24

Why can’t we do this at book value? Everything you need to know about maintenance of capital 4 July 2012 Glafkos Tombolis James Wilkinson

Why can’t we do this at book value?

Everything you need to know about maintenance of capital

4 July 2012

Glafkos Tombolis

James Wilkinson

What does it all mean?

What are the rules?

Distributions in kind

Decision tree analysis

Real-life examples

Agenda

1 Why can’t we do this at book value? – Everything you need to know about maintenance of capital

What does it all mean?

2 Why can’t we do this at book value? – Everything you need to know about maintenance of capital

A company’s balance sheet

3

Assets 100

Liabilities (50)

Net assets 50

Share capital 10

Share premium account 10

Profit and loss account 30

Shareholders’ funds/equity 50

Why can’t we do this at book value? – Everything you need to know about maintenance of capital

What does it all

mean?

4 Insert footer text by selecting 'Insert - Header & Footer' / page numbers may also be taken off with this function

What does it all

mean?

Share capital – no specific statutory definition, but see Sections

540(1) and 548 CA 2006

Share premium account and merger reserve – Sections 610(1)

and 612 CA 2006

Other undistributable reserves – Section 831(4) CA 2006

–capital redemption reserve

–excess of accumulated unrealised profits over accumulated

unrealised losses (revaluation reserve)

–any other reserve designated as such in articles

Distributable reserves – Section 830 CA 2006

What is “capital”?

Basic rule: Share capital and other non-distributable

reserves (e.g. share premium) constitute a “buffer” primarily

for the benefit of creditors and shareholders (in that

order)

It is the relationship between this “buffer” and the company’s

net assets that will determine whether maintenance of

capital rules have been breached

5 Why can’t we do this at book value? – Everything you need to know about maintenance of capital

What does it all

mean?

Basic rule

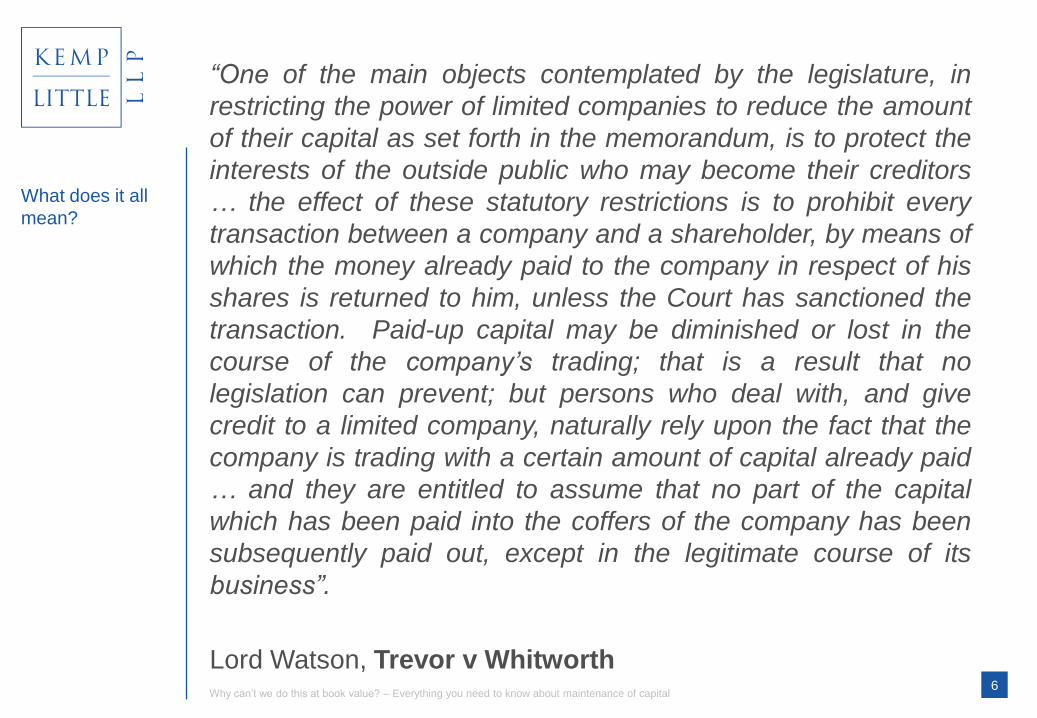

“One of the main objects contemplated by the legislature, in

restricting the power of limited companies to reduce the amount

of their capital as set forth in the memorandum, is to protect the

interests of the outside public who may become their creditors

… the effect of these statutory restrictions is to prohibit every

transaction between a company and a shareholder, by means of

which the money already paid to the company in respect of his

shares is returned to him, unless the Court has sanctioned the

transaction. Paid-up capital may be diminished or lost in the

course of the company’s trading; that is a result that no

legislation can prevent; but persons who deal with, and give

credit to a limited company, naturally rely upon the fact that the

company is trading with a certain amount of capital already paid

… and they are entitled to assume that no part of the capital

which has been paid into the coffers of the company has been

subsequently paid out, except in the legitimate course of its

business”.

