40

1 Peter Hodgson Group Managing Director Institutional (previously CRO) David Stephen Chief Risk Officer What do I worry about? July 2007

1

Peter HodgsonGroup Managing Director Institutional (previously CRO)

David StephenChief Risk Officer

What do I worry about?July 2007

2

Key takeaways

• Environment still supportive

• “De-risking” worked, ANZ risk profile now in line with peers

• Some concerns, but not likely to have material impact on ANZ

– Isolated pockets of NSW housing

• Longer term, we can’t ignore the risks posed by climate change

– Indirect, including higher electricity prices

3

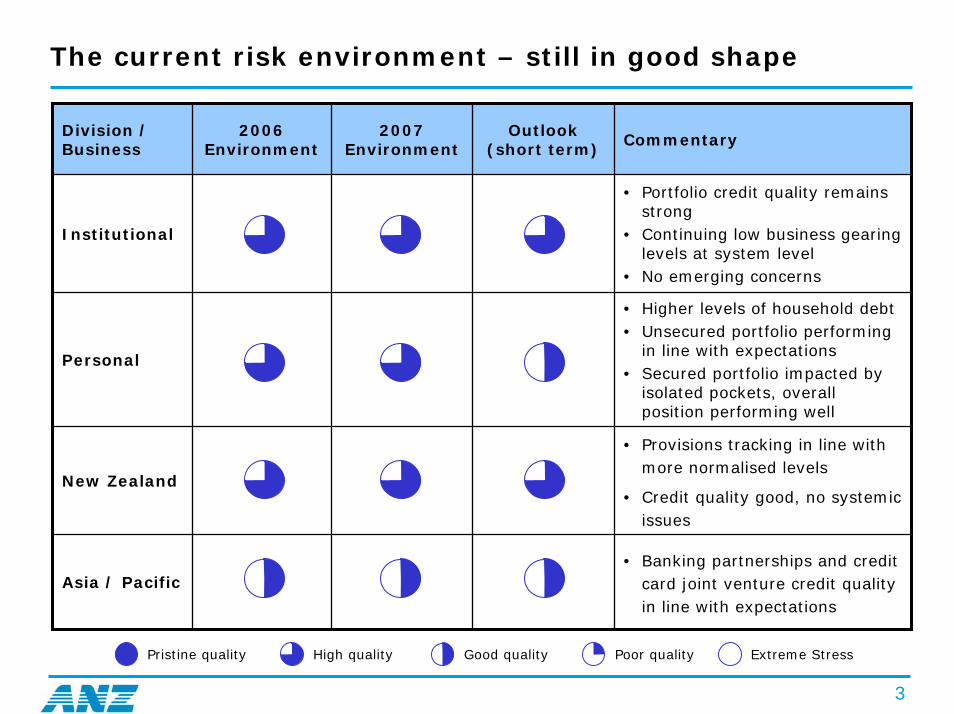

The current risk environment – still in good shape

Division / Business

2006 Environment

2007 Environment

Outlook (short term) Commentary

Institutional

• Portfolio credit quality remains strong

• Continuing low business gearing levels at system level

• No emerging concerns

Personal

• Higher levels of household debt• Unsecured portfolio performing

in line with expectations• Secured portfolio impacted by

isolated pockets, overall position performing well

New Zealand

• Provisions tracking in line with more normalised levels

• Credit quality good, no systemic issues

Asia / Pacific• Banking partnerships and credit

card joint venture credit quality in line with expectations

Pristine quality High quality Good quality Poor quality Extreme Stress

4

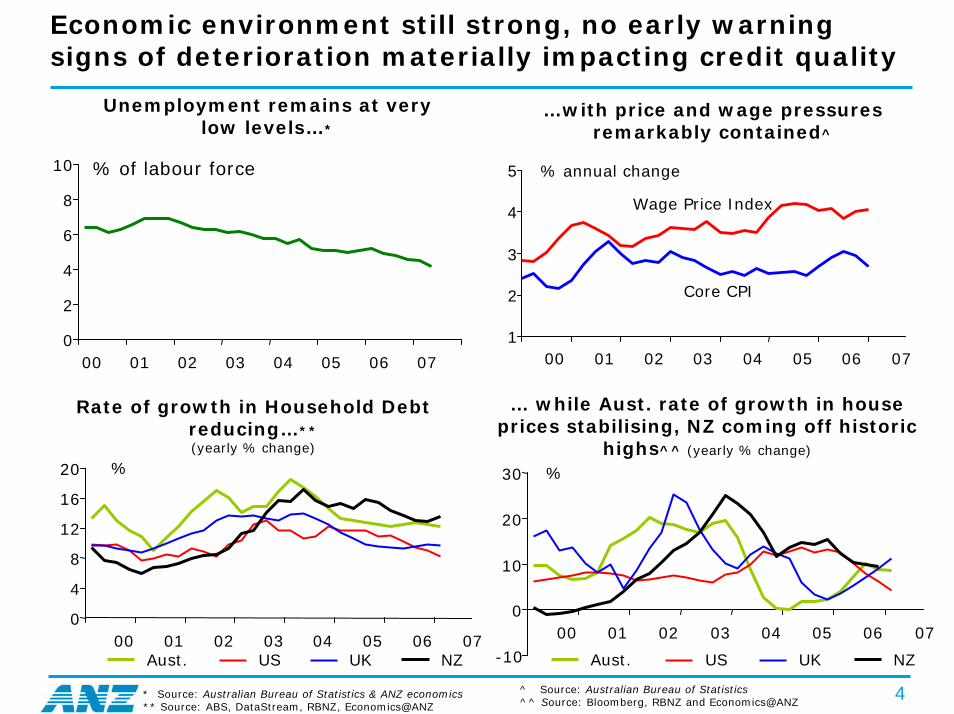

Economic environment still strong, no early warning signs of deterioration materially impacting credit quality

Unemployment remains at very low levels…*

…with price and wage pressures remarkably contained^

% of labour force

0

2

4

6

8

10

00 01 02 03 04 05 06 07

1

2

3

4

5

00 01 02 03 04 05 06 07

% annual change

Wage Price Index

Core CPI

Rate of growth in Household Debt reducing…**(yearly % change)

… while Aust. rate of growth in house prices stabilising, NZ coming off historic

highs^^ (yearly % change)

^ Source: Australian Bureau of Statistics ^^ Source: Bloomberg, RBNZ and Economics@ANZ

0

4

8

12

16

20

00 01 02 03 04 05 06 07Aust. US UK NZ

%

-10

0

10

20

30

00 01 02 03 04 05 06 07

Aust. US UK NZ

%

* Source: Australian Bureau of Statistics & ANZ economics ** Source: ABS, DataStream, RBNZ, Economics@ANZ

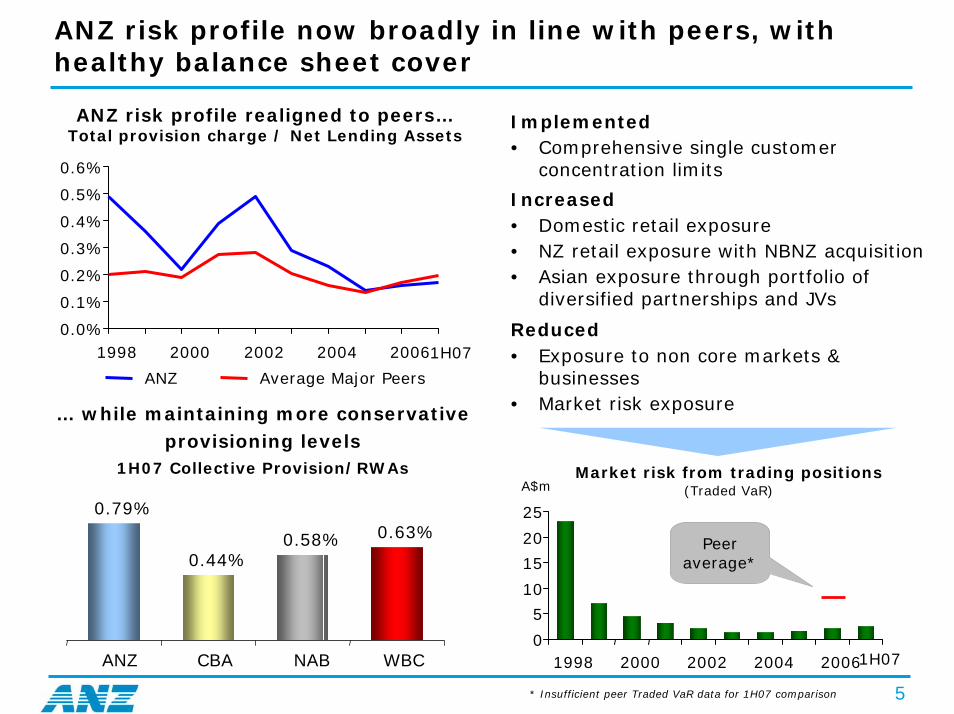

ANZ risk profile now broadly in line with peers, with healthy balance sheet cover

5

… while maintaining more conservative provisioning levels

1H07 Collective Provision/RWAs

ANZ risk profile realigned to peers…Total provision charge / Net Lending Assets

Implemented• Comprehensive single customer

concentration limits

Increased• Domestic retail exposure • NZ retail exposure with NBNZ acquisition• Asian exposure through portfolio of

diversified partnerships and JVs

Reduced• Exposure to non core markets &

businesses• Market risk exposure

A$mMarket risk from trading positions

(Traded VaR)

Peer average*

1H07

1H070.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

1998 2000 2002 2004 2006

ANZ Average Major Peers

0.79%

0.44%0.58% 0.63%

ANZ CBA NAB WBC 0

5

10

15

20

25

1998 2000 2002 2004 2006

* Insufficient peer Traded VaR data for 1H07 comparison

6

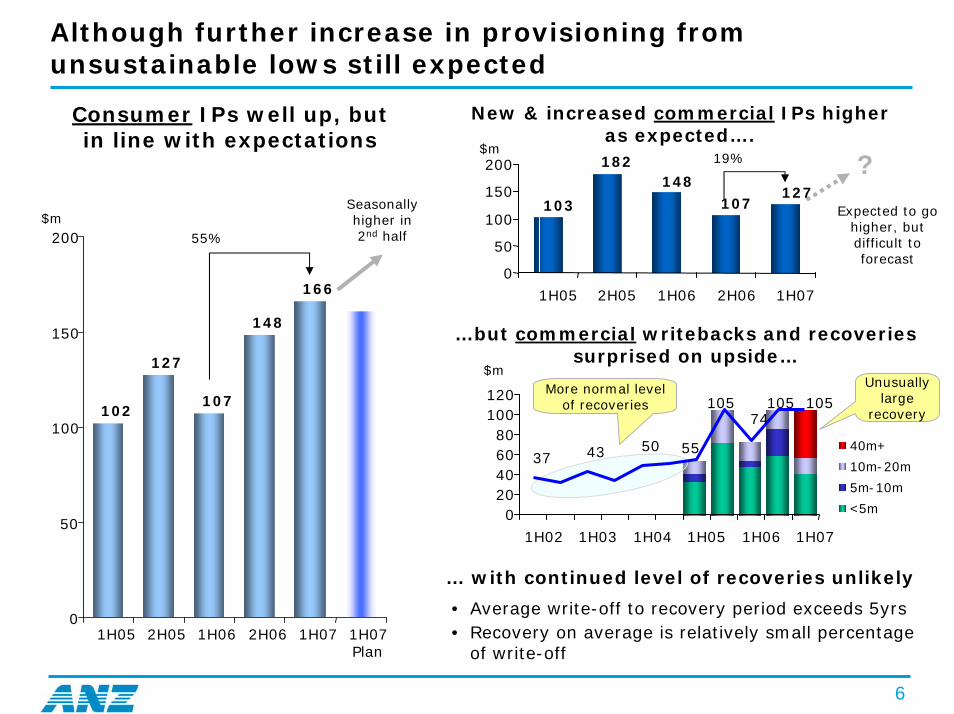

40m+

10m-20m

5m-10m

<5m

Consumer

Although further increase in provisioning from unsustainable lows still expected

IPs well up, but in line with expectations

$m55%

New & increased commercial IPs higher as expected….

