22

Workshop on TDS and e- filing of TDS returns K Brahmanayagam FCA

| Date post: | 14-Dec-2015 |

| Category: |

Documents |

| Upload: | malakai-jakeway |

| View: | 244 times |

| Download: | 0 times |

Workshop on TDS and e-filing of TDS returns

K Brahmanayagam FCA

Legal provisions

The scheme of tax deduction at source (TDS) is such that, persons responsible for making payment of income, are responsible to deduct tax at the prescribed percentage and deposit the same to the Central Government’s account within the stipulated time.

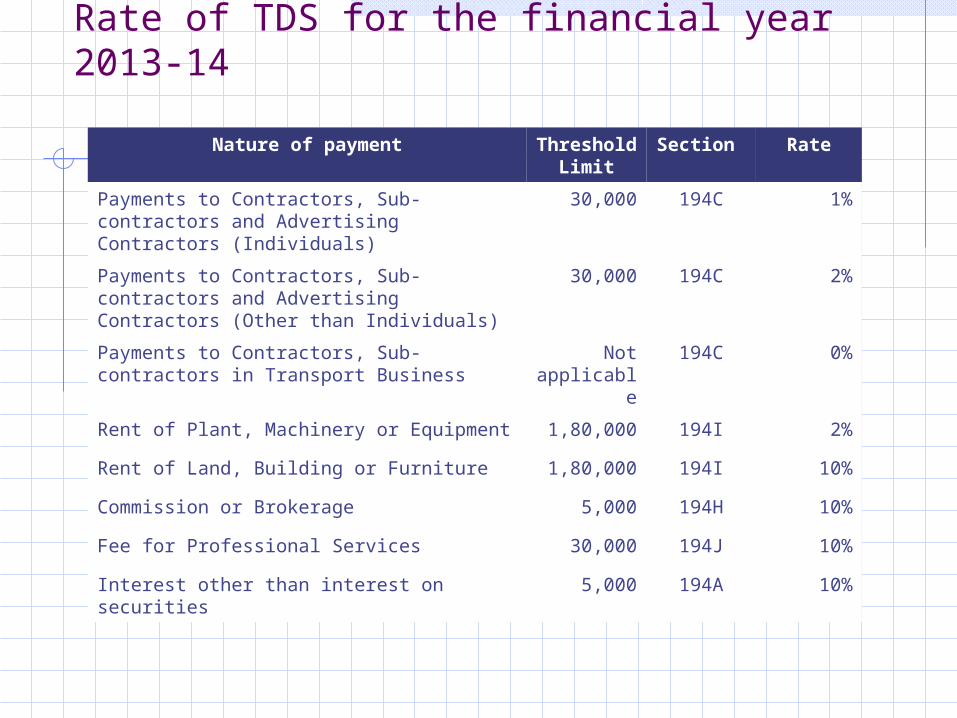

Rate of TDS for the financial year 2013-14

Nature of payment Threshold

Limit

Section Rate

Payments to Contractors, Sub-contractors and Advertising Contractors (Individuals)

30,000 194C 1%

Payments to Contractors, Sub-contractors and Advertising Contractors (Other than Individuals)

30,000 194C 2%

Payments to Contractors, Sub-contractors in Transport Business

Not applicable

194C 0%

Rent of Plant, Machinery or Equipment 1,80,000 194I 2%

Rent of Land, Building or Furniture 1,80,000 194I 10%

Commission or Brokerage 5,000 194H 10%

Fee for Professional Services 30,000 194J 10%

Interest other than interest on securities 5,000 194A 10%

Rate of TDS for the financial year 2013-14

Notes: • Threshold limit of Rs. 30000/- is for single payment and TDS will be NIL

if the annual payment is less than Rs. 75000/-, if Payments to Contractors, Sub-contractors and Advertising Contractors (Individuals).

• If the recipient does not furnish his PAN to the deductor, tax has to be deducted at the rate of 20%.

