12

WHAT SPONSORS WANT FROM PARTNERS THE MOST IMPORTANT BENEFITS, SERVICES AND OBJECTIVES

www.sponsorship.com 1

WHAT SPONSORS WANT FROM PARTNERS THE MOST IMPORTANT BENEFITS, SERVICES AND OBJECTIVES

www.sponsorship.com 2

FINDINGS FROM THE 14TH ANNUAL

PERFORMANCE RESEARCH/SPONSORSHIP

DECISION-MAKERS SURVEY REFLECT A FAIRLY

CONSISTENT APPROACH OVER THE YEARS

TO WHAT CORPORATE MARKETERS HOPE TO

ACHIEVE FROM THEIR RELATIONSHIPS WITH

RIGHTSHOLDERS.

The 2014 results reveal an interest in more tangible benefits beyond those that offer visibility, an increasing reliance on marketing agencies to help execute sponsorships, and improvement into measuring the impact of partnership programs.

www.sponsorship.com 3

SURVEY FINDS SPONSORS LOOKING FOR SLIGHTLY DIFFERENT BENEFITS AND SERVICES FROM PROPERTIES

ACCORDING TO THE SURVEY, BRAND MARKETERS SAY THEY ARE NO LONGER AS INTERESTED IN RECEIVING IDENTIFICATION ON SPONSORED PROPERTIES’ MEDIA BUYS AND COLLATERAL MATERIALS, WITH BOTH OF THOSE BENEFITS NO LONGER AMONG THE TEN MOST VALUABLE.

Reflecting a desire for benefits that deliver more than just visibility, sponsors are instead prioritizing connections to personalities and talent associated with properties, as well as access to sponsored organizations’ databases and mailing lists. The latter returned to the top ten, while the former cracked the list for the first time in the survey’s history.

HOW VALUABLE ARE THE FOLLOWING BENEFITS TO YOU?

Percent of respondents who ranked the factor a 9 or a 10 on a 10-point scale, where 10 is extremely valuableSource: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

How Valuable Are The Following Benefits To You?

43% ON-SITE SIGNAGE

42%

41%

31%

BROADCAST AD OPPORTUNITIES

RIGHT TO PROPERTY MARKS AND LOGO

TITLE OF A PROPRIETARY AREA

58% CATEGORY EXCLUSIVITY

30% ACCESS TO PROPERTY CONTENT

28%

27%

SPOKESPERSON/ACCESS TO PERSONALITIES

TICKETS AND HOSPITALITY

ACCESS TO PROPERTY MAILING LIST/DATABASE 25%

RIGHT TO PROMOTE CO-BRANDED PRODUCTS/SERVICES

23%

Percent of respondents who ranked the factor a 9 or a 10 on a 10-point scale, where 10 is extremely valuable

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

www.sponsorship.com 4

Sponsors are also making it clear that help with determining the impact of their partnerships is a top priority. Assistance in measuring ROI and/or ROO topped the list of valuable services provided by properties in this year’s survey. In 2013, sponsors said it was the fourth most valuable service.

Also increasing in importance: rightsholder-provided research on whether audiences recognize and recall sponsors.

Conversely, sponsorship fulfillment reports fell to only the fourth most valuable service. Since best practices for producing such reports include reporting the type of metrics and research that sponsors say is critical, the conclusion here is that the majority of properties must not be following such practices, instead producing reports that sponsors don’t find useful.

Despite the fact that measurement help is now the top service sponsors want from rightsholders, their partners are not very good at delivering it, according to respondents. Nearly three-quarters of sponsors said properties did not meet their expectations in helping measure ROI or ROO.

How Valuable Are The Following Property-Provided Services?

42% AUDIENCE RESEARCH ON PROPENSITY TO PURCHASE

34%

32%

32%

25%

AUDIENCE RESEARCH ON RECOGNITION/RECALL

POST-EVENT REPORT/FULFILLMENT AUDIT

AUDIENCE RESEARCH ON ATTITUDE/IMAGE

LEVERAGING IDEAS

42% ASSISTANCE MEASURING ROI/ROO

21% AUDIENCE CONTACT INFORMATION

18%

13%

AUDIENCE RESEARCH ON BUYING HABITS

THIRD-PARTY VALUATION STATEMENT

12% TRACKING OF PROMOTIONAL OFFERS

Percent of respondents who ranked the factor a 9 or a 10 on a 10-point scale, where 10 is extremely valuable

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

HOW VALUABLE ARE THE FOLLOWING PROPERTY-PROVIDED SERVICES?

