Wolters Kluwer Wolters Kluwer Half Year Results 2001 Half Year Results 2001 Rob Pieterse, Chairman of the Executive Rob Pieterse, Chairman of the Executive Board Board Analysts & Investors, August/September 2001 Analysts & Investors, August/September 2001

Transcript

Wolters KluwerWolters Kluwer

Half Year Results 2001Half Year Results 2001

Rob Pieterse, Chairman of the Executive BoardRob Pieterse, Chairman of the Executive Board

• IHS immediate priority to address unsatisfactory performance IHS immediate priority to address unsatisfactory performance

• Strong increase in electronic sales, up 37%: now 26% of total (20%)Strong increase in electronic sales, up 37%: now 26% of total (20%)

• Internet sales doubled to EUR 175 million: now 10% of total (5%)Internet sales doubled to EUR 175 million: now 10% of total (5%)

• Many acquisitions of (smart) information tool companies Many acquisitions of (smart) information tool companies

• Portfolio reviews LTB Europe and North America concludedPortfolio reviews LTB Europe and North America concluded

• Professional Training sale almost completedProfessional Training sale almost completed

• Accounting for intangibles in line with new (IAS) standardsAccounting for intangibles in line with new (IAS) standards

• Outlook for 2001 reiterated: Ordinary Net Profit before Amortization of Outlook for 2001 reiterated: Ordinary Net Profit before Amortization of

Intangible Fixed Assets up approximately 5%, at constant currenciesIntangible Fixed Assets up approximately 5%, at constant currencies

Focus on Growing DifferentlyFocus on Growing Differently

3

SUMMARY FIGURES HY1-2001SUMMARY FIGURES HY1-2001• Single-digit sales growth, +7% (+5% at constant currencies)Single-digit sales growth, +7% (+5% at constant currencies)

• Organic sales growth 2%, due to modest market growth and product Organic sales growth 2%, due to modest market growth and product development lead-timedevelopment lead-time

• Doubling of profitable Internet sales; strong growth electronic salesDoubling of profitable Internet sales; strong growth electronic sales

• Again healthy flow of acquisitions, focused on (smart) information tool and Again healthy flow of acquisitions, focused on (smart) information tool and service companies, as well as electronic publishingservice companies, as well as electronic publishing

• EBITA growth -5% (-8% at constant currencies)EBITA growth -5% (-8% at constant currencies)

• Increased product development spending by operating companiesIncreased product development spending by operating companies

• No new provisions for reorganizationsNo new provisions for reorganizations

• Additional (Internet) product development investment: EUR 43 million (HY1-Additional (Internet) product development investment: EUR 43 million (HY1-2000: EUR 8 million)2000: EUR 8 million)

• Excluding additional (Internet) product development spending EBITA Excluding additional (Internet) product development spending EBITA +5% (+2% at constant currencies)+5% (+2% at constant currencies)

• Ordinary net income before amortization of intangible fixed assets on Ordinary net income before amortization of intangible fixed assets on track, at EUR 173 million (HY1-2000: EUR 191 million)track, at EUR 173 million (HY1-2000: EUR 191 million)

4

RESULTS HY1-2001RESULTS HY1-2001EUR millionEUR million HY1-2001HY1-2001 HY1-2000HY1-2000

Pro forma restatedPro forma restated**

Variance Variance

%%

SalesSales

EBITAEBITA

EBITA marginEBITA margin

1,8081,808

344344

19.0%19.0%

1,6901,690

362362

21.4%21.4%

77

(5)(5)

Amortization of intangiblesAmortization of intangibles (149)(149) (130)(130)

EBITEBIT 195195 232232 (16)(16)

Financing resultsFinancing results

Ordinary pre-tax income (after Ordinary pre-tax income (after amortization) amortization)

Taxation**Taxation**

(88)(88) (84)(84)

107107

(72)(72)

(1)(1)

148148

(78)(78)

(2)(2)

(28)(28)

Minority interestMinority interest

Ordinary net income (after amortization)Ordinary net income (after amortization) 3434 6868

