23

Wells Fargo & CompanyAnnual Report

Wells Fargo &CompanyAnnual Report

a

Contents Highlights 2

Stockholders Letter 3

Financial Review 6

Summary of Operations 12

Financial Statements 13

Directors 36

Organization 37

Left One of Wells Fargo'slarge banking offices Indowntown San Francisco

InsIde Back CoverPlymouth Office in theMother Lode Country.

Assets $7,804,729.801 $6.225,565,510 $1,579,164,291

Deposits 6,382,964,091 5,254,183,131 1,128,780,960

Loans 4,472,784,121 3,694,511,914 778,272,207

Investments 1,335,670,626 1,052,881,470 282,789,156

Total Capital Accounts 415,337.217 403,455,150 11,882,067

Book Value Per Share (Excluding Capital Notes) $36.69 $35.44 $1.25

$ 34,351.952 $ 32,583.807 $ 1.768.145

(4,967,002) 147.587 (5,114589)

$ 29,384,950 $ 32,731,394 $ (3,346.444)

$3.71 $3.54 $ .17

$3.17 $3.55 $ (.38)

$14,835,989 $ 14,747,582 $ 88,407

$1.60 $1.60

2

Highlight

FOR THE YEAR

Income Before Security Gains or Losses

Security Gains (Losses) Net of Tax

Net Income

Income Before Security Gains or Losses Per Share*

Net Income Per Share*

Dividends Declared

Year-End Annual Dividend Rate

·Based on average number of shares outstandingof 9,271,581 for 1971 and 9.210.740 for 1970.

AT THE YEAR END

1971 1870

To Our The past year was an active one for Wells Fargo & Company durStockholders ing a period of fitful economic recovery in the State and Nation.

As 1972 opens, the recovery appears to be strengthening.During 1971, negotiations with World Airways, Inc., were con

cluded for purchase of First Western Bank and Trust Company.First Western, 99.5 per cent-owned by World Airways, is a LosAngeles-based institution with total deposits"of $995 million.

Terms of the merger agreement called for Wells Fargo & Company to pay stockholders of First Western $45 million in cash and$50 million face value 71/2 per cent intermediate-term debentures. The total of $95 million is equivalent to $69.44 per share onthe 1,368,080 outstanding shares of First Western.

On December 20, the Comptroller of the Currency approvedthe mergel' proposal, which would add 54 branches to WellsFargo's Southern California operations, stating that the mergerwould have a favorable competitive effect on banking throughout the State. However, on January 17, 1972, the Justice Departmentfiled suit to prohibit the proposed merger. As of this date,we are in the process of preparing our reply to the Justice Department's complaint.

During 1971, a number of oth8l' impol1ant steps were taken tobroaden and improve Wells Fargo's operations. As a result, earnings for the year (stated as income before security transactions)totaled $34,351,952 or $3.71 per share, compared to $32,583,807or $3.54 per share in 1970.

This growth, despite ten changes in the prime rate during 1971,was made possible by intensive efforts to hold down controllableexpenses and staff expansion, a temporary drop in the interestrate on passbook savings, and an aggressive lending policy.

The slow pace of economic recovery in 1970 had promptedthe Federal Reserve Boal"d to ease monetary policy. Subsequentstrong deposit growth early in 1971 and a plentiful money supplyassured Wells Fargo of adequate funds to fill the needs of customers. Our loan growth during most of the year exceeded thenational pattern of the banking industry.

By late summer, it became apparent that consumers and businessmen were still concerned about the economic recovery andthe continued high pace of inflation. Consumer and businessspending did not live up to expectations, and nationally loandemand by both sectors was weak.

On August 15, President Nixon imposed a 90-day wage-pricefreeze, Phase I of a New Economic Program designed to bringinflation under control and to provide more jobs. Inilially, theseand other decisive steps helped to bolster confidence in the economy. In September, the national rate of consumer savings droppedbelow 8 pel" cent of disposable income for the first time in manymonths and consumer spending-particularly for autos-beganmoving upward. Wells Fargo Bank's consumer loan volume beganto expand more strongly, as well.

3

Wells Fargo & Company, the parent company, continued itsexpansion during the year. Wells Fargo Mortgage Investors, acompany-sponsored, publicly-owned real estate investment trust,showed increasing earnings throughout 1971; as a consequence,Wells Fargo Realty Advisors, our subsidiary which manages theportfolio of the trust, increased its contribution to Wells Fargoprofits. Plans were finalized for a subsidiary to' lease heavy equipment, and Wells Fargo Leasing Cmporation began operations inDecember. The new subsidiary will further diversify the alreadybroad activities of the holding company.

Two new directors were elected in 1971. They are: Mr. MalcolmMacNaughton, president and chief executive officer of Castle &Cooke, Inc., Honolulu, and Mr. Atherton Macondray Phleger, SanFrancisco attorney.

During 1971, Wells Fargo continued its affirmative action programs aimed at improving the social and environmental settingin which we operate. These programs will go forward in 1972under the direction of J. O. Elmer, executive vice president, Publicand Governmental Affairs, who will give strong emphasis to OUI'

efforts in1he sphere of corporate responsibility.

We thank our Board of Directors for their counsel during 1971.The achievements of the year were due in large measure to theoutstanding efforts of our staff, particularly in restraining expensesand personnel increases. We are indeed grateful for the fine support of each member of the Wells Fal'go family.

4

As questions about the nature and complexity of Phase II arose,however, there was another period of hesitation in the economy.In October, President Nixon outlined Phase II of the New Economic Program and called for continued restraint in wage andprice increases, with commissions established to rule on permissible rises. A Committee on Interest and Dividends was also set upto review interest rate and dividend increases. In our view, thiscommittee will not find it necessary to exercise controls on lendinginterest rates, which are set by money market influences.

After Phase II was set in motion, business confidence in theU. S. economy seemed to return. As the year drew to a close,business sales and appropriations for capital investment beganto move upward. The banking industry looks forward to expansionin business loans in 1972.

Efforts by the Nixon Administration to bring inflation under control and to improve U. S. economic activity had far-reaching ramifications. On December 19, it was announced that the price ofgold would be raised from $35 to $38 per ounce, effectively devaluing the dollar. Other governments subsequently revalued theircurrencies to provide a more favorable structure for internationalparities. These moves will lower the price of U. S. goods in international markets, strengthening the position of American exportingfirms. Banks active in foreign trade financing, such as Wells Fargo,should benefit from increased export trade in 1972.

California underwent even more severe recession than did theNation in 1970 and 1971, which called for extra efforts on the partof our Bank to expand our lending business in the State. However,by the end of 1971, declines in the State's important aerospaceelectronics companies were slowing and some firms in thisindustry were adding jobs for the first time since late 1967.

All of these factors, together with the demonstrated determination of the Nixon Administration to curb inflation and improve thestrength of the dollar at home and abroad, indicate that WellsFargo Bank will have excellent opportunities for loan and depositgrowth in 1972. We are studying possible new types of computation for a base or prime rate, which would be tied to other moneymarket rates. Over the coming year, we expect lending rates toremain lower than they were in the 1969-70 period.

Our international banking capabilities were expanded in 1971:a branch was opened in Tokyo, our first in the Far East; and representative offices were opened in Sao Paulo, Brazil, and Caracas,Venezuela. Wells Fargo lnteramerican Bank, a subsidiary for international business with emphasis on Latin America, was openedin Miami during 1971, and Wells Fargo Bank International acquireda minority interest in Broadbank Corporation Ltd. in Auckland,New Zealand. We were the first U. S. bank to enter that country'smarket. We also received approval for establishment of a merchant bank in London, to be known as Wells Fargo Ltd., and fora branch in Nassau, Bahamas.

January 20, 1972

Ernest C. Arbuckle,Chairman of the Board

~~Richacd P co~President

5

Earnings (income before security transactions) for the year were$34,351,952, equal to $3.71 per share, compared to $32,583,807or $3.54 per share in 1970. The high interest rates of 1970 softened substantially in 1971 making it difficult to improve earningsover the previous year. However, an earnings gain was achievedthrough an increase in loan and investment volume, a lower costof borrowed funds, lower savings interest rates and a successful program in holding down operating costs and staff expansion.

The 1970 prime mte range of 7 to 8% per cent was in contrastto a rate of 5% to 6 per cent through most of 1971. The averageloan yield dropped to 7.22 per cent from 8.07 per cent in 1970.For a four-month period-when the prime rate had moved to a lowof 5% per cent-passbook savings interest also dropped from4% pel" cent to 4 per cent, thus reducing interest expense by $2.7million. An aggressive staff and expense control program reducedexpenses some $6 million over those originally planned for 1971and was a significant contributor to our improved earnings.

Commencing in 1971, Wells Fargo's earnings include its shareof the annual net income of companies in which it has equityinvestments exceeding 20 per cent of the voting common stock.This action conforms with a recent Opinion of the AccountingPrinciples Board of the Amel'ican Institute of Certified PublicAccountants. The investments for which our share of income orloss was recorded were Western American Bank (Europe) Ltd.(24% owned), Digitek Corporation (43% owned) and Wells FargoInvestment Company (45% owned). Net addition to income as aI'esult of this new procedure was nominal.

Loss on sale of securities of $5 million (after taxes) resultedfrom sales of lowel' yielding, longer-term bonds which werereplaced with short-term maturities. The move provides futureflexibility and opportunities for reinvestment at higher yieldingrates. Net income after these security tmnsactions was $29,384,950 or $3.17 per share, compared to $32,731,394 or $3.55 pershare in 1970.

-i"!I'- 1.00..... I-

i ..... -II. I~~ .......... .75

I.

"

I:.

I ~' .50

I~:

Ii

I .~

I

~ 0

$150.000 loan is helping 30Mexican-American familiesto raise strawberries on 115acres of land near Salinas,California. In the first year,annual family incomes areexpected to Increase froman average of $3,600 to arange of $7,000 to $10,000.

