23

What’s on an investor’s mind? Stephen Blackman, RBS Group Economics

| Date post: | 20-Dec-2015 |

| Category: |

Documents |

| View: | 218 times |

| Download: | 3 times |

What’s on an investor’s mind?

Stephen Blackman, RBS Group Economics

Slide 2

Three questions

What is the likely path of global growth?

Why does macro matter so much to investors?

Where would you put your last penny?

Slides available from: [email protected] or http://www.rbs.com

Slide 3

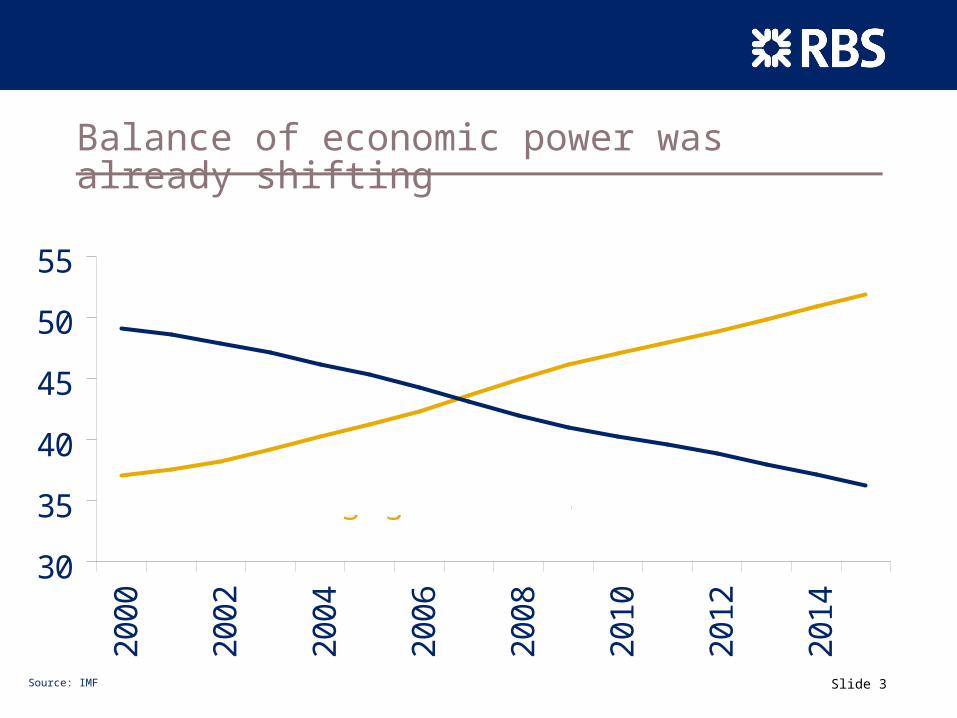

Balance of economic power was already shifting

30

35

40

45

50

55

2000

2002

2004

2006

2008

2010

2012

2014

Share of World GDP in PPP terms (%)