Lord Watson, Trevor v Whitworth 6 Why can’t we do this at book value? – Everything you need to know about maintenance of capital

What does it all

mean?

The rules

7 Why can’t we do this at book value? – Everything you need to know about maintenance of capital

The basic common law rule: a distribution of a company’s assets

to a shareholder, except in accordance with specific statutory

procedures, is a return of capital that is unlawful and ultra vires the

company

Section 851 CA 2006 – common law rules on distributions

preserved

Trevor v Whitworth (1887) – A company cannot lawfully make a

distribution out of capital

Aveling Barford v Perion (1989) – Undervalue sideways or

upstream transactions are distributions

Progress Property v Moorgarth Group (2010) – Must consider true

character of transaction to determine if a distribution at all.

Directors’ intentions likely to be relevant factor

8

The rules

8

Common law

Why can’t we do this at book value? – Everything you need to know about maintenance of capital

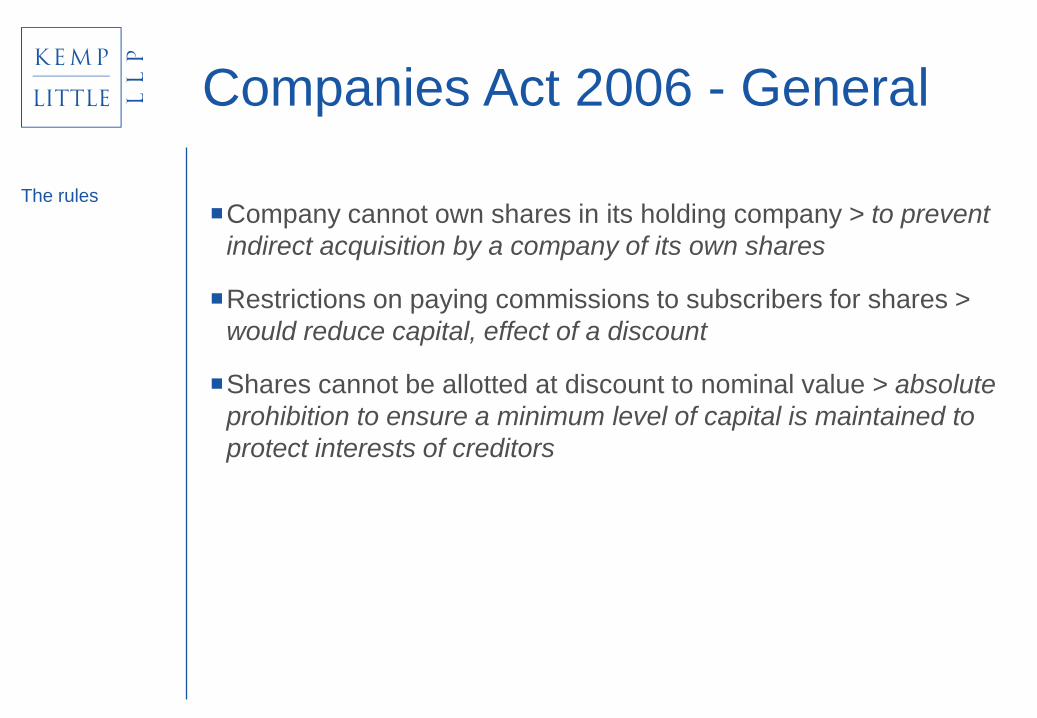

Company cannot own shares in its holding company > to prevent

indirect acquisition by a company of its own shares

Restrictions on paying commissions to subscribers for shares >

would reduce capital, effect of a discount

Shares cannot be allotted at discount to nominal value > absolute

prohibition to ensure a minimum level of capital is maintained to

protect interests of creditors

Companies Act 2006 - General

The rules

Reductions of capital > only by court sanction or solvency

statement so as not to adversely affect creditors

Companies may not acquire their own shares (certain exceptions

exist) > to protect third parties from disguised reduction of capital,

indirect ownership by the company of itself and manipulation of its

share price

Financing of redemption > potentially prejudicial to interests of

company’s creditors so can only be done out of distributable

profits, a fresh issue of shares or, if a limited company, out of

capital

Value of premiums on shares must be credited to share premium

account > share premium is a non-distributable reserve and may

only be reduced as per reduction of capital procedures

10 Why can’t we do this at book value? – Everything you need to know about maintenance of capital

Companies Act 2006 – General

(cont.)

