56

What Your Financials Say Depends on Who’s Reading Them! Presented by CohnReznick’s Government Contracting Industry Practice Christine Williamson, Partner & David Gaver, Director

| Date post: | 12-May-2018 |

| Category: |

Documents |

| Upload: | nguyenliem |

| View: | 215 times |

| Download: | 1 times |

W h a t Y o u r F i n a n c i a l s S a y D e p e n d s o n W h o ’ s R e a d i n g T h e m !

Presented by CohnReznick’s Government Contracting Industry Practice

Christine Williamson, Partner & David Gaver, Director

P L E A S E R E A D

This presentation has been prepared for information purposes and general guidance only and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice.

No representation or warranty (express or implied) is made as to the accuracy or completeness of the information contained in this publication, and CohnReznick LLP, its members, employees and agents accept no liability, and disclaim all responsibility, for the consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

This presentation and its content are the property of CohnReznick LLP and are protected by applicable copyright laws. Any unauthorized use of the information herein will be considered a violation of CohnReznick LLP’s intellectual property rights. Unless stated otherwise herein, no part of this presentation may be copied, distributed, or published, in whole or in part, without the prior written agreement of CohnReznick LLP.

1

A G E N D A

2

Users of Financials

Types - Financials, Standards, Opinions

What do Financials include

Disclosures – Norm vs unusual

Specific Users look at………

Common Ratios/Covenants

D E F I N I T I O N S

3

CEO - chief embezzlement officer

CFO - corporate fraud officer

NAV - normal Andersen valuation

P/E - parole entitlement

EPS - eventual prison sentence

BULL MARKET-A random market movement causing an investor to

mistake him/her self for a financial genius

U S E R S O F F I N A N C I A L S

4

Audience – who are the users of your

financial statements?

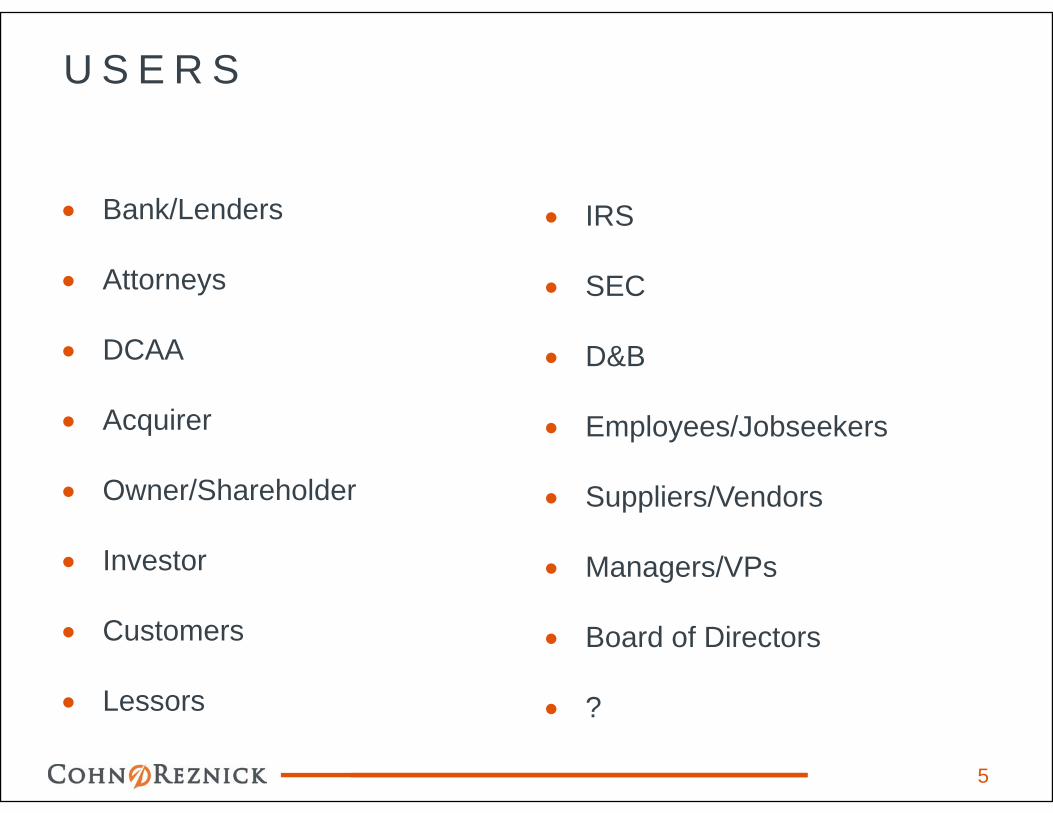

U S E R S

5

IRS

SEC

D&B

Employees/Jobseekers

Suppliers/Vendors

Managers/VPs

Board of Directors

?

Bank/Lenders

Attorneys

DCAA

Acquirer

Owner/Shareholder

Investor

Customers

Lessors

T Y P E S O F F I N A N C I A L S

6

Audience – what types of

financial statements are there?

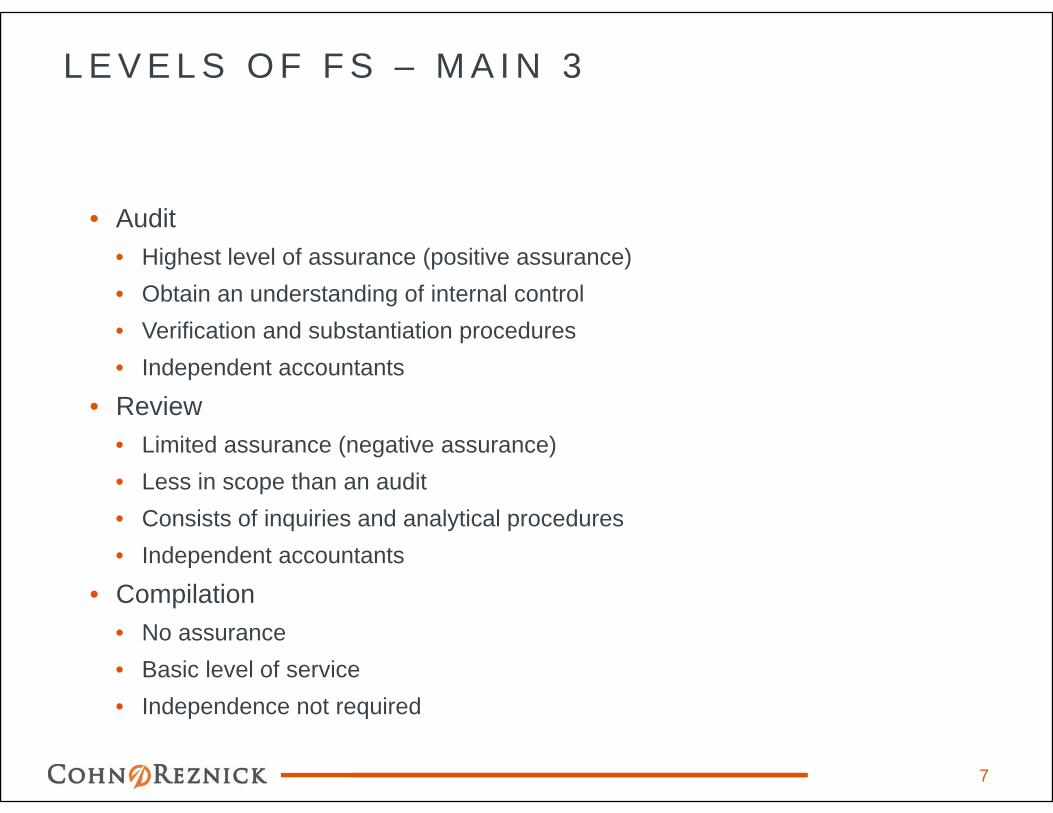

L E V E L S O F F S – M A I N 3

• Audit• Highest level of assurance (positive assurance)• Obtain an understanding of internal control• Verification and substantiation procedures• Independent accountants

• Review• Limited assurance (negative assurance)• Less in scope than an audit• Consists of inquiries and analytical procedures• Independent accountants

