1 Report No: AUS0000215 . Western Africa ECOWAS Regional Communications: Toward Integration of Infrastructure and Services . August 13, 2018 . Digital Development Department . Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

All queries on rights and licenses, including subsidiary rights, should be addressed to World Bank Publications, The World Bank Group, 1818 H Street NW, Washington, DC 20433, USA; fax: 202-522-2625; e-mail: [email protected].

Executive Summary Advancements in the provision of communications and data services are providing the West Africa region

with new approaches not only for people to communicate and access information, but also for the

facilitation of trade, financial transactions, and service delivery (such as entertainment, digital learning,

and telemedicine). The digital space is becoming an industry in its own right, disrupting traditional

business models and providing new economic opportunities, especially for youth. A new dimension of

regional integration and pathway for the regional digital economy is fast emerging.

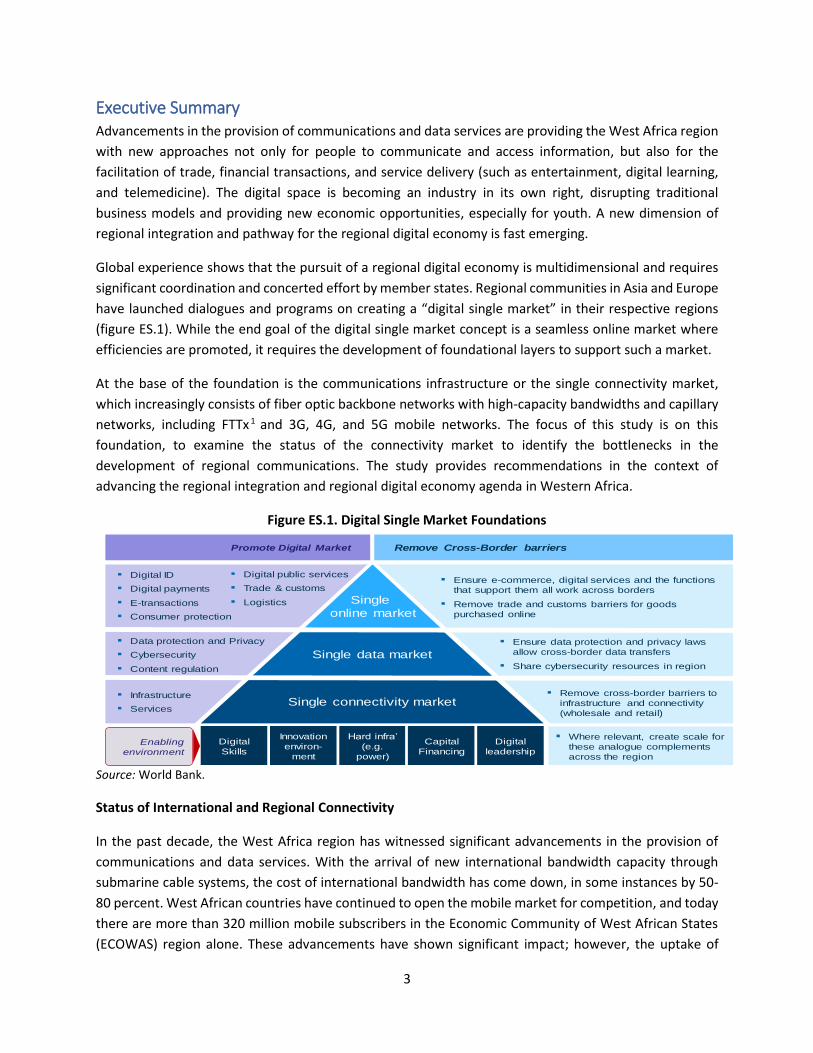

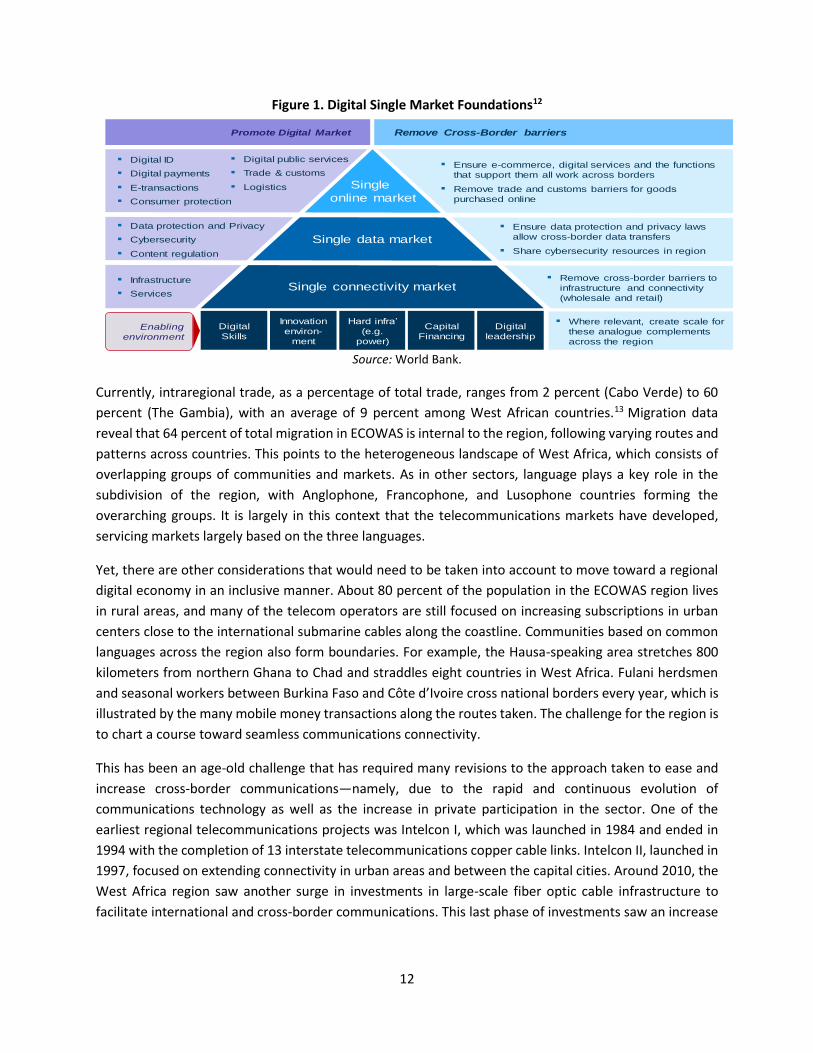

Global experience shows that the pursuit of a regional digital economy is multidimensional and requires

significant coordination and concerted effort by member states. Regional communities in Asia and Europe

have launched dialogues and programs on creating a “digital single market” in their respective regions

(figure ES.1). While the end goal of the digital single market concept is a seamless online market where

efficiencies are promoted, it requires the development of foundational layers to support such a market.

At the base of the foundation is the communications infrastructure or the single connectivity market,

which increasingly consists of fiber optic backbone networks with high-capacity bandwidths and capillary

networks, including FTTx 1 and 3G, 4G, and 5G mobile networks. The focus of this study is on this

foundation, to examine the status of the connectivity market to identify the bottlenecks in the

development of regional communications. The study provides recommendations in the context of

advancing the regional integration and regional digital economy agenda in Western Africa.

Figure ES.1. Digital Single Market Foundations

Source: World Bank.

Status of International and Regional Connectivity

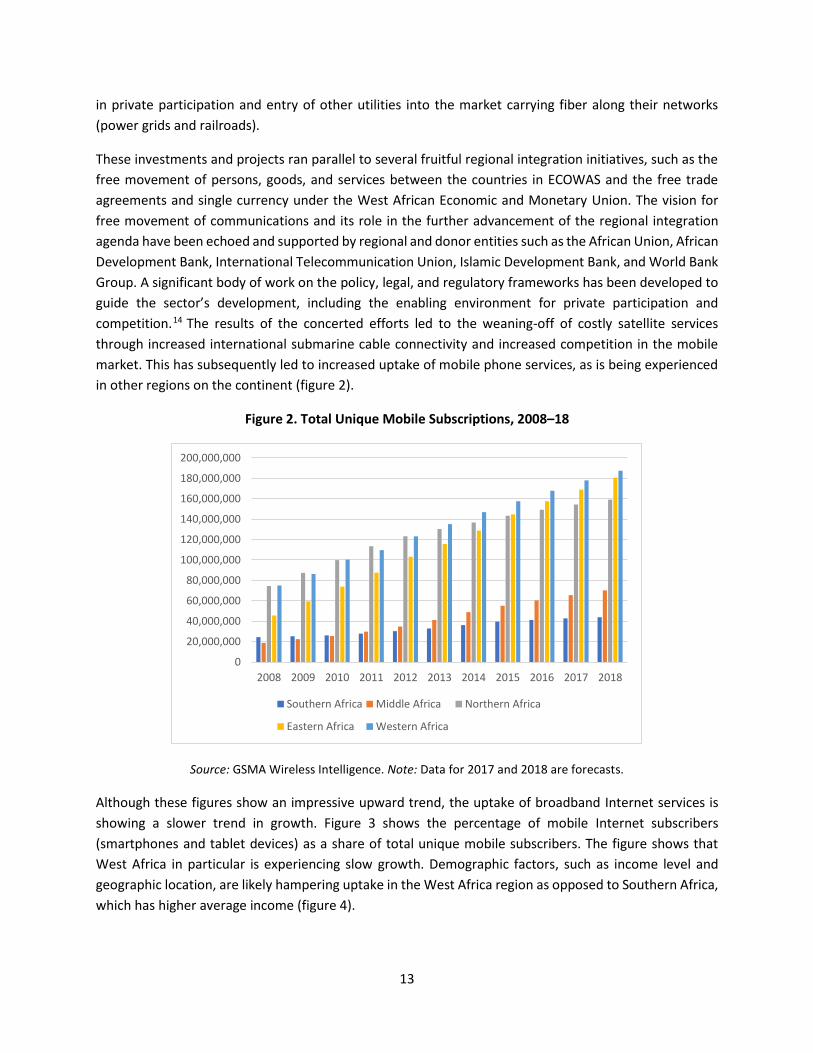

In the past decade, the West Africa region has witnessed significant advancements in the provision of

communications and data services. With the arrival of new international bandwidth capacity through

submarine cable systems, the cost of international bandwidth has come down, in some instances by 50-

80 percent. West African countries have continued to open the mobile market for competition, and today

there are more than 320 million mobile subscribers in the Economic Community of West African States

(ECOWAS) region alone. These advancements have shown significant impact; however, the uptake of

Single connectivity market

Single data market

Single

online market

▪ Ensure data protection and privacy laws

allow cross-border data transfers

▪ Share cybersecurity resources in region

▪ Remove cross-border barriers to

infrastructure and connectivity

(wholesale and retail)

Remove Cross-Border barriers

▪ Ensure e-commerce, digital services and the functions

that support them all work across borders

▪ Remove trade and customs barriers for goods

purchased online

Promote Digital Market

▪ Where relevant, create scale for

these analogue complements

across the region

▪ Digital ID

▪ Digital payments

▪ E-transactions

▪ Consumer protection

▪ Data protection and Privacy

▪ Cybersecurity

▪ Content regulation

▪ Infrastructure

▪ Services

Digital

Skills

Innovation

environ-

ment

Hard infra’

(e.g.

power)

Capital

FinancingEnabling

environment

Digital

leadership

▪ Digital public services

▪ Trade & customs

▪ Logistics

4

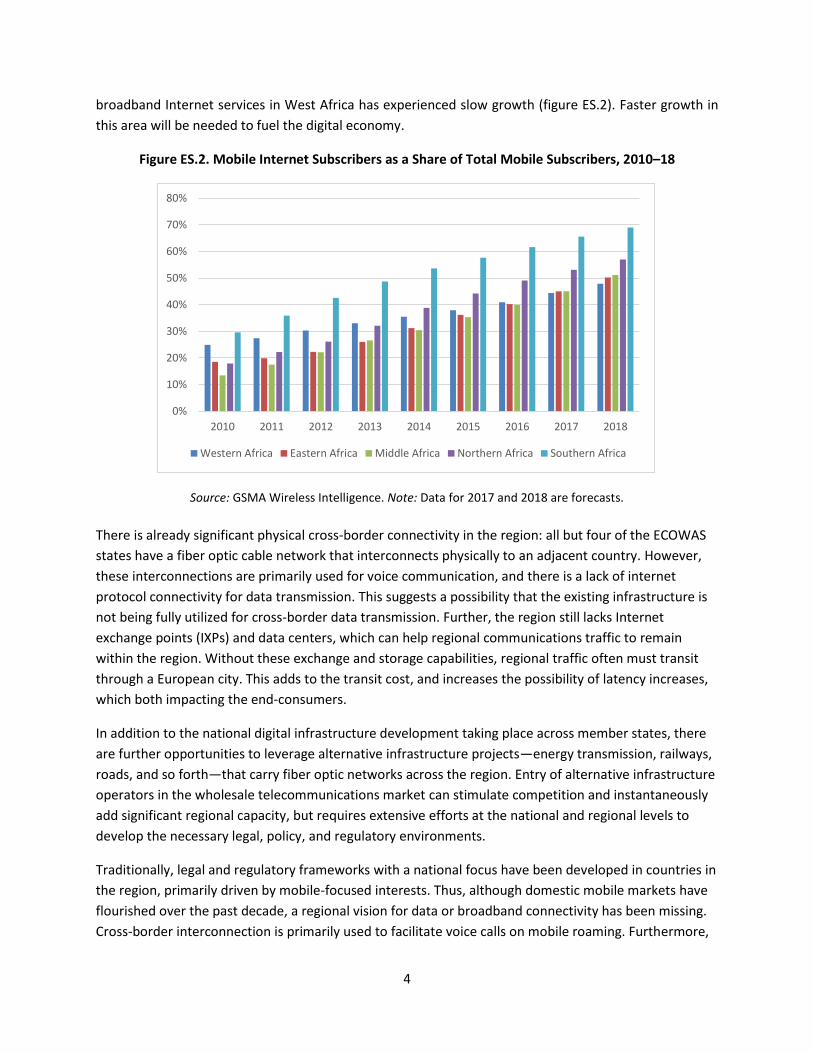

broadband Internet services in West Africa has experienced slow growth (figure ES.2). Faster growth in

this area will be needed to fuel the digital economy.

Figure ES.2. Mobile Internet Subscribers as a Share of Total Mobile Subscribers, 2010–18

Source: GSMA Wireless Intelligence. Note: Data for 2017 and 2018 are forecasts.