• Section 194C are applicable only where contract is either a WORKS CONTRACT or a CONTRACT FOR SUPPLY OF LABOUR FOR WORKS CONTRACT. Section 194C is not applicable to the contract for sale of goods.

• Time of deposit of TDS/TCS Where the income or amount is paid or credited in the month of March –

April 30 Where the income or amount is paid or credited before March 1 – within 7

days from the end of the month in which tax is deducted

Rate of TDS for the financial year 2013-14

Notes: Consequences for failure:

Fails to deduct/collect Interest at 1% pm from the date on which tax was deductible to the date of actual deduction

Fails to pay after deduction

Interest at 1.50% pm from the date on which tax was actually deducted to the date of actual payment

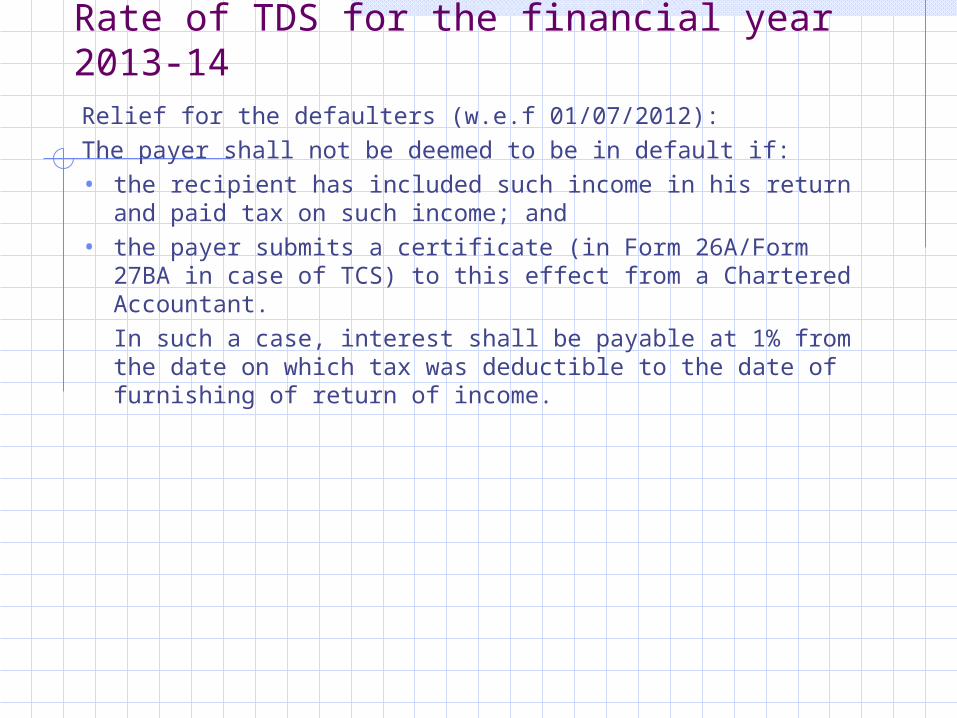

Rate of TDS for the financial year 2013-14Relief for the defaulters (w.e.f 01/07/2012):The payer shall not be deemed to be in default if:• the recipient has included such income in his return and

paid tax on such income; and• the payer submits a certificate (in Form 26A/Form 27BA in

case of TCS) to this effect from a Chartered Accountant.In such a case, interest shall be payable at 1%

from the date on which tax was deductible to the date of furnishing of return of income.

Quarterly statement of tax deduction/collection

Particulars Form No

Tax deduction from salary u/s. 192 24Q

Tax deduction from the payments to non-resident 27Q

Tax deduction in any other case 26Q

Tax collection 27EQ

Notes: Where an employee has worked with a deductor for part of the financial year only, the deductor should deduct tax at source from his salary and report the same in the quarterly statement of the respective quarters up to the date of employment with him. While submitting Form no. 24Q4, the deductor should include particulars of that employee in Annexure II & III irrespective of the fact that the employee was not under his employment on the last day of the year.Similarly, where an employee joins employment with deductor during the course of the financial year, his particulars should be reported by the current deductor in Form 24Q of the relevant quarter. Further, while submitting Form No. 24Q for the last quarter, the deductor should include particulars of such employee for the actual period of employment under him in Annexure II & III