…but commercial writebacks and recoveries surprised on upside…

19%$m

Seasonally higher in 2nd half

?

Expected to go higher, but difficult to forecast

$mUnusually

large recovery

More normal level of recoveries

… with continued level of recoveries unlikely

• Average write-off to recovery period exceeds 5yrs• Recovery on average is relatively small percentage

of write-off

102

127

107

148

166

0

50

100

150

200

1H05 2H05 1H06 2H06 1H07 1H07Plan

127107103

182148

0

50

100

150

200

1H05 2H05 1H06 2H06 1H07

37 43 50

105 105

55

74105

020406080

100120

1H02 1H03 1H04 1H05 1H06 1H07

7

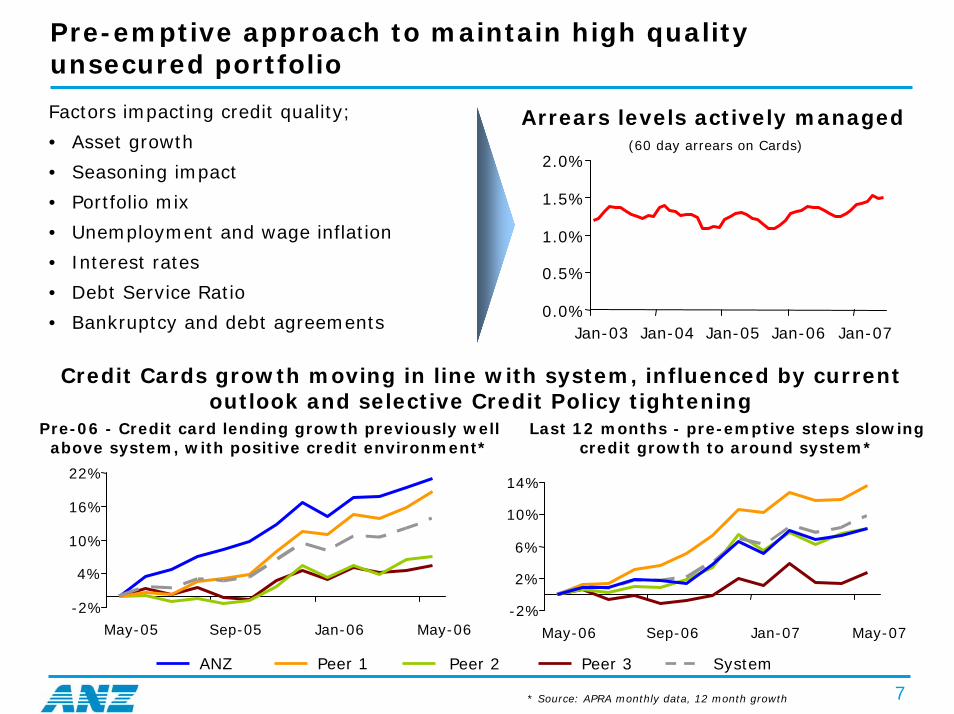

Pre-emptive approach to maintain high quality unsecured portfolio

Factors impacting credit quality;

• Asset growth

• Seasoning impact

• Portfolio mix

• Unemployment and wage inflation

• Interest rates

• Debt Service Ratio

• Bankruptcy and debt agreements

Arrears levels actively managed(60 day arrears on Cards)

* Source: APRA monthly data, 12 month growth

Credit Cards growth moving in line with system, influenced by current outlook and selective Credit Policy tightening

Last 12 months - pre-emptive steps slowing credit growth to around system*

Pre-06 - Credit card lending growth previously well above system, with positive credit environment*

ANZ Peer 1 Peer 2 Peer 3 System

0.0%

0.5%

1.0%

1.5%

2.0%

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07

-2%

4%

10%

16%

22%

May-05 Sep-05 Jan-06 May-06-2%

2%

6%

10%

14%

May-06 Sep-06 Jan-07 May-07

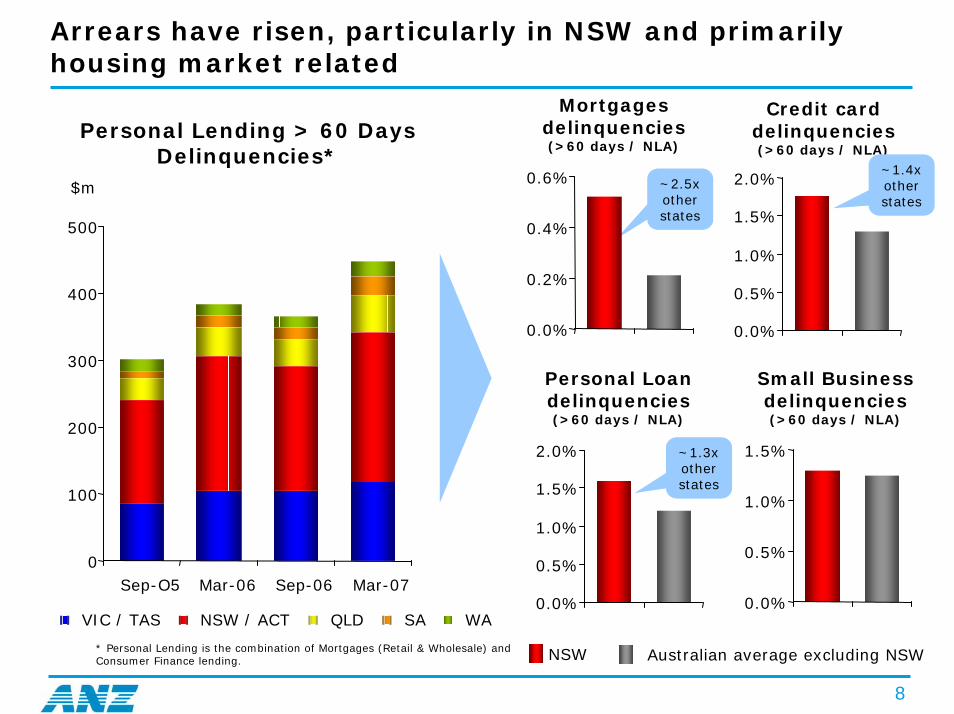

Arrears have risen, particularly in NSW and primarily housing market related

8

Personal Lending > 60 Days Delinquencies*

* Personal Lending is the combination of Mortgages (Retail & Wholesale) and Consumer Finance lending.

$m

NSW

Mortgages delinquencies (>60 days / NLA)

Credit card delinquencies (>60 days / NLA)

Personal Loan delinquencies (>60 days / NLA)

Small Business delinquencies (>60 days / NLA)

~2.5x other states

~1.4x other states

~1.3x other states

0

100

200

300

400

500

Sep-O5 Mar-06 Sep-06 Mar-07

VIC / TAS NSW / ACT QLD SA WA0.0%

0.5%

1.0%

1.5%

2.0%

0.0%

0.5%

1.0%

1.5%

0.0%

0.2%

0.4%

0.6%

0.0%

0.5%

1.0%

1.5%

2.0%

Australian average excluding NSW

9

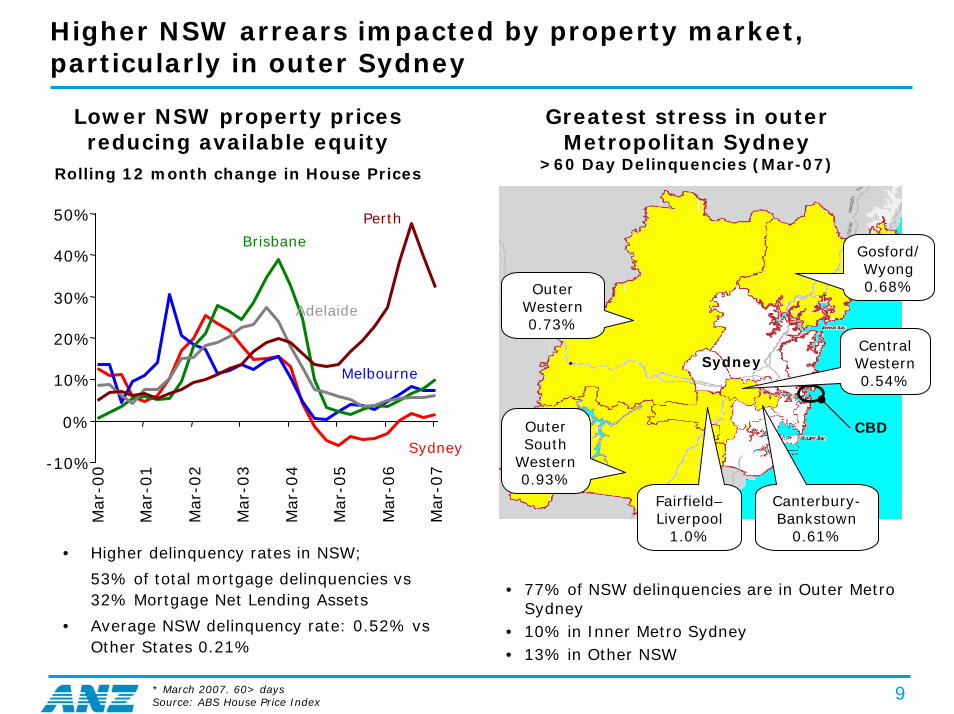

Higher NSW arrears impacted by property market, particularly in outer Sydney

Lower NSW property prices reducing available equity

Rolling 12 month change in House Prices

Greatest stress in outer Metropolitan Sydney

>60 Day Delinquencies (Mar-07)

Sydney

CBDSydney

Melbourne

Brisbane

Adelaide

Perth

-10%

0%

10%

20%

30%

40%

50%

Mar

-00

Mar

-01

Mar

-02

Mar

-03

Mar

-04

Mar

-05

Mar

-06

Mar

-07

Outer Western0.73%

Outer South

Western0.93%

Fairfield–Liverpool

1.0%

Canterbury-Bankstown

0.61%

Central Western 0.54%

Gosford/ Wyong0.68%

• Higher delinquency rates in NSW;

