26

Welcome Law Seminars International “Audits of Operating Expenses and Real Estate Taxes: Language and Reality”

Welcome LawSeminars

International“Audits of Operating

Expenses and RealEstate Taxes:Language and

Reality”

Introduction to the Panel

Terry Barger, Managing Member

CyberLease, LLC

*********

Marc Betesh, President

KBA Lease Services

CyberLease, LLCand

KBA Lease ServicesLease audit services for tenants for the past 20

years

Unique Perspective

• Part Landlord / Property Manager• Part Broker• Part Attorney• Part Accountant• Part Arm-chair Quarterback

Landlord’s thought process

Complexity of Operating Expenses

Today’s Agenda

Explore 2 specific issues – GAAP andAudit Rights

Show problematic lease language fromactual leases

Discuss how to negotiate better language

Questions and answers

GAAPWhat is GAAP?

• Generally Accepted Accounting Principles A series of books which one can obtain clarification Standardizes treatment of financial statements Bolsters reliability of statements

• What does it require? Matching (expenses to revenue)

(cost to time period incurred) Accruals (12 months in each year) Definition of capital expenditures and the treatment

thereof

Where is GAAP applicable?

• Financial statements• Real estate leases

GAAP - Lease Applicability

• Management Fee Requires uneven rent streams to be straight-lined (FASB

13) for financial statement purposes. If rent partially or fully abated in base year,

management fee would be artificially low.

• Annualization / Equivalency – Protects against base year having 10 months of

expense, and other years having 13 months of expense.

• Capital Expenditures• Applying expenses to the year it was incurred –

Real Estate Taxes in particular• Isolates P&L’s for Special Cost Centers

HVAC and Garage expenses

GAAPOther Benefits

Basic Protections

• No duplication of costs or revenues

• Mathematical / proceduralsoundness

• Provide clarification for “fuzzy”description of capital contained inmost leases

