Page 1

www.eia.govU.S. Energy Information Administration Independent Statistics & Analysis

What drives crude oil prices?

April 12, 2016 | Washington, DC

An analysis of 7 factors that influence oil markets,

with chart data updated monthly and quarterly

Page 2

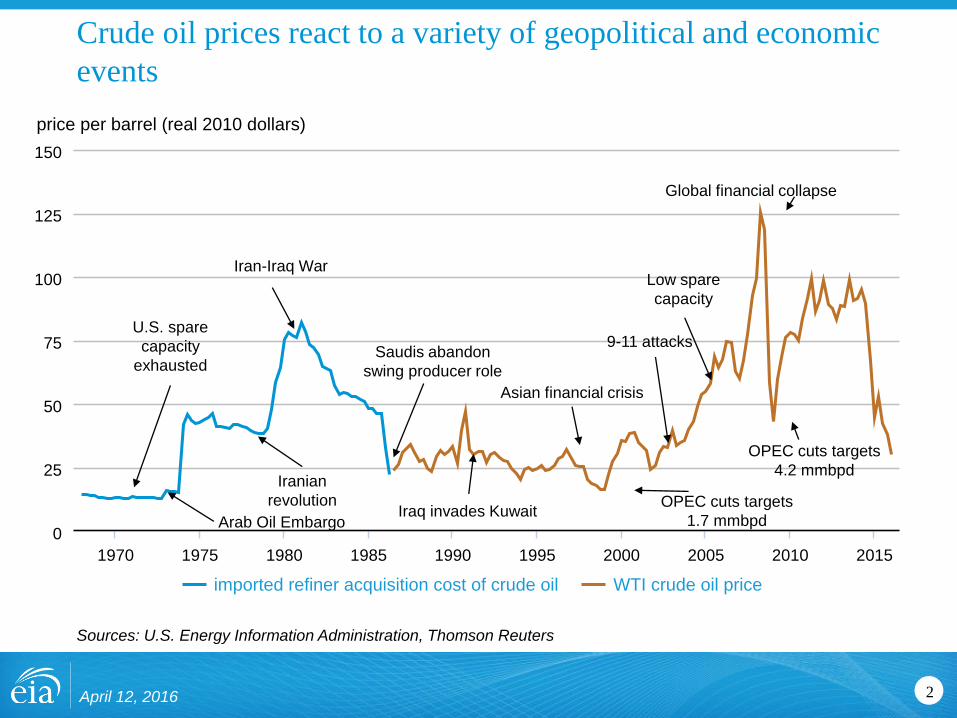

price per barrel (real 2010 dollars)

imported refiner acquisition cost of crude oil WTI crude oil price

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

0

25

50

75

100

125

150

Crude oil prices react to a variety of geopolitical and economic

events

April 12, 2016 2

Low spare

capacity

Iraq invades Kuwait

Saudis abandon

swing producer role

Iran-Iraq War

Iranian

revolution

Arab Oil Embargo

Asian financial crisis

U.S. spare

capacity

exhausted

Global financial collapse

9-11 attacks

OPEC cuts targets

1.7 mmbpd

OPEC cuts targets

4.2 mmbpd

Sources: U.S. Energy Information Administration, Thomson Reuters

Page 3

World oil prices move together due to arbitrage

3

Sources: Bloomberg, Thomson Reuters

April 12, 2016

$/bbl (real 2010 dollars, monthly average)

WTI Brent Mars Tapis Dubai

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

0

20

40

60

80

100

120

140

160

Page 4

Crude oil prices are the primary driver of petroleum product

prices

4

Sources: EIA Short Term Energy Outlook, Thomson Reuters

April 12, 2016

Page 5

Economic growth has a strong impact on oil consumption

5

Sources: U.S. Energy Information Administration, IHS Global Insight

April 12, 2016

Page 6

Changes in expectations of economic growth in can affect oil

prices

6

Source: IHS Global Insight

April 12, 2016

percent GDP growth in non-OECD countries (annual expectations)

forecast year: 2013 2014 2015 2016 2017

2012 2013 2014 2015 2016

0

2

4

6

8

Note: Starting in January of each year, each line shows the expected forecast of GDP growth for the specified calendar year, which tends

to move toward the actual realized growth outcome as the year progresses. Expectations continue to evolve into the next calendar year as

revised GDP data become available (e.g., 2008 GDP expectations are revised even during 2009).