G7

Emerging Economies

Source: IMF

Slide 4

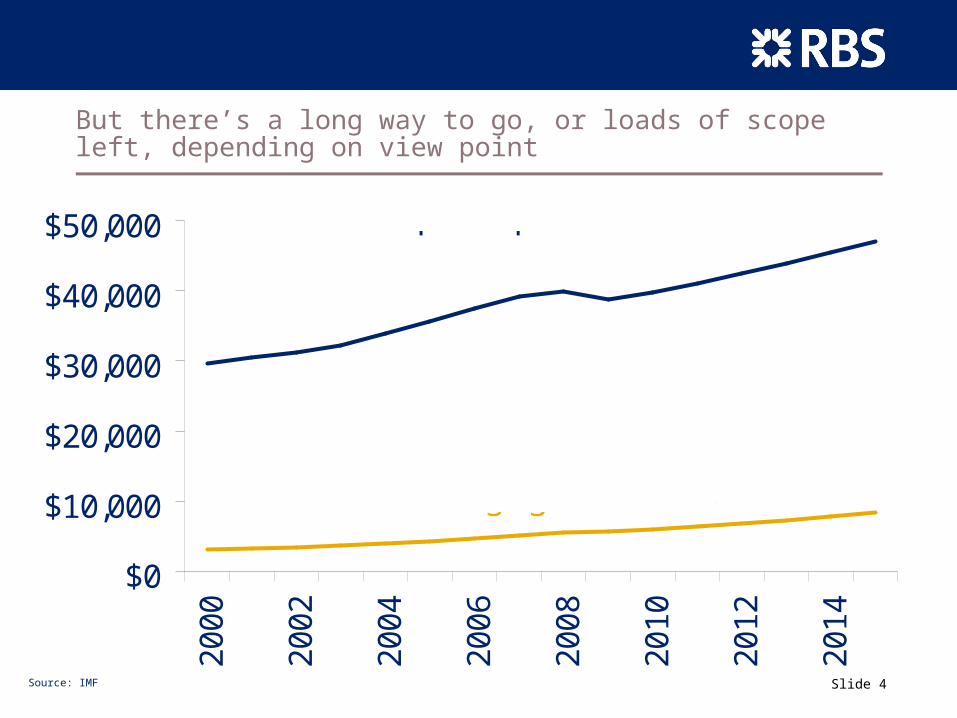

But there’s a long way to go, or loads of scope left, depending on view point

$0

$10,000

$20,000

$30,000

$40,000

$50,00020

00

2002

2004

2006

2008

2010

2012

2014

GDP per Capita in PPP

G7

Emerging Economies

Source: IMF

Slide 5

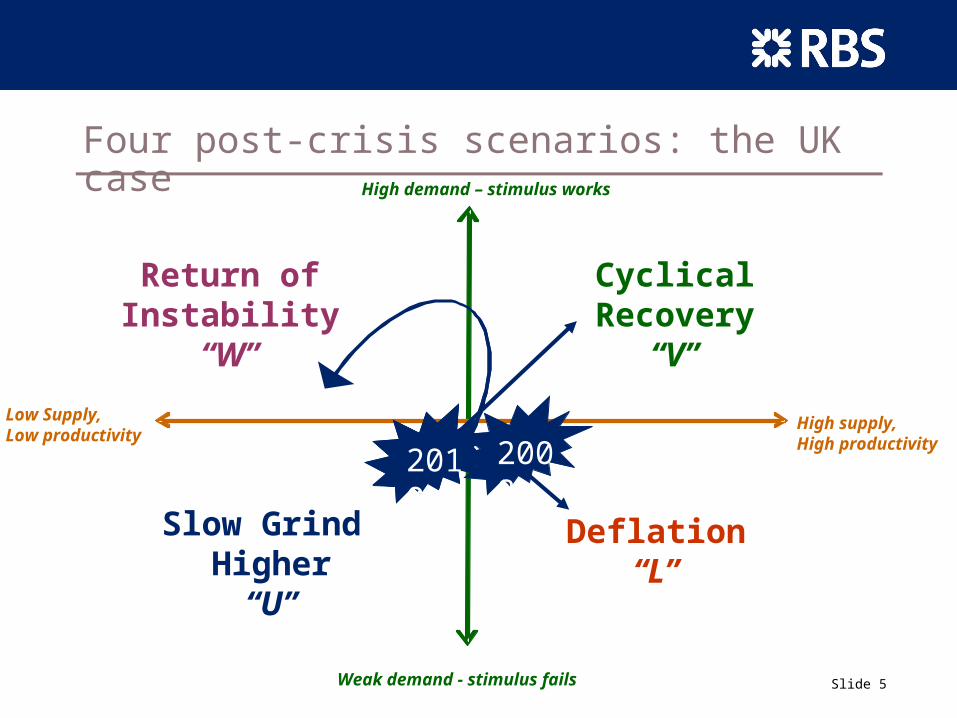

Four post-crisis scenarios: the UK case

Slow Grind Higher

“U”

Return ofInstability

“W”

Cyclical Recovery“V”

Deflation“L”

High supply, High productivity

Low Supply,Low productivity

High demand – stimulus works

Weak demand - stimulus fails

2009 20082010

Slide 6

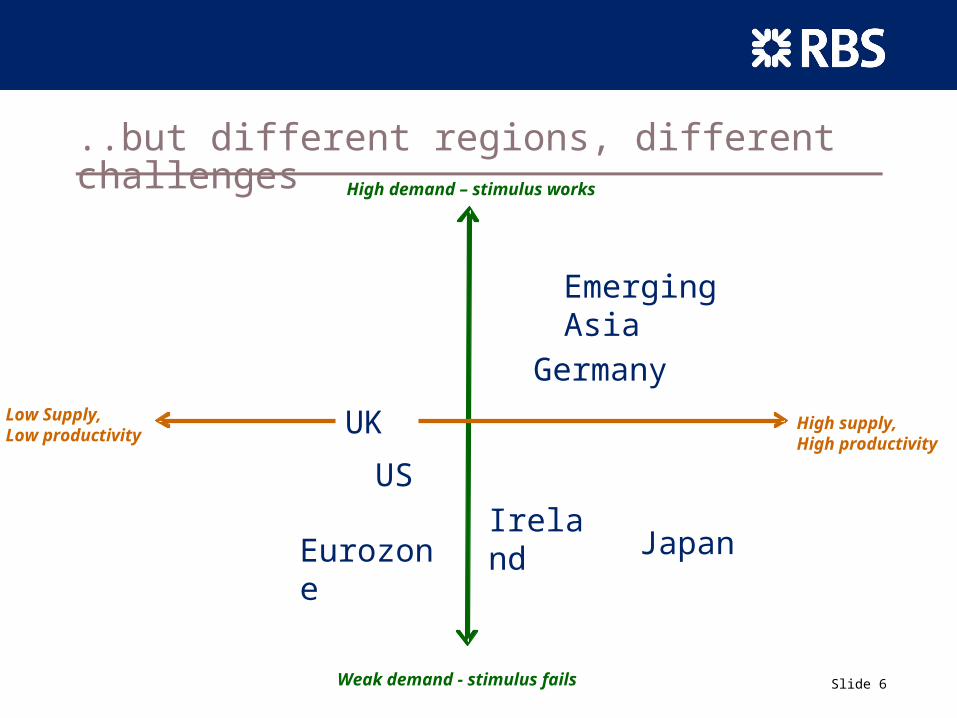

..but different regions, different challenges

Japan

US

UK

Eurozone

Emerging Asia

Ireland

GermanyLow Supply,Low productivity

High supply, High productivity

High demand – stimulus works

Weak demand - stimulus fails

Slide 7

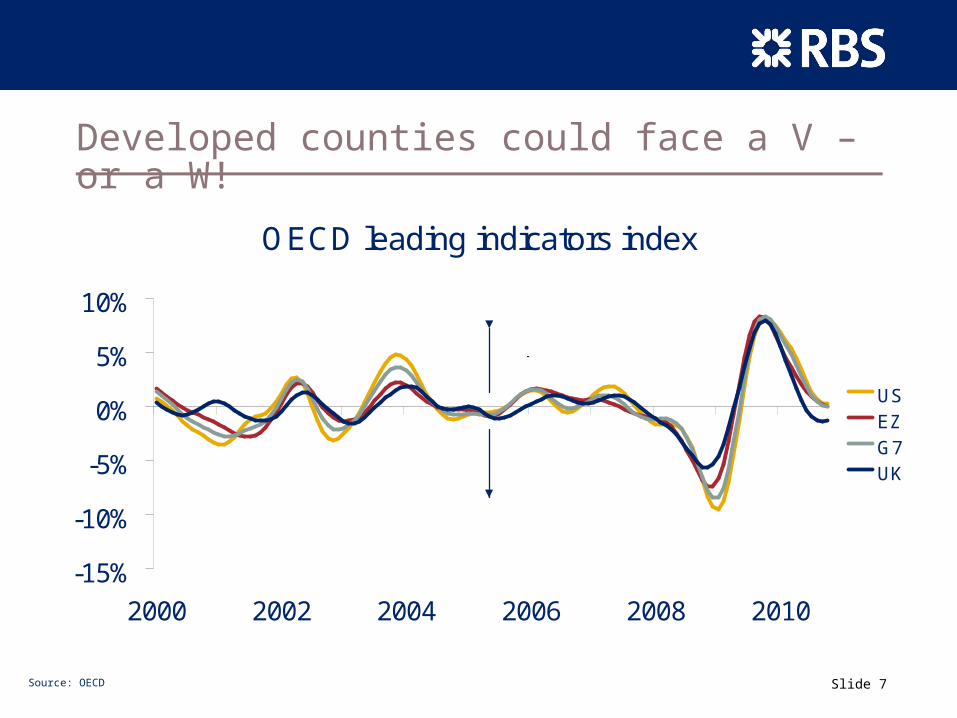

Developed counties could face a V – or a W!