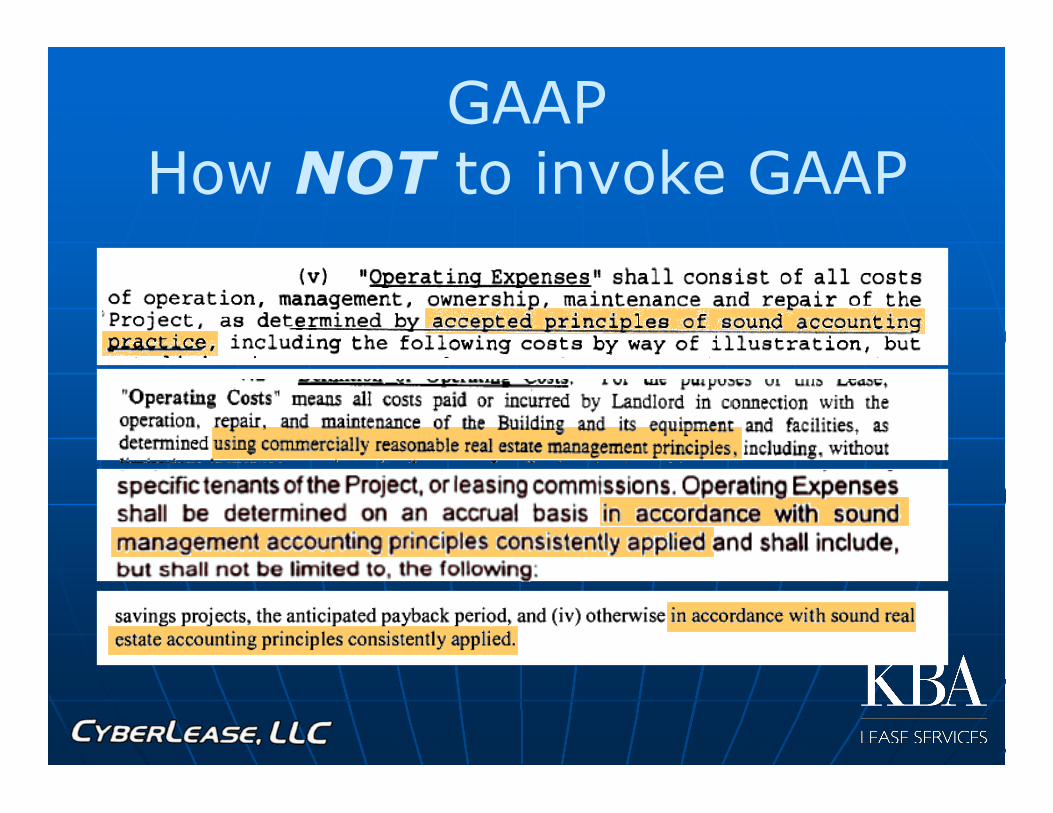

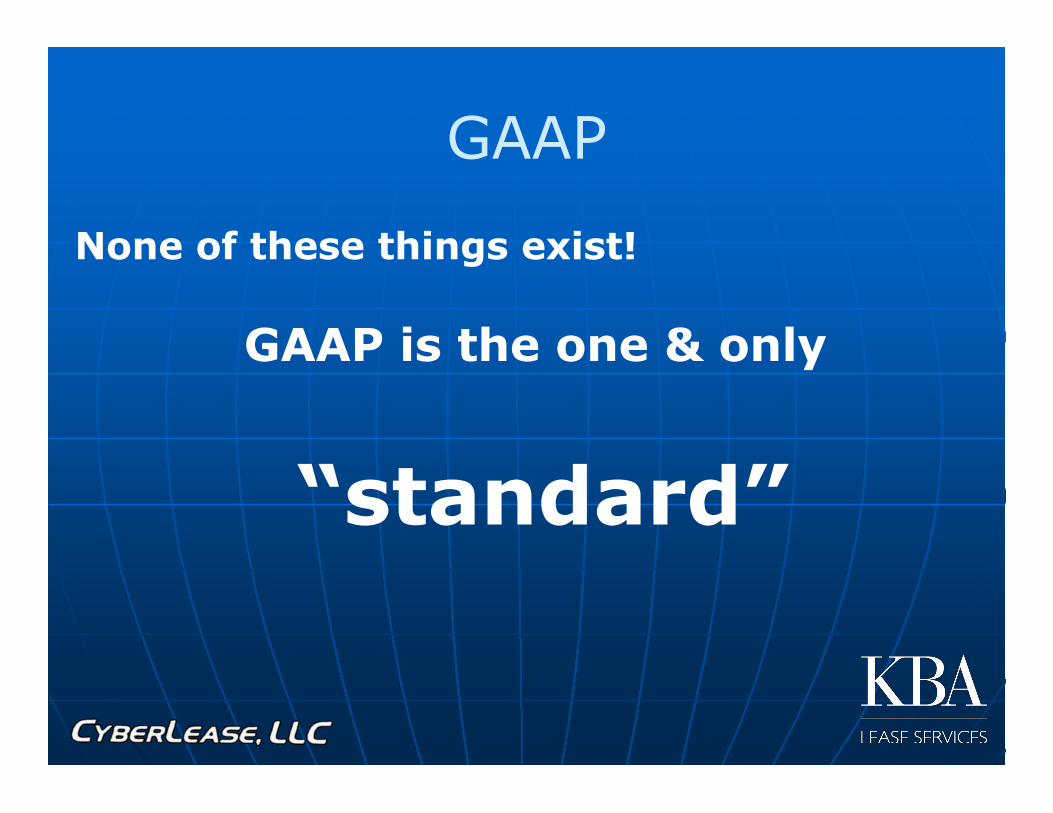

GAAPHow NOT to invoke GAAP

GAAP

None of these things exist!

GAAP is the one & only

“standard”

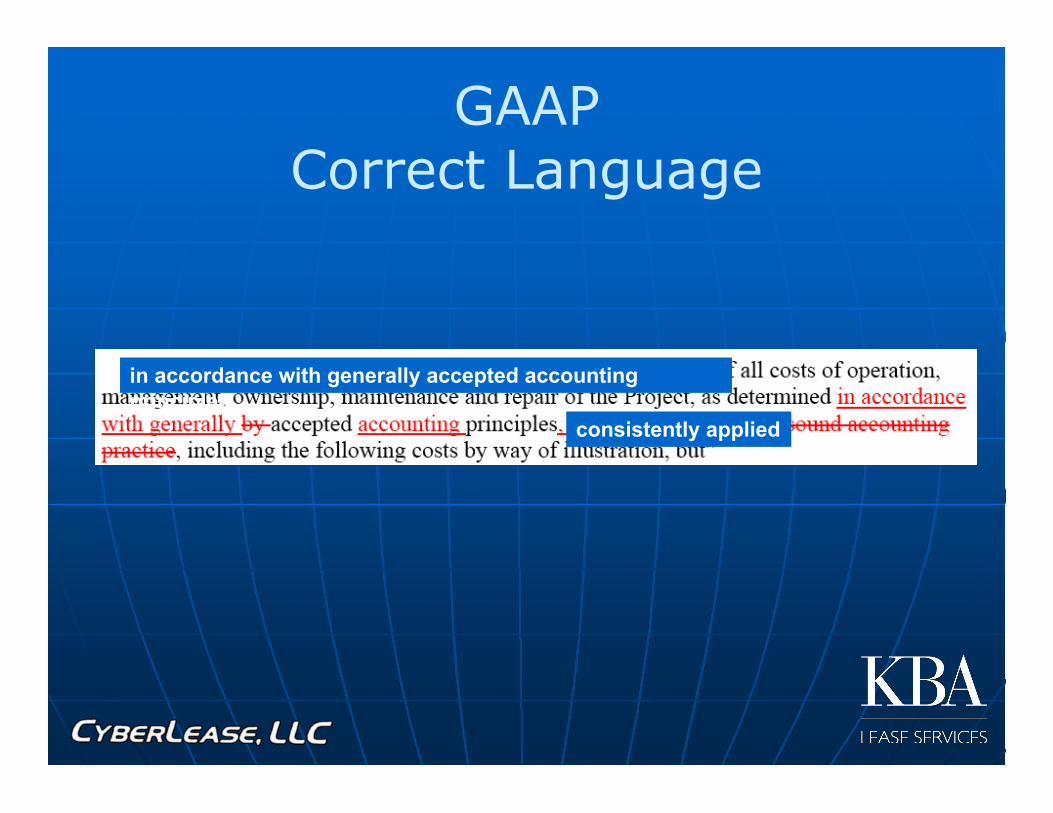

in accordance with generally accepted accountingprinciples

consistently applied

GAAPCorrect Language

GAAP or No GAAP Negotiating the Best

Language REITS and pensions funds already required to

maintain financials pursuant to GAAP

If landlord not a REIT or pension fund, usecompetitive buildings as basis for “market”