Page 7

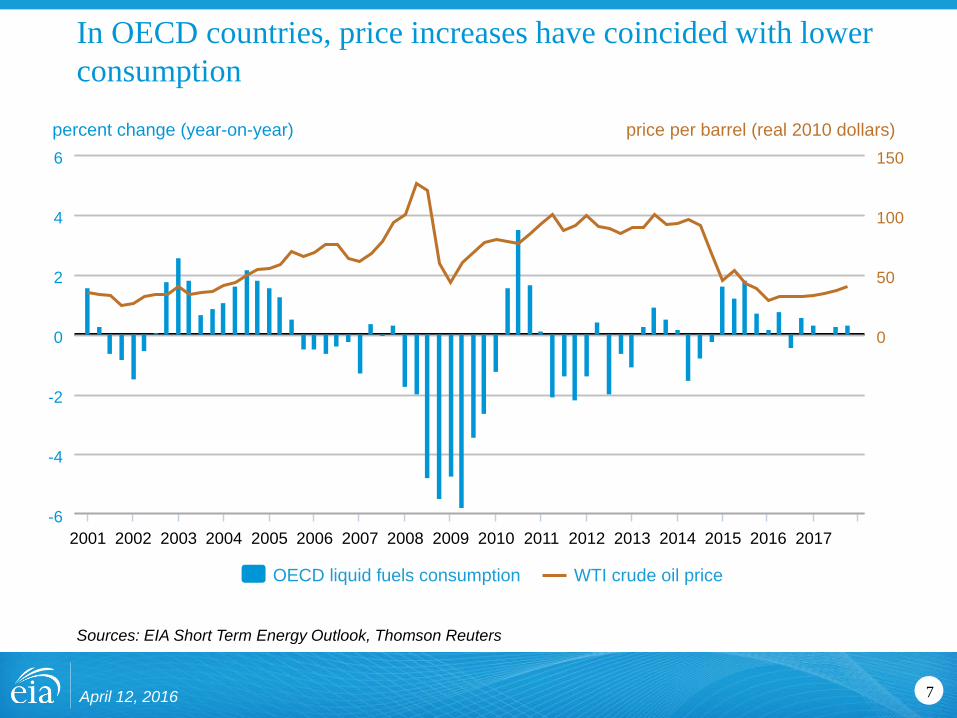

In OECD countries, price increases have coincided with lower

consumption

7

Sources: EIA Short Term Energy Outlook, Thomson Reuters

April 12, 2016

percent change (year-on-year) price per barrel (real 2010 dollars)

