Where is the Money in Payments? EPCA conference presentation March 25 th 2013 Brussels CONFIDENTIAL AND PROPRIETARY Any use of this material without specific permission of McKinsey & Company is strictly prohibited

Transcript

Where is the Money

in Payments?

EPCA conference presentation

March 25th 2013

Brussels

CONFIDENTIAL AND PROPRIETARY

Any use of this material without specific permission of McKinsey & Company is strictly prohibited

McKinsey & Company | 1

Contents

Real challenges to profitability

Levers for improvement

The importance of being

payments!

McKinsey & Company | 2

Globally, payments represent close to 1 trillion EUR in revenues,

out of which 25% are generated in Europe Global banking revenues, %, 2011

100% = EUR 3,100 billion

70

Other banking

revenues

Payments

& accounts

30

Retail accounts

Corporate accounts

Credit card issuing

Card acquiring

E-purse/prepaid

34

35

25

5 1

North

America

Europe

APAC

LatAm

Other

25

25

33

15

2

100% = EUR 930 billion

Pre-tax profits margin 20-25% (equivalent to

EUR 180-230 billion operating result)

McKinsey & Company | 3

Despite a drop during the crisis, European payments revenues have

proven resilient and importance for banks should increase

128

11495

106 99 101 106112

120

14

237

13

227

126

12

131 124

11

234

+5%

223

-5%

2016

267

146

15

250

137 129

10

217

122

09

237

123

2008

270

142

35%

Share of

banking

revenue

30%

Retail payments Corporate payments

33%

European1 payments revenues, EUR billions

McKinsey & Company | 4

79.6

234.4

26.0

25.715.2

Profits Cash/

Check

-40.6

CT/DD

-9.7

Debit

-6.8

Credit

cards

-23.8

Maint.

-64.7

Risk

-9.2

Reve-

nue

Inter-

est

119.8

Fees Credit

cards

35.4

Debit

12.2

CT/DD Cash/

Check

Key contributors

Europe generates 80 bn EUR in payment profits,

mostly through interest revenues on accounts Europe, EUR billions, 2011

Revenues Costs

Transactions Accounts Credit

cards

Accounts Credit

cards

Transactions

McKinsey & Company | 5

UK

TU

CH SE

ES

PT

PL

NO

NL

IT

IE

HU

EL

DE

FR

FI

ET

DK CZ

BU BE

AT

Ch

eq

ue

Ele

ctr

on

ic

Card transaction per capita 39 Finland Norway 42 Sweden 50 France 50 Denmark 51 Netherlands 52 Belgium 54 UK 57 Austria 64 Estonia 65 Switzerland 66 Germany 69 Ireland 75 Portugal 78 Spain 80 Hungary 88 Czech Rep. 88 Italy 89 Poland 90 Turkey 94 Greece 97 Bulgaria 98

Cash’s share of total transactions

Percent

Electronic share of non-cash transactions

Percent, transactions per capita

Users display very different payment behavior…

Card & cheque

Full

electronic

Cash & paper

Cash & electronic

McKinsey & Company | 6

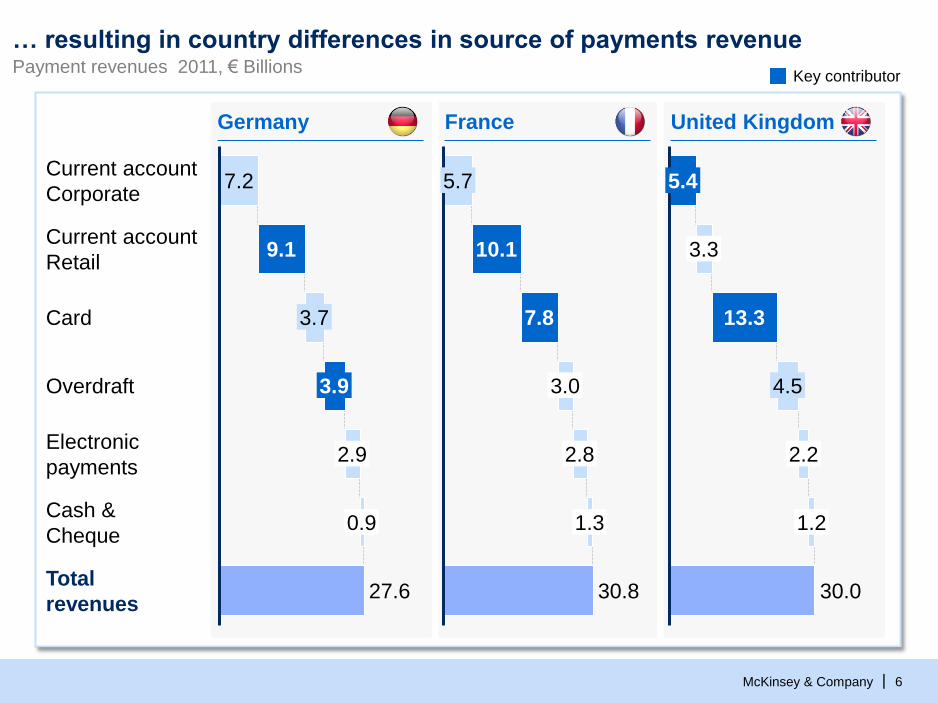

France United Kingdom

Total

revenues 27.6

Cash &

Cheque 0.9

Electronic

payments 2.9

Overdraft 3.9

Card 3.7

Current account

Retail 9.1

Current account

Corporate 7.2

3.0

7.8

10.1

5.7

30.8

1.3

2.8

30.0

1.2

2.2

4.5

13.3

3.3

5.4

… resulting in country differences in source of payments revenue

Key contributor

Germany

Payment revenues 2011, € Billions

McKinsey & Company | 7

Users are also being charged in different ways

8

2

10

8

12

13

13

11

14

12

28

64

4

4

12

3

2

1

2

1

1

1

1

1

0

0

0

74 12

27

Poland 58 16 ~22

Italy 68 20

UK 68 7

Switzerland 70 21 ~8

Sweden 71 15

Austria 71 16

Belgium 72 20

France 75 12

Netherlands 75 23

Russia

Denmark

6

Spain 31 39

Norway 55

30

~25

Portugal 56 31

Germany 58

18

Net interest income

Maintenance fees

Transactional fees

Incident fees

Retail payments revenue, percent, 2011

McKinsey & Company | 8

Level of profitability is also highly differentiated

![INDUSTRY REPORT Payments: Star Of The FinTech World · sharespost.com Payments: Star Of The FinTech World | 6 Exhibit 3: Payments is a $110 Trillion opportunity [3] PAYMENT MARKET](https://static.documents.pub/doc/80x56/5ec44513b7e51a165221e8ca/industry-report-payments-star-of-the-fintech-world-sharespostcom-payments-star.jpg)