Welded Tube and Pipe Market Tracker OCTG • linepipe •standard pipe • mechanical tubing • HSS Issue 110 April 2013 26 April 2013 www.metalbulletinresearch.com Contents Market prices 2 Americas 3 Asia 6 Europe and Middle East 9 Stainless 12 Little room to decline for welded tubular prices z The rise in US welded tube and pipe prices last month receded in April as scrap and substrate prices slipped through the month. Scrap prices are also expected to decline for May settlements. Both energy and non-energy tubing exhibited price declines as the prevailing fundamentals can not support pricing. HR coil is down $20/ton while plate prices resisted the cuts so far. This is now putting pressure on LSAW mills looking to compete with spiral mills for project work. Prices for commodity- grade welded OCTG have likely reached a near-term floor, but there is still room for declines in pricing for premium grades, constricting the discount for lesser grades. z Chinese steelmakers, including their pipe and tube mills, are experiencing another spring retreat. Production was quick to recover but output has run ahead of orders. Ordinary HR coil prices have fallen by Rmb200/tonne ($32/tonne) but steelmakers have tried to maintain prices for line pipe and casing grades, with apparent success. Popular construction grades of pipe are down only marginally. Surprisingly, 300 series welded stainless steel grades are unchanged on the month, despite the continued fall in nickel prices. z Despite an acute weakness in demand, EU prices have been fairly resistant to declines. The hopes of a seasonal pick-up in sales spurred sellers to show resolve. Sentiment now, however, appears to be turning increasingly bearish, raising the likelihood for prices to take a leg lower next month. Europe in particular with all its woes is far from out the woods. Weak economic conditions, including rising unemployment, will extend at least through the first half of 2013 amid austerity programs. Full resolution of the sovereign debt crisis still looks some way off. z Coil prices undermine US welded price stability: page 3 z Chinese output outpaces orders: page 6 z EU prices maintain footing for now: page 9 Source: Metal Bulletin Research Global historical HSS prices ($/tonne) We expect strengthening prices later in the year as construction activity improves 400 500 600 700 800 900 1,000 1,100 1,200 1,300 1,400 Oct-10 Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Jul-12 Oct-12 Jan-13 Apr-13 Q4 13 US HSS domestic European HSS domestic Turkey HSS fob Chinese HSS fob THIS IS YOUR FREE SAMPLE This is April’s issue and does not contain the latest analysis, forecasts or data. Only subscribers have access to our most valuable and up-to-date information April 2013

Issue 110April 201326 April 2013www.metalbulletinresearch.com

ContentsMarket prices 2Americas 3Asia 6Europe and Middle East 9Stainless 12

Little room to decline for welded tubular prices

The rise in US welded tube and pipe prices last month receded in April as scrap and substrate prices slipped through the month. Scrap prices are also expected to decline for May settlements. Both energy and non-energy tubing exhibited price declines as the prevailing fundamentals can not support pricing. HR coil is down $20/ton while plate prices resisted the cuts so far. This is now putting pressure on LSAW mills looking to compete with spiral mills for project work. Prices for commodity-grade welded OCTG have likely reached a near-term floor, but there is still room for declines in pricing for premium grades, constricting the discount for lesser grades.

Chinese steelmakers, including their pipe and tube mills, are experiencing another spring retreat. Production was quick to recover but output has run ahead of orders. Ordinary HR coil prices have fallen by Rmb200/tonne ($32/tonne) but steelmakers have tried to maintain prices for line pipe and casing grades, with apparent success. Popular construction grades of pipe are down only marginally. Surprisingly, 300 series welded stainless steel grades are unchanged on the month, despite the continued fall in nickel prices.

Despite an acute weakness in demand, EU prices have been fairly resistant to declines. The hopes of a seasonal pick-up in sales spurred sellers to show resolve. Sentiment now, however, appears to be turning increasingly bearish, raising the likelihood for prices to take a leg lower next month. Europe in particular with all its woes is far from out the woods. Weak economic conditions, including rising unemployment, will extend at least through the first half of 2013 amid austerity programs. Full resolution of the sovereign debt crisis still looks some way off.

Coil prices undermine US welded price stability: page 3 Chinese output outpaces orders: page 6 EU prices maintain footing for now: page 9

Source: Metal Bulletin Research

Global historical HSS prices ($/tonne) We expect strengthening prices later in the year as construction activity improves

US HSS domestic European HSS domestic Turkey HSS fob Chinese HSS fob

THIS IS YOUR FREE SAMPLE

This is April’s issue and does not contain

the latest analysis, forecasts or data.

