Who Benefits from Inconsistent Multinational Tax Transfer-Pricing Rules?* ANJA DE WAEGENAERE, Tilhurg University RICHARD C. SANSING, Dartmouth College and Tilburg University JACCO L. WIELHOUWER, Tilburg University Abstract This paper uses a strategic tax compliance model to examine taxpayer reporting and tax authority audit strategies in an international setting with two tax authorities. The setting inconsistent tax transfer-pricing rules. The latter creates the possibility of each country trying to tax the same income. We study the effect of the probability of transfer-price rule inconsis- tency on the strategies and payoffs of the taxpayer and the tax authorities. We find that an increase in the probability of transfer-price rule inconsistency induces more aggressive auditing by governments. It therefore deters taxpayers from shifting income to the country with the lower tax rate in situations in which the transfer-pricing rules are consistent, and can either increase or decrease the income reported to the low-tax-rate country in cases in which the transfer-pricing rules are inconsistent. We find that an increase in transfer-price rule inconsistency could either increase or decrease the taxpayer's exp)ected tax liability and could either increase or decrease the deadweight loss from auditing. Our results call into question the conventional wisdom that the prospect of double taxation due to transfer-price rule inconsistency increases a firm's expected tax liability and governments' expected audit costs. Keywords Double taxation; Tax compliance; Tax law inconsistency; Transfer pricing JE L Descriptors H26. K42 Accepted by Ken Klassen. An earlier version of paper was p resented at the 2(X) 4 Contemporary Accounting Research Accountants and Ordre des complables agrees du Quebec. We thank Jon Davis, John Hand.

RICHARD C. SANSING, Dartmouth College and Tilburg University

JACCO L. WIELHOUWE R, Tilburg University

Abstract

This paper uses a strategic tax compliance model to examine taxpayer reporting and tax

authority audit strategies in an international setting with two tax authorities. The setting

features both information asymmetry between the taxpayer and the tax authorities and

inconsistent tax transfer-pricing rules. The latter creates the possibility of each country trying

to tax the same income. We study the effect of the probability of transfer-price rule inconsis-

tency on the strategies and payoffs of the taxpayer and the tax authorities. We find that an

increase in the probability of transfer-price rule inconsistency induces more aggressive

auditing by governments. It therefore deters taxpayers from shifting income to the country

with the lower tax rate in situations in which the transfer-pricing rules are consistent, andcan either increase or decrease the income reported to the low-tax-rate country in cases in

which the transfer-pricing rules are inconsistent. We find that an increase in transfer-price

rule inconsistency could either increase or decrease the taxp ayer 's exp)ected tax liability and

could either increase or decrease the deadweight loss from auditing. Our results call into

question the conventional wisdom that the prospect of double taxation due to transfer-price

rule inconsistency increases a firm's expected tax liability and governments' expected audit

costs.

K ey w ord s Double taxation; Tax com pliance; Tax law inconsistency; Transfer pricing

Qui beneficie de Tincoherence des regies fiscales multinationales

sur les prix de transfert ?

Condense

Les atJteurs se penchent sur la question de la double imposition d'une society m ultinationaleen eiaborant et en analysant un modele d'obiigations fiscales ititemationales. Le benefice

realise par une societe multinationale peut faire Tobjet d'une double imposition si plusieurs

iidministrations fiscales affimient leur droil de lever un impot sur ce benefice. Le cas se produit

notamment lorsque ies gouvernements appliquent des regies sur les prix de transfert qui

sont differente.s en ce qui a trait a la repartilion du benefice entre les pays.

Pour Illustrer les questions etudiees dans leur modele, les auteurs proposent un exemple

representatif de I'enjeu monetaire eteve des litiges en matiere de prix de transfert, puisque

cet exemple met en cause des actifs incorporels appartenant a une societe multinationalerentable. Une societe mere exer9ant ses activites dans un pays possede une liliale qui exerce

les siennes dans un autre pays. La filiale fabrique et vend un produit qui genere un proHt de

30 dollars. La tiliale utilise un bien incorporel apparlenant a la societe mere dans la fabrication

et (ou) la vente de soti produit. Elle doit verser une redevance a la societe mere afin de remu-

nerer cette demiere pour Futilisation dudit bien. Si cette redevance s'eieve a 10 dollars, la

societe mere paiera Timpot sur 10 dollars de benefice et la filiale paiera Timpot sur 20 dollars

de benefice ; si la redevance s'eieve a 20 dollars, la societe mere paiera Timpot sur 20 dollars de

benefice et la filiale paiera I'impot sur tO dollars de benefice. Les societ^s peuvent done

choisir le montant de la redevance. mais il leur faut declarer le benefice imposable corres-

pondant a ce choix. Ainsi s'assure-t-on que le benefice imposable total dont Ia societe fait

6tal dans les deux pays est egal au profit resultant de I'operation.

Reste a savoir si Taccord relatif a la redevance sera accepte par les deux pays, aux fins

fiscales. Les operations entre apparentes preoccupent tout particulierement les administra-

tions fiscales parce qu'elles peuvent etre utilisees pour transferer des benefices vers ie pays

ayant Ie taux d'impo sition le plus faible. D ans le modele des auteu rs. Ies deux pays adherent

au « principe de pleine concurrence » en ce qui a trait a la determination des prix de transfert

par les apparentes. En vertu de ce principe, le montant de la redevance que verse la filiale a

la societe m ere doit correspondre h la somme que paierait une partie non apparentee concluant

une operation comparable dans des circonstances analogues. L'application de ce principe

peut s'operer selon differentes methodes, notamment la methode du prix de marche com-

parable, la methode des profits comparables et la methode du partage des profits. En outre,

le mode d'application de ces methodes depend, dans une certaine mesure, des operations

entre parties non apparentees qui sont jugees comparables aux operations entre apparentes.

