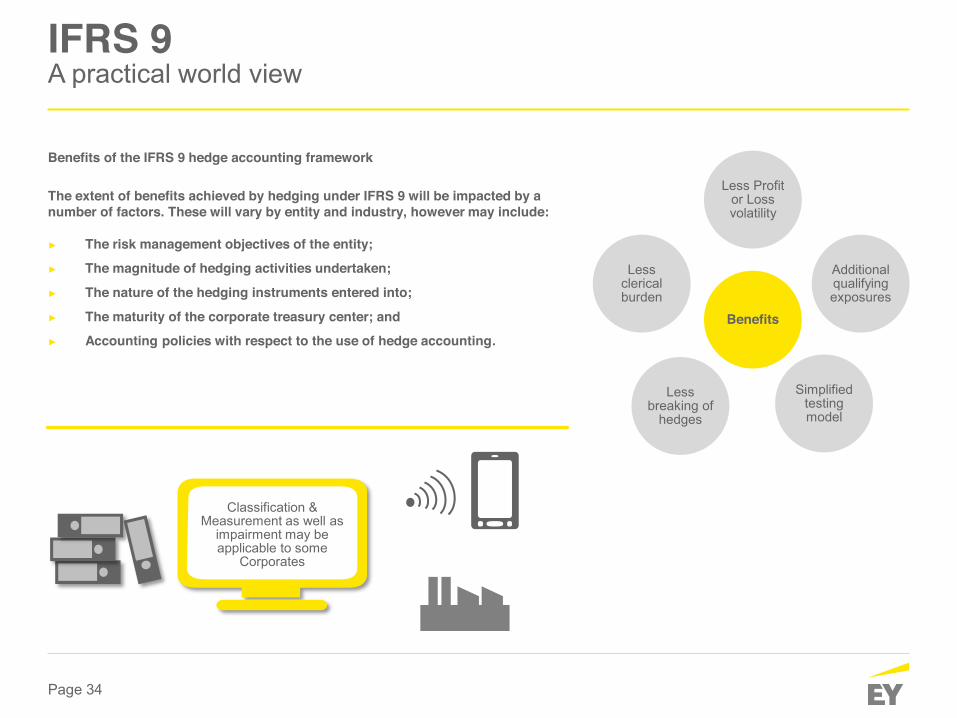

Benefits of the IFRS 9 hedge accounting framework The extent of benefits achieved by hedging under IFRS 9 will be impacted by a number of factors. These will vary by entity and industry, however may include: ► The risk management objectives of the entity;

► The magnitude of hedging activities undertaken;

► The nature of the hedging instruments entered into;

► The maturity of the corporate treasury center; and

► Accounting policies with respect to the use of hedge accounting.

Classification & Measurement as well as

impairment may be applicable to some

Corporates

Benefits

Less Profit or Loss volatility

Additional qualifying exposures

Simplified testing model

Less breaking of

hedges

Less clerical burden

Page 35

IFRS 9 Brochure

► EY periodically publishes updates about IFRS 9 and the impact it has

► We have published a brochure on the 7th of March, which will be shared with you together with the material of today’s session

The better the question. The better the answer.�The better the world works.

Dutch Association of Corporate Treasurers Valuations adjustments: IFRS 13

Page 37

Agenda

This section contains information regarding: ► Pre-Lehman and Post-Lehman situation ► Credit risk in valuation of derivative ► What is Credit Valuation Adjustment (CVA) / Debit Valuation Adjustment (DVA)? ► CVA Components

This section contains information regarding:

► Counterparty Credit Risk exposure ► What is the exposure to counterparty risk? ► Exposure at Default (EAD): Maturity model ► Reducing exposure ► Collateral and Margining

This section contains information regarding:

► Probability of Default (PoD) calculation: Market vs. Historical PoD’s ► Main data and proxies used for PoD calculation ► Proxy curves

Page 38

CVA / DVA

Page 39

What is CVA/DVA?