The rules

11 Insert footer text by selecting 'Insert - Header & Footer' / page numbers may also be taken off with this function

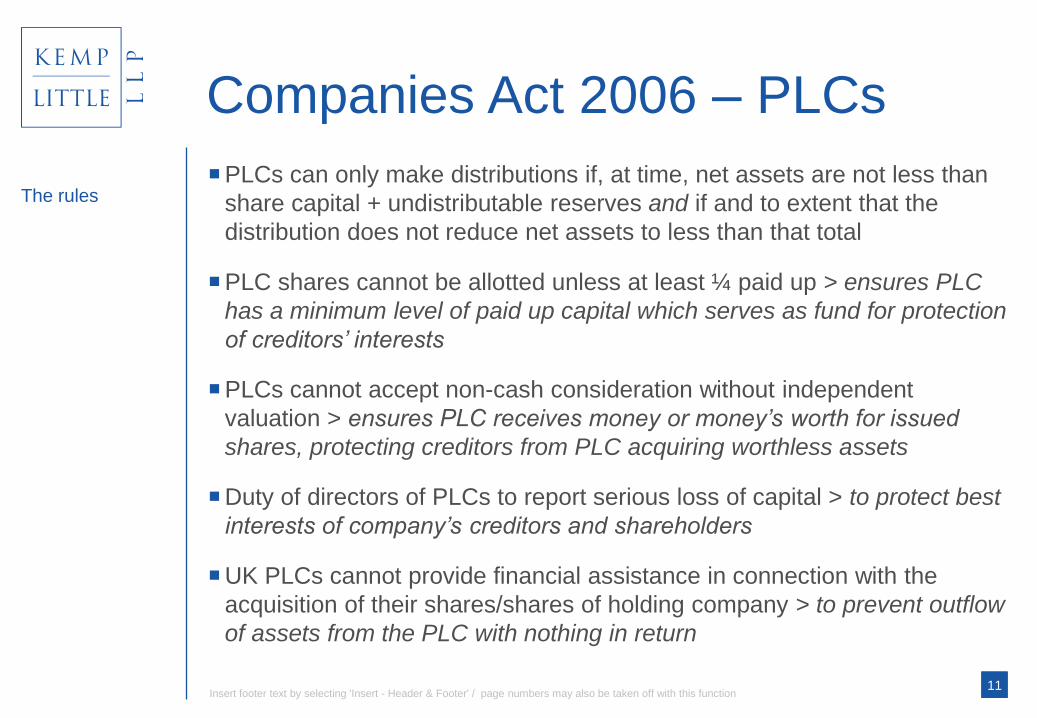

PLCs can only make distributions if, at time, net assets are not less than

share capital + undistributable reserves and if and to extent that the

distribution does not reduce net assets to less than that total

PLC shares cannot be allotted unless at least ¼ paid up > ensures PLC

has a minimum level of paid up capital which serves as fund for protection

of creditors’ interests

PLCs cannot accept non-cash consideration without independent

valuation > ensures PLC receives money or money’s worth for issued

shares, protecting creditors from PLC acquiring worthless assets

Duty of directors of PLCs to report serious loss of capital > to protect best

interests of company’s creditors and shareholders

UK PLCs cannot provide financial assistance in connection with the

acquisition of their shares/shares of holding company > to prevent outflow

of assets from the PLC with nothing in return

11

Companies Act 2006 – PLCs

The rules

Directors’ duties (Sections 170-181 CA 2006). In particular,

company law does not recognise a concept of group benefit.

Therefore, any proposed transaction must be in the best interests

of the particular company

Reviewable transactions:

–transactions at an undervalue – Section 238 Insolvency Act 1986

–preferences – Section 239 Insolvency Act 1986

–transactions defrauding creditors – Section 423 Insolvency Act

1986

Capacity – check powers in articles (and/or memorandum of

association)

12 Why can’t we do this at book value? – Everything you need to know about maintenance of capital

Don’t forget…

The rules

Distributions

13 Why can’t we do this at book value? – Everything you need to know about maintenance of capital

Company must have “profits available” – Sections 830(1) and

853(4) CA 2006

Question is an accounting one

Distribution must be justified by “relevant accounts” – Sections

836-839 CA 2006

Post balance sheet events to be taken into account

Basic rule

Why can’t we do this at book value? – Everything you need to know about maintenance of capital

Check articles

Comply with Companies Act formalities for distributions in Part 23

(Section 829 et seq.)