Only subscribers have access to our most

valuable and up-to-date information

April 2013

Subscribe today!

www.metalbulletinstore.com/weldedsteel

(£1,875 / €2,675 / $3,625)* *prices exclude VAT

Subscribe today and:l Get the most recent issue of WeldedTube and Pipe Market Tracker

l Benefit from additional data,downloadable into Excel

l Have regular consultations with theeditor to discuss how their forecastsaffect your business

“Metal Bulletin provides accurate and timely advice on thedirection of the market and I recommend MBR’s WeldedSteel Tube and Pipe very highly to my colleagues”Shehzad Khan, Director (Executive) & Chief Financial Officer, DATA Steel and Pipe Industries PVT. Ltd

April 2013 Welded Steel Tube and Pipe Market Tracker 3

Metal Bulletin Research

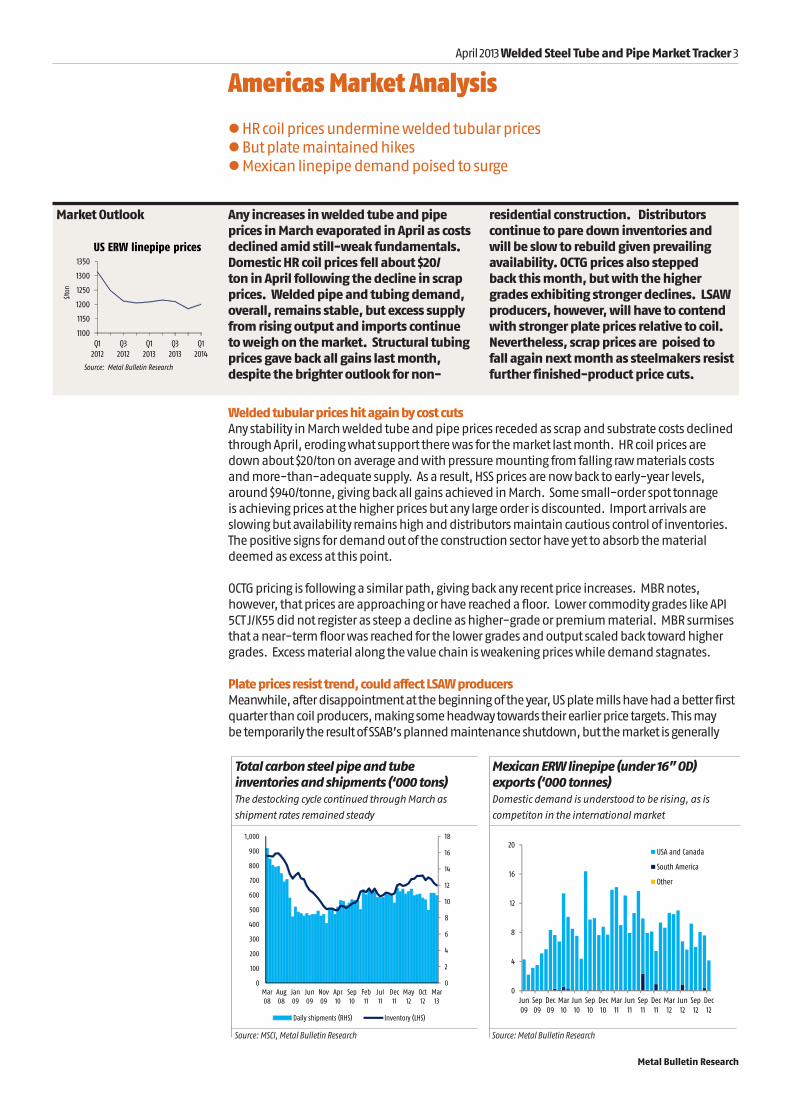

Americas Market Analysis

l HR coil prices undermine welded tubular pricesl But plate maintained hikesl Mexican linepipe demand poised to surge

Market Outlook Any increases in welded tube and pipe prices in March evaporated in April as costs declined amid still-weak fundamentals. Domestic HR coil prices fell about $20/ton in April following the decline in scrap prices. Welded pipe and tubing demand, overall, remains stable, but excess supply from rising output and imports continue to weigh on the market. Structural tubing prices gave back all gains last month, despite the brighter outlook for non-

residential construction. Distributors continue to pare down inventories and will be slow to rebuild given prevailing availability. OCTG prices also stepped back this month, but with the higher grades exhibiting stronger declines. LSAW producers, however, will have to contend with stronger plate prices relative to coil. Nevertheless, scrap prices are poised to fall again next month as steelmakers resist further finished-product price cuts.

Welded tubular prices hit again by cost cutsAny stability in March welded tube and pipe prices receded as scrap and substrate costs declined through April, eroding what support there was for the market last month. HR coil prices are down about $20/ton on average and with pressure mounting from falling raw materials costs and more-than-adequate supply. As a result, HSS prices are now back to early-year levels, around $940/tonne, giving back all gains achieved in March. Some small-order spot tonnage is achieving prices at the higher prices but any large order is discounted. Import arrivals are slowing but availability remains high and distributors maintain cautious control of inventories. The positive signs for demand out of the construction sector have yet to absorb the material deemed as excess at this point.

OCTG pricing is following a similar path, giving back any recent price increases. MBR notes, however, that prices are approaching or have reached a floor. Lower commodity grades like API 5CT J/K55 did not register as steep a decline as higher-grade or premium material. MBR surmises that a near-term floor was reached for the lower grades and output scaled back toward higher grades. Excess material along the value chain is weakening prices while demand stagnates.