► Credit Value Adjustment (CVA) is the market value of the risk component correcting for the Counterparty Credit Risk (CCR) in the value of the derivative

► Debt Value Adjustment (DVA) is the market value of the risk component correcting for the own

credit risk in the value of the derivative

► IFRS requires adjustment of Fair Value for CVA/DVA

CVA was a major driver of balance sheet volatility during the crisis

Page 40

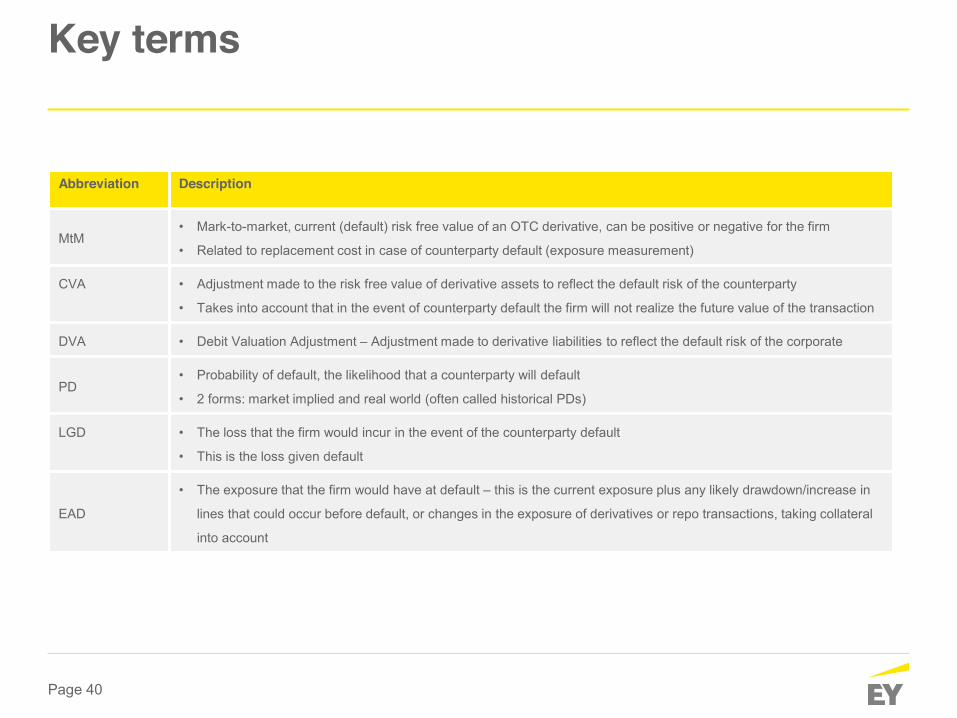

Key terms

Abbreviation Description

MtM • Mark-to-market, current (default) risk free value of an OTC derivative, can be positive or negative for the firm

• Related to replacement cost in case of counterparty default (exposure measurement)

CVA • Adjustment made to the risk free value of derivative assets to reflect the default risk of the counterparty

• Takes into account that in the event of counterparty default the firm will not realize the future value of the transaction

DVA • Debit Valuation Adjustment – Adjustment made to derivative liabilities to reflect the default risk of the corporate

PD • Probability of default, the likelihood that a counterparty will default

• 2 forms: market implied and real world (often called historical PDs)

LGD • The loss that the firm would incur in the event of the counterparty default

• This is the loss given default

EAD

• The exposure that the firm would have at default – this is the current exposure plus any likely drawdown/increase in

lines that could occur before default, or changes in the exposure of derivatives or repo transactions, taking collateral

into account

Page 41

Pre-Lehman Banks are considered to have very low risk

Lehman defaults September 15, 2008 Lehman Brothers defaults and goes bankrupt.