Dollars 1.25

4th3rd

QUARTERLY INCOMEBEFORE SECURITY GAINS

OR LOSSES PER SHARE

2nd1st

1970

.1971

27

18

INCOME AND DIVIDENDS

Millions 536

1966 1967 1968 1969 1970 1971

INCOME BEFORE SECURITYGAINS OR LOSSES

• DIVIDENDS

FinancialReview

EarningsRise 4.8%:

6

Fourth quarter earnings showed only a slight improvement over1970 since the final year-ago period showed an unusually highprofit in trading bond income. For 1971, fourth quarter earningswere $9,740,138 or $1.05 per share, compared to $9,484,242 or$1.03 per share in 1970.

The continued ease in the Federal Reserve' Board's monetarypolicy contributed to the record domestic deposit gains, At yearend, total deposits rose 21.5 per cent to $6.4 billion, a $1,1 billionincrease over a year ago. Part of the gain was due to increasedforeign deposits through the Luxembourg branch. Deposits of theinternational branch nearly doubled, reaching $847 million byyear end.

Total assets of Wells Fargo & Company reached a new high of$7,8 billion, a 25.4 per cent increase or $1.6 billion over 1970.

9

4000

Millions $5000

YEAR END LOANS

1966 1967 1968 1969 1970 1971

MONTHLY PAYMENT LOANS

REAL ESTATE LOANS

• COMMERCIAL LOANSMillions $7500

6000

YEAR END DEPOSITS

1966 1967 1968 1969 1970 1971

OEMANO OEPOSITS)

•

TOTAL DEPOSITSTIME OEPOSITS

Wells Fargo's loan demand remained strong in 1971. With theending of tight money and an increased flow of funds into thebanking system, the Bank began an aggressive policy to seeknew loans, In the earlier part of the yeal', most of the gain was incommercial loans, but by fall, consumer borrowing began toincrease substantially.

By year end, total loans were up to $4.5 billion, an increase of21.1 per cent or $778 million over a year ago. Commercial (including foreign) loans, which account for approximately 60 per cent ofthe total, were up $605 million to $2.6 billion, Real estate loans,representing about 30 per cent of the loan portfolio, were up $65million to $1,3 billion; and consumer loans (including MasterCharge) gained $109 million to reach $541 million at year end,

Gross loan losses were moderately lower in 1971, despite thedifficulties in the economic recovery, However, recoveries werealso down, so that net loan losses were $7 million, up from $6,3million in 1970.

Loans Increase$778 Million:

SubstantialIncrease

in Deposits:

First phase of multi-milliondollar residential development at Hunter's Point inSan Francisco, financedby Wells Fargo. The projectincludes 101 apartmentsand is one of 15 similar lowand moderate costhousing projects financedby the Bank in 1971.

Our first banking house inthe Far East opened inTokyo In December. The.branch will specialize incorporate finance. workingclosely with Japanesecorrespondents and FarEast representatives.

AVERAGE ANNUAL YIELDSAND RATES PAID

LOANS

INVESTMENTS'

• TIME DEPOSITS & BORROWINGS Pareent 9

1966 1967 1968 1969 1970 1971*Taxable equivalent yield

1200

1966 1967 1968 1969 1970 1971

YEAR END INVESTMENTS

OTHER SECURITIES

FEDERAL AGENCY SECURITIES

• ~&:~I~~E~~~61~J1~J~~ & Millions $1600

• U.S. TREASURY SECURITIES

Wells Fargo acted as manager or syndicate member for undel-wl-iting new state and municipal bonds totaling $1.1 billion, up $292million from a year ago. In addition, the Investment Departmentwas active in providing secondary markets. Some emphasis hasbeen placed on broader participation in out-of-state bond issues,but primary efforts continue to be concentrated with bidding onCalifornia state and local obligations. The Bank was particularlyaggressive in bidding for tax anticipation notes to replenish theoperating funds of local communities pending the collection oftaxes. Trading activity has also increased in U. S. Governmentobligations, money market instruments, such as certificates ofdeposit and bankers' acceptances, and in underwriting and secondary market trading of Federal agency obligations.

Capital funds increased $11.9 million to $415 million. The reservefor loan losses rose to $73.4 million from $67.7 million a year ago.

Stockholders were paid dividends of $14,835,989 or $1.60 pershare. As of December 31, 9,274,388 shares were outstanding.

Investments: The investment portfolio was increased substantially in 1971 withthe easing of monetary policy and a gain in Bank deposits. Thiswas in contrast to the previous two years when it was reducedfrom its 1968 high of $1.2 billion to meet customer loan commitments. By year end, the portfolio totaled $1.3 billion, comparedto $1.05 billion in December 1970.

As interest rates declined and bond prices improved, adjustments were made in maturity distribution to create a greaterdegree of flexibility in the portfolio.

The average maturity of municipal bonds was eight years, sixmonths compared to 12 years, nine months at the end of 1970.The average maturity of government bonds at year end was 28months compared to 21 months a year ago. The market value ofthe portfolio was 96.9 per cent of book value as compared to91.9 per cent a year ago.

UnderwritingActivities:

Capital, Reserves,and Dividends:

10

Summary ofOperations

Trust Services:

With increased emphasis on the marketing of trustservices, a record volume of new business wasplaced on the books in 1971. Particulady gratifying increases were shown in the pension area andin the investment advisory services for individualsand corporations.

James K. Dobey. Exec. V.P. A new service backed by more than two yearsand Director. heads the Bank's

Asset Management Group. of Wells Fargo research was introduced to the

business community and initially offered to large pension funds.Known as Investment Technology, it represents one of the firstsuccessful integrations of traditional security analysis and portfolio management techniques with major concepts of ModernCapital Theory. (Modern Capital Theory deals with the pricebehavior of securities in the mal'ketplace and the problems of combining securities in orderto consistently achieve expected returns.)

Another new service, Wellsplan, is now offered to individualswith substantial assets or high income who are seeking skilledtotal tax and financial planning and investment counsel. Trustdepartments traditionally have been identified with conservationof assets and with knowledge and expertise in administeringestates. While these continue as the major functions of the TrustDivision, more emphasis is now being placed on services whichhave a lifetime orientation. Wellsplan represents an extension ofthis trend by emphasizing the accumulation of capital.

"

Financial Statements

12

Master Charge: Wells Fargo's sales volume again showed a substantial increaseover the previous year. Cardholder sales were up 37 per cent to$130 million and merchant sales volume increased 30 per cent to$65 million. The number of cardholders has remained near the360,000 mark, with the addition of new customers offsetting theelimination of inactive accounts.

Credit losses represent seven-tenths of one per cent of cardholder sales volume, down 21 per cent from a year ago. Fraudlosses were down 16 per cent, representing only three-tenthsof one per cent of the sales volume.

The credit card operation's profitable year, contributing aboutfour cents a share to earnings, was due to increased volume, operating and staff efficiencies and a lower cost of borrowed funds.

Staff Efficiencies: Despite an increase of 12 domestic branches and expanded international operations in 1971, the total Bank staff was maintainednear the 1970 level. A year ago, there were 10,416 Wells Fargoemployees. At the end of 1971, the staff numbered 10,429. Manyemployees work a part-time day, and on a full-time equivalentbasis, the staff totaled 9,788 compared to 9,783 a year ago.

Economic conditions and the management decision to holddown operating costs required tight staff control. Increasedemployee efficiencies and a lower turnover rate were major factorscontributing to the success of the program.

ASSETSDECEMBER 31, DECEMBER 31,

CHANGE1971 1970

Cash and Due from Banks $ 947,471,165 $ 662,444,510 $ 285,026,655

Time Deposits in Foreign Banks 518,450,244 200,337,060 31 8,11 3,1 84

Investment Securities:

U.S. Treasury Securities 374,721,535 409,428,481 (34,706,946)

Securities of Other U. S. GovernmentAgencies and Corporations 141,879,981 - 141,879,981

Obligations of States and Political Subdivisions 768,246,997 574,302,287 193,944,710

Other Securities 50,822,113 69,150,702 (18,328,589)

Total Investment Securities (Note 2) 1,335,670,626 1,052,881,470 282,789,156

Trading Account Securities (Note 2) 108,181,798 112,024,315 (3,842,517)

Funds Sold 90,155,000 206,083,000 (115,928,000)

Loans 4,472,784,121 3,694,511,914 778,272,207

Direct Lease Financing 43,795,573 36,734,398 7,061,175

Premises and Equipment (Notes 2 and 3) 114,760,596 114,976,148 (215,552)

Customers' Acceptance Liability 50,729,895 67,732,647 (17,002,752)

Accrued Interest Receivable 57,616,955 47,569,293 10,047,662

Other Assets 65,113,828 30,270,755 34,843,073

Total Assets $7,804,729,801 $6,225,565,510 $1,579,164,291

The accompanying notes are an integral part of these statements.

WELLS FARGO & COMPANYAND SUBSIDIARIES

14

LIABILITIES AND CAPITALDECEMBER 31, DECEMBER 31,

CHANGE1971 1970

Demand Deposits $2,218,131,813 $1,910,496,402 $ 307,635,411

Savings Deposits 1,681,229,777 1,495,346,390 185,883,387

Savings Certificates 832,831,830 696,029,626 136,802,204

Certificates of Deposit 269,314,510 251,147,687 18,166,823

Other Time Deposits 524,527,740 474,876,207 49,651,533

Foreign Deposits 856,928,421 426,286,819 430,641,602

Total Deposits 6,382,964,091 5,254,183,131 1,128,780,960

Funds Borrowed 700,661,316 262,970,516 437,690,800

Mortgages Payable (Note 3) 19,715,299 20,761,600 (1,046,301 )

Acceptances Outstanding 50,729,895 67,732,647 (17,002,752)

Accrued Taxes and Other Expenses 41,368,142 49,171,183 (7,803,041 )

Reserve for Unearned Discount 56,598,739 43,320,001 13,278,738

Other Liabilities 63,970,515 56,316,027 7,654,488

Total Liabilities 7,316,007,997 5,754,455,105 1,561,552,892

Reserve for Loan Losses (Note 4) 73,384,587 67,655,255 5,729,332

Capital Accounts

Borrowed Capital:

4% % Capital Notes of Wells FargoBank, N.A., due 1989 (Note 5) 50,000,000 50,000,000 -

3% % Convertible Notes due 1989 (Note 5) 25,062,700 25,070,700 (8,000)

Total Borrowed Capital 75,062,700 75,070,700 (8,000)

Equity Capital:

Common Stock-$10 par value, authorized12,000,000 shares, outstanding 9,274,388shares on December 31, 1971 (Note 6) 92,743,880 92,668,460 75,420

Capital Surplus 160,617,531 160,685,092 (67,561 )

Retained Earnings (Note 5) 86,913,106 75,030,898 11,882,208

Total Equity Capital 340,274,517 328,384,450 11,890,067

Total Capital Accounts 415,337,217 403,455,150 11,882,067

Total Liabilities and Capital $7,804,729,801 $6,225,565,510 $1,579,164,291

The accompanying notes are an integral part of these statements.