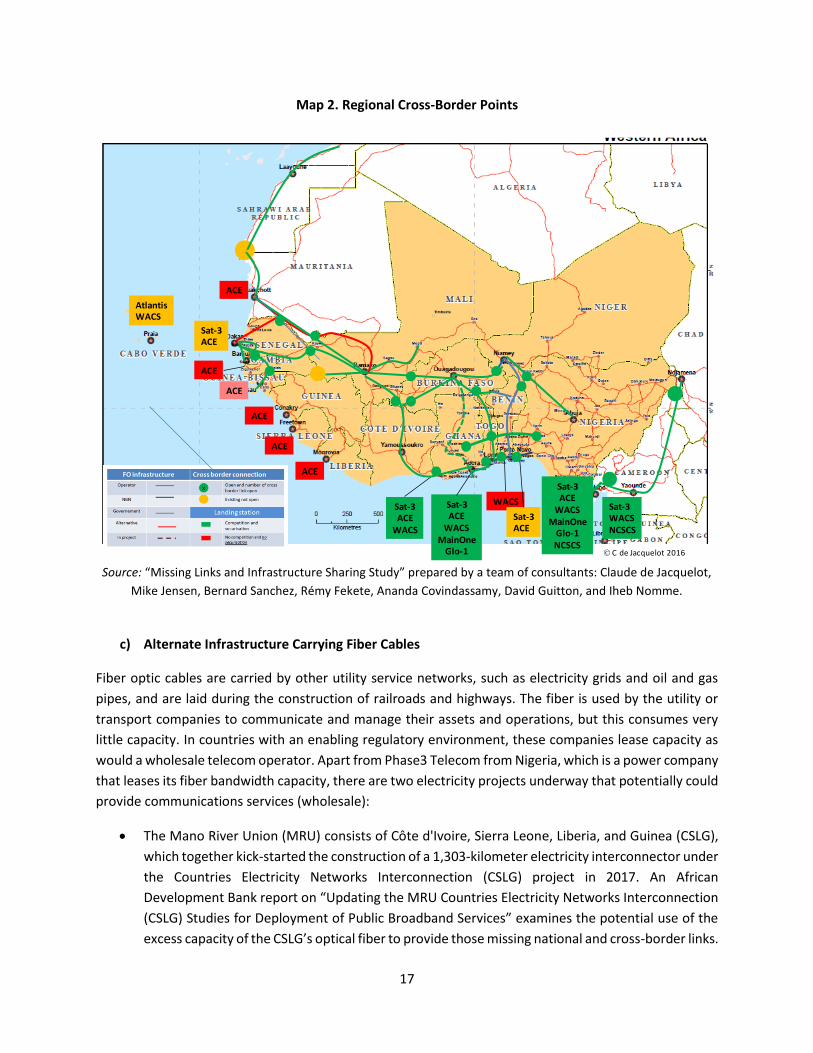

There is already significant physical cross-border connectivity in the region: all but four of the ECOWAS

states have a fiber optic cable network that interconnects physically to an adjacent country. However,

these interconnections are primarily used for voice communication, and there is a lack of internet

protocol connectivity for data transmission. This suggests a possibility that the existing infrastructure is

not being fully utilized for cross-border data transmission. Further, the region still lacks Internet

exchange points (IXPs) and data centers, which can help regional communications traffic to remain

within the region. Without these exchange and storage capabilities, regional traffic often must transit

through a European city. This adds to the transit cost, and increases the possibility of latency increases,

which both impacting the end-consumers.

In addition to the national digital infrastructure development taking place across member states, there

are further opportunities to leverage alternative infrastructure projects—energy transmission, railways,

roads, and so forth—that carry fiber optic networks across the region. Entry of alternative infrastructure

operators in the wholesale telecommunications market can stimulate competition and instantaneously

add significant regional capacity, but requires extensive efforts at the national and regional levels to

develop the necessary legal, policy, and regulatory environments.

Traditionally, legal and regulatory frameworks with a national focus have been developed in countries in

the region, primarily driven by mobile-focused interests. Thus, although domestic mobile markets have

flourished over the past decade, a regional vision for data or broadband connectivity has been missing.

Cross-border interconnection is primarily used to facilitate voice calls on mobile roaming. Furthermore,

0%

10%

20%

30%

40%

50%

60%

70%

80%

2010 2011 2012 2013 2014 2015 2016 2017 2018

Western Africa Eastern Africa Middle Africa Northern Africa Southern Africa

5

there is limited competition, with four pan-regional operators in West Africa that offer wholesale

services in the West Africa region and about 10 other providers that provide limited cross-border

connectivity. Due to the geographic size of the region, there is little overlap of the networks; hence, they

consist of clusters of single-operator markets. There are several regulatory bottlenecks to regional

communications:

• Regional licensing of operators. Currently in the ECOWAS region, an operator licensed or

authorized as an operator in a member state is not recognized in other member states.

• Open access policy, especially for dark fiber. Open and fair access policies for backbone

infrastructure running through a country and cross-border to another country are largely

missing.

• Infrastructure sharing and colocation. Specific regulations or guidelines for access to the core

network by other network operators are lacking. These include guidelines on sharing masts and

poles, spaces in buildings with termination and switching equipment, ducts and so on.

• Dispute resolution. In many ECOWAS member states, there are currently no specific provisions

allowing operators established in an ECOWAS member state to settle a dispute with an operator

in another member state.

Furthermore, the lack of a regional outlook to the development of the communications market in

ECOWAS has led to an absence of a framework for regional wholesale pricing. This is evidenced by the

limitation of Reference Interconnect Offers (RIO) to national operators only and no explicit offers for

access to cross-border interconnection points were found.

Low-Cost International Mobile Roaming: Boosting Consumer Welfare

The communications market in Africa still relies heavily on 2G voice services, constituting 55 percent of

total subscriptions, but this is projected to decline to 10 percent by 2023.2 Internationally, regional

economic communities have leveraged the digital sector to strengthen regional economic integration,

while also promoting consumer welfare through increasing the affordability of services, including the

reduction and eventual elimination of roaming charges.

A reduction or abolishment of roaming tariffs would constitute a reduction in operator revenues in the

medium term. However, it would create a large consumer surplus—by one estimation amounting to

US$775 million over the next four years for the region.3

Globally, regional roaming initiatives have been met with varying degrees of success and have followed

different approaches. However, a common outcome across all initiatives is a significant increase in

roaming usage, which can be seen as an indicator of the consumer surplus. In Kenya, for example, the

volume of calls went up by 264 percent when regional roaming rates were abolished.4

There are a total of 21 mobile operators in the ECOWAS region serving the 320 million subscribers, with a high degree of market concentration between the top 5 operators. Roaming prices offered by operators in the region are highly heterogeneous across countries, operators and visited countries, varying by over 10 times for the same type of voice call, depending on the roaming location for subscribers of the same home network. The same spread is also observed for data traffic with the price of 1 MB of roaming data

6

usage varying from US$ 0.08 (MTN Liberia within the MTN zone) to US$ 60 (Airtel Ghana roaming in Senegal).

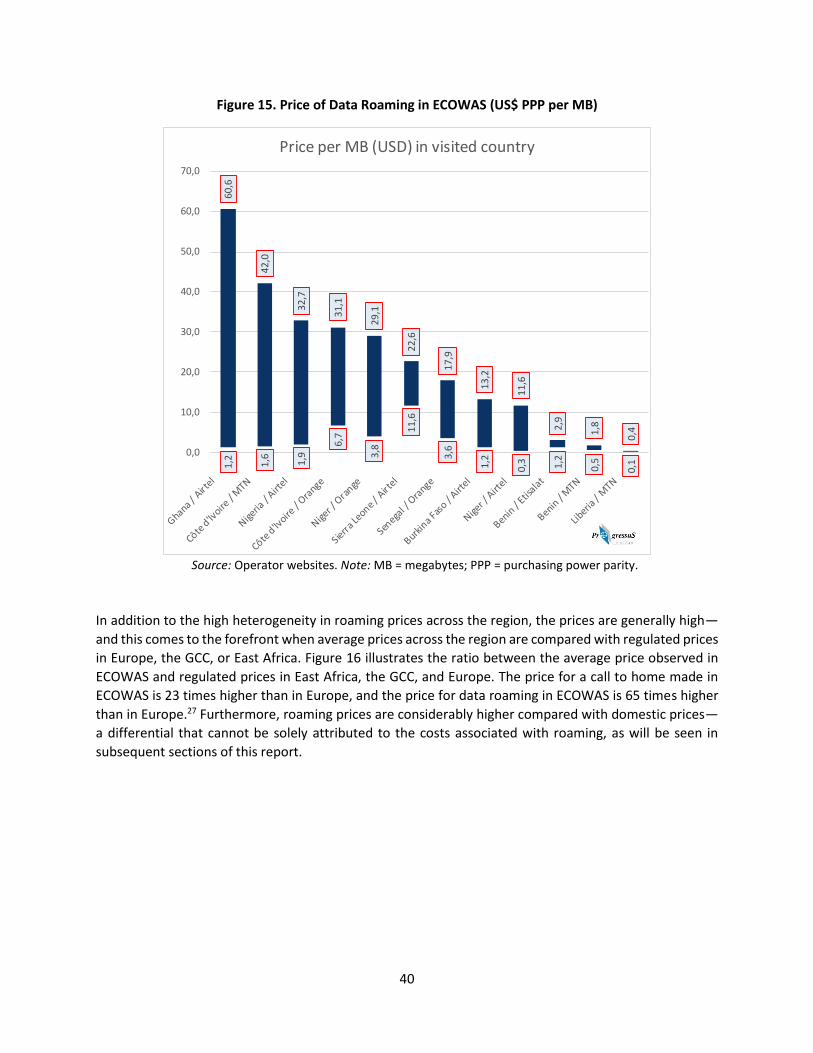

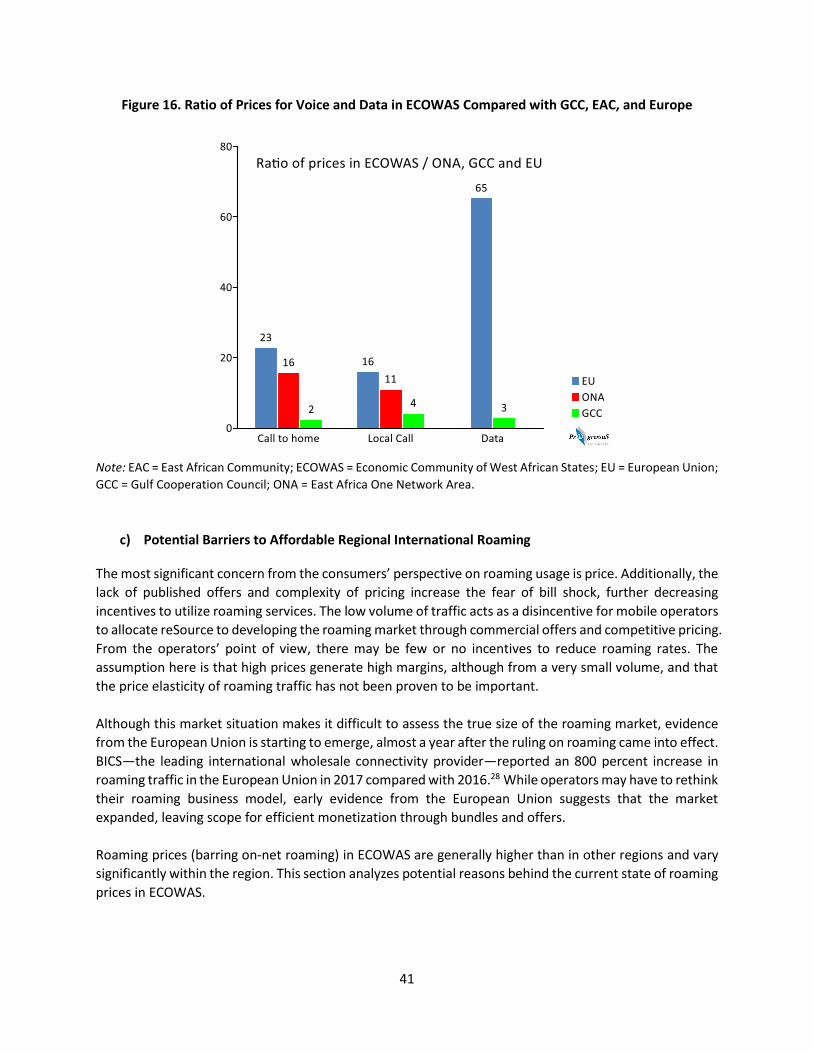

In addition to the high heterogeneity in roaming prices across the region, the prices are generally high—

in absolute terms - and this comes to the forefront when average prices across the region are compared

with regulated prices in Europe, the Gulf Cooperation Council, or East Africa. The price for a call to home

made in ECOWAS is 23 times higher than in Europe, and that for data roaming in ECOWAS is 65 times

higher than in Europe.5 Furthermore, roaming prices are considerably higher when compared to domestic

prices, a differential that cannot be solely attributed to costs associated with roaming.

The wholesale markets in the region display similar trends as the retail markets. The roaming market is

comprised of retail and wholesale components, at the domestic and international levels. In addition to

operating costs, such as network and signaling costs, a roaming call incurs certain tariffs, which are high

compared with those in other regions and vary significantly within the region.

Roaming regulation aims to develop the retail market to maximize utility for consumers and profit for

operators. However, other aspects, such as incentives to invest or eliminating fraud and arbitrage that

can arise in international traffic, should be considered as well. The evolution of international roaming in

four regions shows broadly two approaches:

• Voluntary, private sector–led models in East and Southern Africa

• Purely regulated models in the European Union and six Gulf Cooperation Council countries.6

Some of these measures may be taken unilaterally by a single country; others may be implemented

between two or more countries7 or applicable within a regional economic community. Examples of the

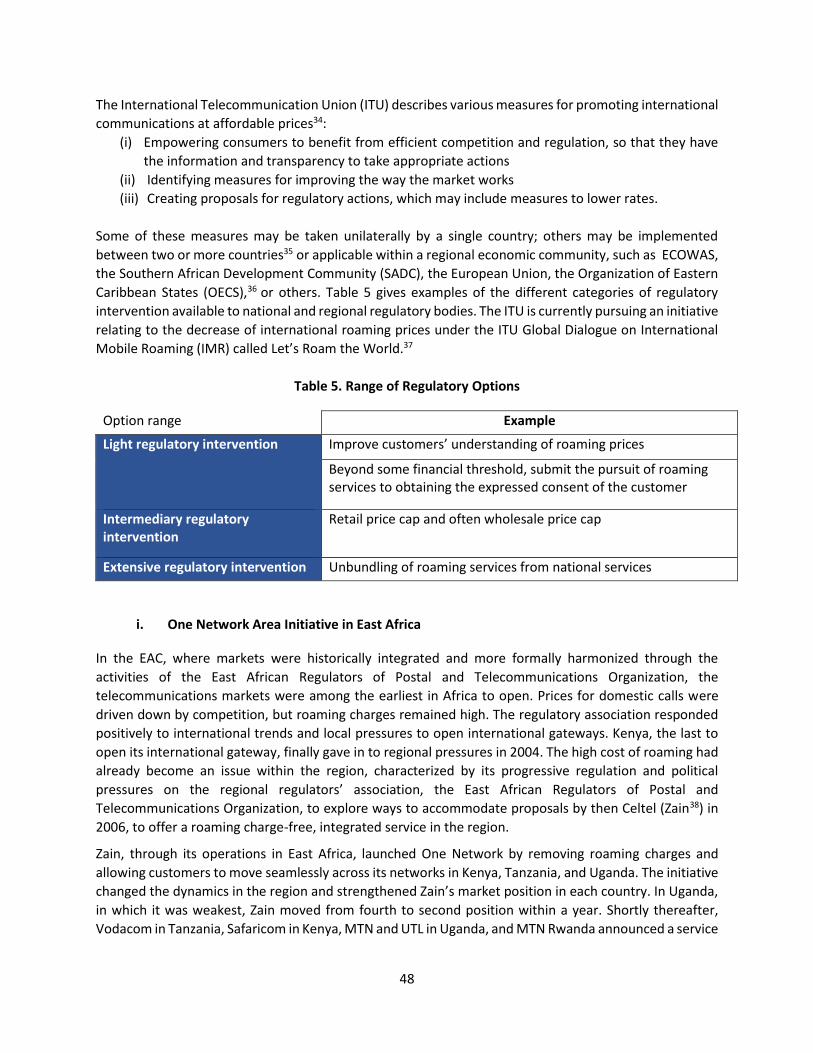

different categories of regulatory intervention available to national and regional regulatory bodies are

noted in table ES.1. The International Telecommunication Union is currently pursuing an initiative relating

to the decrease of international roaming prices under the ITU Global Dialogue on International Mobile

Roaming—Let’s Roam the World.8

Table ES.1. Range of regulatory options

Option range Example

Light regulatory intervention Improve customers’ understanding of roaming prices

Beyond some financial threshold, submit the pursuit of roaming services to obtaining the expressed consent of the customer

Intermediary regulatory intervention

Retail price cap and often wholesale price cap

Extensive regulatory intervention Unbundling of roaming services from national services

7

Recommendations and Conclusions

Economies of scale and network effects are critical for driving the growth of the digital economy,

starting from telecommunications infrastructure and services. This is particularly pertinent for several of

the ECOWAS countries that are too small in isolation to pursue development of a digital economy. And

most individuals in the ECOWAS region remain disconnected from the Internet. In addition to the large

size of the region, its inherent heterogeneity further increases the importance of developing subregional

linkages. For example, the West African Economic and Monetary Union offers an opportunity for a

subset of ECOWAS member states to forge stronger partnerships in developing their digital economies.