GAAP provides the parties with an impartialauthority – helps eliminate/resolve disputes

Provides tenant with most basic protections –landlord refusal makes its intentions appearsuspect

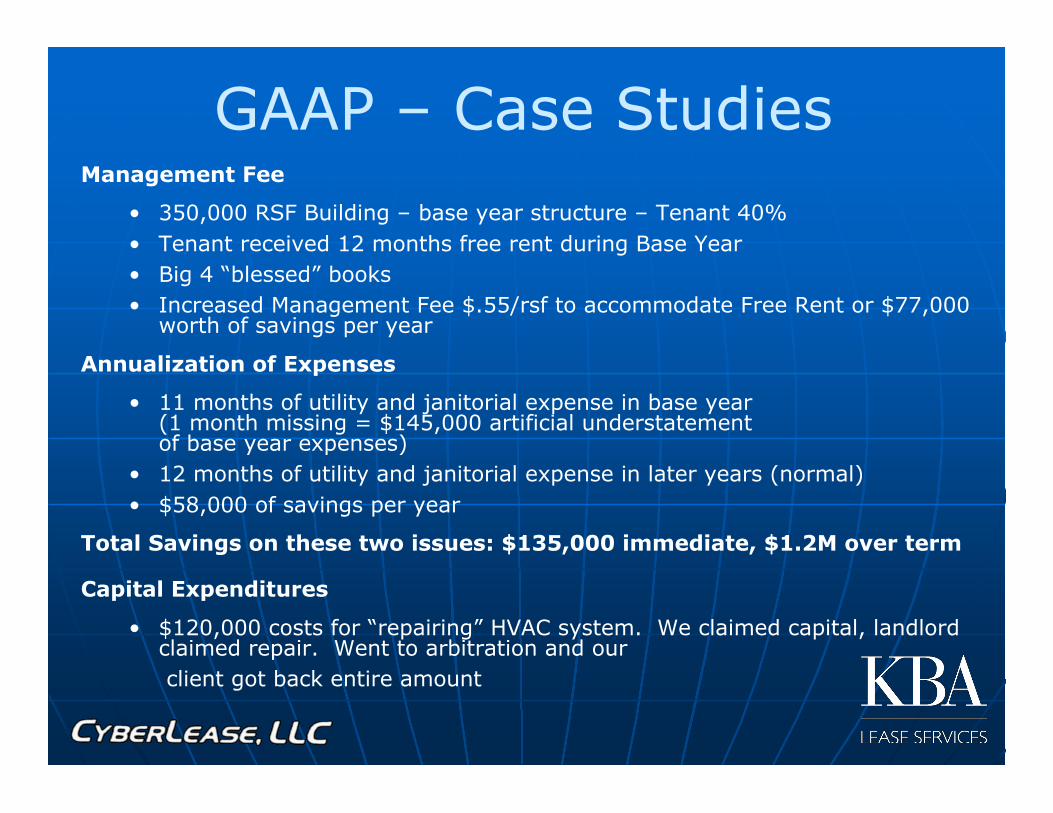

GAAP – Case StudiesManagement Fee

• 350,000 RSF Building – base year structure – Tenant 40%• Tenant received 12 months free rent during Base Year• Big 4 “blessed” books• Increased Management Fee $.55/rsf to accommodate Free Rent or $77,000

worth of savings per year

Annualization of Expenses

• 11 months of utility and janitorial expense in base year(1 month missing = $145,000 artificial understatementof base year expenses)

• 12 months of utility and janitorial expense in later years (normal)• $58,000 of savings per year

Total Savings on these two issues: $135,000 immediate, $1.2M over term

Capital Expenditures

• $120,000 costs for “repairing” HVAC system. We claimed capital, landlordclaimed repair. Went to arbitration and our client got back entire amount