15

Consolidated Statement of Earnings

YEAR ENDED YEAR ENDEDDECEMBER 31, DECEMBER 31, CHANGE

1971 1970

INCOMEInterest and Fees on Loans $296,197,844 $300,508,701 $ (4,310,857)Interest and Dividends on Investment Securities:U. S. Treasury Securities 22,743,908 22,897,563 (153,655)Securities of Other U. S. Government Agenciesand Corporations 6,348,604 1,297 6,347,307Obligations of States and Political Subdivisions 23,055,841 20,529,497 2,526,344

Other Securities 4,544,687 3,899,693 644,994Interest on Time Deposits in Foreign Banks 25,872,636 13,653,171 12,219,465Trading Account Income 5,375,715 5,364,408 11,307Trust Income 11,408,827 10,745,051 663,776Service Charges on Deposit Accounts 20,078,241 19,600,379 477,862Other Income 23,167,672 14,451,208 8,716,464

Total Income 438,793,975 411,650,968 27,143,007

EXPENSESalaries 86,967,164 79,923,393 7,043,771Pension and Other Employee Benefits (Note 7) 17,153,157 15,224,111 1,929,046Interest on Deposits 192,690,032 159,566,639 33,123,393Interest on Borrowed Money 19,088,509 39,838,238 (20,749,729)Interest on Capital Notes 3,064,582 3,064,906 (324)Net Occupancy Expense (Note 2) 17,851,067 15,103,404 2,747,663Equipment Expense 11,009,526 9,924,956 1,084,570Provision for Losses on Loans (Note 4) 6,478,700 5,937,000 541,700Other Expense 34,821,286 32,400,214 2,421,072

Total Expense 389,124,023 360,982,861 28,141,162

INCOME BEFORE INCOME TAXES AND SECURITYGAINS OR LOSSES 49,669,952 50,668,107 (998,155)Less Applicable Income Taxes (Note 8) 15,318,000 18,084,300 (2,766,300)

INCOME BEFORE SECURITY GAINS OR LOSSES $ 34,351,952 $ 32,583,807 $1,768,145Security Gains (Losses) Net of Income TaxEffect of $(5,415,900) and $178,200 (4,967,002) 147,587 (5,114,589)

Net Income $ 29,384,950 $ 32,731,394 $ (3,346,444)

INCOME PER SHARE (Note 9):Income Before Security Gains or Losses $3.71 $3.54 $ .17Security Gains or Losses, Net of Tax (.54) .01 (.55)--Net Income $3.17 $3.55 $ (.38)

INCOME PER SHARE ASSUMING FULL DILUTION (Note 9):Income Before Security Gains or Losses $3.58 $3.42 $ .16Security Gains or Losses, Net of Tax (.51 ) .01 (.52)--Net Income $3.07 $3.43 $ (.36)

The accompanying notes are an integral part of these statements.

WELLS FARGO &COMPANYAND SUBSIDIARIES

16

Consolidated Statement of Capital AccountsFor the Two Years Ended December 31,1971

1971 1970

BALANCE AT BEGINNING OF YEAR $403,455,150 $383,426,289

CAPITAL NOTES-Conversion of convertible notes (Note 5) (8,000). (4,700)

COMMON STOCKConversion of convertible notes (Note 5) 1,300 780Issued incident to mergers and acquisitions 74,120 1,102,160

CAPITAL SURPLUSConversion of convertible notes (Note 5) 6,559 3,907Incident to mergers and acquisitions (74,120) 572,840

RETAINED EARNINGS

Additions:Net income for the year 29,384,950 32,731,394Incident to mergers and acquisitions - 597,474

Deductions:Cash dividends declared (14,835,989) (14,747,582)Provision for losses on loans, exclusive of portion charged againstincome, less related income tax effect $3,373,600 (Notes 4 and 8) (2,906,400) -Other-net of tax 239,647 (227,412)

BALANCE AT END OF YEAR $415,337,217 $403,455,150

Consolidated Statement of Changes in Financial PositionFor the Two Years Ended December 31,1971

1971 1970

SOURCES OF FINANCIAL RESOURCESNet income $ 29,384,950 $ 32,731,394Non-cash items (deferred taxes, depreciation and amortization) 20,943,227 6,981,502

Total obtained from income 50,328,177 39,712,896

Increases in:Deposits 1,128,780,960 614,380,082Funds borrowed 437,690,800 -Other increases-net 23,995,664 51,225,160

Decreases in:Funds sold 115,928,000 -Cash and due from banks - 42,868,111

Total $1,756,723,601 $748,186,249

APPLICATION OF FINANCIAL RESOURCESDividends paid to stockholders $ 14,835,989 $ 14,747,582Reduction in funds borrowed - 391,987,706Additional investments in:Loans 778,272,207 21,681,227Time deposits in foreign banks 318,113,184 77,306,612Cash and due from banks 285,026,655 -Securities (including trading) 278,946,639 32,787,079Premises and equipment 8,003,084 20,097,892Funds sold - 175,890,500

Other applications 73,525,843 13,687,651

Total $1,756,723,601 $748,186,249

The accompanying notes are an integral part of these statements.

WELLS FARGO &COMPANYAND SUBSIDIARIES

17

Consolidated Statement of Condition

YEAR-END BALANCES AVERAGE BALANCES (UNAUDITED)

ASSETS DECEMBER 31, DECEMBER 31, (In millions of dollars)1971 1970 YEAR 1971 YEAR 1970

Cash and Due from Banks $ 947,452,552 $ 662,421 ,484 $ 890 $ 793

Time Deposits in Foreign Banks 518,450,244 200,337,060 400 144

Investment Securities:

U. S. Treasury Securities 365,672,594 409,428,481 367 370

Securities of Other U. S. GovernmentAgencies and Corporations _141,879,981 - 119 -

Obligations of States andPolitical Subdivisions 768,246,997 574,302,287 639 554

Other Securities 49,423,938 69,150,702 77 68 .

Total Investment Securities (Note 2) 1,325,223,510 1,052,881,470 1,202 992

Trading Account Securities (Note 2) 108,181,798 112,024,315 84 40

Funds Sold 90,155,000 206,083,000 52 85

Loans 4,469,028,834 3,686,238,357 3,991 3,465

Direct Lease Financing 43,787,863 36,734,398 41 34

Bank Premises andEquipment (Notes 2 and 3) 112,994,244 113,321,942 113 107

Customers' Acceptance Liability 50,729,895 67,732,647 54 52

Accrued Interest Receivable 57,571,774 47,559,472 51 47

Other Assets 62,108,508 24,089,098 34 63

Total Assets $7,785,684,222 $6,209,423,243 $6,912 $5,822

See accompanying notes to Wells Fargo & Company consolidated financial statements.

WELLS FARGO BANK, N.A.AND SUBSIDIARIES

18

YEAR-END BALANCES AVERAGE BALANCES (UNAUDITED)LIABILITIES AND CAPITAL DECEMBER 31, DECEMBER 31, (In millions of dollars)

1971 1970 YEAR 1971 YEAR 1970

Demand Deposits $2,219,717,903 $1,911,405,240 $1,977 $1,824

Savings Deposits 1,681,229,777 1,495,346,390 1,612 1,448

Savings Certificates 832,831,830 696,029,626 775 631

Certificates of Deposit 269,314,510 251,348,154 254 193

Other Time Deposits 524,527,740 474,876,207 460 343

Foreign Deposits 856,928,421 426,286,819 678 287

Total Deposits 6,384,550,181 5,255,292,436 5,756 4,726

Funds Borrowed 697,911,316 251,248,926 406 343

Mortgages Payable (Note 3) 19,715,299 20,761,600 20 21

Acceptances Outstanding 50,729,895 67,732,647 54 52

Accrued Taxes and Other Expenses 40,153,862 48,082,671 50 48

Reserve for Unearned Discount 56,583,167 43,320,001 47 45

Other Liabilities 63,733,453 56,061,154 109 131

Total Liabilities 7,313,377,173 5,742,499,435 6,442 5,366

Reserve for Loan Losses (Note 4) 73,384,587 67,655,255 68 67

Capital Accounts

Borrowed Capital:

4Y2 % Capital Notes due 1989 (Note 5) 50,000,000 50,000,000 50 50

Total Borrowed Capital 50,000,000 50,000,000 50 50

Equity Capital:

Capital Stock-$10 par value,authorized 12,000,000 shares,outstanding 9,293,409 shareson December 31 ,1971 92,934,090 92,859,970 93 92

Surplus 160,678,440 160,744,560 161 161

Surplus Representing ConvertibleCapital Note Obligation Assumedby Parent Corporation (Note 5) 25,062,700 25,070,700 25 25

Undivided Profits 70,247,232 70,593,323 73 61

Total Equity Capital 348,922,462 349,268,553 352 339

Total Capital Accounts 398,922,462 399,268,553 402 389

Total Liabilities and Capital $7,785,684,222 $6,209,423,243 $6,912 $5,822

See accompanying notes to Wells Fargo & Company consolidated financial statements.Member Federal Deposit Insurance Corporation / Member Federal Reserve System

19

Additions to this reserve are made in accordance with provisionsof the Internal Revenue Code under which such additions are taxdeductible. The Bank's policy is to make additions to the reserve in themaximum amount permitted by the formula. The provision for loanlosses charged to expense is based on the ratio of the moving averagefor the most recent five years of actual net charge-offs to average outstanding loans. To compute the provision the ratio so obtained is

1. GeneralThe consolidated financial statements include the accounts of WellsFargo & Company (the Company), Wells Fargo Bank, N.A. (the Bank)and their principal subsidiaries.