OECD leading indicators index

-15%

-10%

-5%

0%

5%

10%

2000 2002 2004 2006 2008 2010

USEZG7

UK

Expansion

Contraction

Source: OECD

Slide 8

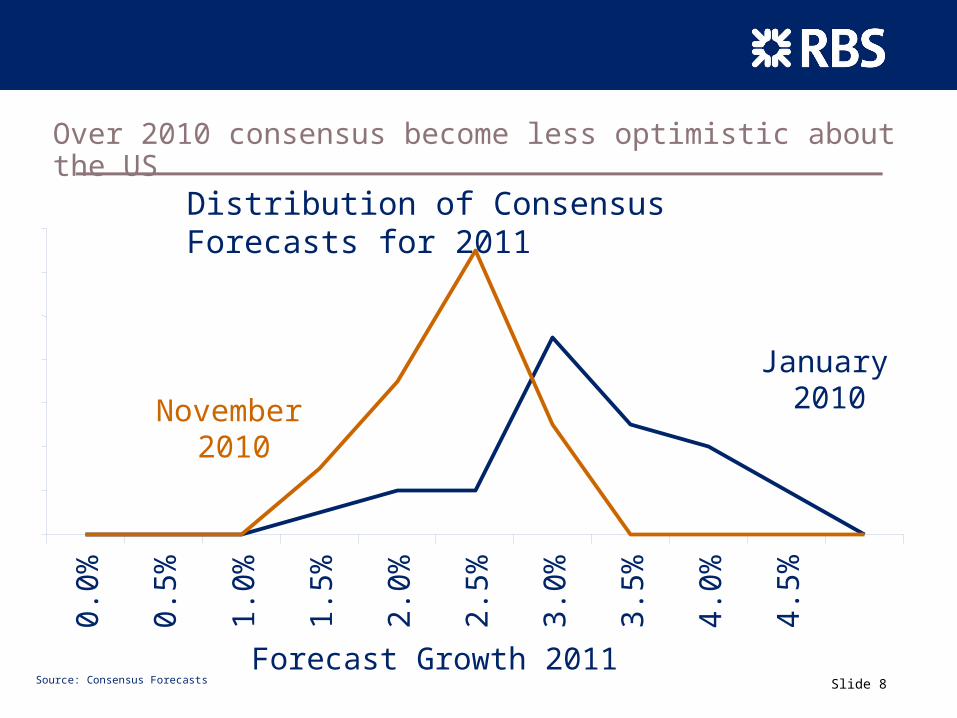

Over 2010 consensus become less optimistic about the US

Distribution of Consensus Forecasts for 2011

Source: Consensus Forecasts

0.0

%

0.5

%

1.0

%

1.5

%

2.0

%

2.5

%

3.0

%

3.5

%

4.0

%

4.5

%

Forecast Growth 2011

January 2010November

2010

Slide 9

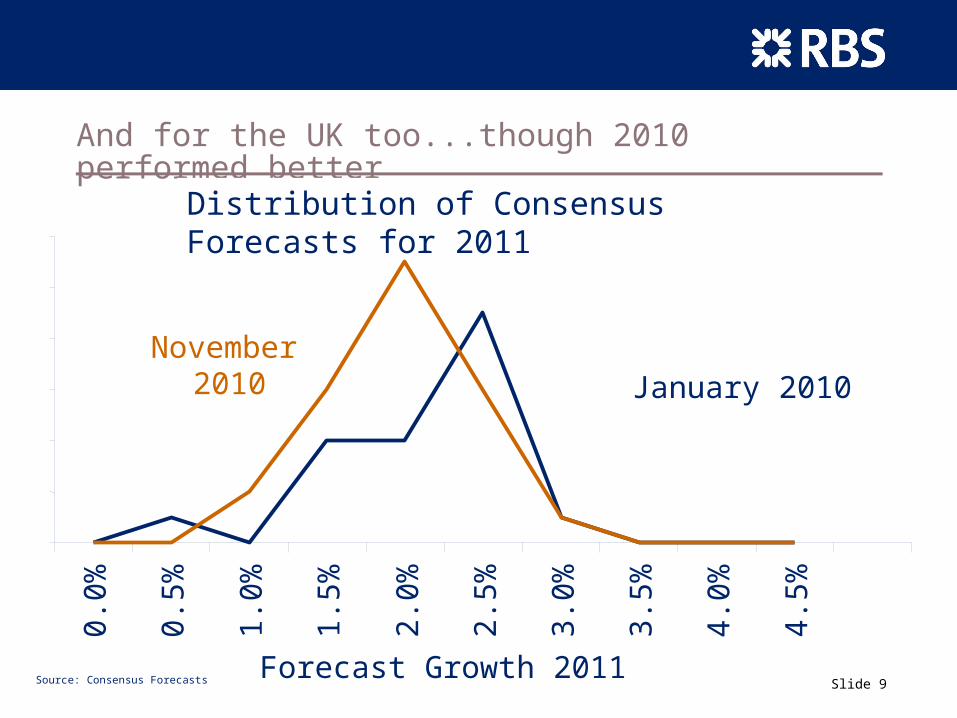

And for the UK too...though 2010 performed better

Source: Consensus Forecasts

Distribution of Consensus Forecasts for 2011

0.0

%

0.5

%

1.0

%

1.5

%

2.0

%

2.5

%