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

NO

27%

73%

YES

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

Do properties meet your expectations in helping you measure your return on investment/objectives?

DO PROPERTIES MEET YOUR EXPECTATIONS IN HELPING YOU MEASURE YOUR RETURN ON INVESTMENT/OBJECTIVES?

Percent of respondents who ranked the factor a 9 or a 10 on a 10-point scale, where 10 is extremely valuableSource: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

www.sponsorship.com 5

Sponsors remain reliant on agency support, with the number of sponsors who manage execution and activation completely in-house setting a new low in the survey’s history, dropping to 22 percent, one point below last year’s level.

However, the 2014 survey saw a notable change in which agency type is providing those services. In 2013, 63 percent of sponsors said they used advertising or media buying agencies, while 60 percent used marketing/promotion/PR agencies for sponsorship support—with many clearly using both.

In 2014, 75 percent of sponsors say they rely on marketing/promotion and PR agencies, while only 52 percent report using ad or media agencies.

In addition, the survey for the first time asked sponsors who used multiple types of agencies to note the type that they relied on most. More than half, 55 percent, selected marketing/promotion/PR agencies versus just 14 percent who said ad or media agencies.

Which Types Of Agencies Do You Use To Support Your Sponsorships?

MARKETING, PROMOTIONS, PR

ADVERTISING

NONE, MANAGE ENTIRELY IN-HOUSE

SPONSORSHIP SPECIALIST REPRESENTING PROPERTY

INDEPENDENT SPONSORSHIP SPECIALIST

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

52%

75%

22%

10%

22%

WHICH TYPES OF AGENCIES DO YOU USE TO SUPPORT YOUR SPONSORSHIPS?

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

www.sponsorship.com 6

WHAT PORTION OF YOUR MARKETING BUDGET IS SPENT ON SPONSORSHIP RIGHTS FEES?

For the first time in the survey’s history, social media claimed the number one spot among marketing communications channels used to activate sponsorship, with nine out of 10 sponsors including it in their leveraging mix. Social media took the top spot from public relations, which saw significantly less sponsors—77 percent in 2014 versus 89 percent in 2013—using it.

On-site interaction moved up to the number three spot from number eight, with 76 percent of sponsors activating at events and venues this year compared to 51 percent last year. On the flip side, internal communications were less popular in 2014, with only 65 percent of sponsors reporting the practice as a leveraging tool compared to 86 percent in 2013 when it was number three.

Survey respondents allocated an average of 23 percent of their overall marketing/advertising/promotion budgets to sponsorship, the second highest average in the survey’s 14 years. Over the past 10 years, sponsorship’s share has bounced between a low of 16 percent in 2004 to a high of 25 percent in 2010.

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

Percent of respondents who ranked the factor a 9 or a 10 on a 10-point scale, where 10 is extremely valuableSource: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

What Channels Do You Use To Leverage Your Sponsorships?

90% SOCIAL MEDIA

77%

65%

41%

76%

40%

67%

66%

PUBLIC RELATIONS

INTERNAL COMMUNICATIONS

DIRECT MARKETING

ON-SITE INTERACTION

BUSINESS TO BUSINESS

HOSPITALITY

DIGITAL/MOBILE PROMOTIONS

71% TRADITIONAL ADVERTISING

28% SALES PROMOTION OFFERS

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

23% SPONSORSHIP

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

What Portion Of Your Marketing Budget Is Spent On Sponsorship Rights Fees?

WHAT CHANNELS DO YOU USE TO LEVERAGE YOUR SPONSORSHIPS?

www.sponsorship.com 7

How Will Your 2014 Sponsorship Spending Compare To 2013?

52% 21%

27%

DECREASE

STAY THE SAME

INCREASE

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

What Is Your Company’s Typical Promotional Spending Ratio?

AVERAGE IS 1.7 TO 1

18%

45%

12% 10%

15% 2 TO 1

4 TO 1OR MORE

1 TO 1

3 TO 1

0 TO 1

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

Another survey data point that has fluctuated over the years is the ratio of activation spending to spending on rights fees. For 2014, sponsors report spending an average of $1.70 on leveraging for every $1 spent on rights fees, up from $1.50 in 2013.

Only 27 percent of sponsors say their spending will increase this year over last, with 21 percent cutting spending and 52 percent keeping their budgets at 2013 levels.