Si les deux pays, compte tenu de ces diverses methodes. derivent la meme redevance dans des

conditions nonnales de concurrence, les regies sur les prix de transfert sont jugees coherentes.Si les deux pays derivent des redevances differentes, les regies sur les prix de transfert sont

Inco nsisten t M ultinatio nal Tax Tran sfer-Pricing Ru les 105

d'imposition ; ou les regies sur les prix de transfert sont incoherentes. La societe observe

privement la situation et declare le benefice faisant l'objet du litige soit dans le pays qui

applique le faible taux d'imposition, soit dans le pays qui applique le taux d'imposition

eleve. Les pays connaissent uniquement la distribution de probabilites des differents etats,

Les auteurs definissent les six equilibres auxquels peut donner lieu le modele. En general,les equilibres I et V correspondent au « comportement declaratif audacieux » selon lequel la

societe procede au partage du benefice en declarant parfois le benefice dans le pays ayant le

faible taux d'imposition alors que ledit benefice est indeniablement imposable dans le pays

ayant le taux d'imposition eleve (c'est-a-dire que les regies sur les prix de transfert sont

coherentes et favorables au pays ayant le taux d'imposition eleve). Les equilibres IV et VI

correspondent au « comportement de controle audacieux », selon lequel le pays ayant le faible

taux d'imposition et le pays ayant le taux d'imposition eleve procedent tous deux a un con-

trole, dans leur effort pour tirer des recettes de la double imposition. Les equilibres II et IUsont des cas intermediaires dans lesquels la societe ne se livre pas au transfert des benefices

et le pays ayant le faible taux d'impo sition ne controle aucune declaration.

Apres avoir defini ces equitibres, les auteurs examinent les repercussions de changem ents

dans la probabilite d'incoherence des regies relatives aux prix de transfert sur la strategie

declarative de la societe et les strategies de controle du pays ayant un faible taux d'imposition

et du pays ayant un taux d'imposition eleve. Les auteurs constatent qu'une augmentation de

la probabilite d'incoherence des regies sur tes prix de transfert pousse les administrations

fiscales a adopter un comportement de controle plus audacieux qui, en retour, incite lessocietes a se livrer moins volontiers au transfert de benefices lorsque les regies sur les prix

de transfert sont coherentes. Cette augmentation peut egalement soit hausser soit reduire la

probabilite que le contribuable declare des benefices au pays ayant le faible taux d'imposition

lorsque les regies sur tes prix de transferi sont incoherentes.

Les auteurs se demandent ensuite comment un changement dans rincoherence des

regies sur les prix de transfert influe sur les obligations fiscales prevues de la soci6te. Ils

constatent qu'une diminution de I'incoherence peut soit augmenter soit reduire ces obligations

fiscales. En effet, une probabiiite plus elevee d'incoherence des regies sur les prix de transfertbeneficiera a la soci^te si la probabilite qu'un pays impose un benefice deja impose par

I'autre pays est suffisamment faible, Cette situation est hautem ent probable dans les cas ou

l'ecan entre les taux d'imposition des deux pays est important.

Enrtn, les auteurs se demandent si les couts du controle augmenteront ou diminueront

si la probabilite d'incoherence des regies sur les prix de transfert diminue. Encore une fois,

les deux situations sont possibles. Meme si I'un ou I'autre pays adopte un comportement de

controle moins audacieux devant une declaration dtSfavorable, les couts pr6vus du controle

peuvent soit augmenter soit diminuer, etant donne qu'une diminution de I'incoherence des

regies sur les prix de transfert peut pousser la societe a un comportement declaratif plus ou

Deuxi^mement, une augmentation de Tincoherence des regies sur les prix de transfert peu

soit augmen ter soit diminuer le poids des pe rtes associ6es aux coflts de controle. Les au teur

definissent les cas dans lesquels la diminution de rincoherence des regies sur les prix d

transfert peut a la fois reduire les recettes fiscales des gouvem em ents et augm enter les cout

de controle prevus. Dans ces situations, les gouvemements n'ont pas interet a coordonnetrop rigoureusement leurs regies sur les prix de transfert et leurs pratiques en cette matiere

Les resuitats obtenus par les auteurs reniettent en question I'idee precon^ue selon laquelle l

perspective d'une double imposition attribuable a Tincoherence des regies sur les prix de

transfert est favorable aux gouvemements. defavorable aux contribuables et socialemen

inefficace. Une politique gouvemem entaie visant a augmen ter rinco here nce des regies su

les prix de transfert n'est ni clairement avantageuse ni indiscutablement desavantageuse

pHJur les societds ou les gouvemements.

1. Introduction

In this paper we examine the issue of double taxation of a multinational enterprise

by developing and analyzing a model of international tax compliance. Income

earned by a multinational enterprise can be subject to double taxation if multiple

tax authorities assert the right to tax the income. In particular, double taxation

arises to the extent that governments use different transfer-pricing rules to allocate

income between countries. In the 1997, 1999, and 2001 Ernst & Young Transfer

Pricing Global Surveys, over 80 percent of multinationals identified "double taxrelief" as an important intemational tax issue because transfer-pricing adjustments

typically result in double taxation (Ackerman and Hobster 2001).

Mechanisms such as mutual agreement procedures (MAPs) exist to make it

possible for a taxpayer to get relief from double taxation. However, in practice the

MAP system often fails to provide such relief because governments are not required

to resolve the conflict in a manner that eliminates double taxation (Mortier 2002).

The failure of the MAP system to provide relief from double taxation has led to a

demand for alternative means of resolving disputes, such as advance pricing agree-

ments (Ring 2000) and arbitration (Morgan 2003 ).

The standard tax compliance model treats the interaction between the taxpayer

and the tax authority as a game between a wealth-maximizing taxpayer and a tax

authority trying to max imize government revenues net of audit costs (Graetz, Rein-

ganum , and Wilde 1986; Reinganum and Wilde 1986; Beck and Jung 1989; Sansing

1993; Rhoades 1997, 1999; Mills and Sansing 2000; Feltham and Paquette 2002).

