30

What’s Different Today Versus The Mid 1990’s? Morgan Stanley Basic Materials Conference February 25, 2004 Dan F. Smith President and CEO

| Date post: | 27-Dec-2015 |

| Category: |

Documents |

| Upload: | sandra-lyons |

| View: | 213 times |

| Download: | 0 times |

What’s Different Today Versus The Mid 1990’s?

Morgan Stanley Basic Materials Conference February 25, 2004

Dan F. SmithPresident and CEO

2

Safe Harbor LanguageStatements in this presentation relating to matters that are not historical facts are forward-looking statements. These forward-looking statements are just predictions or expectations and are subject to risks and uncertainties. Actual results could differ materially, based on factors including but not limited to the cyclical nature of the chemical and refining industries; availability, cost and volatility of raw materials and utilities; governmental regulatory actions and political unrest; global economic conditions; industry production capacity and operating rates; the supply/demand balance for Lyondell's and its joint ventures' products; competitive products and pricing pressures; access to capital markets; and technological developments and other risk factors. For more detailed information about the factors that could cause our actual results to differ materially, please refer to Lyondell Chemical Company’s Annual Report on Form 10-K for the year ended December 31, 2002, filed in March 2003, Lyondell’s Quarterly Report on Form 10-Q, filed in November, 2003, and Lyondell’s Annual Report on Form 10-K for the year ended December 31, 2003, which will be filed in March 2004. Reconciliations of GAAP financial measures to non-GAAP financial measures are provided at the end of this presentation.

3

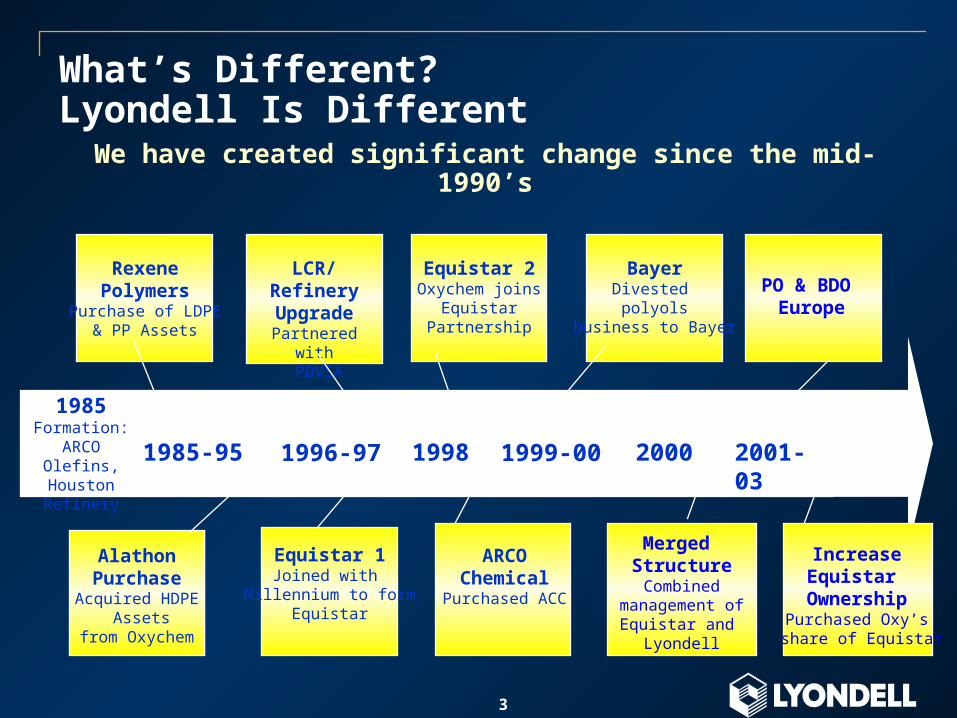

RexenePolymers

Purchase of LDPE& PP Assets

AlathonPurchase

Acquired HDPE Assets

from Oxychem

LCR/RefineryUpgrade

Partnered with PDVSA

Equistar 1Joined with

Millennium to formEquistar

Equistar 2Oxychem joins

EquistarPartnership

ARCOChemical

Purchased ACC

BayerDivested polyols

business to Bayer

Merged StructureCombined

management ofEquistar and

Lyondell

PO & BDO Europe

What’s Different?Lyondell Is Different

1985Formation:

ARCO Olefins, Houston Refinery

1998 1999-00 2000 2001-031996-971985-95

IncreaseEquistar

OwnershipPurchased Oxy’s share of Equistar

We have created significant change since the mid-1990’s

4

We’ve Developed A Balanced Portfolio

Lyondell

IC&D

LCR

Equistar

Commodity Leverage-- A leading North American producer of ethylene, propylene

and polyethylene-- Low cost position based on feedstock flexibility and scale

Growth & International Presence-- A leading global producer of PO and derivatives-- Process technology strength

Cash Generation-- Unique capability to refine heavy crude oils-- Contractually stable business; strong cash flow generator

($ MM)

Revenues EBITDALyondell

OwnershipIC&D $3,801 $245 100.0%Equistar 6,545 175 70.5LCR 4,162 377 58.75

2003

5

Leading Product Positions Create Significant Earnings Leverage

1 Source: LYO capacities as of January 2004, CMAI2 Includes 100% of joint venture volumes3 Does not include refinery-grade material or production from the product flexibility unit at Equistar’s Channelview

facility.4 Based on 1¢/gal change

Inte

rmed

iate

C

hem

ica

ls a

nd

D

eriv

ati

ves

Eq

uis

tar

Product Annual Capacity(1)

Capacity Position

Propylene Oxide(2)

( lbs) 4.5 billion 1st in North America1 st in the world

Styrene Monomer (lbs) 5.0 billion 1st in North America4th in the world

MTBE (bbl/day) 58,500 1st in North America1st in the world

Ethylene (lbs) 11.6 billion 2nd in North America5th in the world

Propylene (lbs) 5.0 billion 2nd in North America7 th in the world

Polyethylene (lbs) 5.7 billion 3 rd in North America4 th in the world

(1)

(3)

$23MM

$21MM

$ 9MM

$116MM

$50MM

$57MM

Pre-TaxLeverage(∆1¢/unit)

(4)

6

We’ve Significantly Strengthened Our Operations

0

30

60

90

120

150

180

Lyondell Equistar PO11 Spending Regulatory

4.2%

9.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

LYO+EQU Peers

SG

&A

+ R

&D

, %S

ale

s

0102030405060708090

1998 2003

Lyondell Equistar

Safety PerformanceEnterprise Incident Rate

Days of Working Capital *Capital Spending

Average SG&A and R&D, % Sales 2000 - 2002

1999 2004 Budget

$MM

Re

co

rda

ble

In

jury

Ra

te

1st Quartile ’02 1.001.180.99

0.8

0.52 0.52

0

0.5

1

1.5

2

1999 2000 2001 2002 2003

Days

* Based on accounts receivable (including those sold), inventories & accounts payable as of 12/03, and fourth-quarter days of sales.

Peers include:

Dow, Nova,

Eastman, Celanese,

Solutia, Westlake,

Millennium, Georgia Gulf

7

Lyondell’s Portfolio Is Significantly Larger Than In The Early 1990’s

Early 1990’s Today

Petrochemicals - 100% Owned - 70.5% Owned

& Polymers - 2 Ethylene Plants - 8 Ethylene Plants

- 1 Polymer Plant - 7 Polymer Plants

- 2 MEG Plants

Refining - 100% Owned - 58.75% Owned

- Sour Crude Refinery - Heavy Crude Refinery

- PDVSA Contract

IC&D - 100% Owned

- 3 POSM Plants

- 5 PO/MTBE Plants

- Nihon Oxirane JV POSM

Plant

8

We’ve Increased Market Cap and Liquidity

Late 1993 Jan-Feb 2004

Shares Outstanding 80 MM 176 MM

Share Price $20 – 23 $17 – 19

Trading Liquidity ~100 M Shares/Day ~1 MM Shares/Day

9

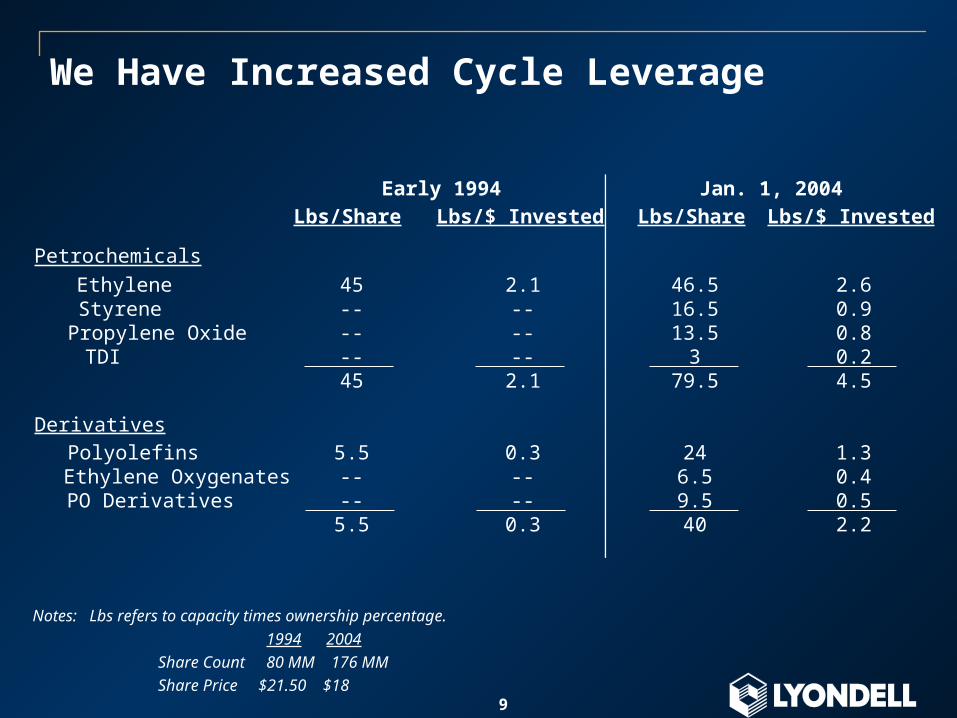

We Have Increased Cycle Leverage

Lbs/Share Lbs/$ Invested Lbs/Share Lbs/$ Invested

Petrochemicals

Ethylene 45 2.1 46.5 2.6 Styrene -- -- 16.5 0.9 Propylene Oxide -- -- 13.5 0.8 TDI -- -- 3 0.2

45 2.1 79.5 4.5

Derivatives

Polyolefins 5.5 0.3 24 1.3 Ethylene Oxygenates -- -- 6.5 0.4 PO Derivatives -- -- 9.5 0.5

5.5 0.3 40 2.2

Early 1994 Jan. 1, 2004

Notes: Lbs refers to capacity times ownership percentage.