OECD liquid fuels consumption WTI crude oil price

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

2018

-6

-4

-2

0

2

4

6

0

50

100

150

Page 8

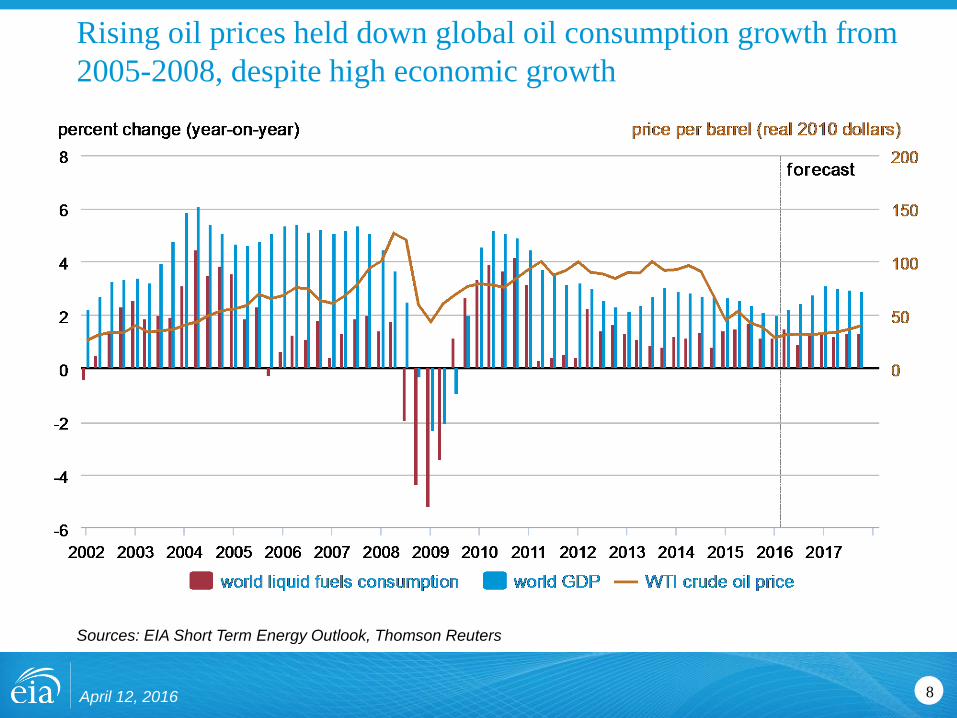

Rising oil prices held down global oil consumption growth from

2005-2008, despite high economic growth

8

Sources: EIA Short Term Energy Outlook, Thomson Reuters

April 12, 2016

Page 9

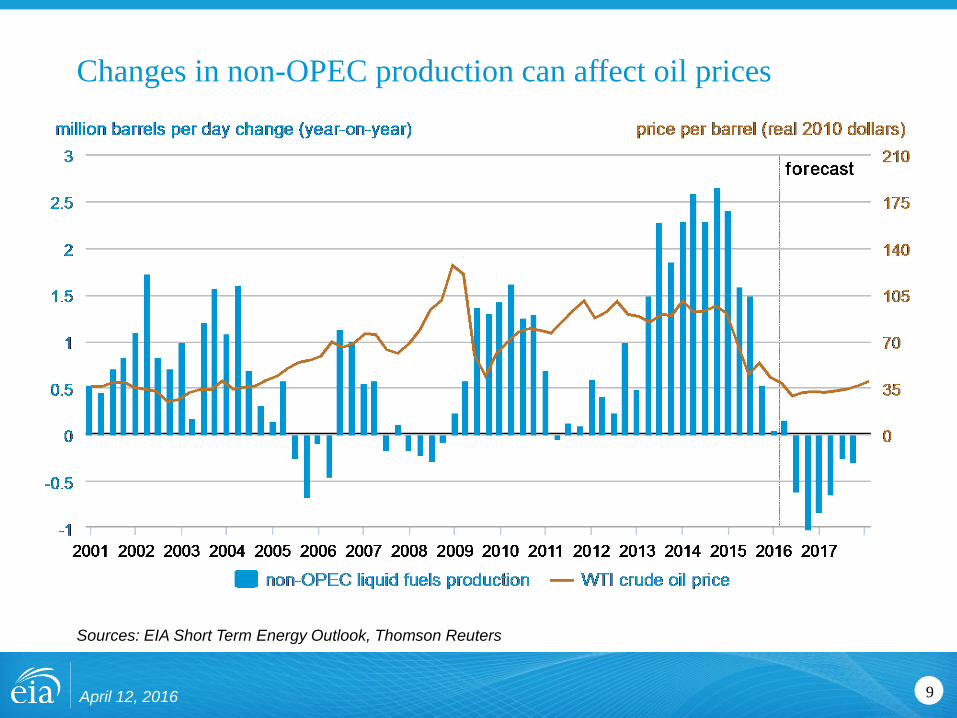

Changes in non-OPEC production can affect oil prices

9

Sources: EIA Short Term Energy Outlook, Thomson Reuters

April 12, 2016

Page 10

million barrels per day (annual expectations)

forecast year: 2013 2014 2015 2016 2017

2012 2013 2014 2015 2016

52.5

53.0

53.5

54.0

54.5

55.0

55.5

56.0

56.5

57.0

57.5

58.0

58.5

59.0

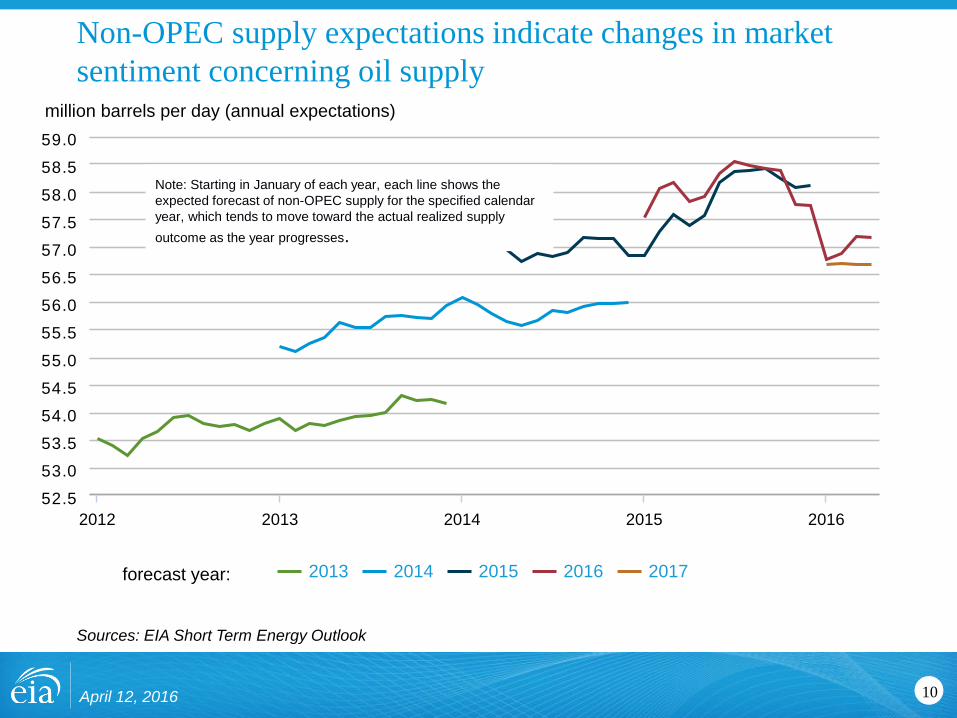

Non-OPEC supply expectations indicate changes in market

sentiment concerning oil supply

10

Sources: EIA Short Term Energy Outlook

Note: Starting in January of each year, each line shows the

expected forecast of non-OPEC supply for the specified calendar

year, which tends to move toward the actual realized supply

outcome as the year progresses.