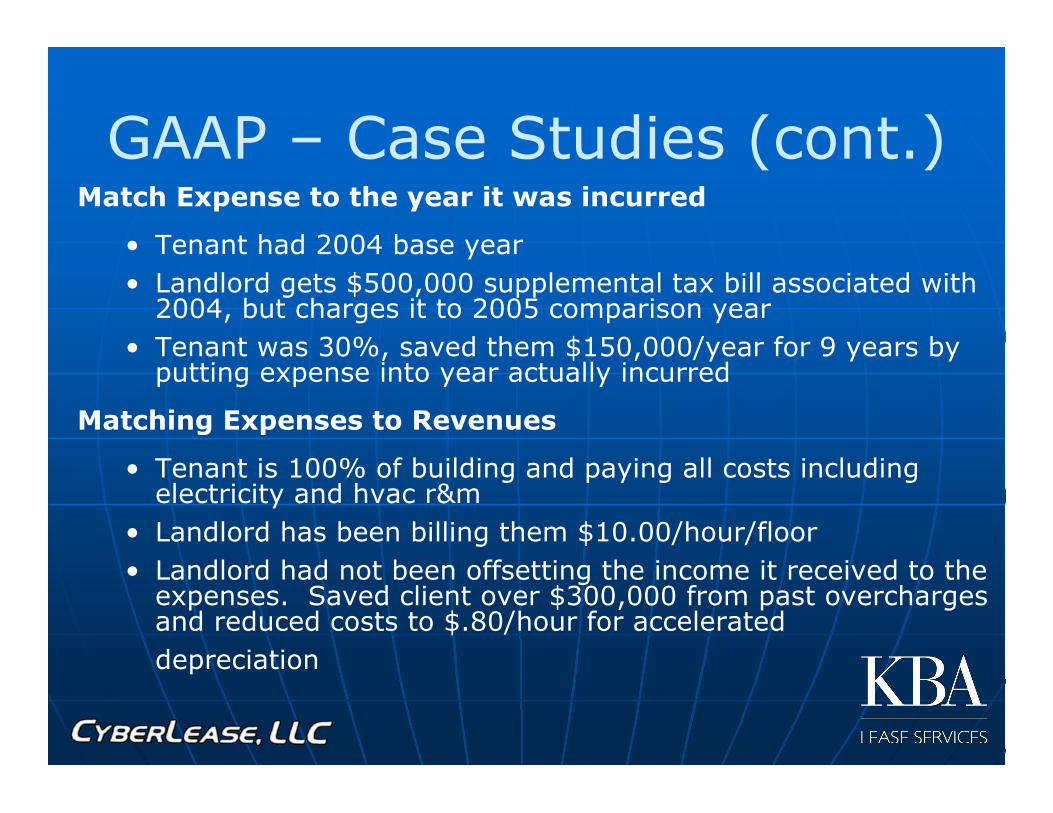

GAAP – Case Studies (cont.)Match Expense to the year it was incurred

• Tenant had 2004 base year• Landlord gets $500,000 supplemental tax bill associated with

2004, but charges it to 2005 comparison year• Tenant was 30%, saved them $150,000/year for 9 years by

putting expense into year actually incurred

Matching Expenses to Revenues

• Tenant is 100% of building and paying all costs includingelectricity and hvac r&m

• Landlord has been billing them $10.00/hour/floor• Landlord had not been offsetting the income it received to the

expenses. Saved client over $300,000 from past overchargesand reduced costs to $.80/hour for accelerateddepreciation