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

WHAT IS YOUR COMPANY’S TYPICAL PROMOTIONAL SPENDING RATIO?

HOW WILL YOUR 2014 SPONSORSHIP SPENDING COMPARE TO 2013?

www.sponsorship.com 8

Is Your Company Considering New Sponsorships In 2014?

YES

NO

66%

34%

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

How Will Your 2014 Leveraging And Activation Spending Compare To 2013?

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

STAYTHE SAME

DECREASE

INCREASE

51%

14%

35%

IS YOUR COMPANY CONSIDERING NEW SPONSORSHIPS IN 2014?

HOW WILL YOUR 2014 LEVERAGING AND ACTIVATION SPENDING COMPARE TO 2013?

The outlook is slightly more positive for activation spending, with more than a third of sponsors— 35 percent—upping the amount they will direct toward activation, while 14 percent are lowering their activation budgets and 51 percent are keeping spending on par with 2013.

The majority of sponsors are in the market for new partnerships, but fewer sponsors are considering first-time deals this year than last. Only 66 percent say they are considering new relationships versus 75 percent in 2013.

Sponsors are seemingly much more dissatisfied with at least one of their partners this year. A majority of survey respondents—57 percent—are looking to drop out of a current sponsorship, compared to only 41 percent of sponsors in 2013.

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

www.sponsorship.com 9

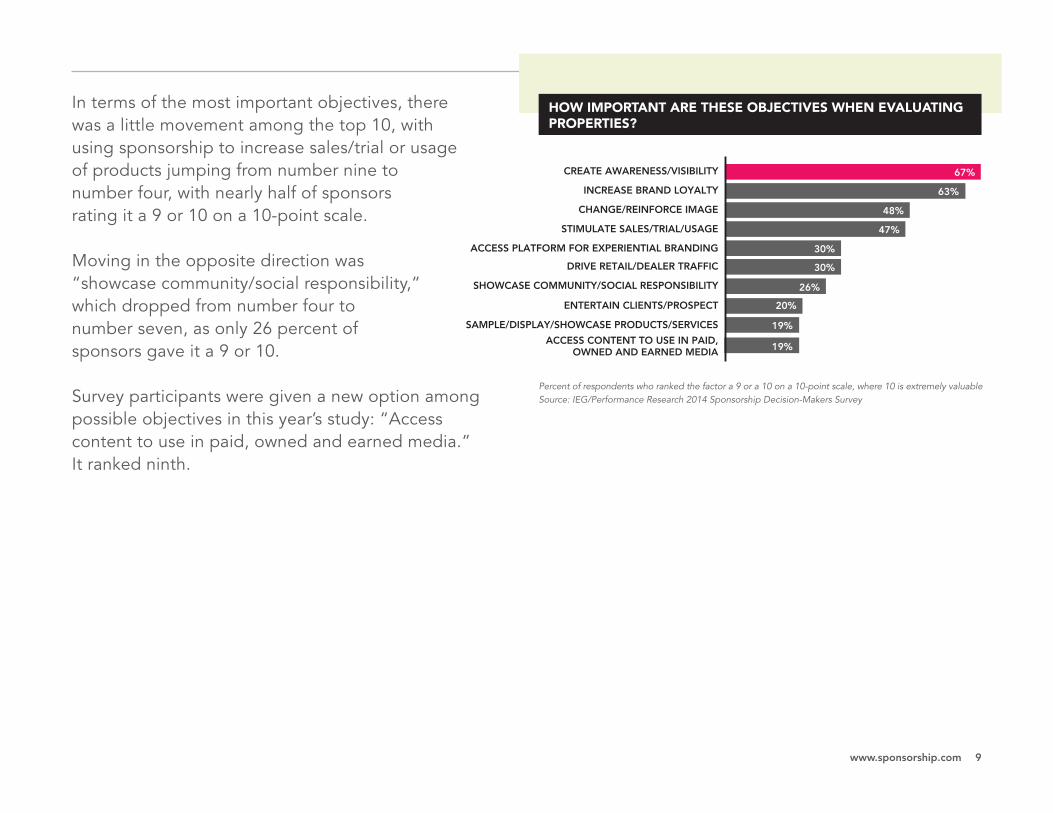

In terms of the most important objectives, there was a little movement among the top 10, with using sponsorship to increase sales/trial or usage of products jumping from number nine to number four, with nearly half of sponsors rating it a 9 or 10 on a 10-point scale.