Results on divestments (after taxation)Results on divestments (after taxation) 3030 00

Net incomeNet income 6464 6868 (6)(6)

Ordinary net income before amortization Ordinary net income before amortization of intangiblesof intangibles

173173 191191 (9)(9)

Ordinary EPS before amortization of Ordinary EPS before amortization of intangibles, fully dilutedintangibles, fully diluted

0.620.62 0.690.69 (10)(10)

** Restated f Restated for or aamortization of mortization of iintangiblesntangibles**** Pre-Pre-ttax preax pre-a-amortization effective tax rate 32.3% (HY1-2000: 30.4 %)mortization effective tax rate 32.3% (HY1-2000: 30.4 %)

• EBITA pre additional (Internet) spending: EBITA pre additional (Internet) spending: From -7% in HY1-2000 to -2%From -7% in HY1-2000 to -2%

• Modest organic EBITA decline LTB Europe compared with large Modest organic EBITA decline LTB Europe compared with large organic fall HY1-2000organic fall HY1-2000

• LTB North America matches organic EBITA and sales growthLTB North America matches organic EBITA and sales growth

• IHS sees organic EBITA under pressure, on balance causing IHS sees organic EBITA under pressure, on balance causing the 2% organic Wolters Kluwer EBITA declinethe 2% organic Wolters Kluwer EBITA decline

6

7

INTERNET AND OTHER ELECTRONIC SALES INTERNET AND OTHER ELECTRONIC SALES Half Year FiguresHalf Year Figures

2089

175

245

255

295

0

100

200

300

400

500

600

HY1-99 HY1-00 HY1-01

Other electronicsales

Internet sales

26%26%

20%20%

18%18%

Percentage figures represent electronic sales as part of total salesPercentage figures represent electronic sales as part of total sales

8

INTERNET AND OTHER ELECTRONIC SALES INTERNET AND OTHER ELECTRONIC SALES Full Year FiguresFull Year Figures

48228

350

504

582

670

0

200

400

600

800

1000

1200

FY-99 FY-00 FY-01E

Other electronicsales

Internet sales

26%26%

22%22%

18%18%

Percentage figures represent electronic sales as part of total salesPercentage figures represent electronic sales as part of total sales

9

SUCCESSFUL ACQUISITION PROGRAMSUCCESSFUL ACQUISITION PROGRAM

• Stronger focus on (smart) information tools Stronger focus on (smart) information tools Nearly allNearly all acquisitions are (smart) information tool companiesacquisitions are (smart) information tool companies

• High growth properties High growth properties Generally (smart) information tool companies have high organic growth; Generally (smart) information tool companies have high organic growth; margins at least in line with Wolters Kluwer averagemargins at least in line with Wolters Kluwer average

• Numerous affordable opportunities Numerous affordable opportunities Large pool of small and medium sized companies with strategic fit; Large pool of small and medium sized companies with strategic fit; multiples in line with traditional pricesmultiples in line with traditional prices

• Bringing new skills and competenciesBringing new skills and competencies

Increasingly High Growth (Smart) Information Tool CompaniesIncreasingly High Growth (Smart) Information Tool Companies

10

OUTCOME PORTFOLIO REVIEWS OUTCOME PORTFOLIO REVIEWS LTB Europe and LTB North AmericaLTB Europe and LTB North America• LTB Europe LTB Europe

• Focus on 6 core rather than 16 customer segments Focus on 6 core rather than 16 customer segments

• From country to matrix approach From country to matrix approach

• Implement new organization structure: customer segment facilitatorsImplement new organization structure: customer segment facilitators

• Harvest or divest non-core customer segmentsHarvest or divest non-core customer segments

• Divest ten Hagen & Stam Divest ten Hagen & Stam

• Improve operational excellence throughout clusterImprove operational excellence throughout cluster

• LTB North AmericaLTB North America

• Increase focus on legal & transaction compliance for the banking, Increase focus on legal & transaction compliance for the banking,

insurance and securities industries insurance and securities industries

• Accelerated expansion into (smart) information (productivity) tools Accelerated expansion into (smart) information (productivity) tools