Post-Lehman “Banks can go bankrupt”

Credit risk banks Credit risks of banks are in Lending or in fair value fluctuations on derivatives

Risk mitigation Market participants can use collateral to mitigate credit risk on derivative transactions

Uncollateralized? For uncollateralized transactions: still a credit risk for banks

Credit risk on FV Credit risk FV should be reflected in valuation of derivative (requirement under IFRS / Dutch GAAP

CVA Credit Valuation Adjustment needs to be made and incorporated in the valuation

Example Valuation ex. CVA: 10

CVA -1

Valuation incl. CVA 9

CVA / DVA An overview

Page 42

Credit Valuation Adjustment (CVA) Example

Fair value Difference (CVA)

Difference %

Value excluding CVA € 50,800,523 - -

Value with counterparty:

Rabobank (AA-) € 47,347,373

€ 3,453,149 6,79%

ING (A) € 46,378,769

€ 4,421,753 8,70%

SNS (BBB-) € 39,760,582

€ 11,039,940 21,73%

CVA takes counterparty risk into account and can vary substantially depending on the creditworthiness of the counterparty

Attention

► Valuation of (uncollateralized) derivative depends on counterparty

Page 43

CVA Components

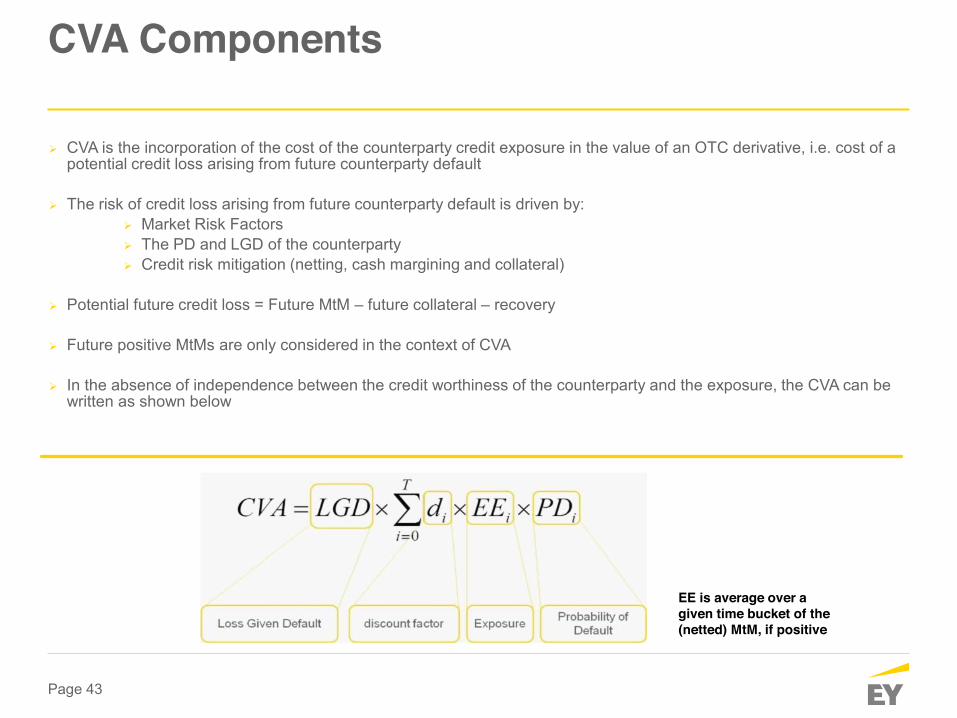

¾ CVA is the incorporation of the cost of the counterparty credit exposure in the value of an OTC derivative, i.e. cost of a potential credit loss arising from future counterparty default

¾ The risk of credit loss arising from future counterparty default is driven by: ¾ Market Risk Factors ¾ The PD and LGD of the counterparty ¾ Credit risk mitigation (netting, cash margining and collateral)

¾ Potential future credit loss = Future MtM – future collateral – recovery

¾ Future positive MtMs are only considered in the context of CVA

¾ In the absence of independence between the credit worthiness of the counterparty and the exposure, the CVA can be written as shown below