53% of total mortgage delinquencies vs 32% Mortgage Net Lending Assets

• Average NSW delinquency rate: 0.52% vs Other States 0.21%

• 77% of NSW delinquencies are in Outer Metro Sydney

• 10% in Inner Metro Sydney• 13% in Other NSW

* March 2007. 60> days Source: ABS House Price Index

10

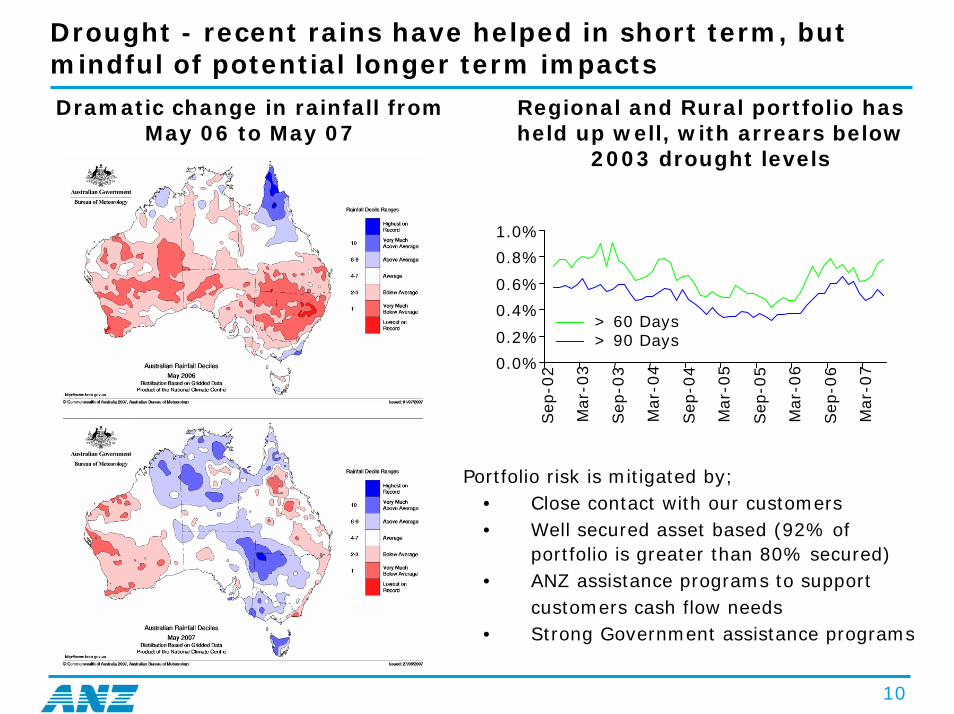

Drought - recent rains have helped in short term, but mindful of potential longer term impacts

Dramatic change in rainfall from May 06 to May 07

Regional and Rural portfolio has held up well, with arrears below

2003 drought levels

Portfolio risk is mitigated by;• Close contact with our customers• Well secured asset based (92% of

portfolio is greater than 80% secured)• ANZ assistance programs to support

customers cash flow needs• Strong Government assistance programs

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

Sep

-02

Mar

-03

Sep

-03

Mar

-04

Sep

-04

Mar

-05

Sep

-05

Mar

-06

Sep

-06

Mar

-07

> 60 Days > 90 Days

11

Impacts from drought can be beyond the obvious -electricity prices up significantly, with water a key input

Calendar 2008 Electricity Futures Prices(dollars per megawatt hour)

Electricity estimated to represent around 5%

of business input costs, so potentially significant impact

Tarongwater

capacity reduction

Start of Q2

Water issue: Swanbank

Water issue:

Hydro Tas

Snowy warning announcement

Jan 07 Feb 07 Mar 07 Apr 07 May 07 Jun 07 July 07

$/MWh

0

10

20

30

40

50

60

70

80

90

100

NSW Calendar 2008 (cal08) Vic Calendar 2008 (cal08)SA Calendar 2008 (cal08) QLD Calendar 2008 (cal08)

Source: ANZ Institutional Banking

12

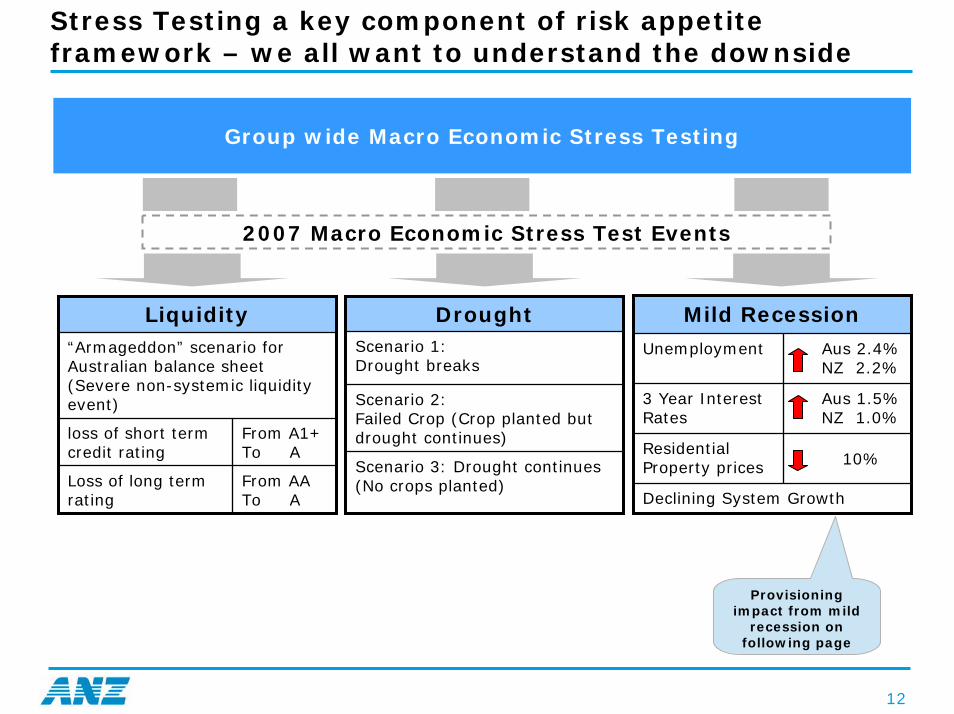

Stress Testing a key component of risk appetite framework – we all want to understand the downside

Group wide Macro Economic Stress Testing

2007 Macro Economic Stress Test Events

Mild Recession

Unemployment Aus 2.4%NZ 2.2%

3 Year Interest Rates

Aus 1.5%NZ 1.0%

Residential Property prices 10%

Declining System Growth

DroughtScenario 1:Drought breaks

Scenario 2: Failed Crop (Crop planted but drought continues)

Scenario 3: Drought continues (No crops planted)

Liquidity“Armageddon” scenario for Australian balance sheet (Severe non-systemic liquidity event)

loss of short term credit rating

From A1+ To A

Loss of long term rating

From AATo A

Provisioning impact from mild

recession on following page

13

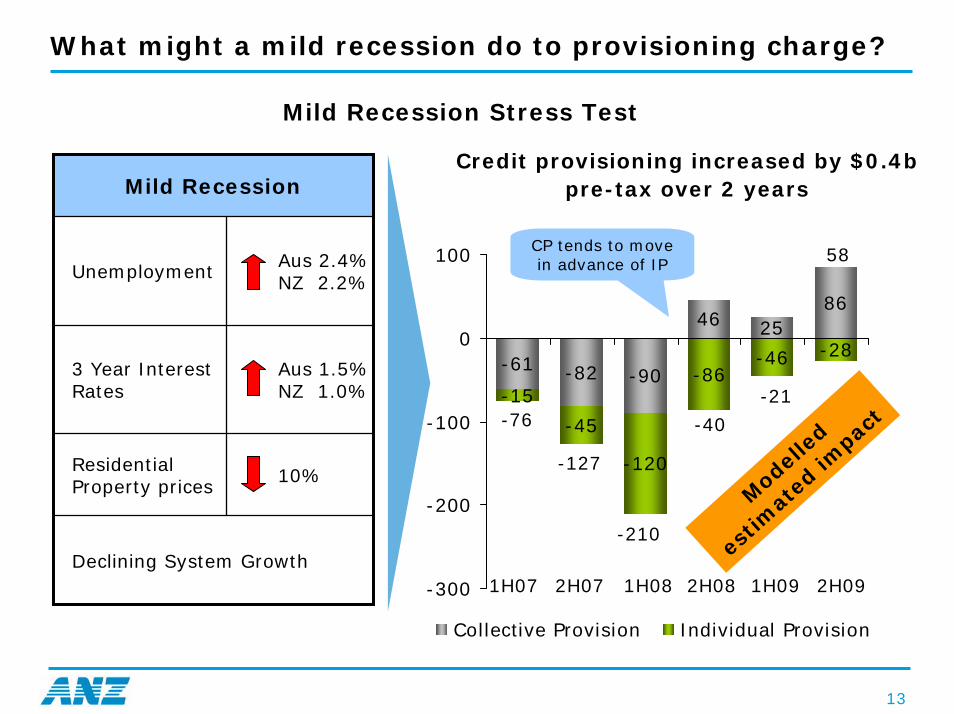

What might a mild recession do to provisioning charge?

Mild Recession Stress Test

Credit provisioning increased by $0.4b pre-tax over 2 yearsMild Recession

Unemployment Aus 2.4%NZ 2.2%

3 Year Interest Rates

Aus 1.5%NZ 1.0%

Residential Property prices 10%

Declining System Growth

-61 -82 -90

46 2586

-28-46-86

-15

-45

-120

-300

-200

-100

0

100

Collective Provision Individual Provision

Mod

elle

d

estim

ated

impac

t

1H07 2H07 1H08 2H08 1H09 2H09

-76

-127

-210

-40

-21

58CP tends to move in advance of IP

14

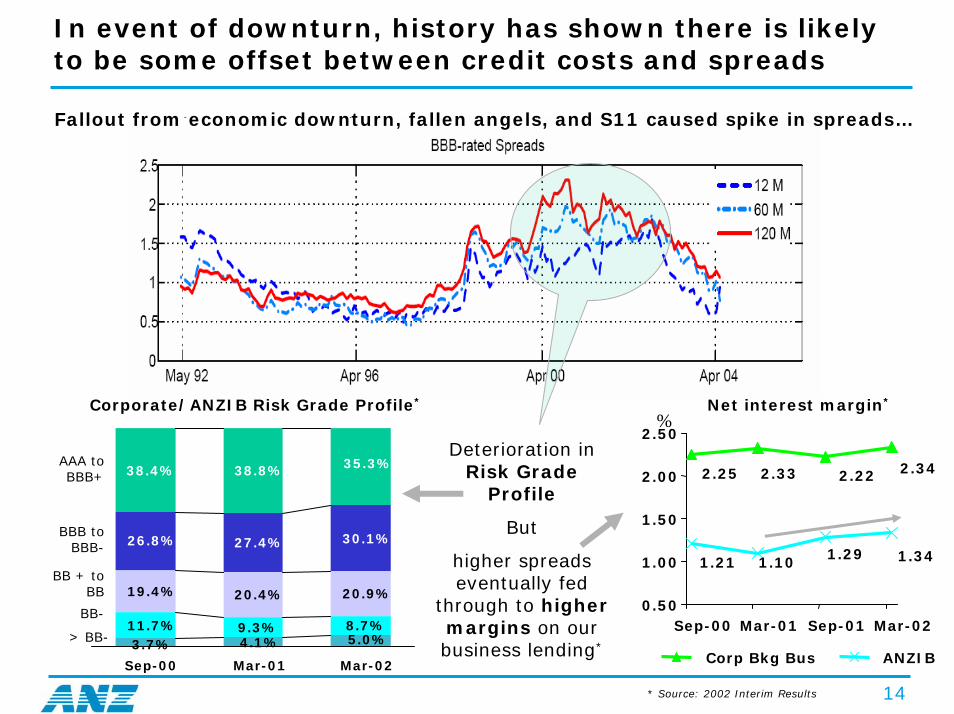

In event of downturn, history has shown there is likely to be some offset between credit costs and spreads