1994 2004

Share Count 80 MM 176 MM

Share Price $21.50 $18

10

Lyondell Stock Has Performed Well In Recessions and Recoveries

-15-10

-505

101520253035

Q4 '90 - Q4 '93Downturn

Q4 '93 - July '95Recovery

Q4 '00 - Q4 '03Downturn

Q4 '03 - ?Recovery

Lyondell S&P 500

1990 – 1995 Cycle 2000 – 200? Cycle

Sh

areh

old

er R

etu

rn %

/ Y

r

Source: Bloomberg

11

Most But Not All Industry Fundamentals Are Unchanged

Energy prices have changed

Economy emerging from a downturn

Cyclicality has not been repealed

Product growth driven by improved quality of life

Sustained advantage requires differential cost, scale and/or technology

12

The Energy World Was Very Different

Source: Platt’s

Early Jan / Feb1990's 1994 / 95 2004

Crude ($/Bbl) $18 - 24 $17 - 18 $32 - 35

Natural Gas ($/MMBtu) $1.50 - 2.00 $1.50 - 1.85 $5.25 - 5.50

Crude / Gas 9 - 14 9 - 11 6

13

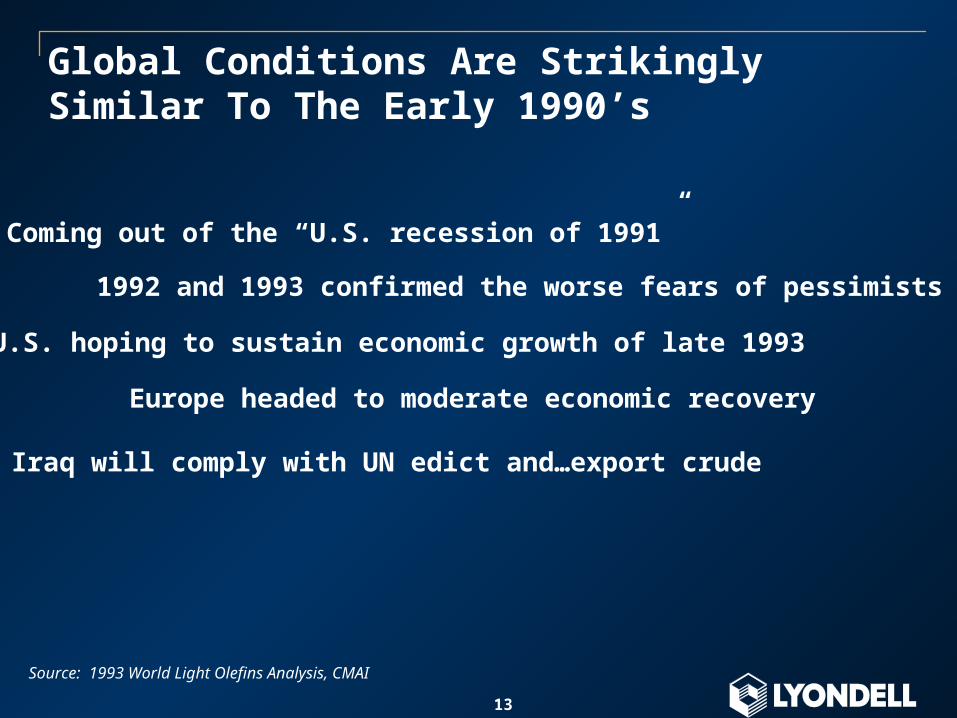

Global Conditions Are Strikingly Similar To The Early 1990’s

Coming out of the “U.S. recession of 1991”

1992 and 1993 confirmed the worse fears of pessimists

U.S. hoping to sustain economic growth of late 1993

Europe headed to moderate economic recovery

Iraq will comply with UN edict and…export crude

Source: 1993 World Light Olefins Analysis, CMAI

14

0

1

2

3

4

5

1986 1989 1992 1995 1998 2001 2004 2007

The Global Economy is Emerging from a Difficult Period

(Percent change in real GDP)Global GDP

Source: Global Insights

15

Within The Ethylene Industry, There Are Striking Similarities Between 1993 And 2003

Demand forecasts

• Annual rate of 4.9% per year 1992-1998 period

• Worldwide growth…during 1993 . . . 2%

• New light olefins in Asia/Pacific and Africa/Middle East will severely impact exports

