33

working capital a source of financing for growth Amsterdam, June3rd. 2014 Budapest, October 16 2014 Jan Schets D.E. Master Blenders 1753

working capital a source of financing for growth

Amsterdam, June3rd. 2014

Budapest, October 16 2014

Jan Schets

D.E. Master Blenders 1753

Agenda

Company

Snapshot OWC Project Key Learnings

The Role of SCF

in the OWC Q&A Intro on SCF

2

Company Snapshot

We are a leading, focused pure-play coffee and tea company with operations across Europe, Brazil, Australia and Thailand.

72% of our sales are generated from markets where we have a Number 1 or Number 2 position.

2

Note: 72% is total company sales in countries where D.E MASTER BLENDERS has a number 1 or 2 position in retail coffee.

3

We have strong local brands

3

France Spain Australia Brazil

NL & BE Global Hungary

Denmark

Global Norway

4

2013: € 2,5 bln

29%

Brazil 17%

France 13%

Belgium 7%

Germany 6%

Australia 6%

Spain 6%

Other 16%

Netherlands

4

Other includes New Zealand, Norway, Denmark, Poland, Thailand, Greece, Hungary, Czech Rep, UK

Our sales split by geography

5

Roast & Ground

6

Senseo

7

Capsules

8

Tea

9

Intended JV with Mondelez announced

Announced on May 7th

To become the world’s leading

pure-play coffee company

JV:

Mondelez #2 sales €2.9 bln 49%

DEMB #3 sales €2.5 bln 51%

JV #2 sales €5.4 bln 100%

Merger is complimentary in regions and in

coffee expertise.

Many 1st and 2nd positions in key markets

10

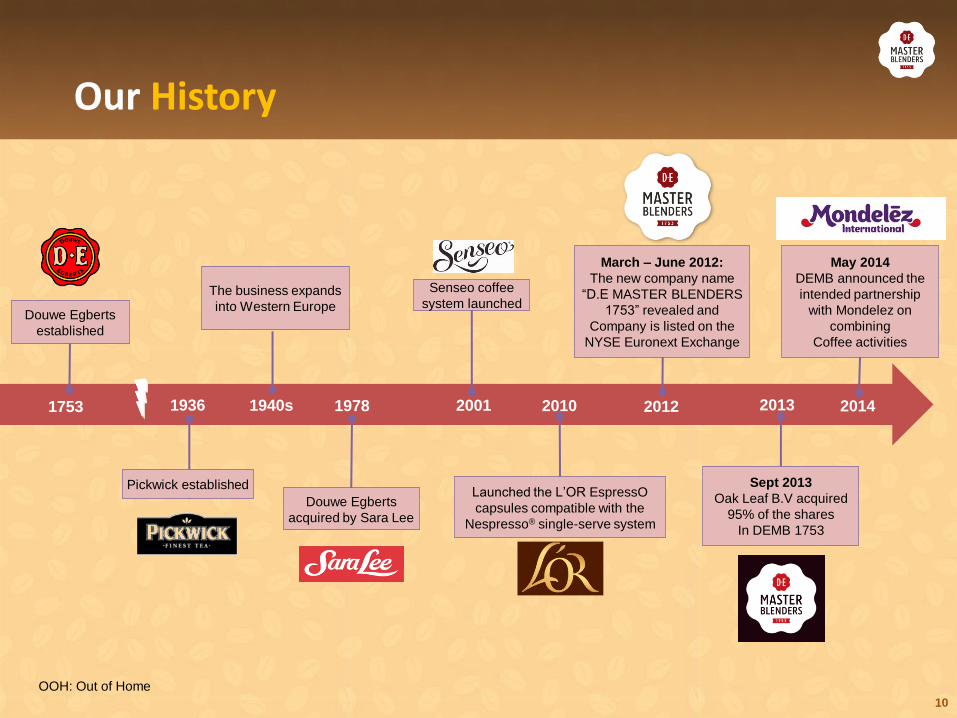

Our History

1936 1940s 1978 2012 1753 2001

Pickwick established

Senseo coffee

system launched

March – June 2012:

The new company name

“D.E MASTER BLENDERS

1753” revealed and

Company is listed on the

NYSE Euronext Exchange

2010

Launched the L’OR EspressO

capsules compatible with the

Nespresso® single-serve system

OOH: Out of Home

Douwe Egberts

established

The business expands

into Western Europe

Douwe Egberts

acquired by Sara Lee

2013

Sept 2013

Oak Leaf B.V acquired

95% of the shares

In DEMB 1753

2014

May 2014

DEMB announced the

intended partnership

with Mondelez on

combining

Coffee activities

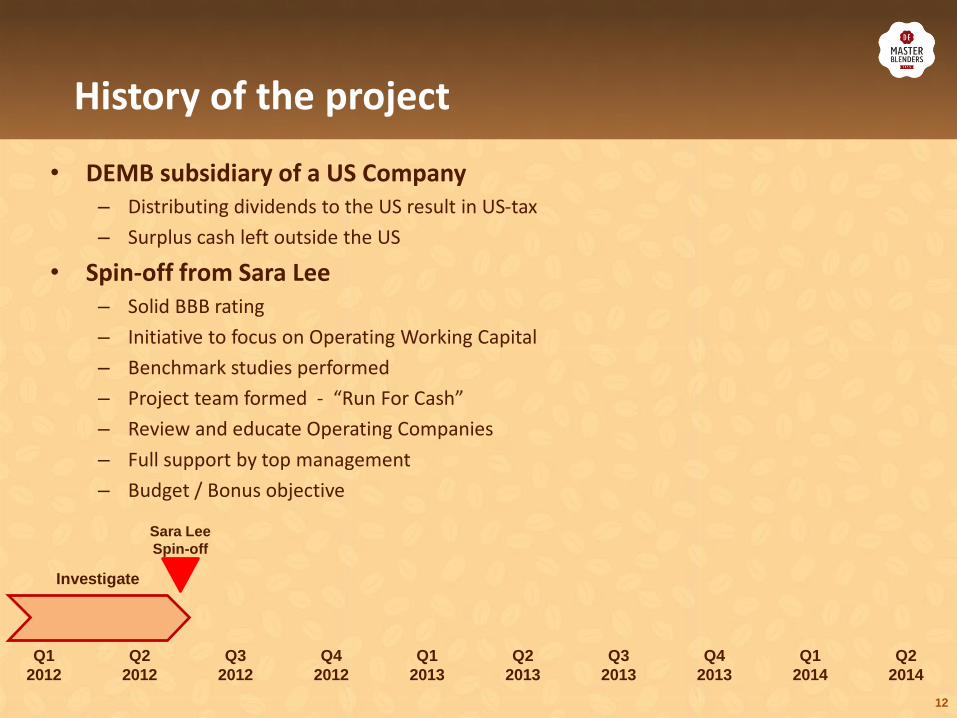

Operating Working Capital project

12

• DEMB subsidiary of a US Company – Distributing dividends to the US result in US-tax

– Surplus cash left outside the US

• Spin-off from Sara Lee – Solid BBB rating

– Initiative to focus on Operating Working Capital

– Benchmark studies performed

– Project team formed - “Run For Cash”

– Review and educate Operating Companies

– Full support by top management

– Budget / Bonus objective

History of the project

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2012 2012 2012 2012 2013 2013 2013 2013 2014 2014