Plate prices resist trend, could affect LSAW producersMeanwhile, after disappointment at the beginning of the year, US plate mills have had a better first quarter than coil producers, making some headway towards their earlier price targets. This may be temporarily the result of SSAB’s planned maintenance shutdown, but the market is generally

1100

1150

1200

1250

1300

1350

Q12012

Q32012

Q12013

Q32013

Q12014

$/to

n

US ERW linepipe prices

Source: Metal Bulletin Research

Source: MSCI, Metal Bulletin Research

Total carbon steel pipe and tube inventories and shipments (‘000 tons) The destocking cycle continued through March as

shipment rates remained steady

Source: Metal Bulletin Research

Mexican ERW linepipe (under 16” OD) exports (‘000 tonnes) Domestic demand is understood to be rising, as is

competiton in the international market

0

4

8

12

16

20

Jun09

Sep09

Dec09

Mar10

Jun10

Sep10

Dec10

Mar11

Jun11

Sep11

Dec11

Mar12

Jun12

Sep12

Dec12

USA and Canada

South America

Other

0

2

4

6

8

10

12

14

16

18

0

100

200

300

400

500

600

700

800

900

1,000

Mar08

Aug08

Jan09

Jun09

Nov09

Apr10

Sep10

Feb11

Jul11

Dec11

May12

Oct12

Mar13

Daily shipments (RHS) Inventory (LHS)

4 Welded Steel Tube and Pipe Market Tracker April 2013

Metal Bulletin Research

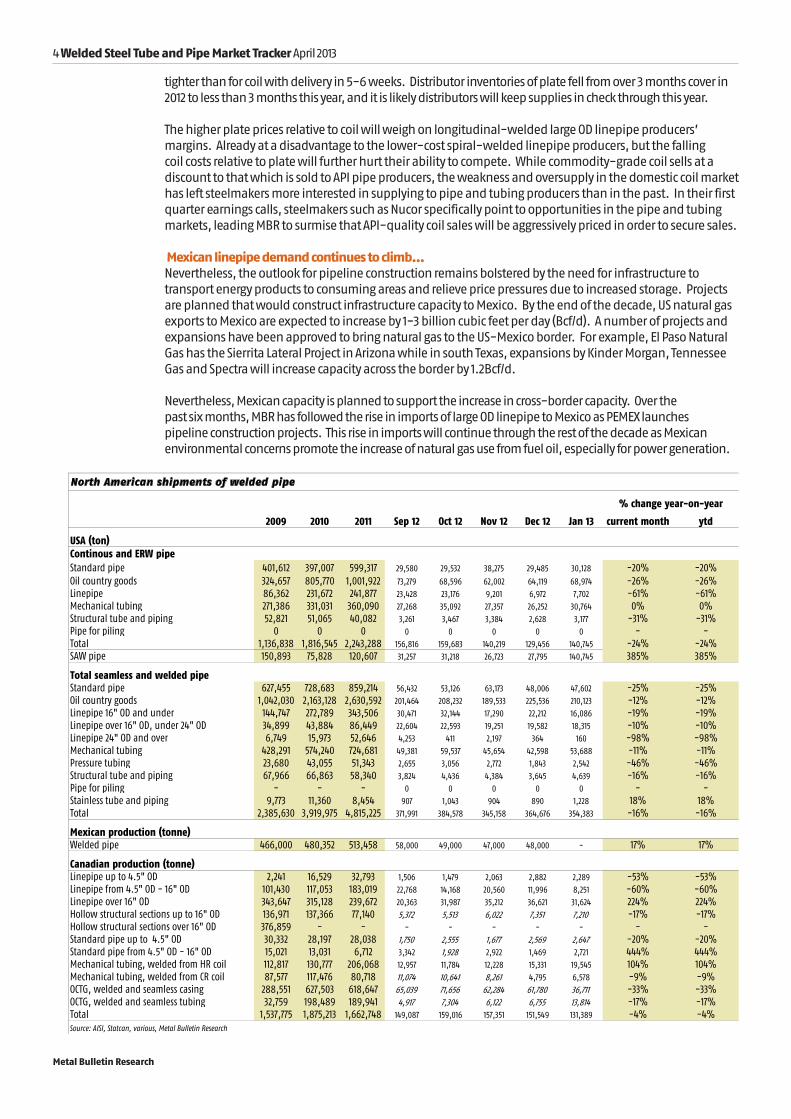

tighter than for coil with delivery in 5-6 weeks. Distributor inventories of plate fell from over 3 months cover in 2012 to less than 3 months this year, and it is likely distributors will keep supplies in check through this year.

The higher plate prices relative to coil will weigh on longitudinal-welded large OD linepipe producers’ margins. Already at a disadvantage to the lower-cost spiral-welded linepipe producers, but the falling coil costs relative to plate will further hurt their ability to compete. While commodity-grade coil sells at a discount to that which is sold to API pipe producers, the weakness and oversupply in the domestic coil market has left steelmakers more interested in supplying to pipe and tubing producers than in the past. In their first quarter earnings calls, steelmakers such as Nucor specifically point to opportunities in the pipe and tubing markets, leading MBR to surmise that API-quality coil sales will be aggressively priced in order to secure sales.