Yet, there are overarching principles to which all countries should adhere, including on their borders:

• Regional licensing. The shift from national to regional licenses for operators, including

alternative utility and transport operators, could accelerate regional expansion and potentially

draw more competition into parts of the region.

• Liberalization and competition. There are likely to be instances where there will be natural

monopolies, particularly the long-distance wholesale providers (or carrier’s carrier). The region

currently lacks frameworks for competition policy and significant market power regulation,

which has led to a situation where dominant behavior is largely left unchecked.

• Open access and infrastructure sharing. Policies and regulations that promote the use and

sharing of infrastructure, including infrastructure sharing, rights of way, and colocation, would

encourage efficient use of infrastructure and allow smaller operators to participate in cross-

border communications. This would also include the alternative infrastructure providers.

• Transparency of tariff information. Increasing the visibility of retail prices would protect

consumers from bill shock and could encourage the use of cross-border communications.

Transparency of wholesale prices (reference interconnection offers) together with the other

open access principles could be catalytic for the efficient utilization of infrastructure.

• Harmonization of sector laws, policies and regulation: Adopting a regional outlook to digital

infrastructure, as well as services such as mobile roaming, requires harmonization of the sector

across the region. This first entails addressing underlying inefficiencies in national markets.

• Aggregation and localization of content. In parallel to easing voice and data traffic across

borders, the region would benefit from keeping regional traffic regional. Even countries that do

not have robust and secure data infrastructure, such as IXPs and data centers, could host their

content in another country in the region that has these capabilities.

• Capacity building of regulators. The ECOWAS member states are on different rungs of the digital

economy ladder, much of which depends on the size of the market, but also the capacity of the

relevant institutions. The transposition of the regional supplementary acts, for example, can be

a complex process involving multiple agencies, laws, and regulations. Capacity building of

regulators and other agencies would be needed in areas such as licensing and pricing

regulations.

A collaborative approach to the digital economy would help deepen existing socioeconomic ties and

circumvent the potential widening of the digital divide between countries. The region has seen

8

significant investments in infrastructure, but further deployment is required to achieve universal

coverage objectives and reinforce the robustness of regional networks. The next challenge is to get the

enabling environment right for voice and data transmission across borders. This would lay the

foundation for producing digital content that is pertinent to the people and businesses of the West

Africa region—digital government services, financial services, entertainment, and innovation.

9

Abbreviations and Acronyms ACE African Coast to Europe ASN autonomous system number COMESA Common Market for Eastern and Southern Africa CSLG Côte d'Ivoire, Sierra Leone, Liberia, and Guinea Countries Electricity Networks

Interconnection CRASA Communications Regulators Association of Southern Africa EAC East African Community ECCAS Economic Community of Central African States ECOWAS Economic Community of West African States EU European Union GCC Gulf Cooperation Council ICT information and communications technology IMR international mobile roaming IOT inter-operator tariffs IP Internet protocol ITR international termination rate ITU International Telecommunication Union IXP Internet exchange point LTE Long-Term Evolution MB megabyte Mbps megabits per second MNO mobile network operator MoU memorandum of understanding MRU Mano River Union MTR mobile termination rate NCC Nigerian Communications Commission OECD Organisation for Economic Co-operation and Development OECS Organization of Eastern Caribbean States ONA One Network Area PPP purchasing power parity RIO reference interconnection offer RWG Roaming Working Group SADC Southern African Development Community SAT-3/WASC South Atlantic 3/West Africa Submarine Cable SMP significant market power SMS short message service UMA Arab Maghreb Union WAEMU West African Economic and Monetary Union

10

Table of Contents

Contents Page No.

I. Introduction 11

II. Status of International and Regional Connectivity 15

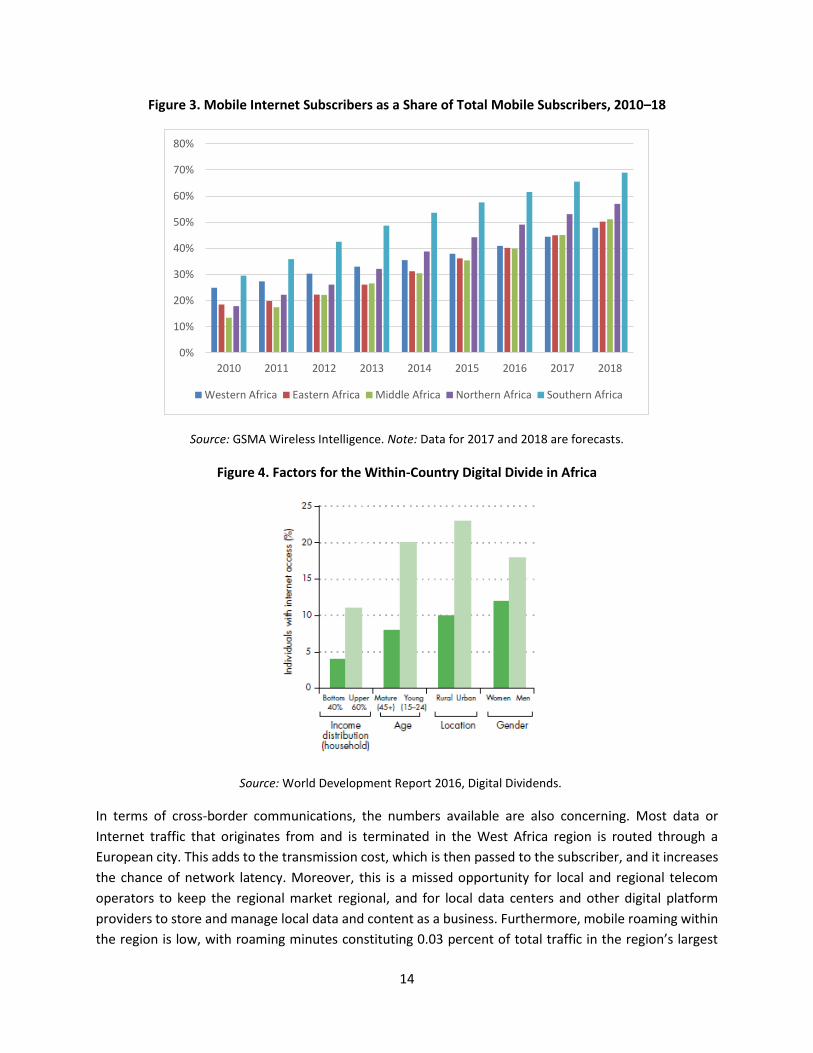

Figure 3. Mobile Internet Subscribers as a Share of Total Mobile Subscribers, 2010–18

Source: GSMA Wireless Intelligence. Note: Data for 2017 and 2018 are forecasts.

Figure 4. Factors for the Within-Country Digital Divide in Africa

Source: World Development Report 2016, Digital Dividends.

In terms of cross-border communications, the numbers available are also concerning. Most data or

Internet traffic that originates from and is terminated in the West Africa region is routed through a

European city. This adds to the transmission cost, which is then passed to the subscriber, and it increases

the chance of network latency. Moreover, this is a missed opportunity for local and regional telecom

operators to keep the regional market regional, and for local data centers and other digital platform

providers to store and manage local data and content as a business. Furthermore, mobile roaming within

the region is low, with roaming minutes constituting 0.03 percent of total traffic in the region’s largest

0%

10%

20%

30%

40%

50%

60%

70%

80%

2010 2011 2012 2013 2014 2015 2016 2017 2018

Western Africa Eastern Africa Middle Africa Northern Africa Southern Africa

15

market, Nigeria. The reasons for this may include limited social and economic activity at some of the

national borders, but an evident challenge is the high price of roaming charges, which can lead to “bill

shock” when the subscriber has a negative reaction if their phone bill has unexpected charges. This

situation is symptomatic of the lack of a regionally focused policy framework that would address the

bottlenecks to the cross-border use of the infrastructure and provision of services. Other regional

experiences, such as in the European Union and Arabian Peninsula, have shown that the pursuit of an

integrated communications market is a long one, but real impact is observed at each milestone.

Based on the aspirations of West African regional bodies to move toward a single connectivity market and

subsequently a regional digital economy, this study aims to identify the key bottlenecks in the

development of regional communications. The study focuses on two segments of the communications

value chain, starting with the wholesale backbone networks that carry traffic across borders and then

examining the status of the regional roaming market to assess how roaming fees affect cross-border

communications. Various aspects across the value chain (for example, tariffs and taxation) can also affect

other segments; hence, the study tries to identify those symptomatic issues that stem from the broader

sectoral challenges. The study draws from studies funded by the Public-Private Infrastructure Advisory

Facility15 that were conducted upon the request of the ECOWAS Commission. Although the data and

analysis focus on the ECOWAS member states, the recommendations reflect the needs of the wider West

Africa region.

II. Status of International and Regional Connectivity

a) International Connectivity

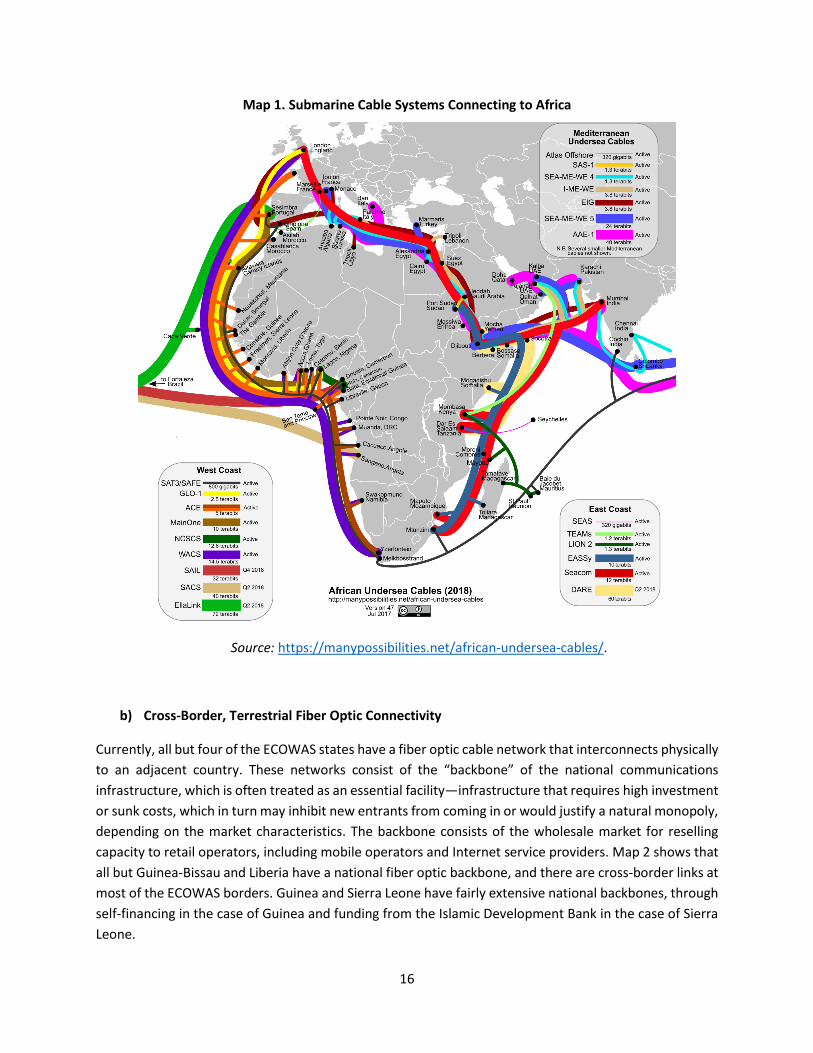

For international connectivity, all coastal countries in the ECOWAS region, except Guinea-Bissau, are served by international submarine fiber optic cable connections. Submarine cables are usually owned by a consortium of operators, with one or two large operators entrusted to manage and maintain the cable system. West Africa is largely connected through three consortiums, the South Atlantic 3/West Africa Submarine Cable (SAT-3/WASC),16 which became operational in 2001; Nigeria’s Main One17 cable system, which became operational in 2010; and the Orange/France Telecom–led African Coast to Europe (ACE)18 cable system, which first became operational in 2012. Burkina Faso, Mali, and Niger, being landlocked, do not have direct access to a submarine cable landing station. Currently, Mali and Niger are connected to the ACE cable system through Orange, and further backbone deployment is underway for Burkina Faso to connect to ACE.

In telecommunications, whether submarine or terrestrial, it is important to have options to route through several cable systems (redundant networks) in the event of a cable outage (map 1). Outages have been reported in West African countries in the past several years, which has left countries that have access to only one submarine cable system in a communications blackout, at times spanning a few days or a couple of weeks. Ghana, Côte d'Ivoire, and Nigeria have secure access to multiple submarine cable systems; Senegal is in a vulnerable position, as its alternate route includes an older generation of cable systems provided by SAT-3/WASC and Atlantis-II. Six countries do not have alternate submarine routes or competitive landing points, including Guinea, Guinea-Bissau, Liberia, Sierra Leone, The Gambia, and Togo. There is therefore a need to develop redundancy and competition for access to submarine cable systems to ensure reliable international connectivity.

16

Map 1. Submarine Cable Systems Connecting to Africa

Source: “Missing Links and Infrastructure Sharing Study” prepared by a team of consultants: Claude de Jacquelot,

Mike Jensen, Bernard Sanchez, Rémy Fekete, Ananda Covindassamy, David Guitton, and Iheb Nomme.

c) Alternate Infrastructure Carrying Fiber Cables

Fiber optic cables are carried by other utility service networks, such as electricity grids and oil and gas

pipes, and are laid during the construction of railroads and highways. The fiber is used by the utility or

transport companies to communicate and manage their assets and operations, but this consumes very

little capacity. In countries with an enabling regulatory environment, these companies lease capacity as

would a wholesale telecom operator. Apart from Phase3 Telecom from Nigeria, which is a power company

that leases its fiber bandwidth capacity, there are two electricity projects underway that potentially could

provide communications services (wholesale):

• The Mano River Union (MRU) consists of Côte d'Ivoire, Sierra Leone, Liberia, and Guinea (CSLG),

which together kick-started the construction of a 1,303-kilometer electricity interconnector under

the Countries Electricity Networks Interconnection (CSLG) project in 2017. An African

Development Bank report on “Updating the MRU Countries Electricity Networks Interconnection

(CSLG) Studies for Deployment of Public Broadband Services” examines the potential use of the

excess capacity of the CSLG’s optical fiber to provide those missing national and cross-border links.