Investigate

Sara Lee

Spin-off

13

Improving Working Capital

• Reduce Inventory

• Improve central coordination of green coffee inventory

• Inventory financing schemes

• Reduce Accounts Receivable

• Improve the A/R operational process

• More active credit management

• Managing discounts

• Extend Accounts Payables

• General extension of payment terms

• Active approach of procurement department

• Implement Supply Chain Financing

14

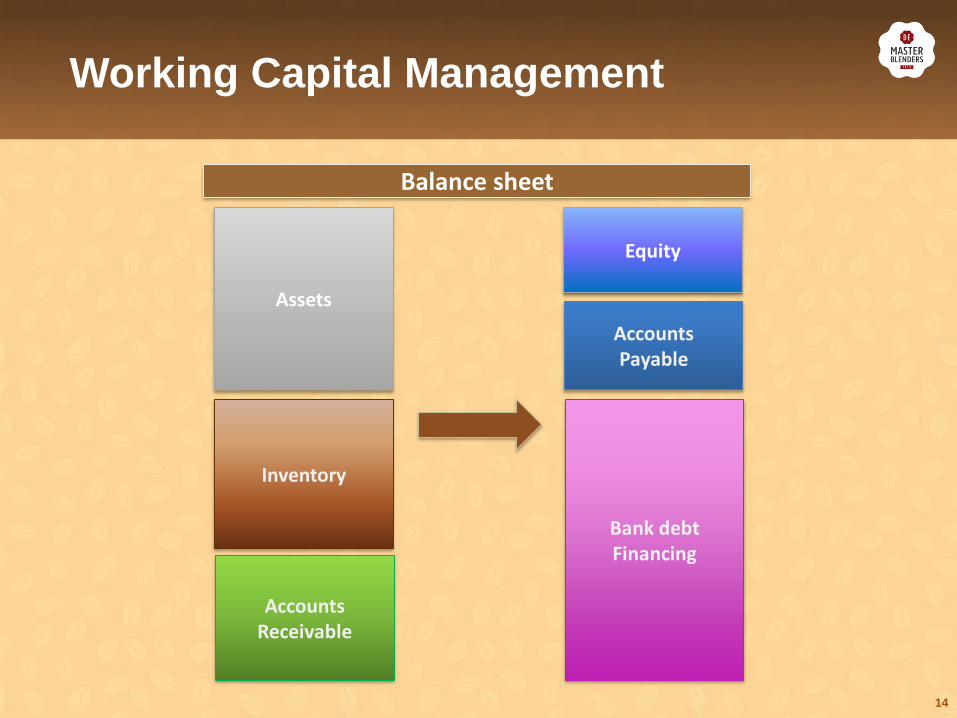

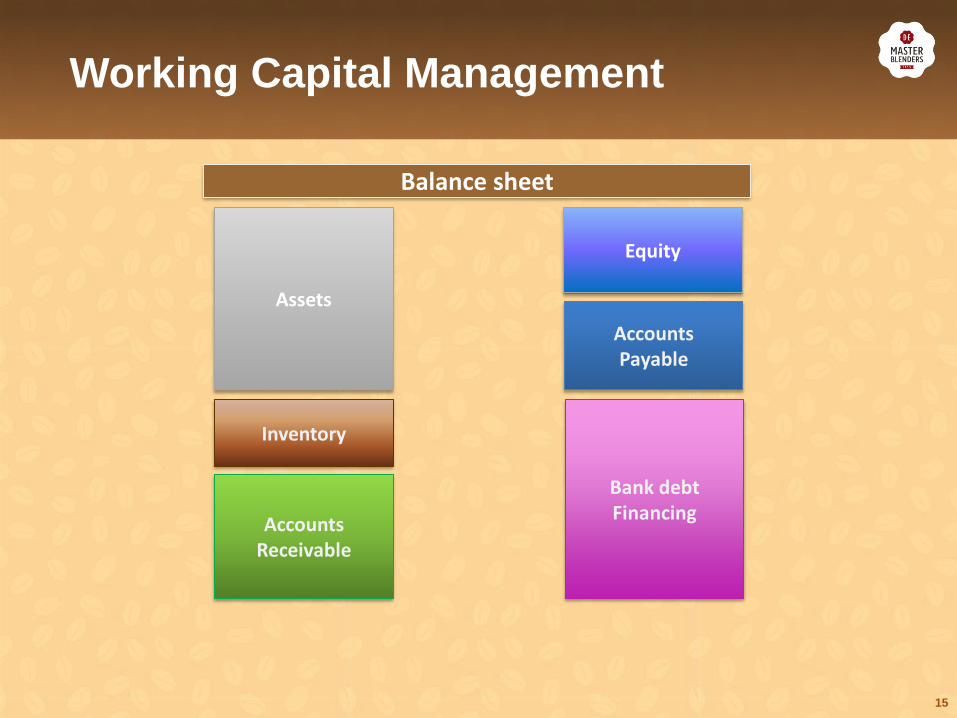

Working Capital Management

Balance sheet

Assets

Accounts Receivable

Equity

Accounts Payable

Bank debt Financing

Inventory

15

Balance sheet

Assets

Accounts Receivable

Equity

Accounts Payable

Bank debt Financing

Inventory

Working Capital Management

16

Balance sheet

Accounts Receivable

Equity

Accounts Payable

Bank debt Financing

Assets

Inventory

Working Capital Management

17

Balance sheet

Accounts Receivable