Distributable reserves must equal or exceed original book value –

ex parte Westburn Sugar Refineries Ltd (1951)

“Mark-to-market” – Section 846 CA 2006:

–must do where, following upwards revaluation, uplifted book

value exceeds DRs

–can do where DRs equal to or exceed book value, but market

value is higher; provides statutory cover

15 Why can’t we do this at book value? – Everything you need to know about maintenance of capital

Distributions

“Express” distributions in kind

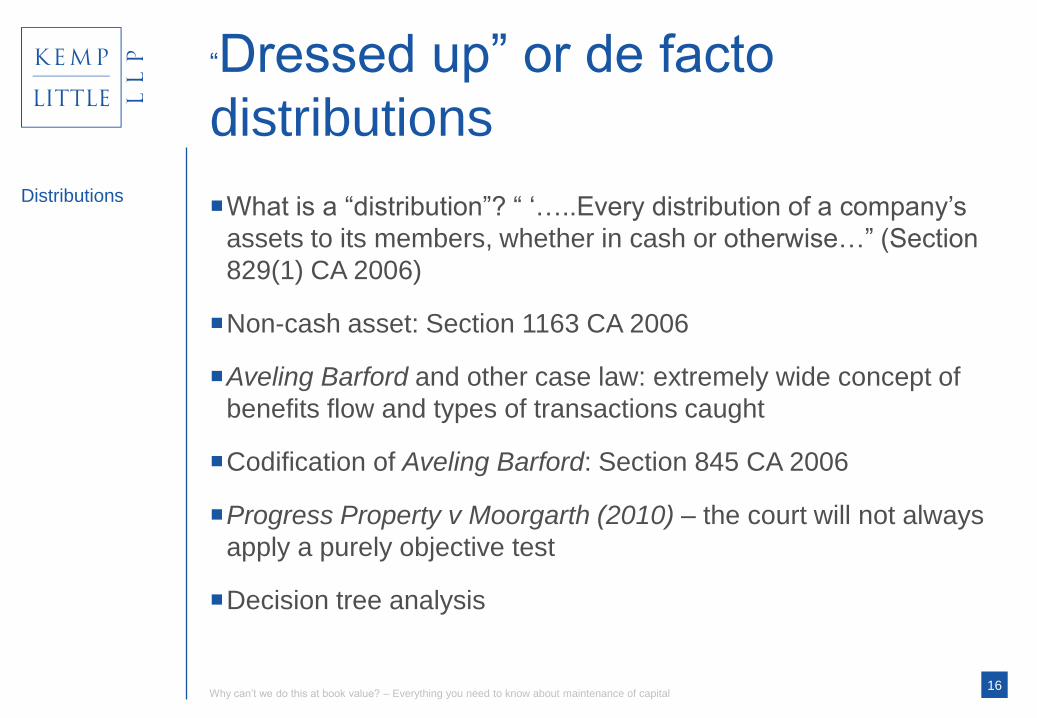

What is a “distribution”? “ ‘…..Every distribution of a company’s

assets to its members, whether in cash or otherwise…” (Section

829(1) CA 2006)

Non-cash asset: Section 1163 CA 2006

Aveling Barford and other case law: extremely wide concept of

benefits flow and types of transactions caught

Codification of Aveling Barford: Section 845 CA 2006

Progress Property v Moorgarth (2010) – the court will not always

apply a purely objective test

Decision tree analysis

16 Why can’t we do this at book value? – Everything you need to know about maintenance of capital

“Dressed up” or de facto

distributions

Distributions

The most comprehensive technical analysis on distributions

available – 168 pages

Particularly useful in relation to intra-group transactions, such as:

–dividends received on investment in subsidiary

–subsequent reinvestment of dividends received from subsidiary

–dividends received from pre-acquisition profits

–sales of asset by parent to subsidiary

–sales of asset by subsidiary to parent followed by dividend of

resulting profit

–capital contributions

ICAEW Tech 02/10

17 Insert footer text by selecting 'Insert - Header & Footer' / page numbers may also be taken off with this function

Decision tree analysis

18 Why can’t we do this at book value? – Everything you need to know about maintenance of capital

19 Why can’t we do this at book value? – Everything you need to know about maintenance of capital

Distributions

Does the transaction involve the provision of

services to a member (direct or indirect)

No distribution

Distribution – company must have sufficient

DRs immediately prior to transfer to cover

amount by which consideration is less than

book value

Yes

Does the transaction involve the

transfer/sale/disposition of a non-cash asset to a

member (direct or indirect?)