Quarterly statement of tax deduction/collection

Quarter ending Due date of submission of quarterly TDS/TCS returns

June 30 July 15

September 30 October 15

December 31 January 15

March 31 May 15 of the following financial year

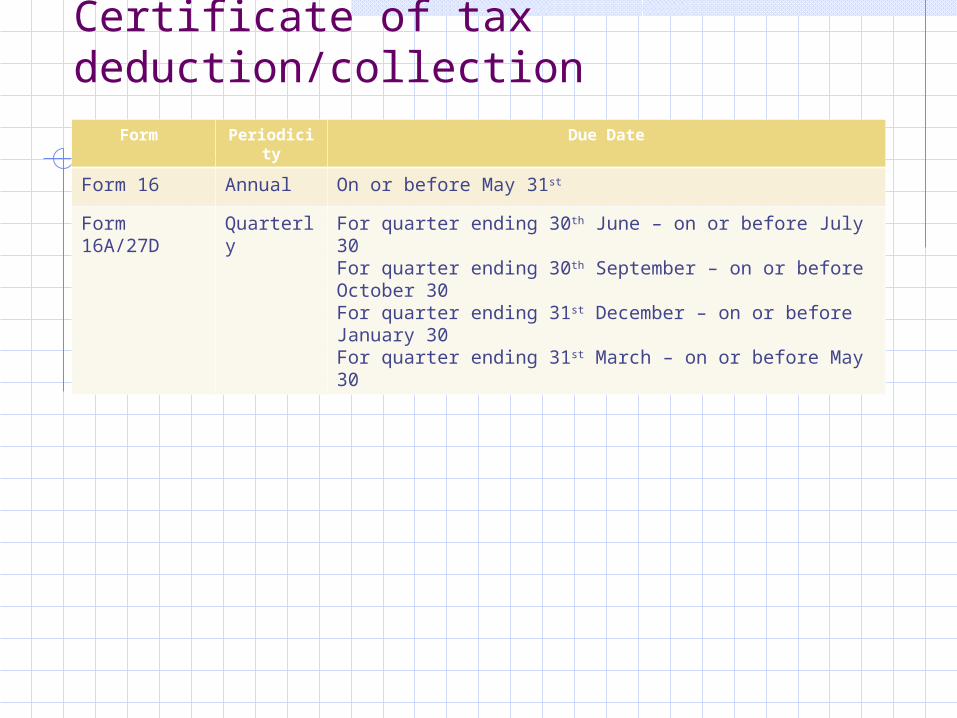

Certificate of tax deduction/collection

Form Periodicity

Due Date

Form 16 Annual On or before May 31st

Form 16A/27D

Quarterly For quarter ending 30th June – on or before July 30For quarter ending 30th September – on or before October 30For quarter ending 31st December – on or before January 30For quarter ending 31st March – on or before May 30

How to prepare quarterly returnsGo to the site www.tin.nsdl.com

Select e-TDS/TCS Filing:

Select e-TDS/TCS RPU:

Save that to your computer (in Program files):

Click on e-TDS/TCS RPU.exe (Version 3.80):