Moving in the opposite direction was “showcase community/social responsibility,” which dropped from number four to number seven, as only 26 percent of sponsors gave it a 9 or 10.

Survey participants were given a new option among possible objectives in this year’s study: “Access content to use in paid, owned and earned media.” It ranked ninth.

Percent of respondents who ranked the factor a 9 or a 10 on a 10-point scale, where 10 is extremely valuableSource: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

HOW IMPORTANT ARE THESE OBJECTIVES WHEN EVALUATING PROPERTIES?

How Important Are These Objectives When Evaluating Properties?

63% INCREASE BRAND LOYALTY

48%

30%

47%

CHANGE/REINFORCE IMAGE

ACCESS PLATFORM FOR EXPERIENTIAL BRANDING

STIMULATE SALES/TRIAL/USAGE

67% CREATE AWARENESS/VISIBILITY

30% DRIVE RETAIL/DEALER TRAFFIC

26% SHOWCASE COMMUNITY/SOCIAL RESPONSIBILITY

20%

19%

ENTERTAIN CLIENTS/PROSPECT

SAMPLE/DISPLAY/SHOWCASE PRODUCTS/SERVICES

19% ACCESS CONTENT TO USE IN PAID,

OWNED AND EARNED MEDIA

Percent of respondents who ranked the factor a 9 or a 10 on a 10-point scale, where 10 is extremely valuable

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

www.sponsorship.com 10

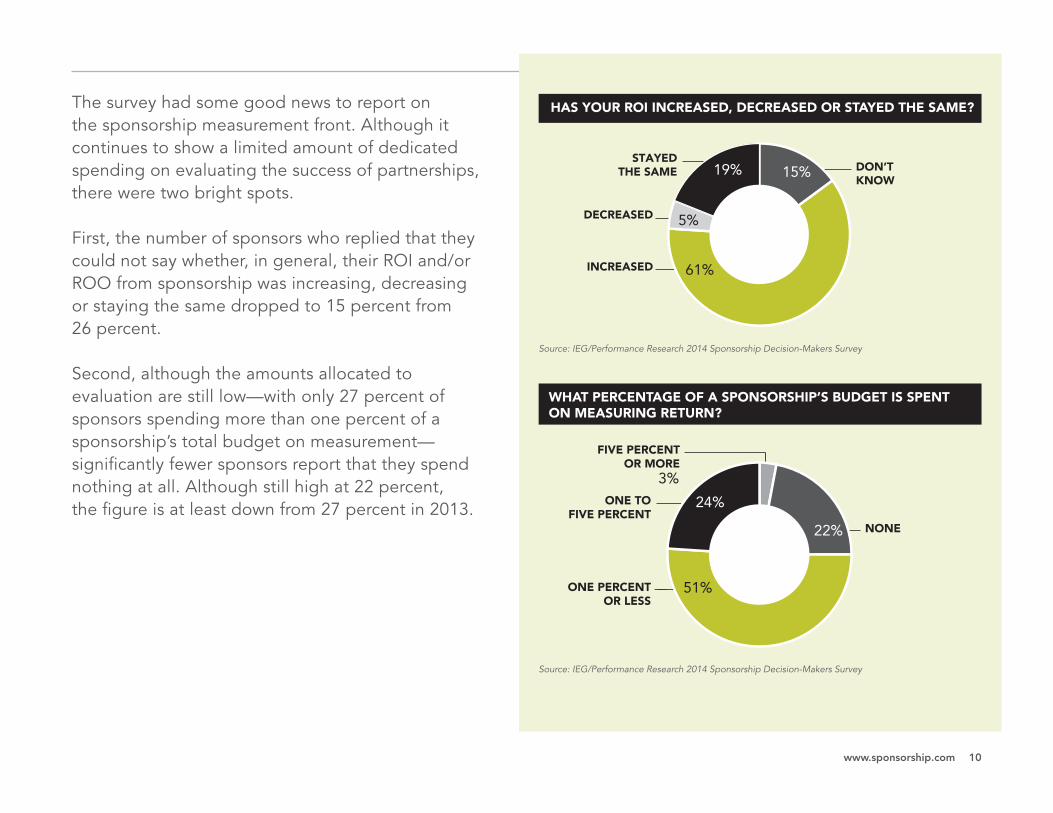

What Percentage Of A Sponsorship’s Budget Is Spent On Measuring Return?