3.0

%

3.5

%

4.0

%

4.5

%

Forecast Growth 2011

January 2010November

2010

Slide 10

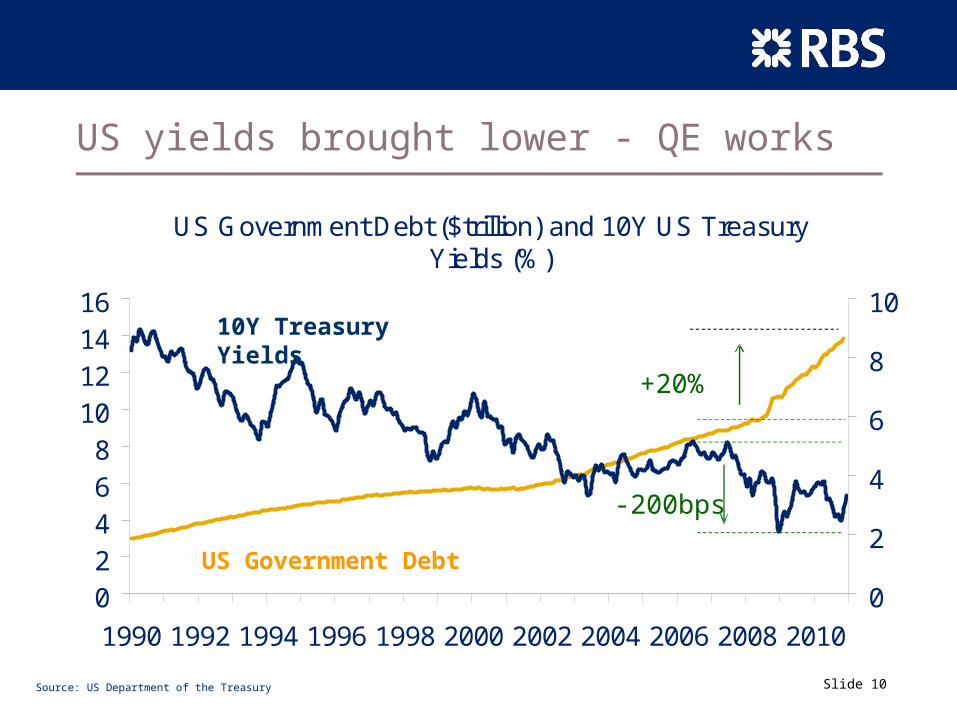

US yields brought lower - QE works

Source: US Department of the Treasury

US Government Debt ($trillion) and 10Y US Treasury Yields (%)

02468

10121416

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

0

2

4

6

8

10

US Government Debt

10Y Treasury Yields

+20%

-200bps

Slide 11

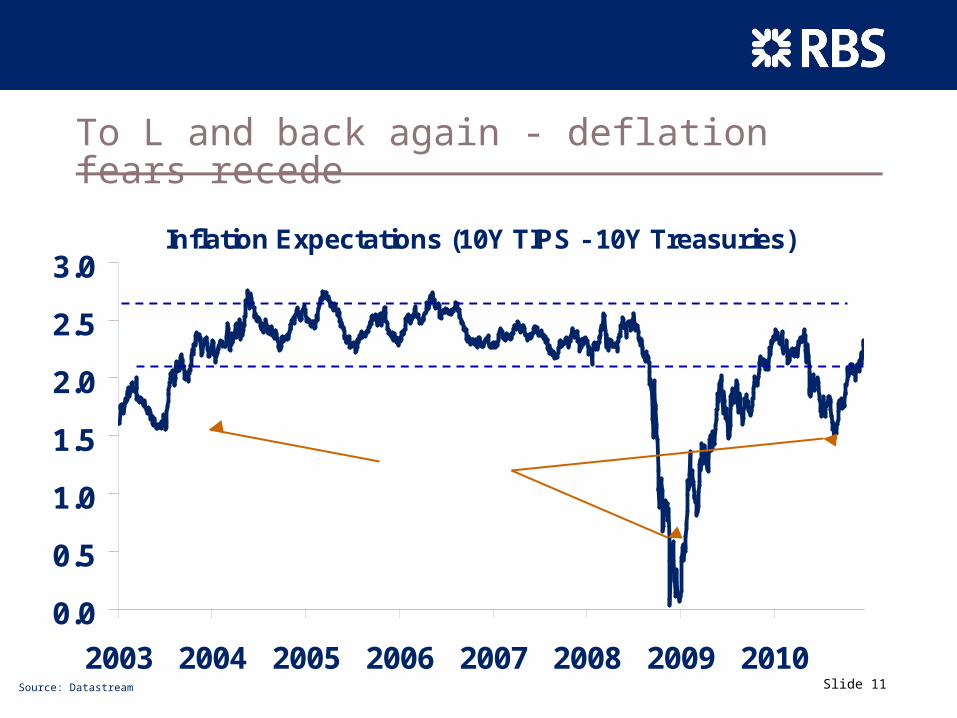

To L and back again - deflation fears recede

Source: Datastream

Inflation Expectations (10Y TIPS - 10Y Treasuries)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2003 2004 2005 2006 2007 2008 2009 2010