• Discontinue Healthcare Administration Business (Aspen)Discontinue Healthcare Administration Business (Aspen)

Aimed at Sustainable GrowthAimed at Sustainable Growth

11

STRATEGIC FOUNDATIONS STRATEGIC FOUNDATIONS Five Business Principles - ProgressFive Business Principles - Progress

• Portfolio review: Portfolio review: e.g.e.g. LTB Europe and LTB North America concludedLTB Europe and LTB North America concluded

• (Smart) information tools: (Smart) information tools: e.g.e.g. Acquisition program on trackAcquisition program on track

• Fostering entrepreneurship: Fostering entrepreneurship: e.g.e.g. UpgradingUpgrading cluster management and incentives in progresscluster management and incentives in progress

• Operational excellence: Operational excellence: e.g. Improvinge.g. Improving customer relation management systems in progresscustomer relation management systems in progress

• Cluster management team installed and portfolio review concludedCluster management team installed and portfolio review concluded• Decision to focus on core customer segments accounting for some 75% Decision to focus on core customer segments accounting for some 75%

of sales, with sales growth target of 7%; margin target over 20% of sales, with sales growth target of 7%; margin target over 20% • Modest improvement organic sales growth, focus on operational Modest improvement organic sales growth, focus on operational

Netherlands (amongst others ten Hagen & Stam)Netherlands (amongst others ten Hagen & Stam)• Reorganizations in progress in notably the Netherlands, Belgium and Reorganizations in progress in notably the Netherlands, Belgium and

Spain Spain

Priority:Priority: Focus Resources on Growth AreasFocus Resources on Growth Areas

13

LEGAL, TAX & BUSINESS NORTH AMERICA: LEGAL, TAX & BUSINESS NORTH AMERICA: Strong Growth Internet SalesStrong Growth Internet Sales

• Electronic sales now 42% of total, Internet sales more than doubled to Electronic sales now 42% of total, Internet sales more than doubled to EUR 86 million, 15% of total sales EUR 86 million, 15% of total sales

• LIS growing strongly, despite slowing business formations and trademark LIS growing strongly, despite slowing business formations and trademark activitiesactivities

• Portfolio review: increased focus on compliance business for the banking, Portfolio review: increased focus on compliance business for the banking, insurance and securities industriesinsurance and securities industries

• Healthy flow of (smart information tool) acquisitions: Loislaw, CBF Healthy flow of (smart information tool) acquisitions: Loislaw, CBF Systems, and TSoftSystems, and TSoft

• Integration Loislaw progressing well: on track for FY-2001 EBITA break-Integration Loislaw progressing well: on track for FY-2001 EBITA break-even target even target

Priority:Priority: Extend Leading Market Position into Extend Leading Market Position into Smart Information Tools and ServicesSmart Information Tools and Services

LEGAL, TAX & BUSINESS ASIA PACIFIC: LEGAL, TAX & BUSINESS ASIA PACIFIC: Strong Growth CCH AsiaStrong Growth CCH Asia

• Sales of electronic products up 50%; Internet represents 13% of total salesSales of electronic products up 50%; Internet represents 13% of total sales• High organic growth of EBITA offset by negative currency impactHigh organic growth of EBITA offset by negative currency impact• Double-digit organic sales growth for CCH AsiaDouble-digit organic sales growth for CCH Asia

Priority: Priority: Further Expansion into AsiaFurther Expansion into Asia

EUR millionEUR million HY1-HY1-20012001

HY1-HY1-20002000

VarianceVariance OrganicOrganic

growthgrowth

Organic after Organic after InternetInternet

SalesSales 3131 3232 (3%)(3%) 0%0% 0%0%

EBITAEBITA 55 66 (16%)(16%) 11%11% (8%)(8%)