In the standard model, the taxpayer privately observes its income and submits a

report to the tax authority. The model in this paper considers a multinational whose

worldwide income is common knowledge, but the division of income between the

These differences can result in both tax authorities trying to tax the same income

(double taxation). The possibility of transfer-price rule inconsistency in turn affects

the reporting and auditing strategies of tbe taxpayer and the two tax authorities.

To illustrate tbe issues that we examine in the model, we offer the following

example that is representative of high-dollar transfer-pricing disputes in that itinvolves intangible assets owned by a very profitable multinational enterprise (Sul-

livan 2004). A parent corporation operating in one country owns a subsidiary

operating in another country. The subsidiary produces and sells a product generat-

ing a profit of $30. The subsidiary uses intangible property owned by the parent in

its production and/or sales process. The subsidiary must pay a royalty to the parent

to compensate the parent for the subsidiary's use of the intangible property. If the

subsidiary pays a royalty of $10, then the parent pays tax on $ 10 of income and the

subsidiary pays tax on $20 of income; if the subsidiary pays a royalty of $20, thenthe parent pays tax on $20 of income and the subsidiary pays tax on $10 of

income. We emphasize that the royalty payment is an actual transaction between

two distinct legal entities (a parent and its subs idiary), and that both report the roy-

alty truthfully on their respective tax re tum s.' In other w ords, we allow the firms to

choose the royalty, but require them to report taxable income in a way that is con-

sistent with that choice. This ensures that the aggregate taxable income that the

firm reports to the two countries is equal to the profit from the transaction.

The issue is whether the royalty arrangement will be accepted by the countriesfor tax purposes. Transactions between related parties are of particular concem to

tax authorities because they can be used to shift income to the jurisdiction with the

lower tax rate. Both countries adhere to the "arm's-length standard" when deter-

mining transfer prices used by related parties in our model. Under the arm's-length

standard, the amount of the royalty that the subsidiary pays to the parent should be

the amount that an unrelated party engaging in a comparable transaction under

comparable circumstances would pay. There are various methods that can be used

when applying this principle in practice, including the comparable uncontrolledtransaction method, the comparable profits method, and the profit-split method.

Furthermore, how these methods are applied in practice depends in part on which

transactions between unrelated parties are considered to be comparable to the

related-party transaction. If, when faced with these various methods, the two coun-

tries would derive the same arm's-length royalty, we consider the transfer-pricing

rules to be consistent. If the two countries would derive different royalties, we con-

sider the transfer-pricing rules to be inconsistent. We emphasize that because both

countries claim to adhere to the arm's-length standard, double taxation arises due

to the inconsistency of how the transfer-pricing rules will be applied in practice.

from the transaction, hui cannot cause aggregate taxable income to be less tha

worldwide economic incom e. This asymmetry in outcomes reflects the asym metr

position of the taxpayer and the tax authorities. The tax authorities can argue tha

the form of the transaction (in this case, the royalty paid by the subsidiary) can b

ignored for tax purposes if it diverges from the substance of the transaction adetermined under the arm's-length standard. The taxpayer, in contrast, having chose

the form of the transaction, must accept the tax consequences of that choice (se

Com missioner v. National Alfalfa D ehydrating).'^ A consequence of this asym

metry is that aggregate taxable income (after audit) from the transaction ca

exceed worldwide economic income from the transaction, but cannot be less.

Our analysis proceeds in two stages. In the first stage, we take the probabilit

of transfer-price rule inconsistency as exogenously fixed, and derive the equilibriut

reporting strategy of the firm and audit strategies of the two countries. We find thaan increase in the probability of transfer-price rule inconsistency induces the ta

authotity to adopt a more aggressive audit strategy. This increase in aggressivenes

in turn induces the firm to engage in less income shifting when the transfer-pricin

rules are consistent. A more aggressive audit strategy can also either increase o

decrease the probability that the taxpayer will report income to the low-tax-rat

country when the transfer-pricing rules are inconsistent.

In the second stage, we view the probability of transfer-price rule inconsistenc

as being influenced by both governments. Governments can decrease transfer-pricrule inconsistency by increasing the extent to which they coordinate their transfer

pricing rules and practices (through regulations, treaties, or informal agreements)

First, we ask how a change in transfer-ptice rule inconsistency affects the firm'

expected tax liability. We find that a decrease in inconsistency could either increas

or decrease the firm 's expected tax liability. The firm benefits from a higher probab il

ity of transfer-price rule inconsistency if the probability that a country successfull

taxes incom e that is already taxed by the other country is sufficiently low. This out

come is most likely to occur in settings in which there is a large difference in ta

rates between the two countries.

Second, we ask whether audit costs will increase or decrease if the probability

of transfer-price rule inconsistency is decreased. Again, either outcome is possible

Audit costs can either increase or decrease because a decrease in transfer-price rul

inconsistency can either induce more or less aggressive tax reporting by the firm

In cases in which an increase in transfer-price rule inconsistency would increas

expected tax revenues and decrease expected audit costs, a certain minimum leve

of transfer-price rule inconsistency is beneficial to governments.'*

We emphasize that our analysis of the effects of a change in the probability o

Sections 2 to 4 treat the probability of transfer-price rule inconsistency as

being exogenously fixed. Section 2 describes the model; section 3 characterizes the

equilibrium behaviors of the taxpayer and the two tax aulhorities; and section 4

examines the effects of transfer-price rule inconsistency on the players' strategies.

In section 5 we ask whether a change in the probability of transfer-price ruleinconsistency would increase or decrease the firm's expected tax liability and the

deadweight loss associated with auditing. Section 6 concludes.