Deflation Scares

Slide 12

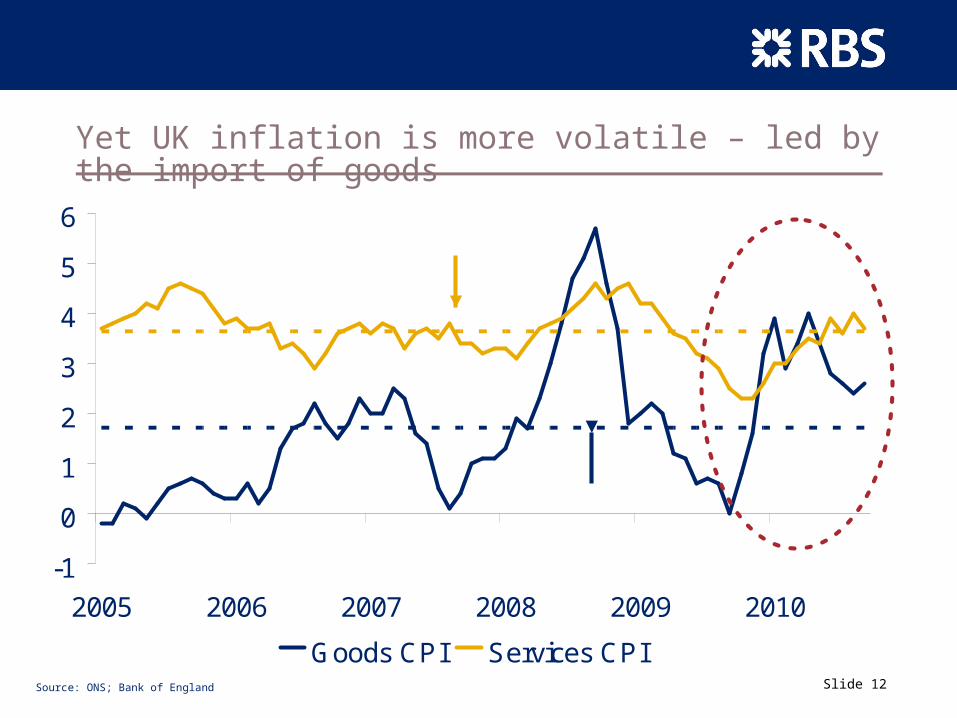

Yet UK inflation is more volatile – led by the import of goods

Source: ONS; Bank of England

-1

0

1

2

3

4

5

6

2005 2006 2007 2008 2009 2010

Goods CPI Services CPI

Average Goods CPI

Average Services CPI

Slide 13

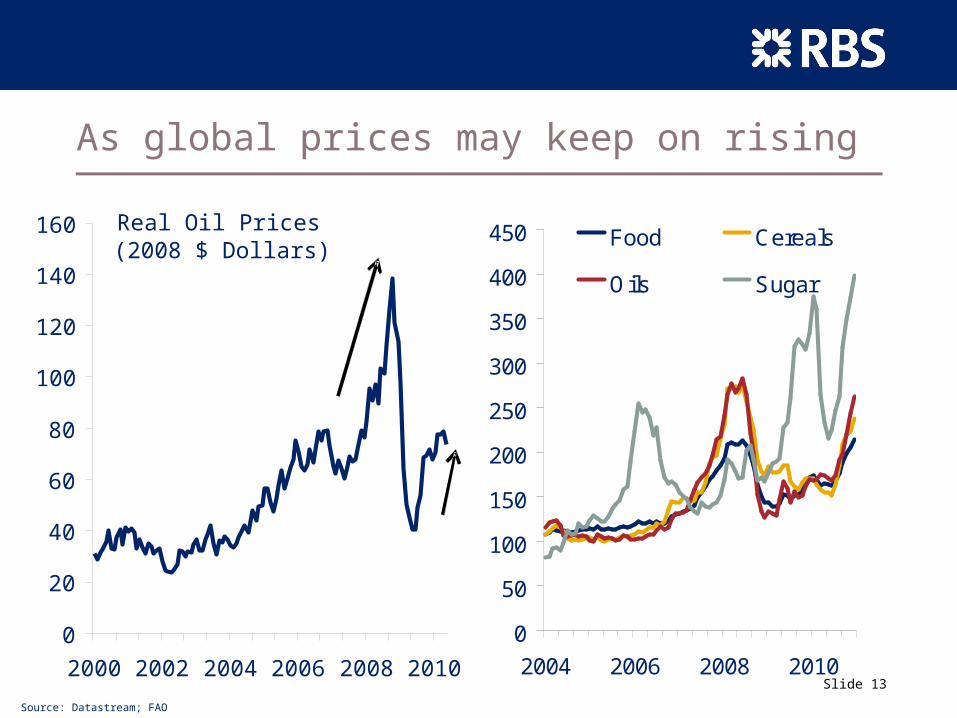

As global prices may keep on rising

0

50

100

150

200

250

300

350

400

450

2004 2006 2008 2010

Food Cereals

Oils Sugar

0

20

40

60

80

100

120

140

160

2000 2002 2004 2006 2008 2010

Real Oil Prices (2008 $ Dollars)

Source: Datastream; FAO

Slide 14

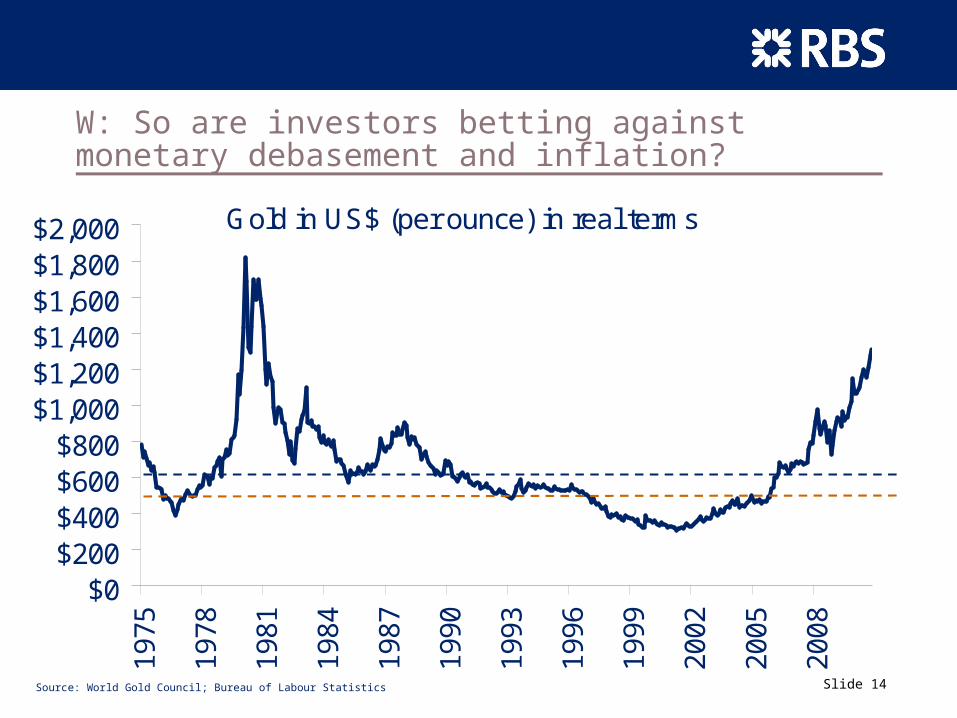

W: So are investors betting against monetary debasement and inflation?