Source: 1993 World Light Olefins Analysis, CMAI

Operating rate forecasts

• Slowly improve from 85% in 1993

• Between 1993 and 1997…17.9 MM tons capacity will be added

• In the U.S. between 1990 and 1992 three new world scale plants

16

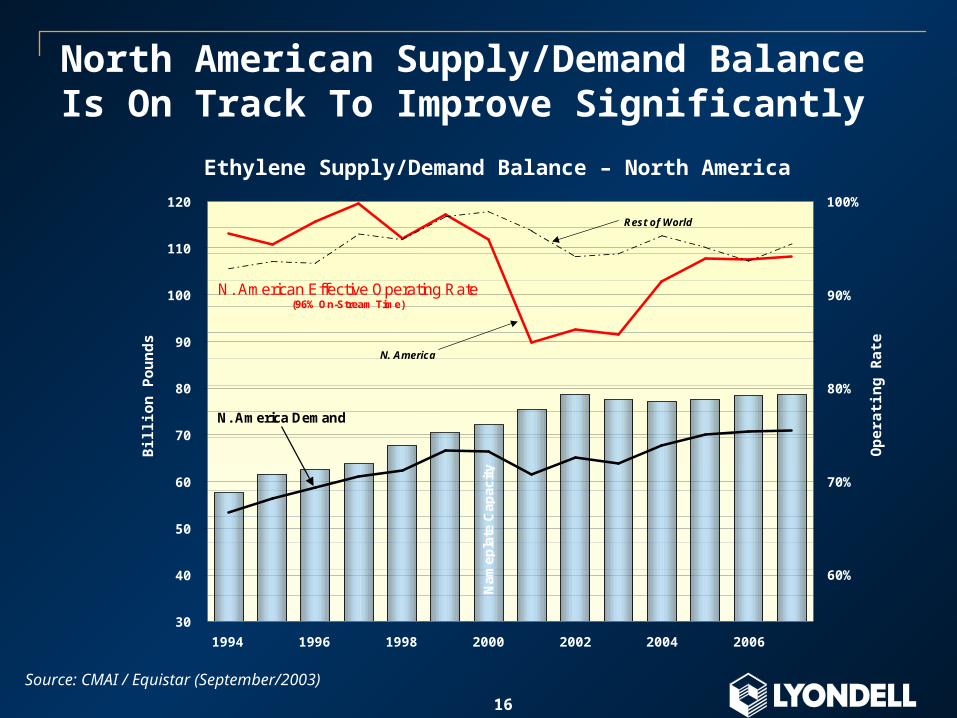

North American Supply/Demand Balance Is On Track To Improve Significantly

30

40

50

60

70

80

90

100

110

120

1994 1996 1998 2000 2002 2004 2006

Bil

lio

n P

ou

nd

s

60%

70%

80%

90%

100%

Op

erat

ing

Rat

e

Ethylene Supply/Demand Balance – North America

Source: CMAI / Equistar (September/2003)

Nam

epla

te C

apac

ity

N. American Effective Operating Rate(96% On-Stream Time)

N. America Demand

Rest of World

N. America

17

We Believe that Global Ethylene Supply/Demand is on a Path to a Tight Balance

175

200

225

250

275

300

2003 2007 '07 + 2% Growth '07 - 18 Mo Delay

Wo

rld

Eth

yle

ne

Su

pp

ly -

De

ma

nd

(billio

n p

ou

nd

s/y

ear)

Effective Capacity Demand

Source: CMAI

SensitivityCMAI base case

96%104%

99%

18

0

20

40

60

80

100

120

0 5, 000 10, 000 15, 000 20, 000 25, 000 30, 000 35, 000 40, 000

US

Korea

Taiwan

WE

Singapore

Japan

Thailand

Malaysia

ChinaIndiaIndonesia

The Emergence of a Middle Class Increases Local Demand for Plastics

Sources: CMAI 2001; Nexant Chemsystems

0

2

4

6

8

10

12

Domestic Exports

1995 2001

China PE Demand

Domestic vs. Export

PE Consumption/capita, lbs

2000 GDP/Capita

19

Historically Ethylene And Styrene Have Had The Most Leverage To A Cyclical Upturn

0

5

10

15

20

25

30

Naphtha -HDPE

Styrene

Contract Pricing Margin Change: Trough To Peak

1992/93 vs. 1995Δ Margin

¢ / lb

Source: CMAI; Lyondell Databook

20

Enterprise Earnings Capability Far Exceeds Recent Trough Results

0

500

1000

1500

2000

2500

3000

2003 1999/2000Margins

1995 Margins 1988 Margins

$MM

LCR IC&D Equistar

1 Chem Data/CMAI industry margins conditions for IC&D and Equistar products (ex. MTBE) applied to current capacities and ownership, LCR 2003 EBITDA. Note: Assumes current capital structure; 175 MM shares.

1

1 1

Recession/ Trough

Pre-Recession

PeakCycle EBITDA Potential

$6.90 / share

$1.40 / share

2003Proportional

Interest,Dividends &

Capital

21

Investing Based on Differential Technology – PO & Derivatives

• Growth rate: 4-5%/yr

• End Use:

• Polyols: seating, mattresses, insulation,

coatings

• PG: deicers, boat hulls, coatings,

countertops/showers, personal care

• Ethers: coatings, electronics

• BDO: Spandex, electrical & auto parts

• Basis of differentiation:

• Proprietary process technology/cost

• Global position

• Derivative integration

Dow

Shell/BASF

LYO & PartnersOther

2003 PO Capacity Share

PG

OtherBDO

Ethers

Polyols

2003 Derivative Demand

Source: SRI, Tecnon, Lyondell estimates

22

Propylene Oxide Is Differentiated From Other Commodity Petrochemicals By Its Technology Position