Mexican linepipe demand continues to climb…Nevertheless, the outlook for pipeline construction remains bolstered by the need for infrastructure to transport energy products to consuming areas and relieve price pressures due to increased storage. Projects are planned that would construct infrastructure capacity to Mexico. By the end of the decade, US natural gas exports to Mexico are expected to increase by 1-3 billion cubic feet per day (Bcf/d). A number of projects and expansions have been approved to bring natural gas to the US-Mexico border. For example, El Paso Natural Gas has the Sierrita Lateral Project in Arizona while in south Texas, expansions by Kinder Morgan, Tennessee Gas and Spectra will increase capacity across the border by 1.2Bcf/d.

Nevertheless, Mexican capacity is planned to support the increase in cross-border capacity. Over the past six months, MBR has followed the rise in imports of large OD linepipe to Mexico as PEMEX launches pipeline construction projects. This rise in imports will continue through the rest of the decade as Mexican environmental concerns promote the increase of natural gas use from fuel oil, especially for power generation.

2009 2010 2011 Sep 12 Oct 12 Nov 12 Dec 12 Jan 13 current month ytd

Canadian production (tonne)Linepipe up to 4.5" OD 2,241 16,529 32,793 1,506 1,479 2,063 2,882 2,289 -53% -53%Linepipe from 4.5" OD - 16" OD 101,430 117,053 183,019 22,768 14,168 20,560 11,996 8,251 -60% -60%Linepipe over 16" OD 343,647 315,128 239,672 20,363 31,987 35,212 36,621 31,624 224% 224%Hollow structural sections up to 16" OD 136,971 137,366 77,140 5,372 5,513 6,022 7,351 7,210 -17% -17%Hollow structural sections over 16" OD 376,859 - - - - - - - - -Standard pipe up to 4.5" OD 30,332 28,197 28,038 1,750 2,555 1,677 2,569 2,647 -20% -20%Standard pipe from 4.5" OD - 16" OD 15,021 13,031 6,712 3,342 1,928 2,922 1,469 2,721 444% 444%Mechanical tubing, welded from HR coil 112,817 130,777 206,068 12,957 11,784 12,228 15,331 19,545 104% 104%Mechanical tubing, welded from CR coil 87,577 117,476 80,718 11,074 10,641 8,261 4,795 6,578 -9% -9%OCTG, welded and seamless casing 288,551 627,503 618,647 65,039 71,656 62,284 61,780 36,711 -33% -33%OCTG, welded and seamless tubing 32,759 198,489 189,941 4,917 7,304 6,122 6,755 13,814 -17% -17%Total 1,537,775 1,875,213 1,662,748 149,087 159,016 157,351 151,549 131,389 -4% -4%Source: AISI, Statcan, various, Metal Bulletin Research

% change year-on-year

North American shipments of welded pipe

April 2013 Welded Steel Tube and Pipe Market Tracker 5

Metal Bulletin Research

While development of Mexican shale gas deposits is likely decades away, access to inexpensive natural gas from the USA and Canada will be available once the infrastructure is expanded or put in place. The Mexican government’s pipeline plans amount to $8bn in investments and include two large pipelines as well as smaller projects to connect the pipelines to consumers, stretching as far as 2,000 miles. Mexican linepipe capacity alone is not enough to support these projects, so imports will be common for the medium to long term.

…but the downward trend in industrial output will affect tubing demand and exportsNevertheless, Mexican demand for non-energy tubing in manufacturing and construction is expected to slip. Mexican economic activity retreated in the first quarter of 2013. Exports, industrial production, and construction declined at the start of the year, following slower growth in late 2012. Total Mexican industrial production fell 1.2% year-over-year in February, after posting a slight increase the previous month, as most of the major contributing sectors registered declines. The steel-intensive machinery and equipment manufacturing component fell 7.4% month-on-month in February and 1.5% year-over-year. Transportation equipment is recovering from a dismal December measure, but remained 0.2% off February 2012 results.

Vehicle export growth fell into negative territory early this year, signaling that the important export sector is weakening, owing to muted demand growth from the major trading partners. Meanwhile, internal demand is not providing relief either as construction growth also declined from year-ago levels.

Nevertheless, Mexican crude steel output climbed 11% February from year-ago levels, while finished steel production was up 8%. According to available trade data, Mexican welded tube and pipe exports fell 4.5% year-over-year between 2011 and 2012, with fourth-quarter 2012 exports declining 10.5% year-over-year from the fourth quarter of 2011. With both domestic and export consumption in retreat, it is likely that producers will look to secure sales with steep discounts or else cut output.

2010 2011 Aug 12 Sep 12 Oct 12 Nov 12 Dec 12 current month ytdUSA (ton)Linepipe over 16" OD Shipments 59,857 139,095 21,763 26,857 23,004 21,448 19,946 45% 127%

*also includes seamless linepipe, OCTG tubing and casing

% change year-to-year

North American trade balance of welded pipe

6 Welded Steel Tube and Pipe Market Tracker April 2013

Metal Bulletin Research

Asia Market Analysis

l Slower growth keeps Chinese prices weakl Trade complaints against Asian exports to the US increase… l … but not all allegations of dumping stand up to examination

China – seasonal recovery starts late and ends earlyIt has been another disappointing spring for Chinese steelmakers, including their pipe and tube mills. Production was quick to recover but output has run ahead of orders. Ordinary HR coil prices have fallen by Rmb200/tonne ($32/tonne) but steelmakers have tried to maintain prices for line pipe and casing grades, with apparent success. Popular construction grades of pipe, such as Q235 (A53B) are only slightly cheaper than in March; pipe diameter 4” (114mm) wall 0.15” (3.75mm) was selling for Rmb4,010/tonne ($647/tonne) only Rmb10/tonne lower, less than $2/tonne.