EE is average over a given time bucket of the (netted) MtM, if positive

Page 44

Expected Exposure

Page 45

Example of Counterparty Credit Risk

Interest Rate Swap between Corporate and Bank

Floating liability payments Lays off exposure to the market

Pay Floating

Pay Fixed rate

Bank Corporate

► Market value at inception is 0 to both counterparties (no arbitrage)

► As soon as interest rates deviate from initial expectations, the trade will become more valuable to one counterparty

► The replacement cost at that point will be positive to one counterparty and negative to the other

► The counterparty to whom the trade is more valuable hence has an exposure

Page 46

Counterparty Credit Risk exposure For OTC derivatives

Life of contract

Out of the money

In the money Counterparty Credit Risk for the firm

Counterparty Credit Risk for the counterparty

Page 47

What is the exposure to counterparty risk?

Source: Pykthin, Jan 2011

Page 48

Exposure at Default (EAD): Maturity model

► The Exposure at Default calculation can be performed through increasingly sophisticated models

1

2

3

4

5

MTM: Where the MTM is the replacement cost

MTM + Regulatory Add-on: Mark-to-Market + (Notional * Add-on Factor)

MTM + Calibrated Add-on: Internal Add-on calculation

Analytical calculation: Analytical solutions for EE and PFE

Montecarlo Simulation: Full projection of market risk factors and revaluation of exposure at default

Page 49

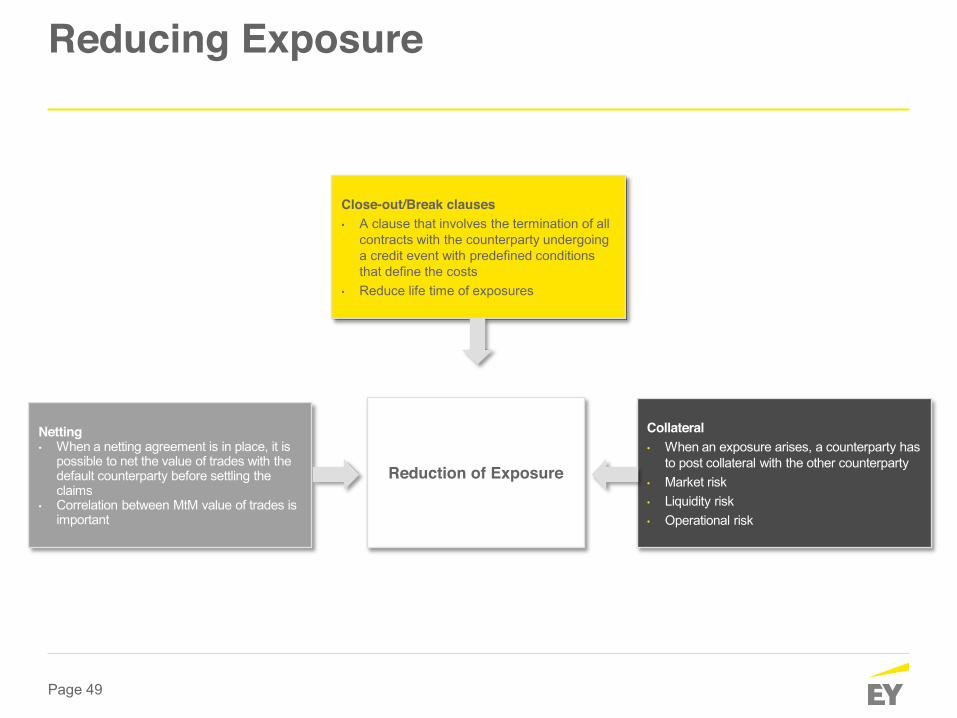

Reducing Exposure

Close-out/Break clauses • A clause that involves the termination of all

contracts with the counterparty undergoing a credit event with predefined conditions that define the costs

• Reduce life time of exposures

Collateral • When an exposure arises, a counterparty has

to post collateral with the other counterparty • Market risk • Liquidity risk • Operational risk

