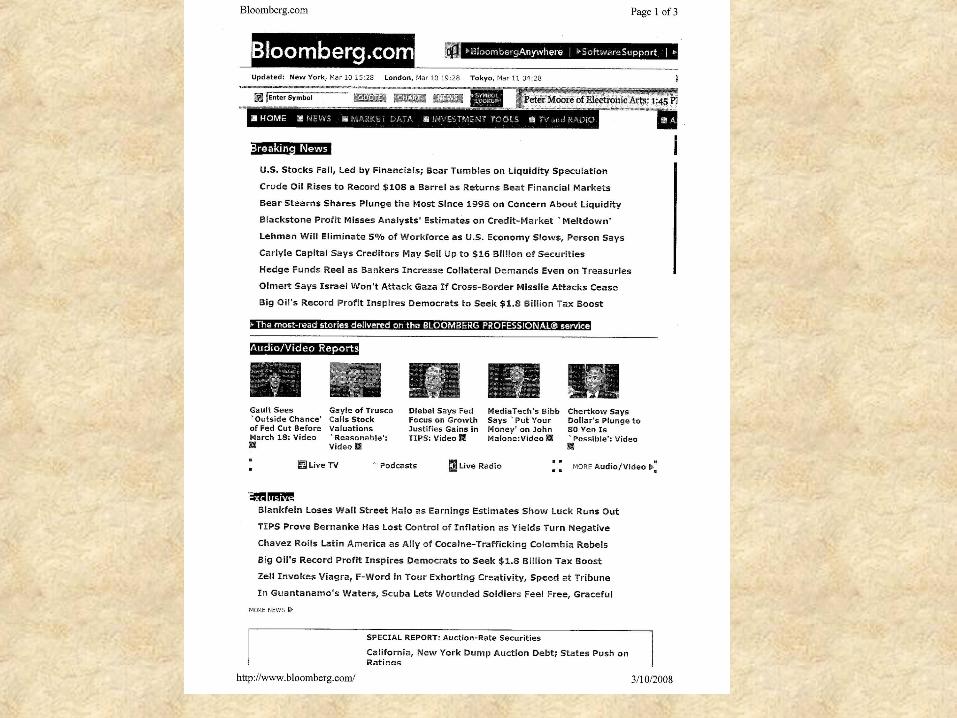

Welcome to the Professional’s Approach to Rollover Concepts Presented by: LFM Fixed Strategies Insurance Services Florian Spinello Lauren Carrasco & Sarah Niss This material is intended to provide general education and is not intended to provide legal or tax advice. It is recommended that decisions be made only after consultation with qualified financial, tax and legal professionals about your specific financial situation.

Transcript

Welcome to the Professional’s Approach to Rollover Concepts

This material is intended to provide general education and is not intended to provide legal or tax advice. It is recommended that decisions be made only after consultation with qualified financial, tax and legal professionals about your specific financial situation.

Who Is LFM Fixed Strategies?

• LFM is a National Marketing Organization for Fixed & Indexed Annuities and Life Insurance Products

• Created by Experienced Producing Registered Representatives / Agents

• Committed to Helping Financial Professionals Address the Growing Demand for Retirement Planning and Income Strategies

FOR PRODUCER USE ONLY. NOT FOR USE WITH THE PUBLIC.

Why LFM Fixed Strategies?

• Experience – We have a team of experienced consultants and seasoned producers to give you the guidance and expertise in your business

• Innovation – We offer innovative sales strategies and unique business opportunities to take you to the next level with your practice

• Dedication – Our support staff is ready to help you submit, track and get you paid on your business, in addition to providing a sales team who is familiar with your company philosophy

FOR PRODUCER USE ONLY. NOT FOR USE WITH THE PUBLIC.

What Carriers does LFM Represent?

FOR PRODUCER USE ONLY. NOT FOR USE WITH THE PUBLIC.