Fallout from economic downturn, fallen angels, and S11 caused spike in spreads…

%Deterioration in

Risk Grade Profile

But

higher spreads eventually fed

through to higher margins on our business lending*

AAA to BBB+

BBB to BBB-

BB + to BB

BB-

> BB-

Net interest margin*Corporate/ANZIB Risk Grade Profile*

11.7% 9.3% 8.7%

19.4% 20.4% 20.9%

27.4% 30.1%

38.8%

3.7% 4.1% 5.0%

26.8%

38.4% 35.3%

Sep-00 Mar-01 Mar-02

2.342.25 2.222.33

1.341.291.101.21

0.50

1.00

1.50

2.00

2.50

Sep-00 Mar-01 Sep-01 Mar-02

Corp Bkg Bus ANZIB

* Source: 2002 Interim Results

15

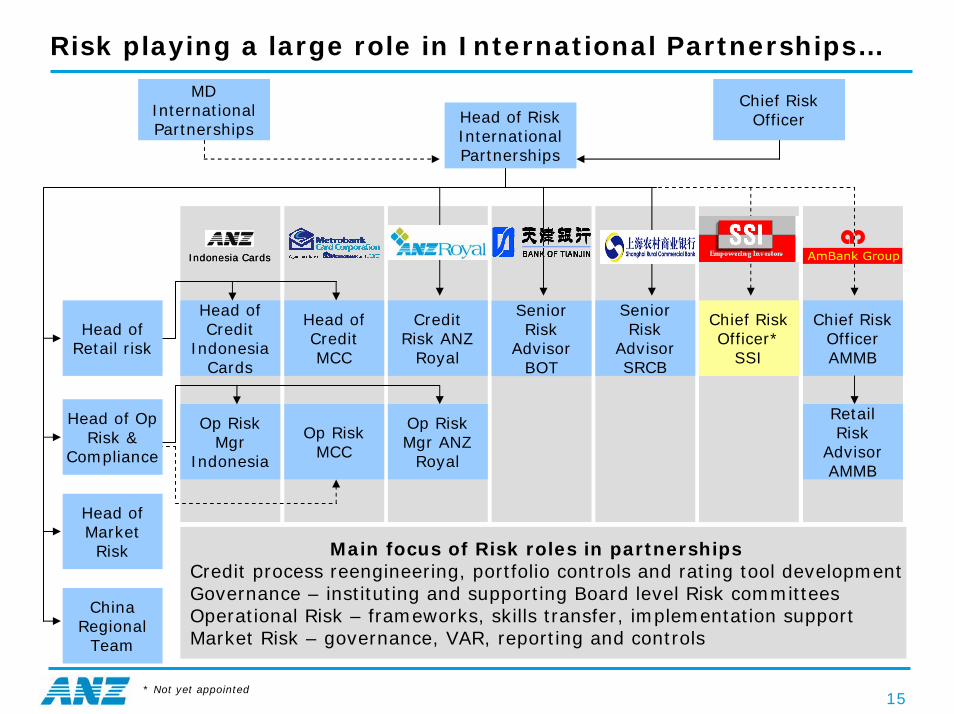

Risk playing a large role in International Partnerships…

Indonesia CardsIndonesia Cards

Head of Market Risk

China Regional

Team

Senior Risk

Advisor BOT

Chief Risk Officer AMMB

Credit Risk ANZ

Royal

Senior Risk

Advisor SRCB

Retail Risk

AdvisorAMMB

Op Risk Mgr ANZ

Royal

Op Risk Mgr

Indonesia

Op Risk MCC

Head of Credit

Indonesia Cards

Head of CreditMCC

Head of RiskInternational Partnerships

MD International Partnerships

Chief Risk Officer

Main focus of Risk roles in partnershipsCredit process reengineering, portfolio controls and rating tool developmentGovernance – instituting and supporting Board level Risk committeesOperational Risk – frameworks, skills transfer, implementation supportMarket Risk – governance, VAR, reporting and controls

Chief Risk Officer*

SSI

Head of Op Risk &

Compliance

Head of Retail risk

* Not yet appointed

16

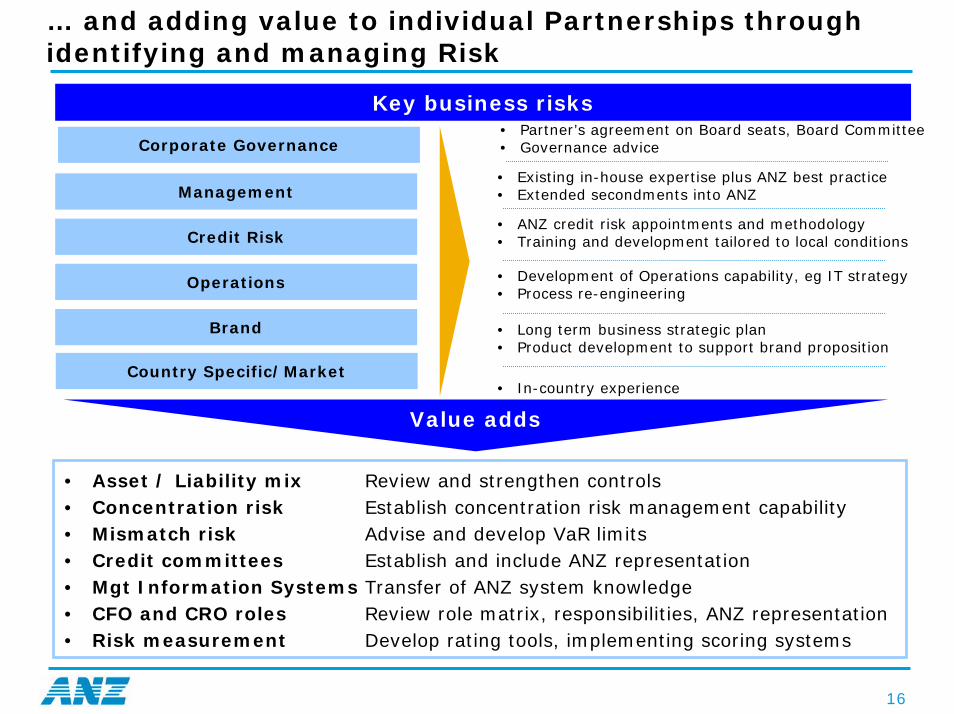

… and adding value to individual Partnerships through identifying and managing Risk

Management

Credit Risk

Brand

Operations

Country Specific/Market

• Long term business strategic plan• Product development to support brand proposition

• In-country experience

• Development of Operations capability, eg IT strategy• Process re-engineering

• Existing in-house expertise plus ANZ best practice• Extended secondments into ANZ

• ANZ credit risk appointments and methodology• Training and development tailored to local conditions

Key business risks

Corporate Governance• Partner’s agreement on Board seats, Board Committee• Governance advice

Value adds

• Asset / Liability mix Review and strengthen controls• Concentration risk Establish concentration risk management capability• Mismatch risk Advise and develop VaR limits• Credit committees Establish and include ANZ representation• Mgt Information Systems Transfer of ANZ system knowledge• CFO and CRO roles Review role matrix, responsibilities, ANZ representation• Risk measurement Develop rating tools, implementing scoring systems

17

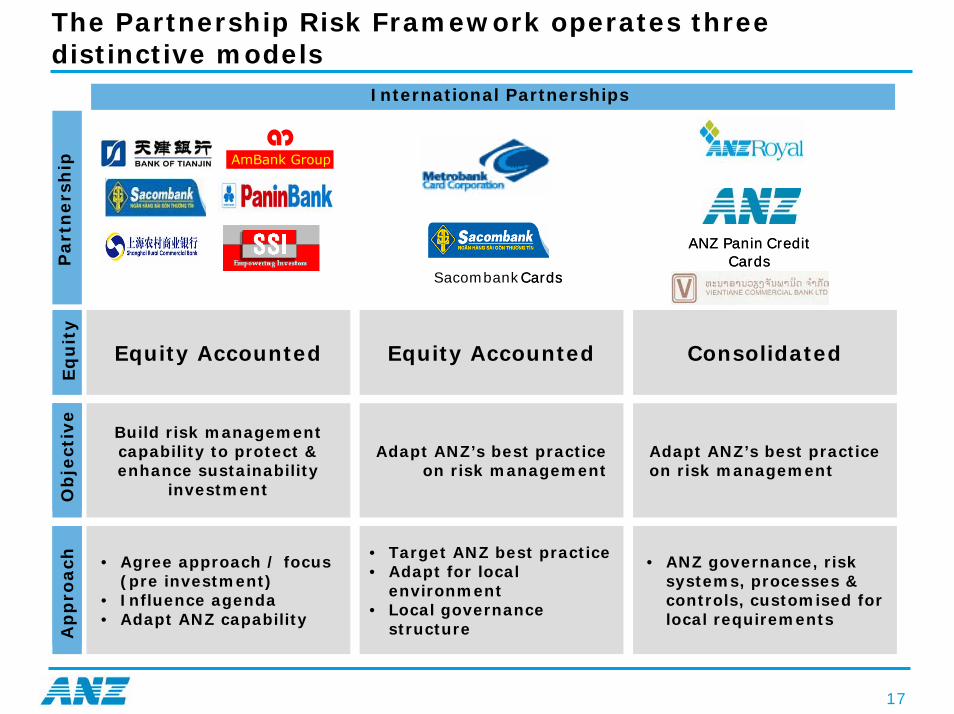

The Partnership Risk Framework operates three distinctive models

SacombankCards

ANZ Panin Credit Cards

Cards

ANZ Panin Credit Cards

Eq

uit

yP

art

ners

hip

International Partnerships

Equity Accounted Equity Accounted Consolidated

Ap

pro

ach

Ob

ject

ive

Ap

pro

ach

Ob

ject

ive

Adapt ANZ’s best practice on risk management

• ANZ governance, risk systems, processes & controls, customised for local requirements

• Agree approach / focus (pre investment)

• Influence agenda• Adapt ANZ capability

Adapt ANZ’s best practice on risk management

Build risk management capability to protect & enhance sustainability

investment

• Target ANZ best practice• Adapt for local

environment• Local governance

structure

18

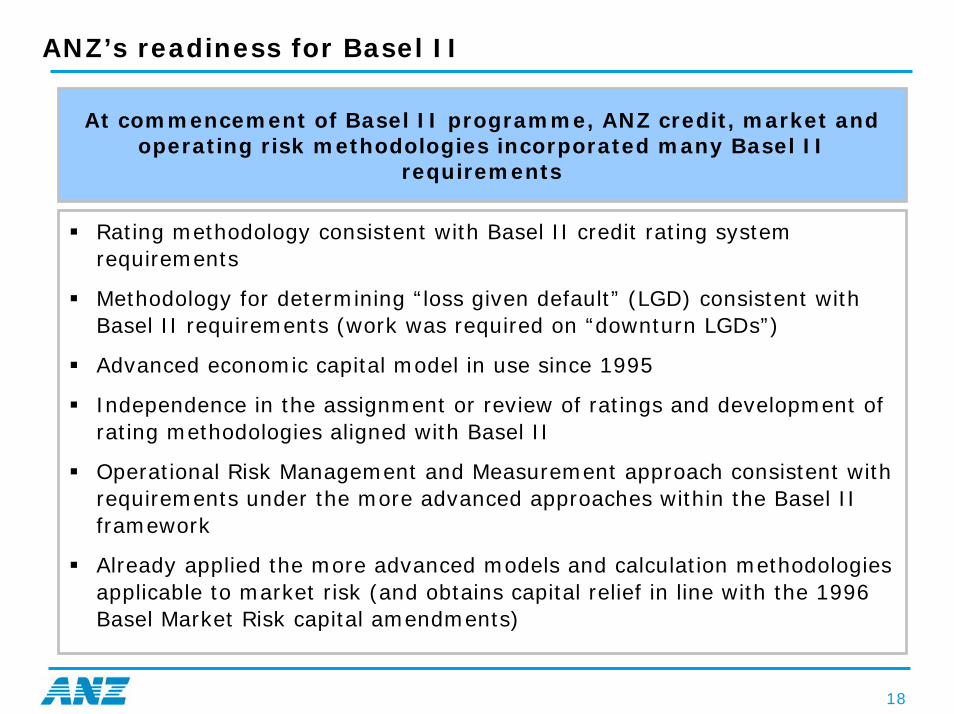

ANZ’s readiness for Basel II

At commencement of Basel II programme, ANZ credit, market and operating risk methodologies incorporated many Basel II

requirements

Rating methodology consistent with Basel II credit rating systemrequirements

Methodology for determining “loss given default” (LGD) consistent with Basel II requirements (work was required on “downturn LGDs”)