2. Model

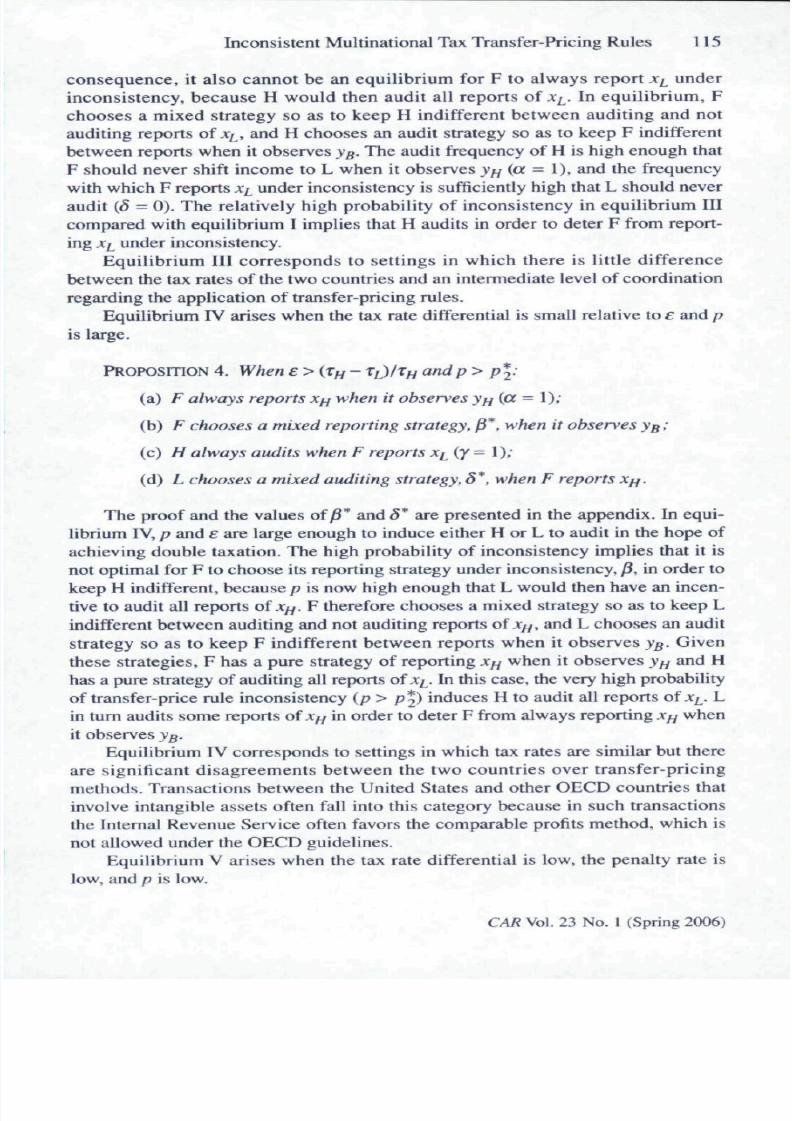

This section describes the game, the players' strategies, and the possible payoffs.

Summary ofthe game

A firm (F) has worldwide income equal to z that must either be taxed by country Lat the rate T^ or by country H at the rate T//, T/ / > z^ . Part of this income is under

dispute with respect to which country has the right to tax the income. Without loss

of generality, we normalize the disputed part to be equal to one. F privately

observes the state of nature _y^, >7y, or y^. State _v means that if either country

audits, both countries will agree that the income under dispute should be taxed by

country L. State >// means that if either country audits, both countries will agree

that the income under dispute should be taxed by country H. State yg means that

hoth countries would claim the right to tax the income. The probabilities of thethree states are (I -p)/2,{l - p ) / 2 , and/ j , respectively, 0 < p < I. We view the

parameter/? as being jointly determined by the transfer-pricing rules and practices

of country H and country L . In sections 3 and 4 of the paper, we treat p as an exogen-

ous parameter; in section 5, we consider the effects of a change in p on the firm's

expected tax liability and the probability that the firm is audited.

After observing the state _y,, F reports its income to country L (ri) and country

H ( r^ ) , rfj + ri = z. We require F to report aggregate taxable income of z because

worldwide income is known, and we assume that the penalty for filing reports thatare inconsistent with what is common knowledge is sufficiently high to deter F

from doing so. Eor example, F can increase r^ and decrease r^ hy varying a royalty

paym ent between affiliates operating in H and L, but must file reports that are con-

sistent w ith the royalty that is paid.

If F reports the disputed income to country L (H), we refer to the reports as

^L (^//)- After observing the reports, country L (H) can audit the reports. Auditing

allows the tax authorities in countries L and H to observe the state. If the state is y^

and the report is x^j, country L collects a tax and penalty of T/ (1 +;r) if an audit

occu rs. Similarly, if the state is y^ and the report is x^, country H collects a tax and

applied in an inconsistent manner hy the two governm ents, we assume that the tax-

payer does not pay a penalty when the state is _vg because although the government

has prevailed, the taxpayer's interpretation ofthe arm's-length standard was not an

unreasonable one. Double taxation occurs because the other country would not

refund the taxes already paid, because both countries claim the right to tax theincome. While the probability of douhle taxation is affected by both p and £, the

two parameters are conceptually distinct. The parameter p is the probability that

the governments apply the arm's-length standard in ways that result in both coun-

tries claiming the right to tax the income under dispute, assuming that the report is

audited. The param ete rs is the probability that the government would prevail in liti-

gation against the firm.

Auditing is costly. The audit cost incurred by country H (L) is kf^ (ki). We

assume that i^ <ETi,k^ <£'^H^ a"* ^H < [^// +? r)]/ 2, which ensure that the costof auditing is sufficiently low that the threat to audit is credible. The game tree is

presented in Figure 1. The payoffs to the players given the state, report, and aud it

is sufficiently low. In equ ilibria I and V, the firm engages in incom e shifting by

sometimes reporting income to L when the income is unambiguously taxable to H.

Equilibria IV and VI are ""aggressive auditing" equilibria that ari.se when both p

an de are sufficiently high. In equilibria IV and VI, both L and H engage in audit-

ing in an effort to generate revenue from double taxation. Equilibria II and III areintermediate cases in which F does not engage in income shifting and L does not

audit any reports.

Next, we formally characterize the six equilibria that can arise in our model.