• Compilation• No assurance• Basic level of service• Independence not required

7

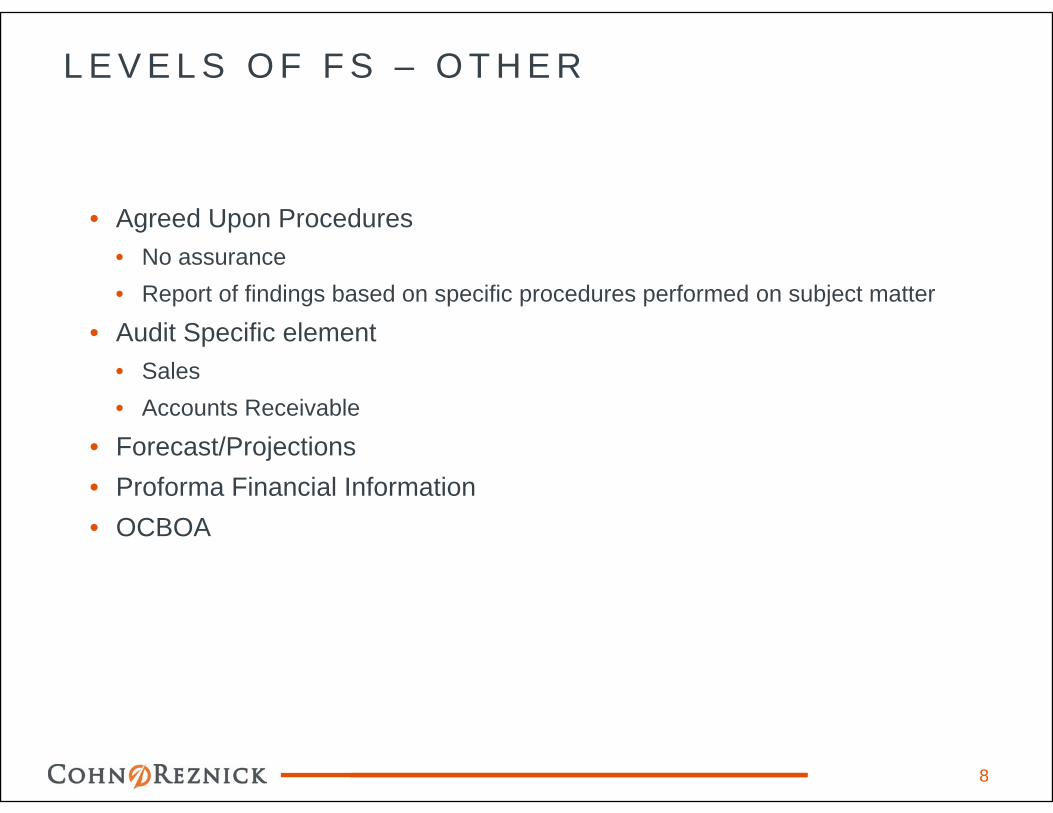

L E V E L S O F F S – O T H E R

• Agreed Upon Procedures• No assurance• Report of findings based on specific procedures performed on subject matter

• Audit Specific element• Sales• Accounts Receivable

• Forecast/Projections• Proforma Financial Information• OCBOA

8

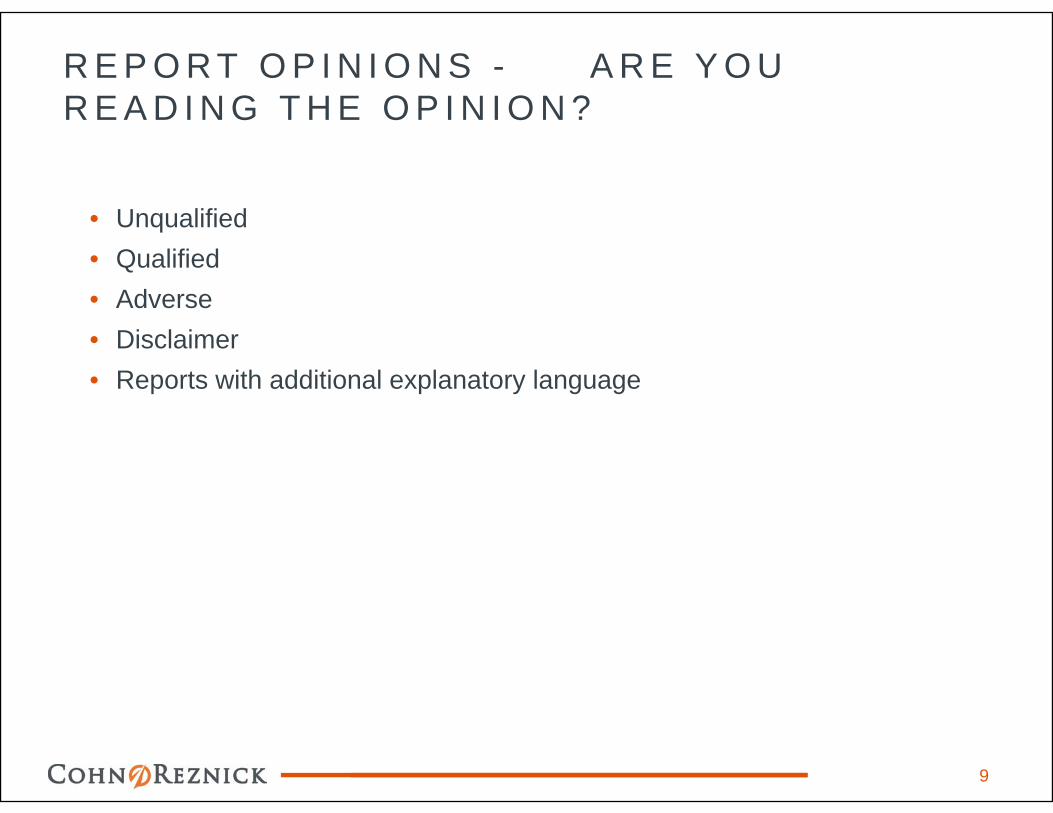

R E P O R T O P I N I O N S - A R E Y O U R E A D I N G T H E O P I N I O N ?

• Unqualified• Qualified• Adverse• Disclaimer• Reports with additional explanatory language

9

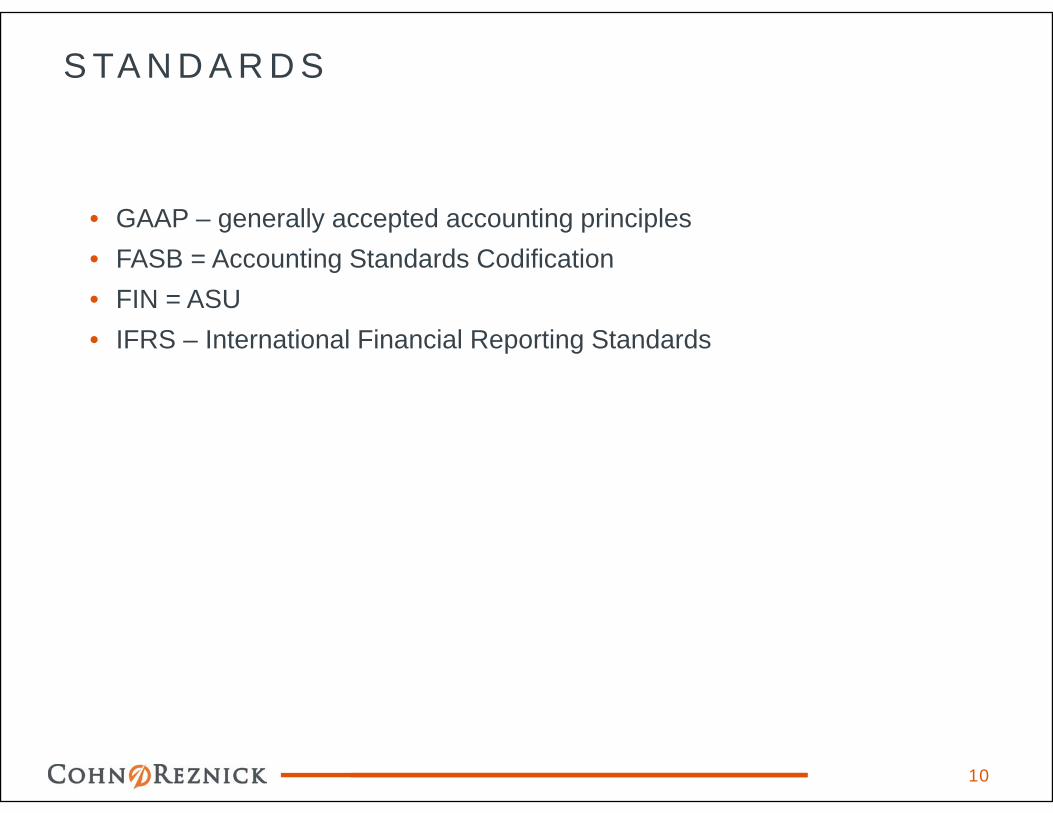

S TA N D A R D S

• GAAP – generally accepted accounting principles• FASB = Accounting Standards Codification• FIN = ASU• IFRS – International Financial Reporting Standards

10

11

F I N A N C I A L S TAT E M E N T S I N C L U D E :

• Balance Sheet• Income Statement• Statement of Cash Flows• Statement of Stockholders’ Equity• Disclosures or Footnotes• Supplementary Data (can be unaudited)

• With Supplementary?