2. AssetsInvestment securities are stated at cost, adjusted for amortization ofpremium and accumulation of discount. Accumulation of discountamounted to $1,697,173 in 1971 and $2,958,650 in 1970. The marketvalue of the investment securities on December 31, 1971 and 1970 wasapproximately $1,294,000,284 and $967,237,086, respectively. Securities at book value of $939,679,061 and $987,138,914 at December 31,1971 and 1970, respectively, were pledged to secure public depositsand for other purposes. Trading account securities of the Bank arestated at the lower of cost or market.

Premises and equipment are carried at cost less accumulated depreciation and amortization in the amount of $39,053,885 at December 31,1971 and $31,651,175 at December 31, 1970. Land included in premisesand equipment amounted to $24,337,238 at December 31, 1971 and$25,332,598 at December 31, 1970. Depreciation and amortizationcharged to expense in 1971 amounted to $8,218,636 and $7,254,402in 1970. Rental paid under non-cancellable leases in 1971 amountedto $5,219,684 and $3,998,554 in 1970. Leases are generally for termsnot in excess of thirty years.

3. Mortgages PayableThe mortgages payable are primarily two series of bonds issued by abank premises subsidiary averaging 4%% interest. The bonds arepayable in annual installments of $1,000,000 until 1988 and then annualinstallments of $500,000 until 1993. The bonds are secured by deedsof trust on $38,401,321 of bank premises, at cost.

253,747

12,758,700 6,190,747

9,662,020 9,687,7792,632,652 3,354,758

~7,029,368 6,333,021

!$73,384,587 $67,655,255

$5,065,850

6,095,022

Incentive andSavings Plan Expense

$2,402,635

2,402,806

Retirement PlanExpense

1970

1971

applied to the average loans outstanding during the year. In 1971 anadditional provision was made by a transfer from retained earnings toincrease the reserve to the maximum allowable for tax purposes.

5. Capital NotesThe 4Y2 % capital notes of the Bank will mature September 15, 1989.These notes may be redeemed at the option of the Bank at a premium ..

The 3% % convertible capital notes also matur.!? September 15, 1989.These notes are convertible into common stock of the Company at aconversion price of $60 per share, subject to adjustment in certainevents and may be redeemed at the option of the Company at anytime at a premium. The Bank is jointly and severally liable with theCompany for payment of the principal and inter'est of the notes. TheCompany has assumed primary liability for all such payments and hasagreed to reimburse the Bank if for any reason it should be requiredto make payments thereon.

The capital and convertible note indenture contains provisions which,among other things, restrict the payment of dividends and specify themaintenance of minimum amounts of capital funds. The amounts ofretained earnings not so restricted for payment of dividends were$86,913,106 at December31, 1971.

The notes are subordinated to obligations to depositors and certainother creditors.

6. Common StockAt December 31, 1971, 417,712 shares of unissued common stockwere reserved for issuance upon conversion of the 3% % convertiblenotes and 7,830 shares for issuance in connection with the acquisitionof the assets of Sonoma Mortgage Corporation.

7. Retirement and Incentive and Savings PlansThe retirement plan is non-contributory and covers substantially all fulltime employees. There are also incentive and savings plans for allemployees. The total expenses for these plans were as follows:

The Company's policy is to fund the accrued cost of the retirementplan. There was no remaining unfunded liability with respect to priorservice and the market value of the pension fund exceeded the actuarial value of vested benefits as of December 31, 1971.

8. Deferred Income TaxesThe income tax returns of the various entities generally are preparedusing the cash basis of accounting as permitted by taXing authorities.Deferred income taxes have been provided primarily in recognition ofthe differences between the accrual method used in preparation offinancial statements and the cash basis used for tax returns.

For the year ended December 31, 1971 there is a deferred tax of$12,724,591 in the consolidated statement of earnings. Current taxprovisions amounted to $2,593,409 and $18,357,200 respectively forthe years ended December 31, 1971 and 1970.

Accumulated deferred taxes on income aggregating $30,347,950 atDecember 31,1971 and $17,794,700 at December 31,1970 are includedprimarily in accrued taxes and other expenses and the reserve forloan losses in the consolidated balance sheet.

WELLS FARGO&COMPANYAND SUBSIDIARIES

1970

5,937,000

$67,797,529

6,478,7002,906,4003,373,600

$67,655,255Balance at beginning of year

AdditionsCharged to

ExpenseRetained EarningsDeferred Taxes

Reserves of acquired banksand other items

Total additions

DeductionsLoans charged offLess recoveries

Total deductions

Balance at end of year

4. Reserve for Loan LossesA summary of the changes in the reserve follows:

1971

Notes toConsolidated

FinancialStatements

20 21

The Board of Directors and Stockholdersof Wells Fargo & Company:

We have examined the consolidated balance sheet of Wells Fargo &Company and subsidiaries as of December 31, 1971 and the relatedstatements of earnings, capital accounts and changes in financialposition for the year then ended and the consolidated statement ofcondition of its wholly-owned subsidiary Wells Fargo Bank, NA andsubsidiaries as of December 31, 1971. Our examination was made inaccordance with generally accepted auditing standards, and accordingly included such tests of the accounting records and such otherauditing procedures as we considered necessary in the circumstances.

In our opinion, such consolidated financial statements present fairlythe financial position of Wells Fargo & Company and subsidiaries atDecember 31, 1971, and the results of their operations, changes incapital accounts and the changes in their financial position for the yearthen ended and the financial position of Wells Fargo Bank, N.A. and subsidiaries at December 31, 1971, in conformity with generally acceptedaccounting principles applied on a basis consistent with that of thepreceding year.

22

9. Income Per ShareIncome per share is computed by dividing income by the average number of shares outstanding. Income per share, assuming full dilution,is computed in the same manner with appropriate adjustment assumingconversion of all convertible notes and issuance of the shares reservedin connection with the acquisition of Sonoma Mortgage Corporationwith related adjustments to income for interest on the convertiblenotes, net of tax.

10. Commitments and Contingent LiabilitiesIn the normal course of business, there are outstanding various commitments and contingent liabilities such as foreign exchange contracts,guaranties, commitments to extend credit, etc. which are not reflectedin the accompanying financial statements. No material losses areanticipated as a result of these transactions.

11. Acquisition of First Western Bank and Trust CompanyThe Company has joined in an agreement and plan for merger betweenFirst Western Bank and Trust Company and Wells Fargo Bank, NationalAssociation, whereby First Western is to be merged with and under thecharter and articles of association of Wells Fargo Bank. Approximately99.5 per cent of the outstanding shares of First Western are owned byWorldamerica Investors Corp., a subsidiary of World Airways, Inc.Worldamerica has also joined in the merger agreement. The terms ofthe merger agreement provide that the Company will pay the shareholders of First Western approximately $95 million, $50 million of whichin 7112 % debentures, due in 1981, and approximately $45 million in cash.The other shareholders will have the election to receive cash or 1.852shares of Common Stock of the Company for each share of CapitalStock of First Western held by them. At present, there are 1,368,080shares of Capital Stock of First Western outstanding, 1.360,950 of whichare owned by Worldamerica. Options for an additional 71,400 shares arealso outstanding, which options may be exercised prior to the consummation of the merger.

As of December 31, 1971, First Western had total deposits of $995million, total loans of $585 million, total assets of $1.13 billion and atotal of 95 branch offices in California. For accounting purposes, theCompany will treat the merger as a purchase.

The merger of First Western and Wells Fargo Bank was approvedby the Comptroller of the Currency on December 20, 1971. The approvalprovided that the merger may not be consummated before the later ofthe following two dates: (a) the thirtieth calendar day after the date ofsaid approval (the period during which an action may be commencedunder the antitrust laws staying the effectiveness of said approval unlessotherwise ordered by the Court), or (b) the date upon which Wells FargoBank delivers to the Comptroller of the Currency a certified copy of adefinitive agreement or agreements between Wells Fargo Bank and oneor more purchasers satisfactory to the Comptroller of the Currency providing for the sale of the 41 Northern California branch offices of FirstWestern to be transferred within 90 days of the consummation of themerger of Wells Fargo Bank and First Western, or as soon thereafteras all of the requisite regulatory approvals to such sale have beenobtained.

An action of the type described in (a) above was commenced whenthe United States Department of Justice filed an action in the DistrictCourt to prohibit the consummation of the merger. The filing of theaction automatically imposes a stay on the merger. The stay remains ineffect during the pendency of the litigation unless removed by the Court.

Accountants'Report

San Francisco, CaliforniaJanuary 17,1972

>fa{ ~t1/U-J~/ ~~~ y c,.Peat, Marwick, Mitchell & Co.Certified Public Accountants

23

ns

1 1970 1969 1968 1967 .,AVERAGE DAILY BALANCES (In millions) 1971 1970 1969 1968 1967

Demand Deposits $1,976 $1,824 $1,731 $1,589 $1,432

98 $300,509 $263,544 $206,389 $167,993 Time Deposits 3,779 2,902 2,811 2,637 2,334

93 47,328 49,116 48,865 40,484

78 19,600 17,814 16,203 14,459Total Deposits $5,755 $4,726 $4,542 $4,226 $3,766

09 10,745 10,101 8,792 7,701 Investment Securities $1,215 $ 995 $1,112 $1,167 $1,080

16 33,469 19,695 11,073 7,736 Trading Account Securities 84 40 25 26 14

94 411,651 360,270 291,322 238,373 Loans 3,993 3,627 3,386 2,867 2,518

Net Borrowings 357 418 361 81 13

ICapital Accounts 411 394 379 366 351

67 79,923 68,599 57,226 48,328

53 15,224 13,306 10,270 8,880

43 202,470 173,435 133,412 108,817 AVERAGE RATES

51 15,104 12,966 11,297 10,171

10 9,925 8,114 7,096 5,184 Securities:

79 5,937 5,945 6,085 5,814U. S. Treasury 5.99% 6.14% 5.54% 5.40% 4.66%

21 32,400 29,670 25,749 20,464State and Municipaj(l) 7.45 7.64 8.21 7.94 6.74

24 360,983 312,035 251,135 207,658Total Securities(1) 6.69% 6.95% 6.97% 6.83% 5.85%

Loans:

Commercial 6.76% 8.41% 7.78% 6.58% 6.15%70 50,668 48,235 40,187 30,715 Real Estate 6.67 6.69 6.39 6.10 5.8818 18,084 16,188 9,842 5,100 Consumer 10.43 10.51 9.86 9.49 8.32

Foreign 7.97 9.68 10.99 - -52 32,584 32,047 30,345 25,615

67) 147 (19) (838) (1,120)Total Loans 7.22% 8.07% 7.53% 6.76% 6.34%

- - - (562) Total Loans and Securities(1) 7.06% 7.83% 7.39% 6.78% 6.19%

85 $ 32,731 $ 32,028 $ 29,507 $ 23,933 Interest Paid on Time Deposits and Borrowings 5.05 5.82 5.27 4.60 4.30

(1lTaxable equivalent yield.