Audit Rights

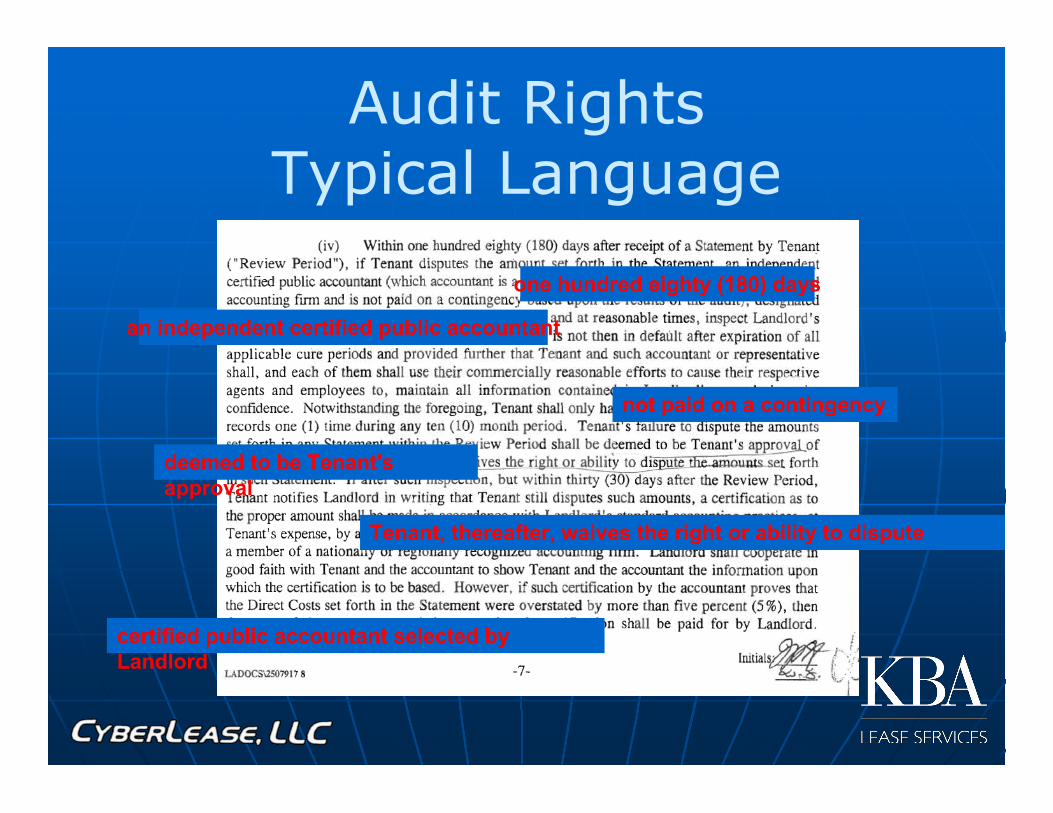

one hundred eighty (180) days

an independent certified public accountant

not paid on a contingency

Tenant, thereafter, waives the right or ability to dispute

deemed to be Tenant'sapproval

certified public accountant selected byLandlord

Audit RightsTypical Language

Audit Rights

Why Does a Tenant Need Them?Need to understand landlord’sthought process

Source of Rights

• Specifically Granted by the Lease

• Specifically Granted by Law

Blue: Explicitly Recognized

Red: Uncommitted on Issue

Audit Rights – Good FaithStates that Recognize Implied Covenant of Good

Faith & Fair Dealing as Applicable to Leases

Audit Rights – TimeRestrictions

Shortened Time Limits

• Notice of objection to bill

• Time to complete audit

• Deadline for commencement ofproceedings if no agreement

• Landlords will “slow play” audit

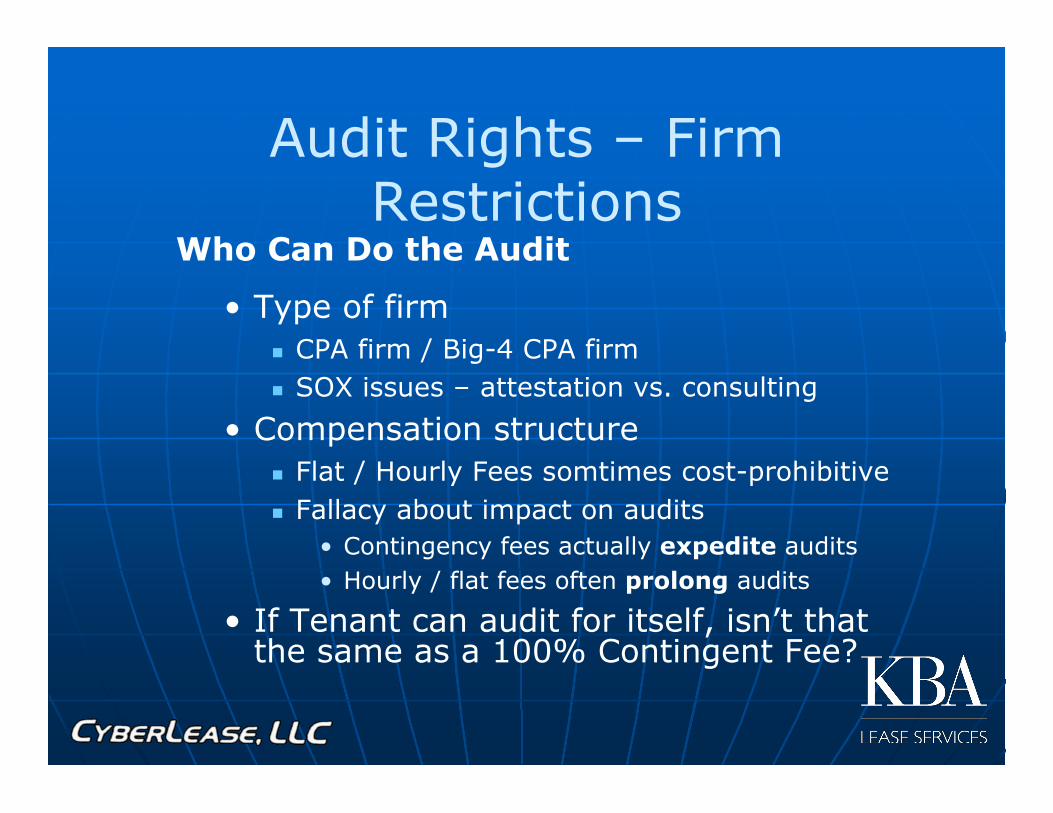

Audit Rights – FirmRestrictions

Who Can Do the Audit

• Type of firm CPA firm / Big-4 CPA firm SOX issues – attestation vs. consulting

• Compensation structure Flat / Hourly Fees somtimes cost-prohibitive Fallacy about impact on audits

• Contingency fees actually expedite audits• Hourly / flat fees often prolong audits

• If Tenant can audit for itself, isn’t thatthe same as a 100% Contingent Fee?