EBITA MarginEBITA Margin 17.5%17.5% 20.1%20.1%

FTE’s (average)FTE’s (average) 526526 484484

15

INTERNATIONAL HEALTH & SCIENCE:INTERNATIONAL HEALTH & SCIENCE:Addressing Performance Immediate Priority Addressing Performance Immediate Priority

• Organic growth held back by LWW, in part due to bankruptcy of Organic growth held back by LWW, in part due to bankruptcy of wholesaler in second half of 2000wholesaler in second half of 2000

• Acquisition of SilverPlatter (June 2001) further enhances Ovid’s leading Acquisition of SilverPlatter (June 2001) further enhances Ovid’s leading position as provider of databases and research tools for the medical and position as provider of databases and research tools for the medical and academic marketsacademic markets

• Decision on single electronic delivery platform takenDecision on single electronic delivery platform taken• Selective allocation of resources aimed at growth and electronic leverageSelective allocation of resources aimed at growth and electronic leverage

Priority:Priority: Acceleration of Electronic Delivery Acceleration of Electronic Delivery of Content and Software Toolsof Content and Software Tools

EDUCATION: EDUCATION: Netherlands and Sweden Doing WellNetherlands and Sweden Doing Well

• High seasonality both in sales and costsHigh seasonality both in sales and costs• Strong performance in the Netherlands and Sweden, with favorable Strong performance in the Netherlands and Sweden, with favorable

phasing towards the first half-yearphasing towards the first half-year• Now ready to move forward with reorganization of Swedish operation, Now ready to move forward with reorganization of Swedish operation,

• Much more favorable movements of organic working capitalMuch more favorable movements of organic working capital• Favorable changes in inventories and debtors, and deferred incomeFavorable changes in inventories and debtors, and deferred income

19

SUMMARYSUMMARY

• Benchmark results consistent with full year 2001 forecastBenchmark results consistent with full year 2001 forecast

• Continued focus on creating conditions sustainable double-digit growthContinued focus on creating conditions sustainable double-digit growth

• Electronic sales targeted to end 2001 above EUR 1 billionElectronic sales targeted to end 2001 above EUR 1 billion

• Internet sales expected to end 2001 at approximately EUR 350 millionInternet sales expected to end 2001 at approximately EUR 350 million

• LTB Europe now focused on implementation of new strategyLTB Europe now focused on implementation of new strategy

• IHS improving managerial execution and tightening strategic visionIHS improving managerial execution and tightening strategic vision

• More acquisitions of (smart) information tool companies More acquisitions of (smart) information tool companies

• Professional Training sale to be completed in HY2-2001 (ROVC) and Professional Training sale to be completed in HY2-2001 (ROVC) and

2002 (ISBW)2002 (ISBW)

Focus on Growing DifferentlyFocus on Growing Differently

20

OUTLOOK 2001: UNCHANGEDOUTLOOK 2001: UNCHANGEDOn Track to Achieve On Track to Achieve ± ± 5% Increase Benchmark 5% Increase Benchmark Profit despite Challenging Market Conditions Profit despite Challenging Market Conditions

• Additional investment EUR 100 millionAdditional investment EUR 100 millionFully expensed additional (Internet) product development investment will Fully expensed additional (Internet) product development investment will more than double to some EUR 100 millionmore than double to some EUR 100 million

• Benchmark profit up approximately 5%Benchmark profit up approximately 5%Ordinary net income before amortization of intangible fixed assets to Ordinary net income before amortization of intangible fixed assets to increase approximately 5%, at constant currenciesincrease approximately 5%, at constant currencies

• Growth in 2Growth in 2ndnd half halfGrowth weighted towards second half of 2001 due to phasing effect of Growth weighted towards second half of 2001 due to phasing effect of additional (Internet) product development investmentsadditional (Internet) product development investments

• (Smart) information tool and electronic publishing companies(Smart) information tool and electronic publishing companies• For example Loislaw, CBF Systems, TSoft, Compliance International, For example Loislaw, CBF Systems, TSoft, Compliance International,

and SilverPlatterand SilverPlatter

23

MOST IMPORTANT ACQUISITIONS MOST IMPORTANT ACQUISITIONS IN HY1-2001IN HY1-2001

Legal Tax & Business Legal Tax & Business North AmericaNorth America

CompanyCompany ActivityActivity Annual Sales (EUR m)Annual Sales (EUR m)