April 12, 2016

Page 11

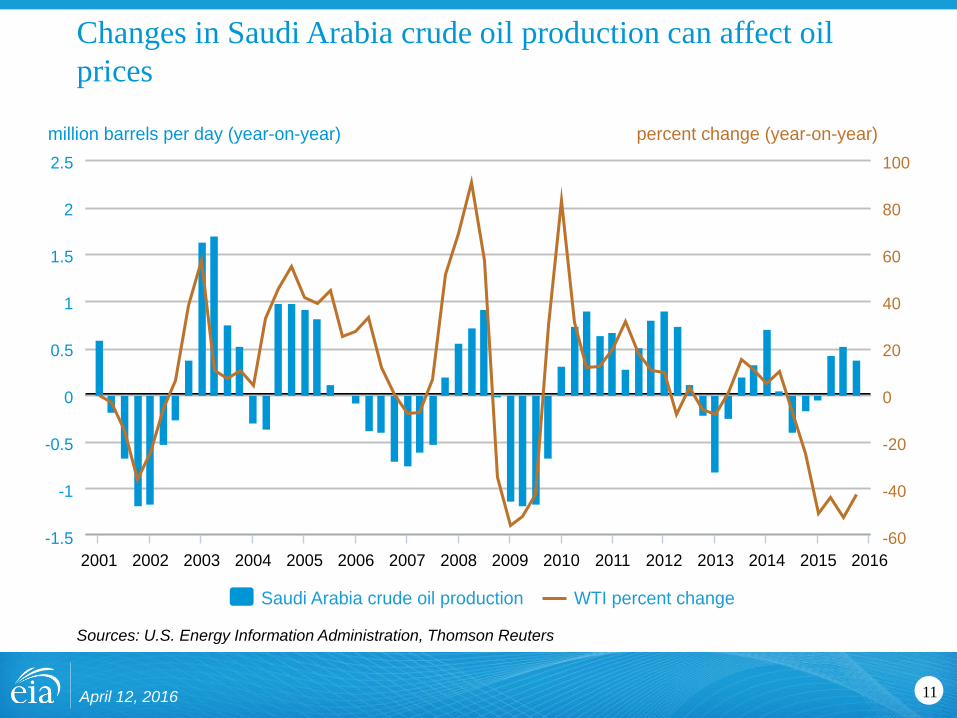

Changes in Saudi Arabia crude oil production can affect oil

prices

11

Sources: U.S. Energy Information Administration, Thomson Reuters

April 12, 2016

million barrels per day (year-on-year) percent change (year-on-year)

Saudi Arabia crude oil production WTI percent change

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

-60

-40

-20

0

20

40

60

80

100

Page 12

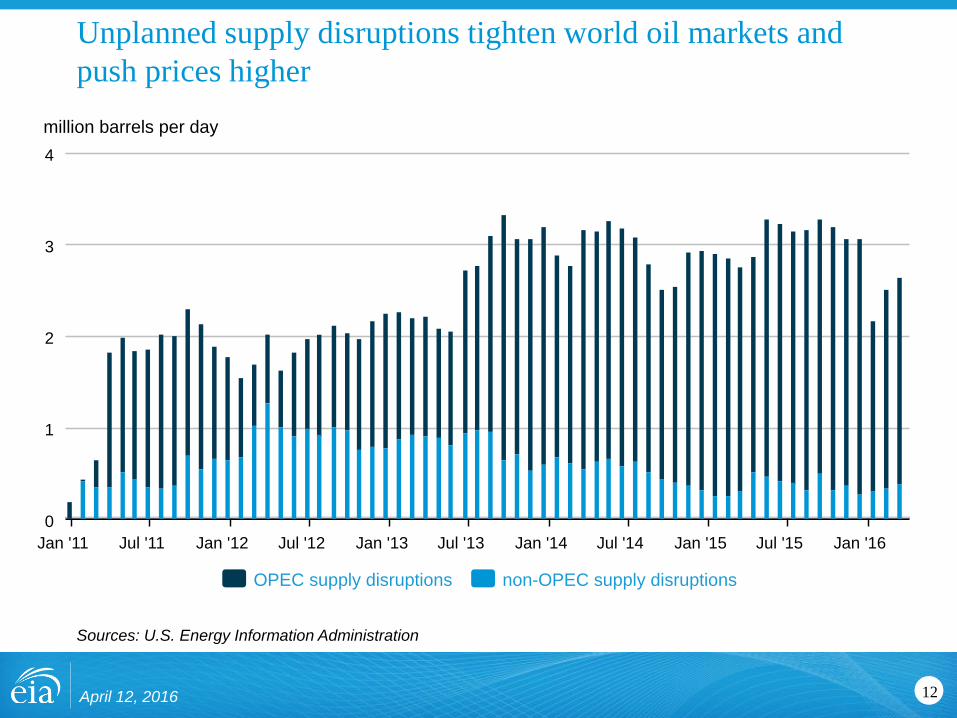

Sources: U.S. Energy Information Administration

Unplanned supply disruptions tighten world oil markets and

push prices higher

12April 12, 2016

million barrels per day

OPEC supply disruptions non-OPEC supply disruptions

Jan '11 Jul '11 Jan '12 Jul '12 Jan '13 Jul '13 Jan '14 Jul '14 Jan '15 Jul '15 Jan '16