6

22%

51%

24%

3% ONE TO

FIVE PERCENT

ONE PERCENTOR LESS

FIVE PERCENTOR MORE

NONE

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

Has Your ROI Increased, Decreased Or Stayed The Same?

DON’TKNOW

DECREASED

STAYEDTHE SAME

INCREASED

19% 15%

5%

61%

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

The survey had some good news to report on the sponsorship measurement front. Although it continues to show a limited amount of dedicated spending on evaluating the success of partnerships, there were two bright spots.

First, the number of sponsors who replied that they could not say whether, in general, their ROI and/or ROO from sponsorship was increasing, decreasing or staying the same dropped to 15 percent from 26 percent.

Second, although the amounts allocated to evaluation are still low—with only 27 percent of sponsors spending more than one percent of a sponsorship’s total budget on measurement—significantly fewer sponsors report that they spend nothing at all. Although still high at 22 percent, the figure is at least down from 27 percent in 2013.

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

HAS YOUR ROI INCREASED, DECREASED OR STAYED THE SAME?

WHAT PERCENTAGE OF A SPONSORSHIP’S BUDGET IS SPENT ON MEASURING RETURN?

www.sponsorship.com 11

When Does Your Company Determine Its Sponsorship Budget?

45% 22%

5%

28%

FIRST QUARTER (JAN. – MARCH)

FOURTH QUARTER (OCT. – DEC.)

SECOND QUARTER (APRIL – JUNE)

THIRD QUARTER (JULY – SEPT.)

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

How Valuable Are These Metrics In Evaluating Sponsorships?

Percent of respondents who ranked the factor a 9 or a 10 on a 10-point scale, where 10 is extremely valuable

91% AWARENESS OF PRODUCTS/SERVICES/BRAND

88%

69%

64%

83%

54%

73%

71%

ATTITUDES TOWARD BRAND

RESPONSE TO CUSTOMER/PROSPECT ENTERTAINMENT

RESPONSE TO SPONSORSHIP-RELATED PROMOTIONS/ADS

AWARENESS OF COMPANY’S/BRAND’S SPONSORSHIP

LEAD GENERATION

AMOUNT OF MEDIA EXPOSURE GENERATED

AMOUNT OF POSITIVE SOCIAL MEDIA ACTIVITY

53%

73%

EMPLOYEE/INTERNAL RESPONSE

PRODUCT/SERVICE SALES

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

Regarding which metrics were most important to sponsors, there was little change among the top ten. Awareness of products/services/brands and attitudes toward the brand each moved up one spot to number one and number two, respectively—replacing the former number one: awareness of the company or brand’s sponsorship.

The survey included a new option for respondents among metrics: “Amount of positive social media activity.” It joined the top ten at number six.

The survey was conducted online in March 2014 and received 115 reponses.

Source: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

Percent of respondents who ranked the factor a 9 or a 10 on a 10-point scale, where 10 is extremely valuableSource: IEG/Performance Research 2014 Sponsorship Decision-Makers Survey

HOW VALUABLE ARE THESE METRICS IN EVALUATING SPONSORSHIPS?

WHEN DOES YOUR COMPANY DETERMINE ITS SPONSORSHIP BUDGET?

www.sponsorship.com 12

ABOUT IEG AND ESP PROPERTIES

© 2014 IEG, LLC. All Rights Reserved. www.sponsorship.com 12

DAN KOWITZ

Senior Vice President, Business Development, ESP Properties

IEG has shaped and defined sponsorship over three decades. It is the globally recognized source for industry insights, trends, training and events via sponsorship.com, its annual conference, online publications, trend reports, surveys and webinars.

IEG is part of ESP Properties, a WPP company. As a commercial and creative advisor for rightsholders, ESP Properties helps organizations unlock greater value from their audiences and brand partnerships.

Our consulting team assesses and advises how to grow the value of rightsholders’ commercial programs. We do this through a full range of services across data, digital and content development to better understand audiences and create more relevant ways to engage with them. This provides brand partners with new ways to connect with communities of fans and followers, growing the potential value of commercial partnerships.

Our sales team provides partnership strategy and sales representation to the world’s most active sponsors, within and beyond the WPP network of brand clients. Through WPP we have extensive contacts and deep insights into what it takes to create successful partnerships.

For more information about the value of sponsorships and partnerships, IEG and ESP Properties, please visit www.sponsorship.com, www.espglobal.com, or call Dan Kowitz at 312/725-5114.