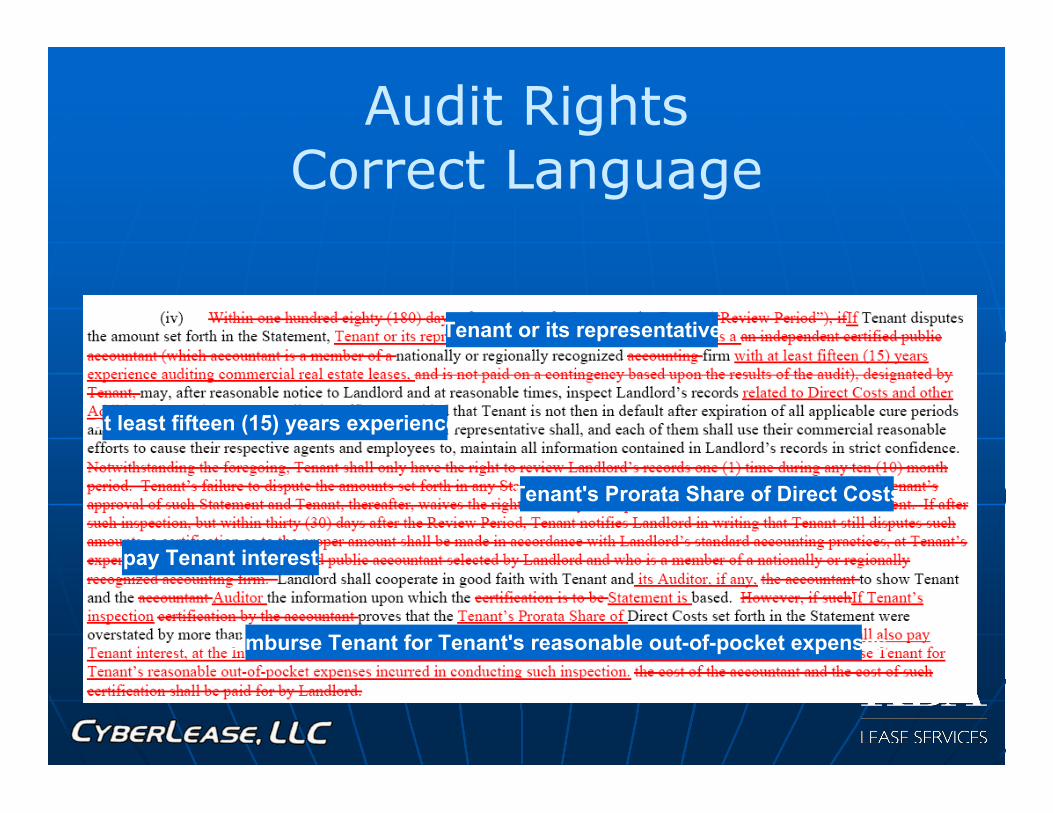

Tenant or its representative

at least fifteen (15) years experience

Tenant's Prorata Share of Direct Costs

pay Tenant interest

reimburse Tenant for Tenant's reasonable out-of-pocket expenses

Audit RightsCorrect Language

Audit Rights -Negotiating Language

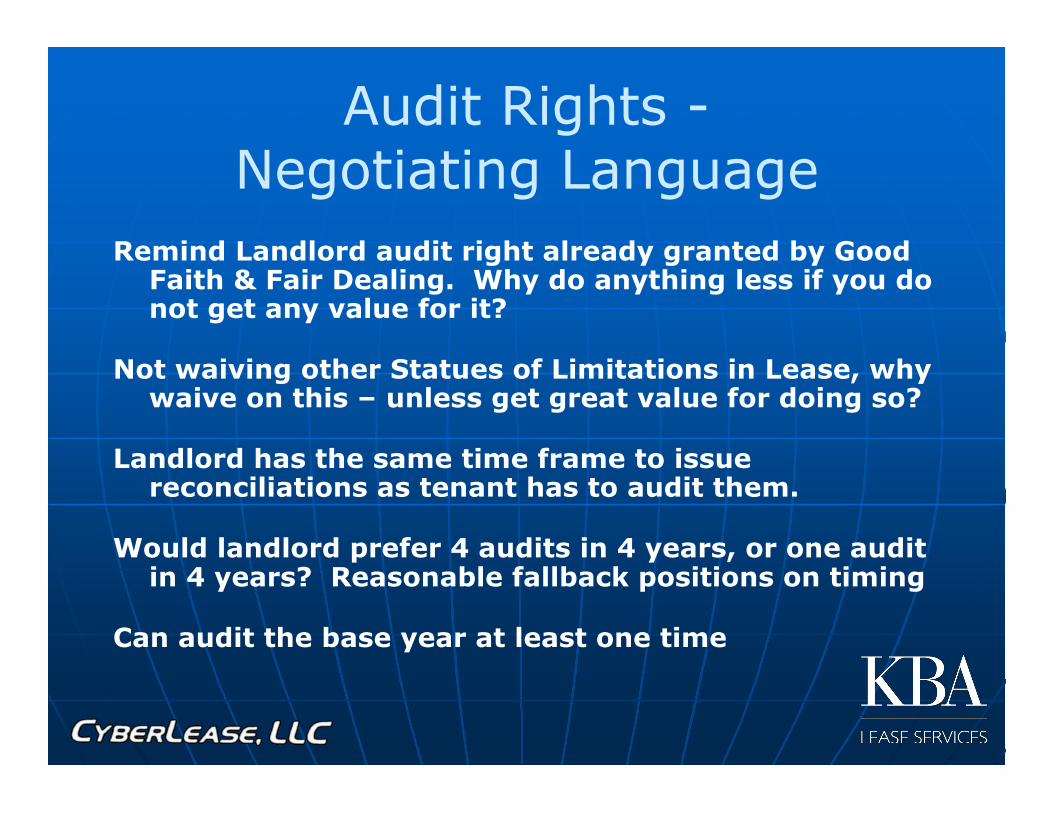

Remind Landlord audit right already granted by GoodFaith & Fair Dealing. Why do anything less if you donot get any value for it?