.71 $3.54 $3.51 $3.36 $2.87

17 $3.55 $3.50 $3.27 $2.68 MISCELLANEOUS DATA

Company Staff at year end (full time equivalent) 10,441 10,262 9,755 8,687 7,624

Number of offices of Bank at year end 287 275 258 242 233

58 $3.42 $3.38 $3.24 $2.78

07 $3.43 $3.37 $3.15 $2.60

60 $1.60 $1.60 $1.45 $1.35

69 $35.44 $33.68 $32.80 $31.46

81 9,210,740 9,141,889 9,036,528 8,921,567

25

86,9

17,1

$3

$3.

438,7

49,6

15,3

$3.

$3.

197

34,3

(4,9

214,8

17,8

11,0

6,4

34,8

389,1

$296,1

56,6

20,0

11,4

54,4

$ 29,3

$1.

$36.

9,271,5

INCOME

Interest and Fees on Loans

Interest and Dividends on Investment Securities

Service Charges on Deposit Accounts

Trust Income

Other Income

EXPENSE

Salaries

Pension and Other Employee Benefits

Interest on Deposits, Borrowings andCapital Notes

Net Occupancy Expense

Equipment Expense

Provision for Losses on Loans

Other Expense

FINANCIAL RESULTS (In thousands)

Consolidated Five Year Summary of Operatio

Total Expense

Total Income

INCOME BEFORE SECURITY GAINS OR LOSSESAND LOSSES ON SALE OF REAL ESTATE LOANS

Security Gains (Losses) after Taxes

Losses on Sale of Real Estate Loans after Taxes

Net Income

WELLS FARGO &COMPANYAND SUBSIDIARIES

INCOME BEFORE INCOME TAXES,SECURITY GAINS OR LOSSES ANDLOSSES ON SALE OF REAL ESTATE LOANS

Applicable Income Taxes

INCOME PER SHARE ASSUMINGFULL DILUTION

Income Before Security Gains or Lossesand Losses on Sale of Real Estate Loans

Net Income

DIVIDENDS AND BOOK VALUE (Per Share)

Cash Dividends Declared

Book Value at end of year

Average Shares Outstanding

INCOME PER SHARE

Income Before Security Gains or Lossesand Losses on Sale of Real Estate Loans

Net Income

24

26

Comparison of Loans (End of Year)

COMMERCIAL LOANS

Loans Unsecured

Loans on Collateral

Loans purchased from Wells Fargo Bank, N.A.by parent company

Bills of Exchange and Acceptances Discounted

REAL ESTATE LOANS

FHA and VA Loans

Conventional Loans

Farm Loans

Interim Construction

Dollar Volume of new loans made during year

Number of loans held by Bank at end of year

Number of sold loans serviced for others at end of year

Dollar volume of sold loans serviced for othersat end of year

CONSUMER LOANS

Total Consumer Loans at end of year

Dollar volume of new loans made during year(1)

Number of new loans made during year(1)

Loan losses as a per cent of loans outstandingat end of year

Total Loans

(1)00es not include Master Charge loans.

WELLS FARGO &COMPANYAND SUBSIDIARIES

Maturity Schedule of Major Categories of Investment Securities-Book ValueIas of December 31,1971 (In millions of dollars)

1971 1970 CHANGE U.S. TREASURY FEDERAL AGENCY STATE, COUNTY ANDI SECURITIES SECURITIES MUNICIPAL BONDS

I BOOK VALUE PER CENT BOOK VALUE PER CENT BOOK VALUE PER CENT

I

$2,165,813,000 $1,716,485,000 $449,328,000Maturing in one year $120 32.00% $ 60 42.25% $244 31.77%

411,903,000 293,038,000 118,865,000Maturing in two through

,Ifive years 205 54.67 82 57.75 125 16.28

263,000 8,179,000 (7,916,000)Maturing in six through

I62,973,000 18,376,000 44,597,000 ten years 50 13.33 - - 85 11.07

$2,640,952,000 $2,036,078,000 $604,874,000 Maturing after ten years - - - - 314 40.88

Total $375 100.00% $142 100.00% $768 100.00%

$ 326,102,000 $ 374,313,000 $ (48,211 ,000)

835,020,000 793,083,000 41,937,000Maturity Schedule of Investment Securities-Par Value

13,012,000 14,544,000 (1,532,000) as of December 31,1971 and 1970 (In millions of dollars) I

117,096,000 44,778,000 72,318,000 I

$1,291,230,000 $1,226,718,000 $ 64,512,0001971 1970 CHANGE

PAR VALUE PER CENT PAR VALUE PER CENT PAR VALUE PER CENT

I

$ 405,687,000 $ 307,512,000 $ 98,175,000 Maturing in one year $430 32.43% $276 26.26% $154 6.17%I

66,700 66,100 600 Maturing in two through

42,000 39,600 2,400five years 419 31.60 289 27.50 130 4.10

Maturing in six through ,

$ 697,095,000 $ 629,637,000 $ 67,458,000ten years 142 10.71 90 8.56 52 2.15

Maturing after ten years 335 25.26 396 37.68 (61 ) (12.42)

$ 540,602,000 $ 431,716,000 $108,886,000

$ 714,508,000 $ 475,896,000 $238,612,000 II126,000 116,800 9,200 I

.40 of 1% .35 of 1% .05 of 1% I

$4,472,784,000 $3,694,512,000 $778,272,000

I

II

WELLS FARGO &COMPANYAND SUBSIDIARIES

27

Sonoma Mortgage loan sales again showed substantial gains, rising toMortgage: $120 million from $99.3 million a year ago. Financing of resi

dential properties was stimulated by the concentrated effort ofproduction and sales departments, the creation of the "spot loan"program and the Bank's interest in Federal low-cost housingprojects.

The "spot loan" program proved to be a successful mediumby which individual single family loans could be processedthrough Wells Fargo branches and ultimately, to Sonoma Mortgage for resale in the secondary market.

The Division financed $4.5 million in FHA projects designed toaid low and moderate-income families purchasing homes or renting apartments. An additional $22.5 million is pending for newFHA projects. Mortgage and rent payments for these units arepartially subsidized by the Government, depending on the families' incomes.

In September, a service office was opened in Fresno bringingto ten the number of strategically located offices throughout theState. The Division contributed about 19 cents a share to earnings, compared to four cents a share in 1970.

InternationalGains:

International activities expanded in Europe, thePacific and Latin America. Wells Fargo's first fullservice branch in the Far East opened in TokyoDecember 1. The new branch offers a full rangeof banking services, but its principal activities willbe concentrated on corporate and foreign trade

AaIPhJ.cral::d.Exec.vp. financing, working closely with our Japanese cor-heads Inlcrn.1lional. National S· I hDivisions; Northe,n branches. respondent banks. Ince 1961, Wei s Fargo ashad a representative office in Tokyo.

A second Edge Act subsidiary, Wells Fargo Interamerican Bank,opened in Miami, Florida in August. Capitalized at $2 million, thenew bank will work closely with the soon-to-open Nassau branchin the Bahamas and the network of Western Hemisphere representative offices. Latin American representation was strengthenedwith the opening of offices in Sao Paulo, Brazil and Caracas,Venezuela. Another representative office is expected to open inColombia early in 1972.

A new merchant bank is now being organized and will open inLondon shortly. Wells Fargo Ltd., with an effective capitalizationof $10 million, will complement the activities of the Europeanrepresentative office and our affiliate, Western American Bank(Europe) Ltd. The new bank will conduct business in sterling,Eurodollars and other Eurocurrencies and will arrange short,medium and long-term credit requirements for multi-national companies. The bank will also offer services in debt underwriting,private placement, and investment counseling.

A minority interest was acquired in Broadbank Corporation Ltd.,Auckland, New Zealand. Wells Fargo became the first U. S. com-

29

mercial bank to enter the New Zealand market. The majorityownership is retained by the parent company, Broadlands Dominion Group Ltd., largest locally-owned finance company in New

Zealand.Unfortunately, one of our international affiliates, in which we

have a 24.5 per cent interest, Martin Corporation Group Limited,holding company for an Australian merchant bank, reported aloss of $4.2 million (U. S. dollars) in 1971. The after-tax loss to

Wells Fargo was $546,000.The Luxembourg branch activities continued to expand dramati

cally. The branch, opened in the summer of 1969, specializes inEurocurrencies and now has a staff of 30. Deposits doubled in1971 to $847 million. Deposits are either placed in foreign banksas time deposits or loaned to multi-national companies overseas.

Interior of the San MarinoOffice, one of the mostrecent branches to openin Southern California.

The five-year goal of 50 offices in Southern California by the end of 1972 is expected to be attained.Thirty-nine offices were in operation by the endof 1971. With a slowdown in both the economy of

1IIIIIIIIIl~ the area and in the rate of population growth,_ ~ future branch expansion in the market will be at

John R. Breeden: Exec. V.P.. a much slower pace.Is in charge of the Bank's A . W II F' I d h f h dSoulhern California OIvisions. yeal ago, e s algo ease t e ormer ea -quarters building of Aerojet General Corporation in EI Monte fora number of departments, including operations, computer center,personnel, training, credit card and marketing headquarters. Addi-

SouthernCalifornia:

Realignment With the key population centers of Northern California now repreof Customer sented by some 240 banking offices, "branch expansion" is

Servicing: taking on a new meaning. First to begin this realignment of activities is the Financial Center Division, organized a year ago to concentrate on the Bank's large corporate and individual customersin the Bay Al'8a. With six metropolitan branches and deposits inexcess of one billion dollars, this division now has special supportgroups in the retail and corporate areas. This pattern of specialized services is now being developed for all branch divisions.