Surprisingly, 300 series welded stainless steel grades are unchanged on the month, despite the continued fall in nickel prices. Industrial grade welded pipes continue to track the prices of equivalent seamless pipe; n Wenzhou and Wuxi welded prices for 3mm wall pipe are Rmb18,500-21,500/tonne ($2,986-3,712/tonne) compared with Rmb17,800-21,400 ($2,873-3,454/tonne) for seamless pipe in the same locations. Chinese exporters of stainless steel welded pipe have run into opposition in Turkey. A year ago two Turkish producers called for an investigation into imports from both China and Taiwan. In a final judgment AD levies of up to 25.27% have been imposed on exports from China and up to 14.65% on Taiwanese imports.

Limited price gains for API pipesAPI grades have made some gains. After remaining unchanged following sharp falls in February, tubing pipe prices have been marked up by Rmb150/tonne ($24/tonne) across the board – but

Market Outlook The Chinese government may maintain its balancing act, controlling inflation but keeping the economy growing at a rates of at least for 7.5% GDP growth, regarded as near the minimum needed to avoid social unrest. Unfortunately tube and pipe mills have still to adjust to this slower rate of growth, and possibly, lower steel intensity; stocks are high, output is high and new capacity is being laid down. Prices in China will remain fragile, and ,mills will still rely on export markets to

clear stocks. Trade restraints making this progressively more difficult for Chinese mills, in Asian as well as North American markets. Exports from other Asian producers, are also under scrutiny; most have excess capacity yet are expanding further.

Source: National Bureau

Chinese PMI ManufacturingThe manufacturing sector is barely in growth territory

Sources: Metal Bulleting Research

Japanese SAW linepipe exports (‘000 tonnes, y/y change), A weaker yen is expected to help turn

around the declining trend in export tonnage this year

40

45

50

55

60

Mar09

Sep09

Mar10

Sep10

Mar11

Sep11

Mar12

Sep12

Mar13

-100,000

-75,000

-50,000

-25,000

0

25,000

50,000

75,000

100,000

Dec08

May09

Oct09

Mar10

Aug10

Jan11

Jun11

Nov11

Apr12

Sep12

Feb13

600

650

700

750

Q12012

Q32012

Q12013

Q32013

Q12014

$/to

n

Asian HSS, fob prices

Source: Metal Bulletin Research

April 2013 Welded Steel Tube and Pipe Market Tracker 7

Metal Bulletin Research

this falls far short of making good the sharp falls in February, which amounted to around Rmb400/tonne ($65/tonne).

Price movements in API casing pipes have been mixed. Prices of large sizes (13-3/8”) remain at Rmb6,700/tonne ($1,082/tonne); smaller sizes have made gains of Rmb50-150/tonne ($8-24/tonne), but these rises still leave some prices as much as Rmb1,000/tonne ($162/tonne) below their January level. There have been no corresponding rises in export prices. ERW API line pipe prices remain in the range $720-850/tonne.

Capacity in Asia continues to rise Other Asian producers in addition to China have excess welded pipe capacity, and are obliged to look abroad for sales. Nevertheless more capacity continues to be added. In October last year Japan’s recently formed Nippon Steel & Sumikin Metal Products Company (NSSMC) set up a joint venture, Nippon Steel & Sumikin Metal Products Vietnam, with Bacviet Steel (Vietnam) and other Japanese companies. Later this year or early in 2014 it will begin

8 Welded Steel Tube and Pipe Market Tracker April 2013

Metal Bulletin Research

producing structural pipe for construction and civil engineering, for both domestic use and export. Capacity details have not been published.

Asian mills’ dependence on exports and consciousness that the US market is a prime target for their sales leads US producers to make frequent accusations of dumping against Asian pipe suppliers. The quasi-judicious process for examining allegations of unfair trading operated by the Commerce Department’s International Trade Administration (ITA) shows some to be mistaken.

For example, the ITA has at last issued interim findings from a survey of imports of circular welded pipe from Turkey received from January to December 2011. The extent of under-pricing – on the ITA’s definition – was disappearingly small, ranging from 0.24% to 0.3%. Such de minimis under pricing rules out any AD or countervailing levy. In another survey the ITA checked whether two of Thailand’s leading pipe mills, Saha Thai Steel Pipe and Pacific Pipe, traded unfairly with the USA during the period March 2011 to February 2012. The complaint fell because neither company made any shipments to the USA during the period.