Netting • When a netting agreement is in place, it is

possible to net the value of trades with the default counterparty before settling the claims

• Correlation between MtM value of trades is important

Reduction of Exposure

Page 50

Collateral and Margining ¾ Financial collateral is used to reduce the positive exposure ¾ Parties typically have to post:

• Initial Margin • Variation Margin

¾ Credit support annex (CSA) – defined terms • One way or two way • Acceptable collateral (e.g. cash, government securities etc.) • Haircuts • Frequency • Threshold amount (unsecured amount) • Minimum Transfer Amount (no smaller collateral transfer) • Independent Amount (given upfront)

¾ Some issues: • Collateral disputes • Operational / settlement failures

¾ Margin period of risk: period over which additional collateral may not be forthcoming • Measures the time between last received margin call and closeout/re-hedge in a worst-case scenario • Collateral haircuts are meant to reflect the potential variation in the value of the collateral over that

period

Page 51

Probability of Default (PD)

Page 52

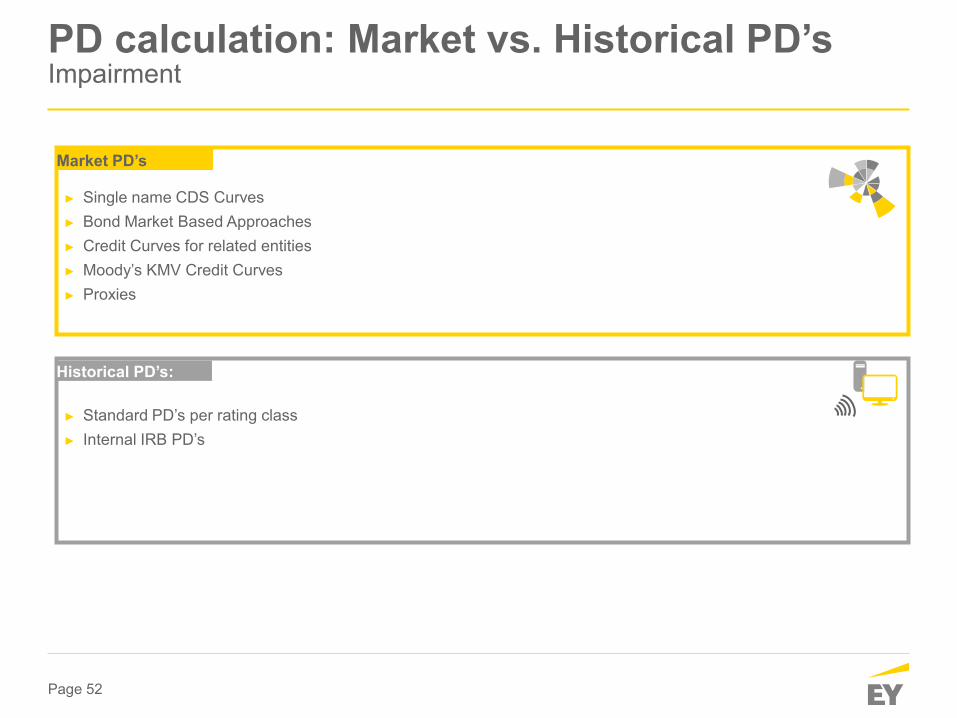

PD calculation: Market vs. Historical PD’s Impairment

► Single name CDS Curves ► Bond Market Based Approaches ► Credit Curves for related entities ► Moody’s KMV Credit Curves ► Proxies

► Standard PD’s per rating class ► Internal IRB PD’s

Market PD’s

Historical PD’s:

Page 53

PROXY CURVES DESCRIPTION

► CDS Spread curves for over 2000 entities published daily – historical data available ► Full term structure information across 11 tenors (6M, 1Y, 2Y, 3Y, 4Y, 5Y, 7Y, 10Y, 15Y,

20Y, 30Y) ► Recovery Rate, Currency, Tier, Sector, Aggregate Ratings, Quote depth available for

each entity ► Additional CDS liquidity details (e.g., Bid/Offer, No of daily quotes, No of EOD

contributions, Quote staleness measures) available as additional service

Single name CDS Curves

► If entity has large bond issuance and a liquid bond market, credit risk information from bond market may be used to proxy CDS curves, e.g., supranationals

► Asset Swap Spreads or spread to bunds of bonds with comparable maturity can be used as proxy for CDS spreads

► Alternatively, OAS can be used as proxies ► Lack of clarity how to define the spread. What is it remunerating (credit, liquidity, risk

free?)