Source: World Gold Council; Bureau of Labour Statistics

Gold in US$ (per ounce) in real terms

$0$200$400$600$800

$1,000$1,200$1,400$1,600$1,800$2,000

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

Average Price

Marginal cost

Slide 15

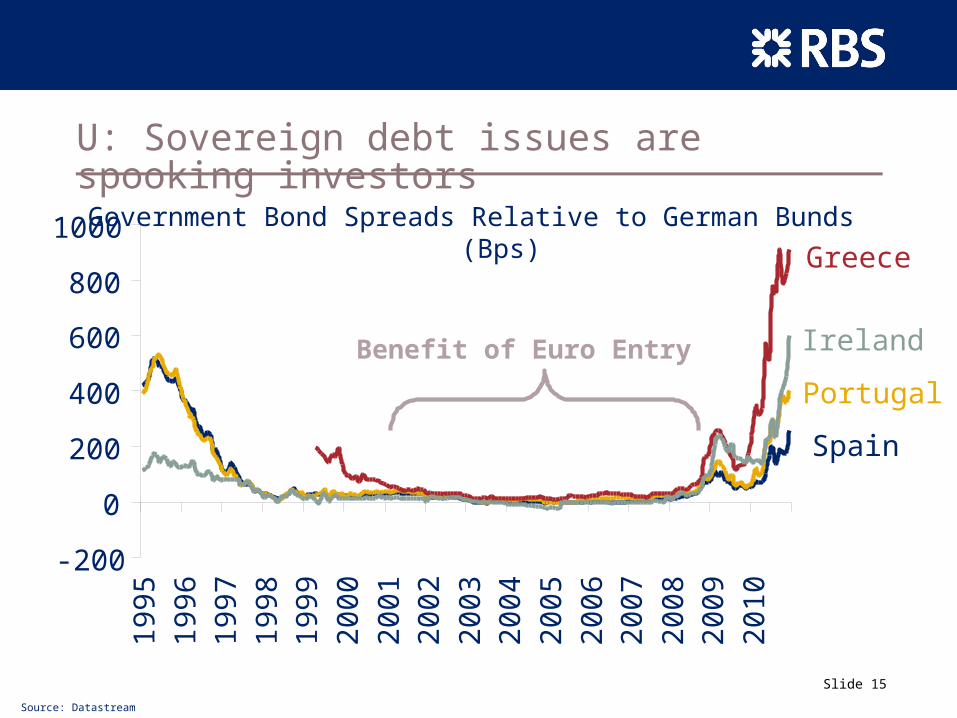

U: Sovereign debt issues are spooking investors

-200

0

200

400

600

800

1000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Greece

Ireland

Portugal

Spain

Government Bond Spreads Relative to German Bunds (Bps)

Benefit of Euro Entry

Source: Datastream

Slide 16Slide 16

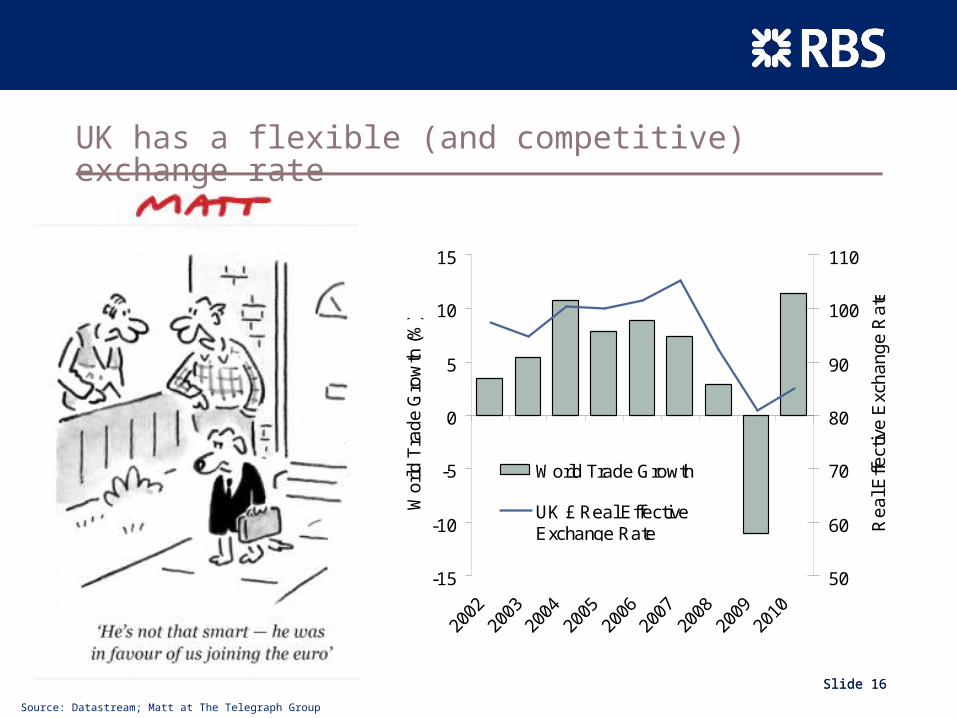

UK has a flexible (and competitive) exchange rate

-15

-10

-5

0

5

10

15

200

2 2

003

200

4 2

005

200

6 2

007

200

8 2

009

201

0

Wo

rld

Tra

de

Gro

wth

(%

)