Advanced economic capital model in use since 1995

Independence in the assignment or review of ratings and development of rating methodologies aligned with Basel II

Operational Risk Management and Measurement approach consistent with requirements under the more advanced approaches within the Basel II framework

Already applied the more advanced models and calculation methodologies applicable to market risk (and obtains capital relief in line with the 1996 Basel Market Risk capital amendments)

19

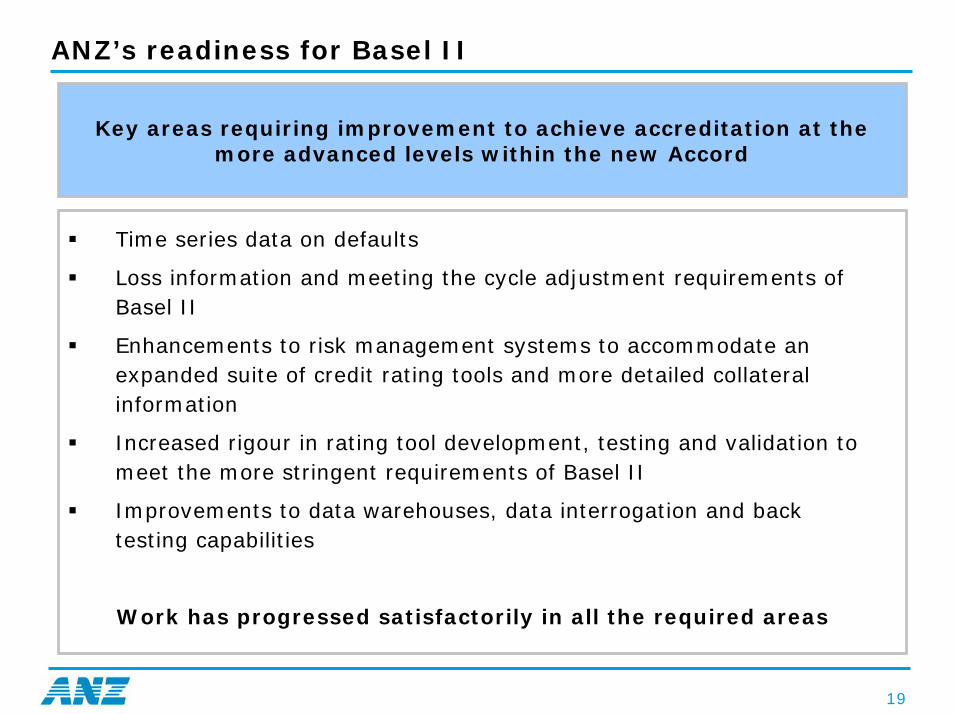

ANZ’s readiness for Basel II

Key areas requiring improvement to achieve accreditation at the more advanced levels within the new Accord

Time series data on defaults

Loss information and meeting the cycle adjustment requirements of Basel II

Enhancements to risk management systems to accommodate an expanded suite of credit rating tools and more detailed collateral information

Increased rigour in rating tool development, testing and validation to meet the more stringent requirements of Basel II

Improvements to data warehouses, data interrogation and back testing capabilities

Work has progressed satisfactorily in all the required areas

20

Other Risk matters

Inner city delinquencies

• No issues

• Previous large supply increase has been absorbed, lack of new supply coming on to market

Low Doc loans

• Lo doc 80 less than 1% of Portfolio

Sub prime market

• No exposure to sub-prime related RMBS or CDO issues.

• Total exposure to CDOs is $5.5m ($3m AA, $1m AA- and $1.5m BBB+)

• Total exposure to MBSs is $191m ($185.5 AAA, A $0.9m, AA $1.4m, AA- $1.6m, BBB $1.3m)

Anti Money Laundering

• Estimated total budgeted cost $66M over 3 years

21

Institutional lending growth – targeting a sensible balance

Focusing on optimal balance sheet usage

Focus on improving RORWA impacting lending growth

Institutional NLA (AUD $b) Highest growth from a major peer (12 months to Mar 2007)

20%

Target growth range to balance;• ROE/RORWA• Revenue

growth• Funding

capability• Debt recycling

*source: ANZ Economics

0%

5%

10%

15%

Institutional division growth (12 months to March 2007)

2007 forecast system growth*

ANZ “Old”Business Bank (12 months to March 07)

6.06.1

5.83.14.1 3.5

3.84.3

4.1

59.857.3

55.553.5

6.23.5

3.9

2H05 1H06 2H06 1H07 0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Australia New ZealandAsia Europe/AmericasTotal Growth Rate

66.569.5 71.4 73.3

(Annualised)

22

Additional information

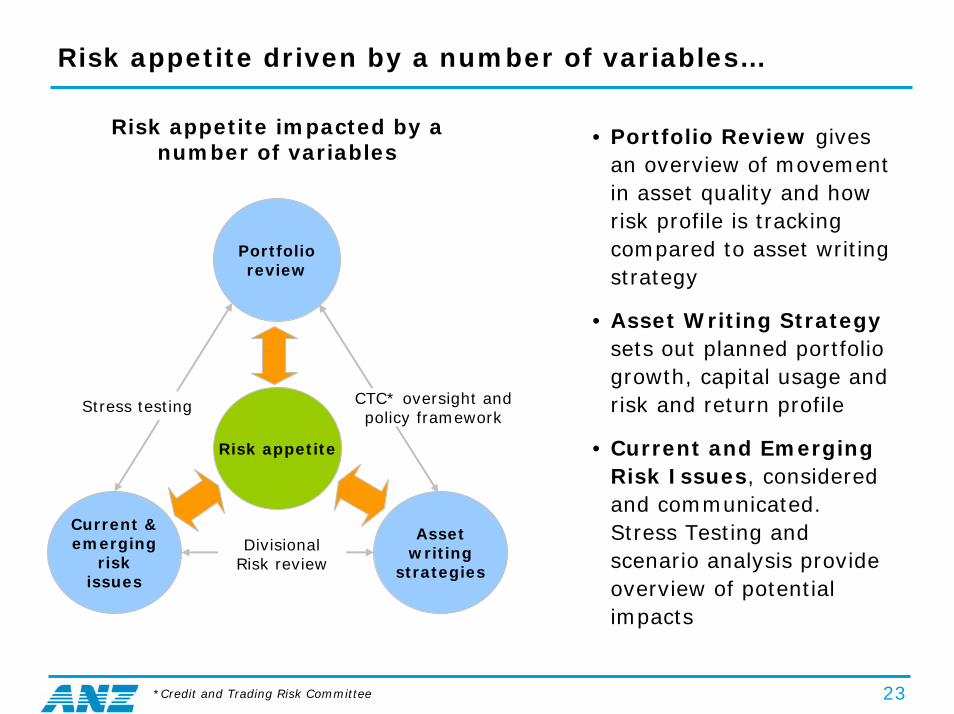

Risk appetite driven by a number of variables…

23

Asset writing

strategies

Risk appetite

Current & emerging

risk issues

Portfolio review

Stress testing

Divisional Risk review

CTC* oversight and policy framework

• Portfolio Review gives an overview of movement in asset quality and how risk profile is tracking compared to asset writing strategy

• Asset Writing Strategysets out planned portfolio growth, capital usage and risk and return profile

• Current and Emerging Risk Issues, considered and communicated. Stress Testing and scenario analysis provide overview of potential impacts

Risk appetite impacted by a number of variables

*Credit and Trading Risk Committee

24

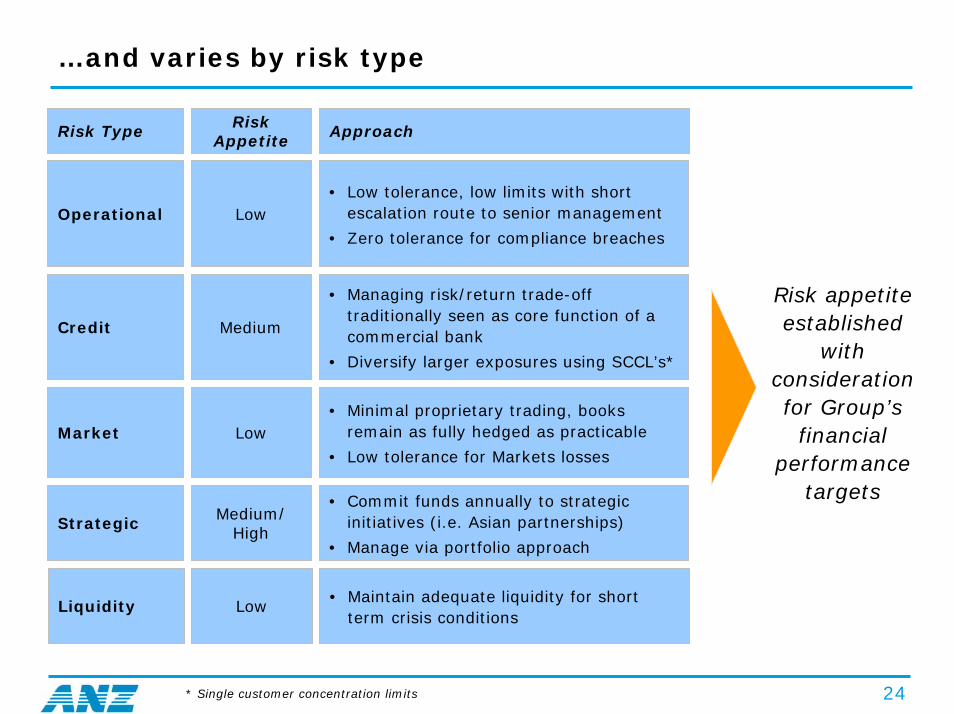

…and varies by risk type

Risk Type Risk Appetite

Approach

Operational Low• Low tolerance, low limits with short

escalation route to senior management

• Zero tolerance for compliance breaches

Credit Medium

• Managing risk/return trade-off traditionally seen as core function of a commercial bank

• Diversify larger exposures using SCCL’s*

Market Low• Minimal proprietary trading, books

remain as fully hedged as practicable

• Low tolerance for Markets losses

Strategic Medium/ High

• Commit funds annually to strategic initiatives (i.e. Asian partnerships)

