36

© 2016 LMC International. All rights reserved. www.lmc.co.uk Where are agricultural prices heading? AGIC, Melbourne July 2016

© 2016 LMC International. All rights reserved. www.lmc.co.uk

Whereareagriculturalpricesheading?AGIC,Melbourne

July2016

Agricultural prices went up from 2003-2013. Why?

Agricultural prices went down from 2013-16. Why?

What happens next?

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

From 2005, almost all crop prices moved to a much higher level than average, but they have come down since 2013.

Indexedworldpricesforvariousmajorcrops

3

0

30

60

90

120

150

180

210

2000 2002 2004 2006 2008 2010 2012 2014 2016

Inde

x: A

vera

ge p

rices

200

0-20

13 =

100

Corn/Maize Soybeans Rapeseed Wheat

Understandingtheriseandfallinprices

Whydidpricesrise?1.Weneededmuchmorefarmland

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

This is the change in the world’s arable area since 1980: no change at all from 1980 to 2002!

Changeinworldarableareavs.1980

6

-20

0

20

40

60

80

100

120

1981 1985 1989 1993 1997 2001 2005 2009 2013

Are

a ch

ange

(mill

ion

hect

ares

)

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

After 2002, the total world arable area changed dramatically.

Changeinworldarableareavs.1980

7

-20

0

20

40

60

80

100

120

1981 1985 1989 1993 1997 2001 2005 2009 2013

Are

a ch

ange

(mill

ion

hect

ares

)

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

If we split the total into oil and grain crops, another story emerges. To 2002, oil crop area was displacing grain crop area, leaving the total area largely unchanged.

Changeinoilandgraincropareasvs.1980

8

-100

-50

0

50

100

150

1982 1986 1990 1994 1998 2002 2006 2010 2014

Tota

l are

a ch

ange

sinc

e 19

81, m

illio

n ha

.

Change since 1981 for oil crops Change since 1981 for grain

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

After 2003, oil crops continued their previous upward trajectory, adding global area each year.

Changeinoilandgraincropareasvs.1980

9

-100

-50

0

50

100

150

1982 1986 1990 1994 1998 2002 2006 2010 2014

Tota

l are

a ch

ange

sinc

e 19

81, m

illio

n ha

.

Change since 1981 for oil crops Change since 1981 for grain

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

However, there was a profound change in direction of the world grain crop area around 2003. With both sectors expanding, total arable area exploded.

Changeinoilandgraincropareasvs.1980

10

-100

-50

0

50

100

150

1982 1986 1990 1994 1998 2002 2006 2010 2014

Tota

l are

a ch

ange

sinc

e 19

81, m

illio

n ha

.

Change since 1981 for oil crops Change since 1981 for grain

Whydidweneedsomuchmoreland?