ACE

ACE

Sat-3ACE

WACS

Sat-3ACE

ACE

ACE

ACE

WACS

Sat-3ACE

Sat-3ACE

WACSMainOne

Glo-1

Sat-3ACE

WACSMainOne

Glo-1NCSCS

Sat-3WACSNCSCS

ACE

C de Jacquelot 2016

AtlantisWACS

18

The report concludes that there is significant potential to use the CSLG power transport cables to

interconnect the four countries.

• The development objective of the Organisation pour la Mise en Valeur du fleuve Gambie (The

Gambia River Basin Development Organization) Interconnection Project for Africa is to enable

electricity trade between The Gambia, Guinea, Guinea-Bissau, and Senegal.

Furthermore, the Blue line rail, which aims to connect Abidjan-Ouagadougou-Niamey-Cotonou-Lomé and

the proposed fiber optic cable to follow the route of the Algeria-Nigeria-Chad Trans-Saharan Road (Route

Trans Saharienne), could provide redundancy networks to reinforce connectivity between the landlocked

countries. However, there are two bottlenecks for the mentioned projects. First, the region in general

lacks a regulatory and licensing framework for pan-regional operators, including alternative infrastructure

operators; hence, they are unable to participate as a wholesale provider in the countries they transit.

Second, in the case of the two electricity projects, the West Africa Power Pool Secretariat has yet to

develop a viable business model on how the extra fiber capacity would be utilized and marketed to

operators in the countries they will operate in as electricity providers. The related policy and regulatory

barriers are further examined in the following section.

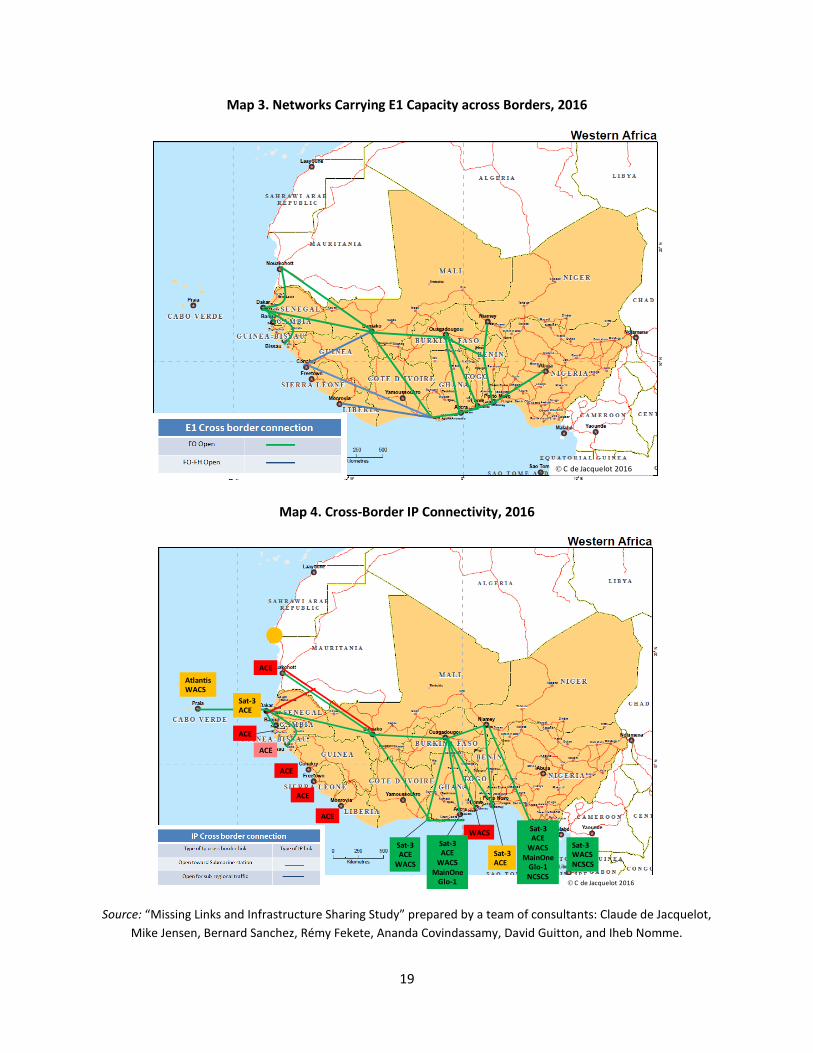

d) Low Development of Internet Protocol Connectivity and Local Content Hosting

Much of the communications traffic that is intended for another West African country first leaves the

region and transits through a European city before it reaches its destination back in the region. This adds

to the cost of the transmission, as it goes through an international or European service operator, which

can cause latency or time delay in signal exchange and is a missed opportunity for local and regional

operators to keep the regional market regional. The physical cross-border connectivity primarily carries

E1 cross-border links the are used by voice service providers, namely mobile operators, for international

connection and roaming. E1 links are configured to be dedicated to voice services and do not carry

enough bandwidth for the broadband Internet market. Map 3 shows the fiber optic cable or E1 capacity

that is open at the national borders allowing for cross-border voice communications.

The transmission of higher capacities (data or broadband speed Internet) across national borders is

usually not the responsibility of country policy, but is a commercial decision to enter an interconnection

agreement with another operator based on a “handshake.” This study found no formal arrangements

between any two ECOWAS countries to interconnect two main data or Internet protocol (IP) operators

whether it be telco operators, data centers, or other hosting businesses, indicating that the wholesale

operators are expanding their own infrastructure rather than entering interconnection agreements

(map 4). However, IP cross-border connectivity has been negotiated between landlocked countries and

their adjacent countries to facilitate traffic to and from the landlocked country to reach submarine cable

landing stations for international connectivity (Bamako, Ouagadougou, and Niamey).

19

Map 3. Networks Carrying E1 Capacity across Borders, 2016

Map 4. Cross-Border IP Connectivity, 2016

Source: “Missing Links and Infrastructure Sharing Study” prepared by a team of consultants: Claude de Jacquelot,

Mike Jensen, Bernard Sanchez, Rémy Fekete, Ananda Covindassamy, David Guitton, and Iheb Nomme.

C de Jacquelot 2016

ACE

ACE

Sat-3ACE

WACS

ACE

ACE

ACE

WACS

Sat-3ACE

Sat-3ACE

WACSMainOne

Glo-1

Sat-3ACE

WACSMainOne

Glo-1NCSCS

Sat-3WACSNCSCS

ACE

Sat-3ACE

AtlantisWACS

C de Jacquelot 2016

20

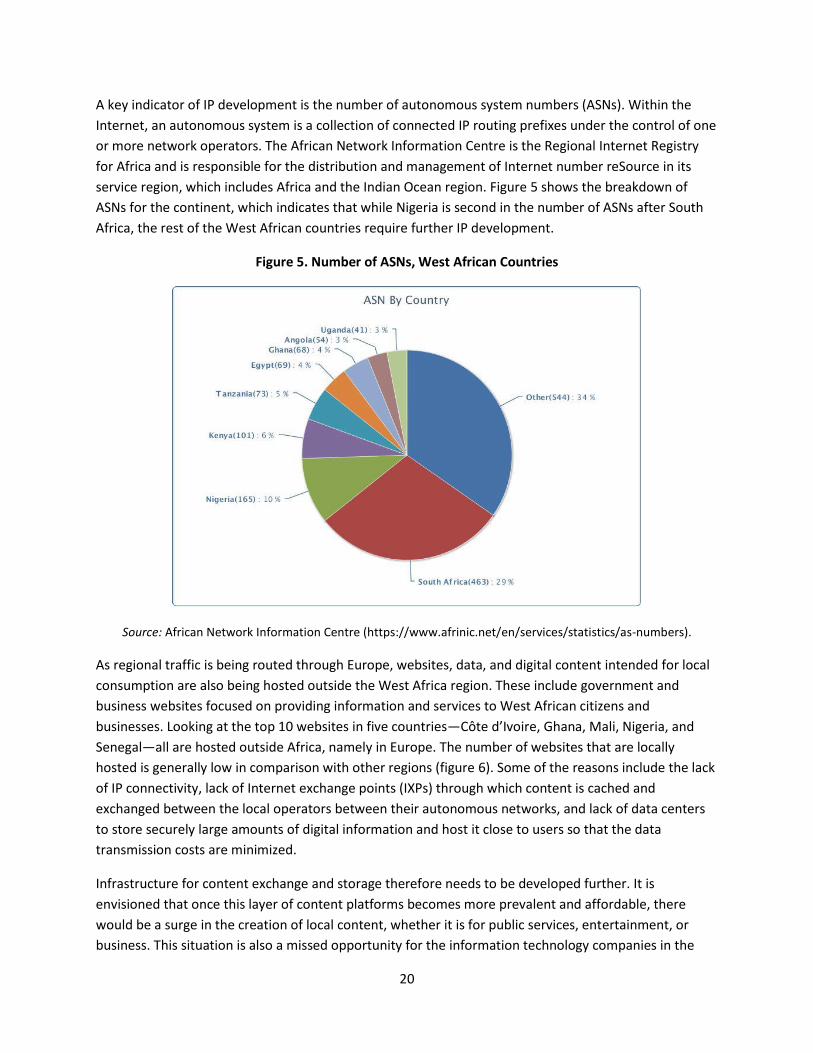

A key indicator of IP development is the number of autonomous system numbers (ASNs). Within the

Internet, an autonomous system is a collection of connected IP routing prefixes under the control of one

or more network operators. The African Network Information Centre is the Regional Internet Registry

for Africa and is responsible for the distribution and management of Internet number reSource in its

service region, which includes Africa and the Indian Ocean region. Figure 5 shows the breakdown of

ASNs for the continent, which indicates that while Nigeria is second in the number of ASNs after South

Africa, the rest of the West African countries require further IP development.

Figure 5. Number of ASNs, West African Countries

Source: African Network Information Centre (https://www.afrinic.net/en/services/statistics/as-numbers).

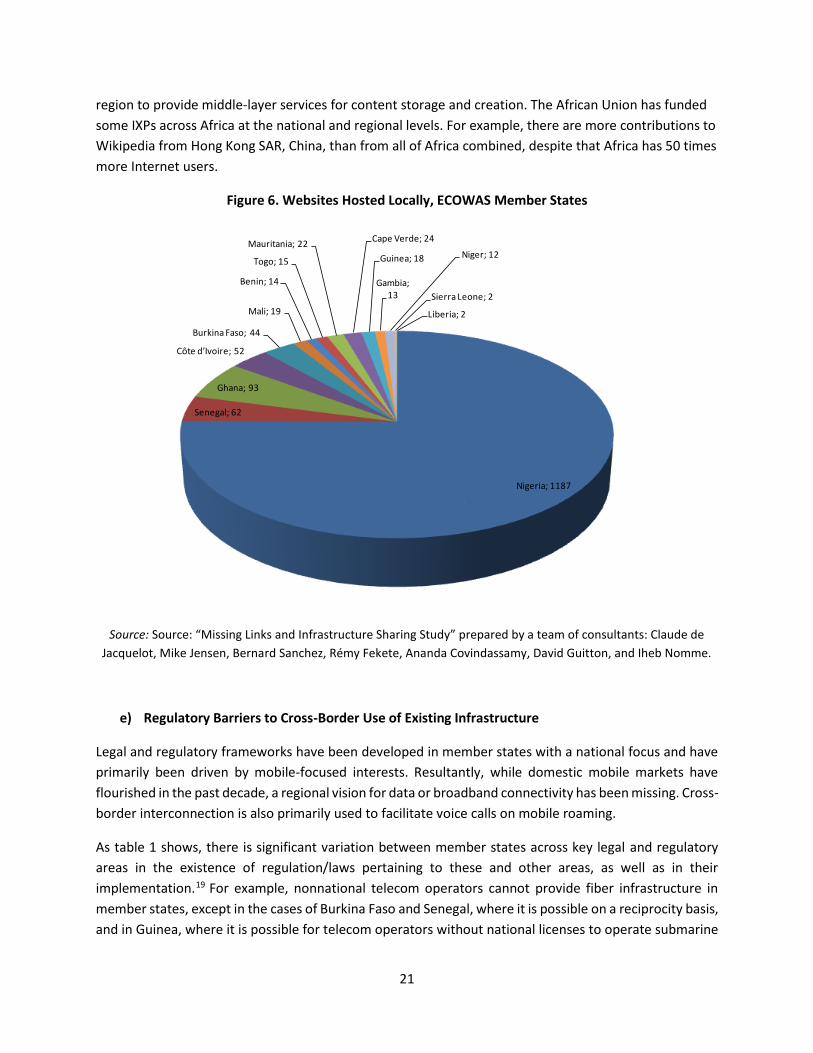

As regional traffic is being routed through Europe, websites, data, and digital content intended for local

consumption are also being hosted outside the West Africa region. These include government and

business websites focused on providing information and services to West African citizens and

businesses. Looking at the top 10 websites in five countries—Côte d’Ivoire, Ghana, Mali, Nigeria, and

Senegal—all are hosted outside Africa, namely in Europe. The number of websites that are locally

hosted is generally low in comparison with other regions (figure 6). Some of the reasons include the lack

of IP connectivity, lack of Internet exchange points (IXPs) through which content is cached and

exchanged between the local operators between their autonomous networks, and lack of data centers

to store securely large amounts of digital information and host it close to users so that the data

transmission costs are minimized.

Infrastructure for content exchange and storage therefore needs to be developed further. It is

envisioned that once this layer of content platforms becomes more prevalent and affordable, there

would be a surge in the creation of local content, whether it is for public services, entertainment, or

business. This situation is also a missed opportunity for the information technology companies in the

21

region to provide middle-layer services for content storage and creation. The African Union has funded

some IXPs across Africa at the national and regional levels. For example, there are more contributions to

Wikipedia from Hong Kong SAR, China, than from all of Africa combined, despite that Africa has 50 times

more Internet users.

Figure 6. Websites Hosted Locally, ECOWAS Member States

Source: Source: “Missing Links and Infrastructure Sharing Study” prepared by a team of consultants: Claude de

Jacquelot, Mike Jensen, Bernard Sanchez, Rémy Fekete, Ananda Covindassamy, David Guitton, and Iheb Nomme.