• Manage via portfolio approach

Liquidity Low• Maintain adequate liquidity for short

term crisis conditions

Risk appetite established

with consideration for Group’s

financial performance

targets

* Single customer concentration limits

25

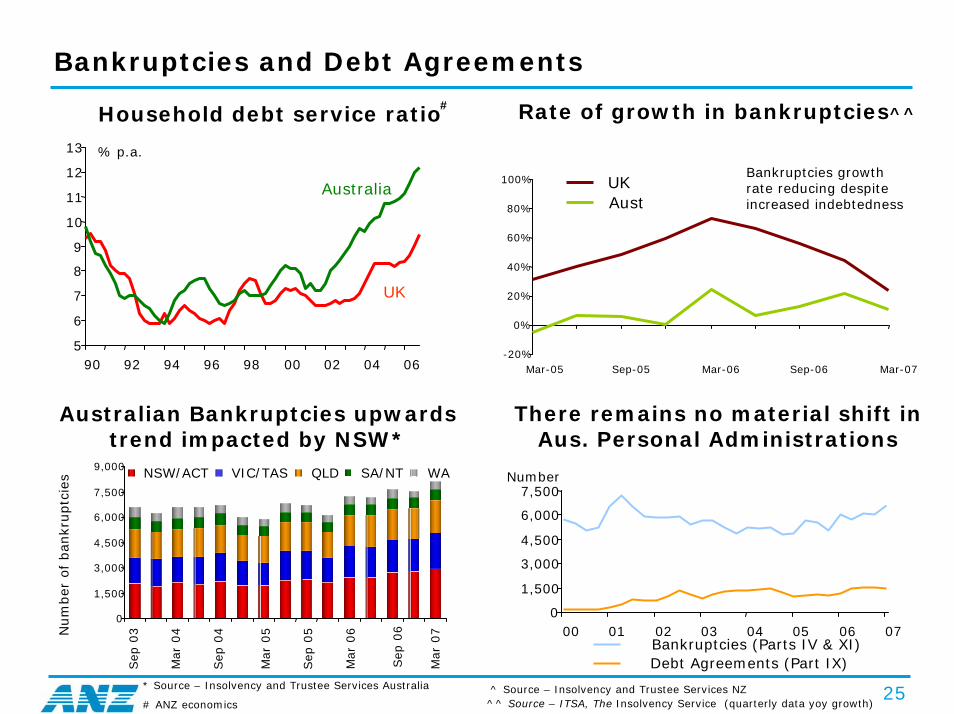

Bankruptcies and Debt Agreements

Australian Bankruptcies upwards trend impacted by NSW*

Sep

03

Mar

04

Sep

04

Mar

05

Sep

05

Mar

06

Sep

06

Mar

07Num

ber

of

ban

kruptc

ies

There remains no material shift in Aus. Personal Administrations

Number

Household debt service ratio

Australia

UK

Bankruptcies growth rate reducing despite increased indebtedness

# Rate of growth in bankruptcies^^

5

6

7

8

9

10

11

12

13

90 92 94 96 98 00 02 04 06

% p.a.

-20%

0%

20%

40%

60%

80%

100%

Mar-05 Sep-05 Mar-06 Sep-06 Mar-07

UKAust

0

1,500

3,000

4,500

6,000

7,500

9,000 NSW/ACT VIC/TAS QLD SA/NT WA

0

1,500

3,000

4,500

6,000

7,500

00 01 02 03 04 05 06 07Bankruptcies (Parts IV & XI)Debt Agreements (Part IX)

* Source – Insolvency and Trustee Services Australia

# ANZ economics^ Source – Insolvency and Trustee Services NZ^^ Source – ITSA, The Insolvency Service (quarterly data yoy growth)

26

Business Bank - Credit quality remains sound, some losses in 1H07 but no systemic issues

$m

Increase in Individual Provisions impacted by 3 customers(accounting for ~9% of 1H07 Group IPs)

^ Source: ANZ Economics research Includes facilities for which theultimate collectability of principle and interest is compromised

Portfolio is well secured across different risk bands

$2.1bn $12.6bn $1.1bn

* Delinquency data represents original Business Banking portfolio only

Very low levels of banking sector impaired assets^

(% of total assets)

Delinquency trends steady*

0%

20%

40%

60%

80%

100%

>BB+ BB+ to BB- <BB-Fully Secured Partly Secured Unsecured

0.0%

0.4%

0.8%

1.2%

Mar-03 Mar-04 Mar-05 Mar-06 Mar-07

>60 Days

0

5

10

15

20

1H06 2H06 1H070.0%

0.1%

0.2%

0.3%

0.4%

0.5%

Individual Provision Charge Loss Rate (RHS)

0.0

0.5

1.0

1.5

2.0

2.5

94 97 00 03 06

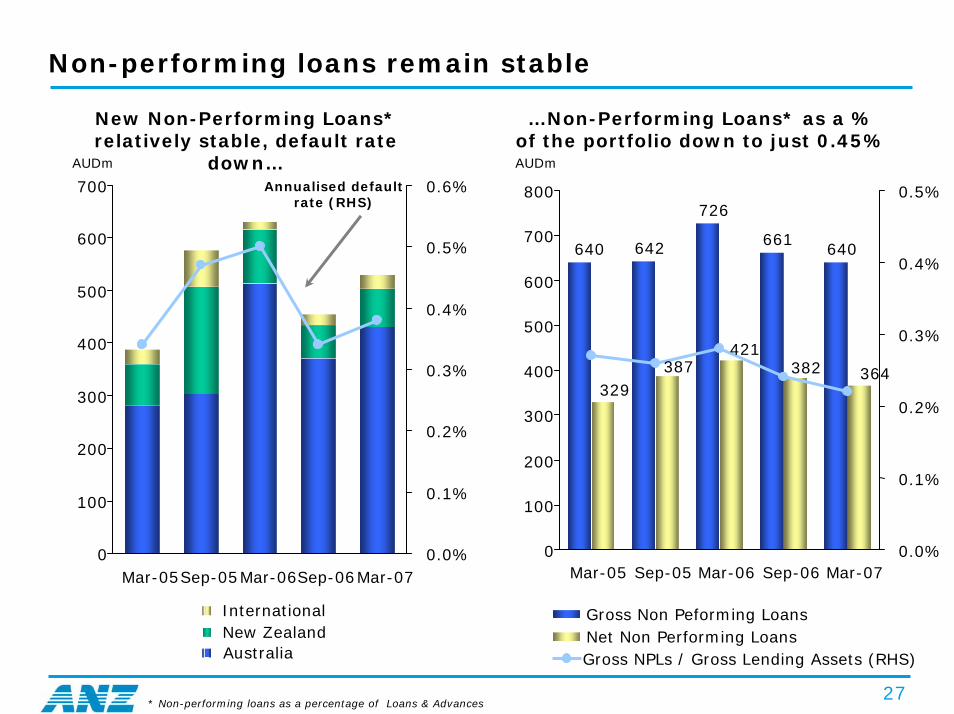

Non-performing loans remain stable

27

…Non-Performing Loans* as a % of the portfolio down to just 0.45%

New Non-Performing Loans* relatively stable, default rate

down…Annualised default

rate (RHS)

AUDmAUDm

0

100

200

300

400

500

600

700

Mar-05Sep-05Mar-06Sep-06Mar-070.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

InternationalNew ZealandAustralia

642

726

661640640

364382421

387329

0

100

200

300

400

500

600

700

800

Mar-05 Sep-05 Mar-06 Sep-06 Mar-070.0%

0.1%

0.2%

0.3%

0.4%

0.5%

Gross Non Peforming LoansNet Non Performing LoansGross NPLs / Gross Lending Assets (RHS)

* Non-performing loans as a percentage of Loans & Advances

28

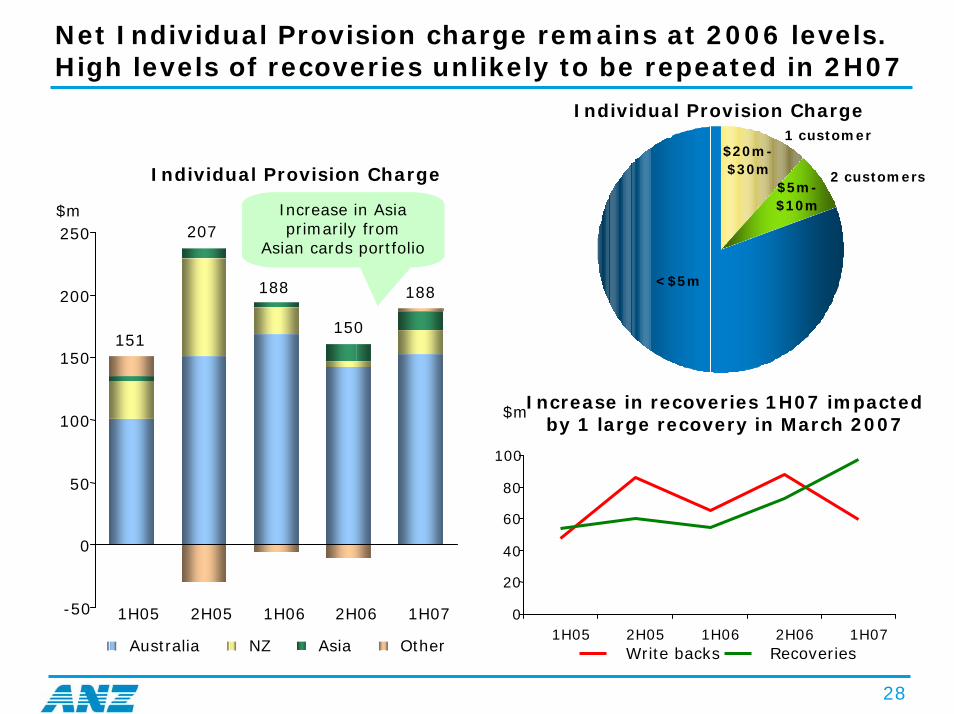

Net Individual Provision charge remains at 2006 levels. High levels of recoveries unlikely to be repeated in 2H07

Individual Provision Charge

Individual Provision Charge

$m

$m

$5m-$10m

$20m-$30m

<$5m

1 customer

2 customers

151

207

188

150

188

Increase in recoveries 1H07 impacted by 1 large recovery in March 2007

Increase in Asia primarily from

Asian cards portfolio

-50

0

50

100

150

200

250

1H05 2H05 1H06 2H06 1H07

Australia NZ Asia Other

0

20

40

60

80

100

1H05 2H05 1H06 2H06 1H07Write backs Recoveries

29

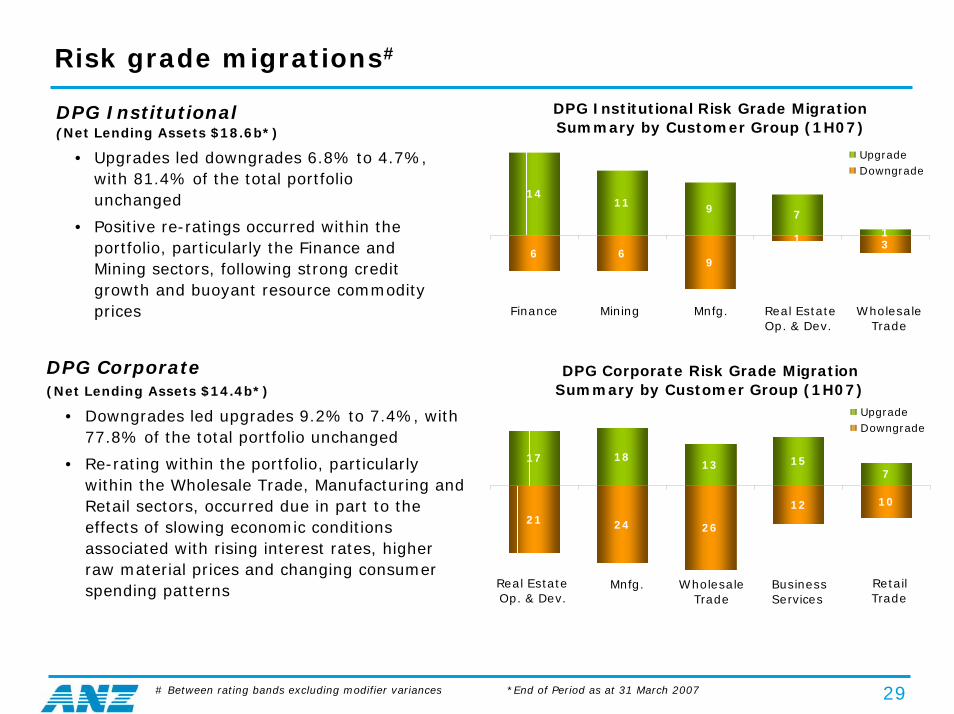

Risk grade migrations#

DPG Institutional Risk Grade Migration Summary by Customer Group (1H07)

1411 9 7

31

966

1

UpgradeDowngrade

Finance Mining Mnfg. Real EstateOp. & Dev.