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

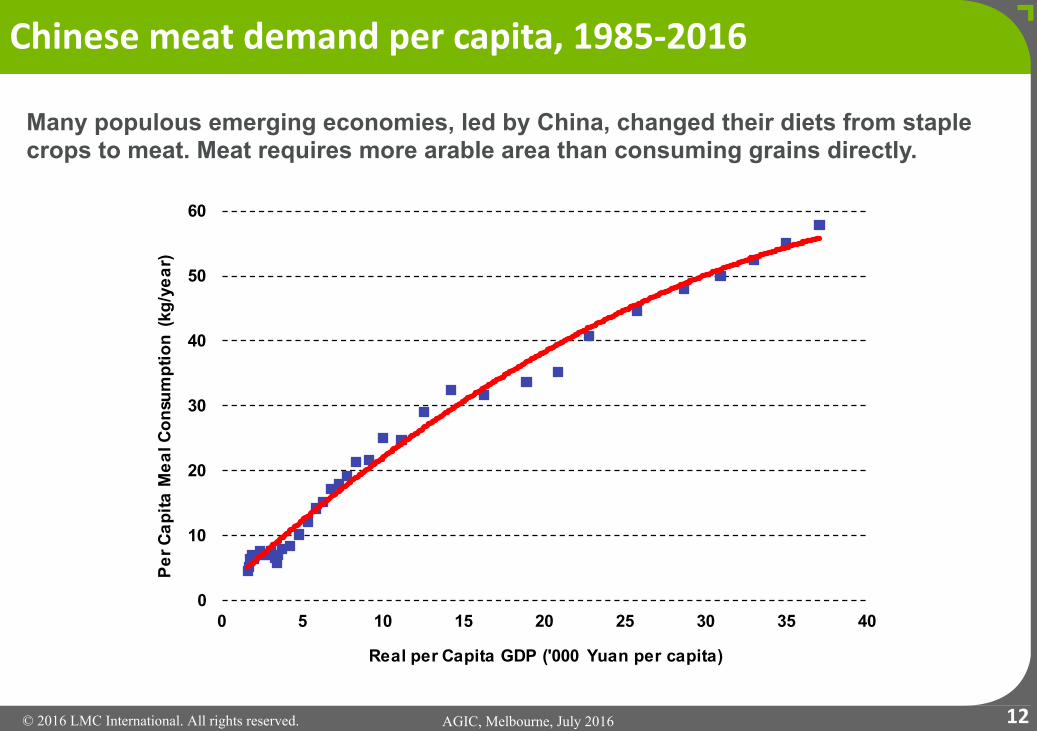

Many populous emerging economies, led by China, changed their diets from staple crops to meat. Meat requires more arable area than consuming grains directly.

Chinesemeatdemandpercapita,1985-2016

12

0

10

20

30

40

50

60

0 5 10 15 20 25 30 35 40

Per C

apita

Mea

l Con

sum

ptio

n (k

g/ye

ar)

Real per Capita GDP ('000 Yuan per capita)

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

For example, China was a major maize/corn exporter but became a large importer by 2010. Production could not keep pace with feed demand.

Chinesenetexportsofmaize(i.e.negativeisimports)

13

-6

-3

0

3

6

9

12

15

18

2000 2002 2004 2006 2008 2010 2012 2014

Net e

xpor

ts o

f cor

n, m

illio

n to

nnes

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

Since 2010, Chinese maize/corn imports have levelled out. This helps explain the market turnaround since 2012/3.

Chinesenetexportsofmaize(i.e.negativeisimports)

14

-6

-3

0

3

6

9

12

15

18

2000 2002 2004 2006 2008 2010 2012 2014

Net e

xpor

ts o

f cor

n, m

illio

n to

nnes

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

Another example: China now imports 60% of the world’s soybeans, almost all for animal feed.

Chinesesoybeanandrapeseedimports

15

0

10

20

30

40

50

60

70

80

90

2000 2002 2004 2006 2008 2010 2012 2014

Mill

ion

tonn

es o

f oils

eeds

Soybean Rapeseed

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

Which crops have increased their area most since 2000?

Totalchangeinworldareaofselectedcropssince2000

16

0 5 10 15 20 25 30 35 40

Corn

Soybean

Rice

Rapeseed

Oil Palm

Wheat

Sugarcane

Peanut

Million hectares

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

The dominant feed crops accounted for most of the world area expansion from 2000. But is it just for feed?

Totalchangeinworldareaofselectedcropssince2000

17

0 5 10 15 20 25 30 35 40

Corn

Soybean

Rice

Rapeseed

Oil Palm

Wheat

Sugarcane

Peanut

Million hectares

Whydidpricesrise?2.Wedecidedtoturnfoodintofuel

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

Nearly 20% of the world’s corn (maize) is now used for fuel.

Totalandnon-fueluseofcorn/maize

19

400

500

600

700

800

900

1,000

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010 2013

Mill

ion

tonn

es

Total Consumption Non-Fuel Consumption

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

Global food and non-food use of vegetable oils, 1980-2015

Totalandfooduseofvegetableoils

20

20

40

60

80

100

120

140

160

180

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010 2013

Mill

ion

tonn

es

Total Consumption Food Use Consumption

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

Food and feed demand for all major crops expanded faster in the 2000s than in the 1990s.

Changeindemandduringdecadeforallmajorcrops

21

0

20

40

60

80

100

120

140

160

180

Food Feed Fuel

Gro

wth

per

dec

ade,

mill

ion

tonn

es

1990s 2000s

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

But the most dramatic change was in fuel demand for crops, which added a vital third element to demand for crops in the 2000s.

Changeindemandduringdecadeforallmajorcrops

22

0

20

40

60

80

100

120

140

160

180

Food Feed Fuel

Gro

wth

per

dec

ade,

mill

ion

tonn

es

1990s 2000s

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

If we look at the annual % growth in demand by end-use category…

Annual%changeindemandforallcrops

23

0%

5%

10%

15%

20%

25%

Food Feed Fuel

Annu

al p

erce

ntag

e gr

owth

1990s 2000s 2010s

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

If we look at the annual % growth in demand by end-use category…the impact of the “biofuel decade” in the 2000s is clear.