12

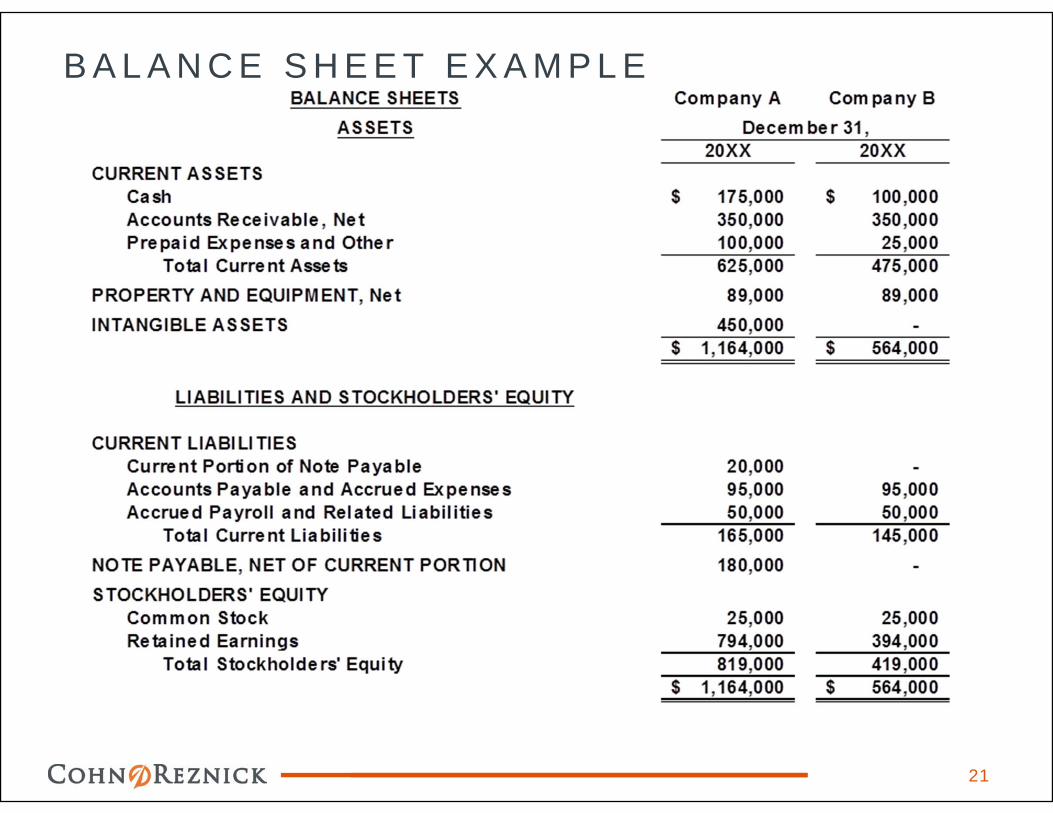

B A L A N C E S H E E T

• Assets = Liabilities + Stockholders’ Equity• Represents a “snapshot” at a point in time of the assets and liabilities of a

business• Assets are listed based on how quickly they can be converted to cash• Liabilities are listed based on their due dates• Reconciling bank accounts every month to the bank statement/knowing

how much cash each day - critical to a well run business

13

B A L A N C E S H E E T

• Government Contractors• Billed A/R• Unbilled A/R

• Timing• Rate Differentials• Retainage/Withholding

• Current Asset-Industry Practice

14

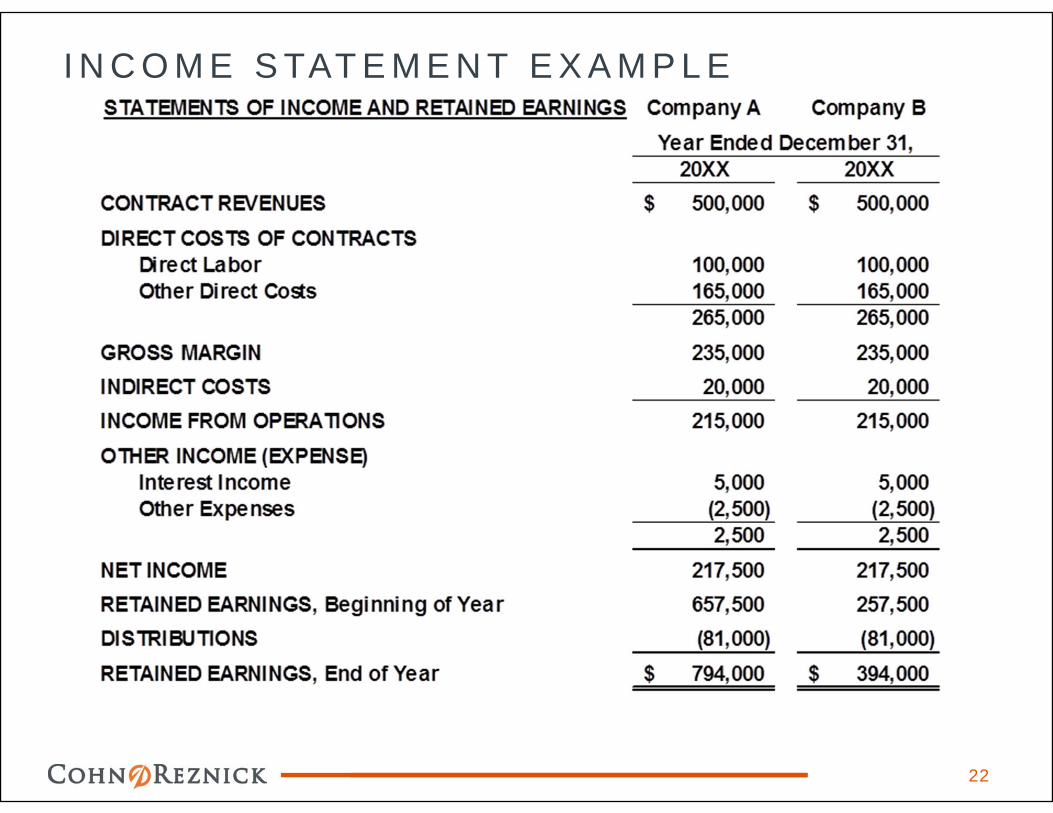

I N C O M E S TAT E M E N T

• “Report Card”

• Dual year presentation

• Summary or Detail

• Vertical IS analysis

15

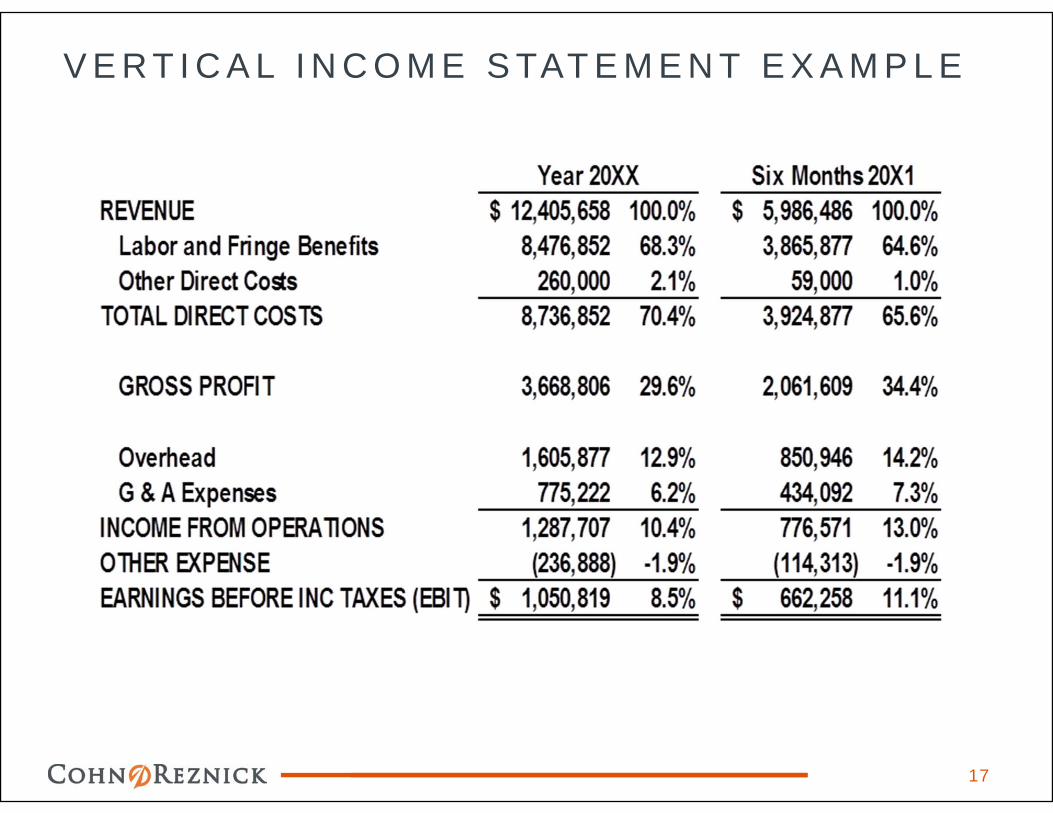

V E R T I C A L I N C O M E S TAT E M E N T A N A LY S I S ( O R T H E C O M M O N S I Z E P L )