When You Retire or Change JobsWhen You Retire or Change Jobs

How to Shape Your Financial FutureHow to Shape Your Financial Future

OppenheimerFundsOppenheimerFunds

RolloverIRA RolloverIRA

RE0000.271.1101 April 2004

The Decision Takes a Minute, the Results Last a LifetimeThe Decision Takes a Minute, the Results Last a Lifetime

• Retirement: what to expect• Knowing your plan options• Special considerations• Take action to control your future

• Retirement: what to expect• Knowing your plan options• Special considerations• Take action to control your future

RE0000.271.1101 April 2004

Retirement: What to ExpectRetirement: What to Expect• Retirement lasts a long time• How much you’ll need• Inflation• Where will the money come from?

• Retirement lasts a long time• How much you’ll need• Inflation• Where will the money come from?

RE0000.271.1101 April 2004

Retirement Lasts a Long TimeRetirement Lasts a Long Time

Source of chart data: National Center for Health Statistics, National Vital Statistics Report, 1999.

Life ExpectancyLife Expectancy

19991999W 85 YrsW 85 YrsM 80 YrsM 80 Yrs

People spend more yearsin retirement today

People spend more yearsin retirement today

66.3 Yrs66.3 Yrs1950s1950s

RE0000.271.1101 April 2004

How Much You’ll NeedHow Much You’ll Need

Retirement FormulaRetirement Formula

80% of Preretirement Salary

Years in Retirement

Amount Needed To Maintain Same LifestyleAmount Needed To Maintain Same Lifestyle

XX

ExampleExample

$800,000$800,000

80% of $50,000 = $40,000

20 Years

80% of $50,000 = $40,000

20 YearsXX

RE0000.271.1101 April 2004

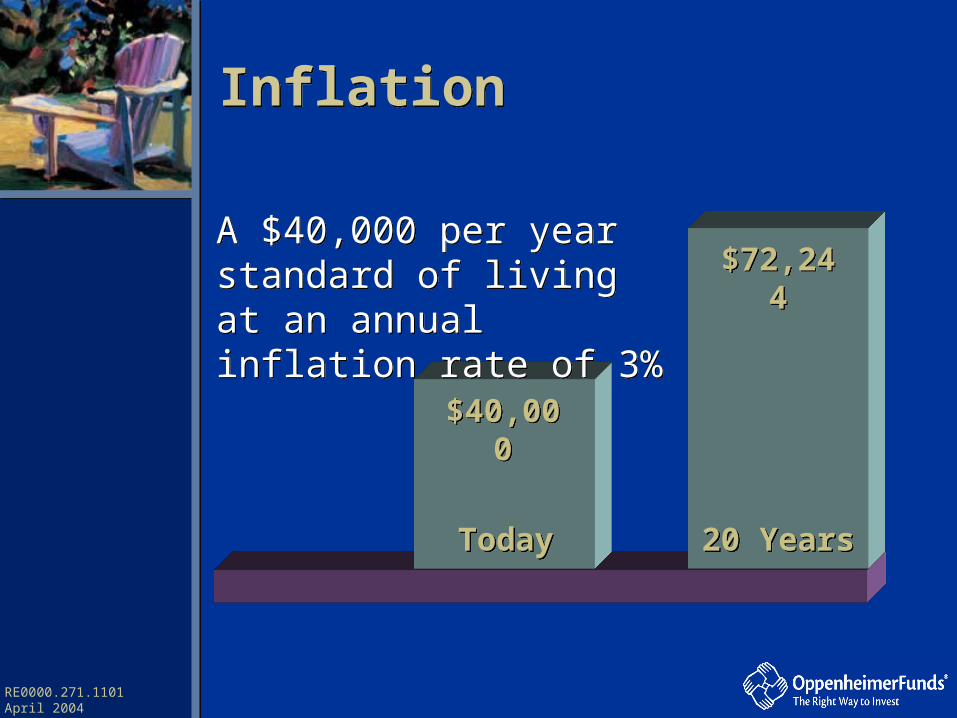

InflationInflation

$72,244$72,244

20 Years20 Years

$40,000$40,000

TodayToday

A $40,000 per year standard of living at an annual inflation rate of 3%

A $40,000 per year standard of living at an annual inflation rate of 3%

RE0000.271.1101 April 2004

Where Will You Get the Money?Where Will You Get the Money?• Pension?• Social Security?• Part-time Work?• Retirement Savings?