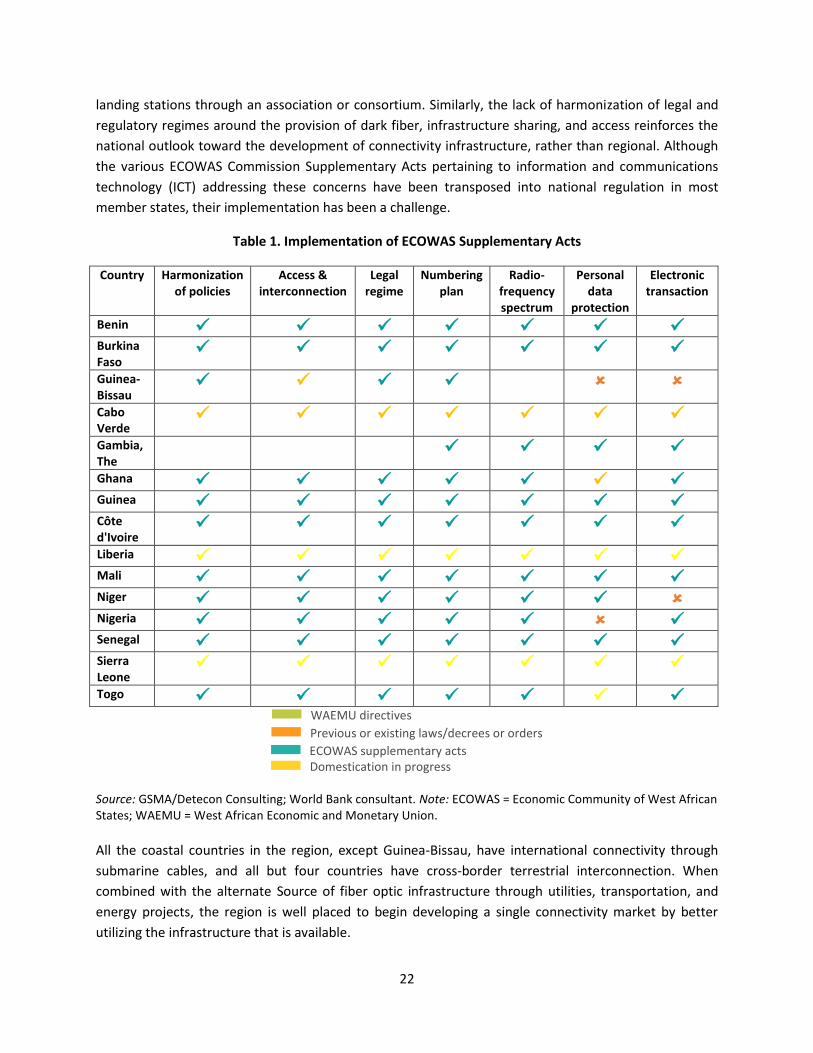

e) Regulatory Barriers to Cross-Border Use of Existing Infrastructure

Legal and regulatory frameworks have been developed in member states with a national focus and have

primarily been driven by mobile-focused interests. Resultantly, while domestic mobile markets have

flourished in the past decade, a regional vision for data or broadband connectivity has been missing. Cross-

border interconnection is also primarily used to facilitate voice calls on mobile roaming.

As table 1 shows, there is significant variation between member states across key legal and regulatory

areas in the existence of regulation/laws pertaining to these and other areas, as well as in their

implementation.19 For example, nonnational telecom operators cannot provide fiber infrastructure in

member states, except in the cases of Burkina Faso and Senegal, where it is possible on a reciprocity basis,

and in Guinea, where it is possible for telecom operators without national licenses to operate submarine

Nigeria; 1187

Senegal; 62

Ghana; 93

Côte d’Ivoire; 52

Burkina Faso; 44

Mali; 19

Benin; 14

Togo; 15

Mauritania; 22Cape Verde; 24

Guinea; 18

Gambia; 13

Niger; 12

Sierra Leone; 2

Liberia; 2

CEDEAO Nombre de sites Web hébergés (06 2016)

22

landing stations through an association or consortium. Similarly, the lack of harmonization of legal and

regulatory regimes around the provision of dark fiber, infrastructure sharing, and access reinforces the

national outlook toward the development of connectivity infrastructure, rather than regional. Although

the various ECOWAS Commission Supplementary Acts pertaining to information and communications

technology (ICT) addressing these concerns have been transposed into national regulation in most

member states, their implementation has been a challenge.

Table 1. Implementation of ECOWAS Supplementary Acts

Country Harmonization of policies

Access & interconnection

Legal regime

Numbering plan

Radio-frequency spectrum

Personal data

protection

Electronic transaction

Benin ✓ ✓ ✓ ✓ ✓ ✓ ✓

Burkina Faso

✓ ✓ ✓ ✓ ✓ ✓ ✓

Guinea-Bissau

✓ ✓ ✓ ✓

Cabo Verde

✓ ✓ ✓ ✓ ✓ ✓ ✓

Gambia, The

✓ ✓ ✓ ✓

Ghana ✓ ✓ ✓ ✓ ✓ ✓ ✓

Guinea ✓ ✓ ✓ ✓ ✓ ✓ ✓ Côte d'Ivoire

✓ ✓ ✓ ✓ ✓ ✓ ✓

Liberia ✓ ✓ ✓ ✓ ✓ ✓ ✓

Mali ✓ ✓ ✓ ✓ ✓ ✓ ✓

Niger ✓ ✓ ✓ ✓ ✓ ✓

Nigeria ✓ ✓ ✓ ✓ ✓ ✓

Senegal ✓ ✓ ✓ ✓ ✓ ✓ ✓

Sierra Leone

✓ ✓ ✓ ✓ ✓ ✓ ✓

Togo ✓ ✓ ✓ ✓ ✓ ✓ ✓

Source: GSMA/Detecon Consulting; World Bank consultant. Note: ECOWAS = Economic Community of West African States; WAEMU = West African Economic and Monetary Union.

All the coastal countries in the region, except Guinea-Bissau, have international connectivity through

submarine cables, and all but four countries have cross-border terrestrial interconnection. When

combined with the alternate Source of fiber optic infrastructure through utilities, transportation, and

energy projects, the region is well placed to begin developing a single connectivity market by better

utilizing the infrastructure that is available.

WAEMU directives Previous or existing laws/decrees or orders ECOWAS supplementary acts Domestication in progress

23

Increasingly, the bottleneck to the development of regional connectivity is not with infrastructure

constraints, but the lack of a regional framework of regulation and intergovernmental agreements. The

main shortcomings, which this section examines, are limited competition and cost effectiveness in the

supply of services. The following are the interrelated challenges for better infrastructure utilization at the

regional level:

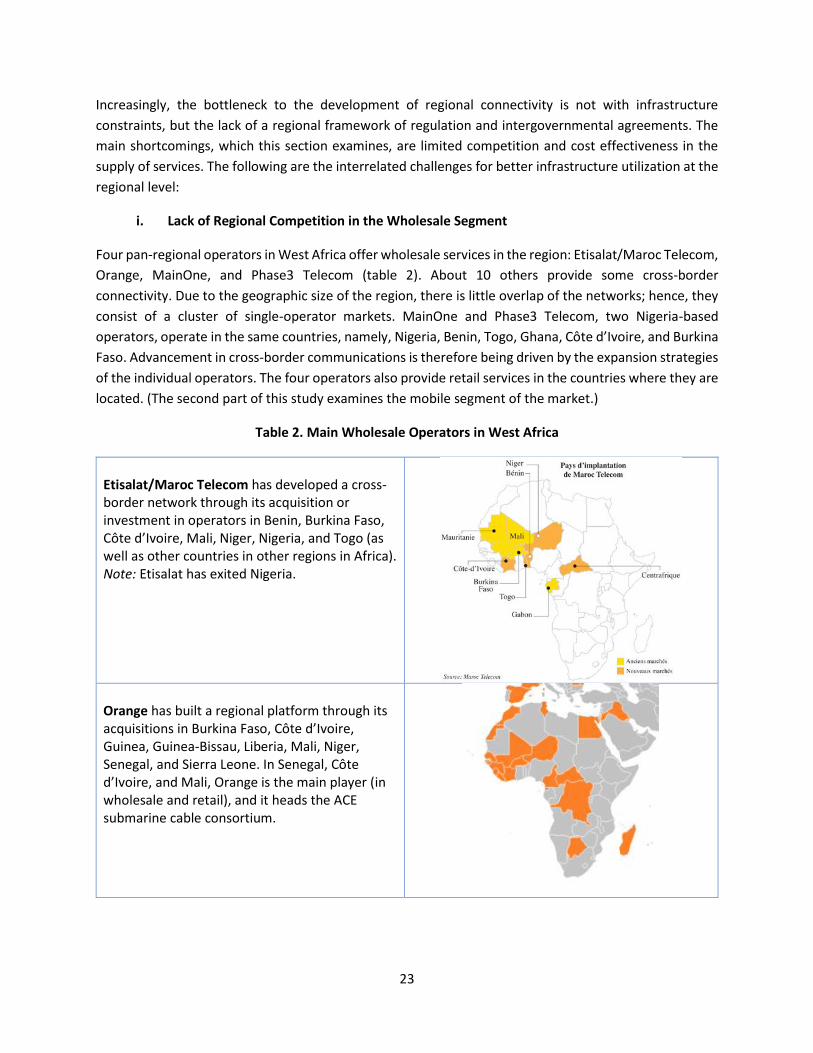

i. Lack of Regional Competition in the Wholesale Segment

Four pan-regional operators in West Africa offer wholesale services in the region: Etisalat/Maroc Telecom,

Orange, MainOne, and Phase3 Telecom (table 2). About 10 others provide some cross-border

connectivity. Due to the geographic size of the region, there is little overlap of the networks; hence, they

consist of a cluster of single-operator markets. MainOne and Phase3 Telecom, two Nigeria-based

operators, operate in the same countries, namely, Nigeria, Benin, Togo, Ghana, Côte d’Ivoire, and Burkina

Faso. Advancement in cross-border communications is therefore being driven by the expansion strategies

of the individual operators. The four operators also provide retail services in the countries where they are

located. (The second part of this study examines the mobile segment of the market.)

Table 2. Main Wholesale Operators in West Africa

Etisalat/Maroc Telecom has developed a cross-border network through its acquisition or investment in operators in Benin, Burkina Faso, Côte d’Ivoire, Mali, Niger, Nigeria, and Togo (as well as other countries in other regions in Africa). Note: Etisalat has exited Nigeria.

Orange has built a regional platform through its acquisitions in Burkina Faso, Côte d’Ivoire, Guinea, Guinea-Bissau, Liberia, Mali, Niger, Senegal, and Sierra Leone. In Senegal, Côte d’Ivoire, and Mali, Orange is the main player (in wholesale and retail), and it heads the ACE submarine cable consortium.

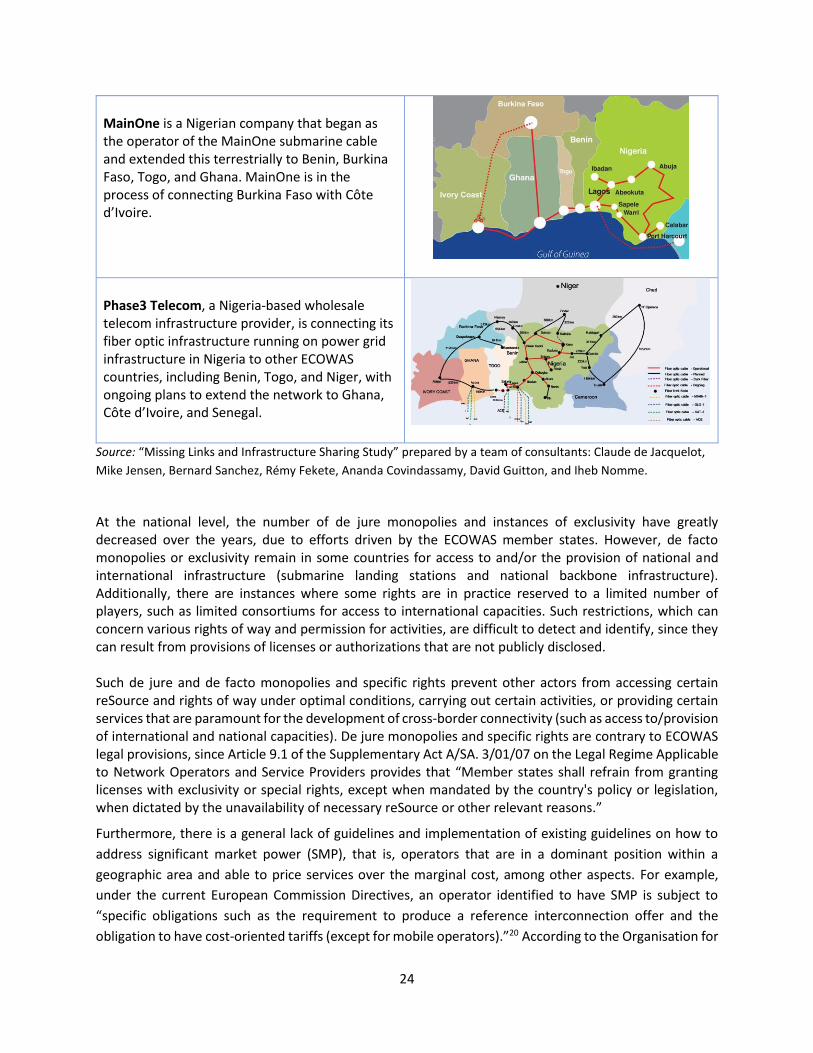

24

MainOne is a Nigerian company that began as the operator of the MainOne submarine cable and extended this terrestrially to Benin, Burkina Faso, Togo, and Ghana. MainOne is in the process of connecting Burkina Faso with Côte d’Ivoire.

Phase3 Telecom, a Nigeria-based wholesale telecom infrastructure provider, is connecting its fiber optic infrastructure running on power grid infrastructure in Nigeria to other ECOWAS countries, including Benin, Togo, and Niger, with ongoing plans to extend the network to Ghana, Côte d’Ivoire, and Senegal.

Source: “Missing Links and Infrastructure Sharing Study” prepared by a team of consultants: Claude de Jacquelot,

Mike Jensen, Bernard Sanchez, Rémy Fekete, Ananda Covindassamy, David Guitton, and Iheb Nomme.

At the national level, the number of de jure monopolies and instances of exclusivity have greatly decreased over the years, due to efforts driven by the ECOWAS member states. However, de facto monopolies or exclusivity remain in some countries for access to and/or the provision of national and international infrastructure (submarine landing stations and national backbone infrastructure). Additionally, there are instances where some rights are in practice reserved to a limited number of players, such as limited consortiums for access to international capacities. Such restrictions, which can concern various rights of way and permission for activities, are difficult to detect and identify, since they can result from provisions of licenses or authorizations that are not publicly disclosed. Such de jure and de facto monopolies and specific rights prevent other actors from accessing certain reSource and rights of way under optimal conditions, carrying out certain activities, or providing certain services that are paramount for the development of cross-border connectivity (such as access to/provision of international and national capacities). De jure monopolies and specific rights are contrary to ECOWAS legal provisions, since Article 9.1 of the Supplementary Act A/SA. 3/01/07 on the Legal Regime Applicable to Network Operators and Service Providers provides that “Member states shall refrain from granting licenses with exclusivity or special rights, except when mandated by the country's policy or legislation, when dictated by the unavailability of necessary reSource or other relevant reasons.”