• Quantify each line item as a % of revenue

• Compare %’s to prior years - great tool to notice fluctuations/changes

• Equal footing

• When percentages vary from prior experience or expectations, the reader

should be inquiring why

16

V E R T I C A L I N C O M E S TAT E M E N T E X A M P L E

17

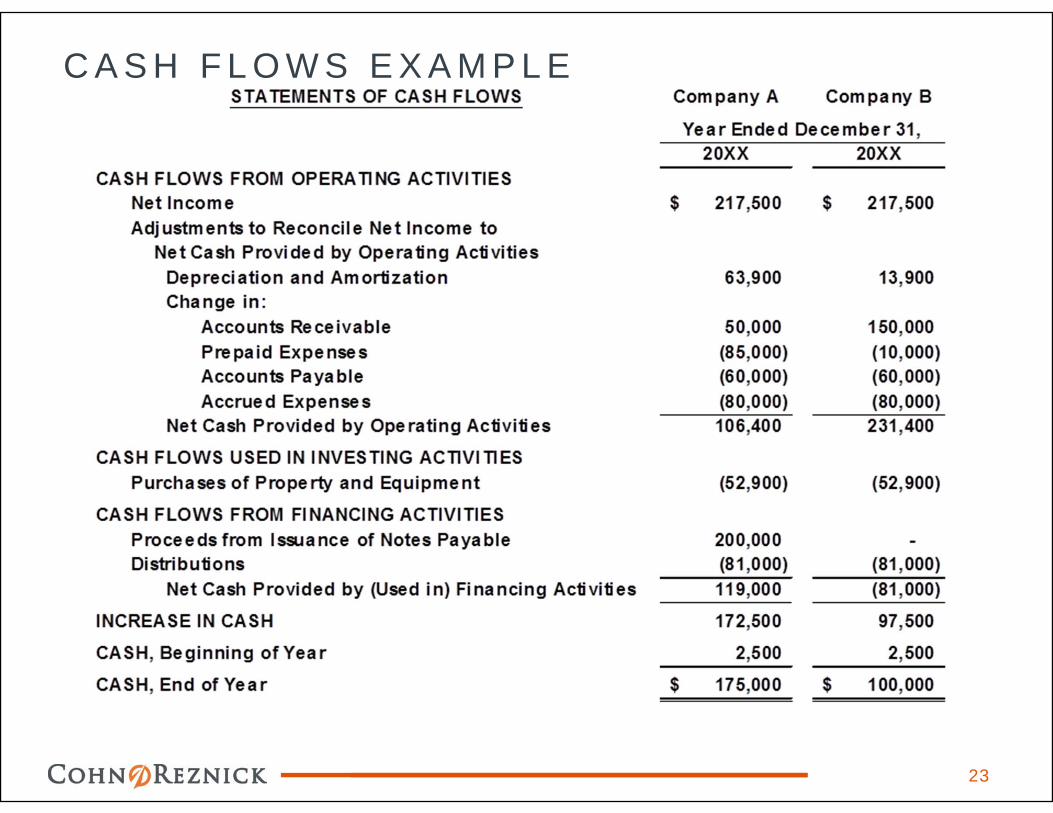

S TAT E M E N T O F C A S H F L O W S

• Shows how the profits or losses during the accounting period combine with

the all of the changes to the balance sheet produce a change in the entity’s

cash balance

• 5 Sections:

• Cash flows from operations

• Cash flows from investing activities

• Cash flows from financing activities

• Net change in cash

• Supplemental disclosure of noncash investing and financing activities

18

S TAT E M E N T O F S T O C K H O L D E R S ’ E Q U I T Y

• Sometimes not necessary

• Changes in retained earnings is combined with the income statement

• Reports:

• Additional Investments

• Stock Changes

• Dividends

• Certain Accounting Changes

19

D E F I N I T I O N S

• EBIT - earnings before irregularities and tampering

• EBITDA = Earnings before I tricked the dumb accountant

• BROKER-What my broker has made me

• STANDARD & POOR-Your life in a nutshell

• VALUE INVESTING-The art of buying low and selling lower

20

B A L A N C E S H E E T E X A M P L E

21

I N C O M E S TAT E M E N T E X A M P L E

22

C A S H F L O W S E X A M P L E

23

F I N A N C I A L S T A T E M E N T D I S C L O S U R E S

24

• At the end of the annual financial statements

• Critical information

• Many notes are required by GAAP

• Certain notes get very technical

D I S C L O S U R E S T O L O O K F O R :

25

• General – read what they do

• Summary of Acct Policies

• Related Party Transactions

• Contingencies & Commitments

• Debt

• Risk and Uncertainties

• Concentrations – Customers/Suppliers

• Subsequent Events

• Going Concern

G E N E R A L

26

• Outlines the nature of the business

• This brief description is important because it is difficult to

understand a company’s accounting practices and financial results

without understanding the nature of the company’s operations

S U M M A R Y O F S I G N I F I C A N T A C C O U N T I N G P O L I C I E S

27

• Usually the first note

• Indicates accounting policies being used

• Such as: revenue recognition, depreciation, securities, etc.

• Where there are matters that seem unusual, follow up questions

should be asked

R E L A T E D P A R T Y T R A N S A C T I O N S

28

Must be disclosed if:

• Exert significant influence over another entity

• Material transactions - the nature of the relationship is disclosed

along with the terms of the transaction

• “Arms-length” transactions

• Always scrutinize these transactions very carefully

C O N T I N G E N C I E S & C O M M I T M E N T S

29

• Caused by a past event and require a future event to happen

• Lawsuit

• Reporting depends on:

• the likelihood of the future event occurring

• can the future impact be reasonable estimated

• Elaborates on any commitments made by a company

• Leases

• If a company has committed to buy X amount of product Y from another

company in the upcoming year

D E B T

30

• Summarize the terms of the debt agreement with the lending

institution

• As well as the debt covenants the company must satisfy

R I S K A N D U N C E R T A I N T I E S

31

• Use of estimates

• Certain significant estimates

• If at least reasonably possible that the estimate will change in the near

term

• Effect material to the financial statements

C O N C E N T R A T I O N S

32

• Major Customers/Suppliers

• Discloses whether there are any customers or suppliers that constitute

an unusually large portion of the company’s business

• Company’s operations may be significantly affected if the

customer/supplier were loss

• Accounts Receivable/Sales

• Cash Concentration

S U B S E Q U E N T E V E N T S

33

• Discloses material developments that occur after the report date

• Should provide enough detail to allow the reader to form an opinion

on how the event may affect the company’s financial performance.