• Pension?• Social Security?• Part-time Work?• Retirement Savings?

Defined Contribution Plans

• There are many types of defined contribution plans. Examples include 401(k), 403(b), SEP-IRA, SIMPLE and others. These plans share the following characteristics:– Employer-sponsored, qualified retirement plans– Tax-deferred retirement savings vehicles– Provide an individual account for each participant– The employee or the employer (or both) may contribute to the

employee’s account– Participants are often responsible for investment selections– Benefits based upon contributions plus or minus income,

expenses, gains or losses– Participants have choices when taking money out of plans

Page 5-3

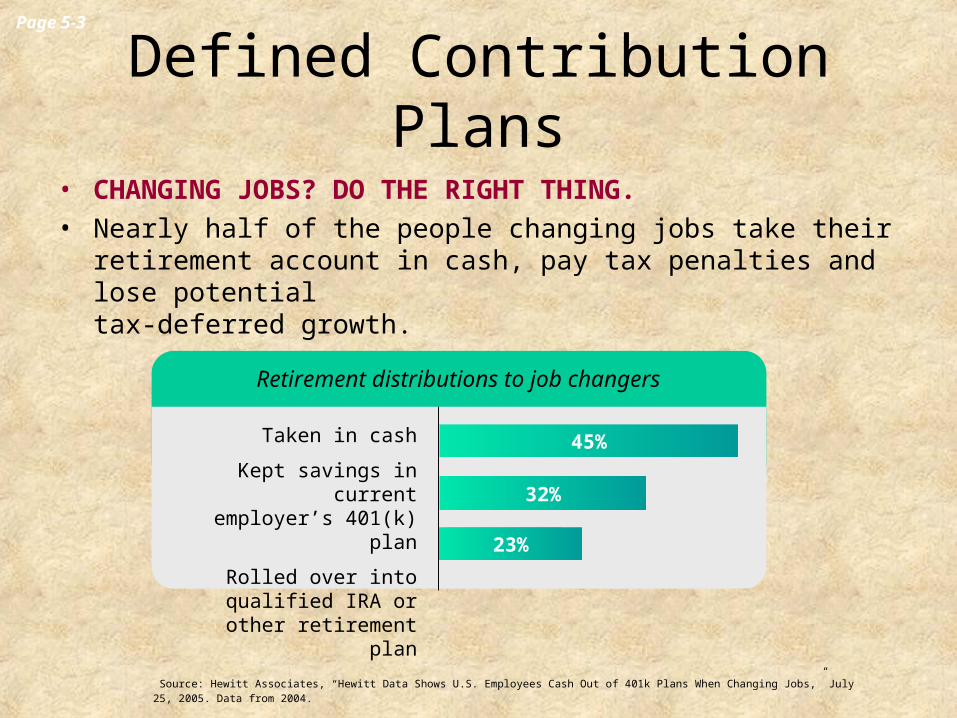

Defined Contribution Plans

• CHANGING JOBS? DO THE RIGHT THING.• Nearly half of the people changing jobs take their retirement account

in cash, pay tax penalties and lose potential tax-deferred growth.

Source: Hewitt Associates, “Hewitt Data Shows U.S. Employees Cash Out of 401k Plans When Changing Jobs,” July 25, 2005. Data from 2004.