0

1

2

3

4

Page 13

Sources: EIA Short Term Energy Outlook, Thomson Reuters

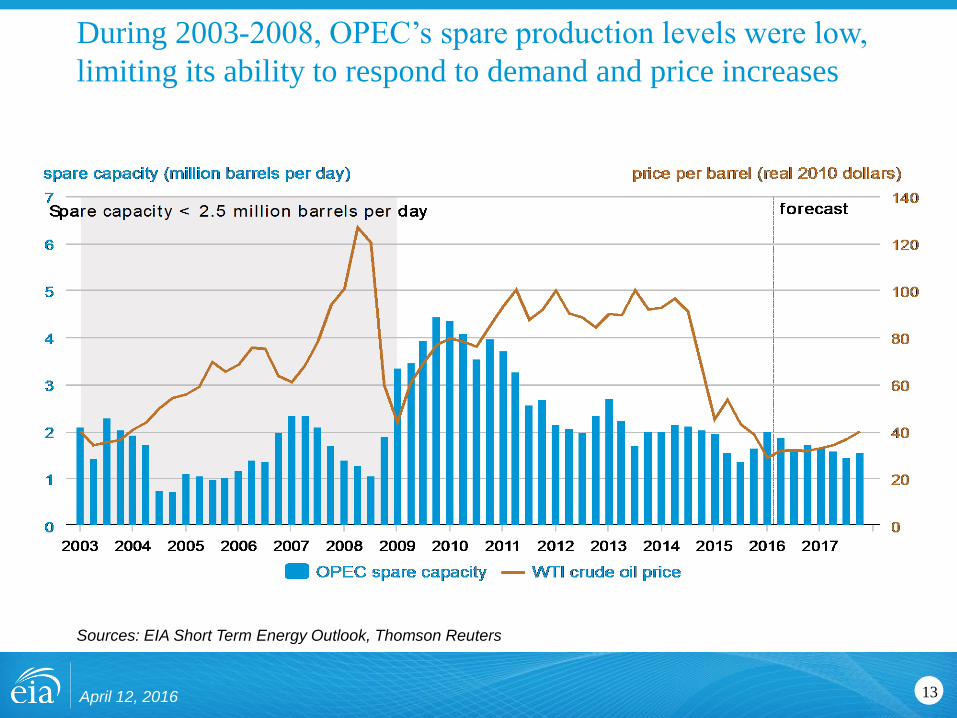

During 2003-2008, OPEC’s spare production levels were low,

limiting its ability to respond to demand and price increases

13April 12, 2016

Page 14

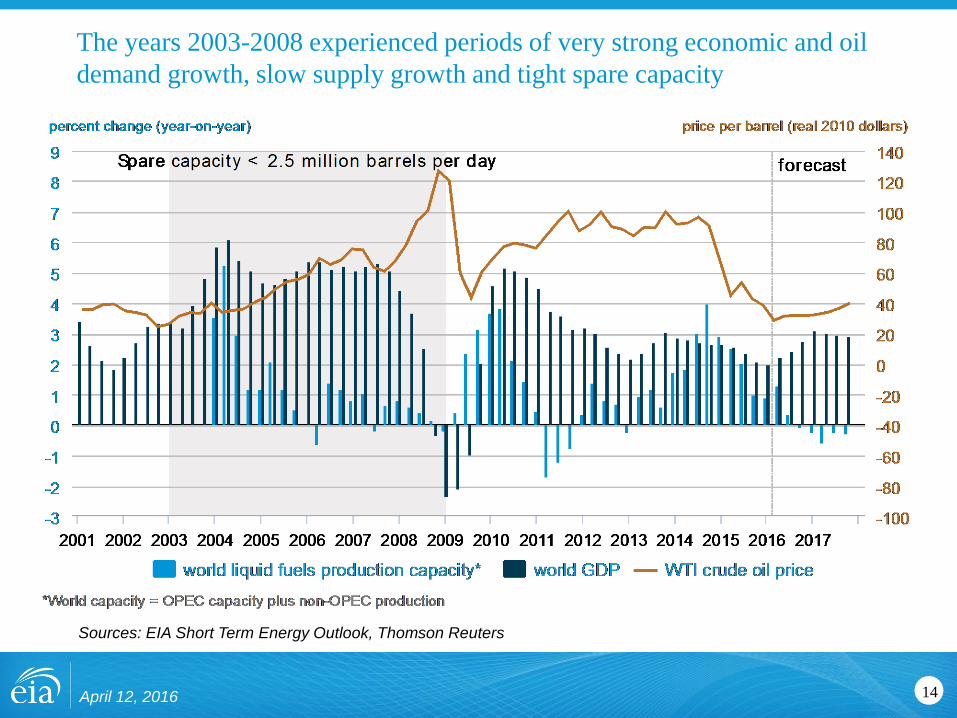

The years 2003-2008 experienced periods of very strong economic and oil

demand growth, slow supply growth and tight spare capacity

14

Sources: EIA Short Term Energy Outlook, Thomson Reuters

April 12, 2016

Page 15

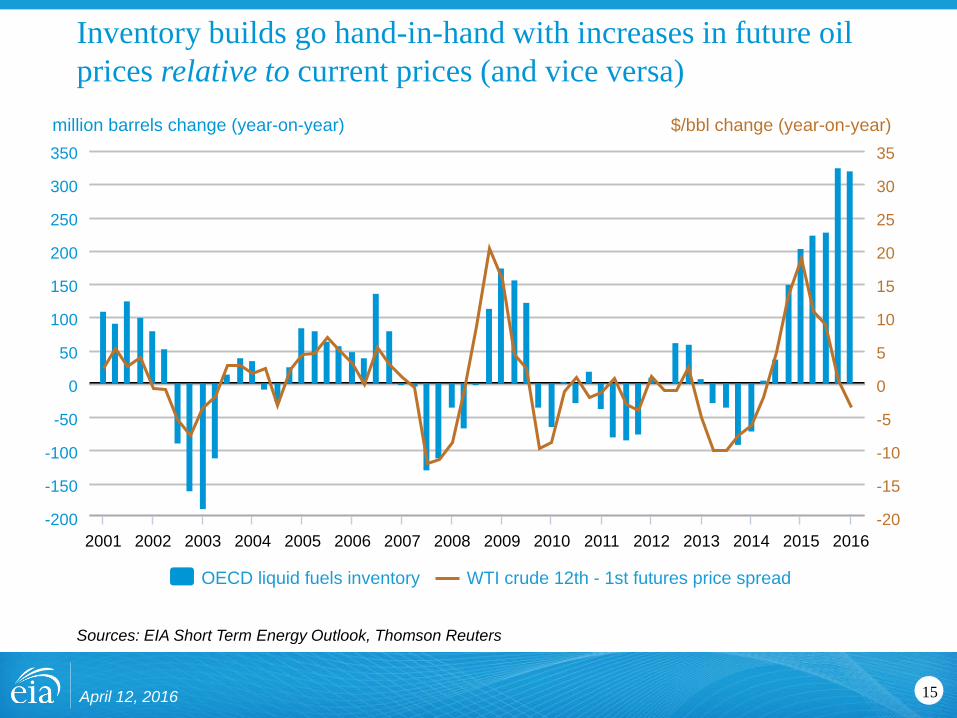

Inventory builds go hand-in-hand with increases in future oil

prices relative to current prices (and vice versa)