G O I N G C O N C E R N

34

• A required note if there is substantial doubt about the ability of a

company to continue operations for the upcoming year

• Provides insight into the financial condition of the company

U S E R S – B R O K E N I N T O G R O U P S

35

• Outsiders

• Insiders

• Regulatory

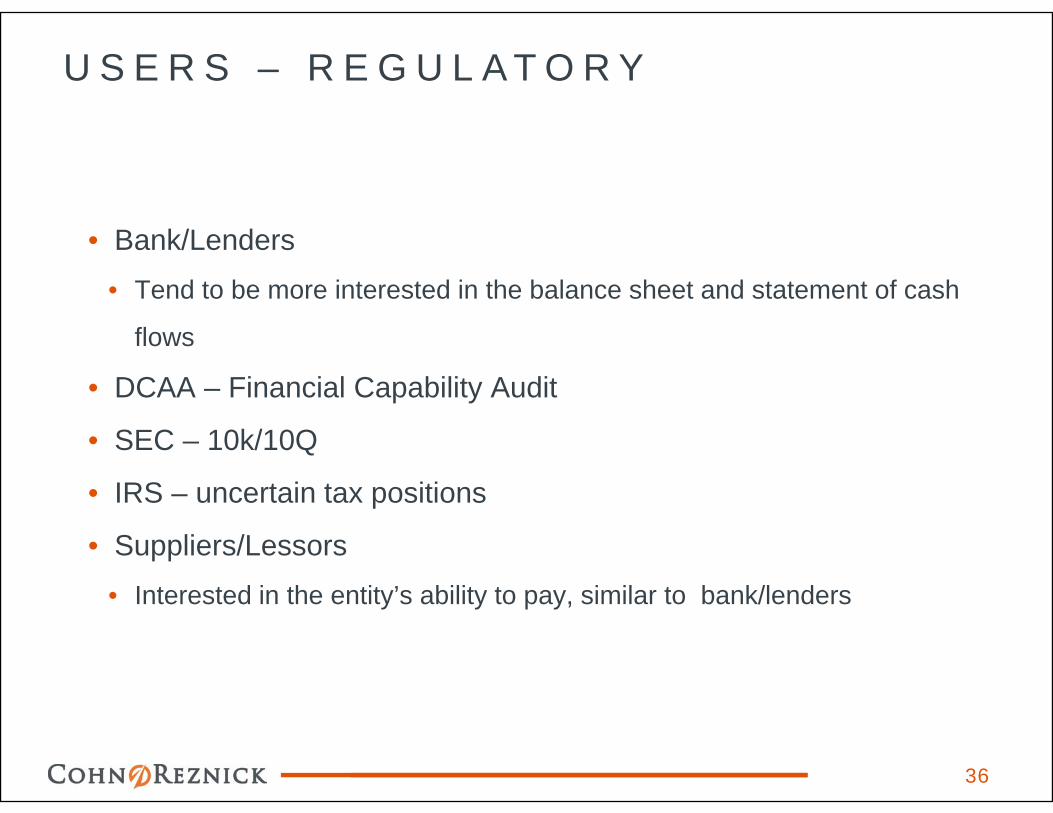

U S E R S – R E G U L A T O R Y

36

• Bank/Lenders

• Tend to be more interested in the balance sheet and statement of cash

flows

• DCAA – Financial Capability Audit

• SEC – 10k/10Q

• IRS – uncertain tax positions

• Suppliers/Lessors

• Interested in the entity’s ability to pay, similar to bank/lenders

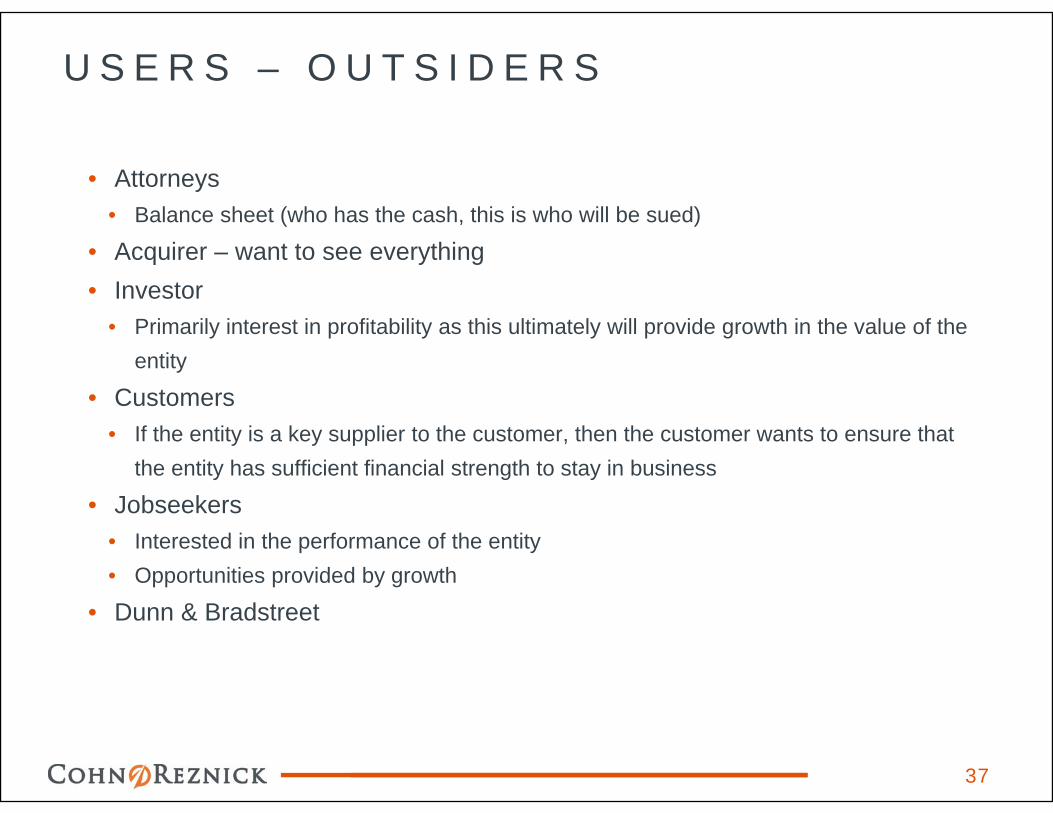

U S E R S – O U T S I D E R S

37

• Attorneys• Balance sheet (who has the cash, this is who will be sued)

• Acquirer – want to see everything• Investor

• Primarily interest in profitability as this ultimately will provide growth in the value of the entity

• Customers• If the entity is a key supplier to the customer, then the customer wants to ensure that

the entity has sufficient financial strength to stay in business

• Jobseekers• Interested in the performance of the entity• Opportunities provided by growth

• Dunn & Bradstreet

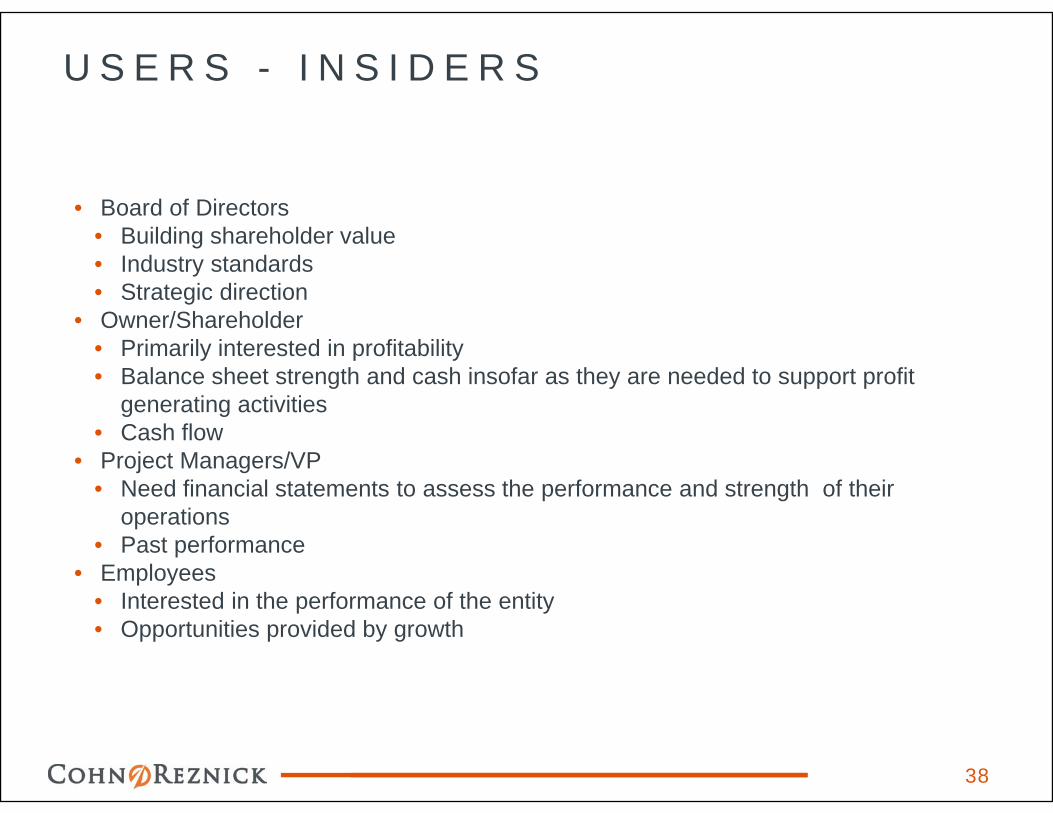

U S E R S - I N S I D E R S

38

• Board of Directors• Building shareholder value• Industry standards• Strategic direction

• Owner/Shareholder• Primarily interested in profitability• Balance sheet strength and cash insofar as they are needed to support profit

generating activities• Cash flow

• Project Managers/VP• Need financial statements to assess the performance and strength of their

operations• Past performance

• Employees• Interested in the performance of the entity• Opportunities provided by growth

D C A A - F I N A N C I A L C A P A B I L I T Y A U D I T

39

To determine if the contractor has adequate financial resources to perform on

Government contracts in the near term.

W H A T W I L L D C A A R E Q U I R E ?

40

• 3 years financials, YTD FS for last Qtr available, and tax returns

• Explanation Off-balance sheet arrangements & Related party transactions

• Cash Flow Forecast

• Operating Budget

D C A A W I L L R E V I E W F S I N D I C A T O R S :

41

• Profit/Loss

• Sales

• Working capital

• Net Worth

• Long-term Liabilities

• Accounts Payable Aging

• Loan Covenants

D C A A W I L L R E V I E W N O N - F S D A T A :

42

• Timely Payment of Payroll Taxes

• Management of Subsidiary using Parents Cash

• Alert to:

• Non-Payment of Insurance premiums

• Borrowing from under-funded pension plans

• Poorly maintained infrastructure

B A N K E R S – W H A T N O W !

