Welcome to The MDBA Business Club Breakfast 2 nd Tuesday of every month THE MDBA VISION To be recognised as a professional, highly respected Business Association representing our members. We show leadership through providing relevance, benefits and value to our members and the business community ensuring growth and prosperity. We are innovative and display integrity and are trusted amongst governing bodies. The MDBA will be accountable and show a community spirit. Our members will be well respected within the business community. MDBA MONTHLY BREAKFAST CLUB MAY 2015

Transcript

MDBA MONTHLY BREAKFAST CLUB MAY 2015

Welcome to The MDBA Business Club Breakfast 2nd Tuesday of every month

THE MDBA VISIONTo be recognised as a professional, highly respected Business Association representing our members. We show leadership through providing relevance, benefits and value to our members and the business community ensuring growth and prosperity. We are innovative and display integrity and are trusted amongst governing bodies. The MDBA will be accountable and show a community spirit. Our members will be well respected within the business community.

MDBA MONTHLY BREAKFAST CLUB MAY 2015

Welcome to The MDBA Business Club Breakfast 2nd Tuesday of every month

OUR MISSIONThe MDBA will show leadership through effective presentation, networking opportunities and exchange of information. We will build member trust through our commitment to these crucial aspects of growing their business. MDBA will be accountable to its members offering relevant, informative topics and training. These will be designed to enhance their business and ensure business knowledge and growth.

MDBA MONTHLY BREAKFAST CLUB MAY 2015

AGENDA

7AM ARRIVE – COFFEE AND NETWORK7.30AM – CEO WELCOME AND UPDATE.7.40AM – ATTENDEES INTRO7.45AM TO 8AM – CASUAL NETWORKING8AM –Steve O’Reilly8.45AM – Q AND A 9AM FINISH AND CASUAL NETWORKING

MDBA MONTHLY BREAKFAST CLUB MAY 2015

MDBA MONTHLY BREAKFAST CLUB MAY 2015

The Malaga and Districts Business Association is very proud to be partnering with these wonderful sponsors.

UNDER

CONSIDERATIO

N

UNDER

CONSIDERATIO

N

UNDER

CONSIDERATIO

N

MDBA MONTHLY BREAKFAST CLUB MAY 2015

Update on what's happening at the MDBA

ACKNOWLEDGE MDBA BOARD MEMBERS NEWSLETTER – Advertising details on our web site New members get a free half page advert as part of the membership WE WANT TO GROW OUR MEMBERSHIP AND ATTENDANCE AT THESE BREAKFASTS –

ENCOURAGE ATTENDEES TO REFER NEW MEMBERS TO CLIVE REMIND MEMBERS OF SUNDOWNERS Finalising our strategy document for 2015/16 Canberra visIt The quality of our internet connections here in Malaga The current plan of rollout of the NBN – NEWSPAPER ARTICLE What problems do businesses face in Malaga regarding communications (Boardband and

Telephone) Sponsorship opportunities are now listed on our website Business awards 2015

MDBA MONTHLY BREAKFAST CLUB MAY 2015

ASSO

CIA

TIO

N L

OBBIE

S F

OR

NBN

IN

MA

LAG

A

WA BUSINESS NEWS

MDBA MONTHLY BREAKFAST CLUB MAY 2015

FacilitatorSteve O’Reilly, KPMG Director Private Enterprise

Steve works collaboratively with clients providing tax, accounting and compliance offerings. Services are tailored to meet the unique challenges of the mid-tier market and to provide business owners with innovative solutions. With over 10 years’ experience, Steve’s portfolio spans a range of industries where he is adept in the preparation of special purpose and general purpose financial statements. He also has significant experience as a director of not-for-profit entities, including roles with the Fremantle Dockers Football Club and Santa Maria College.

KPMG and the KPMG logo are registered trademarks of KPMG International.