15

Sources: EIA Short Term Energy Outlook, Thomson Reuters

April 12, 2016

million barrels change (year-on-year) $/bbl change (year-on-year)

OECD liquid fuels inventory WTI crude 12th - 1st futures price spread

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

-200

-150

-100

-50

0

50

100

150

200

250

300

350

-20

-15

-10

-5

0

5

10

15

20

25

30

35

Page 16

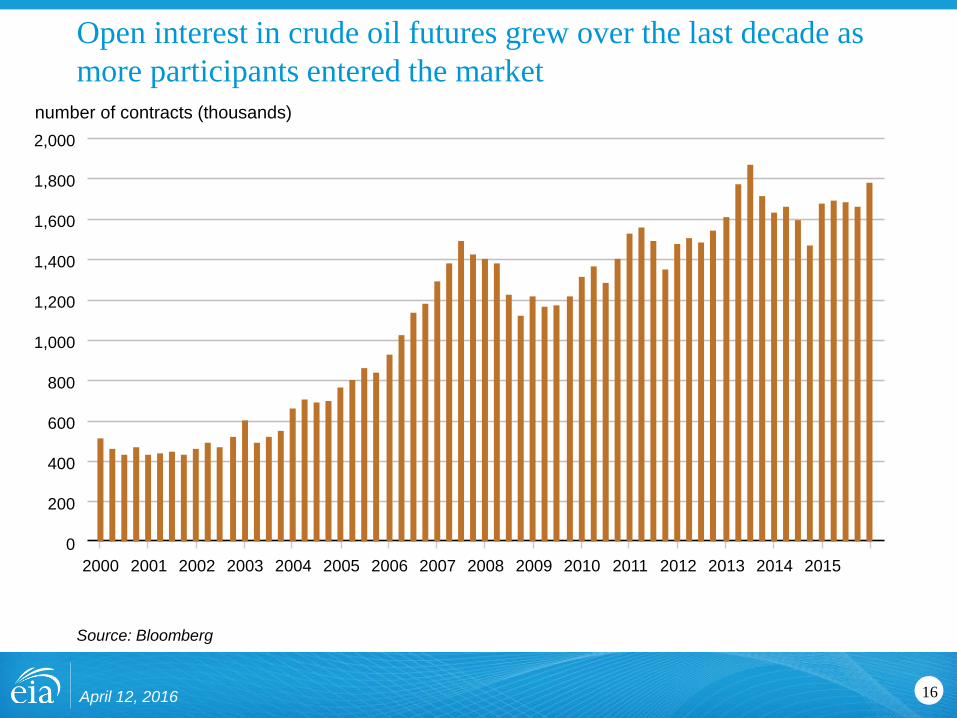

Open interest in crude oil futures grew over the last decade as

more participants entered the market

16

Source: Bloomberg

April 12, 2016

number of contracts (thousands)

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

2016

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Page 17

Physical participants’ (producers, merchants, processors, and end users) U.S.

futures market contract positions

17

Source: CFTC Commitment of Traders

April 12, 2016

number of contracts (thousands)

producers/merchants long producers/merchants short producers/merchants net

2008 2009 2010 2011 2012 2013 2014 2015 2016

-600

-500

-400

-300

-200

-100

0

100

200

300

400

500

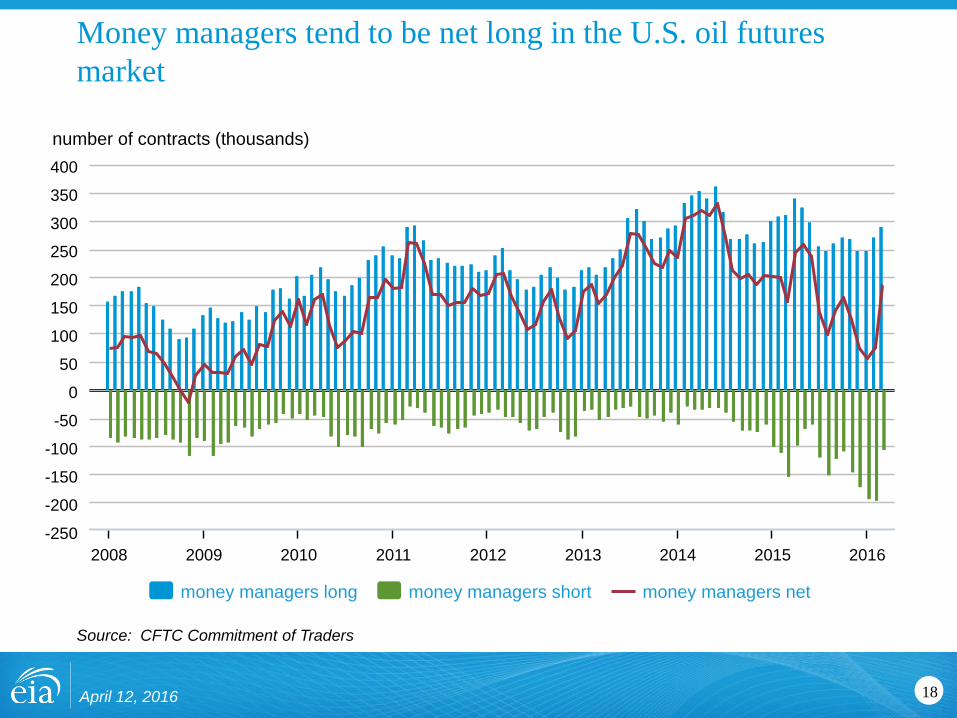

Page 18

Money managers tend to be net long in the U.S. oil futures

market

18

Source: CFTC Commitment of Traders

April 12, 2016

number of contracts (thousands)