Which equilibrium arises depends on the value of/? and the value off. The equilibria

are distinguished by two values off— (r^y - T i) /r // and K + (r,/ - r^)/r// — and

three values of p —

~x k

Fig ure 2 Equilibria regions when Xff = 40%, T^ = 20%. K = 30%, kf^ - it^ = 0.0 5, and

The value p* is the value of/? for which H would be indifferent between auditing

and not auditing reports of x ^ if the firm would never shift income to L when there

is no inconsistency, and would always report .\[^ in case of inconsistency. The value

/;* (/?*) is the value of/J for which neither country is willing to adopt a pure strategy

of never auditing if (T,f - t[)/Tf^ <e<jr+ [{Xf/ - Xi)lxij \ (resp. £ > ff + (T// - W/TH)

The assumptions we have made ensure that 0 </?*</?*< I and 0 < /?* < /J2 ^ I.

Equilibrium I arises when p is lower than p* and the tax rate differential and/or

the penalty rate is sufficiently large.

PROPOSITION I. When e<7r+(Xf^-^OI'^H " « ^ P ^ P*'

(a) F chooses a mixed reporting strategy a* when it observes y^f ;

(b) F always reports .v when it observes yg {(i = 0),

(c) H chooses a mixed auditing strategy y* when F reports .v ;

(d) L never audits when F reports Xf^ (6- 0).

The proof and the values of a* and / are presented in the appendix. In equi-

librium I, there is no pure strategy equilibrium with respect to the strategies a and

7. The relatively low value of p implies that if F reports J :^ whenever V// occurs

(a = 1). H should never audit (y - 0); but if H never audits, F should always shift itsincome to L (a - 0). On the other hand, the cost of an audit for H is sufficiently

low that, if F always shifts its income to L under V// (a = 0), then H should always

audit (y = 1). Therefore, the only equilibrium is for F to choose a mixed reporting

strategy, a*, so as to keep H indifferent between auditing and not auditing reports

of .V/ , and for H to choose a mixed audit strategy, y", so as to keep F indifferent

between reports when it observes yff. The resulting audit frequency by H is low

enough that it is optimal for F Io always report .v^ under inconsistency (j3 ^ 0).

Consequently, L should never audit {S 0). The low probability of inconsistency

causes H's audit strategy to be driven by its desire to deter F from engaging in

income shifting when v// occurs.

In general, equilibrium I corresponds to settings where the level of coordina-

tion between governments regarding the application of their transfer-pricing rules

is very high because p < p*. For example, we would expect equilibrium I to arise

in transactions involving countries that both adhere to the Organisation for Economic

Co-operation and Development's (OECD's) transfer-pricing guidelines and have a

well-functioning competent authority process that reduces the probability that the

two countries will try to impose different transfer prices on the same transaction.

consequence, it also cannot be an equilibrium for F to always report x^ under

inconsistency, because H would then audit all reports of xi^. In equilibrium, F

choose s a mixed strategy so as to keep H indifferent between auditing and not

auditing reports of A ^ , and H chooses an audit strategy so as to keep F indifferent

between reports when it observes yg. The audit frequency of H is high enough thatF should never shift income to L when it observes j ^ ^ (a = 1), and the frequency

with w hich F reports .v^ under inconsistency is sufficiently high that L should never

audit (5 = 0). The relatively high probability of inconsistency in equilibrium III

compared with equilibrium I implies that H audits in order to deter F from report-

ing Xf^ under inconsistency.

Equilibrium III corresponds to settings in which there is little difference

between the tax rates of the two countries and an intermediate level of coordination

regarding the application of transfer-pricing rules.Equilibrium IV arises when the tax rate differential is small relative to e an d p

is large.

PROPOSITION 4. When £ > (T// - Xi)/rff andp > p^:

(a) F always reports Xff when it observes yff (a = I );

(b) F chooses a mixed reporting strategy, P*. when it observes yg;

(c) H always audits when F reports xi{Y=^). '

(d) L chooses a mixed auditing strategy, S*, when F reports Xff.

The proof and the values of )8* and S* are presented in the appendix. In equi-

librium IV, p and £ are large enough to induce either H or L to audit in the hope of

achieving double taxation. The high probability of inconsistency implies that it is

not optimal for F to choose its reporting strategy under inconsistency, j8, in order to

keep H indifferent, because p is now high enough that L would then have an incen-tive to audit all reports of J : ^ . F therefore chooses a mixed strategy so as to keep L

indifferent between auditing and not auditing repOTts of Xff, and L chooses an audit

strategy so as to keep F indifferent between reports when it observes yg. Given

these strategies, F has a pure strategy of reporting Xff when it observes y^f and H

has a pure strategy of auditing all reports of .v^. In this case, the very high probability

of transfer-price rule inconsistency {p > / J*) induces H to audit all reports of Xf . L

in turn audits some reports of Xff in order to deter F from always reporting Xffwhen

it observes yg.

Equilibrium IV corresponds to settings in which tax rates are similar but there

that an increase in p weakly increases the probability that a report will be audited,

weakly decreases the probability that F will engage in income shifting, and has

countervailing effects on F's reporting strategy when the transfer-pricing rules are

inconsistent. The analyses in this and the next section assume that the change in p

affects neither the worldwide income (z) nor the amount of income under dispute(normalized to one).

There are three cases to consider. First, we consider the case in which (T// - T^)/r;/

> £, which we denote the high tax rate differential case. Second, w e consider the

effects in the case of low tax rate ditterential and high penalty — that is, (i/y - Ti^ )IT^

<E<K + {x^-Xi )lTyf. Third, we conside r the case of a low tax rate differential and

low penalty — that is. £ > ;i: -i- (T// - Xi)lTff.

High tax rate differential

First, consider how th e firm and the governments behave when / ; - 0 . A t that point.