For some time South Korean pipe exporters have been among the main suppliers to the USA and were unquestionably the leading overseas source in January, shipping 97,785 tonnes of OCTG and 79,429 tonnes of line pipe. US producers have been threatening the Koreans with a trade complaint for months. Korean producers deny under-pricing; on average their prices in January were $967/tonne, compared with goods from Taiwan, at $850/tonne and Vietnam at $842/tonne. No complaint has emerged so far, perhaps because there is a good chance that Korean pricing will be found entirely legitimate.

Anti-dumping dispute; defining country of originWhere AD levies have already been imposed on Asian exporters, US mills are also on the look out for attempts to divert exports via other countries. A Texas-based importer currently faces a legal challenge mounted by US Steel Corporation and Maverick Tube Corporation over pipes originating in China but brought in from Indonesia after heat treatment and processing to final specifications. It argues that the work in Indonesia amounts to a substantial transformation of the product, such that the products can be legitimately described as of Indonesian origin. As such this means it should avoid the AD levy that has normally been due on Chinese pipes since 2010.

US Steel and Maverick Tube claim that heat treatment and the other related processes are not as substantial as clear and well recognised manufacturing transformations such as the rolling down of imported slab, or the re-rolling of imported POSCO HR coil by US-Posco Industries (UPI). They even claim that the Indonesian processing arrangement was set up specifically to circumvent the AD order. The importers point out that the AD orders date back two to three years, the Indonesian arrangement was set up even earlier and this is the first time they have been challenged.

% change2010 2011 May 12 Jun 12 Jul 12 Aug 12 Sep 12 Oct 12 Nov 12 Dec 12 Jan 13 year to date

April 2013 Welded Steel Tube and Pipe Market Tracker 9

Metal Bulletin Research

Europe, Middle East and Africa

l No immediate let-up for Europe in sightl Prices set to take a leg lower following disappointing demandl Softer substrate costs ease pressure on producers

Europe is gripped by an imminent sense of price fatigueDespite the market weakness in Europe, monthly prices in Italy were mainly stable, although some declines of around 1.5% month-on-month were seen. Domestic prices for Italian pipes (ex-works, ex-vat) made from HR coil stood at around €580/tonne, while material coming from Turkey into Italy was noted to be competitively priced at €560/tonne CFR.

The prospects for discounts are now beginning to build in domestic European markets as sellers grow weary of a lack of demand. Moreover, buyers are likely to be reticent without discounts, having noted softer substrate costs. Prices in Eastern European held on despite weaker market conditions. In both eastern Europe, domestic ERW pipes made from HR coil stood broadly stable at around €550-€600/tonne, depending on location.

According to a recent report from the World Steel Association, EU steel demand is expected to contract by 0.5% in 2013 to 139.5m tonnes. However demand is likely to rebound, increasing by 3.3% to 144.1m tonnes in 2014. Furthermore exports are expected to stagnate at 2012 levels this year as international competition increases and the stronger Euro restricts future growth potential on key foreign markets. In contrast, the report expects GDP growth in the EU will remain stable at 1.5% in 2013 before expanding in 2014.

Market Outlook Despite an acute weakness in demand, prices have been fairly resistant to declines. The hopes of a seasonal pick-up in sales spurred sellers to show resolve. However sentiment now appears to be turning increasingly bearish, raising the likelihood for prices to take a leg lower next month. Europe in particular with all its woes is far from out the woods. Weak economic conditions, including rising unemployment, will extend at least through the first half of 2013 amid austerity. Full resolution of the sovereign debt crisis still looks some way off, as highlighted by recent developments in

Cyprus and the lingering political stalemate in Italy.

Elsewhere in the Middle East we suspect producers are finding the export market challenging. As such, material in their local markets is expected to build. In the CIS, their competitive stance has ensured some price stability.

Nevertheless we are not confident in the region as a whole to stave off growing pessimism in the short-term, as the miss-match between supply and demand becomes more evident.

Welded substrate costsThe recent declines in substrate prices reduces the pressure

on producer margins

0

10

20

30

40

50

60

70

Jan'12

Mar'12

May'12

Jul'12

Sep'12

Nov'12

Jan'13

Source: Metal Bulletin Research

500

550

600

650

700

750

Nov11

Jan12

Mar12

May12

Jul12

Sep12

Nov12

Jan13

Mar13

CIS export hot rolled coil $/tonne fob (BlackSea)Turkey domestic hot rolled coil $/tonne exw

600

650

700

750

800

Q12012

Q32012

Q12013

Q32013

Q12014

$/to

n

Turkish HSS, fob prices

Source: Metal Bulletin Research

10 Welded Steel Tube and Pipe Market Tracker April 2013

Metal Bulletin Research

Chiming with the overall sense of a lack-lustre European market, US tube and pipe maker Tenaris expects demand from its European customers to remain tepid. The company note that competition for standard products has increased as producers in Russia have stepped up production and exports. Aggressive sales by Ukrainian and Russian producers ensured prices held their trading ranges.