money managers long money managers short money managers net

2008 2009 2010 2011 2012 2013 2014 2015 2016

-250

-200

-150

-100

-50

0

50

100

150

200

250

300

350

400

Page 19

Crude oil plays a major role in commodity investment

19

2015 Target Weights of the Bloomberg Commodity Index

Source: Bloomberg

April 12, 2016

Crude Oil: WTI: 7.8 %

Crude Oil: Brent: 7.2 %

Natural Gas: 8.7 %

Heating Oil: 3.8 %

Gasoline: 3.7 %

Corn: 7.2 %

Soybeans: 5.7 %

Wheat: 4.5 %Sugar: 4.0 %

Soybean Oil: 2.8 %

Soy Meal: 2.7 %

Coffee: 2.2 %

Cotton: 1.5 %

Gold: 11.9 %

Copper: 7.5 %

Aluminum: 4.6 %

Silver: 4.3 %

Zinc: 2.4 %

Nickel: 2.1 %

Live Cattle: 3.3 %

Lean Hogs: 1.9 %

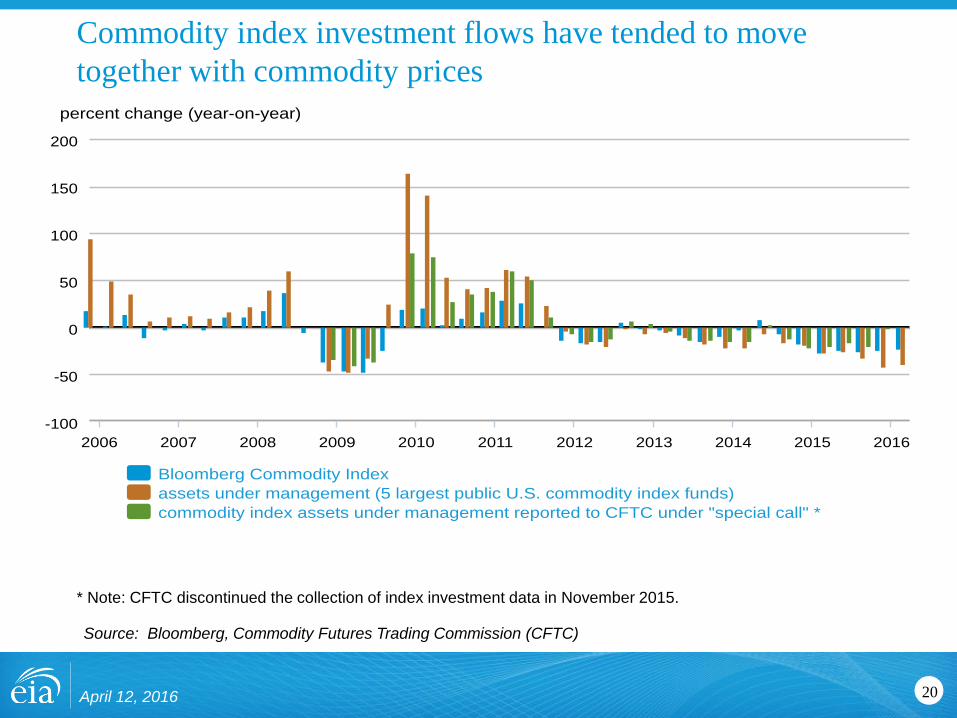

Page 20

Commodity index investment flows have tended to move

together with commodity prices

20

* Note: CFTC discontinued the collection of index investment data in November 2015.

April 12, 2016

percent change (year-on-year)

Bloomberg Commodity Index

assets under management (5 largest public U.S. commodity index funds)

commodity index assets under management reported to CFTC under "special call" *

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

-100

-50

0

50

100

150

200

Source: Bloomberg, Commodity Futures Trading Commission (CFTC)