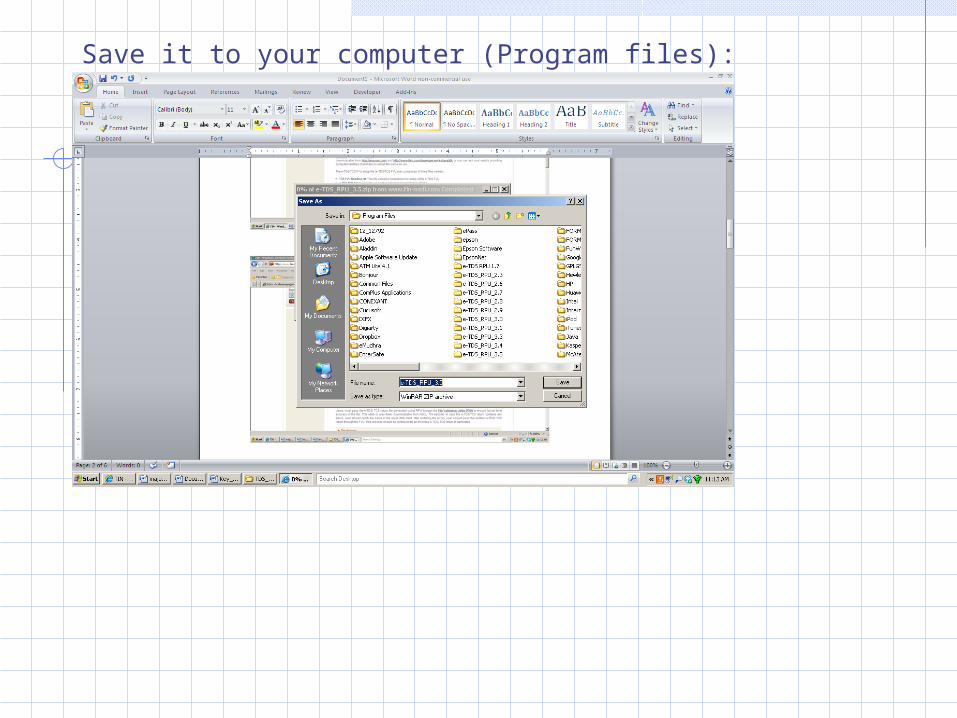

Save it to your computer (Program files):

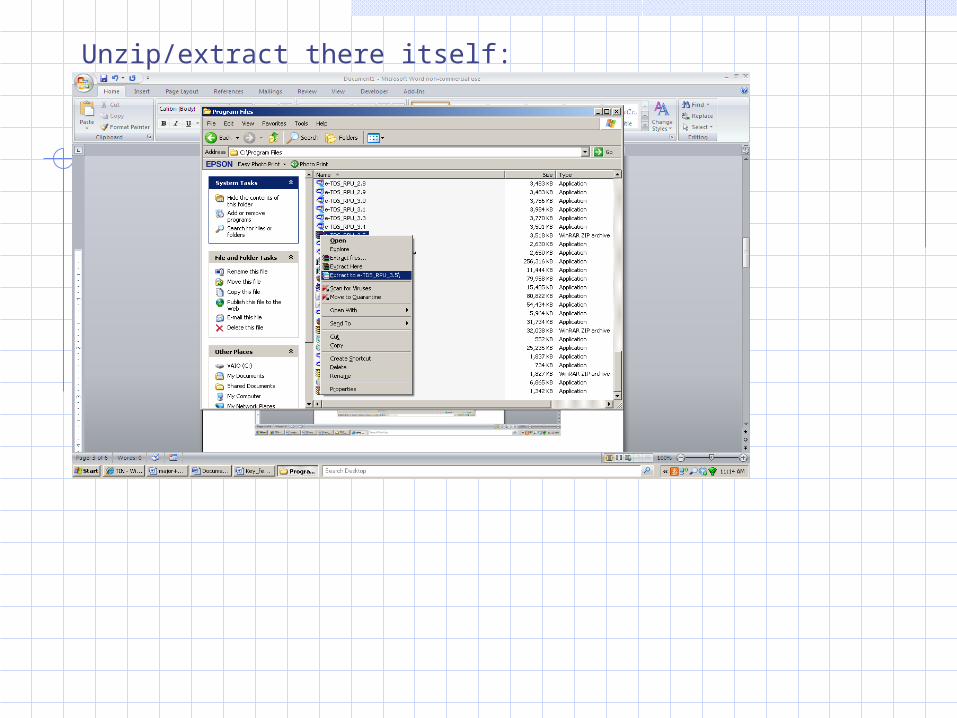

Unzip/extract there itself:

Go to that extracted folder:

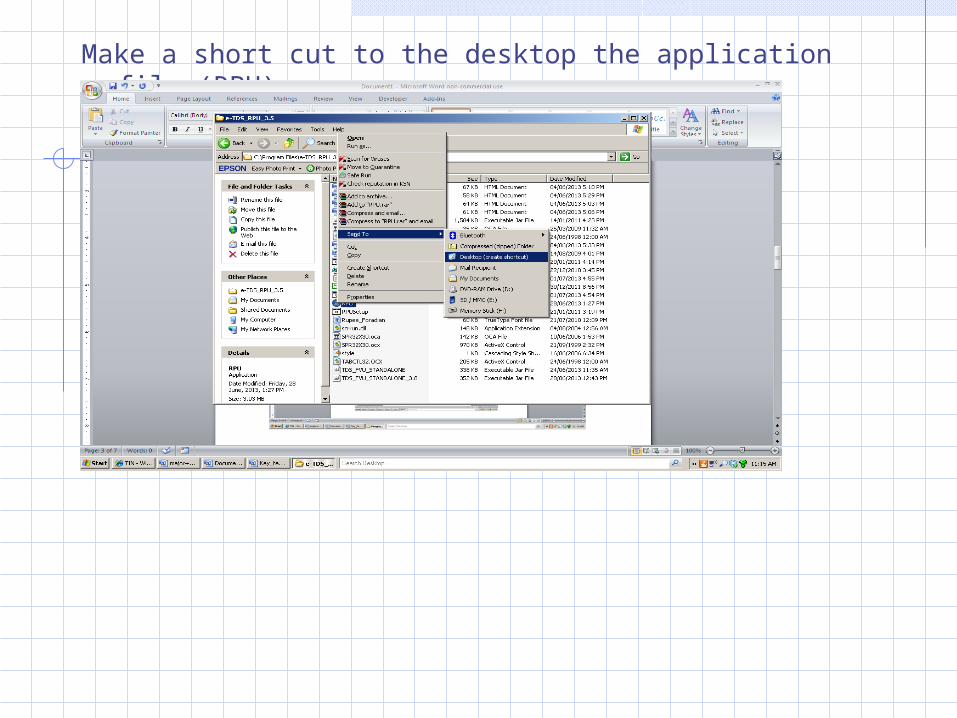

Make a short cut to the desktop the application file (RPU):