New offices were opened in some selected growth markets inNorthern California. San Francisco's 30th office opened on UnionStreet, once a neighborhood shopping area that has become astreet of speciality shops serving the Bay Area. The City's 31 stoffice opened in July near the internationally-known Cannery andGhirardelli Square shops and restaurants. The Silverado office,named after a nearby 19th century silver mine, opened in Napa,the second branch in that city.

Two offices were opened in the San Joaquin Valley, one infamed Yosemite National Park, the second in the agricultural community of Hanford. New and larger quarters were provided foroffices in Moraga, Alameda, Santa Cruz, Yuba City, Piedmont,North Sacramento and Sacramento.

30

ElectronicTransfer of Funds:

Urban Affairs:

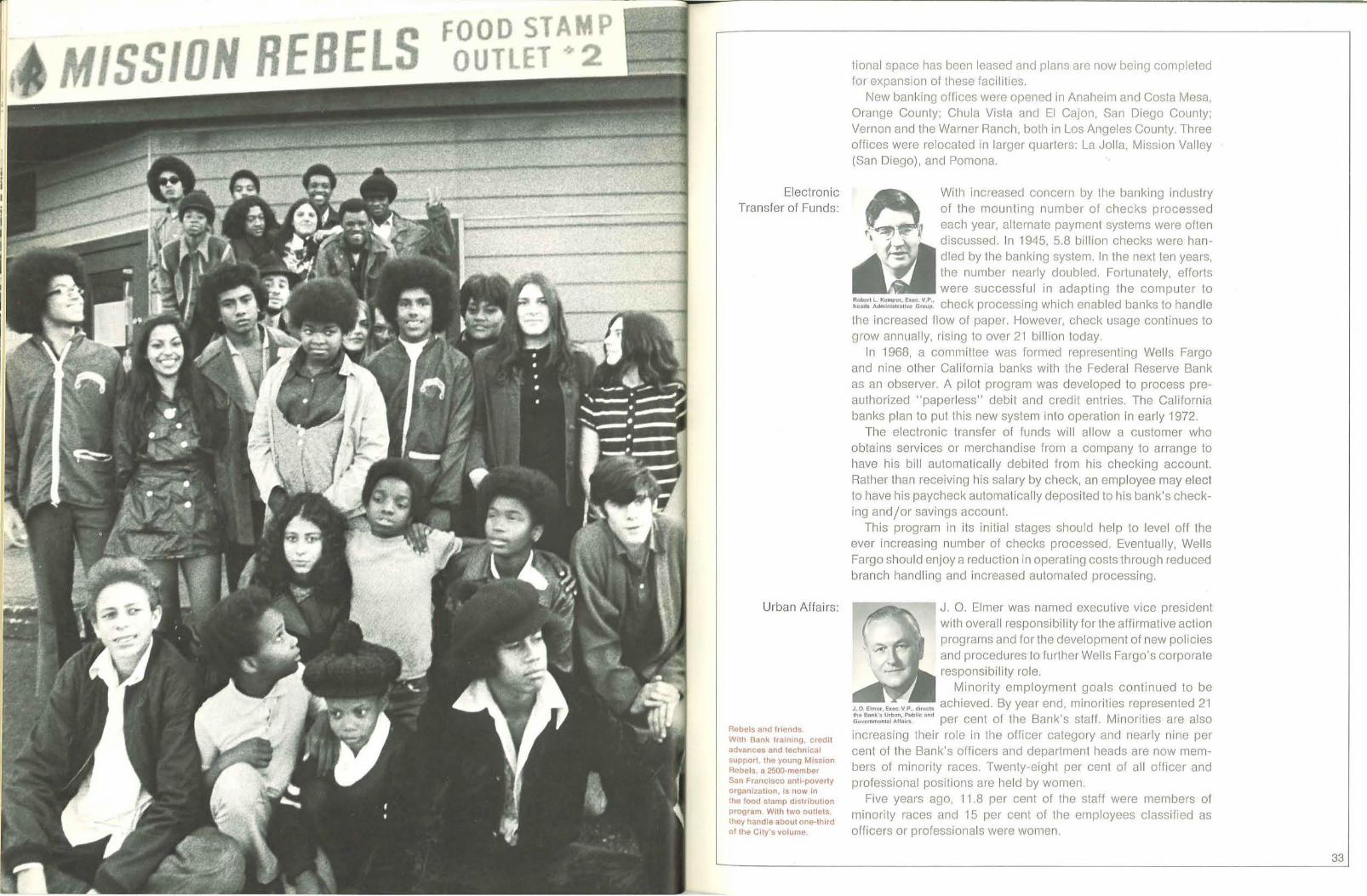

Rebels and friends.With Bank training, creditadvances and techn icalsupport, the young MissionRebels, a 2500-memberSan Francisco anti-povertyorganization, is now inthe food stamp distributionprogram. With two outlets,they handle about one-thirdof the City's volume.

tional space has been leased and plans are now being completedfor expansion of these facilities.

New banking offices wem opened in Anaheim and Costa Mesa,Orange County; Chula Vista and EI Cajon, San Diego County;Vernon and the Wamer Ranch, both in Los Angeles County. Threeoffices were mlocated in larget' quarters: La Jolla, Mission Valley(San Diego), and Pomona.

With incmased concem by the banking industryof the mounting number of checks processedeach year, altemate payment systems wet'e oftendiscussed. In 1945, 5.8 billion checks wem handled by the banking system. In the next ten years,the numbel' nearly doubled. Fortunately, effortswere successful in adapting the computer to

Robert L. Kemper, Exec. V,P., h k . I' h bl d b I h dIheads Admlnist,allvoGroup. C ec processlngwllc ena e an~sto an ethe incl'eased flow of paper. However, check usage continues togrow annually, I'ising to over 21 billion today,

In 1968, a committee was formed representing Wells Fargoand nine other Califomia banks with the Fedeml Reserve Bankas an observer. A pilot progmm was developed to process preauthorized "paperless" debit and cl'edit entries. The Californiabanks plan to put this new system into operation in early 1972.

The electronic transfer of funds will allow a customer whoobtains sel'vices or merchandise from a company to arrange tohave his bill automatically debited from his checking account.Rather than receiving his salary by check, an employee may electto have his paycheck automatically deposited to his bank's checking and/or savings account.

This program in its initial stages should help to level off theever increasing number of checks processed. Eventually, WellsFargo should enjoy a reduction in operating costs through reducedbranch handling and incl'8ased automated processing.

J. O. Elmer was named executive vice presidentwith overall responsibility for the affirmative actionprograms and for the development of new policiesand procedures to fUl'ther Wells F8I'go's corporateresponsibility role.

Minority employment goals continued to be

J.D.Elme',Exec.V.P.,directs achieved. By year end, minorities repl'esented 21~~v~~:~:n~:lb~~~i.~blic.nd per cent of the Bank's staff. Minorities are alsoincreasing their role in the officer category and nearly nine percent of the Bank's officers and dep8l'tment heads al'e now members of minority races. Twenty-eight per cent of all officer andprofessional positiollS are held by women.

Five yeal's ago, 11.8 per cent of the staff were membel's ofminority mces and 15 per cent of the employees classified asofficers or professionals were women.

33

Student Loans: Helping students meet the increased costs of higher education,the student loan program continued to grow with loans to 34,300students, totaling more than $37 million. This was a 39 per centincrease over 1970. The delinquency ratio (loans more than 30days past due) was a fractional percentage point above the delinquency ratio for regular personal loans.

34

Low-incomeHousing:

Minority Loans:

Specialized minority programs continue to expand. In 1971, aprogram for senior officers and supervisory management wasintroduced to increase the effectiveness of our existing minorityhiring and promotion practices.

Wells Fargo played a key role in the formation of OpportunityCapital Corporation, the first large Minority Enterprise Small Business Investment Company (MESBIC) to be established by a consortium of Bay Area corporations and banks.

Total capitalization will be in excess of $1 million which will besupplemented by $2 million in Small Business Administrationdebentures. The investors include 41 major banking, financial andindustrial concerns. The participants will also supply managementand technical advisory assistance to the new corporation.

Low and moderate-income housing projects are being financed inboth rural and ul'ban areas in California. Projects vary from the$1 million senior citizen project in Sacramento to the $2.1 millionproject for low-income families at Hunter's Point in San Francisco.Two of the real estate experts with Sonoma Mortgage are available to community groups for financial planning for low-incomehousing. In 1971, loans for such projects exceeded $30 millionfor 1,871 family units.

A unique effort is underway in Oakland with Wells Fargo, theOakland Redevelopment Agency and the Federal Housing andUrban Development (HUD) cooperating on a program to restoreVictorian homes in a 50-block area.

Prospective homeowners can purchase the property from theRedevelopment Agency through a first mortgage with Wells Fargo.Approved applicants are granted low-cost loans by HUD for complete renovation and restoration of the old houses.

Loans are made to minority businesses through a number ofprograms: (1) bank loans partially guaranteed by the Small Business Administration; (2) direct loans without government guarantee and (3) loans through a California Job Development Corporation known as Opportunity Through Ownership. Bank minorityloans this year increased 78 per cent to $9.2 million for 350 minority business firms ranging from wrought iron product manufacturing to tortilla bakeries. Loans through OPTO in 1971 were$1,336,095 to 45 minority businesses. Wells Fargo, with a 26 percent share in this venture, contributed $387,400 in loan fundsand $80,000 in operating expenses.

Wasle paper from WellscoDala subsidiary and Bank'scomputer center is nowrecycled. Recycled paper isalso being used on internalbulletins, pUbl ications,and promotional material.

36

Directors WELLS FARGO & COMPANYand its principal subsidiary,

WELLS FARGO BANK, N.A.