43

• In addition to financial statements, banks may want to see the following:

• Accounts Receivable Aging

• Accounts Payable Aging

• Contract Backlog Reports/Pipeline/Waterfall

• Company Projections

• Interim Financial Statements

• Tax Returns

• Personal Financial Statements

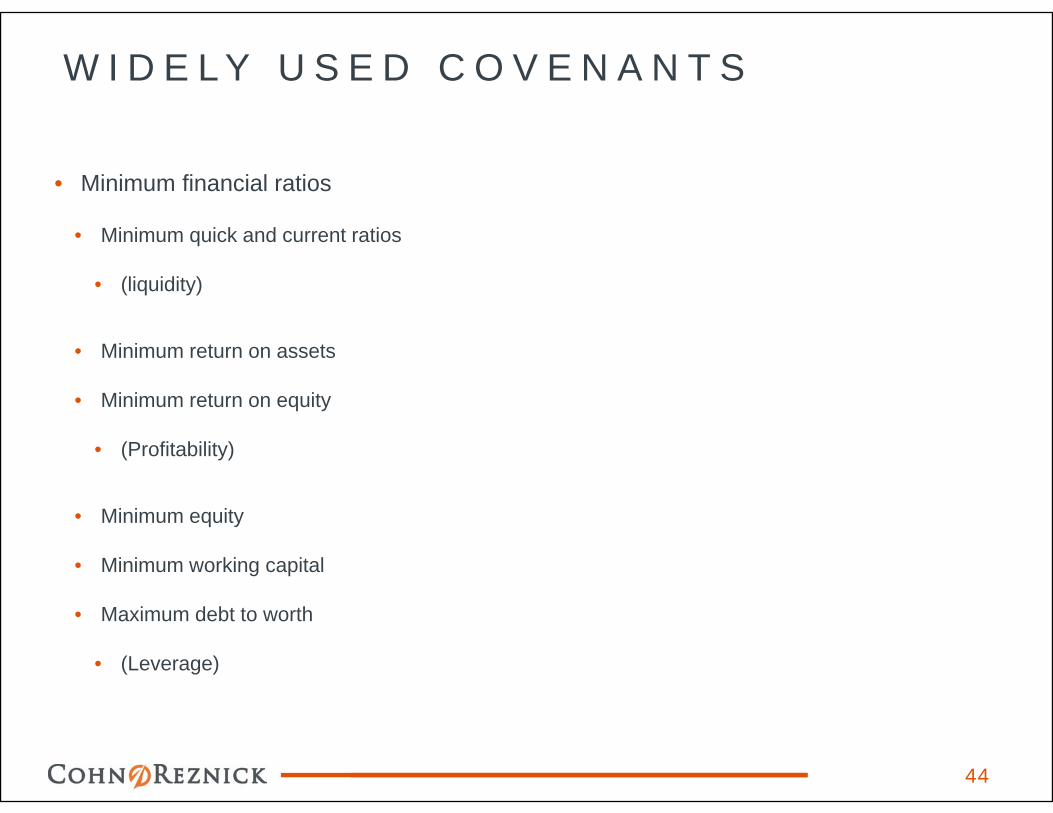

W I D E L Y U S E D C O V E N A N T S

44

• Minimum financial ratios

• Minimum quick and current ratios

• (liquidity)

• Minimum return on assets

• Minimum return on equity

• (Profitability)

• Minimum equity

• Minimum working capital

• Maximum debt to worth

• (Leverage)