Furthermore, there is a general lack of guidelines and implementation of existing guidelines on how to

address significant market power (SMP), that is, operators that are in a dominant position within a

geographic area and able to price services over the marginal cost, among other aspects. For example,

under the current European Commission Directives, an operator identified to have SMP is subject to

“specific obligations such as the requirement to produce a reference interconnection offer and the

obligation to have cost-oriented tariffs (except for mobile operators).”20 According to the Organisation for

25

Economic Co-operation and Development (OECD), an operator is presumed to have SMP if it has more

than 25 percent of a telecommunications market in the geographic area in which it is allowed to operate.21

Article 19.2 of the Supplementary Act A/SA. 2/01/07 on Access and Interconnection in Respect of ICT

Sector Networks and Services requires the ECOWAS Commission to publish (i) guidelines for market

analysis and assessment of market power and (ii) a recommendation on relevant markets in products and

services in the telecommunication sector that can be regulated ex ante. The wholesale market has a direct

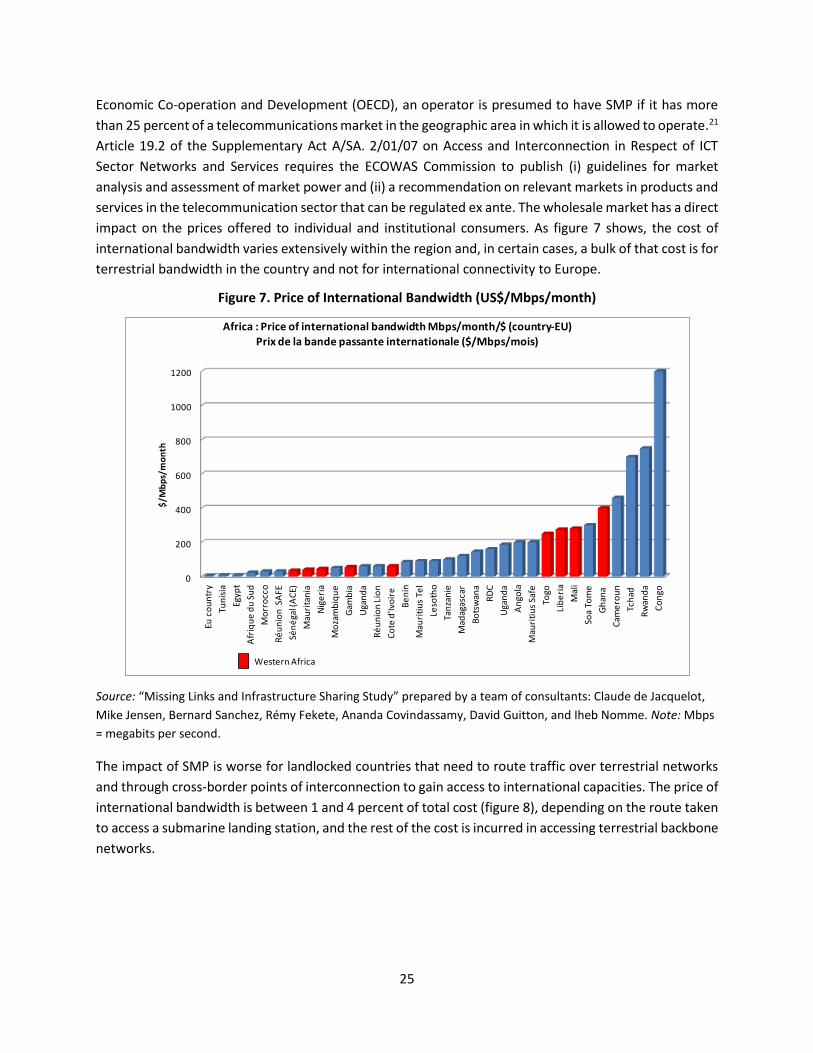

impact on the prices offered to individual and institutional consumers. As figure 7 shows, the cost of

international bandwidth varies extensively within the region and, in certain cases, a bulk of that cost is for

terrestrial bandwidth in the country and not for international connectivity to Europe.

Figure 7. Price of International Bandwidth (US$/Mbps/month)

Source: “Missing Links and Infrastructure Sharing Study” prepared by a team of consultants: Claude de Jacquelot,

Mike Jensen, Bernard Sanchez, Rémy Fekete, Ananda Covindassamy, David Guitton, and Iheb Nomme. Note: Mbps

= megabits per second.

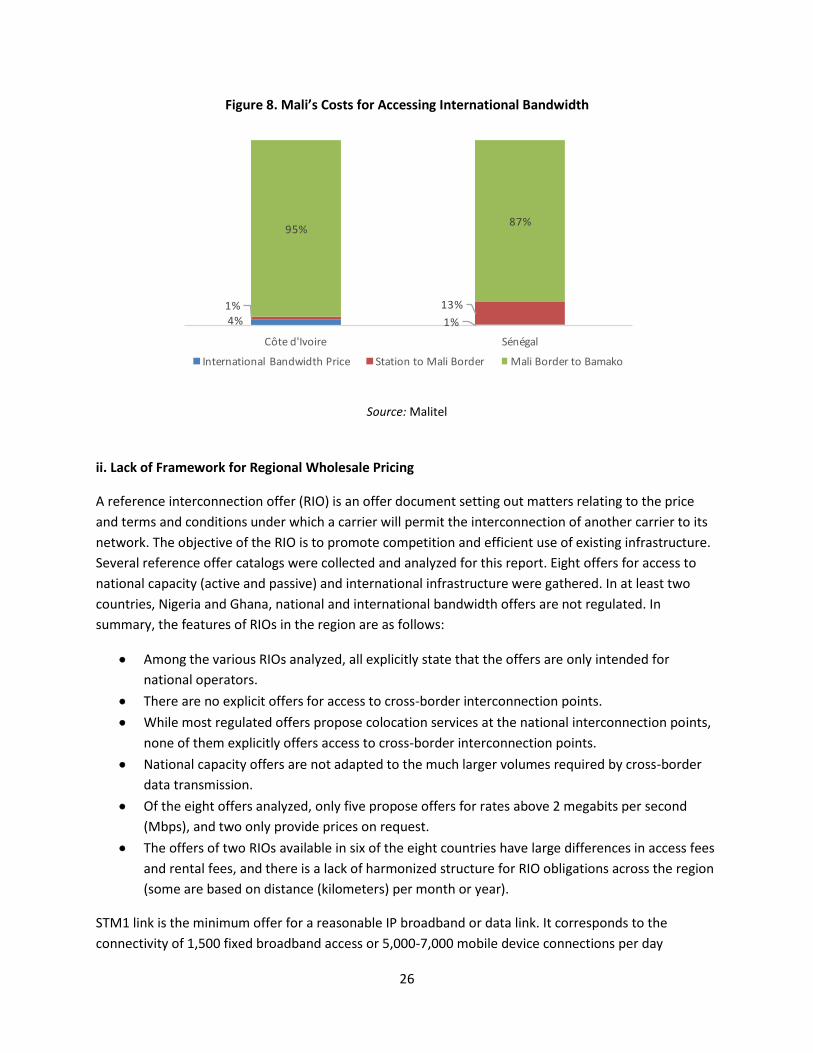

The impact of SMP is worse for landlocked countries that need to route traffic over terrestrial networks

and through cross-border points of interconnection to gain access to international capacities. The price of

international bandwidth is between 1 and 4 percent of total cost (figure 8), depending on the route taken

to access a submarine landing station, and the rest of the cost is incurred in accessing terrestrial backbone

networks.

0

200

400

600

800

1000

1200

Eu c

ou

ntr

y

Tun

isia

Egyp

t

Afr

iqu

e d

u S

ud

Mo

rro

cco

Ré

un

ion

SA

FE

Sén

éga

l (A

CE)

Mau

rita

nia

Nig

eri

a

Mo

zam

biq

ue

Gam

bia

Uga

nd

a

Ré

un

ion

Lio

n

Co

te d

'Ivo

ire

Be

nin

Mau

riti

us

Tel

Leso

tho

Tan

zan

ie

Mad

agas

car

Bo

tsw

ana

RD

C

Uga

nd

a

An

gola

Mau

riti

us

Safe

Togo

Lib

eri

a

Mal

i

Soa

Tom

e

Gh

ana

Cam

ero

un

Tch

ad

Rw

and

a

Co

ngo

$/M

bp

s/m

on

th

Africa : Price of international bandwidth Mbps/month/$ (country-EU)Prix de la bande passante internationale ($/Mbps/mois)

Western Africa

26

Figure 8. Mali’s Costs for Accessing International Bandwidth

Source: Malitel

ii. Lack of Framework for Regional Wholesale Pricing

A reference interconnection offer (RIO) is an offer document setting out matters relating to the price

and terms and conditions under which a carrier will permit the interconnection of another carrier to its

network. The objective of the RIO is to promote competition and efficient use of existing infrastructure.

Several reference offer catalogs were collected and analyzed for this report. Eight offers for access to

national capacity (active and passive) and international infrastructure were gathered. In at least two

countries, Nigeria and Ghana, national and international bandwidth offers are not regulated. In

summary, the features of RIOs in the region are as follows:

• Among the various RIOs analyzed, all explicitly state that the offers are only intended for

national operators.

• There are no explicit offers for access to cross-border interconnection points.

• While most regulated offers propose colocation services at the national interconnection points,

none of them explicitly offers access to cross-border interconnection points.

• National capacity offers are not adapted to the much larger volumes required by cross-border

data transmission.

• Of the eight offers analyzed, only five propose offers for rates above 2 megabits per second

(Mbps), and two only provide prices on request.

• The offers of two RIOs available in six of the eight countries have large differences in access fees

and rental fees, and there is a lack of harmonized structure for RIO obligations across the region

(some are based on distance (kilometers) per month or year).

STM1 link is the minimum offer for a reasonable IP broadband or data link. It corresponds to the

connectivity of 1,500 fixed broadband access or 5,000-7,000 mobile device connections per day

(smartphone or tablet). The main capacities at the backbone level are in billions of bits per second

and/or STM4/16/64 (backhaul and small backbone). Offers for bandwidth exceeding 2 Mbps are

available in a limited set of countries. Only three of the eight countries analyzed offer 1 STM1 for

national capacity. Operators negotiate and reach agreements among themselves for this level of

capacity, often through capacity swaps.

iii. Other Regulatory Enabling Environments Driven by National and Mobile-Focused Interests

The existing policy and regulatory frameworks at the national and regional levels (ECOWAS

Supplementary Acts) have largely focused on advancing national or domestic connectivity. There is

currently no formal framework for fostering optimal economic and technical conditions for regional or

cross-border communications. As a result, investments in completing cross-border or regional

connectivity remain insufficient, and there is a lack of competition for the provision of services based on

cross-border or regional infrastructure, which maintains nontransparent pricing of wholesale bandwidth

capacity that is unregulated.

Licensing of a telco operator. Currently in the ECOWAS region, an operator licensed or authorized as an

operator in a member state is not recognized in another member state. This applies to the operators of

alternative infrastructure (such as energy grids and roads), who currently have no status or rights

enabling them to participate in the rollout of cross-border or regional networks. In this respect, the

ECOWAS Supplementary Act on the Legal Regime Applicable to Network Operators and Service

Providers encourages member states to exempt some activities from a licensing requirement. However,

in practice, licenses remain necessary to provide basic telecommunications services (such as provision of

national and international capacities, or even provision of dark fibers) in most member states. Such

limitations are implemented through the specific requirement to be a national company to carry out

electronic communication activities. This requirement may be specified in the applicable law or

regulations, licenses and their related specifications, regulatory authorities’ websites, and so forth. As a

result, nonnational telecommunications operators that are willing to develop cross-border networks

cannot provide services in the other member states where such networks would be located.

The Supplementary Act on Access and Interconnection in Respect of ICT Sector Networks and Services

provides that “Member states shall ensure that the general regulatory framework for access and

interconnection incorporates the general community regulation principles foreseen for the

establishment of the West African Common Market, including non-discrimination between companies

established in different States.” Likewise, the Supplementary Act on the Legal Regime Applicable to

Network Operators and Service Providers promotes the coordination of national regulatory authorities

toward the establishment of a single point of contact for licensing and authorization procedures.

However, these provisions remain general, are not sufficiently detailed, and have not been implemented

by most ECOWAS member states.

Open access policy, in particular to dark fiber. Open and fair access to backbone infrastructure running

through a country and across the border to another country would trigger an increase in cross-border

communications. It is notable that there are no RIOs for dark fiber indefeasible rights of use (IRU) or

28

wavelengths. Under most legal and regulatory frameworks, nonnational operators cannot benefit from

the rules applicable to access and interconnection, which prevent them from gaining access to national

capacities, international capacities, and dark fiber. Yet, access to such reSource is necessary for the

deployment of cross-border or regional networks. ECOWAS Regulation C/REG. 06/06/12, on conditions

for access to submarine cable landing stations, which is directly applicable in all member states, aims to

ensure that landlocked countries have equal access to submarine fiber that the coast countries have.

Infrastructure sharing and colocation. Related to the principle of open access, specific regulations or

guidelines are required for access to the core network by other network operators. These include

guidelines on sharing masts and poles, spaces in buildings with termination and switching equipment,

trenches through which the fiber optic cable runs, and so on. Rights of way and access to electric power

may require securing additional approval from the granting authority, which should be obtained before

the infrastructure-sharing arrangement between operators can be finalized. And currently there is no

“dig once” policy whereby construction of ducts and pipes underground is planned for the needs of the

various operators and future needs so as not to dig the ground multiple times, which has significant cost

implications as well as disruptions to roads and other facilities (around 75 percent of the cost to lay fiber

underground is in construction and works).

Dispute resolution. One of the best practices in telecommunications is the clear guidelines for dispute

resolution procedures. Yet, in many ECOWAS member states, there are currently no specific provisions

allowing operators established in an ECOWAS member state to settle a dispute with an operator in

another member state. Such dispute settlement procedures are essential to ensure that difficulties

faced when developing cross-border networks can be solved adequately and in a timely fashion. The

ECOWAS Supplementary Act on the harmonization of Policies and of the Regulatory Framework for ICT

sector provides for specific rules dealing with this issue. However, the provisions of this article are not

directly applicable in member states, and most member states have not transposed this article in their

domestic law.

f) Recommendations

The agenda for the transition from a national to a regional regulatory framework and from mobile

network-centric policies to data traffic policies points to the need for a renewed commitment toward

the objective of easing cross-border communications connectivity. The following recommendations

consider the regional and national levels:

➢ Regional Legal and Regulatory Frameworks

National legal and regulatory frameworks are currently designed to foster the growth of the

communications sector at the national level. Although some regional frameworks have been put in

place (such as the ECOWAS Supplementary Acts), there is scope for improvement in their

transposition and implementation. Hence, while national infrastructure and international

connectivity through submarine cables have developed, investments in regional cross-border

connectivity, policy, and regulatory measures for market development and the provision of the

resultant services at affordable costs by the private sector have lagged. The development of a

formal framework to foster optimal technical and financial conditions for regional connectivity,

29

which shifts the focus from developing individual domestic markets to a single connectivity market,

is necessary to develop further regional connectivity.

The ECOWAS Supplementary Acts provide a strong framework for governments and national

regulatory authorities to develop the necessary national legal and regulatory frameworks to foster a

regional market for digital infrastructure. Transposing and implementing these acts into national

frameworks in a prioritized and staggered manner can serve as a starting point toward developing

such a regional outlook for digital sector regulation. The following areas are identified as priorities

for the consideration of member states and their national regulatory authorities:

• Regional licensing regime. Facilitate telecom operators that are licensed or authorized in a

member state to provide certain services across the region, such as the rollout of passive

infrastructure, leasing of dark fiber, and so forth. Similarly, enable owners of alternate

infrastructure, such as utilities, to roll out national as well as regional networks. In doing so

regionally, it is recommended to develop a single window for licensing and authorization

for infrastructure development that facilitates engagement with the necessary authorities.