50

60

70

80

90

100

110

Re

al E

ffect

ive

Exc

ha

ng

e R

ate

World Trade Growth

UK £ Real EffectiveExchange Rate

Source: Datastream; Matt at The Telegraph Group

Slide 17

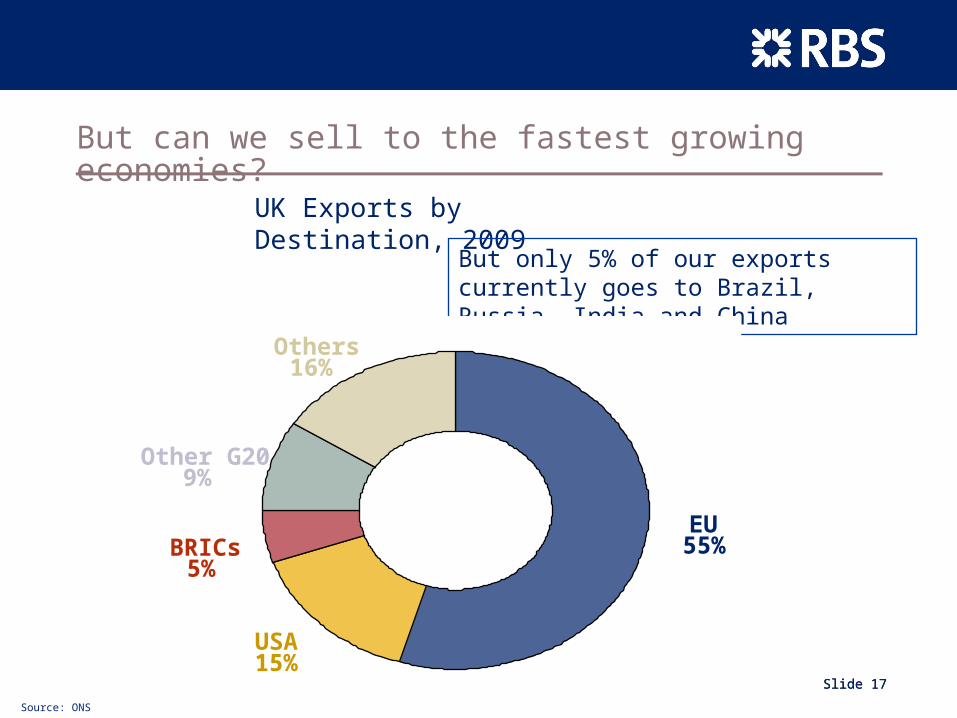

But can we sell to the fastest growing economies?

Slide 17

UK Exports by Destination, 2009

But only 5% of our exports currently goes to Brazil, Russia, India and China

EU55%

Others16%

USA15%

BRICs5%

Other G209%

Source: ONS

Slide 18

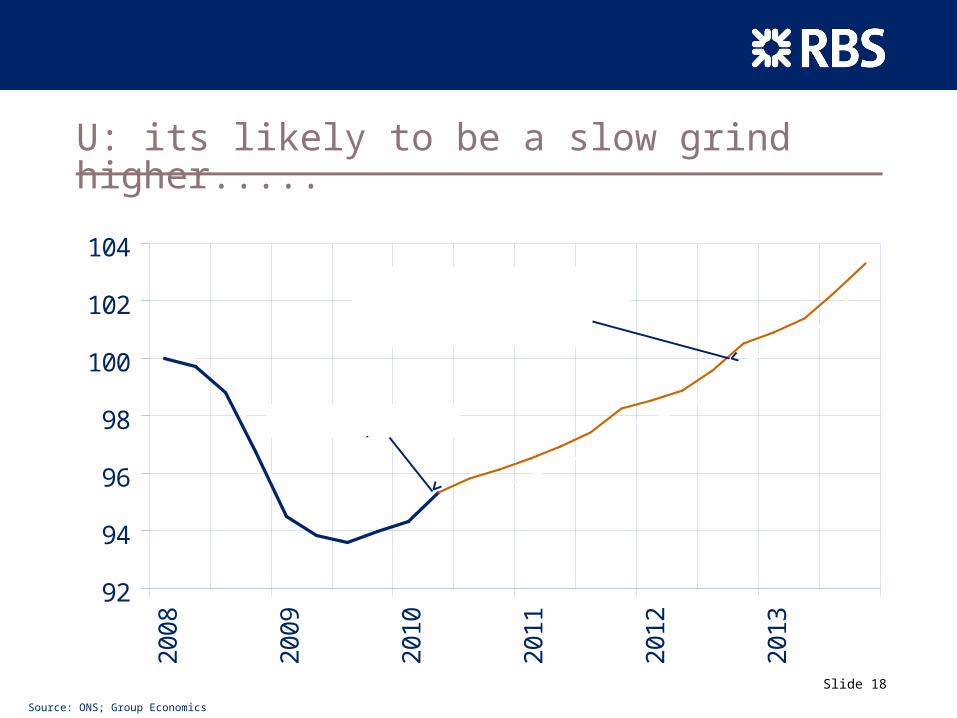

U: its likely to be a slow grind higher.....

92

94

96

98

100

102

104

20

08

20

09

20

10

20

11

20

12

20

13

UK Economic Output (Index Start of Recession Q1 2008 = 100)

Current position

3 Years to make up the ground we've lost

Source: ONS; Group Economics

Slide 19

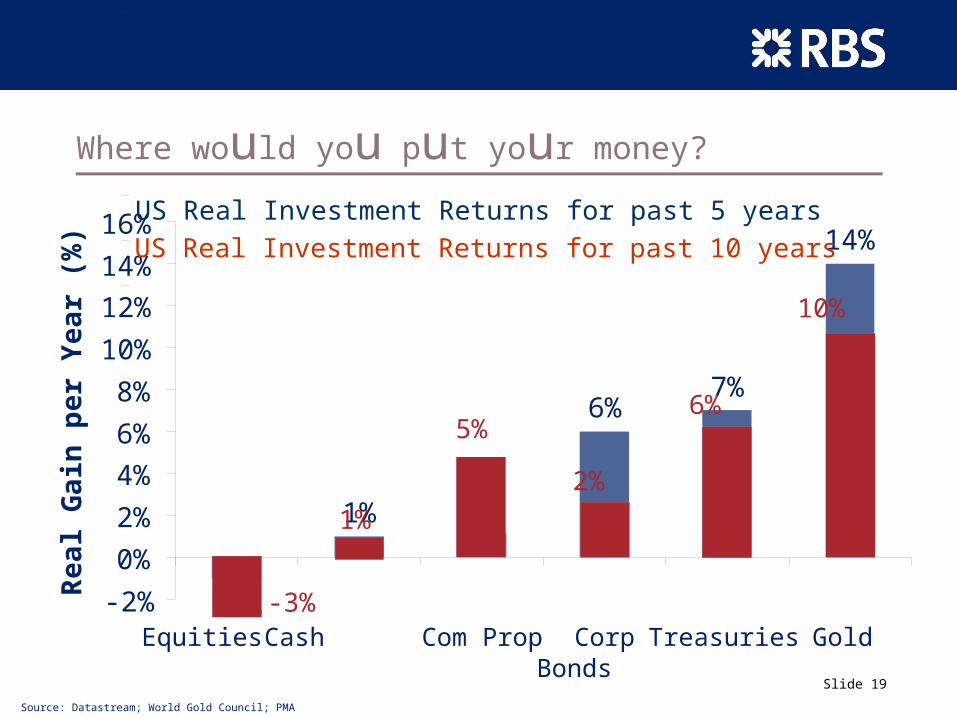

Where would you put your money?