LoislawLoislaw Online provider ofOnline provider of

comprehensive legal comprehensive legal

informationinformation

2323

CBF SystemsCBF Systems Mortgage products for Mortgage products for financial services industryfinancial services industry

2626

TSoftTSoft Lending softwareLending software 44

Compliance InternationalCompliance International Electronic regulatory Electronic regulatory information for financial information for financial services industryservices industry

44

International Health & International Health & ScienceScience

Total electronicTotal electronic 100%100% 470470 344344 37%37%

Overview Internet salesOverview Internet sales EUR millionEUR million % of cluster (HY1 2000)% of cluster (HY1 2000)LTB Europe LTB Europe 32 32 5% 5% (3%)(3%)LTB North AmericaLTB North America 8686 15% 15% (7%)(7%)LTB Asia PacificLTB Asia Pacific 44 13%13% (0%)(0%)International Health and ScienceInternational Health and Science 5151 13%13% (9%)(9%)EducationEducation 2 2 2%2% (1%)(1%)

Total printTotal print 100%100% 1,3001,300 1,2711,271 2%2%

27

ADDITIONAL (INTERNET) PRODUCT ADDITIONAL (INTERNET) PRODUCT DEVELOPMENT INVESTMENTSDEVELOPMENT INVESTMENTS

Breakdown by ClusterBreakdown by Cluster

EUR millionEUR million

HY1-2001HY1-2001 HY1-2000HY1-2000

Legal, Tax & Business EuropeLegal, Tax & Business Europe 1010 44

Legal, Tax & Business North AmericaLegal, Tax & Business North America 2121 22

Legal, Tax & Business Asia PacificLegal, Tax & Business Asia Pacific 11 ----

International Health & ScienceInternational Health & Science 99 22

EducationEducation 22 ----

TOTALTOTAL 4343 88

28

CLUSTER BREAKDOWN SALES CLUSTER BREAKDOWN SALES 2000 And HY1-20012000 And HY1-2001

Breakdown by ClusterBreakdown by Cluster SALES SALES

EUR millionEUR million

HY1-HY1-20012001

HY1-HY1-20002000

FY-FY-20002000

Legal, Tax & Business EuropeLegal, Tax & Business Europe 658658 624624 1,3161,316

Legal, Tax & Business North Legal, Tax & Business North AmericaAmerica

584584 505505 1,0931,093

Legal, Tax & Business Asia PacificLegal, Tax & Business Asia Pacific 3131 3232 6060

International Health & ScienceInternational Health & Science 382382 339339 752752

EducationEducation 115115 113113 311311

Professional TrainingProfessional Training 3838 7777 132132

TOTALTOTAL 1,8081,808 1,6901,690 3,6643,664

29

CLUSTER BREAKDOWN EBITA CLUSTER BREAKDOWN EBITA 2000 And HY1-20012000 And HY1-2001

Breakdown by ClusterBreakdown by Cluster EBITA EBITA

EUR millionEUR million

HY1-HY1-20012001

HY1-HY1-20002000

FY FY 20002000

Legal, Tax & Business EuropeLegal, Tax & Business Europe 119119 121121 237237

Legal, Tax & Business North AmericaLegal, Tax & Business North America 147147 146146 333333

Legal, Tax & Business Asia PacificLegal, Tax & Business Asia Pacific 55 66 1212

International Health & ScienceInternational Health & Science 7575 8080 179179

EducationEducation 77 1212 5454

Professional TrainingProfessional Training 33 1010 1111

CorporateCorporate -12-12 -13-13 -37-37

TOTALTOTAL 344344 362362 789789

30

BREAKDOWN SALES GROWTH BREAKDOWN SALES GROWTH 2000 And HY1-20012000 And HY1-2001

HY1-HY1-20012001

HY1-HY1-20002000

FY 2000FY 2000

OrganicOrganic 2%2% 4%4% 5%5%

AcquisitionsAcquisitions 5%5% 9%9% 8%8%

DivestmentsDivestments (2%)(2%) (2%)(2%) (1%)(1%)