Taken in cash

Kept savings in currentemployer’s 401(k) plan

Rolled over into qualified IRA or other retirement plan

Retirement distributions to job changers

32%

45%

23%

Page 5-3

RE0000.271.1101 April 2004

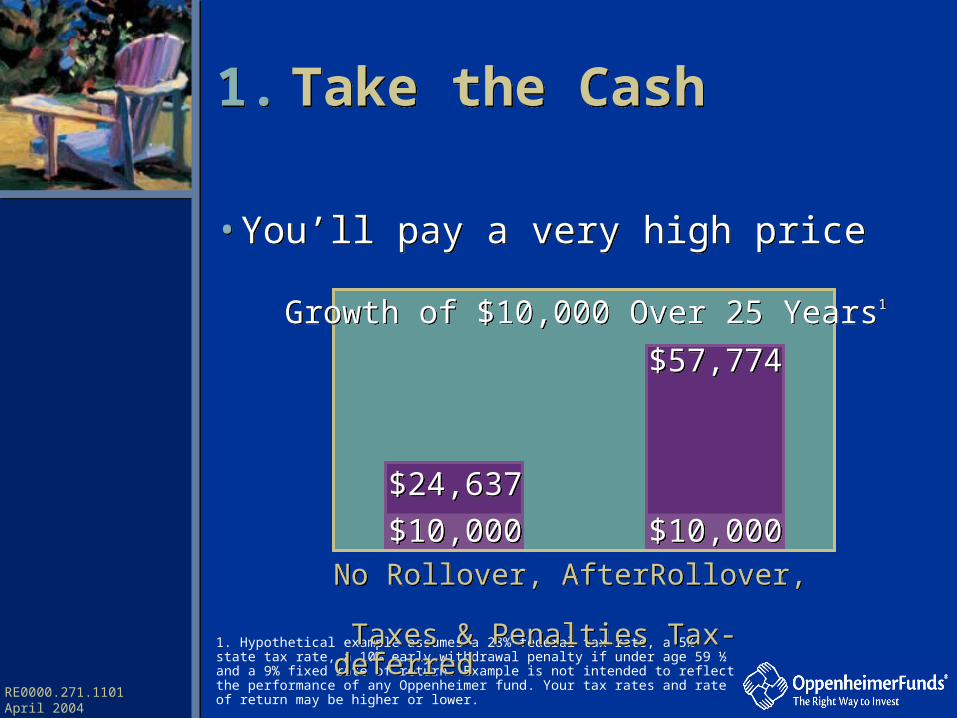

1. Take the Cash1. Take the Cash

Advantages• You get the money right away

Disadvantages• You’ll pay a very high price

Advantages• You get the money right away

Disadvantages• You’ll pay a very high price

RE0000.271.1101 April 2004

1. Take the Cash1. Take the Cash

• You’ll pay a very high price• You’ll pay a very high price

1. Hypothetical example assumes a 28% federal tax rate, a 5% state tax rate and a 10% early withdrawal penalty if under age 59 ½. Your tax rates may be higher or lower.

$10,000 initial distribution

–2,800 federal income tax

–500 state income tax

–1,000 penalty tax

$10,000 initial distribution

–2,800 federal income tax

–500 state income tax

–1,000 penalty tax

$5,700 could be all you see of your original $10,000.1

$5,700 could be all you see of your original $10,000.1

RE0000.271.1101 April 2004

1. Take the Cash1. Take the Cash

• You’ll pay a very high price• You’ll pay a very high price

1. Hypothetical example assumes a 28% federal tax rate, a 5% state tax rate, a 10% early withdrawal penalty if under age 59 ½ and a 9% fixed rate of return. Example is not intended to reflect the performance of any Oppenheimer fund. Your tax rates and rate of return may be higher or lower.

Growth of $10,000 Over 25 Years1Growth of $10,000 Over 25 Years1

No Rollover, After Rollover, Taxes & Penalties Tax-deferredNo Rollover, After Rollover, Taxes & Penalties Tax-deferred

$24,637

$10,000

$24,637

$10,000

$57,774

$10,000

$57,774

$10,000

Additional Tools to Assist in Closing Business

• Detailed financial profile

• Prospective client illustrations

• Agent product packet

FOR PRODUCER USE ONLY. NOT FOR USE WITH THE PUBLIC.