Co-Product Technology

Chlorine-Based

Technology

LYO &Partners

Asian Region European

Region

AmericanRegion

LYO LYO

LYO

PO Regional CapacityPO Technology Source

Source: SRI, Tecnon , Lyondell estimates

23

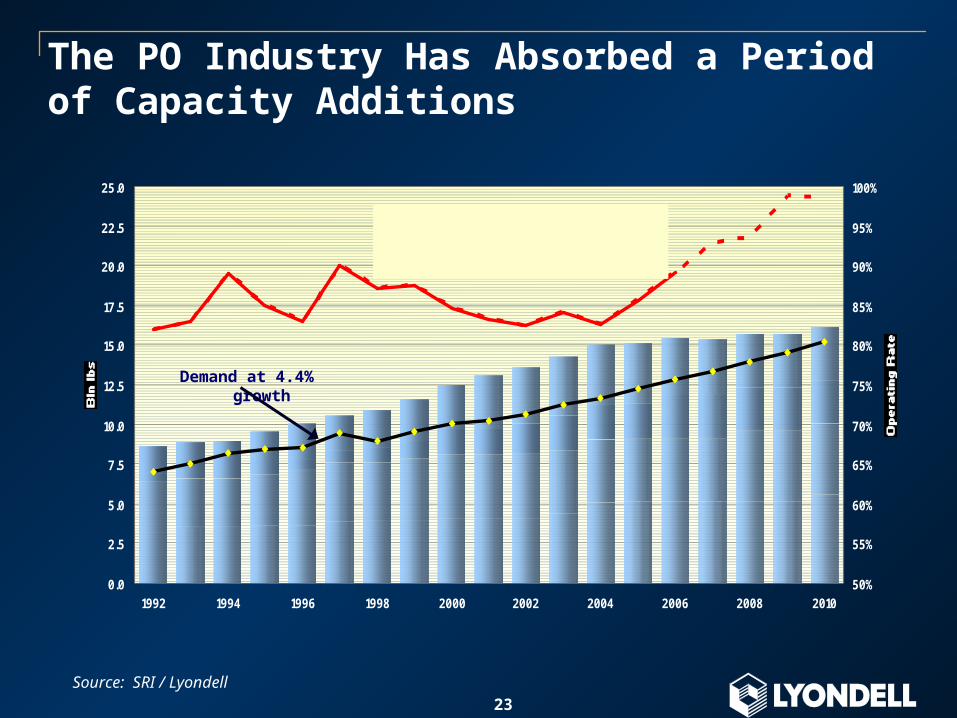

The PO Industry Has Absorbed a Period of Capacity Additions

Source: SRI / Lyondell

0.0

2.5

5.0

7.5

10.0

12.5

15.0

17.5

20.0

22.5

25.0

1992 1994 1996 1998 2000 2002 2004 2006 2008 201050%

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%

Nam

epla

te C

apac

ity

Effective Operating Rate(96% On Stream Time)

Demand at 4.4% growth

24

The Lyondell Enterprise Has A Well Established Presence in Asia

Presence established in 1972

40% interest in Nihon Oxirane

$1 B revenue 1

2.5 B lbs of sales 1

Leading PO and derivative positions

Strong styrene relationships

1 Includes 100% of Nihon Oxirane

BeijingTokyo

Shanghai

Taipei

Hong Kong

Guangzhou

Offices

Inventory

Point

Manufacturing

25

The Asian / Middle East Propylene And PO Chain Supply / Demand Balance Represent An Opportunity