Bond Market Based Approaches

► Parent or subsidiary entities may be actively traded in the CDS market – may use these curves but may need to adjust the spreads according to relationship between entities, guarantees

► Entities with Op Co/Hold Co structures, only LGD adjustment may be necessary without any adjustments to the default probabilities

Credit Curves for related entities

Main data & proxies used for PD calculation

Page 54

Main data & proxies used for PD calculation (continued)

► Equity implied CDS curves based on the Merton type ► Moody’s model links CDS spreads to risk neutral default probabilities and risk-neutral

default probabilities to physical default probabilities – conversion of CDS spreads into EDF levels and vice-versa. Sharpe ratio approach.

► Implied LGD, Sector LGD and spreads/EDFs across the term structure available ► Historical data available

► Use entities with CDS spreads with same rating, sector and region ► Benchmark curve constructed using geometric mean of all CDS spreads with similar

attributes ► Calculate geometric mean across all tenor points

► Use past default experience to predict future default likelihood ► For example, Moody’s publishes transition matrices per rating class ► Can be used to calculate PD per rating class

PROXY CURVES DESCRIPTION

Moody’s KMV Credit Curves

Benchmark Curve Construction

Historical data

The better the question. The better the answer.�The better the world works.

Dutch Association of Corporate Treasurers Other Regulation

Page 56

Agenda

This section contains information regarding: Regulation, challenges and impact of: ► OTC Derivatives reform: EMIR & MiFID II ► Notional Pooling ► Tax: FTT and BEPS

Wrap-up and Questions

Page 57

Regulation

About color themes Choose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

2013 2014 2015 2016 2017 2018 2019

Basel III: 2013

Gradual phasing in of capital requirements

The following provides a summary of regulatory change over the recent and coming period:

Paym

ent r

egul

atio

n FX

/ H

edgi

ng re

gula

tion

SEPA: August 2014

SEPA SCT and SDD effective. Non-EUR countries follow in 2016

Basel III: 2015

Higher capital requirements. Leverage ratio tracked/disclosed

PSD II: 2015

Complete legislative process by end 2015

Basel III: 2017

Update to Leverage ratio requirements

PSD II: 2017

PSD II effective in law EEA

EMIR: 2012

EMIR comes into force. Regulation on OTC derivatives, CCP and trade repositories

MiFID II: July 2014

MiFID II and MiFIR announced replacing MiFID I

Dodd Frank: July 2015

Volcker Rule live

MiFID II: July 2016

Deadline for implementation of MiFID II under national laws

EMIR: September 2016

NFC+: Variation margining requirements for non-centrally cleared trades

MiFID II: January 2018

Start of application MiFID II and MiFIR Level 1 and 2 in EU States

Dodd Frank: 2019

Supplementary leverage ratio

Other matters Regulatory developments

Page 58

About color themes Choose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

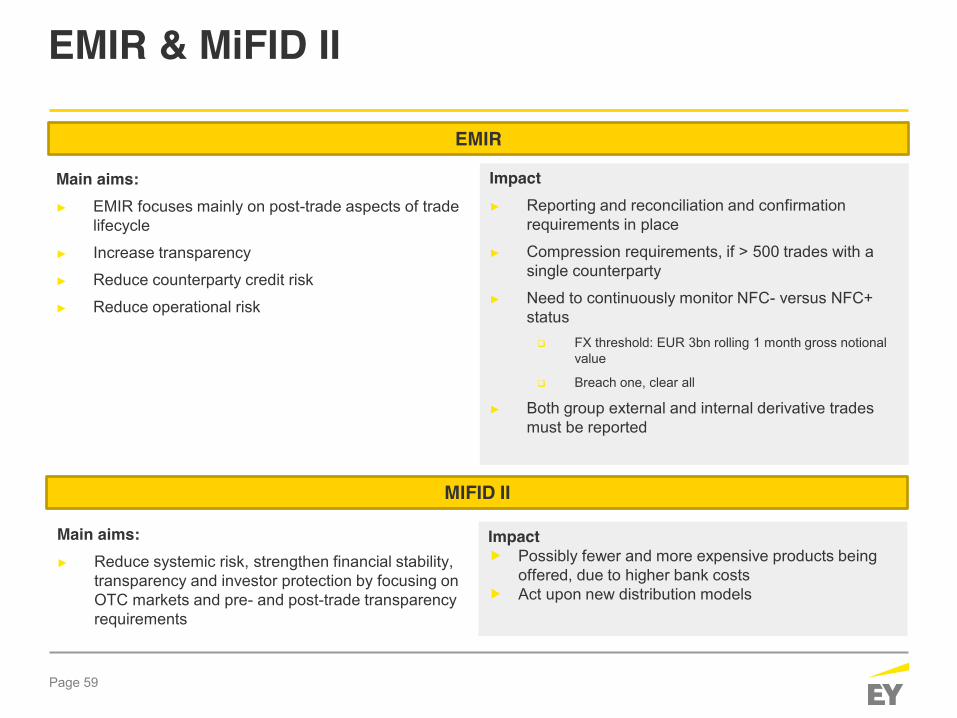

EMIR & MiFID II

Main aims: ► EMIR focuses mainly on post-trade aspects of trade

lifecycle

► Increase transparency

► Reduce counterparty credit risk

► Reduce operational risk

Impact ► Reporting and reconciliation and confirmation

requirements in place

► Compression requirements, if > 500 trades with a single counterparty

► Need to continuously monitor NFC- versus NFC+ status � FX threshold: EUR 3bn rolling 1 month gross notional

value

� Breach one, clear all

► Both group external and internal derivative trades must be reported

EMIR

MIFID II

Main aims: ► Reduce systemic risk, strengthen financial stability,

transparency and investor protection by focusing on OTC markets and pre- and post-trade transparency requirements