Over the past month prices of European HR coil and CR coil prices have fallen to €470-500/tonne and €540-570 per tonne CFR, respectively, while CIS-origin HR coil import offer prices into Europe now stand at $555 – 580/tonne CFR. It is widely recognized that overcapacity issues and poor demand continue to dog the sector. Alarmingly first quarter new passenger vehicle registrations in the eurozone of 2.1 million showed a decline of 14% compared with the same period a year ago and the lowest volume for a first quarter in over 20 years. The need therefore to stimulate lending has grown more urgent as the eurozone economy struggles to emerge from recession. Surveys out this week for Germany, Italy, Spain and France will likely show further declines in business and consumer confidence, while unemployment is predicted to jump in Spain and France. The political situation in Italy is still unresolved, and while Cyprus’ banking crisis was resolved with a bailout package, Slovenia faces a possible financial crunch of its own. As such pressure on the region is likely to mount in May.

Export data released by the Turkish Statistical Institute showed that welded tube products fell back by 48.6% month-on-month in January to 31.9k tonnes and by 31.2% compared with the same period last year. Although, volumes were noted too decline from the highest ever monthly level in 6 years, from December. In late-2012

West European trade and shipment of welded pipe (tonne)% change

April 2013 Welded Steel Tube and Pipe Market Tracker 11

Metal Bulletin Research

Turkey appeared to show a greater preference towards markets outside of Europe, owing to scant demand. It could be argued that such a destination shift was successful in driving exports higher until January, by which time demand to most, if not all destinations was flagging.

Early indications suggest the seasonal pick-up in the Middle East is likely to disappoint In the Middle East Iranian prices have been experiencing increased volatility. The unstable currency has worked to top slice export prices by as much as 2% in dollar terms. Domestically, consumption is lack-lustre, although a few traders are excited by the notion of a seasonal pick-up. Moreover, Chinese exporters are showing greater conviction to the Iranian market, having seen their prices rise by around 2% month-on-month. We conclude that despite some optimism among sellers, buyers are likely to move cautiously in the near-term.

Elsewhere, consumers in the UAE are comforted by sufficient inventory levels, in effect pressing domestic suppliers to reduce prices. As a result, quotations have slipped lower, falling 1.5 - 2% month-on-month. Unlike the situation in Iran, Chinese exporters operating in the UAE and Saudi Arabia have been unable to push for higher prices.

Monthly Turkish steel pipe exports (k tonnes): Turkish exports slip back 48.6% month-on-month in January to 31.9k tonnes

Central, East European and CIS trade and shipment of welded pipe (tonne)% change

12 Welded Steel Tube and Pipe Market Tracker April 2013

Metal Bulletin Research

Alloy surcharges on nickel-containing stainless steel fell in April, by an average of about 3% in Europe and 5% in the USA on the back of falling nickel costs through March.

Despite a brief recovery, nickel prices have continued to fall sharply over the last few weeks and are now down by about 10%, to just above $15,000/tonne, since the end of March. As such, alloy surcharges on the most common grades of stainless steel will drop slightly for May deliveries. A larger fall in these surcharges was only prevented by the rise in the second quarter ferrochrome contract price, which rose by 13% to $1.27/lb.

Those buying stainless steel substrate may find now a good time to buy, however. Although there is a degree of risk in trying to call the bottom of a market, Metal Bulletin Research notes that in each occasion in recent years that the nickel price has dipped below $16,000/tonne (in both August and November last year, as well as July 2009) it has quickly rebounded. It is thought that a floor in nickel prices of about $15,000/tonne exists nowadays due to the fact that marginal producers (generally nickel pig iron producers in China) operate at a cost-level just above this and so they suspend production, thereby reducing supply, when prices fall much below $16,000/tonne. Hence, with an expected uptick in nickel prices over the coming couple of months, and the recent rise in ferrochrome contract prices, we would expect to see surcharges move upward again in the coming months.

Welded Steel Tube an

d Pipe Market Tracker / Issue 110 / 26 April 2013

12 Welded Steel Tube and Pipe Market Tracker April 2013

Stainless steel

l Stainless prices generally stable despite falling nickel costs...l ...due to rising ferrochrome costsl Expected uptick in nickel prices suggests higher prices in coming months

Published monthly by Metal Bulletin LtdISSN 1749-3765Produced by: Kim Leppold, Contributors: Kimberly Leppold, Brad MacAulay and Robert Cartman

Metal Bulletin Research Nestor House, Playhouse Yard, London EC4V 5EXTel: +44 20 7827 6488 Fax: +44 20 7827 6430

l Seamless Steel Tube and Pipe Market Trackerl Steel Raw Materials: Weekly Market Trackerl Steel: Weekly Market Trackerl Coated Steels Market Trackerl Stainless Steels Market Trackerl Ferro-alloys Market Tracker

To receive a free sample of any of the above reports, email your details to: [email protected]

DISCLAIMER - IMPORTANT PLEASE READ CAREFULLY

This Disclaimer is in addition to our Terms and Conditions as available on our website and shall not supersede or otherwise affect these Terms and Conditions.

Prices and other information contained in this publication have been obtained by us from various sources believed to be reliable. This information has not been independently verified by us. Those prices and price indices that are evaluated or calculated by us represent an approximate evaluation of current levels based upon dealings (if any) that may have been disclosed prior to publication to us. Such prices are collated through regular contact with producers, traders, dealers, brokers and purchasers although not all market segments may be contacted prior to the evaluation, calculation, or publication of any specific price or index. Actual transaction prices will reflect quantities, grades and qualities, credit terms, and many other parameters. The prices are in no sense comparable to the quoted prices of commodities in which a formal futures market exists.