Equity

Accounts Payable

Bank debt Financing

Assets

Inventory

Working Capital Management

18

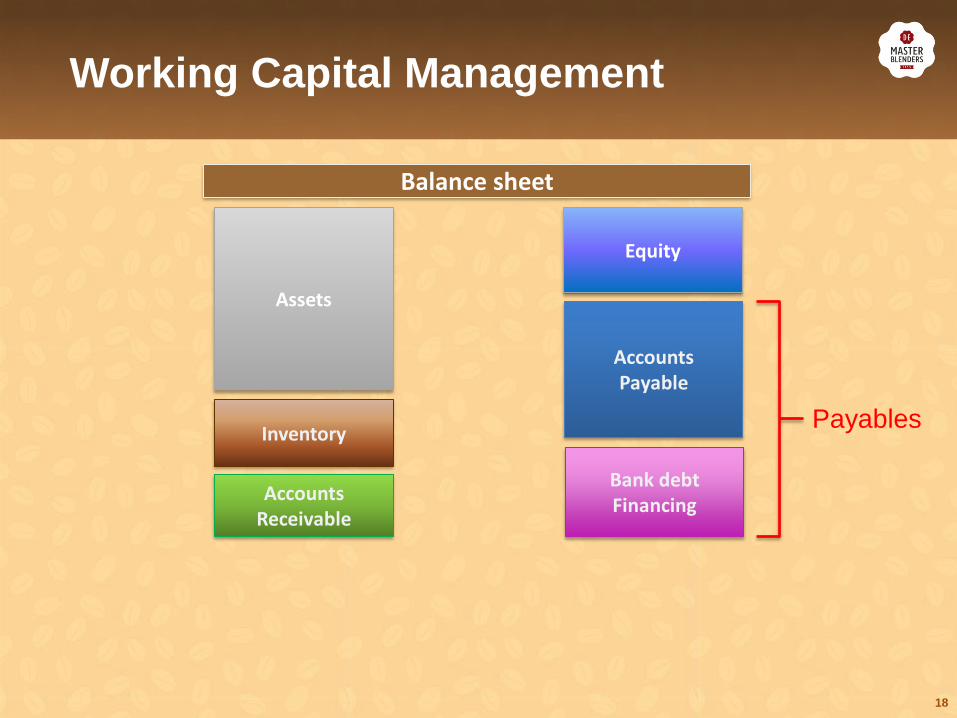

Balance sheet

Accounts Receivable

Equity

Accounts Payable

Bank debt Financing

Payables

Assets

Inventory

Working Capital Management

The role of SCF in OWC

20

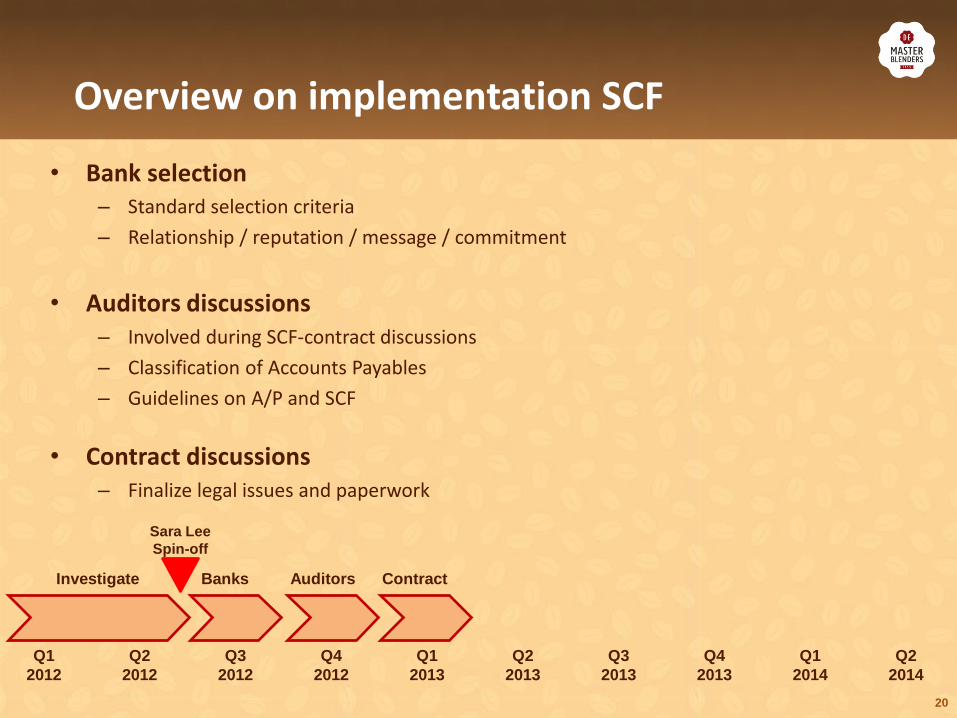

Overview on implementation SCF

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2012 2012 2012 2012 2013 2013 2013 2013 2014 2014

Investigate Banks Auditors Contract

Sara Lee

Spin-off

• Bank selection – Standard selection criteria

– Relationship / reputation / message / commitment

• Auditors discussions – Involved during SCF-contract discussions

– Classification of Accounts Payables

– Guidelines on A/P and SCF

• Contract discussions – Finalize legal issues and paperwork

21

Overview on implementation SCF

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2012 2012 2012 2012 2013 2013 2013 2013 2014 2014