Ernest C. Arbuckle

Chairman of the Board

Kenneth K. Bechtel

Chairman of the Executive Commitlee,

Industrial Indemnity Company

William R. Breuner

President,

John Breuner Company

Robert L. Bridges

Thelen. Marrin, Johnson & Bridges,

Attorneys at Law

Ransom M. Cook

President, Wells Fargo Bank, 1960-64;

Chairman, 1964-66

Richard P. Cooley

President and Chief Executive Officer

John E. Countryman

Director and Member of

Finance Commillee,

Del Monte Corporation

James K. Dobey

Executive Vice President

Leonard K. Firestone

Retired President,

Firestone Tire & Rubber Company

of California

James Flood

Trustee,

Flood Estate

J. A. Folger

Retired Chairman of the Board,

The Folger Coffee Company

W, P. Fuller IIIVice President,

Western Region, PPG Industries

Richard E. Guggenhime

Partner,

Heller, Ehrman, White & McAuliffe,

Atlorneys at Law

James M. Hait

Senior Consultant and Director,

FMC Corporalion

I. W. HellmanPresident, Wells Fargo Bank, 1943-60;

Chairman, 1960-64

Thomas V. Jones

President and Chairman of the Board,

Northrop Corporation

Daniel E. Koshland*

Chairman of the Executive Commitlee,

Levi Strauss & Co.

Roger D. Lapham, Jr.

President,

Frank B. Hall & Co. of California

Edmund W. Littlefield

Chairman of Ihe Board and

CI,ief Execulive Officer.

Utah International Inc.

James K. Lochead·

President, American Trust Company,

1938-56; Chairman, 1956-57

Donald Maclean*

Retired Chairman of the Board,

California and Hawaiian

Sugar Company

Malcolm MacNaughton

Presidenl and Chief Executive Officer,

Castle & Cooke. Inc.

J. W. Mailliard III

Chairman of the Board,

Mailliard & Schmiedell

Donald H. McLaughlin*

Chairman of the Execulive Commitlee,

Homestake Mining Company

Wilson Meyer*

Chairman of the Board,

Wilson & Geo. Meyer & Co.

Arjay Miller

Dean. Graduate School of Business,

Stanford University

Paul A. Miller

President and Chief Execulive Officer,

Pacific Lighling Corporalion

George G. Montgomery·

Retired Chairman of the Board,

Kern County Land Company

Robert S. Odell*

President,

Allied Properlies

B. Regnar Paulsen

President,

Rice Growers Associalion

of California

Atherton Pilleger

Brobeck, Phleger & Harrison,

Attorneys at Law

Herman Phleger*

Brobeck, Phleger & Harrison,

Atlorneys at Law

William E. Roberts

Chairman of the Board,

Ampex Corporation

Allan Sproul*

Economist;

President. Federal Reserve Bank

of New York, 1941-56

• Directors Emeritus,

Wells Fargo Bank. N.A.

!I

I

I

1

iI

1

:jI

Organization WELLS FARGO & COMPANY420 Montgomery StreetSan Francisco, California 94104

CHAIRMAN OF THE BOARD

Ernest C. Arbuckle

PRESIDENT ANDCHIEF EXECUTIVE OFFICER

Richard P. Cooley

SENIOR VICE PRESIDENTS

J. O. ElmerLeonard Ma rks Jr.

VICE PRESIDENTS

Ralph J. Crawford, Jr.

James K. DobeyPaul N. EricksonHerbert W. FaulknerDaniel S. Livingston

VICE PRESIDENT AND TREASURER

Robert L. Kemper

VICE PRESIDENT AND SECRETARY

Philip G. Bowser

GENERAL AUDITOR

Orion A. Hill, Jr.

TRANSFER AGENTS

Wells Fargo Bank, N.A.Corporate Trust Department

475 Sansol11e Sireet

San Francisco, California 94111

Morgan Guaranty Trust Company30 West Broadway Street

New York, New York 10015

REGISTRARS OF STOCK

Bank of America N.T. & SA55 Hawthorne Sireet

San Francisco. California 94105

First National City Bank111 Wall Street

New York. New York 10015

STOCK EXCHANGE LISTINGS

New York Stock ExchangePacific Coast Stock Exchange

WELLS FARGO BANKHead Office: 464 California StreetSan Francisco, California 94104

CHAIRMAN OF THE BOARD

Ernest C. Arbuckle

PRESIDENT ANDCHIEF EXECUTIVE OFFICER

Richard P. Cooley

EXECUTIVE VICE PRESIDENTS

John R. Breeden

Ralph J. Crawford. Jr.

James 1<' Dobey

J. O. Elmer

Jol,n F. Holman

RiChard D. Jackson

Robert L. Kemper

VICE PRESIDENT ANDSECRETARY-TREASURER

Philip G. Bowser

GENERAL AUDITOR

Orion A. Hill, Jr.

CREDIT POLICY, ECONOMICS

AND PLANNING

Ward C. KrebsSenior Vice President

VICE PRESIDENTS:

Harold L. Buma

Stephen G. Gribi

Mattheus Visser

INVESTMENT COMMITTEE

Lester H. EmpeySenior Vice President and Chairman

PUBLIC ANDGOVERNMENTAL AFFAIRS

J. O. ElmerExecutive Vice President

VICE PRESIDENTS,

Ross Buell

Robert J. Gicker

Henry F. Grady, Jr.

ADMINISTRATIVE GROUP

Robert L. KemperExecutive Vice PreSident

ADMINISTRATION DIVISION

Richard D. JacksonExecutive Vice President

VICE PRESIDENTS:

Harold R. ArthurCashier

Gerard E. Downey

Fred W. Engelbrecht

R. Wayne Fillpot

Carroll H. George

John P. Griffiths

Joseph P. Hiss

CONTROLLER'S DEPARTMENT

Donald E. SeeseSenior Vice President and Controller

DATA PROCESSING DIVISION

Watson M. McKee. Jr.Vice President

VICE PRESIDENTS:

Charles J. Bold

Richard D. Buckwalter

Robert R. Hewlett

Miss Janet Wright

LEGAL DEPARTMENT

Lane P. BrennanVice President and Counsel

MANAGEMENT SCIENCESDEPARTMENT

John A. McQuownVice President

MARKETING ANDADVERTISING DIVISION

Richard M. RosenbergSenior Vice President

VICE PRESIDENTS:

Edward E. Munger

Roger D. Radcliffe

Richard B. West

37

ASSET MANAGEMENT PERSONNEL DIVISION Richard C. Smith PENINSULA DIVISION VALLEY DIVISION South Lake Tahoe FINANCIAL CENTER LUXEMBOURG BRANCH

GROUP William A. Stimson II Leslie C. Smith Stockton (4) DIVISION Leon M. WeyerDaniel S. Livingston Robert L. Altick, Jr.Semor Vice President Suller Creek Gilman B. Haynes, Jr. Vice President and ManagerSenior Vice President Glendon A. Wardllaugh Senior Vice PresidentJames J<. Dobey

Franklin H. Watson III Tahoe City Senior Vice PresidentExecutive Vice President K. Stanley ThompsonTracySenior Vice President John V. W. Zaugg VICE PRESIDENTS:Turlock

NASSAU BRANCHVICE PRESIDENTS:

W. Wayne Akert VICE PRESIDENTS W. Terence IrishVacavilleVICE PRESIDENTS: Graham G. Adams Alfred S. Anderson Vlsaha Duane G. Anderson Manager

FINANCIAL ANALYSISW. Gary Alford, Jr. Joseph E. Ault West Sacramento Elmer E. AndersonEarl J. AureliusDEPARTMENT BANKING GROUP Russell D. Andersen Williams TOKYO BRANCHGeorge A. Dujmovich Howard J. Boscus Alan E. Beck

James R. VerlinMax H. Forster Ralpll J. CraWford, Jr. Sigmund E. Beritzhoff

George E. Briare Woodland Robert F. Davidson Robert H. MorehouseSenior Vice President Director of Training Executive Vice President Dean ChaixEllis M. Cripe Yosemite L. Eston Davis Vice President and

George Lowther Warren B. Cottrell Yuba City (2) General ManagerNed B. Dickson Robert L. DeMallei

William P. Stritzler EAST BAY DIVISION Thomas L. CraigCletus J. Doneux William L. Hart

Gerald L. HeckVICE PRESIDENTS: Thomas A. Bigelow I. Michael Danielson Vice President and

Eugene B. Erskme Fredenck B Henderson, Jr. Deputy General ManagerSenior Vice President Charles J. DavisChester M. BoltwoodForest Helland WEST BAY DIVISION Wilham B. MacCoII, Jr.SONOMA MORTGAGE Peter R. HammondWilliam L. Fouse

COMPANY DIVISION Ralph B. Hofer William L. Isham Robert McLean ARGENTINAVICE PRESIDENTS: A. William Barkan REPRESENTATIVE OFFICEJulius P. HammerBertram Holmes William G, Isherwood Senior Vice President Harry East Miller, Jr.Henry F. Trione Carl 1<. Bomberger

Arthur W. Johansen DeWill C Moon William M. ScearceW. Rodney Hughes Senior Vice President David D. Brown Ellis A. HowardVice President

Thomas A. Middleton Merle D. Brown John A. I<ern Robert D Livingston Fredenck L. Novy

Robert S. Leeper James M. McCabe VICE PRESIDENTS:Thomas E PetersonVICE PRESIDENTS: Orvin L. Brown

AUSTRALIALawrence W. Liston Charles P. Morgan Glenn E Adams Donald CRegoJohn J. Cunningham Gino Cecchini REPRESENTATIVE OFFICEWilliam H. Mauel Richard L. Nelepovllz Leo M. Blanco Arthur W. RelleMrs. Dorolhe D. Hutchinson Conrad R. Craig

Joseph L. Nessler Edwin W. Bode, Jr. Hugh W. FosterINVESTMENT William J. Maxwell Jack E. RlcaudJohn Irvine David W. CraneWilliam T. Clarke RepresentativeDEPARTMENT Andrew McConnell Gordon G. Nevis Robert A, SaxeWilliam Kellinger Earl B. Duarte Alvin L. JohnsonD. Pat McGuire George L Olson George G. SkouGeorge F. Casey, Jr. Donald D. Rachuy Waller H. Ehlers Edwin Johnson BRAZIL