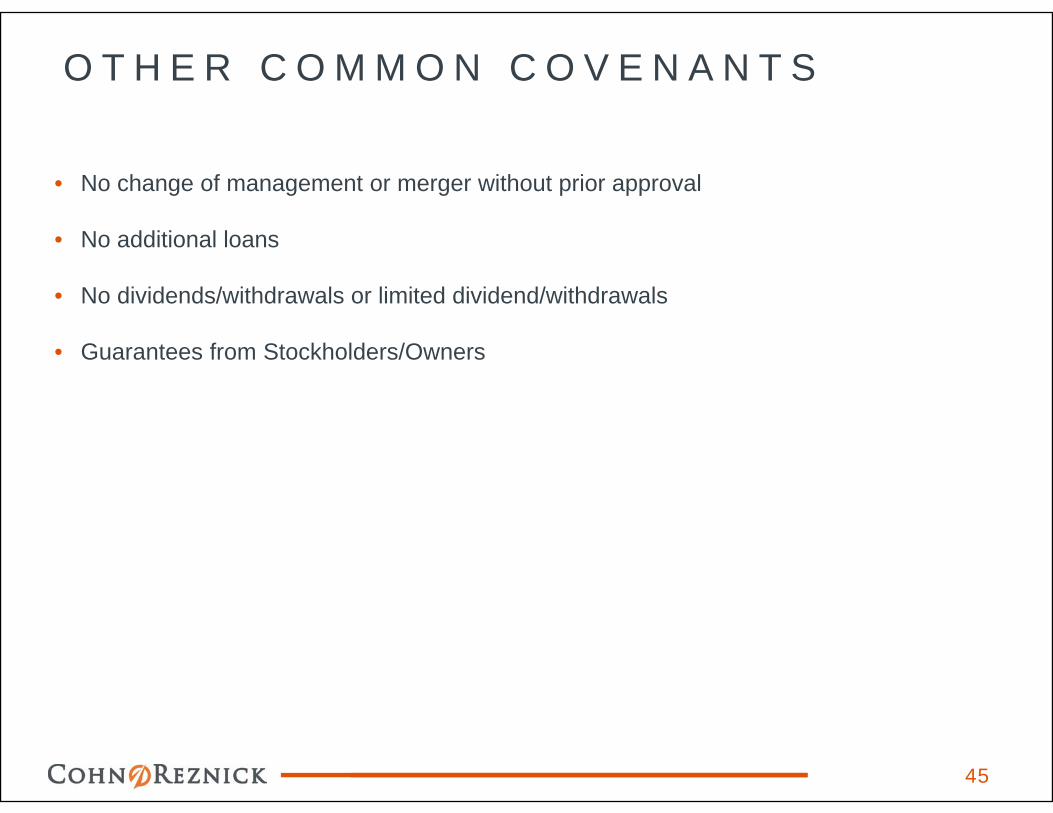

O T H E R C O M M O N C O V E N A N T S

45

• No change of management or merger without prior approval

• No additional loans

• No dividends/withdrawals or limited dividend/withdrawals

• Guarantees from Stockholders/Owners

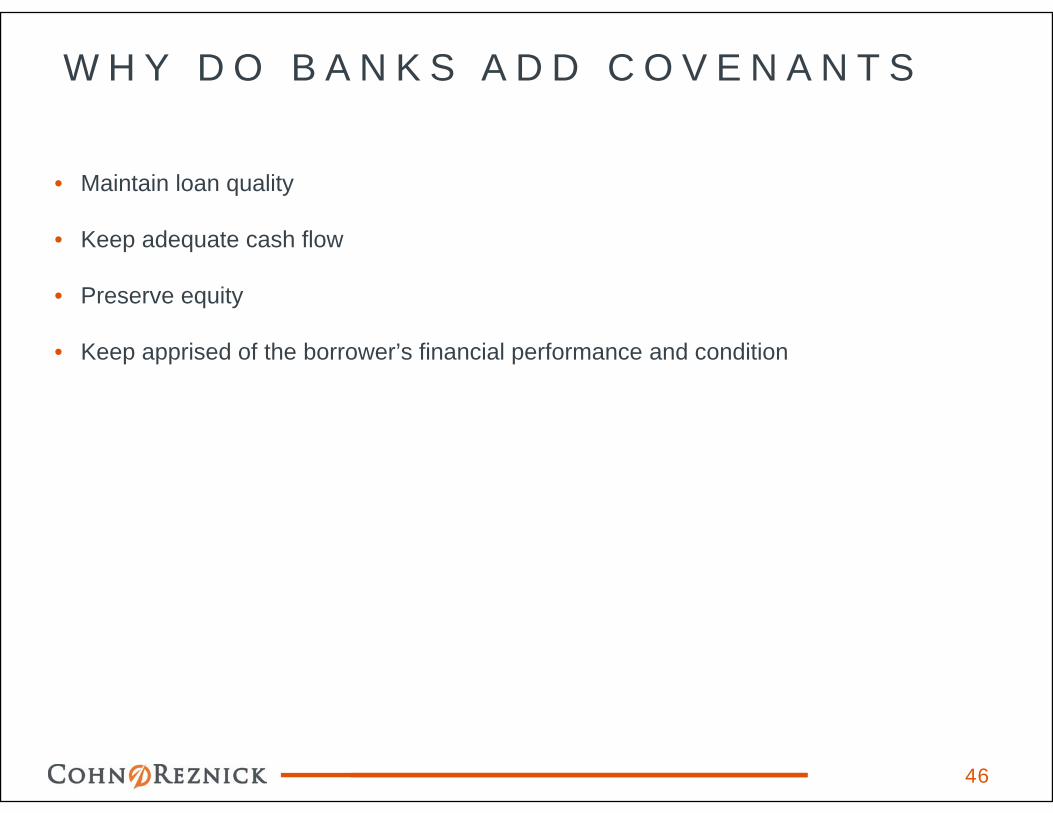

W H Y D O B A N K S A D D C O V E N A N T S

46

• Maintain loan quality

• Keep adequate cash flow

• Preserve equity

• Keep apprised of the borrower’s financial performance and condition

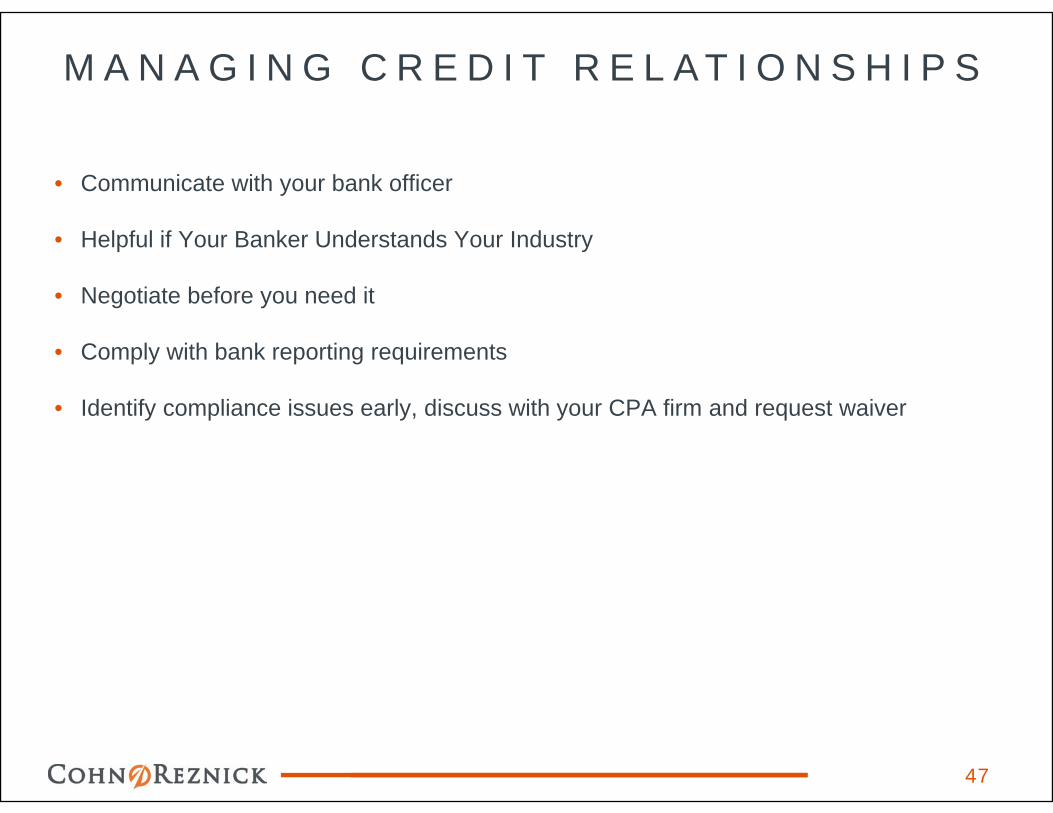

M A N A G I N G C R E D I T R E L A T I O N S H I P S

47

• Communicate with your bank officer

• Helpful if Your Banker Understands Your Industry

• Negotiate before you need it

• Comply with bank reporting requirements

• Identify compliance issues early, discuss with your CPA firm and request waiver

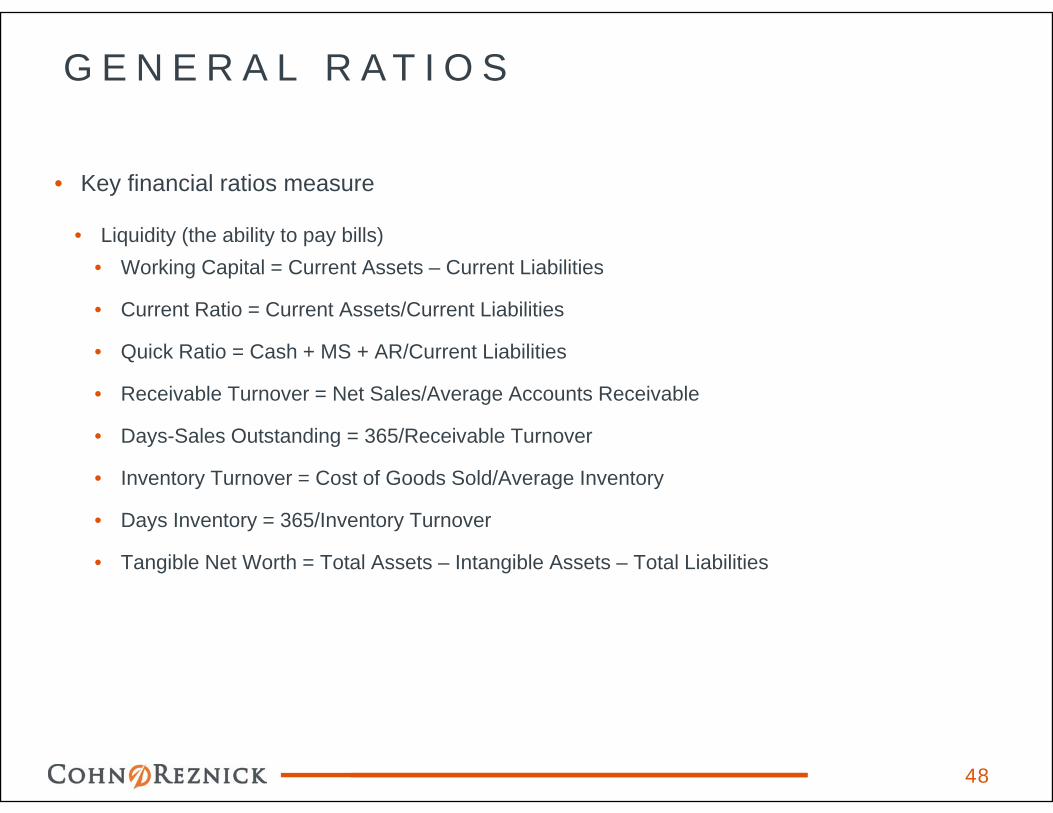

G E N E R A L R A T I O S

48

• Key financial ratios measure

• Liquidity (the ability to pay bills)• Working Capital = Current Assets – Current Liabilities

• Current Ratio = Current Assets/Current Liabilities

• Quick Ratio = Cash + MS + AR/Current Liabilities

• Receivable Turnover = Net Sales/Average Accounts Receivable

• Days-Sales Outstanding = 365/Receivable Turnover

• Inventory Turnover = Cost of Goods Sold/Average Inventory

• Days Inventory = 365/Inventory Turnover

• Tangible Net Worth = Total Assets – Intangible Assets – Total Liabilities

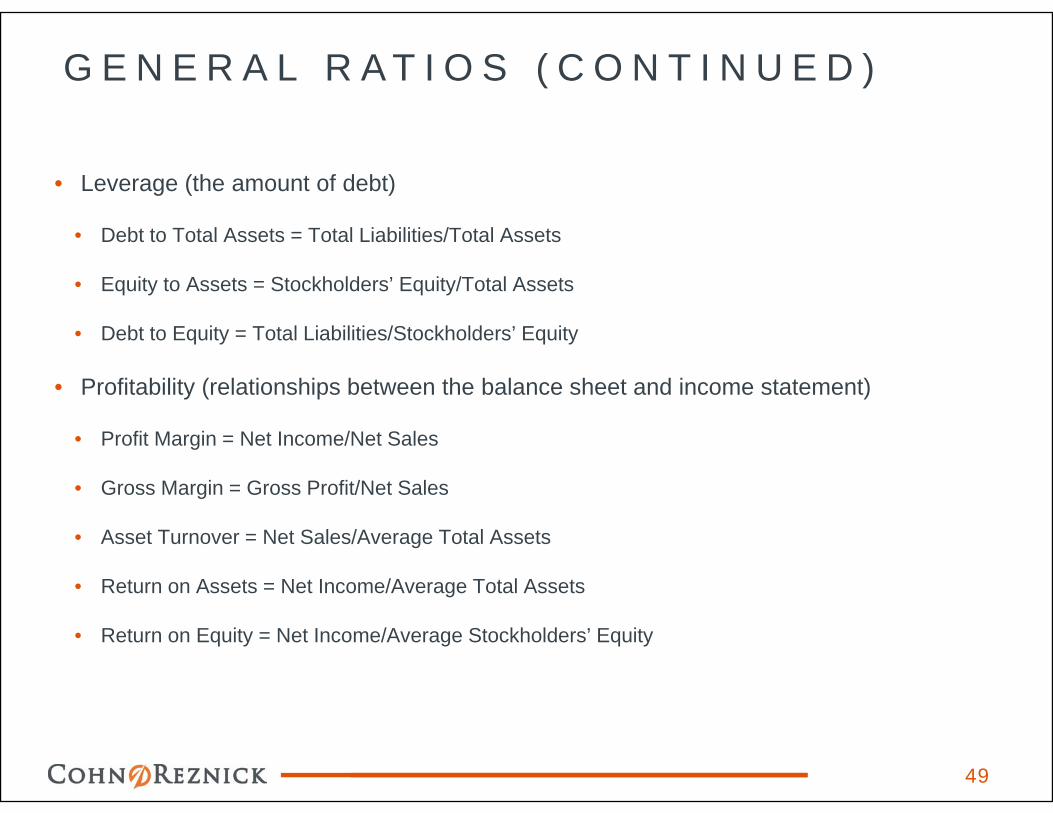

G E N E R A L R A T I O S ( C O N T I N U E D )