Annual%changeindemandforallcrops

24

0%

5%

10%

15%

20%

25%

Food Feed Fuel

Annu

al p

erce

ntag

e gr

owth

1990s 2000s 2010s

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

If we look at the annual % growth in demand by end-use category…the impact of the “biofuel decade” in the 2000s is clear. This effect has now declined.

Annual%changeindemandforallcrops

25

0%

5%

10%

15%

20%

25%

Food Feed Fuel

Annu

al p

erce

ntag

e gr

owth

1990s 2000s 2010s

Theirrationaleconomicsofbiofuels

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

How much more do you want to pay for your fuel?

Pricesofmajorbiodieselfeedstocksvs.Brentcrudeoil

27

200

400

600

800

1,000

1,200

1,400

1,600

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

EU p

rices

, US

$ pe

r ton

ne

Brent Crude Soy oil Rapeseed oil Palm oil

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

Let’s revisit our opening diagram of indexed world arable crop prices, adding palm oil.

Indexedpricesofmajorcrops

28

0

30

60

90

120

150

180

210

Jan-00 Jul-01 Jan-03 Jul-04 Jan-06 Jul-07 Jan-09 Jul-10 Jan-12 Jul-13 Jan-15

Inde

x: A

vera

ge p

rices

200

0-20

13 =

100

Corn/Maize Soybeans RapeseedPalm Oil Wheat Brent Crude

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

Biofuels have tied almost all crop prices to the price of petroleum.

IndexedpricesofmajorcropsandBrentcrudeoil

29

0

30

60

90

120

150

180

210

Jan-00 Jul-01 Jan-03 Jul-04 Jan-06 Jul-07 Jan-09 Jul-10 Jan-12 Jul-13 Jan-15

Inde

x: A

vera

ge p

rices

200

0-20

13 =

100

Corn/Maize Soybeans RapeseedPalm Oil Wheat Brent Crude

Sowhydidcroppricesfallfrom2013?

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

We linked crop prices to energy prices, so when the price of petroleum falls, crop prices had to fall in line.

Brentcrudeoilprice

31

0

20

40

60

80

100

120

140

Jan-00 Jan-02 Jan-04 Jan-06 Jan-08 Jan-10 Jan-12 Jan-14 Jan-16

US$

per b

arre

l

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

The world developed enough new crop land to meet demand. The total additions are now levelling out.

Changeinareaofmajorcropsvs.2006

32

0

10

20

30

40

50

60

70

80

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Chan

ge in

are

a ha

rves

ted

sinc

e 20

05

Wheat Soybean Corn Rapeseed

Whathappensnext?

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

After the general exuberance of the biofuel decade, we may be entering a period like the 1990s, when the market was more selective about which crops it wanted to expand. Has the “protein decade” begun?

Soybeanareaas%ofcombinedsoybean/palmoilarea

34

85%

86%

87%

88%

89%

90%

91%

92%

93%

1961 1967 1973 1979 1985 1991 1997 2003 2009 2015

Soyb

ean

area

as

% o

f tot

al s

oy+

oil p

alm

are

a

© 2016 LMC International. All rights reserved. AGIC, Melbourne, July 2016

Singapore16 Collyer Quay #21-00

Singapore 049318Singapore

T +65 6818 9231

This presentation and its contents are to be held confidential by the client, and are not to be disclosed, in whole or in part, in any manner, to a third party without the prior written consent of LMC International.

While LMC has endeavoured to ensure the accuracy of the data, estimates and forecasts contained in this presentation, any decisions based on them (including those involving investment and planning) are at the client’s own risk.

LMC International can accept no liability regarding information analysis and forecasts contained in this presentation.

© LMC International, 2016All rights reserved

New York1841 Broadway

New York, NY 10023USA

T +1 (212) 586-2427F +1 (212) 397-4756

Oxford 4th Floor, Clarendon House

52 Cornmarket StreetOxford OX1 3HJ

UK

T +44 1865 791737F +44 1865 791739

Kuala LumpurB-03-19, Empire Soho

Empire SubangJalan SS16/1, SS1647500 Subang Jaya

Selangor Darul EhsanMalaysia

T +603 5611 9337

www.lmc.co.uk

Formoreinformation,pleasevisitwww.lmc.co.uk