'

p . th e firm's strategy under transfer-price rule inconsistency, is irrelevant because

when p = 0 . yg never occurs . W hen /) = 0, there is no transfer-price rule inconsistency

and there is n o conflict of interest between th e firm (F) and the low-tax-rate country(L ) . F 's only incentive t o misreport is to shift income thai should b e taxed by the

high-tax-rate cou ntry (H ) to L . Therefo re. L always collects the tax that it is due when

yi^ occurs and sometimes collects taxes when y^f occurs. H and F engage in a mixed

strategy equilibrium in which F makes H indifferent between auditing and not audit-

ing reports of A ^ ^ ; H tnakes F indifferent between reporting .v ^ an d .v/y when V/y occurs.

As p increases, F decreases th e frequency with which it shifts income away

from H ( a * increases) so as to keep H indifferent between auditing and n o t audit-

ing reports of x^ (eq uilibrium I). This continues until p reaches the critical value

p * . A t this point, F needs to always report Xf^ if j / y occurs in order to keep H indif-

When the critical level is crossed {p > p*), the probability of transfer-price

rule inconsistency is sufficiently high that if F always reports A:^ under inconsis-

tency, it is optimal for H to audit all reports of A:^, even when F always reports x//

when it observes _v//. Because the tax rate differential is high, F has a pure strategy

of reporting A^ when it observes yg; L in tum has a pure strategy of never auditinga report of A/y. F's strategy of always reporting .v/ under inconsistency implies that,

when the critical level p* is crossed, the probability of inconsistency is high

enough that auditing for the sole purpose of achieving double taxation is beneficial

for H. There is a pure strategy equilibrium in which a = I. p = O,y=], and 5 = 0

(equilibrium 11). A further increase in/? does not affect these strategies.

The effects of changes in p on the players' strategies when e < ( T / / - T ^ ) / T / /

are summarized in Table 3. An increase in p when the tax rate differential is high

decreases income shifting when yf^ occurs (a increases) and increases the fre-quency with which H audits low reports (/ increases).

Low tax rate d ifferential and high penalty

Second, we consider the case in which ( T / / - Ti)IXf^ <e<K + (T// - r^)/T//. The

players' strategies are the same as in the high tax rate differential case until p = p*..

As soon as p > /;*, the relatively high value off implies that F no longer has a

dominant strategy of reporting x^ when there is inconsistency, because the conse-

quences of a certain audit by H are too severe. F therefore chooses a mixed strategy

(/3 > 0) to deter H from always auditing reports of A^; H chooses an audit frequency

so as to keep F indifferent between reports when it observes yg (equilibrium III).

As p increases further, F increases ^ in order to keep H indifferent. When p reaches

its second critical value {p\), an increase in /3 could keep H indifferent, but would

induce L to audit all reports of A://. Alternatively, a decrease in ^ could keep L

indifferent, but would induce H to audit all reports of A ^. Therefore, the probability

of transfer-price rule inconsistency becomes sufficiently high that either H or L has

an incentive to always audit, regardless of F's reporting strategy. However, it cannot

TABLE 3

Effeclsofpon strategies when e < (r/y-T^)/r//(high tax rate differentia!)

be an equilibrium for L to always audit. If L always audits, F will report Xi^ under

inconsistency, regardless of H's strategy, because T^ + ysTf^ < ^// + ^^L f*"" ^"y

choice of 7. But if F always reports j ^ , L should never audit. In equilibrium, F

therefore decreases P to make L indifferent between auditing and not auditing

reports of % ; L chooses a mixed strategy (S > 0) to make F indifferent betweenreporting Xf^ and jr when _Vg occurs; and H audits all low reports (equilibrium IV

As p increases, F continues to decrease (i to keep L indifferent between auditing

and not auditing reports of JT//.

The effect of changes in p on players' strategies when (r^^ - '^L)I'^H ^ ^ '^ ?r +

(T// - T^) / T / / are summarized in Table 4. An increase in the probability of transfer-

price rule inconsistency when the tax rate differential is low and the penalty rate is

high affects F's reporting strategy both when the transfer-pricing rules are incon-

sistent and when they are consistent. An increase in/j increases the probability that

H (L) audits a report ofx^ (jc/y) (7 and 5 increase). F responds in tum by decreasing

the probability of income shifting when it observes y^ {a increases). An increase

in/j has ambiguous effects on/3*, F's reporting strategy when the transfer-pricing

ruies are inconsistent.

Low tax rate differential and low penalty

Third, we consider the case in which £ > ;r + (T// - T[^)/tff. The combination of a

low tax rate differential and a low penalty implies that income shifting is difficult

for H to deter. When 0 < p < p*, F chooses a m ixed strategy when it observes v//

but always reports Xf^ under inconsistency, while H employs a mixed audit strategy

when F reports J:^ and L never audits (equilibrium V). As soon as p reaches the

critical value p*, the relatively high value of £ implies that L has an incentive to

audit in an effort to achieve double taxation. As p increases , F increases

(decreases) the probability of reporting x// when there is no inconsistency (when

there is inconsistency) in order to keep both H and L indifferent between auditing

and not auditing (equilibrium V I). This continues until p reaches the critical value

Pj. At that point, F always reports j / / when there is no inconsistency, and Halways audits. In order to keep L indifferent between auditing and not auditing as p

increases further, F decreases the probability of reporting Xf^ under inconsistency

(equilibrium IV).

The effects of changes in p on players' strategies when e> K + {Tf^ - T^) / T

are summarized in Table 5. An increase in the probability of transfer-price rule

incon sistency when the tax rate differential is low and the penalty rate is low

increases the probability that H (L) audits a report of x^ (Xf^) (7 and 5 increase).

responds in tum by decreasing the probability of income shifting when it observes>•// (a increases) and increasing the probability that it reports x^ when the transfer-

practices. Once the transaction occurs, p is simply a fixed parameter. In this section,

we consider the effects of changes in p on the firm's expected tax liahility and on

the deadweight loss associated with auditing.

How p affects the firm's expected tax liabilityProposition 7 establishes how F's expected tax liability changes as p changes in

each equilibrium.

PROPOSITION 7. F's expected tax liability is:

(a) decreasing in p in equilibrium I if and only ifE < [T/y( 1 + ;r) -

(b) decreasing in p in equilibrium II if and only ife < (T// -

(c) increasing in p in equilibria III, IV, V, and VI.