Investigate Banks Auditors Contract Suppliers Go Live

Sara Lee

Spin-off

JAB led

acquisition

• SCF made available to suppliers – Training of procurement team

– Mixed reception

• Going live – Start small

– Alignment operational and payment procedures

– IT-systems

• JAB led acquisition of DEMB – Acquisition debt push-down; credit rating BB- / B+

– Impact on SCF-program

22

• Leverage = Debt / EBITDA

• Leverage DEMB = 3,000 / 500 = 6

7

6

5

4

3

2

1

2013 2014 2015 2016

Leverage post JAB acquisition (illustrative example)

AA

A BBB

BB

BB

B B

Plan DEMB

Max. allowed by banks

23

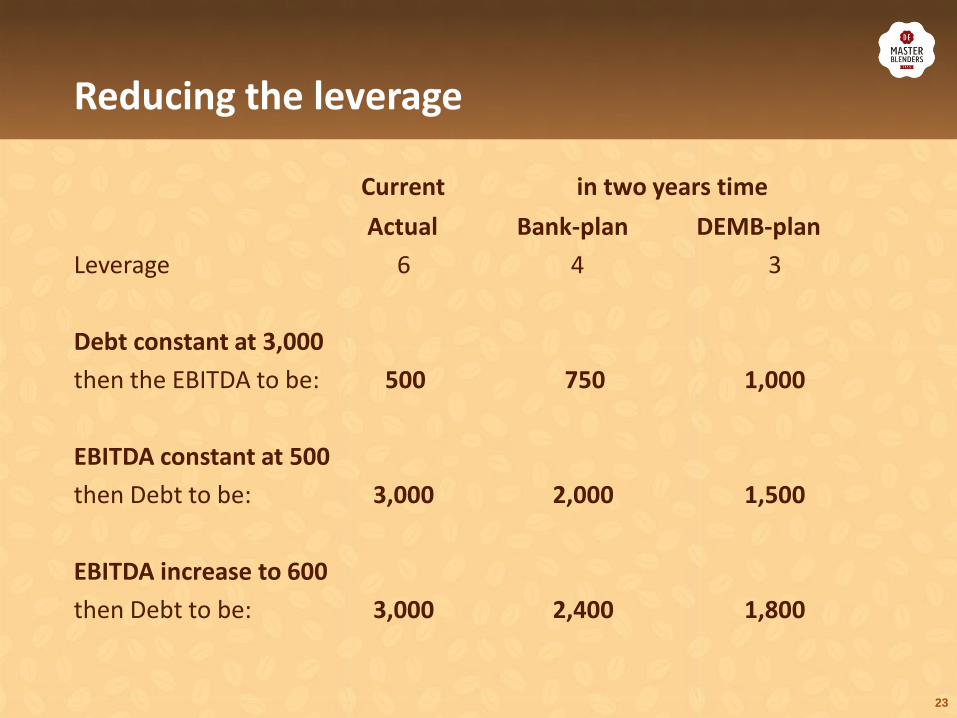

Reducing the leverage

Current in two years time

Actual Bank-plan DEMB-plan

Leverage 6 4 3

Debt constant at 3,000

then the EBITDA to be: 500 750 1,000

EBITDA constant at 500

then Debt to be: 3,000 2,000 1,500

EBITDA increase to 600

then Debt to be: 3,000 2,400 1,800

24

Reducing the leverage

Why:

• Requirement of the banks

• To become an Investment Grade (BBB) company – Optimal for DEMB Cost of Capital

– Better access to financing

– Lower cost of funding (debt & accounts payable)

– Lighter debt documentation

25

Reducing the leverage

Conclusion:

reduction in the leverage can be achieved by:

• Create more income • To be achieved by higher sales / lower costs

• Results in higher EBITDA

• Lower bank debt • Which can be achieved by:

– Using the cash from the realized profits

– Working Capital Management

– Alternative financing of investments

26

Overview on implementation SCF

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2012 2012 2012 2012 2013 2013 2013 2013 2014 2014

Investigate Banks Auditors Contract Suppliers Life Roll-out Co-funding

Sara Lee

Spin-off

JAB led

acquisition

• Roll-out of SCF program – Adding more group companies

– Including remote suppliers

• Co-funding – Include other bank in the SCF-program

– Access to growth

– Diversification

27

• Use SCF wisely!

– Available to help key suppliers

– Diversify funding risk via co-funding by other banks

– Maintain financial headroom to absorb the ending of a SCF program

– SCF is one of the tools to improve OWC

Use of SCF

Key learnings

29

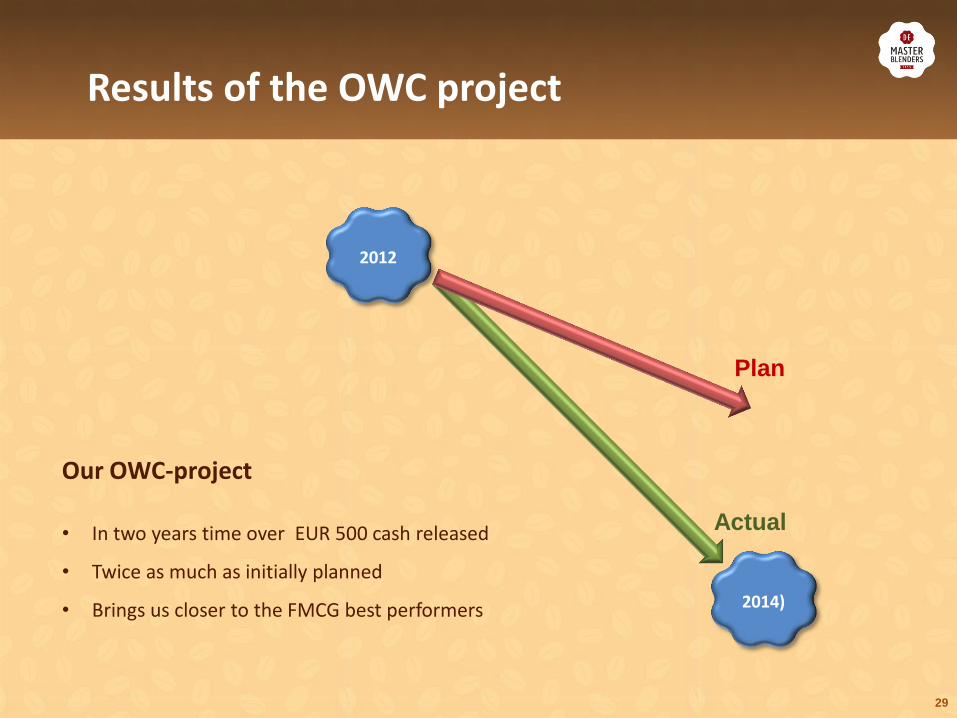

Results of the OWC project

2012

2014)

Our OWC-project

• In two years time over EUR 500 cash released

• Twice as much as initially planned

• Brings us closer to the FMCG best performers

Plan

Actual

30

• Commitment from the top

• Awareness within the organisation

• Focus focus focus

– Reporting and visibility

– monthly monitoring

– kpi´s

• Alignment and team effort

• Dedicated team and resources

Key success factors for OWC

31 31

Is treasury in the driving seat?

Thank you all