WholesaleTrade

DPG Corporate Risk Grade MigrationSummary by Customer Group (1H07)

17 1813 15

7

1012

262421

UpgradeDowngrade

Real EstateOp. & Dev.

Mnfg. WholesaleTrade

Business Services

RetailTrade

DPG Institutional (Net Lending Assets $18.6b*)

• Upgrades led downgrades 6.8% to 4.7%, with 81.4% of the total portfolio unchanged

• Positive re-ratings occurred within the portfolio, particularly the Finance and Mining sectors, following strong credit growth and buoyant resource commodity prices

DPG Corporate(Net Lending Assets $14.4b*)

• Downgrades led upgrades 9.2% to 7.4%, with 77.8% of the total portfolio unchanged

• Re-rating within the portfolio, particularly within the Wholesale Trade, Manufacturing and Retail sectors, occurred due in part to the effects of slowing economic conditions associated with rising interest rates, higher raw material prices and changing consumer spending patterns

# Between rating bands excluding modifier variances *End of Period as at 31 March 2007

30

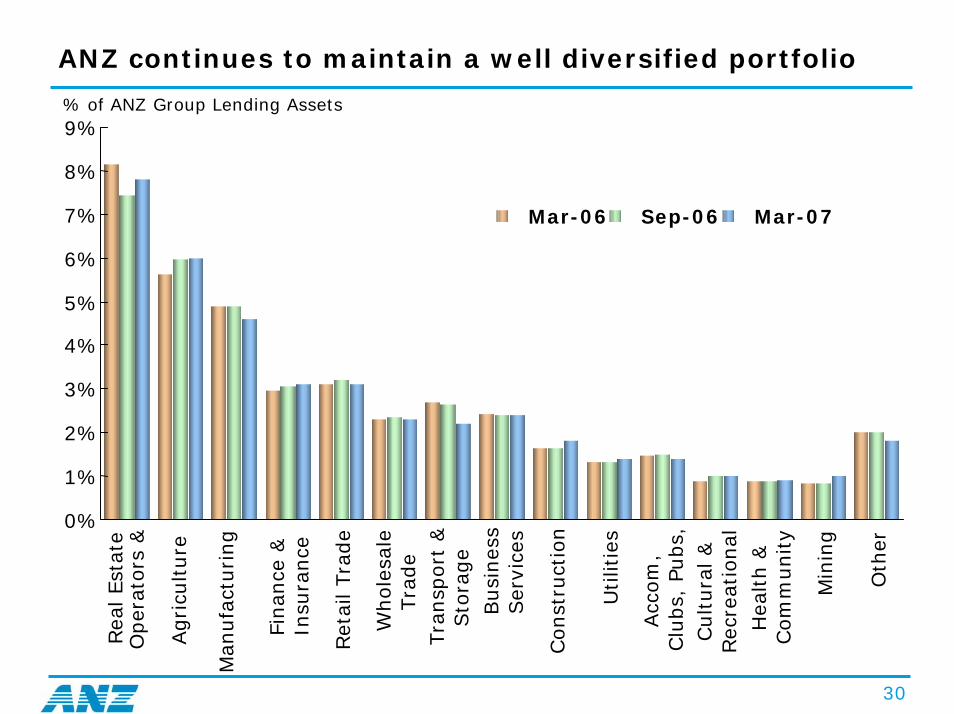

ANZ continues to maintain a well diversified portfolio

% of ANZ Group Lending Assets

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%Rea

l Est

ate

Oper

ators

&

Agricu

lture

Man

ufa

cturing

Finan

ce &

Insu

rance

Ret

ail Tra

de

Whole

sale

Tra

de

Tra

nsp

ort

&Sto

rage

Busi

nes

sSer

vice

s

Const

ruct

ion

Utilit

ies

Acc

om

,Clu

bs,

Pubs,

Cultura

l &

Rec

reat

ional

Hea

lth &

Com

munity

Min

ing

Oth

er

Mar-06 Sep-06 Mar-07

31

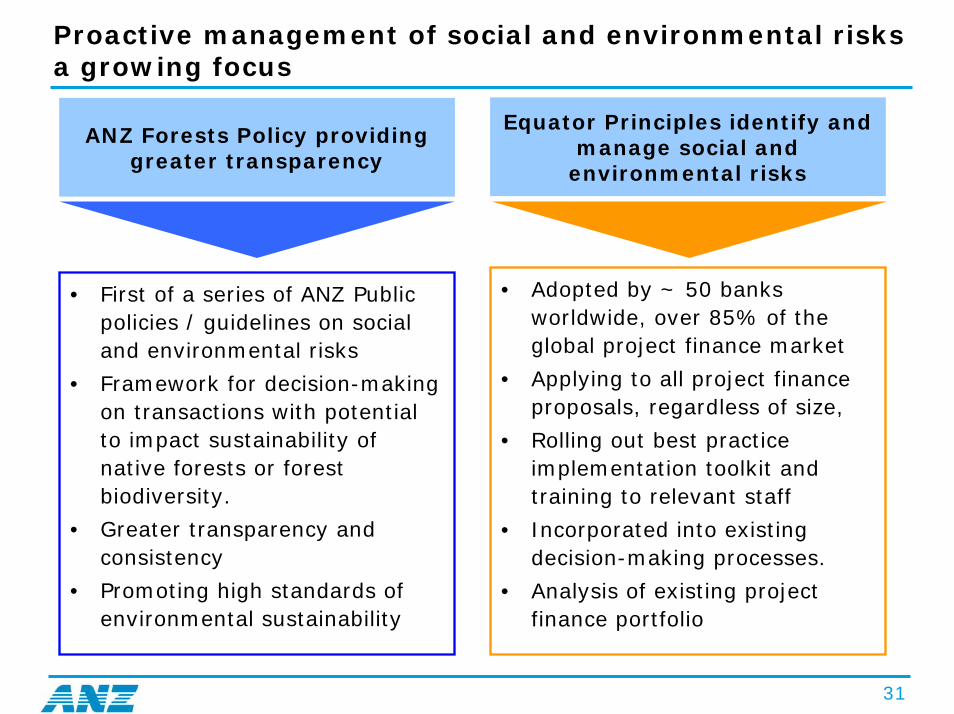

Proactive management of social and environmental risksa growing focus

Equator Principles identify and manage social and

environmental risks

ANZ Forests Policy providinggreater transparency

• Adopted by ~ 50 banks worldwide, over 85% of the global project finance market

• Applying to all project finance proposals, regardless of size,

• Rolling out best practice implementation toolkit and training to relevant staff

• Incorporated into existing decision-making processes.

• Analysis of existing project finance portfolio

• First of a series of ANZ Public policies / guidelines on social and environmental risks

• Framework for decision-making on transactions with potential to impact sustainability of native forests or forest biodiversity.

• Greater transparency and consistency

• Promoting high standards of environmental sustainability

32

Consumer Finance is at the forefront of Responsible Lending

ANZ Customer Charter includes new ‘responsible lending promises’ to prevent credit limit increase (CLI)

Enhanced filtering process excludes CLI offers to recent “poor” credit performers

A second behavioural scoring filter eliminates CLI offers to customers with “unreliable” credit history over a longer period

Behavioural scoring tool has effectively reduced the pool of customers to whom ANZ would have otherwise issued a CLI offer by 11%

ANZ’s performance is independently audited and reported each year - the only Australian bank to commit to formal, public, auditable responsible lending promises

Program will extend to all areas of ANZ Personal division

What are we doing?

Promoting

responsible

lending practices

to ANZ customers

with poor recent

credit

performance or

on income

support

33

Economic factors impacting the credit environment

34

Australian Credit Cycle Trends– Key Facts

Credit quality remains sound

• No clear signs of systemic deterioration

• Private sector credit growth strong (near 15%) but converging towards income growth