Total Constant RatesTotal Constant Rates 5%5% 11%11% 12%12%

CurrenciesCurrencies 2%2% 7%7% 7%7%

Total Total 7%7% 18%18% 19%19%

31

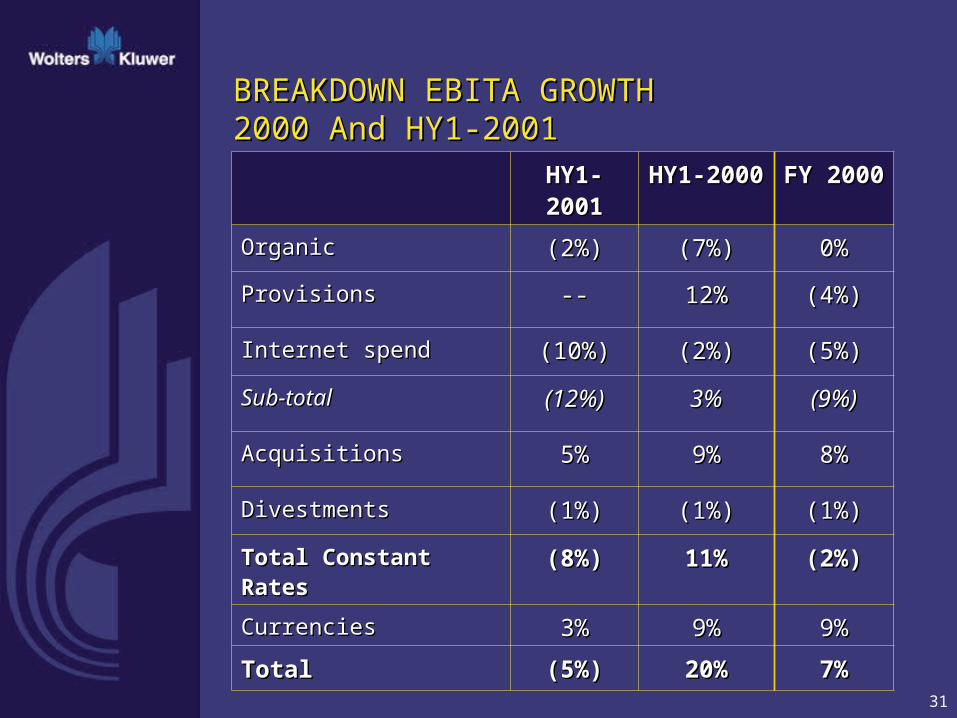

BREAKDOWN EBITA GROWTH BREAKDOWN EBITA GROWTH 2000 And HY1-20012000 And HY1-2001

HY1-2001HY1-2001 HY1-2000HY1-2000 FY 2000FY 2000

OrganicOrganic (2%)(2%) (7%)(7%) 0%0%

ProvisionsProvisions ---- 12%12% (4%)(4%)

Internet spendInternet spend (10%)(10%) (2%)(2%) (5%)(5%)

Sub-totalSub-total (12%)(12%) 3%3% (9%)(9%)

AcquisitionsAcquisitions 5%5% 9%9% 8%8%

DivestmentsDivestments (1%)(1%) (1%)(1%) (1%)(1%)

Total Constant RatesTotal Constant Rates (8%)(8%) 11%11% (2%)(2%)

CurrenciesCurrencies 3%3% 9%9% 9%9%

Total Total (5%)(5%) 20%20% 7%7%

32

CHARACTERISTICS OF BUSINESSCHARACTERISTICS OF BUSINESS

• Growth orientedGrowth orientedDouble-digit sales growth in each of past five years; sales tripled since 1994Double-digit sales growth in each of past five years; sales tripled since 1994