Relevant ECOWAS Supplementary Acts: Article 3.1 of Supplementary Act A/SA. 2/01/07 on

Access and Interconnection in Respect of ICT Sector Networks and Services; Articles 8.1 and

30 of the Supplementary Act A/SA. 3/01/07 on the Legal Regime Applicable to Network

Operators and Service Providers.

• Significant market power and competition. Addressing SMP at the national and regional

levels is necessary to promote competition and a marginal cost–based pricing mechanism

for services in the region, which is the cornerstone for regulating ICT markets. In addition

to identifying and outlining necessary action to address SMP, measures should be taken to

prevent the creation of such market distortions in the future. This requires significant

efforts at the national level through periodic market analysis to assess SMP and the

implementation of pro-competition measures, such as open access obligations to

infrastructure, price ceilings, liberalization of critical infrastructure (such as gateways), and

so forth.

Relevant ECOWAS Supplementary Acts: Article 9.1 of the Supplementary Act A/SA. 3/01/07

on the Legal Regime Applicable to Network Operators and Service Providers; Article 19.2 of

the Supplementary Act A/SA. 2/01/07 on Access and Interconnection in Respect of ICT

Sector Networks and Services.

• Passive infrastructure sharing and dark fiber. Although Article 10 of the Supplementary Act

A/SA. 2/01/07 on Access and Interconnection in Respect of ICT Sector Networks and

Services lays down provisions for the national authorities promoting the sharing of passive

infrastructure, they do not cover specific aspects, such as rules applicable to accessing

alternative infrastructure, publication of the list of active and passive infrastructure by

operators, and conditions for passive infrastructure sharing. It is recommended that the

ECOWAS Commission, in conjunction with member states, detail the applicable provisions

for passive infrastructure sharing across the region.

• Dispute resolution. In Burkina Faso, Guinea, Côte d’Ivoire, Mali, and Senegal, operators

established in other ECOWAS member states benefit from the right to go before the

regulatory authority, but the same is not true for other member states. To achieve the goal

of establishing a West African Common Market, it is necessary to have an independent

30

dispute resolution mechanism or authority that is accessible to entities from all member

states.

• Standardized data collection. Accurate and periodically updated data on connectivity

infrastructure at the national level—aggregating to regional data—is a must for optimal

utilization of the existing infrastructure. It is recommended that the ECOWAS Commission

establish standardized reporting guidelines for infrastructure data, which should be

collected and published periodically. The key data that are needed include, but are not

limited to, the number of base transceiver stations (BTS) by type, fiber infrastructure,

point-of-presence (POP) sites, and the capacity of each type of connectivity infrastructure.

This effort also provides an opportunity to integrate geospatial information into the data

sets and create digital connectivity maps and informational platforms for the region. This

would include information on the presence and availability of passive linear infrastructure,

such as roads, rail lines, and electricity grids.

➢ Supply-Side Enablers at the National Level

• Reference interconnection offers. The lack of availability and transparency of wholesale

connectivity prices is a bottleneck for operators without large-scale infrastructure to connect

across borders. A lack of standardization in the technical information provided and high degree

of variation in the price points of RIOs were observed, with all reference offers limited to

national stakeholders only. It is recommended that the ECOWAS Commission mandate the

publication of standardized RIOs at the national level, with a long-term goal of operators (and

owners of passive infrastructure) eventually providing regional RIOs.

• Alternate infrastructure. The utility, energy, and transportation sectors can play a significant role

in developing national and regional backbone infrastructure. The Senegal River Development

Organization (OMVS) and CSLG projects can be used as key drivers of subregional cross-border

connectivity and serve as examples for leveraging future infrastructure projects in the region. By

allowing non-telecom operators to engage in rolling out connectivity infrastructure such as dark

fiber, national and regional connectivity can expand at a more rapid pace. This requires

development of the necessary legal and regulatory frameworks at the national level, which can

integrate regionally and promote infrastructure sharing and utilization of alternate Source of

infrastructure at the regional level. Additionally, it can foster greater competition in the

wholesale market and address SMP-related concerns to an extent. It can also serve as a starting

point to implement a regional “dig-only-once” strategy, contracting infrastructure developers to

lay fiber optic cable and commercialize the available infrastructure using innovative business

models, as regulated by national authorities.

• Subregional connectivity. Creating multiple subregional hubs of fiber optic infrastructure and

digital platform infrastructure (data centers, exchange points, and cyber security centers) and

leveraging alternative infrastructure projects, such as the Senegal River Development

Organization and CSLG, could promote robust and secure national and subregional digital

ecosystems. This would in turn provide different options for redundancy networks for the

individual countries. In this instance, the heterogeneous economic and market groupings within

the region could be turned into an advantage.

31

➢ Demand-Side Stimulation (Regional IP Usage)

Most member states have yet to establish neutral IXPs, and many that have been established are

operating sub-optimally. Without an enabling environment that fosters the growth of independent

networks, which would require more IXPs, regional traffic will continue to leave the region and be

interconnected in Europe. This, in turn, does not allow the price of regional IP interconnection to be

as competitive as international interconnection. This is further evidenced by websites receiving the

highest traffic from the region all being hosted outside Africa. Promoting local content development

and hosting in the region will redirect a large proportion of international IP traffic within the region,

and thus reduce the cost of regional interconnection and bandwidth due to higher traffic volume.

Developing greater IP usage through establishment and implementation of comprehensive

broadband strategies at the national and regional levels should be an immediate priority.

III. Low-Cost International Mobile Roaming: Boosting Consumer Welfare Although the communications market in Africa still relies heavily on 2G voice services, which constitute

55 percent of total subscriptions, it is projected to decline to 10 percent by 2023. 22 Internationally,

regional economic communities have leveraged the digital sector to strengthen regional economic

integration, while also promoting consumer welfare through increasing the affordability of services,

including the reduction and eventual elimination of roaming charges. Roaming does not form a large part

of mobile operator revenues, but it has traditionally been a high-margin business segment, partially due

to the need to compensate for the high risk of subscribers’ bad debt, delayed payments, and potential

fraud, among other reasons.

Estimating the market for international roaming requires information on prices and volumes (of calls and

data usage) for each operator in each country, as well as information on cross-border movement. Such

data are not widely available for the region, as transparency in retail pricing is not enforced, and the

information would include commercially sensitive data owned by mobile operators. Additionally, the

limited international experiences in regional mobile roaming regimes do not allow for accurate estimation

of the price elasticity of roaming and resulting changes in consumer behavior. This study aims to highlight

the current state of international mobile roaming in the region and the challenges to the reduction and

abolishment of roaming charges. This section also highlights challenges to the development of a regional

outlook for the sector, particularly since the roaming market includes wholesale and retail elements.

On the one hand, the reduction or abolishment of roaming tariffs would constitute a reduction in operator

revenues from the service in the medium term. On the other hand, it would create a large consumer

surplus, which, by one estimation, would amount to US$775 million over the next four years for the

region.23 Table 3 presents the estimated consumer surplus per inhabitant due to the abolishment of

roaming based on the same study. For comparison, the ECOWAS region has a higher population and lower

gross national income per capita than the Gulf Cooperation Council (GCC) and European Union.

32

Table 3. Transfer of Welfare (Additional Consumer Surplus) (US$ per inhabitant)

GCC (2012) $1.8

EU (2009 to 2013, yearly average) $5.0

ECOWAS (2017 to 2020, yearly average) $0.6

Source: “Study on Policies to Reduce Mobile Roaming Rates,” prepared by Progressus including Olivier Jacquinot, Katia Duhamel, Laurent Cohen, and Russel Southwood. Note: ECOWAS = Economic Community of West African

States; EU = European Union; GCC = Gulf Cooperation Council.

Regional roaming initiatives have been met with varying degrees of success and followed different paths.

A common result across all initiatives is a significant increase in roaming usage, which can be seen as an

indicator of consumer surplus. In Kenya, for example, the volume of calls increased by 264 percent when

regional roaming rates were abolished. Similarly, in France, call volumes increased by 50 percent when

tariffs decreased by 50 percent, and more recently, some European operators have reportedly seen an

increase in roaming data usage of 870 percent.24

Operators across Africa, including in the ECOWAS region, have recognized the potential of the roaming

market and developed on-network roaming plans in response. Additionally, certain country pairs within

ECOWAS have started implementing free roaming to benefit consumers and facilitate greater integration.

As highlighted in the previous section, the region has significant infrastructure, and the retail market is

gradually moving toward seamless movement. However, regional policy and regulatory efforts can further

aid in the development of this market. In addition to increasing consumer welfare, affordable regional

roaming can help smaller operators provide services to their subscribers and not be burdened by the costs

associated with being in a net payable situation.

The roaming market also allows taking a regional view of mobile communications, since it entails

wholesale (requiring interconnectivity) and retail elements of the communications market. Analyzing this

market enables the identification of underlying issues for greater harmonization of the sector at the

regional level.

a) Potential for a Regional International Mobile Roaming Regime

Affordable and seamless roaming can help develop regional economic activity. To assess the potential for

roaming, the following subsections consider trade, migration, and tourism flows within the region as

proxies.

i. Trade Flows in ECOWAS

Trade flows within ECOWAS can serve as a proxy for regional economic activity that can be further

supported through affordable roaming services. As highlighted in figure 9, regional trade as a percentage

of total trade varies from 2 to 60 percent, with an average of 9 percent across member states.

33

Figure 9. Intra-ECOWAS Trade (%)

Source: UN COMTRADE data.

As a possible and observable proxy to estimate potential development for roaming, the trade exchange

values show that there is no significant difference between ECOWAS countries and countries in other

regions. Additionally, this analysis demonstrates that the most important trade flows are between Nigeria

and other countries, as Nigeria is the biggest economy in the region (figure 10).

Figure 10. Major Trading Parties within ECOWAS: Annual Trading Value (US$, millions)

Source: UN COMTRADE data.

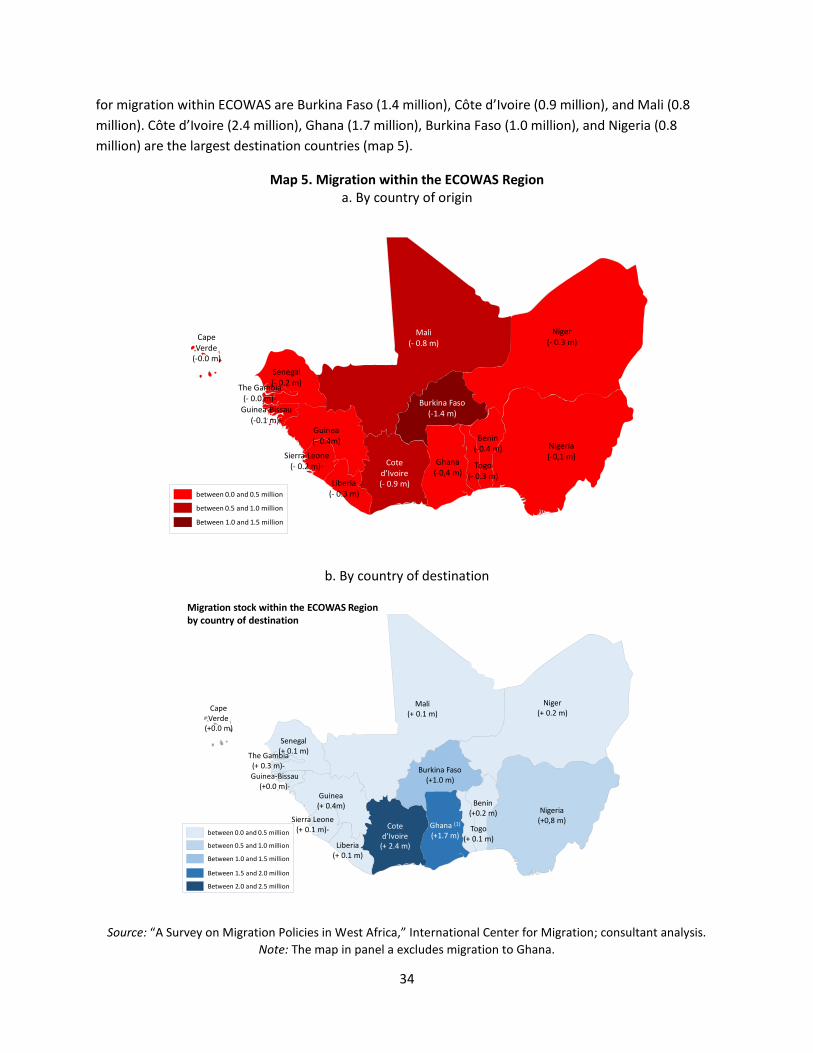

ii. Migration Flows within the ECOWAS Region

Intra-ECOWAS migration flows as a portion of total migration flows are significant, accounting for 64

percent. Only 30 percent of migrants from ECOWAS reside outside Africa, of which 15 percent are in

Europe, 6 percent in North America, and 9 percent in the rest of the world. The main countries of origin

60%

46%

38%

29%24% 23%

20% 19% 19% 17%

8%4% 2%

9%

% of trade with other ECOWAS countries

0

500

1000

1500

2000

2500

3000

Nigeria/ Côte

d'Ivoire

Nigeria/

Ghana

Nigeria/ Niger

Mali /Senegal

Nigeria/

Senegal

Côted'Ivoire

/Burkina

Faso

Côted'Ivoire

/Ghana

Côted'Ivoire/ Mali

Ghana/

BurkinaFaso

Senegal/

Nigeria

Senegal/ Mali

Guinea/

Ghana

SierraLeone /Senegal

Annual trading value (million USD)

34

for migration within ECOWAS are Burkina Faso (1.4 million), Côte d’Ivoire (0.9 million), and Mali (0.8

million) are the largest destination countries (map 5).

Map 5. Migration within the ECOWAS Region a. By country of origin

b. By country of destination

Source: “A Survey on Migration Policies in West Africa,” International Center for Migration; consultant analysis.

Note: The map in panel a excludes migration to Ghana.

Coted’Ivoire(- 0.9 m)

Sierra Leone(- 0.2 m)-

Mali(- 0.8 m)

Guinea-Bissau(-0.1 m)-

Ghana(-0,4 m)

Niger(- 0.3 m)

Guinea(- 0.4m)

Nigeria(-0,1 m)

Senegal(- 0.2 m)

Liberia(- 0.3 m)

Benin(-0.4 m)

The Gambia(- 0.0 m)-

CapeVerde

(-0.0 m)

Burkina Faso(-1.4 m)

Migration stock within the ECOWAS Regionby country of origin (1)

Source : A survey on Migration Policies in West Africa, ICMPD et OIM, Consultant Analysis(1) Excluding migration to Ghana

between 0.0 and 0.5 million

between 0.5 and 1.0 million

Between 1.0 and 1.5 million

Togo(- 0.3 m)

Coted’Ivoire

(+ 2.4 m)

Sierra Leone(+ 0.1 m)-

Mali(+ 0.1 m)

Guinea-Bissau(+0.0 m)-

Ghana (1)

(+1.7 m)

Niger(+ 0.2 m)

Guinea(+ 0.4m)

Nigeria(+0,8 m)

Senegal(+ 0.1 m)

Liberia(+ 0.1 m)

Benin(+0.2 m)

The Gambia(+ 0.3 m)-

CapeVerde

(+0.0 m)

Burkina Faso(+1.0 m)

Migration stock within the ECOWAS Regionby country of destination

Source : A survey on Migration Policies in West Africa, ICMPD et OIM, Consultant Analysis(1) estimates

between 0.0 and 0.5 million

between 0.5 and 1.0 million

Between 1.0 and 1.5 million

Between 1.5 and 2.0 million

Between 2.0 and 2.5 million

Togo(+ 0.1 m)

35

iii. Short-Term Travel and Tourism within ECOWAS

Analysis of short-term migration and travel is another way to assess the potential market for roaming.