• Consumer confidence trending upwards since 2006

Increased household debt more than offset by growth in net assets

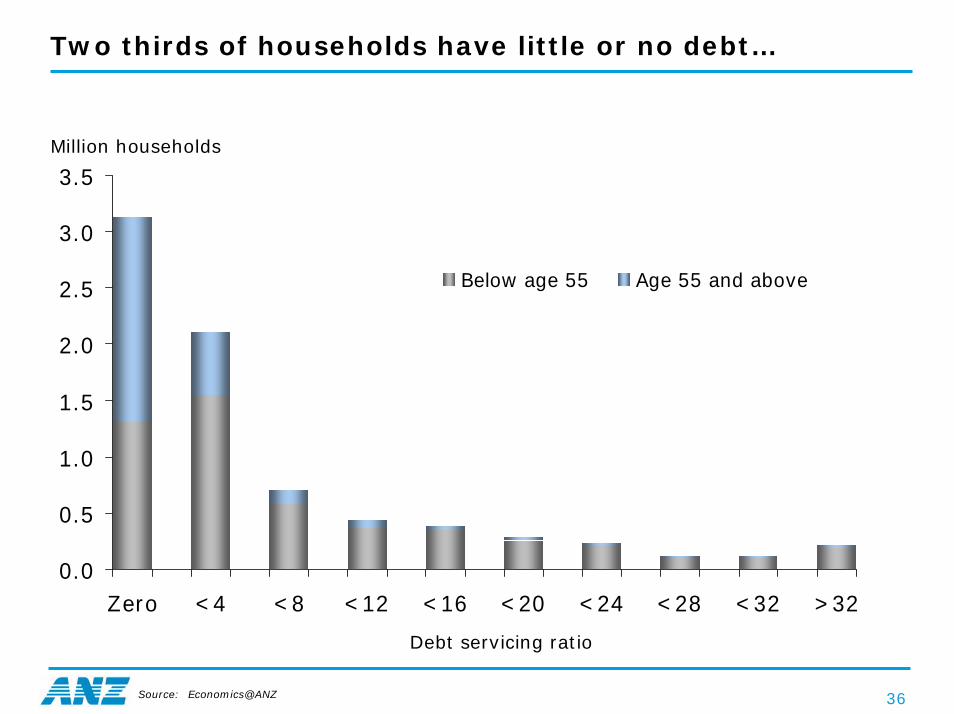

• 2/3 households have little or no debt

• HH debt to income and DSR at record levels but HH debt capacity high

– HH assets dwarf liabilities

– HH gearing increased<10% over 17years

• Housing affordability increasingly an issue

No indicators to support delinquency rise

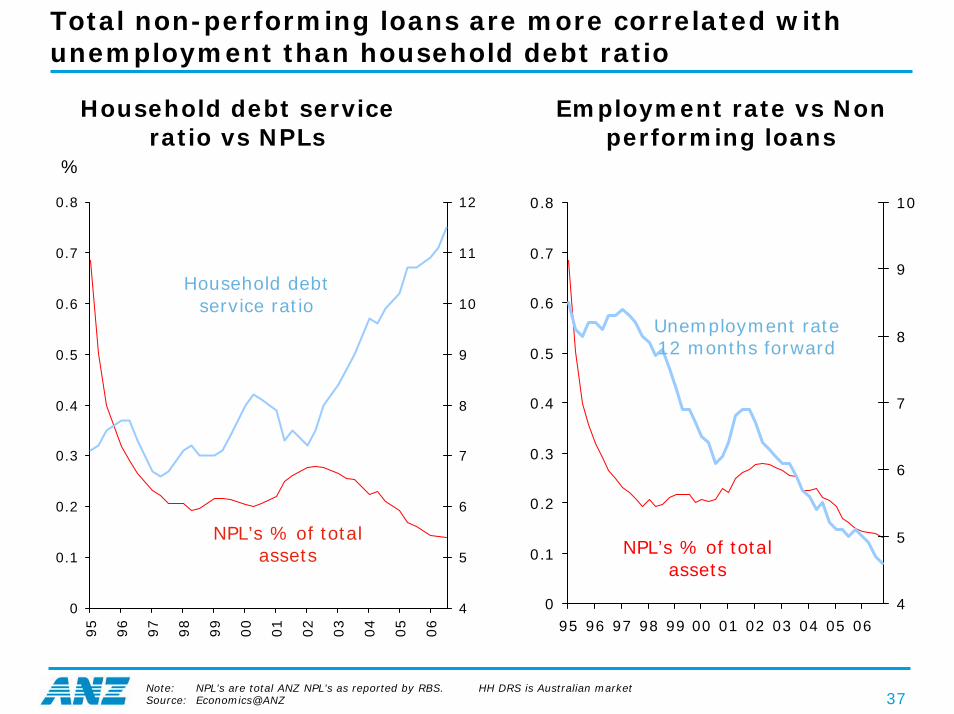

• No proven relationship between DSR and NPL

• High correlation between unemployment and NPLs - unemployment at 30 year lows

35

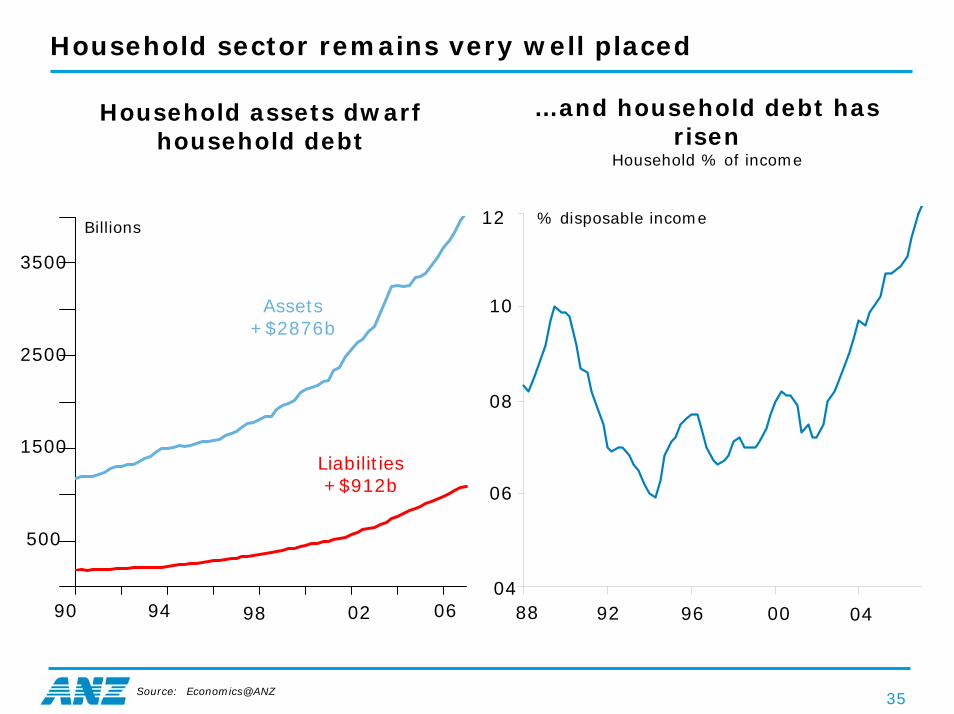

Household sector remains very well placed

Household assets dwarf household debt

…and household debt has risen

Household % of income

88 92 96 00 0490 94 98 02 06

06

08

10

12

04

1500

500

2500

3500

Assets+$2876b

Liabilities+$912b

% disposable incomeBillions

Source: Economics@ANZ

36

Two thirds of households have little or no debt…

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Zero <4 <8 <12 <16 <20 <24 <28 <32 >32

Below age 55 Age 55 and above

Million households

Debt servicing ratio

Source: Economics@ANZ

37

Total non-performing loans are more correlated with unemployment than household debt ratio

Household debt service ratio vs NPLs

Employment rate vs Non performing loans

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

95

96

97

98

99

00

01

02

03

04

05

06

4

5

6

7

8

9

10

11

12

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

95 96 97 98 99 00 01 02 03 04 05 064

5

6

7

8

9

10

Household debt service ratio

NPL’s % of total assets

%

Unemployment rate 12 months forward

NPL’s % of total assets

Note: NPL’s are total ANZ NPL’s as reported by RBS. HH DRS is Australian marketSource: Economics@ANZ

38

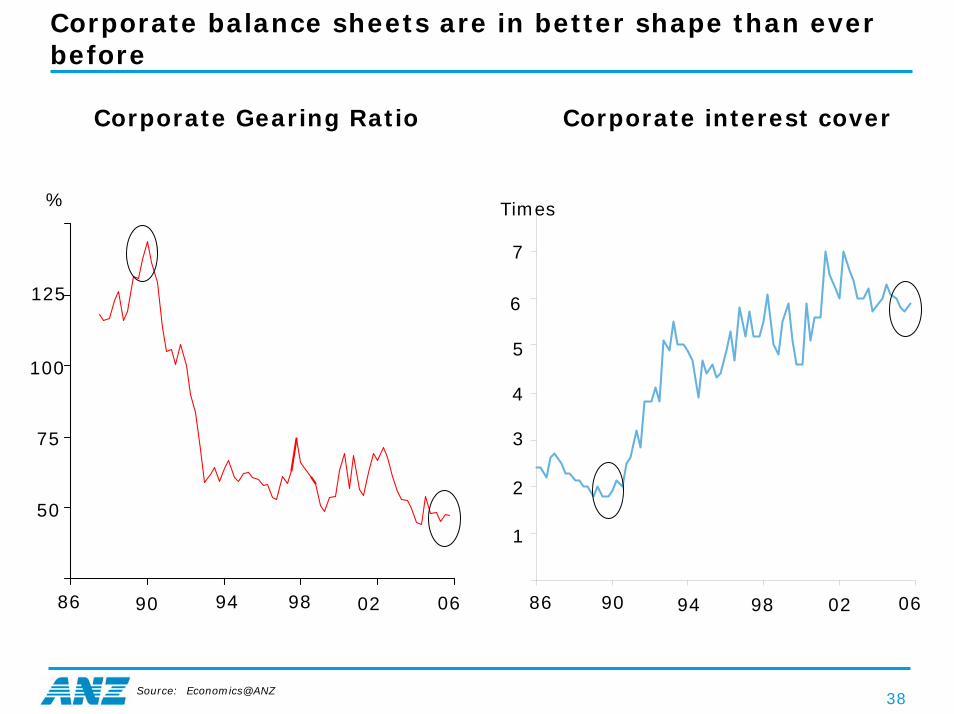

Corporate balance sheets are in better shape than ever before

Corporate Gearing Ratio Corporate interest cover

86 90 98 02 06 86 90 94 98 02 0694

1

3

5

7

50

75

125

100

6

4

2

% Times

Source: Economics@ANZ

39

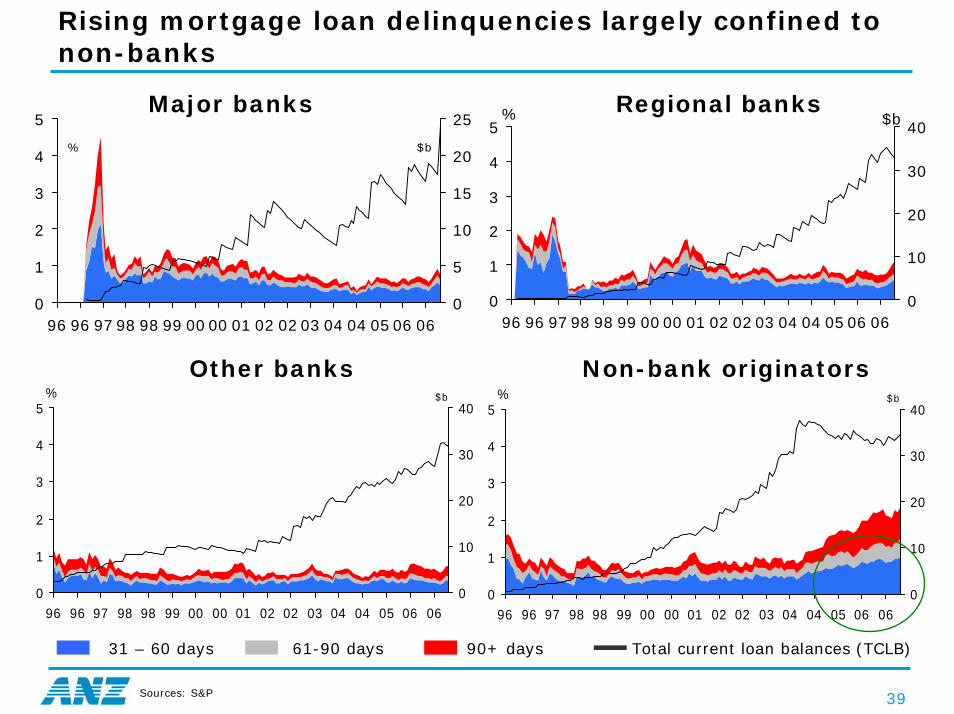

Rising mortgage loan delinquencies largely confined to non-banks

Major banks Regional banks

0

1

2

3

4

5

96 96 97 98 98 99 00 00 01 02 02 03 04 04 05 06 060

5

10

15

20

25

% $b

0

1

2

3

4

5

96 96 97 98 98 99 00 00 01 02 02 03 04 04 05 06 060

10

20

30

40% $b

0

1

2

3

4

5

96 96 97 98 98 99 00 00 01 02 02 03 04 04 05 06 060

10

20

30

40% $b

Non-bank originatorsOther banks

0

1

2

3

4

5

96 96 97 98 98 99 00 00 01 02 02 03 04 04 05 06 060

10

20

30

40% $b

31 – 60 days 61-90 days 90+ days Total current loan balances (TCLB)

Sources: S&P

40

The material in this presentation is general background information about the Bank’s activities current at the date of the presentation. It is information given in summary

form and does not purport to be complete. It is not intended to be relied upon as advice to investors or potential investors and does not take into account the investment

objectives, financial situation or needs of any particular investor. These should be considered, with or without professional advice when deciding if an investment is

appropriate.

For further information visit

www.anz.comor contact

Stephen HigginsHead of Investor Relations

ph: (613) 9273 4185 fax: (613) 9273 4899 e-mail: [email protected]