Evaluations or calculations of prices and price indices by us are based upon certain market assumptions and evaluation methodologies, and may not

conform to prices or information available from third parties. There may be errors or defects in such assumptions or methodologies that cause resultant evaluations to be inappropriate for use. Your use or reliance on any prices or other information published by us is at your sole risk. Neither we nor any of our providers of information make any representations or warranties, express or implied as to the accuracy, completeness or reliability of any advice, opinion, statement or other information forming any part of the published information or its fitness or suitability for a particular purpose or use. Neither we, nor any of our officers, employees or representatives shall be liable to any person for any losses or damages incurred, suffered or arising as a result of use or reliance on the prices or other information contained in this publication, howsoever arising, including but not limited to any direct, indirect, consequential, punitive, incidental, special or similar damage, losses or expenses.

We are not an investment advisor, a financial advisor or a securities broker. The information published has been prepared solely for informational and educational purposes and is not intended for trading purposes or to address your particular requirements. The information provided is not an offer to buy or sell or a solicitation of an offer to buy or sell any security,

commodity, financial product, instrument or other investment or to participate in any particular trading strategy. Such information is intended to be available for your general information and is not intended to be relied upon by users in making (or refraining from making) any specific investment or other decisions. Your investment actions should be solely based upon your own decisions and research and appropriate independent advice should be obtained from a suitably qualified independent advisor before making any such decision.

Net imports of welded stainless steel tube and pipe (tonnes)

FIVE EASY WAYS TO ORDER+44 (0) 20 7779 8000 +44 (0) 20 7779 8090 [email protected]

www.metalbulletinstore.com Metal Bulletin Research, Nestor House, Playhouse Yard, London, EC4V 5EX UK

You are also able to request a brochure, sample extracts and detailed table of contents for more information Quote promo code 5079 when ordering

New andUpdated

The Five Year Strategic Outlook for the

Global Large-diameterLinepipe Market

l How has the global large diameter (over 16”OD) linepipe market been affected by therecession? Has there been any structuralchanges to the industry due to the downturn?

l How will the market emerge from the recession?When will demand return?

l Where are prices for steel raw material andsubstrate prices (plate and HR coil) headedover the next five years?

l Where will most new demand be located? Will trade flows change? How will yourcompetitor’s strategy impact your futurebusiness plans, if at all?

Welded Steel Tube and Pipe Market Tracker (Annual Subscription)

FIVE EASY WAYS TO ORDERTel: +44 (0) 20 7779 8000Fax: +44 (0) 20 7779 8090E-mail: [email protected]: www.metalbulletinstore.com/weldedsteelMail: Metal Bulletin Research, PO Box 18083 EC4V 5JS, UK

Family Name

Mr/Miss/Mrs/Ms/Dr

First/Given Name

E-mail

Company Name

Job Title

Address

Post/Zip Code

Country

Tel +( )

Use of your information The information you provide on this form will be used by Euromoney Institutional Investor PLC and its groupcompanies (“we” or “us”) to process your order and/or deliver relevant products/services and content. We may also monitor your use ofour website(s), including information you post and actions you take, to improve our services to you and track compliance with our termsof use. Except to the extent you indicate your objection below, we may also use your data (including data obtained from monitoring) (a)to keep you informed of our products and services; (b) occasionally to allow companies outside our group to contact you with details oftheir products/services; or (c) for our journalists to contact you for research purposes. As an international group, we may transfer your dataon a global basis for the purposes indicated above, including to countries which may not provide the same level of protection to personaldata as within the European Union. By submitting your details, you will be indicating your consent to the use of your data as identifiedabove. Further information on our use of your personal data is set out in our privacy policy, which is available at www.euromoneyplc.comor can be provided to you separately upon request. Marketing choices If you object to contact as identified above by telephone q, faxq, or email q, or post q, please tick the relevant box. If you do not want us to share your information with our journalists q, or othercompanies q please tick the relevant box.

YOUR COMPANY TYPERaw Material Supply (0003)Metal/Steel Production/ Processing(0027)Fabrication/Manufacturing (0055)Distribution (0095)Services/Products for the Industry(0111)End-User Sector (0167)

Ferro Alloys (13000)Scrap & Secondary Metals(14000)Steelmaking Raw Materials(12231)Iron Ore (12232)

DATA PROTECTION NOTICE

PROMO CODE

Study published September 2013

I wish to pay by the following method (please tick appropriate box):

CREDIT CARD – I wish to pay by credit card.Please call the Metal Bulletin Research hotline on +44 (0) 20 7779 8000.For your own safety please do not fax or email credit card details.

INVOICE – Please invoice me for US$/£/€ ______________I understand my access will not begin until the invoice has been paid.

CHEQUE – I enclose a cheque for US$/£/€ _____________made payable to Metal Bulletin.

BANK TRANSFER – A bank transfer has beenmade payable to Metal Bulletin for US$/£/€ _____________

Please provide a copy of the transfer document with your order quoting code MWS