-1%

1% 1%

6%7%

14%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Equities Cash Com Prop CorpBonds

Treasuries Gold

Rea

l G

ain

per

Yea

r (%

)

US Real Investment Returns for past 5 years

-3%

1%

5%

2%

6%

10%

US Real Investment Returns for past 10 years

Source: Datastream; World Gold Council; PMA

Slide 20

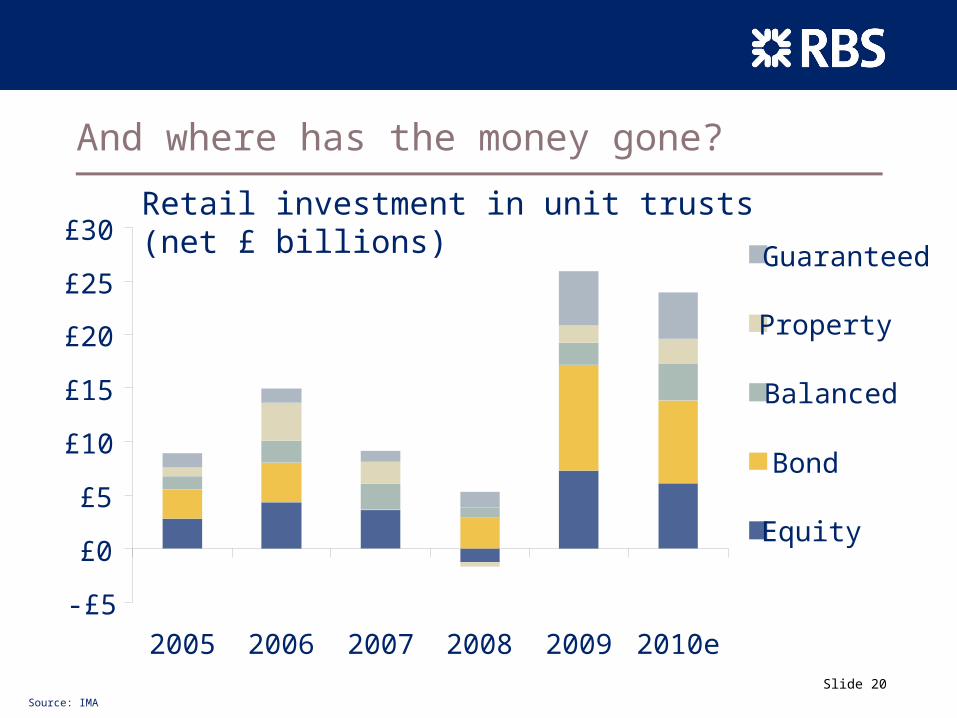

And where has the money gone?

Source: IMA

-£5

£0

£5

£10

£15

£20

£25

£30

2005 2006 2007 2008 2009 2010e

Guaranteed

Property

Balanced

Bond

Equity

Retail investment in unit trusts (net £ billions)

Slide 21

Thank You and Questions

Slide 22

Legal disclaimer

This material is published by The Royal Bank of Scotland plc (“RBS”) which is authorised and regulated by the Financial Services Authority for the conduct of regulated activities in the UK. It has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments, other financial instruments or related derivatives (“Securities”). It should not be reproduced or disclosed to any other person, without our prior consent.

This material is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

Whilst this information is believed to be reliable, it has not been independently verified by RBS and RBS makes no representation, express or implied, nor does it accept any responsibility or liability of any kind, with regard to the accuracy or completeness of this information. Unless otherwise stated, any views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the RBS Group’s Group Economics Department, as of the date of publication of this material and are subject to change without notice. Recipients of this material should make their own independent evaluation of this information and make such other investigations as they consider necessary (including obtaining independent financial advice), before acting in reliance on this information.

This material should not be regarded as providing any specific advice. RBS accepts no obligation to provide any advice or recommendations in respect of the information contained in this material and accepts no fiduciary duties to the recipient in relation to this information.

Slide 23

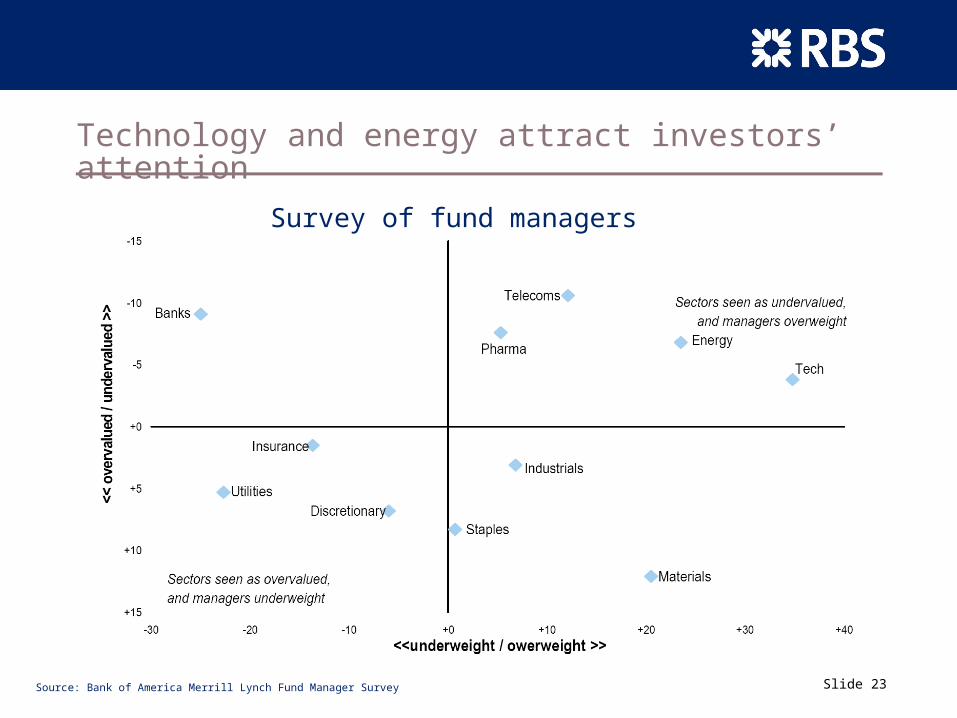

Technology and energy attract investors’ attention

Survey of fund managers

Source: Bank of America Merrill Lynch Fund Manager Survey