Higher levels of economic integration in the region may be associated with increased short-term regional

travel and support tourism in the region, as citizens can travel freely within the region. International

tourism currently exceeds one billion persons a year and has been growing at an annual rate of 3 percent.

Tourism in Africa has varied over the past year between 55 million and 62 million persons, which

represents 5 to 7 percent of world tourism. Figure 11 highlights the share of tourism between some of

the countries, which ranges between US$15 and US$43 per incoming tourist.

Figure 11. Total and Internal Tourism in ECOWAS

Source: “Study on Policies to Reduce Mobile Roaming Rates,” prepared by Progressus including Olivier Jacquinot,

Katia Duhamel, Laurent Cohen, and Russel Southwood.

Lengths of stay vary from 3 to 8 days (figure 12). In addition to overnight visitors (0.6 million), Nigeria has

an important flow of same-day visitors (3.4 million), likely due to its economic size and position as an

international hub in Africa.

Figure 12. Lengths of Stay in Days

Source: “Study on Policies to Reduce Mobile Roaming Rates,” prepared by Progressus including

Olivier Jacquinot, Katia Duhamel, Laurent Cohen, and Russel Southwood.

257

191

33

152

600

44

327

110

70

836

132

7

62

43%

37%

24% 24%22%

15%

19%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

100

200

300

400

500

600

700

Benin Burkina Faso Guinea Mali Nigeria Sierra Leone Togo

Internal ECOWAS tourism vs Total ECOWAS tourismin thousands and %

Total Internal %

8 8

7 76.5

4.43.9

3.4 3.1 3

0

1

2

3

4

5

6

7

8

9

36

International tourism is still in its developmental stages in Africa, and it is expected to grow as incomes

increase and the various regional integration efforts across the continent mature. Given the low average

lengths of stay and relatively high amount of internal travel within the region, the roaming market

demonstrates potential for growth.

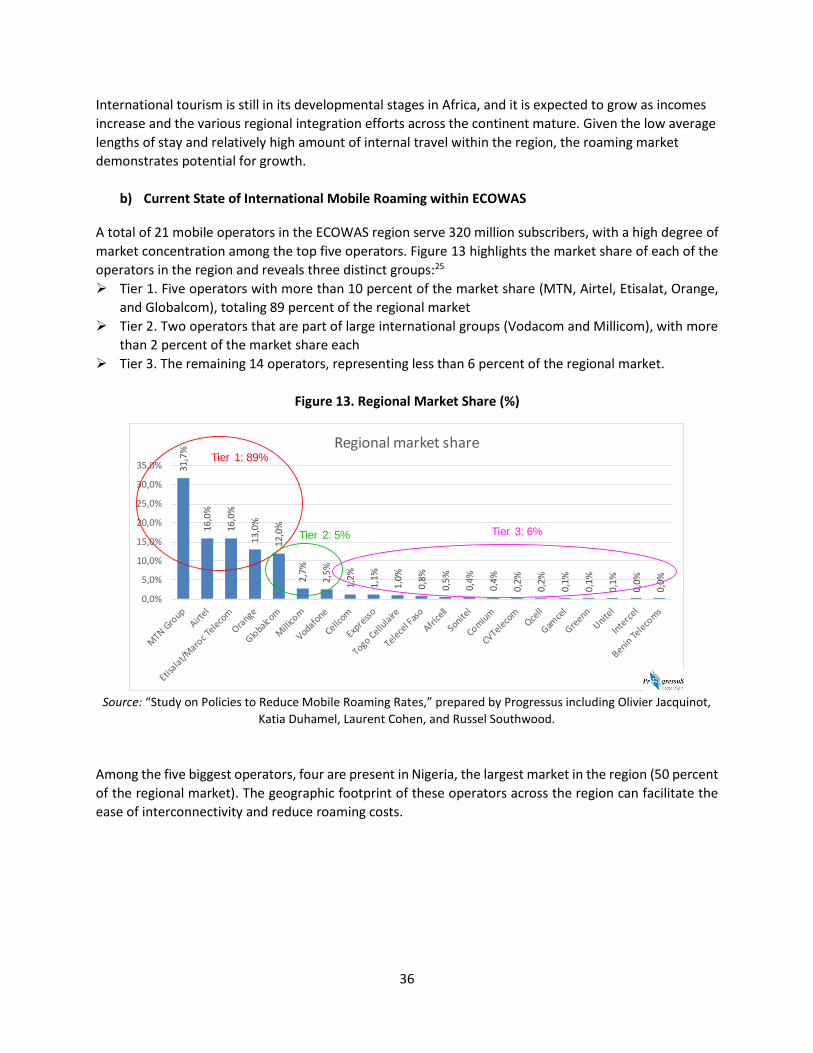

b) Current State of International Mobile Roaming within ECOWAS

A total of 21 mobile operators in the ECOWAS region serve 320 million subscribers, with a high degree of

market concentration among the top five operators. Figure 13 highlights the market share of each of the

operators in the region and reveals three distinct groups:25

➢ Tier 1. Five operators with more than 10 percent of the market share (MTN, Airtel, Etisalat, Orange,

and Globalcom), totaling 89 percent of the regional market

➢ Tier 2. Two operators that are part of large international groups (Vodacom and Millicom), with more

than 2 percent of the market share each

➢ Tier 3. The remaining 14 operators, representing less than 6 percent of the regional market.

Figure 13. Regional Market Share (%)

Source: “Study on Policies to Reduce Mobile Roaming Rates,” prepared by Progressus including Olivier Jacquinot,

Katia Duhamel, Laurent Cohen, and Russel Southwood.

Among the five biggest operators, four are present in Nigeria, the largest market in the region (50 percent

of the regional market). The geographic footprint of these operators across the region can facilitate the

ease of interconnectivity and reduce roaming costs.

31

,7%

16,0

%

16,0

%

13

,0%

12,0

%

2,7%

2,5%

1,2%

1,1%

1,0

%

0,8

%

0,5

%

0,4%

0,4%

0,2

%

0,2%

0,1%

0,1

%

0,1

%

0,0

%

0,0%

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

35,0%

Regional market shareTier 1: 89%

Tier 2: 5% Tier 3: 6%

37

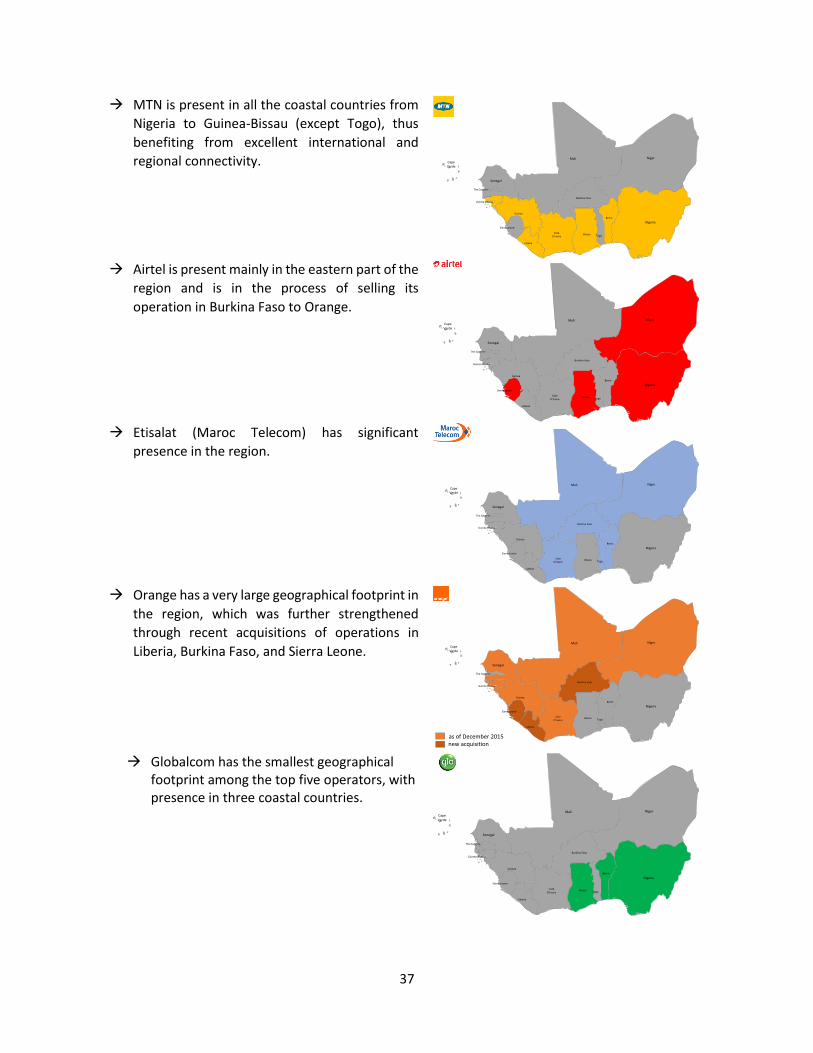

MTN is present in all the coastal countries from

Nigeria to Guinea-Bissau (except Togo), thus

benefiting from excellent international and

regional connectivity.

Airtel is present mainly in the eastern part of the

region and is in the process of selling its

operation in Burkina Faso to Orange.

Etisalat (Maroc Telecom) has significant

presence in the region.

Orange has a very large geographical footprint in

the region, which was further strengthened

through recent acquisitions of operations in

Liberia, Burkina Faso, and Sierra Leone.

Globalcom has the smallest geographical

footprint among the top five operators, with presence in three coastal countries.

CoteD’Ivoire

Sierra Leone-

Mali

Guinea-Bissau-

Ghana

Niger

Guinea

Nigeria

Senegal

Togo

Liberia

Benin

The Gambia-

CapeVerde

Burkina Faso

CoteD’Ivoire

Sierra Leone-

Mali

Guinea-Bissau-

Ghana

Niger

Guinea

Nigeria

Senegal

Togo

Liberia

Benin

The Gambia-

CapeVerde

Burkina Faso

CoteD’Ivoire

Sierra Leone-

Mali

Guinea-Bissau-

Ghana

Niger

Guinea

Nigeria

Senegal

Togo

Liberia

Benin

The Gambia-

CapeVerde

Burkina Faso

CoteD’Ivoire

Sierra Leone-

Mali

Guinea-Bissau-

Ghana

Niger

Guinea

Nigeria

Senegal

Togo

Liberia

Benin

The Gambia-

CapeVerde

Burkina Faso

as of December 2015new acquisition

CoteD’Ivoire

Sierra Leone-

Mali

Guinea-Bissau-

Ghana

Niger

Guinea

Nigeria

Senegal

Togo

Liberia

Benin

The Gambia-

CapeVerde

Burkina Faso

38

The primary motivation behind further development of international mobile roaming in the ECOWAS

region is to facilitate the fluidity of cross-border exchanges, be it communications, goods and services,

people, or cultural. Estimating the impact of seamless and affordable roaming in terms of increased

traffic and usage is challenging, and only now are we seeing preliminary data from the European Union

after the adoption of Regulation No. 2015/2120 in June 2017, which abolished roaming tariffs. From the

consumers’ perspective, the main obstacle to the use of roaming is unaffordability, which pushes a large

portion of the latent demand or potential customers to resort to substitution offers, such as buying local

SIM cards or using over-the-top (OTT) services on Wi-Fi networks. These options have drawbacks for the

consumer and cannot offer the continuity and seamlessness that affordable roaming can. Additionally, it

may become increasingly difficult to obtain SIM cards for short stays, as more countries strengthen their

Know Your Customer requirements.

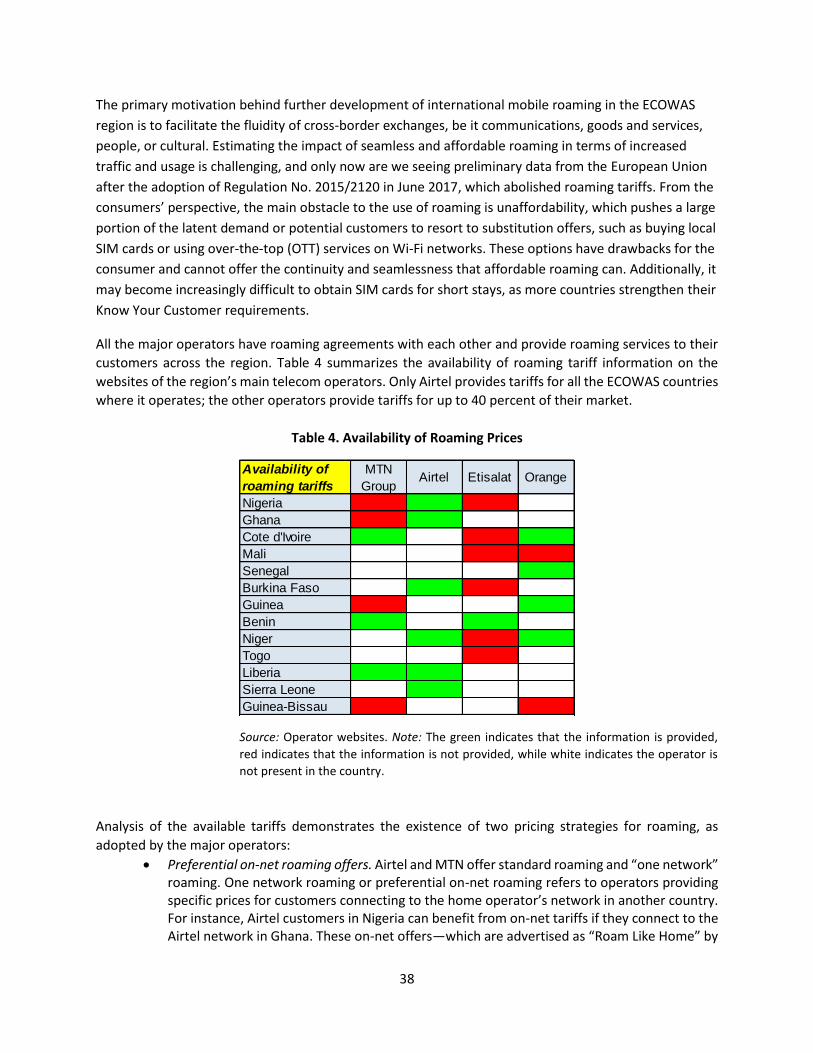

All the major operators have roaming agreements with each other and provide roaming services to their

customers across the region. Table 4 summarizes the availability of roaming tariff information on the

websites of the region’s main telecom operators. Only Airtel provides tariffs for all the ECOWAS countries

where it operates; the other operators provide tariffs for up to 40 percent of their market.

Table 4. Availability of Roaming Prices