Senior Vice President Byron L. Morlenson John E. WeaverJames B. Keegan Phlhp T. Smtth REPRESENTATIVE OFFICEMrs. Elizabeth B. Roberls Sian ley B. Gerdes

Henry M. Nissen Raymond F. WhitgroveFrank V. Hodges Raymond R. Lillie Samuel P. Stevens William C. KeenJames A. Radich

Joseph D. Martino Robert G. Wlnden Vice PresidentEdward P. JepsenHarvey E. SchapanskyVICE PRESIDENTS: SONOMA MORTGAGE Colin J. Mason Roland J. WynneJohn W. Larsen Roland Tavernetti OFFICES:

Thomas H. Boughey COMPANY OFFICES:Byron E. Lewis Charles E. Nussbaum Robert J. Zaro CENTRAL AMERICA

Alturas Campbell S. O'Neill REPRESENTATIVE OFFICELouis E. Ciapponi Santa Rosa Philip L. McClur Anderson Robert H. Rehfeld Charles M JohnsonDavid G. Stead Encino William R. McGuire Auburn Waller J. Spaelli OFFICES:OFFICES: RepresentetlveAndrew E. Steen Fresno Raymond A. McKellar BealeAFB Roderick H. Speetzen SAN FRANCISCO (6):Donald G. Wharton, Jr. Los Angeles E. Julian Unruh Aptos Carmichael Waller K. Stevenson Crown-Zellerbach Office

COLOMBIASacramento R. Neil Wood Belmont Chico H E. Waite 464 Cal fornia Street Office REPRESENTATIVE OFFICESan Diego Campbell ClOVIS Market-Main Street Office

Gustavo Arango BernalSan Francisco Capilola Corning Market-Montgomery OfficeAssl tant Vice PresidentOFFICES: Carmel Davis New Montgomery OfficeLOAN DIVISION San Jose

OFFICES:Santa Ana

Alameda (4) Castroville Fairfield Union Trust OHiceJohn F. Holman Antioch (2) Cupertino Fresno (4) Arcata EUROPEANExecutive Vice President Walnut Creek

Berkeley (6) Gilroy Grass Valley Burlingame (3) REPRESENTATIVE OFFICE

Russell F. Dwyer Castro Valley Gonzales Gridley CoveloINTERNATIONAL

Henry Pansh IIISenior Vice President Concord (3) Greenfield Hanford Crescent City Vice P a dent

TRUST DIVISIONDanville Hollister Huron Daly City

DIVISION

George A. Hopiak Dublin King City Jackson Eureka Robert N. Bee HONG KONGVICE PRESIDENTS:

Sen ior Vice Presidont EI Cerrito Los Altos Kingsburg Foster City Senior Vice President REPRESENTATIVE OFFICEand Senior Trust OfficerEmeryville Los Galos Lodl Larkspur R. Wickham BaxterDickson BeckettFremont (3) Menlo Park (2) Los Banos Middletown VICE PRESIDENTS: Vice Pre IdentVICE PRESIDENTS:

Jack A. Byers Hayward (3) Milpitas (2) Madera MillbraeGemt E. VenemaMario R. AnconaLouis F. Cimina Lafayette Monterey (2) Manteca Mill Valley Manager MEXICO

Darwin M. CochraneJohn B. Anderson Livermore Morgan Hill Marysville Napa (2) Gerrlt P. Vander Ende REPRESENTATIVE OFFICE

Chief Appraiser William R. Barnett Martinez Mountalll View (2) Merced Novato Assistant ManagerJohn E. SanfordEugene E. Cochrane Alan D. Bigelow Moraga Pacific Grove Modesto (2) PaCifica William E. Biggerstaff Assistant Vice President

W. Slanford Durranl Edmund J. Brunswick Newark Palo Allo (4) Oakdale Petaluma John A. Bohn, Jr.Ronald E. Eadie Francis E. Canatsy Oakland (10) Redwood City (3) Pallerson SI. Helena Samuel A. Costanzo

VENEZUELARobert L. Essick Warren E. Danforth Orinda Salinas (4) Placerville San Anselmo Charles H. Green REPRESENTATIVE OFFICE

Christopher T. Ford Piedmont San Carlos Plymouth San Bruno Wilham E. Henley Waller A. BustardArthur L. FoskettKenneth N. Galloway Pittsburg San Jose (9) Qumcy San Francisco (25) Gardner S. Jacobs Assistant Vice PreSidentKenneth L. Jones

Chief Loan Examiner Robert M. HarperPleasant Hill Santa Clara (4) Rancho Cordova San Mateo (3)

Donald W. JardineLawrence E. Kinsella. Jr. Pleasanton Santa Cruz (2) Red Bluff San Rafael (2)Stanley S. Hasbrook

Richmond (2) Saratoga Reddmg (2) Santa Rosa (3)Carlos Rodriquez-Pastor AFFILIATES:

Charles R. Looney Hasell L. Henderson San Leandro SeaSide Roseville Sausalito Lester A, Roth AuslraliaWilliam L. Marlin E. Gearey Johnstone San Lorenzo Sunnyvale (2) Sacramento (13) Sonoma Karl E. Seeger ColombiaFielding McDearmon Alexander M. Millar Vallejo Watsonville (2) San Joaquin South San Francisco (2) William R. Sweet EcuadorEdward B. Wilkinson Basil C. Pearce Wainul Creek Woodside Sonora Ukiah Robert R. van Veerssen EI Salvador

38 39

Hong Kong James A. Horsburgh Sherman W. McKlssock WELLS FARGOJapan L. Robert Koenig Robert F. Meurer SECURITIES CLEARANCEMexIco Robert B. Leet Robert D. Thomas CORPORATIONNew Zealand Hans J. Lund Wilham J. Ward

27 William StreetNicaragua W. Peter McAndrew Leonard E. Wasserstein

New York, New York 10005Peru Paul A. Renstrom Walter J WinrowPhilippines Robert M. Ridley, Jr.Taiwan Donald C. Smith Richard D. Jackson

Thailand Glenhall E. Taylor, Jr. OFFICES:President

Trucial States Wood W. WilkinsonAnaheim Joseph C. Werba

Unated Kingdom Peter C. WrrghtAzusa

Vice President andGeneral Manager

Bakersfield

WELLS FARGO BANKBeverly HillsCosta Mesa

INTERNATIONAL SOUTHERN CALIFORNIA Lakewood WELLSCO DATA CORP.40 Wall Street HEADQUARTERS Long BeachNew York. New York 10005 44 Montgomery Street

415 West Fifth Street LOS ANGELES (10): San Francisco, California 94104Charles E. Lillen Los Angeles, California 90054 Century CityExecutive Vice President

Encino

John R. Breeden Hollywood Robert L. KemperPresidentVICE PRESIDENTS: Executive Vice President Miracle Mile

Wilham F. Boland Panorama City

George J. Hawkins SE;NIOR VICE PRESIDENTS Pershing Square VICE PRESIDENTS.

Nikita D. LobanovJohn H. Griffith

Tujunga Wilham P. StritzlerNorman Y Tao

W James RobertsonWestchester Peter L. OvermlreWlish re-Shatto PlaceWoodland Hills

WELLS FARGOVICE PRESIDENTS' Oak View

INTERNATIONAL INVESTMENT George L. Schindler Orcult WELLS FARGO

CORPORATION D. Guy Gibb Pasadena REALTV ADVISORS

420 Montgomery Street John A. Held Pomona Airport Imperial TowersSan FrancIsco, California 94104 H. Dale Meredith San BernardinO 909 SepUlveda, Suite 1100

Glenn C. Bassell, Jr. John M. Pitman San Manno EI Segundo, California 90245PreSident Henry J. Powell, Jr. Santa Ana

Arthur A. Schwalge Santa Maria Carl E. ReichardtJohn K Snyder Santa Monica PreSident

WELLS FARGO Andrew H. Stone South Pasadena

INTERAMERICAN BANK TorranceSENIOR VICE PRESIDENTS:

1111 South Bayshore Drive VENTURA (2)Miami. Florida 33t3t CORPORATE BANKING Ventura Paul Hazen

Thomas J. Carter DIVISION College View Daniel M. Ardell

Executive Vice PreSident Vernon

VICE PRESIDENTS West Covina VICE PRESIDENTS:

William G. BrockWhittier

Jerry L. CalfeeWELLS FARGO LTD. James C. Barrett, Jr. Peter L. RheinWinchester House Eugene D. Bishop Donald A. Ring80 London Wall Robert D. BivinsLondon. England SAN DIEGO BRANCH Whylle Somers

Robert T. Collie DIVISIONClive R. Sanders L. Eugene HollowayManaging Director

John E. LindstedtRobert M. O'Neill VICE PRESIDENTS: WELLS FARGO

VICE PRESIDENTS'Maunce D. Berchdorf

INVESTMENT COMPANY

WIlliam F. Adam James F. Anderson 475 Sansome StreetGeorge H. Hoffman, Jr SOUTHERN CALIFORNIA Edward E, Grimm San Francisco, California 94111

BRANCH DIVISION Andrew J. SiordlaLowell W. Sutherland Leonard Marks Jr

NATIONAL DiVISION VICE PRESIDENTS. PreSident

Robert F. Smith James R. Gibson Robert G. PerringSen or Vice PreSident Hamson J. BradleyOFFICES:

Vice Presldenl andKenneth C. Carlson Chula Vista Secretary-Treasurer

VICE PRESIDENTS. Richard H. Clark Et CajonHarold B. Bray, Jr. Norman G. Eckles HoltvilleJohn Z. Bulkeley Richard P. Feldmlller La Mesa

WELLS FARGOJackson Eaves George H. Grandstaff SAN DIEGO (3):Theodore W. Flnkbohner Thomas B. Lathrop San Diego LEASING CORPORATION

Frederick D. Greenley Gene R. Ley La Jolla 425 California StreetHubert W. Hitchcock Harry L. Maynard Mission Valley San Francisco, California 94104

40

"