Not waiving other Statues of Limitations in Lease, whywaive on this – unless get great value for doing so?

Landlord has the same time frame to issuereconciliations as tenant has to audit them.

Would landlord prefer 4 audits in 4 years, or one auditin 4 years? Reasonable fallback positions on timing

Can audit the base year at least one time

Audit Rights – Who CanPerform

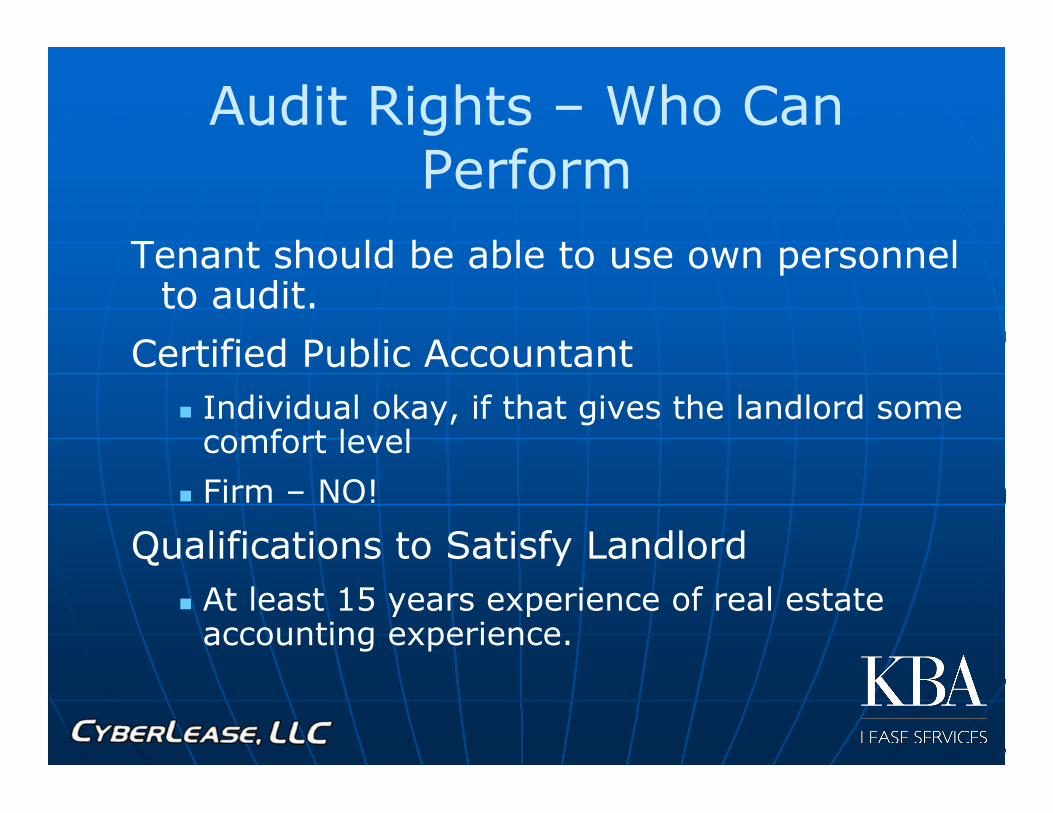

Tenant should be able to use own personnelto audit.

Certified Public Accountant Individual okay, if that gives the landlord some

comfort level

Firm – NO!

Qualifications to Satisfy Landlord At least 15 years experience of real estate

accounting experience.