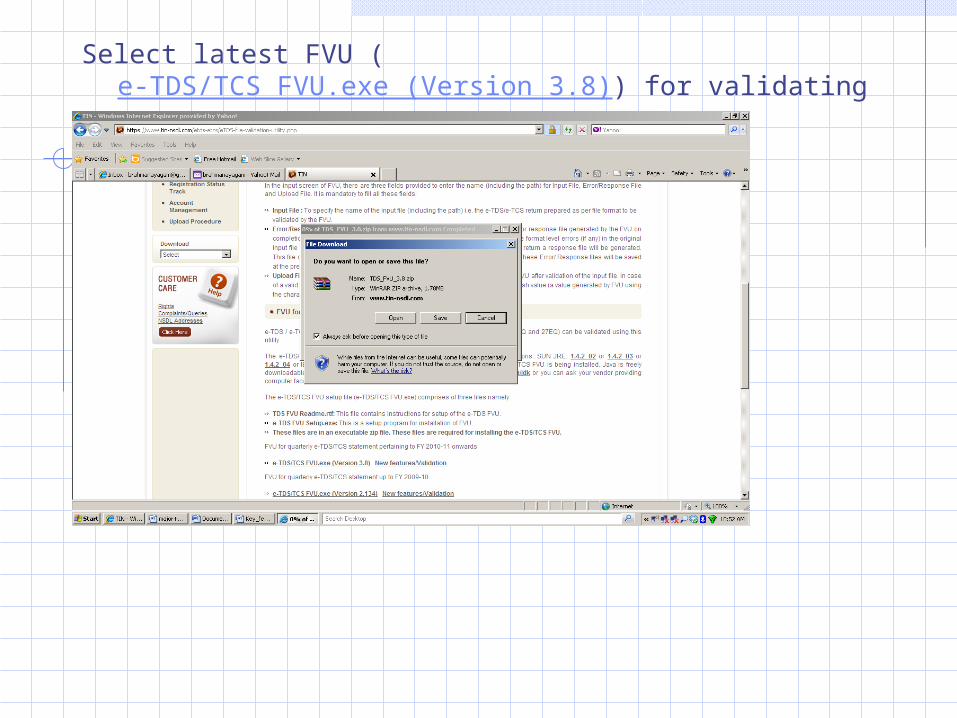

Select latest FVU (e-TDS/TCS FVU.exe (Version 3.8)) for validating the file prepared:

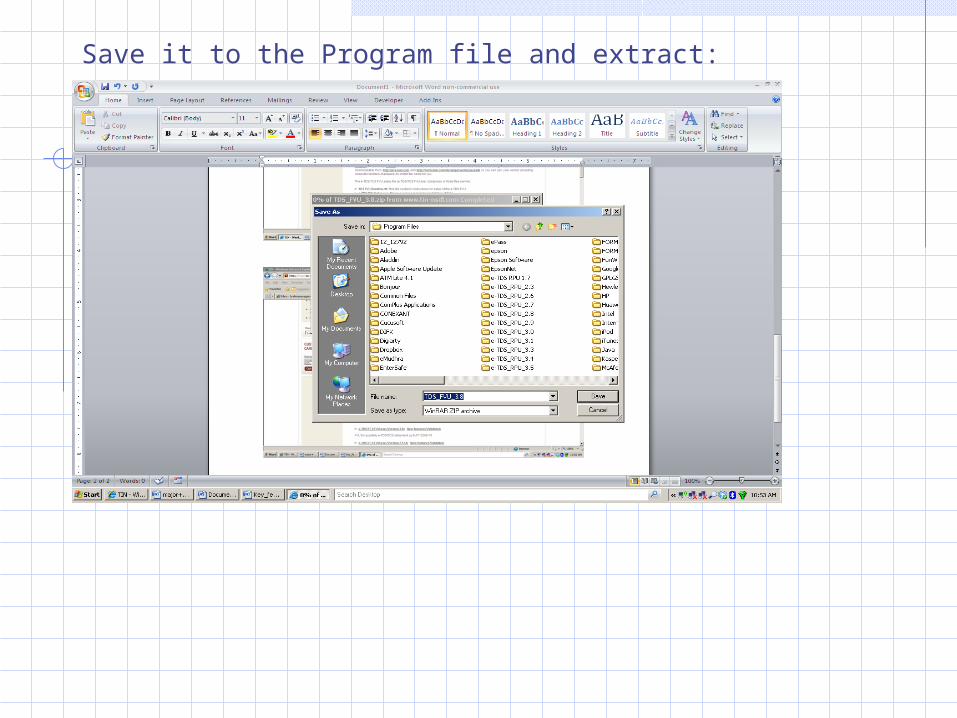

Save it to the Program file and extract:

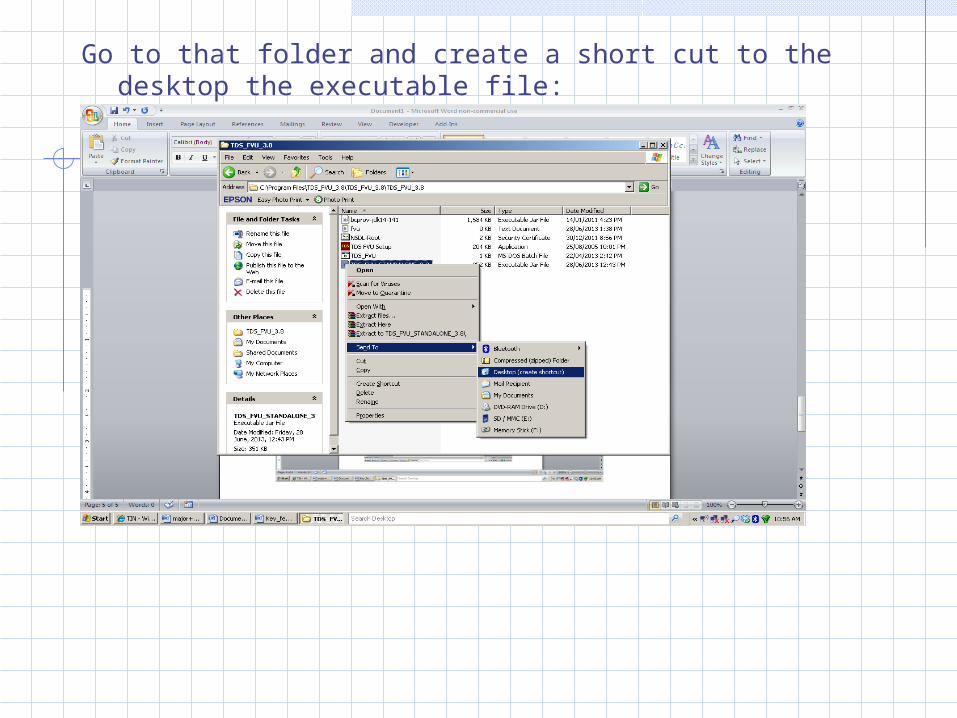

Go to that folder and create a short cut to the desktop the executable file:

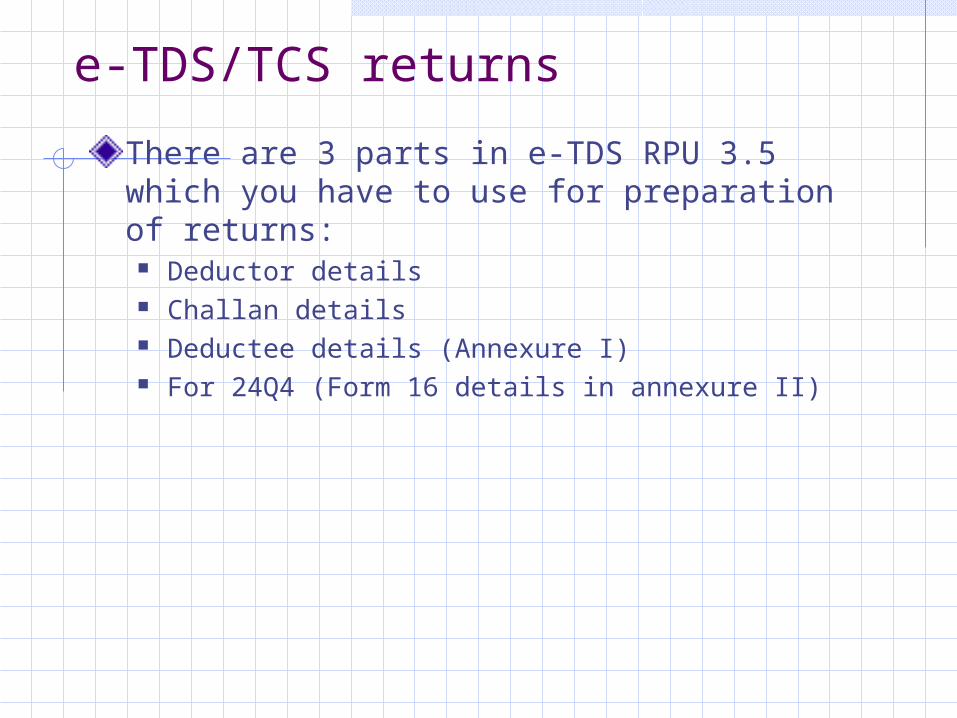

e-TDS/TCS returns

There are 3 parts in e-TDS RPU 3.5 which you have to use for preparation of returns:

Deductor details Challan details Deductee details (Annexure I) For 24Q4 (Form 16 details in annexure II)