49

• Leverage (the amount of debt)

• Debt to Total Assets = Total Liabilities/Total Assets

• Equity to Assets = Stockholders’ Equity/Total Assets

• Debt to Equity = Total Liabilities/Stockholders’ Equity

• Profitability (relationships between the balance sheet and income statement)

• Profit Margin = Net Income/Net Sales

• Gross Margin = Gross Profit/Net Sales

• Asset Turnover = Net Sales/Average Total Assets

• Return on Assets = Net Income/Average Total Assets

• Return on Equity = Net Income/Average Stockholders’ Equity

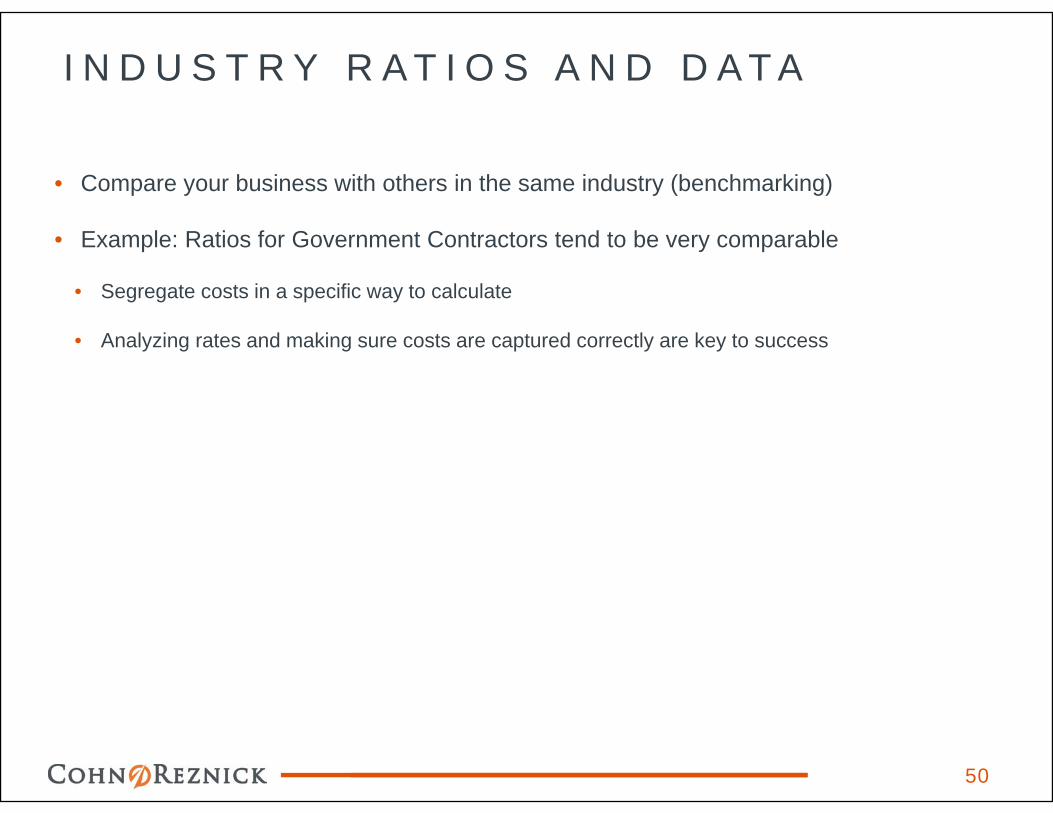

I N D U S T R Y R A T I O S A N D D A T A

50

• Compare your business with others in the same industry (benchmarking)

• Example: Ratios for Government Contractors tend to be very comparable

• Segregate costs in a specific way to calculate

• Analyzing rates and making sure costs are captured correctly are key to success

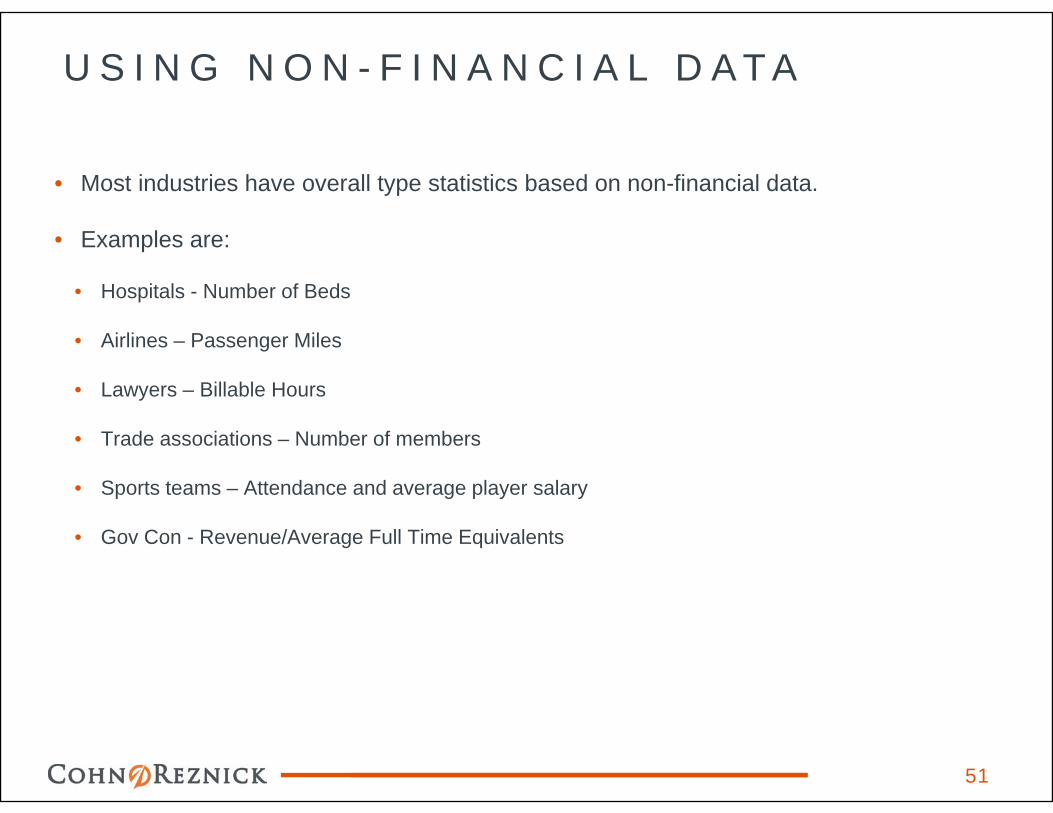

U S I N G N O N - F I N A N C I A L D A T A

51

• Most industries have overall type statistics based on non-financial data.

• Examples are:

• Hospitals - Number of Beds

• Airlines – Passenger Miles

• Lawyers – Billable Hours

• Trade associations – Number of members

• Sports teams – Attendance and average player salary

• Gov Con - Revenue/Average Full Time Equivalents

L I M I T A T I O N S O F F I N A N C I A L S T A T E M E N T S

52

• Financial statements are strictly historical measures of performance and a fair

representation of current condition

• Most serious limitation is that with the exception of cash and most liabilities, practically

everything else is based on forecasts, estimates, and assumptions

• Some of these are more reliable than others

S U M M A R Y

53

• Measure a combination of financial and performance indicators

• Management needs this data

• Concentrate on areas which will create a more successful, profitable business

• Know your users

Q U E S T I O N S / C O M M E N T S

54

R E S O U R C E S

55

Christine Williamson, [email protected](703) 847-4412

David Gaver, [email protected](703) 847-4456

GovCon360 keeps you abreast of the ever-changing regulatory environment that is Government contracting. From reference materials, like searchable pdf copies of the FAR and DCAM, to our past

Lunch and Learn seminar slide decks and thought pieces on industry matters, we’ve got it covered. Subscribe to our RSS feed to receive short alerts on recent industry changes. It’s always been

our job to help our clients maintain a competitive advantage by staying ahead of the curve. This website is an extension of the services we’ve been providing for over 35 years by putting useful

resources and up-to-date information at your fingertips.

www.govcon360.com