• Geographic diversificationGeographic diversificationBusiness is geographically balanced with activities in three continentsBusiness is geographically balanced with activities in three continents

• Local play, global leverageLocal play, global leverageOften local information markets served by local operating companies, yet capitalizing on Often local information markets served by local operating companies, yet capitalizing on global scaleglobal scale

• Focus on professionalsFocus on professionalsClearly defined portfolio, fully focused on professional customer groupsClearly defined portfolio, fully focused on professional customer groups

• Need-To-KnowNeed-To-KnowThe company has a strong base of proprietary and copyrighted content and tools (approx. The company has a strong base of proprietary and copyrighted content and tools (approx. 75% of sales) that are crucial (need-to-know) for professionals in their work75% of sales) that are crucial (need-to-know) for professionals in their work

• Strong subscription baseStrong subscription baseMore than 50% of sales is subscription based (prepaid), and we have established a loyal More than 50% of sales is subscription based (prepaid), and we have established a loyal customer basecustomer base

• Well-established brandsWell-established brandsWe own some of the oldest and longest established, and most respected brands in our We own some of the oldest and longest established, and most respected brands in our markets that represent core values such as authority, quality, reliability and trustmarkets that represent core values such as authority, quality, reliability and trust

• Almost Recession proofAlmost Recession proofStrong subscription base, need-to-have services, low dependency on advertisingStrong subscription base, need-to-have services, low dependency on advertising

33

SMART INFORMATION TOOLSSMART INFORMATION TOOLS

• Focus investment on smart information tools:Focus investment on smart information tools: Leverage content with software and servicesLeverage content with software and services

• InformationInformation: : Content and knowledge about a specific field (tax, medicine, Content and knowledge about a specific field (tax, medicine, law etc.) is embedded in all products and serviceslaw etc.) is embedded in all products and services

• ToolsTools: : ‘Something regarded as necessary to the carrying out of ‘Something regarded as necessary to the carrying out of one's occupation or profession’; essentialone's occupation or profession’; essential

Extend Leading Content Positions into Extend Leading Content Positions into Smart information Tools and ServicesSmart information Tools and Services

• In past no amortization requirement In past no amortization requirement

• New standards assume economic life of 20 years (unless compelling grounds point to New standards assume economic life of 20 years (unless compelling grounds point to more, up to 40 years) more, up to 40 years)

• Retrospective amortization charge against shareholders’ equity: EUR 451 millionRetrospective amortization charge against shareholders’ equity: EUR 451 million

• Amortization through P&L: HY1-2001 EUR 42 million chargeAmortization through P&L: HY1-2001 EUR 42 million charge

• Goodwill Goodwill • Until 2000 amortized over average period of 33 years Until 2000 amortized over average period of 33 years

• New standards assume economic life of 20 years (unless compelling grounds point to New standards assume economic life of 20 years (unless compelling grounds point to more, up to 40 years) more, up to 40 years)

• No retrospective charge, but increased prospective chargeNo retrospective charge, but increased prospective charge

• Amortization through P&L: HY1-2001 EUR 107 million chargeAmortization through P&L: HY1-2001 EUR 107 million charge

• If already applied in 2000, goodwill amortization charge would have been If already applied in 2000, goodwill amortization charge would have been

EUR 193 million compared with EUR 121 million reportedEUR 193 million compared with EUR 121 million reported

• ImpairmentImpairment• New standards prescribe stricter measures for valuing intangible assetsNew standards prescribe stricter measures for valuing intangible assets

• One-off correction of EUR 162 million (3% of total intangibles) against shareholders’ equityOne-off correction of EUR 162 million (3% of total intangibles) against shareholders’ equity

• Possible future corrections to be charged through P&LPossible future corrections to be charged through P&L

Wolters KluwerWolters Kluwer

Half Year Results 2001Half Year Results 2001

Rob Pieterse, Chairman of the Executive BoardRob Pieterse, Chairman of the Executive Board

Analysts & Investors, August 2001Analysts & Investors, August 2001