0

2

4

6

8

10

12

14

16

18

20

Demand Growth Supply Growth0

1

2

3

4

DemandGrowth

SupplyGrowth

DemandGrowth

SupplyGrowth

Propylene Oxide GrowthPropylene Growth

2002 - 2007 2002 - 2007 2007 - 2010Blbs Blbs

EthyleneEthylene

Co-ProductCo-Product

FCCFCC

Co-ProductCo-Product

Source: CMAI, SRI, Lyondell Estimates

26

LyondellWhat Is NOT Different? Our Financial Strategy

Maintain Sufficient Liquidity

Repay Debt

Create Shareholder Value

27

Lyondell Stock Has Performed Well In Recessions and Recoveries

-15-10

-505

101520253035

Q4 '90 - Q4 '93Downturn

Q4 '93 - July '95Recovery

Q4 '00 - Q4 '03Downturn

Q4 '03 - ?Recovery

Lyondell S&P 500

1990 – 1995 Cycle 2000 – 200? Cycle

Sh

areh

old

er R

etu

rn %

/ Y

r

Source: Bloomberg

28

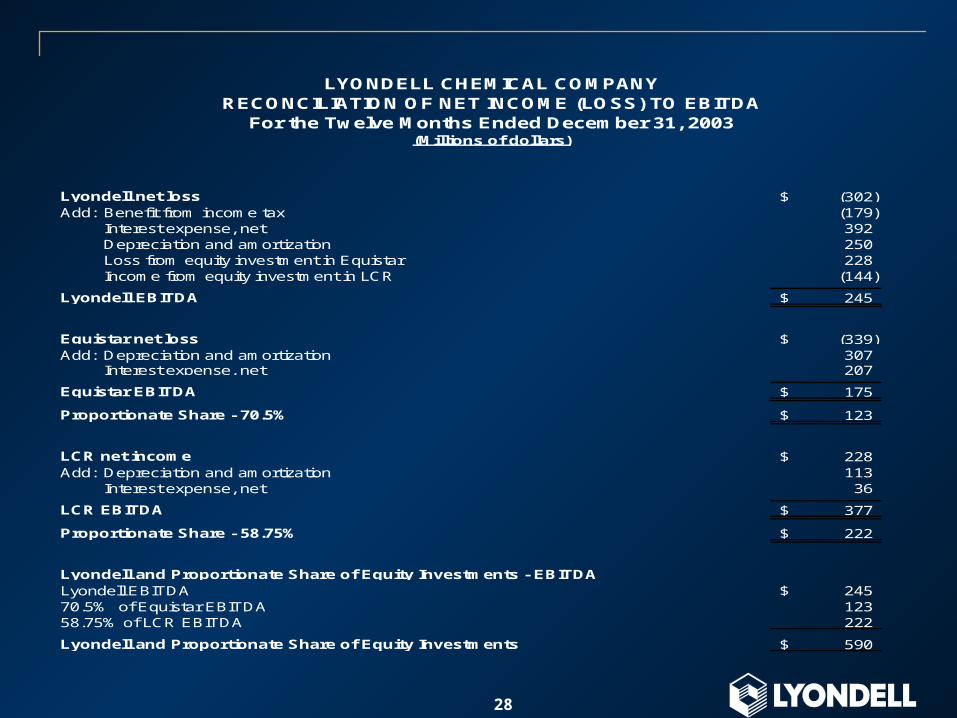

Lyondell net loss (302)$ Add: Benefit from income tax (179)

Interest expense, net 392 Depreciation and amortization 250 Loss from equity investment in Equistar 228 Income from equity investment in LCR (144)

Lyondell EBITDA 245$

Equistar net loss (339)$ Add: Depreciation and amortization 307

Interest expense, net 207

Equistar EBITDA 175$

Proportionate Share - 70.5% 123$

LCR net income 228$ Add: Depreciation and amortization 113

Interest expense, net 36

LCR EBITDA 377$

Proportionate Share - 58.75% 222$

Lyondell and Proportionate Share of Equity Investments - EBITDA Lyondell EBITDA 245$ 70.5% of Equistar EBITDA 123 58.75% of LCR EBITDA 222