No

Is the company receiving any consideration for the transfer?

Theoretical risk of

distribution of services

provided at below cost

Yes No No Yes

Does the company have positive

DRs immediately prior to transfer?

Distribution in specie.

Company must have

sufficient DRs to cover book

value of non-cash asset being

transferred

Yes No

Is the company receiving consideration equal to

or greater than book value of non-cash asset?

Yes No

No distribution

Distribution – unless

consideration is market

value or Progress

Property applies

Non-cash distributions

20 Why can’t we do this at book value? – Everything you need to know about maintenance of capital

Distributions

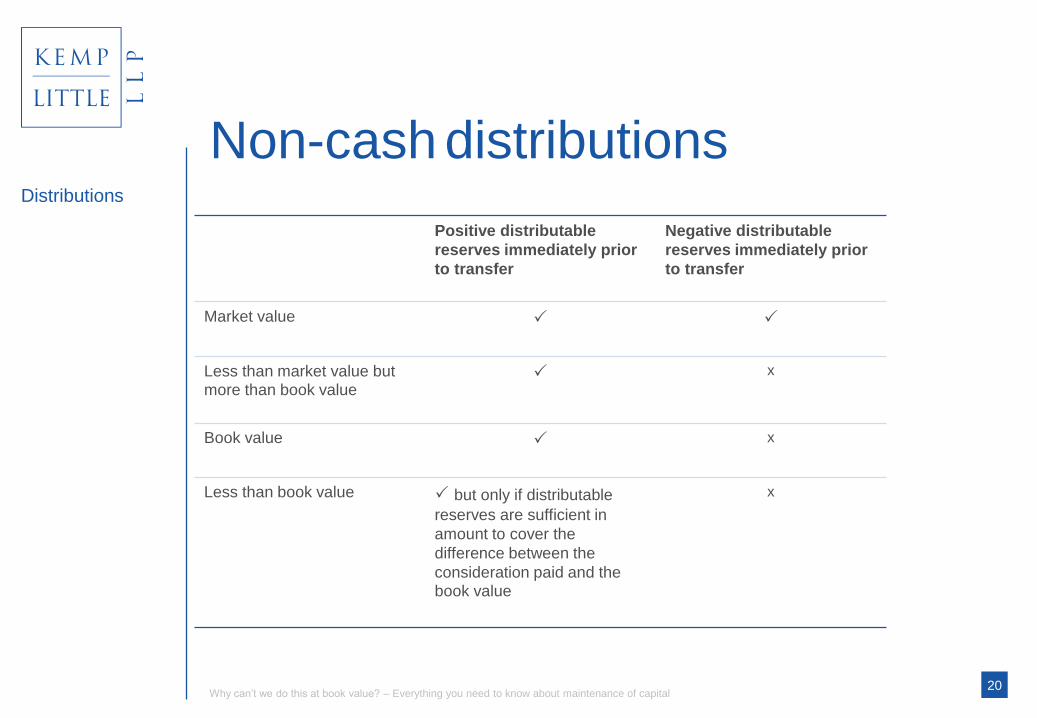

Non-cash distributions

Positive distributable

reserves immediately prior

to transfer

Negative distributable

reserves immediately prior

to transfer

Market value

Less than market value but more than book value

x

Book value

x

Less than book value

but only if distributable

reserves are sufficient in

amount to cover the

difference between the

consideration paid and the book value

x

Our clients

We provide a

comprehensive

range of legal

services for

technology and

digital media

companies and

companies in

sectors that

technology

transforms

We actively work

for a range of the

largest global

public companies,

AIM listed entitles,

PE backed

businesses, private

companies and

investors in the

technology and

digital media

sectors

21

Why can’t we do this at book value? – Everything you need to know about maintenance of capital

22 Why can’t we do this at book value? – Everything you need to know about maintenance of capital

Glafkos Tombolis

Partner

ddi 020 7710 1672

James Wilkinson

Associate

ddi 020 7710 1679

Kemp Little LLP

Solicitors

Cheapside House

138 Cheapside

London EC2V 6BJ

Tel: 020 7600 8080

Fax: 020 7600 7878

www.kemplittle.com

Kemp Little LLP is a limited liability partnership.

Registered number OC300242 England. Registered office as shown

Kemp Little is supporting SCI to treat 40,000

children suffering from neglected tropical diseases.

Treatment costing 50p per child per year will allow

them to attend school, learn more effectively & live

more prosperous lives.