Reason Six

Poor cash flow forecasting

Three way forecasting

“Telling the future by looking at the past assumes that conditions remain constant. This is like driving a car looking in the rear-view mirror” Source: Anon

Historical financials statements

Forecasts

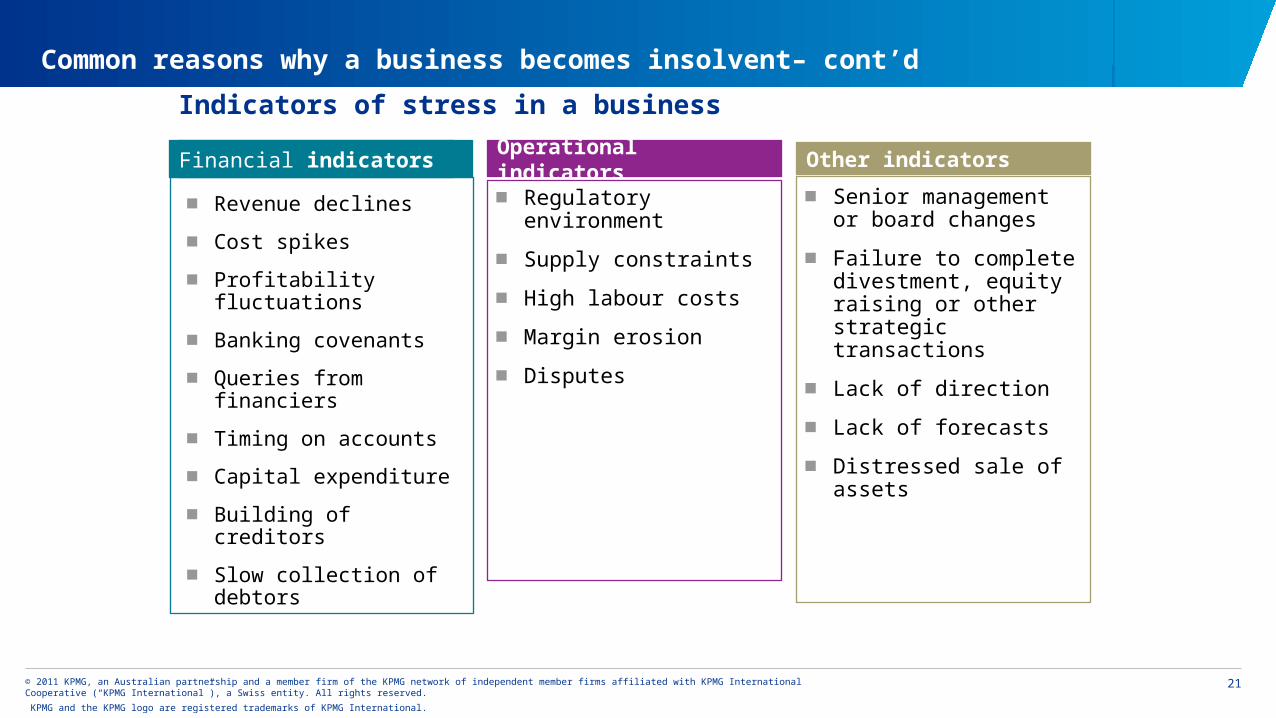

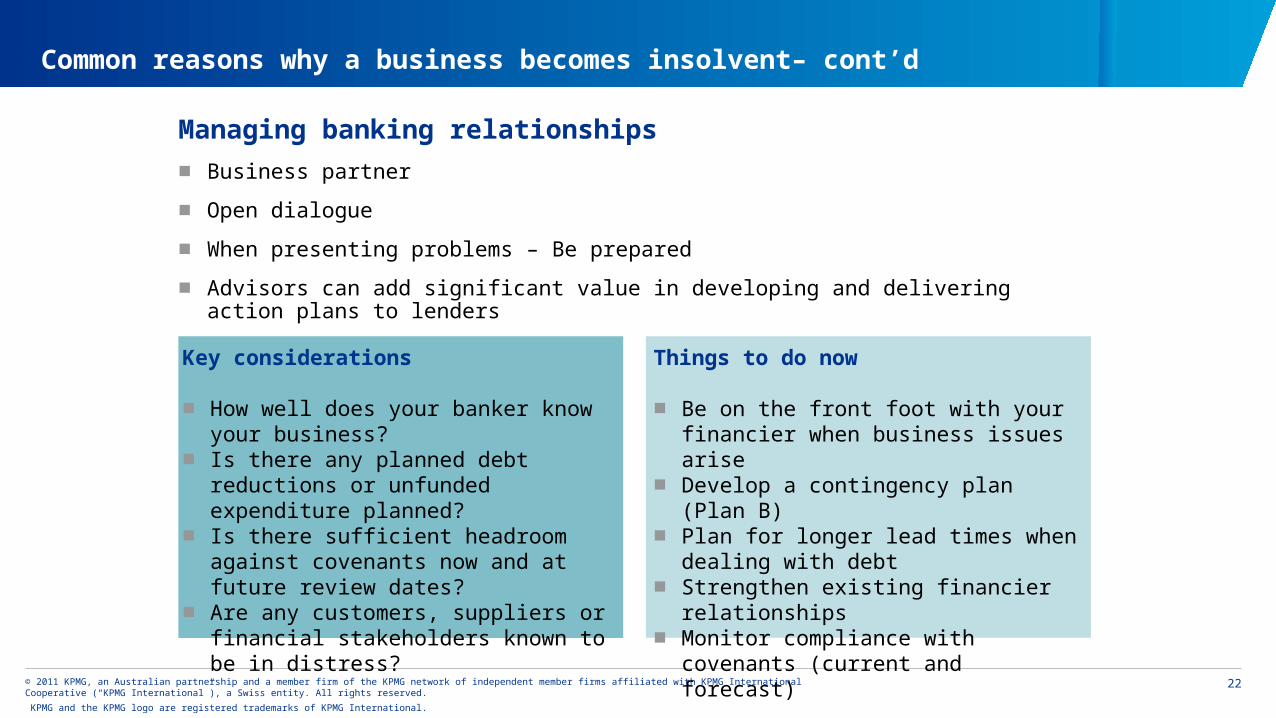

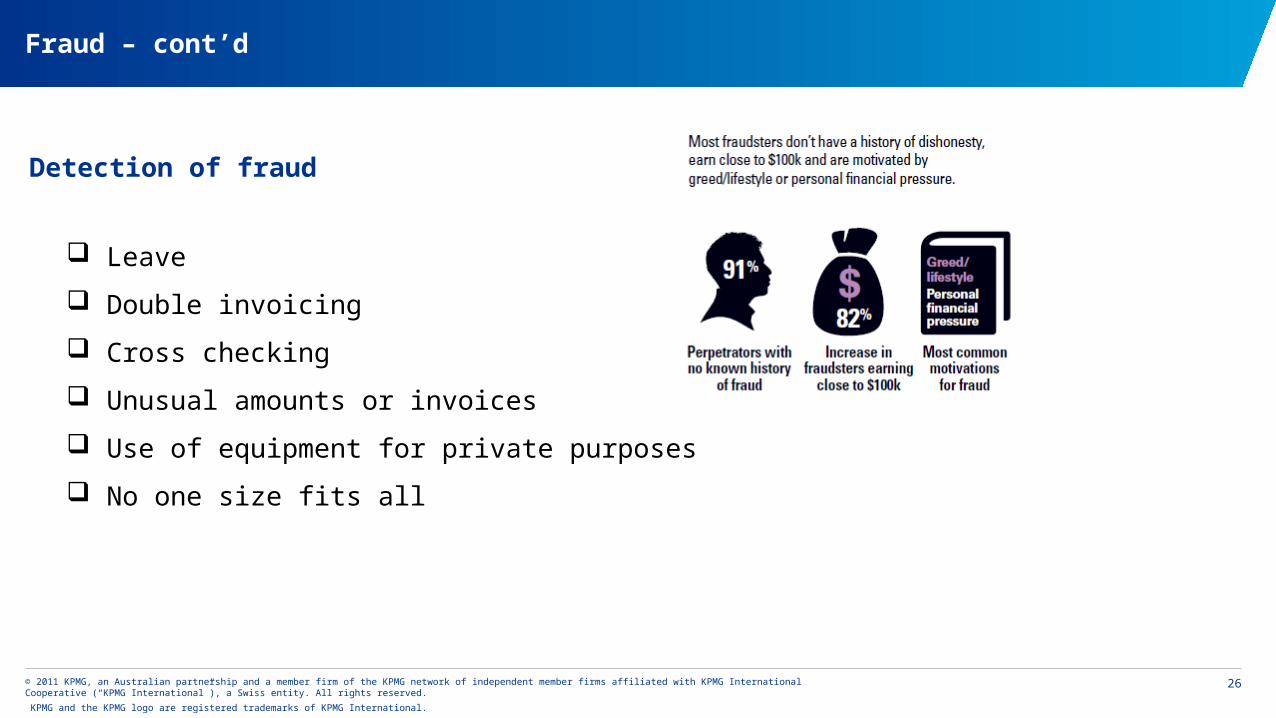

Common reasons why a business becomes insolvent– cont’d

KPMG and the KPMG logo are registered trademarks of KPMG International.

Disclaimer

■ This presentation has been prepared without taking account of the objectives, financial situation or needs of any particular business or individual. Before acting on the information in this presentation you should consider its appropriateness to your circumstances and, if necessary, seek appropriate professional advice