The proof is in the appendix. Increasing transfer-price rule inconsistency

increases F's expected tax liability in equilibria III-VI, but the effect depends one

in equilibria I and II, In equilibria I and II, \fe is sufficiently small, then transfer-

price rule inconsistency reduces the firm's expected tax liability for two reasons.

First, F always reports .v^ when the transfer-pricing rules are inconsistent, so a

higher/? reduces F's expected tax payment associated with the initial report. Second,

e is sufficiently low that there is little chance of H prevailing in its effort to imposedouble taxation. For example, suppose that T/ = 0.2. r// = 0.4. and;r = 0.2. An

increase in tax law inconsistency in equilibriutn I is beneficial to the firm as long as

the probability of double taxation in case of inconsistency is below 35 percent.

Thus, the conventional wisdom that inconsistent transfer-pricing rules that make

double taxation possible increase the firm's expected tax liability need not hold in

our model. Because the cutoff values fore are higher when the tax rate differential

TABLE 5

Effects ofp on strategies when f > ;r + (% - r^^)/!// (low tax rate differential, low penalty)

is higher, an increase in p will be more likely to decrease the firm's expected tax

liability when the tax rates of the two countries are far apart. Iff: is sufficiently

high, however, an increase inp will increase F's expected tax liability.

How p affects deadweight loss

An increase in transfer-price rule inconsistency not only affects the amount of

wealth transferred between F and the governments of H and L, but also the dead-

weight loss associated with the tax compliance process due to costly auditing. A

plausible conjecture is that an increase in transfer-price rule inconsistency

increases the cost of auditing. Surprisingly, this conjecture is false. Proposition 8

shows the conditions under which an increase in transfer-price rule inconsistency

increases the deadweight lo ss.

PROPOSITION 8. The deadweight loss from auditing is:

(a) increasing in p in equilibrium I ijfe < (I +Tr)/2;

(b) increasing in p in equilibrium II:

(c) decreasing in p in equilibria HI and V;

(d) increasing inp in equilibrium IV iffk^ -5*jt^ > 0."

(e) increasing inp in equilibrium V I iff (I -\-n - 2e){y*kff -S*ki) > 0.

The proof is in the appendix. The effect of an increase in p on deadweight loss

from auditing depends on the firm's reporting strategies, how an increase in p

changes those reporting strategies, and the government's audit strategies. To illus-

trate the possible effects, consider equilibria II and V. In both cases, no reports of

Xff are audited. Moreover, the probability that H audits a report of x^ is independent

of/J. Consequently, audit costs increase if and only if an increase in p increases the

probability of a report of j ^ ^ . In equilibrium II, an increase inp increases the prob -

ability of a report of x^. In contrast, in equilibrium V an increase in/ J decreases theprobability of a report of x^. In equilibria IV and VI, both countries audit, so the effect

of an increase in p on the aggregate audit cost depends on its effect on the fre-

quency that A-^ {Xff) is reported, and whether k^^y* > ki8*. In equilibrium IV, an

increase in p always increases the probability that x^ is reported, whereas in equi-

librium VI, this is only the case w h e n £ < ( l +K)I2.

Taken together. Propositions 7 and 8 demonstrate that there are settings in

which an increase in transfer-price rule inconsistency both increases aggregate

expected tax revenues and decreases expected audit costs. This result alwaysoccurs in equilibria III and V and may occur in equilibria I, IV. and VI. When it

price rule inconsistency, which is a necessary condition for double taxation to

occu r in our model. We find that an increase in the probability of transfer-price rule

inconsistency induces the tax authority to adopt a more aggressive audit strategy.

This increase in aggressiveness in turn induces the firm to engage in less income

shifting when the transfer-pricing rules are consistent, but could induce either anincrease or a decrease in the probability of reporting income to the low-tax-rate

country when the transfer-pricing rules arc inconsistent. The combined effect of

these strategy changes leads to two surprising results. First, an increase in transfer-

price rule inconsistency may decrease the firm's expected tax liability, which

implies that inconsistency could be good for firms and bad for governments. Second,

an increase in transfer-price rule inconsistency can either increase or decrease the

deadweight losses associated with audit costs. Our results call into question the con-

ventional wisdom that the prospect of double taxation due to transfer-price rule

inconsistency is helpful to governments, detrimental to taxpayers, and socially

inefficient. A government policy that strives to increase transfer-price rule consist-

ency is neither clearly beneficial nor unequivocally harmful for either the firm or

the governments. We identify settings in which the reduction of transfer-price rule

inconsistency would both lower government tax revenues and increase audit costs.

In these settings, governments should not coordinate their transfer-pricing rules

and practices too closely.

Appendix

Proof of Proposition I

We show that

t^(\+7t)i\p) + 2{per^k^) , ^

( l ) [ { l ) ^ ] ' ^ '•^

is an equilibrium when e < (T// - T^)/r// + ;r and p < p*.

(a) F is willing to random ize with probability a because when yf^ is observed,

F's payoff from reporting x^ is 7*[-t//( 1 + ;r)l + [-T/^( I - 7*)] = -T/ / , which is the

same as F's payoff from reporting x^. a* is a feasible strategy because f < p* =

k^ /(2£T// - kf ) ensures that a < I.

(b) ^ - 0 is optimal because when yg is observed, reporting x/^ yields a payoff

(d) 5 ^ 0 is optimal for L because not auditing Xff yields a payoff of zero and

auditing Xff yields a payoff of -kf^ < 0. •

Proof of Proposition 2

We show that

is an equilibrium when £<{Xfj- Xf)IXff and p > /?*.

(a) « ^ I is optimal because when F observes >•//, reporting Xff yields a payoff

of -Xff and reporting .v^ yields a payoff of -Xjfi 1 +K).

(b) j8 ^ 0 is optimal because when F observes yg, reporting Xff yields a payoff

of -Xff and reporting A'^ yields a payoff of -r^ - £Xff > -Xff for all £<{Tff- Xi)IXff.