Lyondell and Proportionate Share of Equity Investments 590$

LYONDELL CHEMICAL COMPANYRECONCILIATION OF NET INCOME (LOSS) TO EBITDA

(Millions of dollars)For the Twelve Months Ended December 31, 2003

29

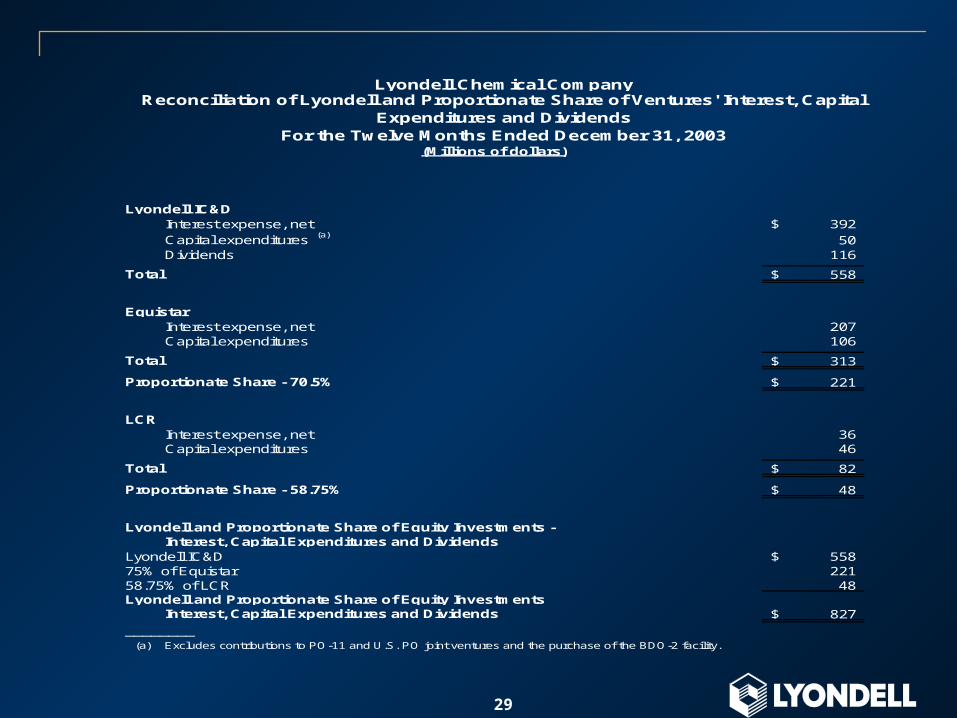

Lyondell IC&DInterest expense, net 392$ Capital expenditures (a) 50 Dividends 116

Total 558$

Equistar Interest expense, net 207 Capital expenditures 106

Total 313$

Proportionate Share - 70.5% 221$

LCRInterest expense, net 36 Capital expenditures 46

Total 82$

Proportionate Share - 58.75% 48$

Lyondell and Proportionate Share of Equity Investments - Interest, Capital Expenditures and DividendsLyondell IC&D 558$ 75% of Equistar 221 58.75% of LCR 48 Lyondell and Proportionate Share of Equity Investments

Interest, Capital Expenditures and Dividends 827$

________(a) Excludes contributions to PO-11 and U.S. PO joint ventures and the purchase of the BDO-2 facility.

Lyondell Chemical Company

(Millions of dollars)For the Twelve Months Ended December 31, 2003

Reconciliation of Lyondell and Proportionate Share of Ventures' Interest, Capital Expenditures and Dividends

30

Dec. 31, 1998 * Dec. 31, 2003

Lyondell Equistar Lyondell Equistar

Working Capital: (a)

Accounts receivable (b) 479$ 522$ 449$ 608$

Inventories 550 549 347 408

Accounts payable (310) (337) (431) (513)

Total 719 734 365 503

Add: Accounts receivable sold (c) 160 130 75 102

Adjusted working capital 879$ 864$ 440$ 605$

Days of Working Capital:

Fourth Quarter Sales Revenue 872$ 1,141$ 945$ 1,665$

Days in Quarter 92 92 92 92

Sales per day 9.5$ 12.4$ 10.3$ 18.1$

Days of working capital (b) (d) 93 70 43 33

(a) Defined as the major controllable components of working capital - receivables, inventories and payables. (b) In consideration of discounts offered to certain customers for early payment for product delivered in December 2003, some

receivable amounts were collected in December 2003 that otherwise would have been expected to be collected in January 2004, including $41 million from Occidental. Had such amounts been collected in January 2004, days of working capitalwould have been 36 days.

(c) Receivables sold are added back for consistency as such amounts are included in sales and in the sales per day calculation. Management believes that this provides useful information to investors because it reflects Lyondell's and Equistar's responsibility for administration and collection of said amounts.

(d) Days of working capital are calculated as adjusted working capital divided by sales per day.

Days of Working CapitalReconciliation

Dollars in Millions