Impact f Possibly fewer and more expensive products being

offered, due to higher bank costs f Act upon new distribution models

Page 59

About color themes Choose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

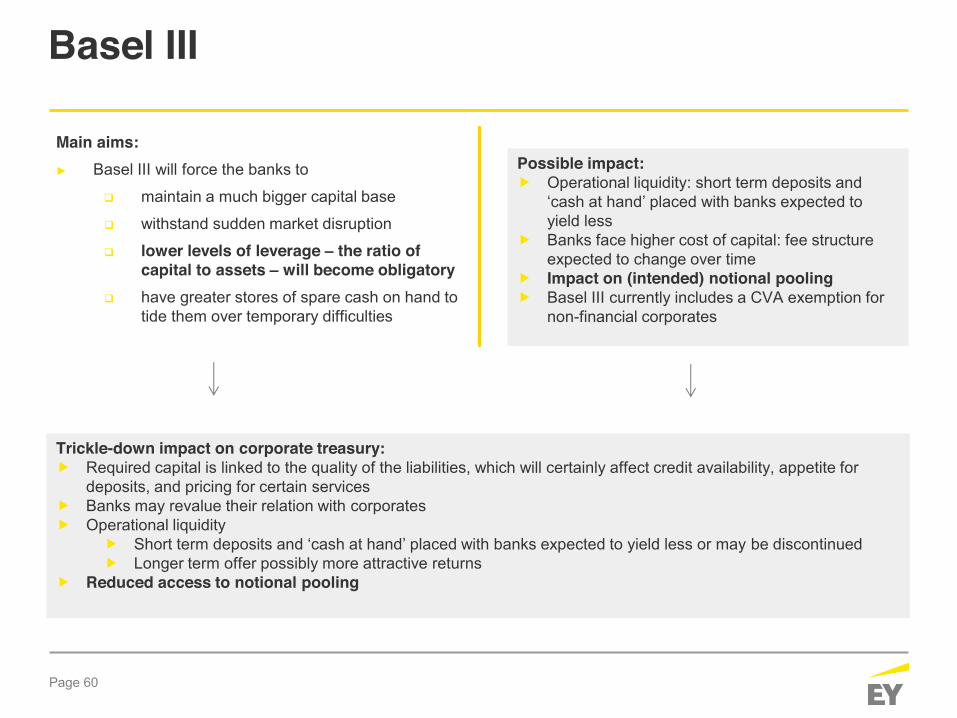

Basel III

Main aims: ► Basel III will force the banks to

� maintain a much bigger capital base

� withstand sudden market disruption

� lower levels of leverage – the ratio of capital to assets – will become obligatory

� have greater stores of spare cash on hand to tide them over temporary difficulties

Possible impact: f Operational liquidity: short term deposits and

‘cash at hand’ placed with banks expected to yield less

f Banks face higher cost of capital: fee structure expected to change over time

f Impact on (intended) notional pooling f Basel III currently includes a CVA exemption for

non-financial corporates

Trickle-down impact on corporate treasury: f Required capital is linked to the quality of the liabilities, which will certainly affect credit availability, appetite for

deposits, and pricing for certain services f Banks may revalue their relation with corporates f Operational liquidity

f Short term deposits and ‘cash at hand’ placed with banks expected to yield less or may be discontinued f Longer term offer possibly more attractive returns

f Reduced access to notional pooling

Page 60

About color themes Choose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

Financial Transaction Tax (FTT)

Main aims: ► Developing a common tax within the EU reserved for financial transactions

► 8 December 2015: 10 Eurozone countries agreed on some aspects of FTT, giving themselves till mid 2016 to reach agreement on remaining issues

Possible impact ► 10 countries: Germany, France, Italy, Austria, Belgium, Greece, Portugal, Slovakia, Slovenia and Spain

► The statement said all share transactions, including intraday trading, would be taxed. The tax would be paid by traders in one of the countries participating in the scheme on shares issued in those countries

► Subject to completion of the (political) process and negotiations

Many question marks and potentially large impact

Page 61

About color themes Choose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

Base Erosion and Profit Shifting (BEPS)

Main aim: ► Address the negative effect of tax avoidance strategy

► Address the widespread perception that corporations don’t pay their fair share of taxes

Timeline: ► BEPS action plan endorsed by G20 in 2013

► OECD produced detailed reports and actions in September 2014 (guidelines, not yet law)

► EU has proposed the EU Anti BEPS directive

► Expected to be approved by EU in 2016/2017

Focus for Treasuries ► Foreign Treasury vehicles: low effective tax rates reason for scrutiny

► Limits on interest expense deductions

► Increased focus on tax-asymmetry (e.g. hybrid debt)

► Transfer pricing (including cashpools, intercompany funding)

► Increasingly important that tax, treasury and business are aligned with regard to decision making on intra-group financial transactions

Page 62

About color themes Choose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

BEPS site on ey.com

Page 63

Alerts

About color themes Choose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

Further information

Should you have any queries or require any further information, please do not hesitate to contact our team of industry leading advisors:

Ruud Bulkmans Director +31 88 407 1193 [email protected]

Sander de Ruiter Senior Manager +31 88 407 1590 [email protected]

Floris van de Loo Director +31 88 407 1654 [email protected]

Page 64

EY | Assurance | Tax | Transactions | Advisory

About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2016 EYGM Limited. All Rights Reserved.

EYG no.

EMEIA Marketing Agency 1001050

ED None. In line with EY’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com