(c) 7= 1 is optimal forH because not auditing,v^yieldsapayoff of zero and audit-

ing Xf^yields a payoff of £Xff \2p /{\+p)]'kff>0 because p> p* = kff/(2£Xff - kff).

(d) 5 = 0 is optimal for L because not auditing Xff yields a payoff of zero andauditing Xff yields a payoff of ~kf < 0.

Proof of Proposition 3

We show that

-k,A\ + p)

is an equ ilibrium when ( r / / - r ^ ) / r ^ < £ < (T /y - r /_ ) / r ^ + ; r and p*<p< p%.(a) a ^ I is optimal because when F observes V//, reporting Xff yields a payoff

of -Xff and reporting x^^ yields a payoff of - / * % ( 1 + ;r) - T/^(] -7* ) < -x^f because

£-K<{Xff-X,_)IXff.

(b) F is willing to randomize when it observes yg because reporting x// yields a

payoff of -Xff and reporting .v/ yields a payoff of /* {-T^ - ET//) + {-x^i 1 -7*) ] = -Xff.

P* is a feasible strategy because p > p* = kf,l{2£Xff - kff) implies^ > 0.

(c) H is willing to random ize with probability / when it observes xi_ because

not auditing v^ yields a payoff of ze ro and auditing .v^ yields a payoff of

(c 1) F's expected tax liability in equilibria III and V. denoted L-^ 5, is

2 ^ 2 •

Differentiating with respect to p yields

dp 2 ^•

(c2) F's expected tax liability in equilibrium IV, denoted L4, is

+ piti +

Differentiating with respect to p yields

which is greater than (less than) zero if e > (<) ix^ - Ti)/2Tf^. Because £ > (TffT/y in Proposition 4, F's tax liability within equilibrium IV is increasing in p.

(c3) F's expected tax liability in equilibrium V I, denoted L5, is

Substituting/* - (r^ - T ^ ) / [ T / / ( 1 +K)-XI^] from Proposition 6 and differentiating

with respect to p yields

dp 2\x,,( ^

which is greater than zero because £ > l r ^ ( l +7:) -

Proof of Proposition 8

(a) In equilibrium 1, the expected deadweight lo ss, deno tedy4 ], is

Substituting the value for^* from Proposition 4 and differentiating with respect top yields

(e) In equilibrium V I, the expected deadweight loss, denotedAg , is

Substituting the values for a* and^* and differentiating with respect to p yields

the sign of which is the same as the sign of (1 + n- 2£)(Y*k^ - 5 * i t ^ ) . •

Endno t e s

1. We assume that the tax authorities can costlessly verify that the taxpayer has reported

the transaction in a consistent fashion on both tax retums and penalize the taxpayer if it

fails to do so. In the U.S. context, the Internal Revenue Service (IRS) can obtain the

foreign country tax retum through an information document request (IDR), one of

several intemational tax enforcement methods available to the IRS (Sharp and

Sheppard 2003).

2. If one country measures taxable income on the basis of separate accounting and arm 's-length transfer prices, while the other uses formulary apportionment, aggregate taxable

income could be less than worldwide econom ic income. Our paper investigates settings

in which both countries measure income under separate accounting using the ami's-

length standard, so aggregate taxable income cannot be less than worldwide economic

income in our model.

3. This result is similar to the case of formulary apportionmen t, in which govem ments

will tend to choose different apportionment formulas instead of coordinating on a

single formula (Anand and Sansing 2000).

4. The assumption of equal penalty rates in the two countries is without loss of generality

Commissioner v. National Alfalfa Dehydrating. 1974. 417 U.S. 134.

E m st& Young. 1997, 1999, 20 01 . £™5/(fe Young transfer pricing g lobal survey. Uevj York:

Emst & Young.Feltham, G., and S. Paquette. 2002. The mterrelationship between estimated tax payments

and taxpayer compliance. Journal ofthe American Taxation Association 24

(Supplement): 27 -4 5 .

Graetz, M ., J. Reinganum , and L, Wilde. 1986. The tax com pliance gam e: Toward an

interactive theory of law enforcement. Journal o f Law. Econ omics, and Organization

2 ( 1 ) : 1-32.

Harris, A. 2004. Multinationals in Kenya face transfer pricing uncertainty. Tax Notes

Internationan5 {\0): 891-2.Mills, L., and R. Sansing . 2000 . Strategic tax and financial reporting decisions: Theory and

evidence. Contemporary Accounting R esearch 17 (1): 85 -10 6.

Morgan. J. 2003. Arbitration clauses in international tax treaties could benefit developing

states. Tax Notes International 31 (7): 681 - 9 1 .

Mortier, R 2002 . International tax arbitration: Toward bener taxpayer protection. Tax Notes

International 27 (14): 5 3 -8 .

Reinganum, J.. and L. Wilde. 1986. Equilibrium verification and reporting policies in a

model of tax compliance. International Economic Review 27 (3): 739-60.Rhoades, S. 1997. Costly false detection errors and taxpayer rights legislation: Implications

for tax com pliance, audit policy, and revenue collections. Journal ofthe American

Taxation Association 64 (Supplement): 27-47.

Rhoades, S. 1999. The impact of m ultiple component reporting on tax compliance and audit

strategies. The Accounting Review 74 (1): 63 -8 5.

Ring, D. 2000 . On the frontier of procedural innovation: Advance pricing agreements and

the struggle to allocate income for cross border taxation. Michigan Journal of

International Law 2\ (2): 143-234.Sansing, R. 1993. Information acquisition in a tax com pliance gam e. The Accounting

Review 6S {4): ^14-M.

Sharp, W., and H . Sheppard. 2003. Privilege, work-product d octrine, and other discovery

defenses in U.S. IRS's international tax, enforcement. Tax Notes International 32 (4):

377- 96 .

Sullivan. M. 2004. With billions at stake, Glaxo puts U .S. APA program on trial. Tax Notes