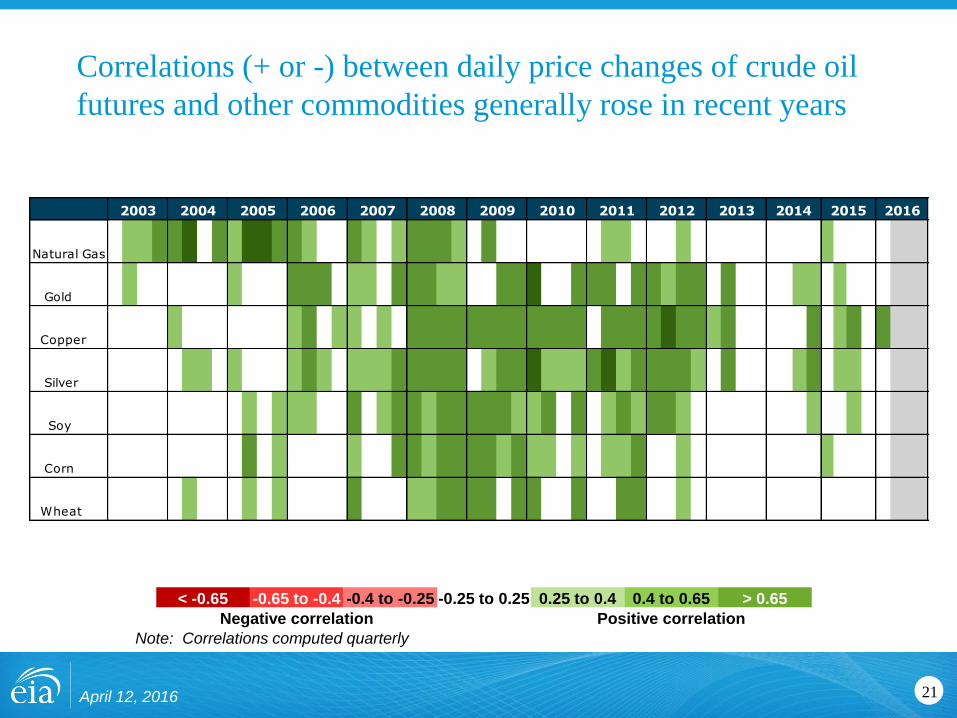

Page 21

Correlations (+ or -) between daily price changes of crude oil

futures and other commodities generally rose in recent years

21

Note: Correlations computed quarterly

< -0.65 -0.65 to -0.4 -0.4 to -0.25 -0.25 to 0.25 0.25 to 0.4 0.4 to 0.65 > 0.65

Negative correlation Positive correlation

April 12, 2016

Date

Natural Gas 0 0 0 1 0 1 0 0 0 1 1 1 0 0 0 0 0 0 0 0 1 1 0 0 0 0 0 0 0 0 # 0 0 0 0 0 0 0 0 0 0 # 0 0 0 0 0 0 0 0 0

Gold 0 0 # 0 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 1 1 1 0 0 0 0 1 0 1 # 0 1 1 1 0 1 0 0 0 0 0 0 0 0 # 0 0 0 0 0 #

Copper # 0 # 0 0 0 0 0 # 0 0 # 0 1 0 0 0 0 0 0 1 0 1 1 0 1 1 1 1 1 0 1 0 1 1 1 1 1 1 0 0 1 0 0 0 0 1 0 0 0 0 1

Silver 0 0 # 0 0 0 0 # 0 0 0 0 0 1 0 0 0 0 0 1 1 1 0 0 0 0 1 1 1 0 0 0 0 1 0 1 0 0 0 0 0 0 0 0 # 0 0 0 0 0 0 0

Soy # 0 # 0 # 0 # 0 0 0 0 0 0 0 0 0 0 0 0 0 1 0 1 1 0 1 0 0 0 0 0 0 0 0 1 0 0 0 0 0 # 0 0 # 0 0 0 0 0 0 0

Corn # 0 # # 0 0 0 # 0 0 0 0 0 0 0 0 0 # 0 0 1 0 0 1 1 0 0 1 0 0 # 0 0 0 0 0 0 0 0 0 # 0 # 0 0 0 0 0 0 0 #

Wheat 0 0 # 0 0 0 0 # 0 0 0 0 # 0 0 0 1 # # 0 0 0 0 0 1 1 0 1 0 0 0 0 0 0 0 0 0 0 0 # # # # # 0 0 0 0 0 0 #

20162003 2008 201520142007200620052004 2009 2010 2011 2012 2013

Page 22

Correlations (+ or -) between daily returns on crude oil futures

and financial investments have also strengthened

22

Note: Correlations computed quarterly

< -0.65 -0.65 to -0.4 -0.4 to -0.25 -0.25 to 0.25 0.25 to 0.4 0.4 to 0.65 > 0.65

Negative correlation Positive correlation

April 12, 2016

Date

S & P 500 # # # # 0 0 # # # 0 # 0 0 0 # 0 0 0 0 # 0 # 0 0 0 1 1 0 1 1 1 1 # 1 1 1 0 1 1 0 0 1 0 0 0 0 0 0 0 0 0 0 1

U.S. Dollar # # # # # # # # # # # # # # # 0 # # 0 # # # # # # # # # # # # # # # # # # # # # # # 0 # # # # # 0 0

U.S. Bonds 0 0 0 0 # 0 0 0 # 0 0 # 0 0 # # # 0 # 0 # 0 # # # # # # # # # # # # # # # # # # # # # 0 # # 0 # # #

WTI Implied Volatility 0 # # 0 # 0 0 # 0 0 0 # 0 # 0 # # # # 0 0 0 # # # # # # # # # # 0 # # # # # # # # # 0 # # 0 # # # #

Inflation Expectations 0 0 0 # 0 0 0 0 0 0 0 0 1 1 0 0 0 0 0 0 1 0 1 # 0 0 0 0 0 1 0 0 0 1 1 0 0 1 0 0 # 1 0 0 0 0 0 0 0 1 1 0 1

201620152003 2008 20142007200620052004 2009 2010 2011 2012 2013

Page 23

For more information

23

U.S. Energy Information Administration home page | www.eia.gov

Short-Term Energy Outlook | www.eia.gov/steo

Annual Energy Outlook | www.eia.gov/aeo

International Energy Outlook | www.eia.gov/ieo

Monthly Energy Review | www.eia.gov/mer

EIA Information Center

(202) 586-8800 | email: [email protected]

April 12, 2016