Audit RightsOther Issues

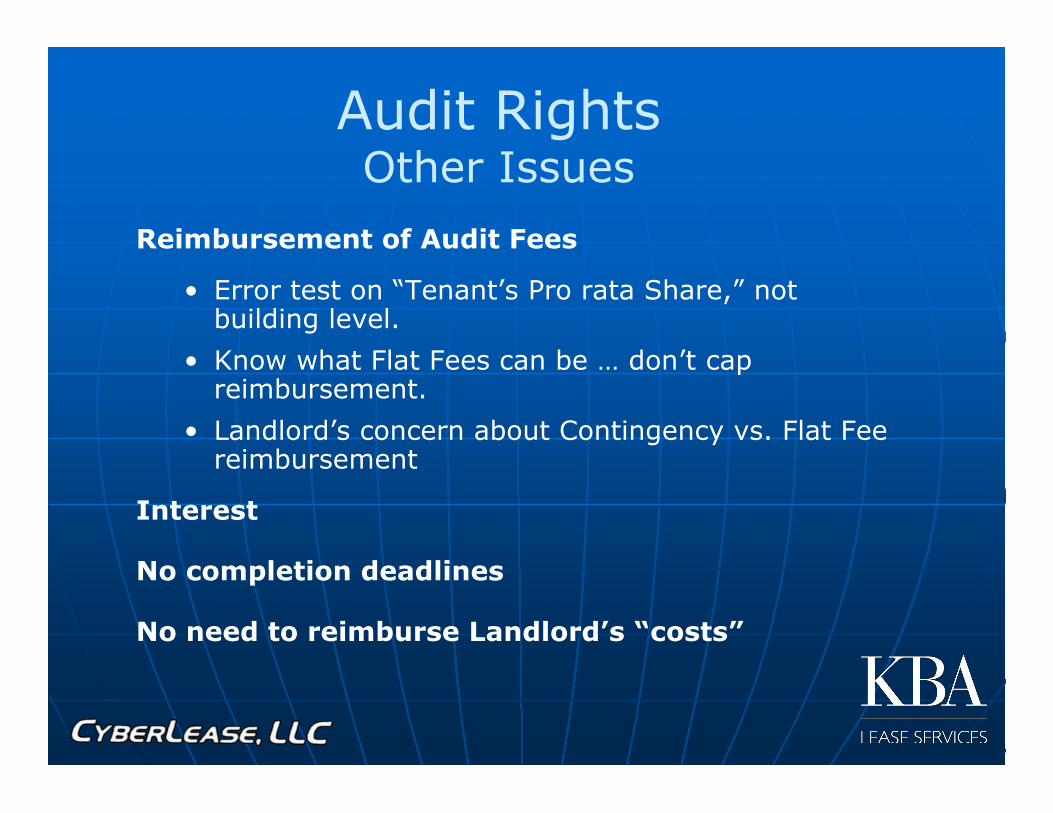

Reimbursement of Audit Fees

• Error test on “Tenant’s Pro rata Share,” notbuilding level.

• Know what Flat Fees can be … don’t capreimbursement.

• Landlord’s concern about Contingency vs. Flat Feereimbursement

Interest

No completion deadlines

No need to reimburse Landlord’s “costs”

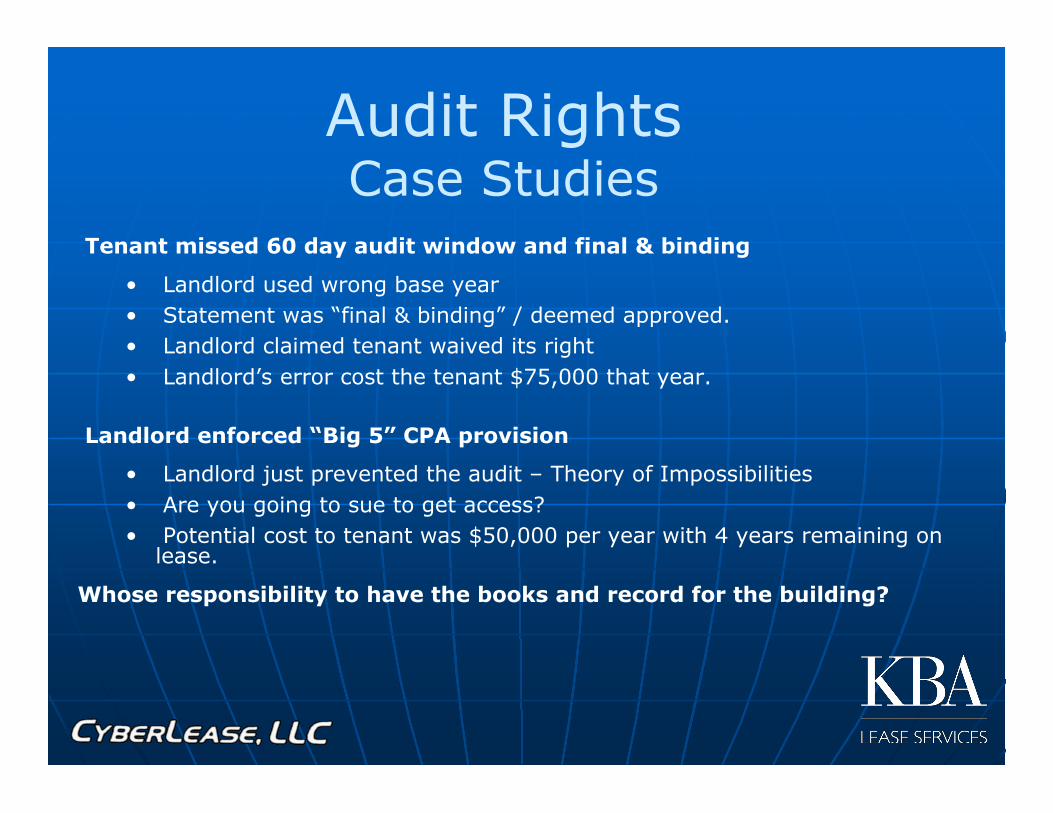

Audit RightsCase Studies

Tenant missed 60 day audit window and final & binding

• Landlord used wrong base year• Statement was “final & binding” / deemed approved.• Landlord claimed tenant waived its right• Landlord’s error cost the tenant $75,000 that year.

Landlord enforced “Big 5” CPA provision

• Landlord just prevented the audit – Theory of Impossibilities• Are you going to sue to get access?• Potential cost to tenant was $50,000 per year with 4 years remaining on

lease.

Whose responsibility to have the books and record for the building?

THANKS!

Q & A